Organic Pigments Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 757.84 kilotons |

| Market Volume (2031) | 889.69 kilotons |

| Growth Rate (2026 - 2031) | 3.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

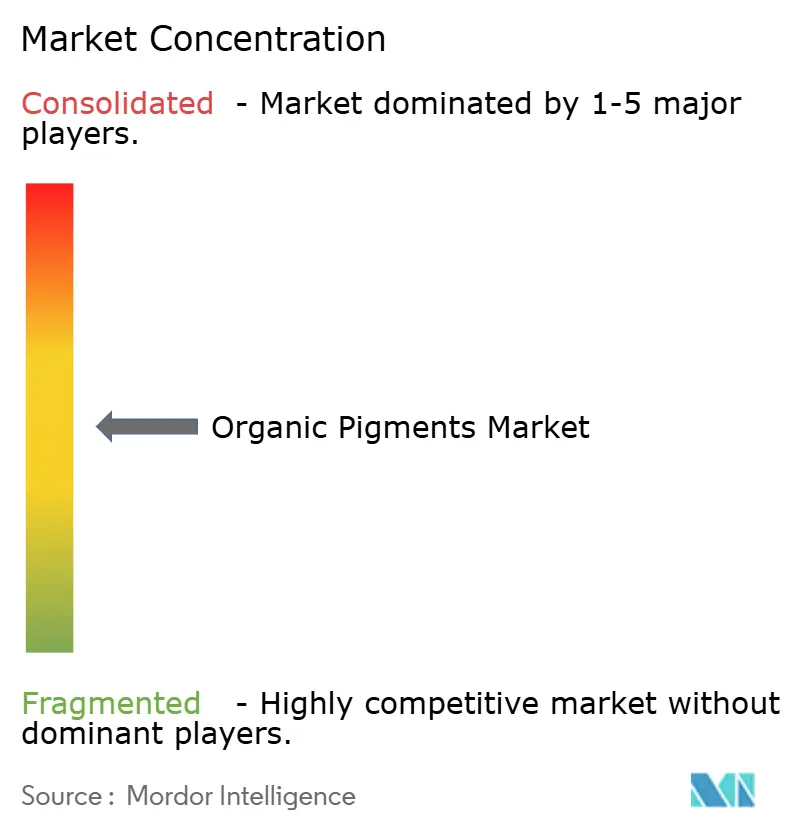

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Pigments Market Analysis by Mordor Intelligence

The Organic Pigments Market size is estimated at 757.84 kilotons in 2026, and is expected to reach 889.69 kilotons by 2031, at a CAGR of 3.26% during the forecast period (2026-2031). The expansion of the organic pigments market is powered by Asia-Pacific’s rapidly urbanizing economies, sustained e-commerce growth that lifts flexible-packaging inks, and the automotive sector’s shift to quinacridone grades that survive decade-long weathering tests. Printing-ink formulators are moving toward high-consistency dispersions compatible with AI-driven color-matching platforms, while brand owners in Europe and North America prefer bio-based options that comply with microplastics rules. Feedstock volatility and tighter hazard-communication laws add cost pressure, yet continuous-flow reactors and cloud-based formulation tools protect margins by cutting waste and cycle times. Competitive focus is migrating from commodity color strength to data-enabled services that guarantee first-time-right shades on any substrate.

Key Report Takeaways

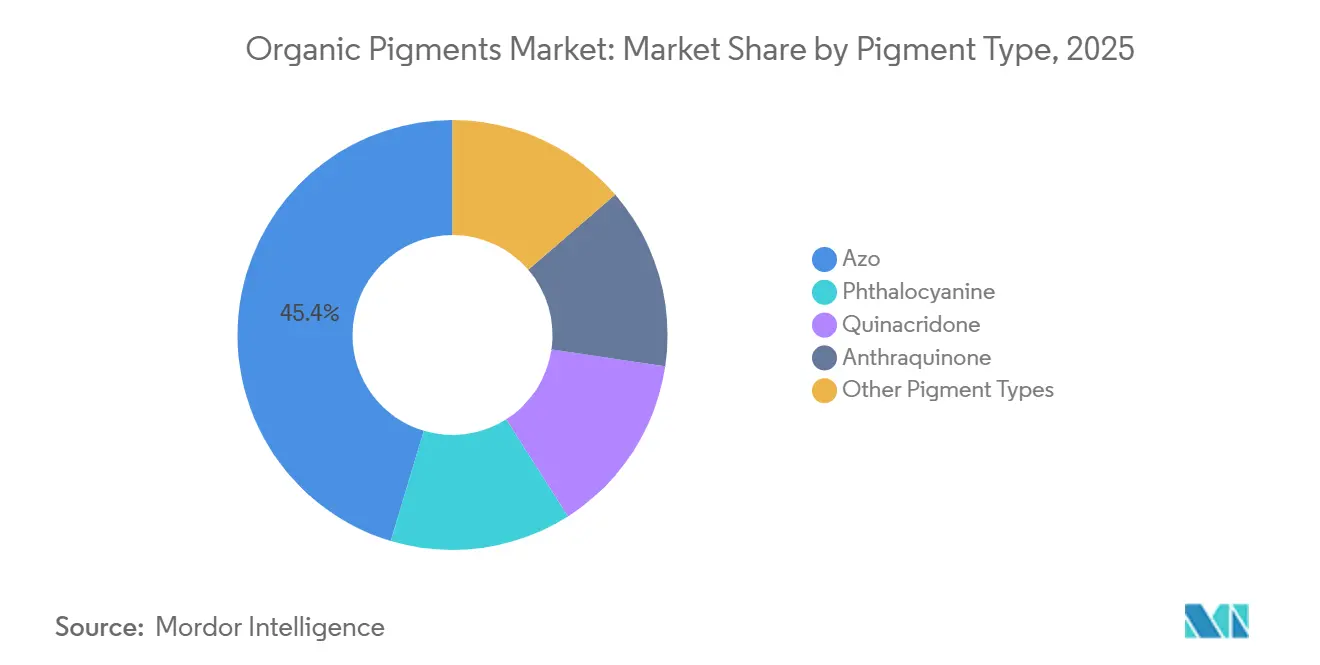

- By pigment type, azo grades held 45.36% of the organic pigments market share in 2025, whereas quinacridone variants are set to post the fastest 4.43% CAGR through 2031.

- By source, synthetic routes commanded 88.47% of the organic pigments market size in 2025, while natural and bio-based alternatives are forecast to expand at a 4.31% CAGR to 2031.

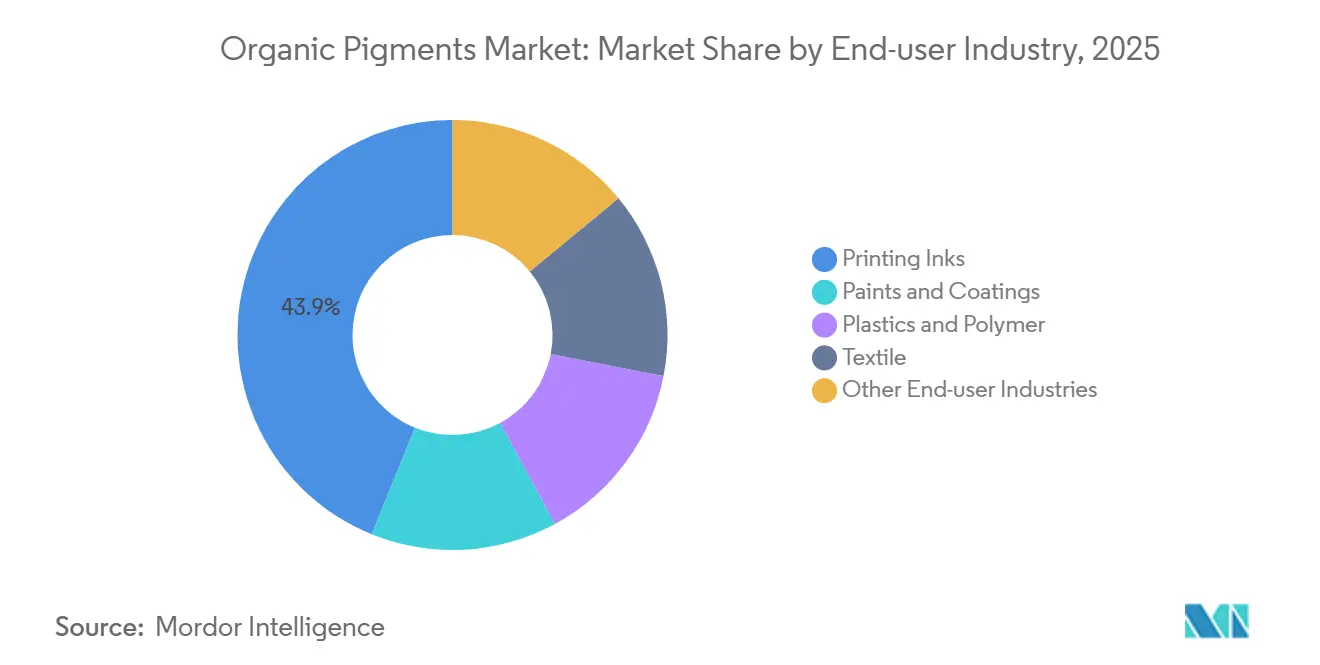

- By end-user industry, printing inks accounted for 43.88% of the organic pigments market size in 2025; the textile segment is advancing at a 4.39% CAGR through 2031.

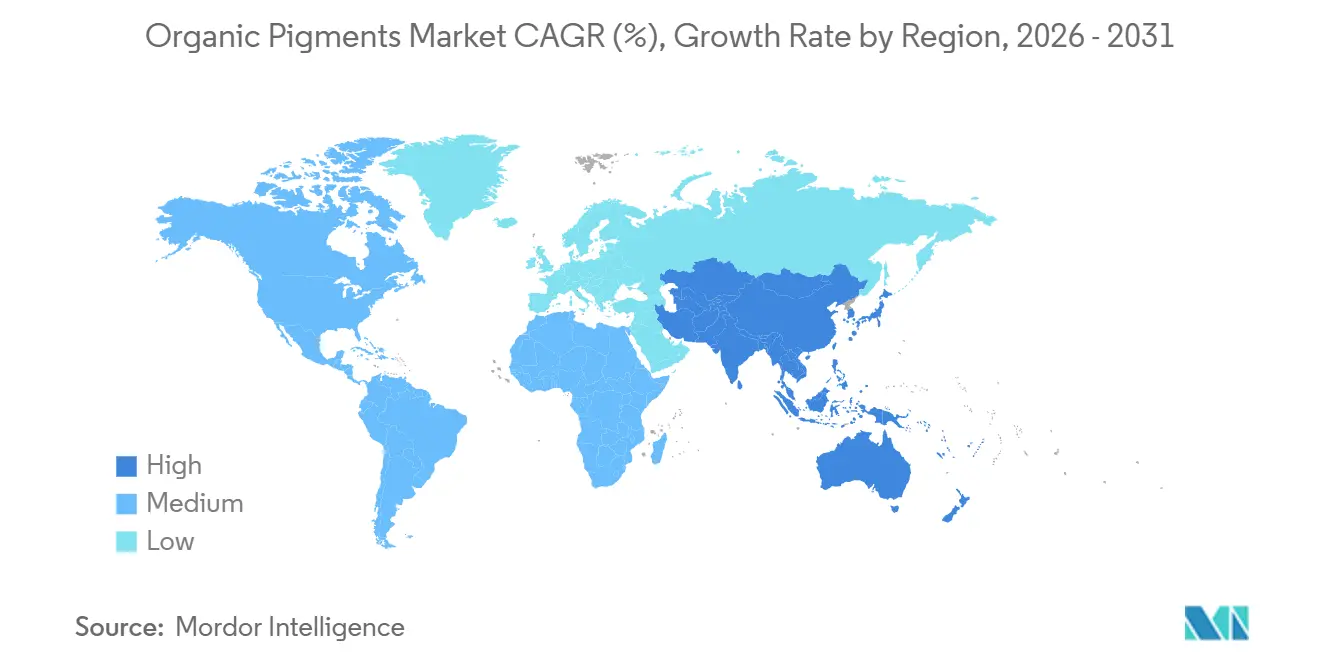

- By geography, Asia-Pacific captured 49.63% of volume in 2025 and is projected to lead the organic pigments market with a 4.92% regional CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Pigments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from paints and coatings | +0.8% | Global, concentrated in Asia-Pacific and Europe | Medium term (2-4 years) |

| Shift toward eco-friendly high-performance pigments | +0.7% | Europe and North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Surging flexible-packaging and digital-printing ink demand | +0.9% | Global, led by Asia-Pacific e-commerce hubs | Short term (≤ 2 years) |

| Expanding textile production in emerging economies | +0.6% | Asia-Pacific core (India, Bangladesh, Vietnam) | Medium term (2-4 years) |

| AI-enabled digital color matching | +0.5% | North America and Europe, early adoption in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand From Paints And Coatings Industry

Architectural and industrial coatings absorbed 39% of China’s 251,000-tonne pigment output in 2024, reflecting rapid urban renewal and infrastructure upgrades. Water-based acrylic emulsions replacing solvent-borne alkyds require pigments that disperse without coupling agents, favoring quinacridone magenta and phthalocyanine blue that resist flocculation in high-pH latex paints. Automotive refinish shops specify effect grades combining quinacridone with aluminum flakes to ensure radar-friendly finishes on electric vehicles, pushing approved pigment lists toward sub-100-nanometer products[1]BASF, “ColorCARE Digital Service Launch,” basf.com. Continuous-flow reactors help producers meet this granularity while holding batch-to-batch ΔE within ±2, preserving brand color integrity. These technical prerequisites sustain premium pricing even when feedstock costs swing.

Shift Toward Eco-Friendly High-Performance Pigments

The European Union’s microplastics restriction, active since October 2023, prohibits intentional particle release under 5 millimeters, propelling formulators to experiment with bio-based quinacridone precursors synthesized from lignin. California’s Safer Consumer Products program lists several azo grades, obligating alternatives analysis for shipments above 1 tonne annually. Natural extractions from turmeric and spirulina win share in food-contact packaging but lack light-fastness beyond Blue Wool 4, limiting outdoor use. As regulations tighten, the organic pigments market rewards suppliers that can balance biodegradability with performance, spurring a bifurcation between commodity producers and specialty players offering certified low-migration grades.

Surging Flexible-Packaging And Digital-Printing Ink Demand

Asia-Pacific processed over 150 billion e-commerce parcels in 2024, each needing printed graphics. Digital inkjet presses, now 18% of installed capacity, call for nano-milled dispersions under 150 nanometers to protect printheads. Sun Chemical’s UV-curable flexo inks cure in 0.5 seconds at 400 meters per minute and use phthalocyanine and quinacridone pigments pre-dispersed in reactive diluents[2]Sun Chemical, “UV Flexo Inks for Fast Throughput,” sunchemical.com. Food-contact flexible-packaging converters favor water-based gravure inks free of toluene, paying 20%-30% premiums for pigments with extractables below 0.1% by mass. These specifications keep digital printing a high-growth node inside the organic pigments market.

Expanding Textile Production In Emerging Economies

India’s textile exports hit USD 44.4 billion in FY 2023-24, supported by seven PM MITRA parks that co-locate dyeing and finishing under integrated effluent systems. Bangladesh added 1.2 million polyester spindles in 2024, targeting sportswear that requires azo-based disperse dyes with ISO 105 wash-fastness above Level 4. Vietnam’s textile shipments rose 8.7% in 2024 under EU tariff preferences. Heat-stable quinacridone and perylene grades endure 200 °C thermosol processing without sublimation, allowing dye houses to maintain vibrant shades. Regional pigment makers expanding dispersion capacity gain speed-to-market advantages that reinforce the organic pigments market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs from environmental rules | -0.5% | Europe and North America, extending to China | Medium term (2-4 years) |

| Cost/performance edge of inorganic pigments | -0.3% | Global, particularly in construction and industrial coatings | Long term (≥ 4 years) |

| Feedstock-price volatility | -0.4% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Production Costs From Stringent Environmental Regulations

The EU’s 2024 Classification, Labelling and Packaging update requires fresh toxicology dossiers costing EUR 50,000-150,000 per pigment. China’s 2024 Water-Pollution Law capped COD discharges at 50 mg/L, prompting CNY 20-50 million (USD 2.8-7 million) wastewater-treatment retrofits. India’s real-time effluent monitoring adds 12%-18% to operating costs for mid-tier producers. These investments burden firms that lack scale to amortize compliance, tempering growth in the organic pigments market.

Performance/Cost Advantages Of Inorganic Pigments

Titanium dioxide supplies superior opacity at one-third the kilogram cost, enabling formulators to hit hiding-power targets with lower loadings. For construction paints, price-sensitive buyers switch when organic quotations climb. Lanxess’s 2025 5% price hike on Bayferrox iron oxides illustrates industry-wide cost escalation. Inorganic pigments, therefore, cap the price elasticity of the organic pigments market, especially in high-volume architectural applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pigment Type: Azo Variants Dominate While Quinacridone Gains Pace

Azo grades secured 45.36% of the organic pigments market share in 2025, a position supported by low-complexity diazo-coupling synthesis that yields vivid yellows and reds at scale. Their ready dispersibility enables water-based flexographic inks to cut milling energy by 20% compared with quinacridone options. Disazo oranges deliver opacity in polypropylene masterbatch at 0.5% loading, doubling output rates on extruders that throttle back torque. Quinacridone pigments, though smaller in tonnage, expand at a 4.43% CAGR as OEMs demand polymorphs retaining hue after 2,000 hours of xenon-arc exposure, critical for 10-year vehicle warranties.

In the forecast horizon, the organic pigments market expects quinacridone’s heat stability above 200°C to unlock new battery-cover and composite-body uses, yet cost sensitivity in flexible packaging keeps azo grades entrenched. Phthalocyanine blues and greens remain workhorses in architectural coatings, trading under USD 8/kg for alpha-crystal copper phthalocyanine. Niche anthraquinone and perylene reds fetch prices beyond USD 50/kg, where Blue Wool 7 light-fastness is non-negotiable. Digital color-matching systems may substitute costly pigments with optimized blends, pressuring specialty grades to prove lifetime value in the organic pigments market.

By Source: Synthetic Routes Prevail As Bio-Based Alternatives Scale Slowly

Synthetic processes held 88.47% of the 2025 volume, buttressed by decades-honed yields surpassing 85% in azo, phthalocyanine, and quinacridone lines. Natural extracts, curcumin, betanin, phycocyanin, win niche adoption in food-contact packaging but lack Blue Wool 5 durability, stalling wider exterior uptake. Bio-based synthetic pigments produced via fermentation shave carbon footprints by 40%, though sub-60% yields keep costs elevated.

The organic pigments market size for bio-based grades is projected to rise at a 4.31% CAGR to 2031, aided by California’s Safer Consumer Products mandates and forthcoming EU Ecodesign rules. Yet until carbon pricing closes the gap, synthetic incumbents will dominate high-performance coatings where consistent chroma and stability outweigh environmental messaging. The trajectory signals parallel supply chains: commodity synthetic for cost efficiency and specialty bio-based for premium eco-labels.

By End-User Industry: Printing Inks Lead While Textile Accelerates

Printing inks consumed 43.88% of the organic pigments market size in 2025, riding e-commerce’s parcel boom and the shift to nano-milled dispersions for inkjet heads. Paints and coatings follow, leveraging water-based acrylics to meet VOC caps of 50 g/L in the EU and 150 g/L in China. Plastics compounding values heat-stable quinacridone reds that endure 280°C in polyamide without hue drift.

Textiles, though a smaller slice, race ahead at a 4.39% CAGR as India, Bangladesh, and Vietnam upgrade dyeing capacity. Disperse dyes integrating azo chromophores achieve ISO 105-C06 wash-fastness above Level 4, essential for fast-fashion polyester. Integrated PM MITRA parks in India shorten pigment lead times, reinforcing growth momentum. Specialty cosmetics and artist-color segments round out demand, insisting on low-migration grades that carry 30%-50% premiums, securing value pockets inside the organic pigments market.

Geography Analysis

Asia-Pacific commanded 49.63% of 2025 volume and will expand at a 4.92% CAGR to 2031 as China’s 251,000-tonne output and India’s fast-growing textile and coatings sectors lift regional offtake. Chinese producers such as Baihehua and Qicai Chemical employ continuous-flow reactors that achieve color-strength tolerances within ±2 ΔE, qualifying for automotive approvals CPCIF.CN. India’s organic pigments market registered 11% growth in FY 2024-25 on the back of USD 44.4 billion in textile exports and infrastructure-driven paint consumption.

North America and Europe jointly represent roughly 30% of global volume. The EU’s microplastics restriction and REACH updates steer formulators toward low-migration and biodegradable grades, letting specialty suppliers capture margin. In the United States, California’s regulatory stance accelerates the substitution of flagged azo pigments with quinacridone and phthalocyanine alternatives, pressuring commodity incumbents to upgrade toxicology data. Digital color-matching tools see early adoption across automotive refinish chains, enhancing service differentiation.

South America and the Middle East-Africa cover the remaining share. Brazil’s construction rebound supports local pigment demand, whereas Saudi Arabia’s downstream diversification under Vision 2030 seeds coatings capacity tied to petrochemical clusters. These regions import high-performance grades yet source commodity azo pigments from Asia, underscoring Asia-Pacific’s role as the supply backbone of the organic pigments market.

Competitive Landscape

The Organic Pigments market is moderately consolidated. Consolidation continued when SK Capital acquired Heubach in November 2024, merging European phthalocyanine lines with a broader specialty-chemicals portfolio. Sudarshan Chemical commissioned a 5,000-tonne dispersion line in 2025 to serve automotive and industrial coatings that require ±2 ΔE consistency. Regulatory compliance costs under REACH and California’s programs raise barriers, favoring diversified players that amortize documentation across portfolios, thereby shaping long-term dynamics in the organic pigments market.

Organic Pigments Industry Leaders

DIC CORPORATION

Sudarshan Chemical Industries Limited

BASF

artience Co., Ltd.

Clariant

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Vipul Organics, to boost its pigments business, inaugurated a new greenfield manufacturing facility in Sayakha, Gujarat. The new plant is projected to ramp up capacity to almost 10,000 tonnes annually.

- March 2025: Sudarshan Chemical Industries Limited (SCIL), via its wholly owned subsidiary Sudarshan Europe B.V., successfully acquired Germany's Heubach Group. This move merged SCIL operations and expertise with Heubach's advanced technological prowess. The acquisition not only broadens SCIL's product offerings but also expands its reach to 19 international sites.

Global Organic Pigments Market Report Scope

Pigments are a set of compounds used for coloring other materials. Organic pigments are often brighter, more powerful, and more clear than inorganic pigments. However, they are not as light-resistant. They could be partially soluble in many thermoplastics, but they have a significantly higher tendency to migrate.

The organic pigments market is segmented by pigment type, end-user industry, and geography. By pigment type, the market is segmented into azo, phthalocyanine, quinacridone, anthraquinone, and other pigment types. By source, market is segmented into synthetic and natural/bio-based. By end-user industry, the market is segmented into paints and coatings, plastics and polymer, printing inks, textile, and other end-user industries. The report also offers market size and forecasts for 16 countries across major regions. For each segment, market sizing and forecasts have been done based on volume (kilotons) for all the above segments.

| Azo |

| Phthalocyanine |

| Quinacridone |

| Anthraquinone |

| Other Pigment Types |

| Synthetic |

| Natural / Bio-based |

| Paints and Coatings |

| Plastics and Polymer |

| Printing Inks |

| Textile |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Pigment Type | Azo | |

| Phthalocyanine | ||

| Quinacridone | ||

| Anthraquinone | ||

| Other Pigment Types | ||

| By Source | Synthetic | |

| Natural / Bio-based | ||

| By End-User Industry | Paints and Coatings | |

| Plastics and Polymer | ||

| Printing Inks | ||

| Textile | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected demand for organic pigments by 2031?

The organic pigments market is forecast to reach 889.69 kilotons by 2031, reflecting a 3.26% CAGR during 2026-2031.

Which region contributes the most to consumption?

Asia-Pacific accounts for 49.63% of 2025 volume and is expected to remain the largest and fastest-growing region.

Which pigment type leads in volume terms?

Azo pigments held 45.36% of volume in 2025 due to low-cost synthesis and broad compatibility with water-based inks.

Why are quinacridone grades gaining traction?

Quinacridone pigments deliver heat stability above 200 °C and 2,000-hour xenon-arc durability, meeting stringent automotive color warranties.

How do environmental regulations affect producers?

EU CLP updates and microplastics rules raise compliance costs by EUR 50,000-150,000 per pigment, increasing production expenses for smaller firms.

Page last updated on: