Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 19.5 Billion |

| Market Size (2026) | USD 20.38 Billion |

| Market Size (2031) | USD 25.38 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Dairy Ingredients Market Analysis by Mordor Intelligence

The Europe Dairy Ingredients Market size was valued at USD 19.5 billion in 2025 and estimated to grow from USD 20.38 billion in 2026 to reach USD 25.38 billion by 2031, at a CAGR of 4.49% during the forecast period (2026-2031). This growth trajectory reflects the region's position as a global dairy powerhouse, with the European Union producing approximately 160 million tonnes of milk annually, representing about 25% of global cow milk production [1]Source: European Commission, "Milk and dairy products", agriculture.ec.europa.eu. The market's expansion is underpinned by sophisticated processing capabilities, with Germany, France, and Poland collectively accounting for nearly 65% of EU milk production and processing capacity. Consolidation moves such as Arla Foods Ingredients’ recent whey asset purchase underline a strategic tilt toward premium sports-nutrition inputs. Meanwhile, buoyant organic adoption, functional infant-formula innovations, and supportive Common Agricultural Policy (CAP) funding reinforce long-term stability for the Europe dairy ingredients market. The market faces headwinds from plant-based alternatives penetration and varying lactose intolerance prevalence across European countries. Nevertheless, regulatory support through the Common Agricultural Policy provides approximately EUR 188 billion in income support for 2023-2027, sustaining dairy farm viability and ingredient supply chains.

Key Report Takeaways

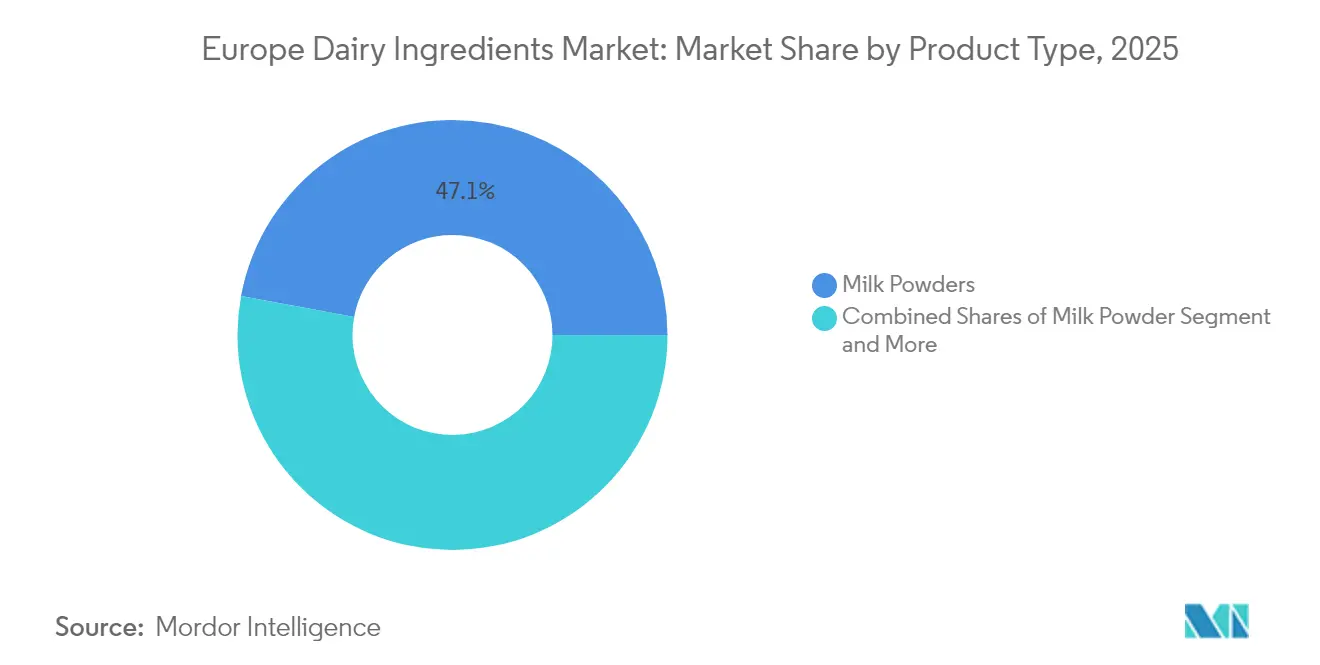

- By product type, milk powders led with 47.10% of the Europe dairy ingredients market share in 2025; whey ingredients posted the fastest expansion at a 4.62% CAGR through 2031.

- By nature, conventional formats accounted for 85.05% of the Europe dairy ingredients market size in 2025, whereas organic varieties are projected to progress at a 5.78% CAGR to 2031.

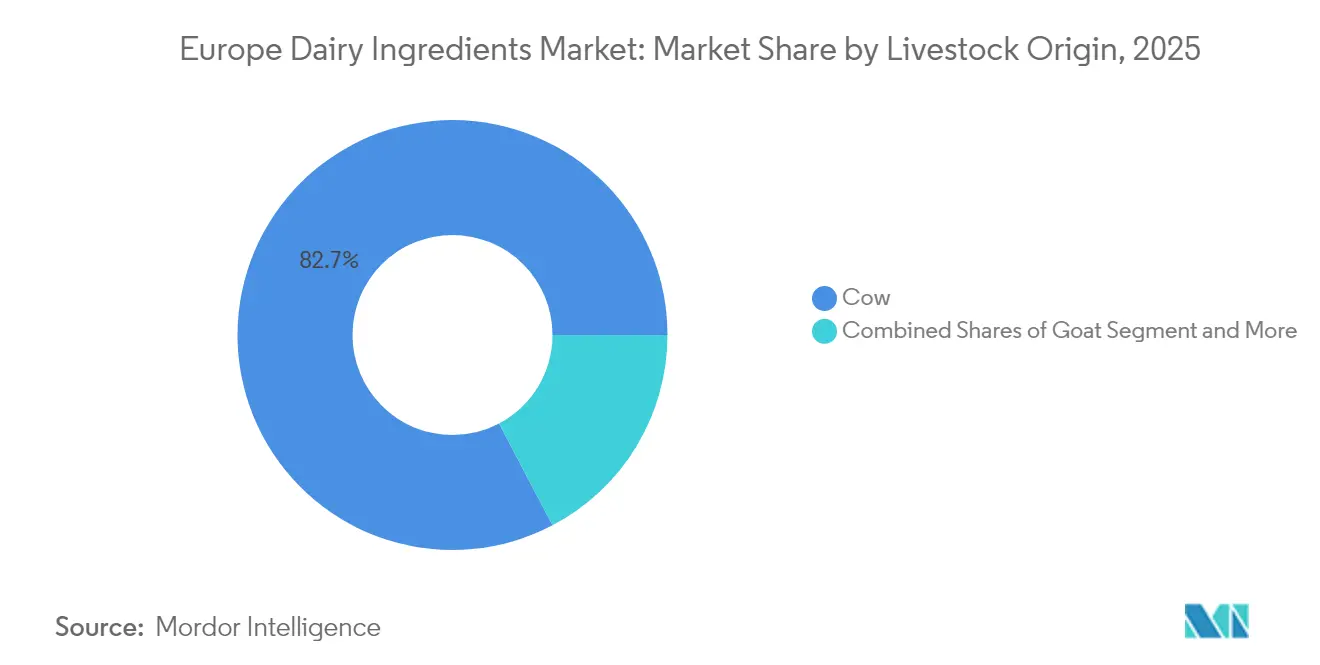

- By livestock origin, cow-milk derivatives represented 82.70% of the Europe dairy ingredients market share in 2025; goat-milk ingredients are set to advance at a 5.52% CAGR during the forecast horizon.

- By application, bakery and confectionery captured 28.55% revenue share in 2025 while sports and clinical nutrition is forecast to rise at a 5.16% CAGR to 2031.

- By geography, Germany held 22.10% of the Europe dairy ingredients market in 2025; Poland is on course for the quickest 6.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Dairy Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Awareness of Protein Intake in Developing Regions Driving Market Expansion | +0.8% | Eastern Europe, Poland, Czech Republic | Medium term (2-4 years) |

| Growing Sports Nutrition Sector Augmenting Demand for Value Added Dairy Ingredients | +1.2% | Germany, Netherlands, Nordic countries | Short term (≤ 2 years) |

| Global Infant Formula Demand Accelerates Market Expansion Significantly | +0.9% | Global with EU export focus | Long term (≥ 4 years) |

| Functional Food Applications Create New Market Growth Opportunities | +0.7% | Western Europe, Germany, France | Medium term (2-4 years) |

| Bakery Industry Adoption Expands Product Application Portfolio Rapidly | +0.5% | EU-wide with Central Europe focus | Short term (≤ 2 years) |

| Developing Economies Show Strong Market Consumption and Growth Pattern | +0.6% | Poland, Eastern European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Awareness of Protein Intake in Developing Regions Driving Market Expansion

Eastern European markets are experiencing accelerated protein consciousness, with Poland's dairy sector demonstrating remarkable resilience through 3.9% production growth in 2024 versus the EU average of 0.6%. This protein awareness surge is particularly pronounced in developing European economies where per-capita dairy consumption patterns are converging toward Western European levels. Poland's position as a potential third-largest EU milk producer by 2025 reflects this underlying demand transformation, supported by modernized processing infrastructure and export capabilities that have grown 400% since EU accession. The trend is amplified by demographic shifts toward health-conscious consumption patterns, creating sustained demand for protein-enriched dairy ingredients across bakery, confectionery, and ready-meal applications. Regulatory influence from EU food-based dietary guidelines recommending 2-3 daily dairy servings further supports this protein intake awareness across member states.

Growing Sports Nutrition Sector Augmenting Demand for Value Added Dairy Ingredients

The sports nutrition sector's expansion is driving strategic consolidation, exemplified by Arla Foods Ingredients' acquisition of Volac's Whey Nutrition business, which strengthens whey protein capabilities across seven international production facilities. This consolidation reflects the sector's evolution beyond traditional protein powders toward sophisticated bioactive ingredients, with whey protein concentrates and isolates commanding premium pricing due to their superior amino acid profiles. The UK Competition and Markets Authority's approval of this acquisition signals regulatory recognition of market concentration benefits for innovation capacity and supply chain efficiency. However, EFSA's stringent health claims evaluation process has rejected several whey protein claims for muscle mass and satiety benefits, requiring manufacturers to focus on scientifically substantiated applications rather than broad wellness positioning [2]Source: European Food Safety Authority, "EFSA-Health Claims Related To Whey Protein and Increase in Satiety", efsa.europa.eu. This regulatory scrutiny paradoxically strengthens market positioning for companies with robust clinical evidence, creating competitive moats around validated functional ingredients.

Global Infant Formula Demand Accelerates Market Expansion Significantly

Infant formula represents a high-value application driving dairy ingredient innovation, with EU infant food exports valued at approximately EUR 8 billion annually and ranking among the top three agri-food export categories. Regulatory tightening through Commission Regulation (EU) 2024/1003 lowered 3-MCPD contaminant limits in infant formulas to 80 µg/kg for powder forms, effective January 2025, requiring enhanced quality control across the dairy ingredient supply chain. This regulatory evolution creates barriers to entry while rewarding established players with advanced processing capabilities and quality systems. FrieslandCampina's TFDA approval for Vivinal MFGM in Thai infant formulas demonstrates the global reach of European dairy ingredient innovation, with 74% of novel infant formulas now containing at least one bioactive ingredient. The sector's premiumization trend toward functional ingredients like lactoferrin, osteopontin, and milk fat globule membrane proteins creates sustained demand for specialized dairy fractions. EU Delegated Regulation (EU) 2016/127 mandates specific compositional requirements including whey-to-casein ratios and DHA content, standardizing ingredient specifications across member states and export markets.

Functional Food Applications Create New Market Growth Opportunities

Functional food applications are expanding beyond traditional boundaries, with iron milk caseinate receiving EU authorization as a novel food ingredient for fortification applications under Commission Regulation (EU) 2024/1821. This regulatory approval demonstrates the pathway for dairy-derived functional ingredients to gain market access, though EFSA's rigorous safety and bioavailability assessments create high barriers for new entrants. The functional foods sector benefits from established health claims for calcium, protein, and live yogurt cultures under EU Regulation 1924/2006, providing clear regulatory pathways for ingredient marketing. However, EFSA's rejection of broader dairy health claims, including casein hydrolysate applications for blood glucose management, emphasizes the need for robust clinical evidence rather than theoretical benefits. CSM Bakery Solutions' patent portfolio for calcium concentrate suspensions in soy-based dairy alternatives illustrates how traditional dairy ingredient companies are adapting to hybrid applications, securing intellectual property around calcium fortification technologies for both dairy and plant-based products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lactose Intolerance Cases Drive Market Transformation | -0.4% | Southern Europe, Italy, Greece | Long term (≥ 4 years) |

| Plant-Based Milk Alternatives Experience Significant Growth | -0.6% | Northern Europe, Germany, Netherlands | Medium term (2-4 years) |

| Raw Milk Price Volatility Influences Market Development | -0.5% | EU-wide with Ireland, Poland impact | Short term (≤ 2 years) |

| Health-Conscious Consumers Shift Towards Alternative Dietary Choices | -0.3% | Western Europe, urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lactose Intolerance Cases Drive Market Transformation

Lactose intolerance prevalence varies dramatically across European markets, creating geographic demand disparities that influence ingredient formulation strategies. Southern European countries exhibit significantly higher intolerance rates, with Italy at 72% and Greece at 55%, compared to Northern European markets like Denmark and Ireland at 4%. This geographic variation drives market segmentation toward lactose-free and reduced-lactose ingredients, with EU Directive 2024/1438 explicitly authorizing lactose reduction through enzymatic conversion to glucose and galactose in preserved milk products. EFSA's scientific guidance establishes that most lactose-intolerant individuals can tolerate up to 12 grams of lactose as a single dose, providing formulation parameters for ingredient manufacturers targeting sensitive populations. The regulatory framework requires clear labeling of lactose content modifications, creating transparency while enabling market differentiation. However, this geographic disparity also creates opportunities for specialized lactose-free ingredient production, particularly in high-prevalence regions where local processing capabilities can serve both domestic and export markets.

Raw Milk Price Volatility Influences Market Development

Raw milk price volatility reached extreme levels in 2024, with Ireland experiencing 15% price increases while 16 EU member states recorded price declines, creating supply chain disruption and margin pressure across ingredient processors. This volatility stems from multiple factors including disease outbreaks, environmental regulations reducing herd sizes, and global demand fluctuations affecting export competitiveness. Poland's milk prices fell 6.5% month-on-month in January 2025 despite strong annual growth, illustrating the short-term volatility that complicates ingredient pricing and procurement planning. EU milk production forecasts indicate continued decline to 149.4 million tonnes in 2025 from 149.6 million tonnes in 2024, driven by falling cow numbers and tight farmer margins, constraining raw material availability for ingredient processing [3]Source: U.S Department of Agriculture, "European Union: Dairy and Products Annual", fas.usda.gov. The Common Agricultural Policy's EUR 188 billion income support framework provides some stability through direct payments, though these are increasingly tied to environmental compliance requirements that may further constrain production volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Powders Dominate Processing Efficiency

Milk powders command 47.10% market share in 2025, reflecting their fundamental role in ingredient applications requiring extended shelf life, concentrated nutrition, and processing versatility. This dominance stems from their critical function in bakery, confectionery, and infant formula applications where consistent protein and mineral content is essential for product standardization. The segment is projected to grow at 4.62% CAGR through 2031, driven by export demand and processing efficiency improvements. Whey ingredients represent the second-largest category, benefiting from sports nutrition expansion and functional food applications, while experiencing consolidation through strategic acquisitions like Arla's Volac purchase. Milk protein concentrates and isolates occupy specialized high-value niches, particularly in clinical nutrition and premium sports applications where protein purity and bioavailability command premium pricing.

Lactose and derivatives serve dual functions as sweetening agents and pharmaceutical excipients, maintaining steady demand despite lactose intolerance concerns due to their technical functionality in processed foods. Casein and caseinates provide unique functional properties for cheese applications and protein fortification, though EFSA's rejection of certain casein hydrolysate health claims limits premium positioning opportunities. The "Others" category includes emerging bioactive ingredients like lactoferrin, with FrieslandCampina's new production facility expansion indicating growing commercial viability for specialized dairy fractions. EU Regulation 2024/1821's authorization of iron milk caseinate as a novel food ingredient demonstrates regulatory pathways for innovative dairy-derived functional ingredients, though the approval process requires substantial clinical evidence and safety documentation.

By Nature: Conventional Maintains Dominance Despite Organic Acceleration

Conventional dairy ingredients maintain 85.05% market share in 2025, reflecting cost advantages and established supply chains that serve mainstream food processing applications. However, organic ingredients are experiencing accelerated growth at 5.78% CAGR through 2031, supported by EU organic farmland expansion to 17.7 million hectares representing 10.9% of total agricultural area. This growth trajectory is constrained by supply limitations, particularly in Poland where only 0.2% of milk production is organic despite being the EU's third-largest milk producer. Organic dairy processing faces concentration challenges, with over 90% of Poland's organic milk processed by four large dairies, creating procurement bottlenecks and price volatility.

The organic premium averages 20-30% above conventional pricing, though Polish organic milk prices often equal or fall below conventional prices due to supply chain inefficiencies and limited retail demand. EU organic regulations require pasture-based systems with at least 60% roughage in daily dry matter intake and maximum stocking densities of 2 dairy cows per hectare, constraining yields to 72-91% of conventional levels. Denmark and Austria lead organic market development with 13.2% and 17.3% organic milk shares respectively, providing models for supply chain organization and premium market development. The organic segment benefits from CAP support through agri-environment-climate measures targeting at least 30% of rural development funding toward environmental objectives, though success requires coordinated producer-processor cooperation and guaranteed procurement arrangements.

By Livestock Origin: Cow Milk Dominance Faces Niche Competition

Cow milk ingredients dominate with 82.70% market share in 2025, reflecting established processing infrastructure, consistent supply, and standardized compositional profiles that meet industrial requirements. This dominance is supported by the EU's 20 million dairy cow herd producing approximately 160 million tonnes annually, with average yields of 7,653 kg per cow providing economies of scale for ingredient processing. However, goat milk ingredients are experiencing the fastest growth at 5.52% CAGR through 2031, driven by perceived digestibility advantages and premium positioning in infant formula and specialty nutrition applications. Buffalo milk ingredients serve niche applications, particularly in traditional cheese production and specialty Mediterranean products where unique protein and fat compositions provide functional advantages.

Goat milk's growth trajectory reflects consumer perceptions of easier digestibility and closer similarity to human milk composition, though scientific evidence for superior digestibility remains limited. The segment benefits from artisanal and premium positioning, with organic goat milk commanding substantial premiums over conventional cow milk equivalents. Sheep milk ingredients occupy the smallest market share but serve specialized applications in traditional European cheeses and premium nutrition products. EU livestock statistics show 1.4 million organic goats representing 12.7% of the total goat herd, indicating strong organic penetration in this segment. Regulatory frameworks under EU animal health and welfare legislation apply uniformly across livestock origins, though specific compositional standards for infant formula explicitly reference cow and goat milk proteins as authorized sources under Delegated Regulation (EU) 2016/127.

By Application: Sports Nutrition Drives Premium Growth

Sports and clinical nutrition represents the fastest-growing application segment at 5.16% CAGR through 2031, reflecting consumer prioritization of functional nutrition and protein supplementation. This growth is exemplified by strategic consolidation including Arla's acquisition of Volac's whey nutrition business, strengthening capabilities in high-protein and specialized whey applications. The segment benefits from established protein health claims under EU Regulation 1924/2006, allowing marketing for muscle mass maintenance and growth, though EFSA has rejected broader whey-specific claims requiring generic protein positioning rather than ingredient-specific benefits. Bakery and confectionery maintains the largest application share at 28.55% in 2025, driven by dairy ingredients' functional properties in dough conditioning, flavor enhancement, and nutritional fortification.

Infant milk formula represents a high-value application commanding premium pricing due to stringent regulatory requirements and specialized compositional needs. EU Delegated Regulation (EU) 2016/127 mandates specific protein sources, whey-to-casein ratios, and mineral content, creating technical barriers that favor established ingredient suppliers with regulatory expertise and quality systems. Dairy products applications encompass cheese, yogurt, and fermented products where dairy ingredients provide functional and nutritional enhancement. Convenience and ready-to-eat foods represent a growing application driven by urbanization and lifestyle changes, requiring ingredients with extended shelf life and processing stability. The regulatory environment supports application diversification through authorized health claims for calcium, protein, and live cultures, though claim substantiation requires robust clinical evidence and EFSA approval processes that favor established players with research capabilities.

Geography Analysis

Germany maintains market leadership with 22.10% share in 2025, leveraging its position as the EU's largest milk producer at approximately 33 million tonnes annually and extensive processing infrastructure serving both domestic and export markets. German dairy ingredient companies benefit from advanced technology, established export relationships, and proximity to major food processing centers across Central Europe.

The Netherlands follows as a significant player despite its smaller geographic size, reflecting high productivity per cow at over 8,000 kg annually and sophisticated cooperative structures that optimize supply chain efficiency. France contributes substantial production capacity particularly in cheese and specialty dairy ingredients, supported by strong domestic consumption and export traditions. Poland emerges as the fastest-growing geography at 6.53% CAGR through 2031, positioned to potentially become the EU's third-largest milk producer by 2025 following 3.9% production growth in 2024 versus the EU average of 0.6%. This growth reflects modernized processing infrastructure, competitive cost structures, and strategic export positioning with 63% of dairy exports directed to EU markets led by Germany at 19% of export value.

Italy and Spain contribute significant production volumes though face challenges from higher lactose intolerance prevalence affecting domestic consumption patterns. The UK's post-Brexit position creates both challenges and opportunities, with trade relationships requiring new regulatory frameworks while maintaining significant processing capabilities. Belgium, Sweden, and other smaller markets serve specialized roles in organic production and premium ingredient applications, with Sweden achieving 18% organic milk share demonstrating advanced sustainable production systems.

Competitive Landscape

The European dairy ingredients market exhibits moderate concentration, characterized by strategic consolidation among established players seeking to strengthen specialized capabilities and geographic reach. Market dynamics reflect a shift toward value-added ingredients and functional applications, with companies pursuing vertical integration and technology-driven differentiation rather than commodity volume competition. Arla Foods' acquisition of Volac's whey nutrition business exemplifies this trend, combining Danish cooperative scale with UK specialty protein expertise to serve growing sports nutrition demand across seven international production facilities. Similarly, Kerry Group's EUR 500 million divestment of dairy operations to refocus on pure-play B2B taste and nutrition solutions demonstrates portfolio optimization toward higher-margin ingredient applications.

Opportunities emerge in bioactive ingredient development, with FrieslandCampina's lactoferrin production facility expansion indicating commercial viability for specialized dairy fractions serving infant nutrition and clinical applications. Technology adoption focuses on precision processing, sustainability improvements, and regulatory compliance capabilities, with CSM Bakery Solutions securing patent protection for calcium concentrate suspensions applicable to both dairy and plant-based formulations.

Emerging disruptors include hybrid dairy-plant ingredient suppliers and specialized organic processors, though regulatory barriers through EFSA health claims evaluation and EU compositional standards favor established players with clinical research capabilities and quality systems. Compliance factors under EU Regulation 1924/2006 for health claims and Delegated Regulation (EU) 2016/127 for infant formula create competitive moats around companies with regulatory expertise and established safety documentation.

Europe Dairy Ingredients Industry Leaders

-

Arla Foods amba

-

Koninklijke FrieslandCampina N.V.

-

Fonterra Co-operative Group Limited

-

Saputo Inc.

-

Groupe Lactalis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Dutch ingredient company Vivici launched Vivitein BLG, a precision-fermented dairy protein (beta-lactoglobulin), in the U.S. market in March 2025. Vivitein BLG offers consumers and food & beverage companies a sustainable, vegan-friendly protein for active nutrition products, providing clear protein beverages, high-performance powders, and luscious protein bars, all without animal involvement.

- September 2024: Arla Foods Ingredients launched a new campaign to inspire dairy manufacturers to create innovative high-protein products. The 'Go High in Protein' campaign showcased the Arla Foods Ingredients Nutrilac ProteinBoost range of patented microparticulated whey proteins, which were rich in all the essential amino acids. It demonstrated how they could be used to overcome technical challenges and create high-protein dairy products with appealing taste and texture.

- November 2023: Finnish dairy company Valio launched a new milk protein concentrate, Valio Eila® MPC 65, in November 2023. The new lactose-free MPC is for creating better-tasting high-protein products like puddings and shakes for manufacturers globally.

Europe Dairy Ingredients Market Report Scope

By type, the European dairy ingredients market is segmented into milk powders, milk protein concentrates and milk protein isolates, whey ingredients, lactose and derivatives, casein and caseinates, and others, and by application, the market is segmented into bakery and confectionery, dairy products, infant milk formula, sports and clinical nutrition, others. Moreover, the study provides an analysis of the dairy ingredients market in the emerging and established markets across European countries, including Germany, the United Kingdom, France, Russia, Italy, Spain, and the Rest of Europe.

By Product Type

| Milk Powders | Skimmed Milk Powder |

| Whole Milk Powder | |

| Others | |

| Milk Protein Concentrates and Isolates | |

| Whey Ingredients | Whey Protein Concentrate |

| Whey Protein Isolate | |

| Hydrolyzed Whey Protein | |

| Lactose and Derivatives | |

| Casein and Caseinates | |

| Others |

By Nature

| Conventional |

| Organic |

By Livestock Origin

| Cow |

| Buffalo |

| Goat and Sheep |

By Application

| Bakery and Confectionery |

| Dairy Products |

| Infant Milk Formula |

| Sports and Clinical Nutrition |

| Convenience and Ready-to-Eat Foods |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Milk Powders | Skimmed Milk Powder |

| Whole Milk Powder | ||

| Others | ||

| Milk Protein Concentrates and Isolates | ||

| Whey Ingredients | Whey Protein Concentrate | |

| Whey Protein Isolate | ||

| Hydrolyzed Whey Protein | ||

| Lactose and Derivatives | ||

| Casein and Caseinates | ||

| Others | ||

| By Nature | Conventional | |

| Organic | ||

| By Livestock Origin | Cow | |

| Buffalo | ||

| Goat and Sheep | ||

| By Application | Bakery and Confectionery | |

| Dairy Products | ||

| Infant Milk Formula | ||

| Sports and Clinical Nutrition | ||

| Convenience and Ready-to-Eat Foods | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe dairy ingredients market?

The market is valued at USD 20.38 billion in 2026.

How fast is the sports-nutrition application segment growing in Europe?

Sports and clinical nutrition ingredients are projected to rise at a 5.16% CAGR between 2026 and 2031.

Which country is the fastest-growing producer of dairy ingredients in Europe?

Poland is forecast for the quickest 6.53% CAGR through 2031.

How large is the milk-powder segment within European dairy ingredients?

Milk powders hold 47.10% of market share as of 2025.

Page last updated on: