Human Augmentation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 394.62 Billion |

| Market Size (2030) | USD 715 Billion |

| Growth Rate (2025 - 2030) | 12.62% CAGR |

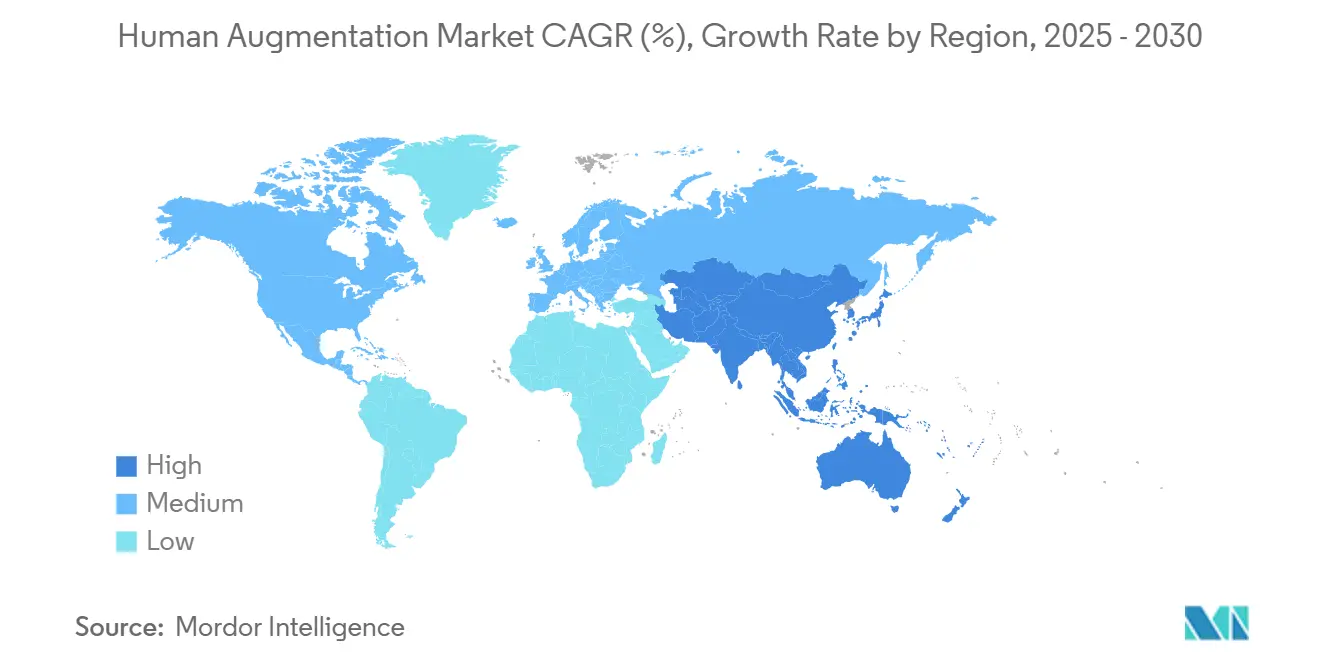

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

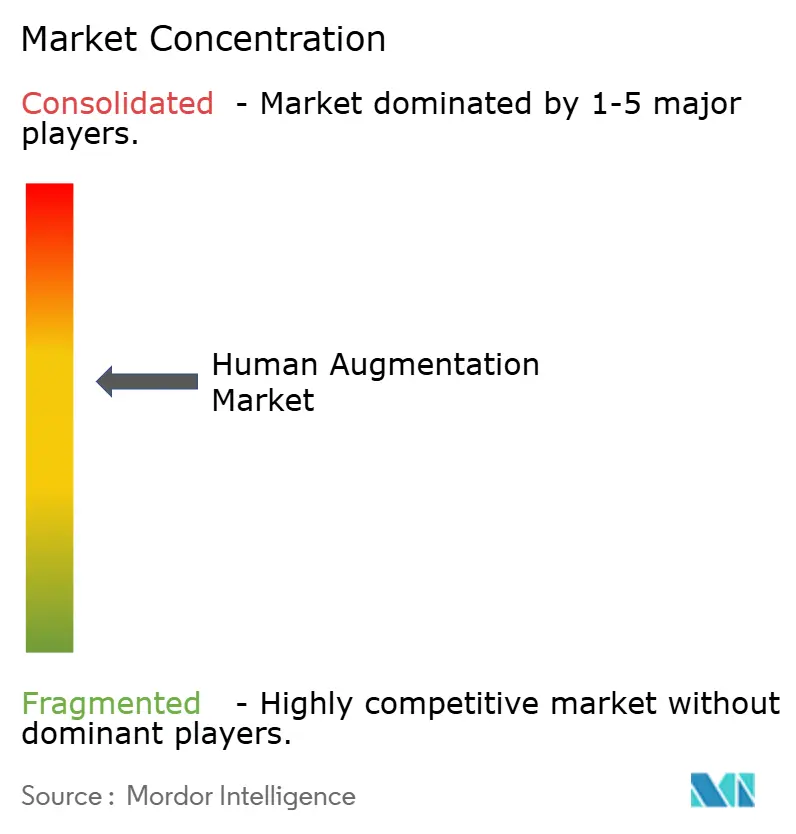

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Augmentation Market Analysis by Mordor Intelligence

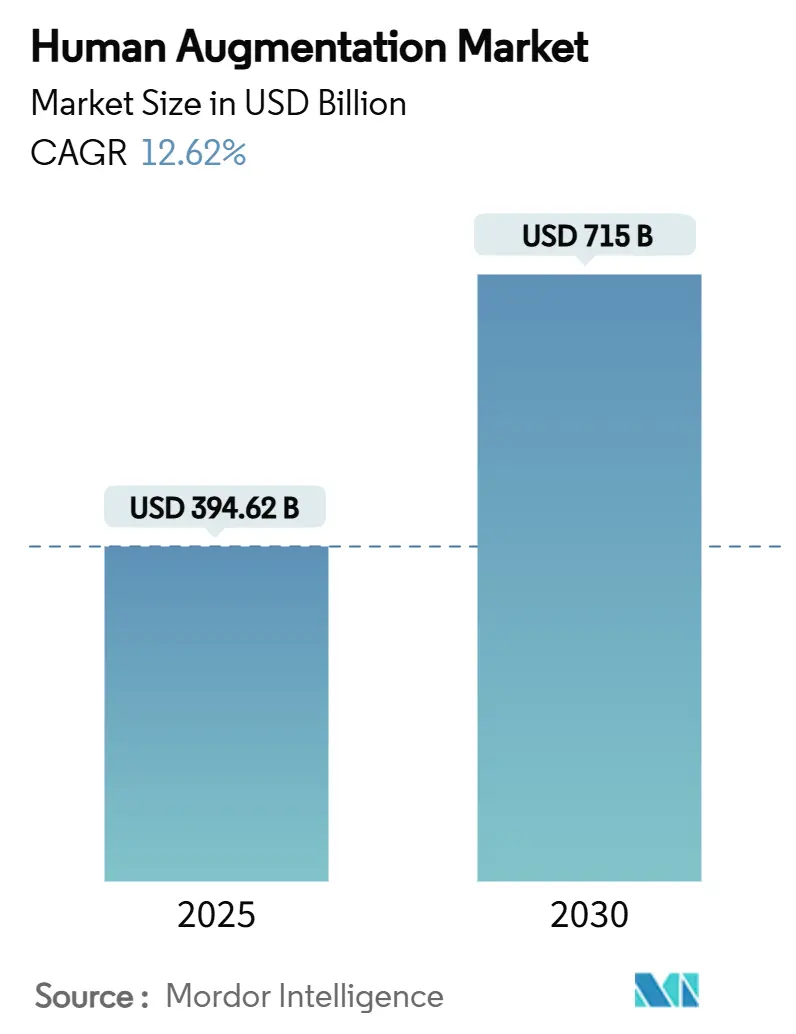

The Human Augmentation Market size is estimated at USD 394.62 billion in 2025, and is expected to reach USD 715 billion by 2030, at a CAGR of 12.62% during the forecast period (2025-2030).

Solid growth mirrors the migration of augmentation technologies from laboratories to regulated commercial environments that address chronic-disease care, industrial productivity, and defense readiness. Annual corporate investments above USD 80 billion, a rising volume of FDA breakthrough device designations, and Medicare's first personal exoskeleton reimbursement signal that the human augmentation market has crossed the threshold to wide-scale adoption, while AI-enabled component integration compresses form factors, lowers power demands, and shortens training curves for end users. Nevertheless, semiconductor and lithium battery bottlenecks lengthen lead times to as much as 12 months and keep battery pack costs near USD 94.5 per kWh, adding price pressure to finished devices.

Key Report Takeaways

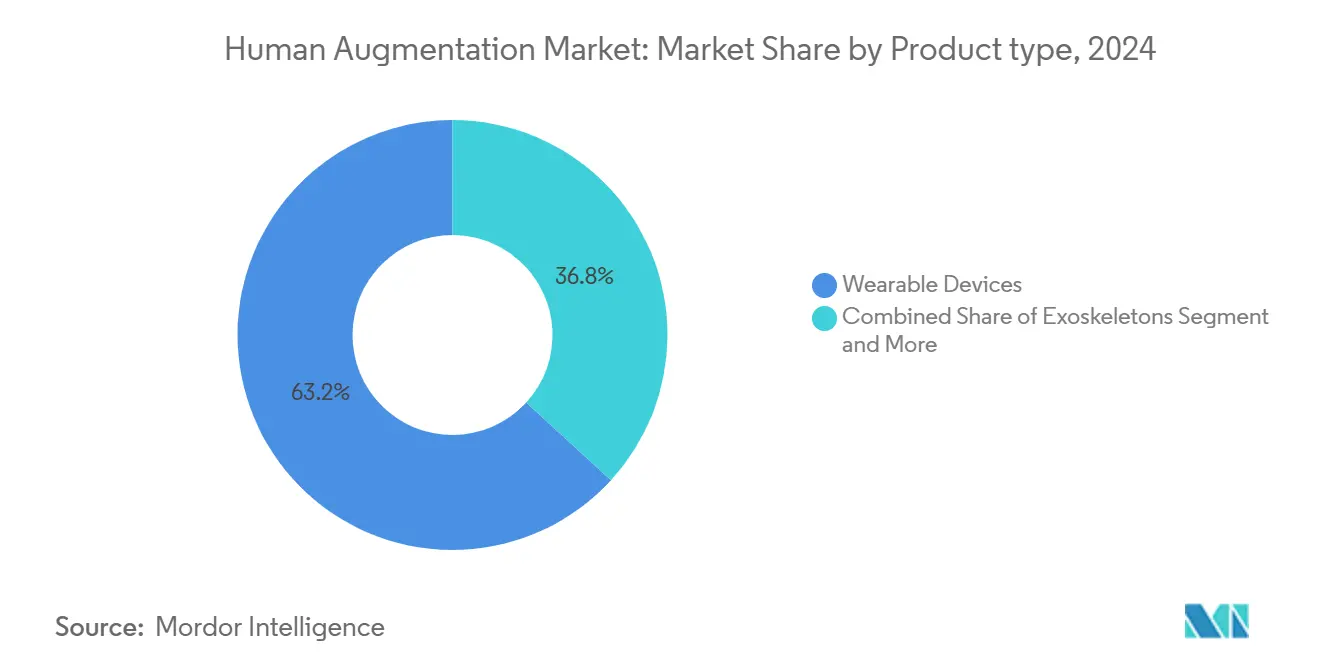

- By product type, wearable devices led with 63.20% of the human augmentation market share in 2024, while smart exoskeletons posted the highest forecast CAGR at 25.70% through 2030.

- By functionality, physical augmentation accounted for 47.20% of the human augmentation market size in 2024, and cognitive augmentation is set to climb at a 27.80% CAGR to 2030.

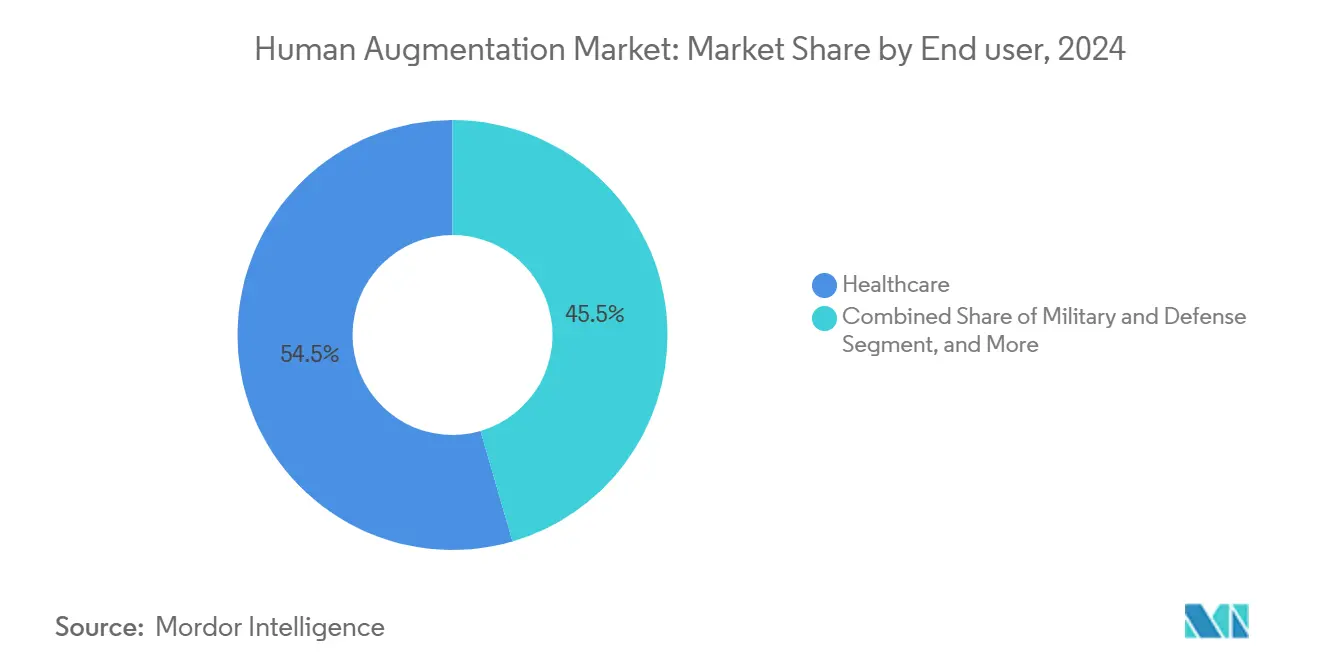

- By end user, healthcare captured a 54.50% share of the human augmentation market size in 2024; industrial and manufacturing is projected to expand at a 30.60% CAGR between 2025-2030.

- By the augmentation method, body-worn external devices held a 70.80% share of the human augmentation market size in 2024, while implantable neural interfaces are advancing at a 28.70% CAGR.

- By geography, North America dominated with 38.90% revenue share in 2024; Asia-Pacific is forecast to accelerate at a 25.10% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Human Augmentation Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory approvals and annual investments above USD 80 billion | +3.0% | North America, Europe | Long term (≥ 4 years) |

| Rising prevalence of chronic diseases requiring assistive devices | +2.8% | North America, Europe | Long term (≥ 4 years) |

| Rapid adoption of wearable technology and IoT in healthcare | +2.1% | APAC, North America | Medium term (2-4 years) |

| Military investments in soldier-performance enhancement | +1.9% | North America, Europe, APAC | Medium term (2-4 years) |

| ESG-driven workplace exoskeleton rollouts | +1.6% | Global industrial hubs | Short term (≤ 2 years) |

| Corporate demand for neuro-tech workforce analytics | +1.4% | North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Requiring Assistive Devices

Hospitals and rehabilitation centres are treating an unprecedented 1.7 billion cases of neurological and musculoskeletal disorders, expanding the addressable pool for exoskeletons and other assistive platforms. Medicare’s landmark decision to reimburse personal exoskeletons at USD 91,031.93 per device validated the clinical and economic case for robotic mobility aids. Follow-on approvals, such as the first East Coast patient financed under the policy, show how reimbursement precedents stimulate provider adoption across multiple states. Clinical trials indicate 40% faster recovery when exoskeletons augment therapy protocols, and stroke programs that integrate robotic gait training witness 32% quicker functional gains versus conventional methods. As public and private payers now cover the capital cost, hospitals can amortize investments over more predictable usage volumes, removing a historical barrier to scale.

Military Investments in Soldier-Performance Enhancement Programs

Defense agencies allocated more than USD 15 billion to augmentation initiatives in 2024, led by the U.S. Hyper-Enabled Operator program that pairs AI-assisted decision support with powered exoskeletons. Japan’s Defense Ministry formed a 30-member task force dedicated to combat drones and AI warfare, underscoring a global race for physiological and cognitive superiority. DARPA’s RBC-Factory project modifies red blood cells to improve endurance without altering DNA, illustrating how chemical enhancements complement mechanical augmentation. Analyses from the Center for a New American Security advise broader R&D collaboration to translate battlefield breakthroughs into civil-market prototypes. Military budgets are less cyclical than commercial capital spending, providing a floor for ongoing R&D even during macroeconomic slowdowns.

ESG-Driven Workplace Exoskeleton Rollouts

Musculoskeletal disorders cost U.S. employers USD 17.7 billion annually, raising worker safety to the forefront of ESG scorecards. HeroWear’s field data confirm 30% reductions in lower-back discomfort and 8% productivity lifts following exosuit adoption. Colorado insurer Pinnacol Assurance reported 80% user acceptance in construction pilots, with most participants asking to keep the devices after the test period. Automotive plants such as Ford documented zero strain injuries in exoskeleton-equipped stations, demonstrating that human augmentation market solutions can deliver measurable ROI within five months. Because ESG audit frameworks now mandate quantitative safety metrics, exoskeleton purchases increasingly shift from discretionary to compliance spending.

Rapid Adoption of Wearable Technology & IoT in Healthcare

Healthcare IoT installations are growing 35% per year as providers embed sensors and augmented-reality headsets into care pathways. Apple Vision Pro has already migrated from consumer launch to operating-room toolkits, assisting orthopedic, rehabilitation, and imaging workflows [1]Apple Inc., “Apple Vision Pro Unlocks New Opportunities for Health App Developers,” apple.com . Cedars-Sinai uses Vision Pro and AI to deliver digital mental-health therapy, an early proof that consumer hardware can satisfy clinical evidence standards. ZEISS’s Surgery Optimizer app projects 3D visualizations directly in the surgeon’s field of view, with peer-reviewed trials showing 25% gains in precision. Because reimbursement and device-approval pathways for hospital use are mature, vendors can unlock revenue streams faster than in purely consumer channels, accelerating the human augmentation market adoption cycle.

Restraints Impact Analysis of Human Augmentation Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced augmentation hardware and procedures | -2.3% | Global, price-sensitive markets | Medium term (2-4 years) |

| Regulatory uncertainties and lengthy approval cycles | -1.8% | North America, Europe | Short term (≤ 2 years) |

| Societal backlash over algorithmic bias in cognitive wearables | -1.2% | Western privacy-focused regions | Long term (≥ 4 years) |

| Supply-chain shortages in semiconductors and batteries | -1.0% | Global electronics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Augmentation Hardware & Procedures

Lithium batteries priced at USD 94.5 per kWh and AI-grade semiconductors with 6-to-12-month lead times inflate bill-of-materials costs, pushing retail prices beyond many consumers’ budgets. Precision manufacturing requirements for 1,024-electrode brain‐computer interfaces restrict supplier pools and limit economies of scale. Although robotic manufacturing expenses fell 40% in 2025, typical consumer humanoids still retail above USD 8,000, a price point palatable only to enterprise buyers. German Bionic’s Exia exoskeleton offers AI-based load balancing but requires sizeable capital outlays that smaller firms hesitate to commit without guaranteed payback. Recycling programs are cutting battery costs by 44%, yet need another 3-5 years to scale.

Regulatory Uncertainties and Lengthy Approval Cycles

The FDA’s new Predetermined Change Control Plan framework clarifies software-update rules but introduces additional design-history-file obligations that can delay launches. Quality System Regulation amendments effective February 2026 will impose further manufacturing documentation, extending development timelines[2]Federal Register, “Medical Devices; Quality System Regulation Amendments,” federalregister.gov . Neuralink experienced congressional scrutiny even after receiving a clinical-trial green light, signaling that political oversight can add non-technical risk layers. Multimarket strategies face inconsistent standards because Japan’s upcoming AI bill diverges from U.S. and EU approaches. Venture capital firms, therefore, discount valuations for early-stage projects until pathway certainty improves, slowing capital formation in the human augmentation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Human Augmentation Market Segment Analysis

By Product Type:

Wearables Dominate Revenue While Exoskeletons Lead GrowthWearable devices contributed 63.20% of the human augmentation market share in 2024, underpinned by integrated sensor modules that piggyback on smartphone ecosystems. The human augmentation market size for wearables rose in tandem with health-tracking subscriptions and enterprise wellness budgets. Smart exoskeletons, though representing a smaller revenue base, are forecast to expand at a 25.70% CAGR as manufacturers focus on injury prevention mandates. German Bionic’s Exia combines AI algorithms with mechanical lift assistance to fine-tune torque output in real time, enhancing factory throughput without adding floor-space constraints.

Price declines and component modularity keep consumer wearables on a steady upgrade cadence, while industrial exoskeletons rely on corporate ROI models that hinge on injury claim reductions. Venture investors placed USD 650 million into Neuralink’s Series E round, illustrating long-term confidence in implantable segments despite their current single-digit revenue contribution. Meanwhile, Hypershell’s X Series exoskeleton targets weekend athletes, promising 30% strain reduction over a 10-mile endurance horizon at prices edging closer to mass electronics brackets. These contrasting trajectories reveal wide dispersion in component spec sheets, supply chains, and regulatory oversight across product classes.

By Functionality:

Physical Leadership Faces Swift Cognitive UpshiftPhysical augmentation retained a 47.20% revenue lead in 2024 as hospitals and factories prioritized mobility aids and strength support. Cognitive platforms, supported by FDA breakthrough tags, are accelerating at a 27.80% CAGR. Synchron’s partnership with NVIDIA’s GPU stack proves that high-bandwidth neural decoding can run on commercial off-the-shelf hardware, materially lowering deployment hurdles. The human augmentation market size for cognitive applications remains modest today, but is scaling rapidly as clinical pilots demonstrate speech restoration in paralyzed patients.

Sensor-based sensory augmentation occupies a middle ground, with Apple Vision Pro already guiding surgeons through overlayed anatomical maps. Ethical debates around mental privacy and algorithmic bias create an additional review layer for cognitive devices, while mechanical aids face more traditional safety testing. Neuralink’s speech-restoration implant secured an FDA breakthrough designation, showing regulator receptiveness to transformative neurotech when risk–benefit ratios are clear.

By End User:

Healthcare Still Commands Majority, Industry Ramps FastHealthcare providers held 54.50% of the human augmentation market size in 2024, enabled by established reimbursement codes and clinically validated outcomes. Industrial and manufacturing buyers are projected to grow 30.60% per year as ESG audit checklists emphasize injury-rate reductions [3]GAO, “Wearable Technologies: Opportunities and Deployment Challenges,” gao.gov . Ford, Hyundai, and other automakers have shown that exoskeleton programs can eliminate shoulder-strain incidents without slowing assembly lines.

Worker-safety economics drive quick paybacks: HeroWear pilots saved enterprises USD 3,900 per employee annually through fewer workers-comp claims and improved productivity. Defense remains a specialized but stable niche as militaries expand augmentation funding. Consumer uptake stays modest because high entry prices deter retail experimentation, although Apple’s mainstream ecosystem could pull select applications into households over the forecast horizon.

By Augmentation Method:

External Devices Rule, Neural Interfaces SurgeBody-worn external devices accounted for 70.80% of the human augmentation market share in 2024, benefitting from lower regulatory barriers and faster design iterations. The human augmentation market size for external wearables spans everything from smartwatches to passive shoulder supports. Implantable neural interfaces are projected to climb at 28.70% CAGR as wireless cortical arrays like Precision Neuroscience’s Layer 7 receive full FDA clearance for 30-day in-patient studies.

Non-invasive methods continue to anchor the consumer and industrial continuum, while minimally invasive techniques gain favor in hospital settings requiring higher fidelity signals. Blackrock Neurotech’s USD 200 million funding injection typifies investor appetite for durable implants that address long-term severe disabilities. The choice of method increasingly aligns with duration of need: short-term rehabilitation favors external gear, whereas lifelong conditions justify implanted solutions.

Geography Analysis

North America Human Augmentation Market

North America generated 38.90% of global revenue in 2024, propelled by USD 15 billion in annual Department of Defense augmentation spending and Medicare’s exoskeleton reimbursement precedent [4]DARPA, “Protecting Warfighters in Extreme Environments,” darpa.mil. FDA breakthrough designations for Neuralink and Precision Neuroscience give U.S. firms a time-to-market edge in neural interfaces, while Microsoft’s USD 80 billion AI infrastructure outlay provides the compute backbone for data-heavy cognitive applications. Semiconductor and battery supply shocks expose the region to cost inflation, prompting OEMs to explore near-shoring strategies to reduce dependence on Asia-sourced inputs.

APAC Human Augmentation Market

Asia-Pacific is the fastest-expanding theatre, set to grow at a 25.10% CAGR as regional AI revenue approaches USD 300 billion by 2030. Japan’s creation of a defense AI task force and South Korea’s convergence of battery and humanoid-robot supply chains underscore a policy push toward sovereign augmentation capabilities. SoftBank’s talks to lead a USD 500 million humanoid-robotics round illustrate deep venture liquidity, while China’s Military-Civil Fusion accelerates technology diffusion from labs to shop floors.

Europe Human Augmentation Market

Europe trails the growth pace but offers fertile ground where stringent worker-safety rules drive industrial exoskeleton demand. German Bionic’s AI-enhanced systems meet EU occupational-health directives, reassuring plant managers about compliance. Rigorous medical-device requirements bolster consumer confidence yet lengthen approval clocks, nudging some start-ups to pilot first in the United States. Privacy-centric legislation could temper uptake of algorithm-heavy cognitive wearables, but physical-assistance platforms face fewer data-sovereignty hurdles.

Competitive Landscape

The human augmentation market is fragmented, with platform giants and specialized players pursuing divergent strategies. Microsoft aligns its cloud stack with OpenAI's models to capture enterprise cognitive workloads, while Apple's 32 AI-startup acquisitions in 2023 strengthen its integrated hardware–software ecosystem. Neuralink, Synchron, and Precision Neuroscience focus narrowly on brain-computer interfaces, each securing FDA designations that shorten the clinical path to commercial release.

Industrial exoskeleton suppliers such as Ekso Bionics and German Bionic leverage hard ROI metrics to win factory contracts, contrasting with longer-horizon neurotech bets that hinge on clinical milestones. World Intellectual Property Organization patent-landscape mapping shows a 26.4% CAGR in filings for occupational-safety prediction systems, indicating data analytics overlays as the next competitive frontier, while new entrants such as Subsense and Paradromics attract capital by promising less invasive brain-computer interfaces and large insurers and hospital groups shape vendor selection through reimbursement policy and outcome-based procurement.

The ability to navigate regulatory complexity, secure reimbursement codes, and prove measurable functional gains increasingly outweighs pure technological differentiation. Strategic alliances—Microsoft with OpenAI, Synchron with NVIDIA—illustrate a convergence trend where compute platforms and specialized hardware co-develop go-to-market plans.

Human Augmentation Industry Leaders

Apple Inc.

Samsung Electronics Co. Ltd.

Medtronic plc

Ekso Bionics Holdings Inc.

Google LLC(Alphabet Inc.)

- *Disclaimer: Major Players sorted in no particular order

Human Augmentation Market Companies Covered in this Report

- Apple Inc.

- Samsung Electronics Co. Ltd.

- Google LLC(Alphabet Inc.)

- Meta Platforms Inc.

- Microsoft Corp.

- Sony Group Corp.

- Vuzix Corporation

- Magic Leap Inc.

- Medtronic plc

- Boston Scientific Corp.

- Abbott Laboratories

- Cochlear Limited

- Ossur hf.

- Ottobock SE & Co. KG

- Stryker Corporation

- Ekso Bionics Holdings Inc.

- ReWalk Robotics Ltd.

- Cyberdyne Inc.

- Sarcos Technology & Robotics Corp.

- Lockheed Martin Corp.

- Neuralink Corp.

Recent Industry Developments in Human Augmentation Market

- July 2025: Zimmer Biomet agreed to acquire Monogram Technologies for USD 177 million to expand its orthopedic robotics line.

- June 2025: Neuralink closed a USD 650 million Series E round that values the firm at about USD 9 billion.

- May 2025: German Bionic introduced the Exia AI-augmented exoskeleton for industrial workplaces.

- April 2025: Precision Neuroscience gained full FDA clearance for the wireless Layer 7 Cortical Interface.

Global Human Augmentation Market Report Scope

Segmentation Overview

| Wearable Devices |

| Exoskeletons |

| Neuro-prosthetics and Bionics |

| Medical and Assistive Implants |

| XR Interfaces |

| Human Machine Interface (HMI) Modules |

| Physical Augmentation |

| Sensory Augmentation |

| Cognitive Augmentation |

| Emotional and Behavioral Augmentation |

| Aesthetic/Appearance Enhancement |

| Healthcare |

| Industrial and Manufacturing |

| Military and Defense |

| Defense and Aerospace |

| Consumer Electronics and Gaming |

| Corporate/Enterprise Training |

| External Body-worn |

| Implantable (Invasive) |

| Neural Interface |

| Immersive Virtual/Software-only |

| Ingestible and Injectable |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Wearable Devices | |

| Exoskeletons | ||

| Neuro-prosthetics and Bionics | ||

| Medical and Assistive Implants | ||

| XR Interfaces | ||

| Human Machine Interface (HMI) Modules | ||

| By Functionality | Physical Augmentation | |

| Sensory Augmentation | ||

| Cognitive Augmentation | ||

| Emotional and Behavioral Augmentation | ||

| Aesthetic/Appearance Enhancement | ||

| By End User | Healthcare | |

| Industrial and Manufacturing | ||

| Military and Defense | ||

| Defense and Aerospace | ||

| Consumer Electronics and Gaming | ||

| Corporate/Enterprise Training | ||

| By Augmentation Method | External Body-worn | |

| Implantable (Invasive) | ||

| Neural Interface | ||

| Immersive Virtual/Software-only | ||

| Ingestible and Injectable | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the human augmentation market?

The human augmentation market size is USD 394.62 billion in 2025 and is projected to reach USD 715 billion by 2030.

Which region holds the largest share of the human augmentation market?

North America leads with 38.90% of global revenue, driven by defense spending and Medicare reimbursement for exoskeletons.

Which product segment shows the fastest growth?

Smart exoskeletons are forecast to grow at a 25.70% CAGR, outpacing other product categories through 2030.

How quickly are cognitive augmentation solutions expanding?

Cognitive augmentation is expected to register a 27.80% CAGR as brain-computer interfaces move from research to clinical practice.

Page last updated on: