Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

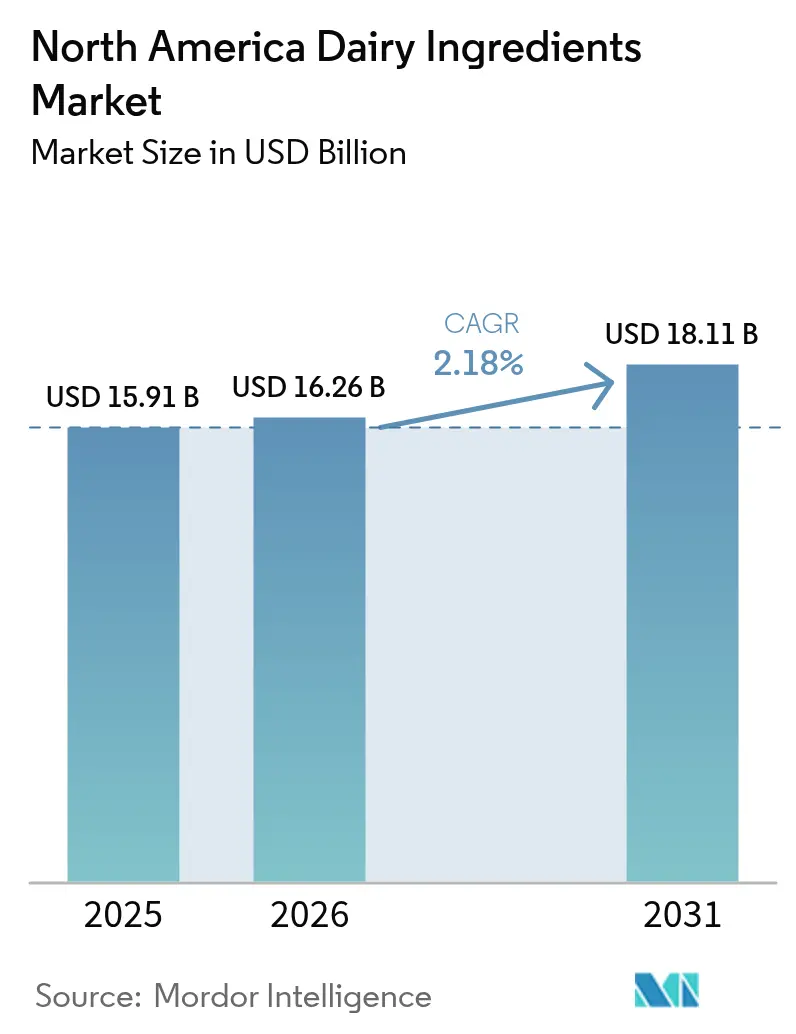

| Base Year Market Size (2025) | USD 15.91 Billion |

| Market Size (2026) | USD 16.26 Billion |

| Market Size (2031) | USD 18.11 Billion |

| Growth Rate (2026 - 2031) | 2.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Dairy Ingredients Market Analysis by Mordor Intelligence

North America dairy ingredients market size in 2026 is estimated at USD 16.26 billion, growing from 2025 value of USD 15.91 billion with 2031 projections showing USD 18.11 billion, growing at 2.18% CAGR over 2026-2031. It is expected to grow steadily, reaching USD 17.86 billion by 2030, with a CAGR of 2.33%. This growth reflects the market's ability to maintain a stable and mature demand base while adapting to shifting consumer preferences and industry trends. Manufacturers in the region actively address the increasing demand for dairy ingredients across diverse applications, including infant formula, sports nutrition, and functional foods. These sectors rely on dairy ingredients for their high nutritional value, functional versatility, and ability to enhance product formulations. Infant formula manufacturers, for instance, incorporate dairy ingredients to replicate the nutritional profile of human milk, ensuring optimal growth and development for infants. Similarly, the sports nutrition sector utilizes these ingredients to create protein-rich products that support muscle recovery and performance enhancement. Functional food producers also leverage dairy ingredients to meet the rising consumer demand for health-focused and fortified food products.

Key Report Takeaways

- By type, milk powders held 31.60% of the North America dairy ingredients market share in 2025, whereas Whey Ingredients are forecast to expand at a 3.55% CAGR through 2031.

- By application, dairy products led with 45.70% revenue share in 2025; Sports and Clinical Nutrition is growing fastest at 3.65% CAGR to 2031.

- By nature, conventional formats dominated with a 91.80% share in 2025, but the organic tier is advancing at 2.85% CAGR.

- By livestock origin, cows dominated with a 90.15% share in 2025, but goat is poised at a 2.85% CAGR to 2031.

- By geography, the United States accounted for 65.31% of the North American dairy ingredients market size in 2025, while Mexico is projected to post a 3.15%CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Dairy Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for protein-rich foods | +0.6% | North America, with spillover to Mexico | Medium term (2-4 years) |

| Increasing adoption in sports nutrition products | +0.4% | United States and Canada core markets | Short term (≤ 2 years) |

| Expansion of the infant formula market | +0.3% | North America, stronger in urban areas | Long term (≥ 4 years) |

| Growing adoption in functional food and beverage sector | +0.5% | North America, early gains in urban centers | Medium term (2-4 years) |

| Surging usage in bakery and confectionery industry | +0.2% | Regional, concentrated in processing hubs | Short term (≤ 2 years) |

| Clean-label and organic dairy ingredient demand | +0.3% | United States and Canada premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for protein-rich foods

Consumers are actively seeking protein sources that go beyond basic nutrition, prioritizing functional benefits such as muscle recovery, satiety, and overall health. This growing awareness is driving manufacturers to develop ingredients with higher protein concentrations and improved bioavailability. The FDA is addressing this trend by requesting information on high-protein yogurt manufacturing practices, signaling its intent to potentially establish new standards of identity[1]United States Food and Drug Administration, "FDA Issues Request for Information on High-Protein Yogurt", www.fda.gov. These standards could create opportunities for dairy ingredients with concentrated protein profiles to gain regulatory and market advantages. In the sports nutrition market, manufacturers are expanding their offerings beyond traditional whey protein isolates. They are increasingly incorporating casein-based formulations, which deliver a sustained release of amino acids. This approach meets the rising demand for products that support recovery and serve as effective meal replacements.

Increasing adoption in sports nutrition products

The increasing adoption of sports nutrition products is a key driver in the North America dairy ingredients market. This growth is fueled by the rising awareness of health and fitness among consumers, particularly in the United States and Canada. According to the Centers for Disease Control and Prevention (CDC), adults need 150 minutes of moderate-intensity physical activity a week. This can also be 75 minutes of vigorous-intensity or an equivalent combination of moderate- and vigorous-intensity physical activity[2]Centers for Disease Control and Prevention, "Adult Activity: An Overview", www.cdc.gov. which has led to a growing demand for products that support active lifestyles. Additionally, the Canadian government’s initiatives promoting healthy eating and physical activity further contribute to this trend. For instance, the Canada Food Guide emphasizes the importance of protein-rich foods, including dairy-based products, which are often used in sports nutrition formulations. The increasing participation in sports and fitness activities, coupled with the growing trend of protein supplementation, is expected to drive the demand for dairy ingredients in this segment during the forecast period.

Expansion of the infant formula market

The infant formula sector has ramped up its ingredient diversification and supplier qualification processes in response to supply disruptions in 2022. This shift has opened doors for specialized dairy protein suppliers, especially those adept at navigating regulatory landscapes. The FDA's Long-Term National Strategy aims to bolster market resiliency, spotlighting the importance of supply chain redundancy and contamination prevention[3].United States Food and Drug Administration, "FDA Announces Release of Long-Term National Strategy to Increase the Resiliency of the U.S. Infant Formula Market", www.fda.gov This focus could benefit suppliers boasting sophisticated quality systems and robust traceability protocols. Ongoing reviews of nutrient requirements might lead to revamped protein specifications and the introduction of new functional ingredients, especially those enhancing cognitive function and immune system development in infants. Starting June 2024, the WIC program's updated food packages will continue to champion infant formula but will also roll out plant-based options for older children, hinting at potential market segmentation [4]Federal Register, "Special Supplemental Nutrition Program for Women, Infants, and Children (WIC): Revisions in the WIC Food Packages", www.federalregister.gov . New manufacturing notification rules now require a 5-day heads-up for production hitches, giving an edge to suppliers with nimble production and savvy inventory management. The sector's pivot towards premium formulations, emphasizing specialized proteins like lactoferrin and immunoglobulins, is spurring a surge in demand for advanced fractionation technologies. These technologies are pivotal in isolating bioactive components without compromising nutritional value.

Growing adoption in functional food and beverage sector

Functional food applications are driving demand for dairy ingredients with proven health benefits beyond basic nutrition, creating opportunities for suppliers with clinical research capabilities and bioactive compound expertise. The FDA's updated definition of "healthy" foods, effective February 2025, establishes specific parameters for added sugars, saturated fat, and sodium that could favor dairy ingredients in reformulation strategies. Kerry Group's strategic focus on sustainable nutrition and functional benefits positions the company to address sodium and sugar reduction challenges while enhancing nutritional profiles through dairy-based solutions. Lactoferrin applications are expanding beyond infant formula into adult nutrition products targeting immune health, with particular growth in products for elderly consumers and individuals with compromised immune systems. The clean-label movement is driving reformulation away from synthetic additives toward dairy-derived functional ingredients that provide similar performance characteristics with improved consumer acceptance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lactose intolerance and dairy allergies | -0.4% | North America, concentrated in urban areas | Medium term (2-4 years) |

| Growing popularity of plant-based alternatives | -0.6% | United States and Canada premium segments | Long term (≥ 4 years) |

| Volatility in raw milk prices | -0.3% | North America, with Mexico sensitivity | Short term (≤ 2 years) |

| Stringent food safety and labeling regulations | -0.2% | United States regulatory jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lactose intolerance and dairy allergies

Lactose intolerance and dairy allergies represent significant restraints in the North America dairy ingredients market. A growing number of consumers are being diagnosed with lactose intolerance, a condition where the body lacks sufficient lactase enzyme to digest lactose, the sugar found in milk and dairy products. This has led to a shift in consumer preferences toward lactose-free and plant-based alternatives, reducing the demand for traditional dairy ingredients. Additionally, dairy allergies, which involve an immune response to milk proteins such as casein and whey, further limit the consumption of dairy products among affected individuals. These factors collectively pose challenges for market growth, compelling manufacturers to innovate and diversify their product offerings to cater to evolving consumer needs. The increasing awareness of these conditions and the rising demand for alternative products are reshaping the dynamics of the dairy ingredients market in the region.

Growing popularity of plant-based alternatives

The growing popularity of plant-based alternatives is emerging as a significant restraint in the North America dairy ingredients market. Consumers are increasingly shifting toward plant-based products due to health concerns, dietary preferences, and environmental sustainability. This trend is driven by the rising awareness of lactose intolerance, veganism, and the perceived health benefits of plant-based diets. Additionally, advancements in plant-based product formulations have improved taste, texture, and nutritional profiles, making them more appealing to a broader audience. The availability of a wide range of plant-based alternatives, such as almond milk, soy milk, oat milk, and coconut milk, further intensifies the competition for traditional dairy ingredients. Moreover, plant-based products are often marketed as environmentally friendly, aligning with the growing consumer demand for sustainable and ethical food choices. The increasing investment in research and development by plant-based product manufacturers has led to the introduction of innovative offerings, such as plant-based cheeses, yogurts, and protein powders, which directly compete with conventional dairy ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Powders Sustain Leadership as Whey Gains Momentum

In 2025, Milk Powders captured 31.60% of North America's dairy ingredients market, underscoring their versatility in bakery mixes, confectionery fillings, and reconstituted dairy beverages. Their long shelf life and balanced protein-to-lactose ratio meet both the functional and economic needs of formulators. Premium chocolate brands are turning to Whole Milk Powder for its sought-after fat-driven mouthfeel, which enhances the sensory appeal of their products, while Skimmed Milk Powder is favored as a budget-friendly protein for industrial sauces, offering a cost-efficient solution without compromising on quality. Although the market size for Milk Powders in North America's dairy ingredients sector is projected to hold steady, price sensitivity is pushing for efficiency gains, driven by innovations in spray-drying and energy-recovery systems. These advancements aim to reduce production costs while maintaining product quality, ensuring competitiveness in a price-sensitive market.

Whey Ingredients are poised to expand at a 3.55% CAGR through 2031, spurred by the surging demand for high-purity whey protein isolate in ready-to-drink sports beverages. This growth is driven by the increasing consumer focus on fitness and protein-rich diets. Hydrolysed whey is carving a niche in medical nutrition, particularly for patients facing digestion issues, as it offers easier absorption and faster recovery benefits. Once deemed a low-margin by-product, whey permeate is now recognized as a valuable mineral source in snack seasonings, contributing to flavor enhancement and nutritional value. This evolution highlights how continuous process innovations, such as advanced filtration and separation technologies, are expanding the applications and profit margins of whey products in North America's dairy ingredients market.

By Nature: Organic Tier Grows as Premium Niche

In 2025, conventional formats dominated the North American dairy ingredients market, capturing a substantial 91.80% share. This stronghold is largely due to the region's easy access to raw milk, guaranteeing a consistent production input supply. The availability of raw milk not only ensures uninterrupted production but also supports economies of scale, reducing overall costs for manufacturers. Furthermore, the established cost structures of conventional dairy ingredients have made them the go-to choice for manufacturers, facilitating competitive pricing and broad adoption across diverse applications. Products like milk powders, whey proteins, and casein, derived from conventional dairy ingredients, play pivotal roles in industries ranging from bakery and confectionery to infant nutrition. These ingredients are integral to the formulation of various end products, offering functional benefits such as improved texture, enhanced shelf life, and nutritional value, which further drive their demand.

Conversely, organic dairy ingredients are on the rise, boasting a projected CAGR of 2.85% through 2031. This surge is largely fueled by a growing consumer inclination towards clean-label and sustainably sourced products. As a result, organic dairy ingredients are increasingly featured in premium formulations, appealing to health-conscious and environmentally aware consumers. Produced under strict regulations, these ingredients are free from synthetic additives, hormones, and pesticides, making them attractive to a niche yet expanding consumer base. The production process of organic dairy ingredients often involves higher costs due to stringent compliance requirements and limited raw material availability, which contributes to their premium positioning in the market. While they hold a smaller market share, organic dairy ingredients are carving out spaces in high-value products, including organic infant formula, nutritional supplements, and specialty dairy offerings. These products cater to consumers willing to pay a premium for quality, safety, and sustainability, further driving the growth of this segment.

By Livestock Origin: Cow Milk Dominance Faces Niche Rivals

In 2025, cow milk commanded a dominant 90.15% share of the livestock origin segment. This stronghold is largely due to the soaring demand for cow-derived dairy ingredients, integral to products like milk, cheese, butter, and yogurt. The widespread availability of cow milk, paired with its nutritional advantages and processing versatility, has cemented its status as the region's primary dairy ingredient source. Cow milk is rich in essential nutrients such as calcium, protein, and vitamins, which contribute to its popularity among consumers. Moreover, with advancements in dairy farming and the embrace of modern technologies, cow milk production has seen boosts in efficiency and productivity, reinforcing its market dominance. These advancements include improved breeding techniques, better feed quality, and automated milking systems, which have collectively enhanced the overall output and quality of cow milk.

Meanwhile, goat milk, despite its smaller market share, is set to expand at a 2.85% CAGR through 2031. Goat-derived dairy ingredients are becoming increasingly sought after, thanks to their distinct nutritional benefits, such as enhanced digestibility and reduced allergenic properties when stacked against cow milk. These qualities have made goat milk and its products favorites among health-conscious consumers and those with specialized dietary requirements. Goat milk contains higher levels of certain nutrients, such as medium-chain fatty acids and bioactive compounds, which contribute to its health benefits. Additionally, as awareness of goat milk's advantages rises, and with its burgeoning presence in niche markets like specialty cheeses and infant formulas, its growth trajectory in North America's dairy ingredients market looks promising. The increasing availability of goat milk products in retail channels and the growing focus on sustainable and small-scale farming practices are further expected to support this growth.

By Application: Sports Nutrition Sets the Growth Pace

In 2025, Dairy Products commanded a notable 45.70% share of the market, underscoring the persistent demand for key ingredients like powders, lactose, and milk proteins. These ingredients are pivotal in producing staple regional items such as cheese, yogurt, and fluid milk. A rising consumer inclination towards premium dairy products, combined with technological advancements in processing, has amplified the demand for these ingredients. Additionally, the increasing use of dairy-based products across diverse food applications, including bakery and confectionery, is propelling the market's expansion. For instance, lactose and milk proteins are extensively utilized in bakery products to enhance texture and flavor, while dairy powders are integral in confectionery for their emulsifying properties. Manufacturers, responding to the growing emphasis on clean-label and natural ingredients, are innovating and broadening their product ranges to align with shifting consumer demands. This includes the development of organic and minimally processed dairy ingredients to cater to health-conscious consumers.

North America's Sports and Clinical Nutrition sector is on an upward trajectory, with a forecasted CAGR of 3.65%. This growth is largely attributed to a heightened interest in active living and the pursuit of healthy aging across various demographics. As awareness grows regarding the advantages of protein-rich diets and functional foods, the demand for dairy-derived ingredients in this sector intensifies. Dairy components like whey protein, casein, and milk protein concentrates are finding their way into sports drinks, protein bars, and dietary supplements. For example, whey protein is widely recognized for its quick absorption and muscle recovery benefits, making it a preferred choice among athletes, while casein is valued for its slow-digesting properties, supporting prolonged muscle repair. Additionally, the aging demographic's commitment to muscle health and overall wellness is spurring the growth of clinical nutrition products. These products are increasingly formulated to address specific health concerns, such as sarcopenia and bone density loss, which are prevalent among older adults. The market is further buoyed by innovative product formulations tailored to specific dietary preferences, including lactose-free options and plant-based alternatives infused with dairy proteins, ensuring inclusivity for consumers with dietary restrictions or preferences.

Geography Analysis

In 2025, the United States commands a dominant 65.31% share of the North American dairy ingredients market, bolstered by its advanced processing infrastructure, well-established supply chains, and closeness to key food manufacturing hubs that amplify ingredient demand. For instance, the United States is a leading producer of whey protein concentrates and isolates, which are widely used in sports nutrition and functional food products. Additionally, the presence of major dairy companies such as Dairy Farmers of America, Land O'Lakes, and Leprino Foods further strengthens its market position. The country also benefits from significant investments in research and development, enabling innovations in dairy ingredient formulations, such as lactose-free and plant-dairy hybrid products, to cater to evolving consumer preferences.

Mexico stands out as the region with the most rapid growth, boasting a 3.15% CAGR projected through 2031, fueled by an uptick in per capita cheese consumption. The growing popularity of traditional Mexican cheeses like Oaxaca, Cotija, and Queso Fresco, along with the increasing adoption of processed cheese in fast food chains and ready-to-eat meals, is driving demand for dairy ingredients in the country. Furthermore, government initiatives to support the dairy sector, such as subsidies for small-scale farmers and investments in cold chain infrastructure, are contributing to market growth. For example, the Mexican government’s "Programa de Fomento Ganadero" (Livestock Promotion Program) has been instrumental in improving milk production efficiency, which indirectly supports the dairy ingredients market.

Canada is honing in on high-protein dairy ingredients, such as milk protein isolates, aligning with premium market strategies that prioritize functional advantages over mere commodity pricing. For example, Canadian manufacturers are focusing on producing high-quality casein and whey protein products to cater to the growing demand for protein-enriched beverages, snacks, and infant nutrition products. Companies like Saputo and Agropur Cooperative are at the forefront of this trend, leveraging Canada’s reputation for stringent quality standards and sustainable production practices. Additionally, the increasing popularity of plant-based dairy alternatives in Canada has prompted manufacturers to explore hybrid products that combine dairy and plant proteins, further diversifying the market.

Regulatory Landscape

In the United States, dairy ingredients used in cheese, powders, and protein fractions are governed by FDA food safety and labeling requirements, including standards of identity such as 21 CFR Part 133 for standardized cheeses. This affects how milk-derived inputs (e.g., nonfat milk, cream, and enzyme systems) are declared and formulated. The FDA Human Foods Program also set 2026 priority deliverables, including a systematic review of food ingredients and work on draft guidance related to color additives, which reinforces the need for ingredient suppliers to maintain documentation, specifications, and change-control discipline aligned with evolving FDA priorities.

In Canada, dairy ingredient labeling and market access are shaped by CFIA and Global Affairs Canada. CFIA issued a Notice to Industry dated February 11, 2026, updating incorporated-by-reference common-name conventions for ingredients and components, with a transition period extending to January 1, 2030, affecting how milk-derived ingredients are described on packaged foods. Cross-border trade dynamics under USMCA/CUSMA remain linked to Tariff Rate Quotas (TRQs) administered by Global Affairs Canada for categories including milk powders and concentrated milk, with quota administration monitored through government trade mechanisms. This influences how ingredient volumes are allocated and routed across North America.

Competitive Landscape

The North American dairy ingredients market demonstrates a moderate concentration. This indicates a fragmented competitive environment where numerous players operate, ranging from regional specialists to global giants. Regional players often focus on catering to local demands and preferences, leveraging their proximity to customers and understanding of regional trends to gain a competitive edge. For example, smaller dairy cooperatives in the United States and Canada emphasize organic and locally sourced ingredients to appeal to health-conscious consumers.

Global companies, on the other hand, bring extensive resources, advanced technologies, and strong brand recognition to the market. They often differentiate themselves through innovation, offering a wide range of specialized products, including whey protein isolates, milk protein concentrates, and lactose-free ingredients. For instance, Arla Foods, Fonterra Co-operative, and Agropur Co-operative have established themselves as key players by consistently expanding their product portfolios and investing in research and development to meet evolving consumer needs.

Furthermore, the competitive landscape is shaped by strategic partnerships, mergers, and acquisitions, which allow companies to strengthen their market positions. Regional specialists often collaborate with larger firms to enhance their market presence and access advanced processing technologies. For example, partnerships between local dairy cooperatives and multinational corporations have enabled smaller players to scale their operations while maintaining their regional identity. Mergers and acquisitions, such as Lactalis Group's acquisition of Kraft Heinz's natural cheese business, have also played a significant role in consolidating the market. This dynamic interplay between regional and global players, coupled with ongoing innovation and strategic alliances, continues to define the competitive structure of the North American dairy ingredients market.

North America Dairy Ingredients Industry Leaders

-

Arla Foods amba

-

Dairy Farmers of America

-

Fonterra Co-operative Group Ltd

-

Agropur Co-operative

-

Saputo, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Investment is concentrating in higher-value protein streams and advanced separation capability, rather than broad commodity milk processing. This creates room for suppliers that can deliver consistent WPC/WPI and milk protein concentrate specifications at scale, supported by 2026 plant-focused programs, including Agropur's USD 130 million investment in Midwestern facilities (including whey processing capacity additions in Wisconsin) and Land O'Lakes' July 2026 announcement to expand high-value dairy protein production at its Tulare, California facility. Saputo also highlighted a value-added ingredients focus in 2026 through its capital planning, and network moves that consolidate production into more efficient sites support tighter control of ingredient quality and cost-to-serve for industrial customers.

Export-oriented demand signals and application diversification across sports and clinical nutrition and infant formula are reinforcing the commercial case for whey and specialized fractions (including hydrolysates and bioactives), alongside quality systems that address stringent buyer requirements. Operational expansions such as MMPA bringing ultrafiltered milk capacity online at Ovid, Michigan (January 2026) and starting operations at its Remus, Michigan cottage cheese facility (March 2026) show continued build-out of component extraction and value-added dairy manufacturing. Within the region's established milk powders base (31.60% share in 2025) and the faster momentum in whey ingredients, opportunities appear strongest where manufacturers pair protein-forward formulation needs with traceability, allergen control, and labeling readiness across the United States and Canada, with Mexico adding additional pull-through via rising cheese-linked ingredient demand.

Recent Industry Developments

- June 2026: Saputo Inc. confirmed capital planning focused on value-added ingredients and other priority categories, reinforcing continued emphasis on higher-margin dairy components within its North American footprint. The company also advanced manufacturing network optimization actions that consolidate production into more efficient sites, supporting better utilization and cost control for ingredient-linked output.

- August 2025: Dairy Farmers of America (DFA) acquired W&W Dairy in Monroe, Wisconsin, expanding its Hispanic cheese production capabilities. The move strengthens DFA's positioning in specialty cheese channels that drive demand for cheese-adjacent ingredients and supports broader portfolio depth for foodservice and retail customers.

- July 2024: Arla Foods Ingredients secured FDA confirmation that four whey protein hydrolysate ingredients can be used in infant formula. This expands compliant formulation options for infant nutrition manufacturers and supports further differentiation of whey-derived ingredients in highly regulated applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the North America dairy ingredients market covers value sales of processed milk-derived ingredients used as inputs by food, beverage, and nutrition manufacturers across the region, counted at the point they are sold as ingredients (not as finished consumer dairy products).

Scope exclusions: We exclude retail sales of finished dairy foods and beverages, and we also exclude non-dairy substitutes and blends where dairy is not the primary ingredient.

Segmentation Overview

-

By Type

-

Milk Powders

- Skimmed Milk Powder

- Whole Milk Powder

- Others

- Milk Protein Concentrates and Isolates

-

Whey Ingredients

- Whey Protein Concentrate

- Whey Protein Isolate

- Hydrolyzed Whey Protein

- Lactose and Derivatives

- Casein and Caseinates

- Others

-

Milk Powders

-

By Nature

- Conventional

- Organic

-

By Livestock Origin

- Cow

- Buffalo

- Goat and Sheep

-

By Application

- Bakery and Confectionery

- Dairy Products

- Infant Milk Formula

- Sports and Clinical Nutrition

- Convenience and Ready-to-Eat Foods

- Other Applications

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure for the model and to set realistic ranges for demand, supply, and pricing across the United States, Canada, and Mexico. We referenced public sources such as USDA market and dairy statistics, Statistics Canada tables, Mexico's INEGI industrial and production series, and UN Comtrade trade flows for key dairy ingredient categories.

To avoid relying on one signal, we also reviewed sources such as Codex Alimentarius standards for ingredient definitions, peer-reviewed dairy science publications for yield and composition benchmarks, and company filings and investor presentations for capacity additions and product mix cues. Where needed, a paid subscription database for company financials and a shipment-level import/export database were used to cross-check trade intensity and manufacturer scale. The sources listed here are illustrative, and we also used other public references for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming how ingredient demand is forming across key application areas like infant formula, bakery and confectionery, dairy processing, and sports and clinical nutrition. We spoke with a mix of ingredient suppliers, processors, distributors, and large end users across North America, so we could check assumptions on pricing moves, substitution behavior, and contracting practices in cases where desk sources did not provide enough detail.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | |

| Mid tier: 52% | Functional/Unit leaders: 30% | |

| Smaller Players: 20% | Managers: 58% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production, trade, and usage signals are used to reconstruct the regional demand pool for dairy ingredients, followed by country splits across the United States, Canada, and Mexico. Those totals are then corroborated using selective bottom-up approximations, such as rolling up a sample of supplier revenues by ingredient lines and checking implied average selling prices against observed contract and spot ranges.

Inputs that matter most for this market include raw milk availability and milk solids yields, whey stream availability from cheese output, import and export balance for powders and protein concentrates, application-level pull from infant formula and sports nutrition, and realized pricing for common ingredient forms (like powders versus concentrates). When a bottom-up check has gaps, we fill them with conservative share-based allocations tied to capacity footprints and trade exposure, and then re-test the totals against the independent demand indicators.

Forecasting is done using scenario analysis supported by short series trend methods (including exponential smoothing) for variables like milk solids supply, trade direction, and pricing progression, with the final path being aligned to what interviewees expect under a normal operating environment. The goal is to keep the steps repeatable so updates can be made quickly when milk prices, trade policies, or end-use demand shifts.

Data Validation & Update Cycle

Validation is handled through multiple checks so the final number is not driven by one dataset or one assumption. We compare implied consumption against trade and production signals, review year-to-year swings for outliers, and re-check unit economics when a category shows a price or volume pattern that is not consistent with what the market typically sees.

Before sign-off, the model and key assumptions are reviewed by another analyst, and follow-up calls are triggered when responses conflict on pricing, mix, or application demand. The report is refreshed annually, and interim updates are made when material events occur, such as major capacity changes, regulation impacts, or sharp milk-price movements. Right before delivery, we complete a final refresh pass so clients receive the latest view.

Mordor Intelligence's North America Dairy Ingredients Market Size Versus Other Published Estimates

Published market sizes for dairy ingredients in North America often do not match because each publisher draws the product boundary differently and uses different timing for prices and currency. Differences also come from whether the estimate is built from ingredient-level demand signals versus broader food inputs, and from how quickly assumptions get updated when milk and whey markets move.

By tracking milk solids availability, trade balance, and application pull, Mordor Intelligence keeps the total tied to ingredient sales used in food and nutrition manufacturing, rather than counting finished dairy products or non-dairy substitutes that can inflate the pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.26 B (2026) | |

| Regional Consultancy A | USD 16.19 B (2024) | Uses an earlier base year and can mix in broader processing value with ingredients, which changes pricing levels and can soften the impact of recent milk price swings. |

| Industry Database B | USD 16.32 B (2023) | Relies on a narrower product emphasis and a different segment lens, and the forecast path is sensitive to higher assumed price progression across powders versus proteins. |

The spread is mainly explained by year selection, what is counted as an ingredient versus a finished product, and how pricing is carried forward in the forecast. Our model stays traceable because each step is tied back to production, trade, and end-use demand signals that can be checked again during refresh cycles.

Key Questions Answered in the Report

What is the current value of the North America dairy ingredients market?

The market stands at USD 16.26 billion in 2026 and is forecast to reach USD 18.11 billion by 2031.

Which ingredient type leads the market?

Milk Powders lead with 31.60% revenue share in 2025, while Whey Ingredients are growing fastest at a 3.55% CAGR.

Why is sports nutrition important for future growth?

Sports & Clinical Nutrition applications are expanding at 3.65% CAGR as consumers seek protein-fortified drinks, bars, and medical formulations, driving demand for high-purity whey and casein fractions.

Which country presents the strongest growth opportunity?

Mexico is the fastest-growing geography at 3.15% CAGR, driven by rising cheese consumption and favourable USMCA trade provisions.

Page last updated on: