Change Management Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

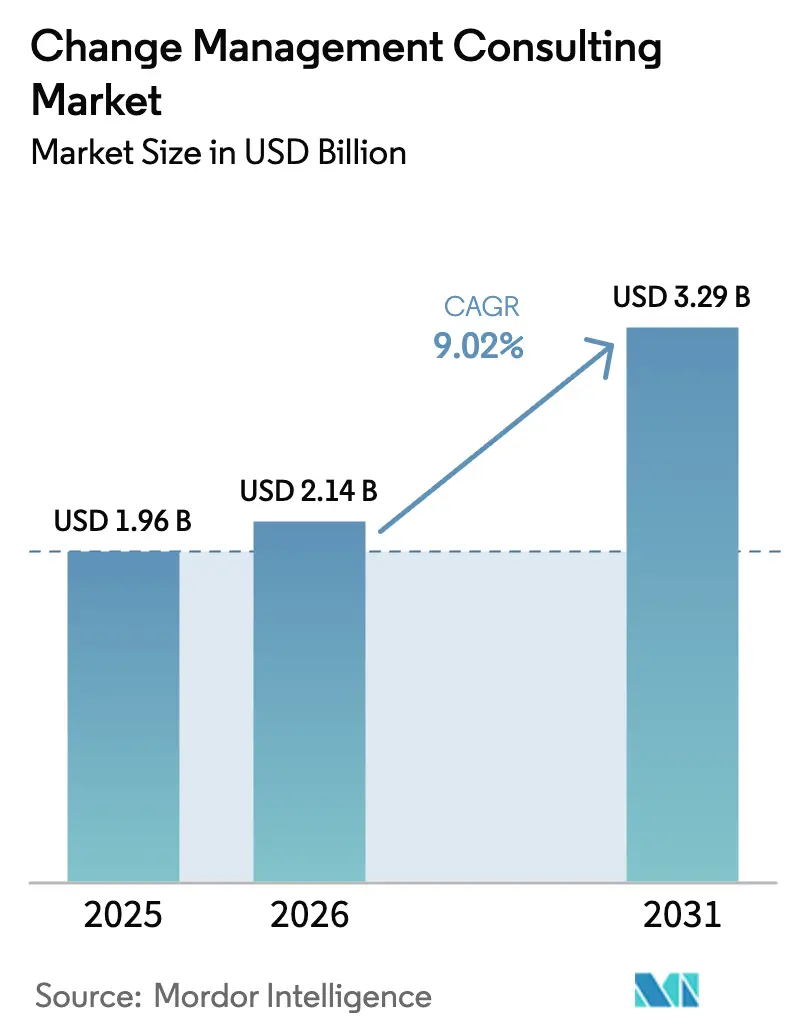

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.29 Billion |

| Growth Rate (2026 - 2031) | 9.02% CAGR |

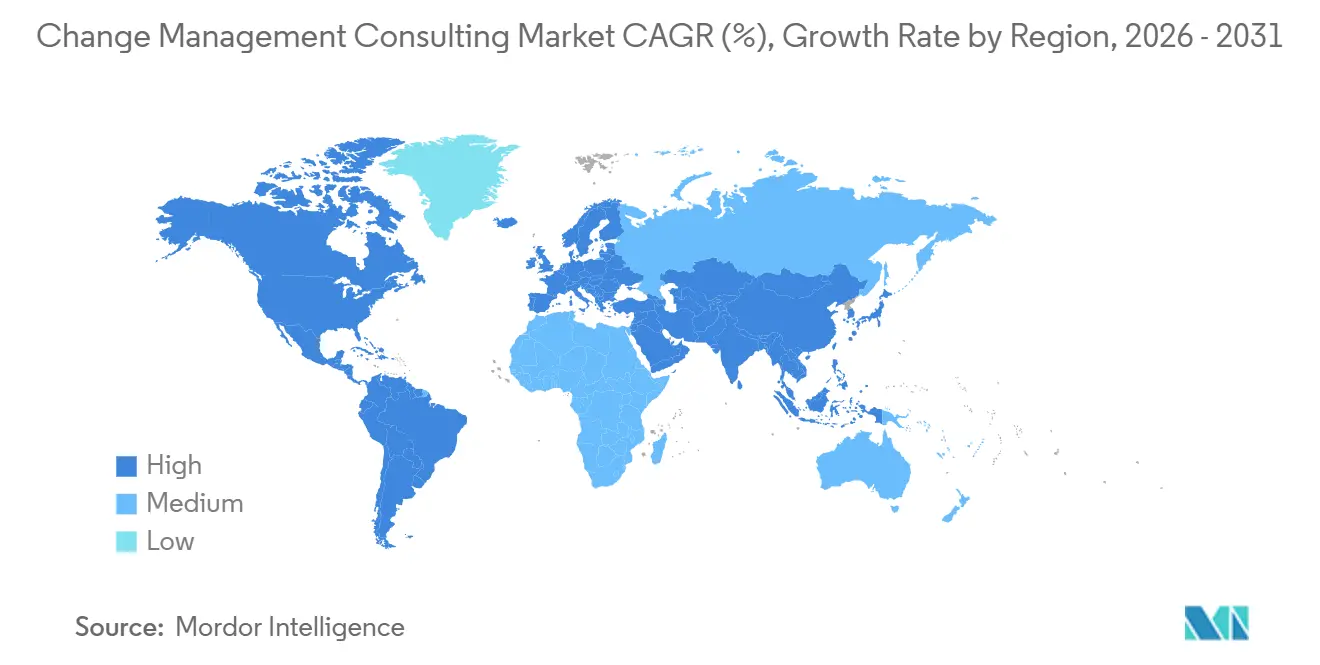

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Change Management Consulting Market Analysis by Mordor Intelligence

The Change Management Consulting Market size is expected to grow from USD 1.96 billion in 2025 to USD 2.14 billion in 2026 and is forecast to reach USD 3.29 billion by 2031 at 9.02% CAGR over 2026-2031.

Fueled by always-on transformation agendas, the change management consulting market is shifting from episodic projects toward continuous adaptation programs that blend artificial intelligence, environmental mandates, and distributed work architectures. Executives now push consultants to deliver clear value, leading to rapid uptake of real-time analytics that link behavioral shifts with financial outcomes. Hybrid work, ESG compliance, and accelerated digitalization among small enterprises are converging, which compresses timelines and raises the complexity of engagements. Competitive intensity is rising as accounting majors, strategy houses, and technology vendors all vie for share, while region-specific data laws and talent shortages create execution risks.

Key Report Takeaways

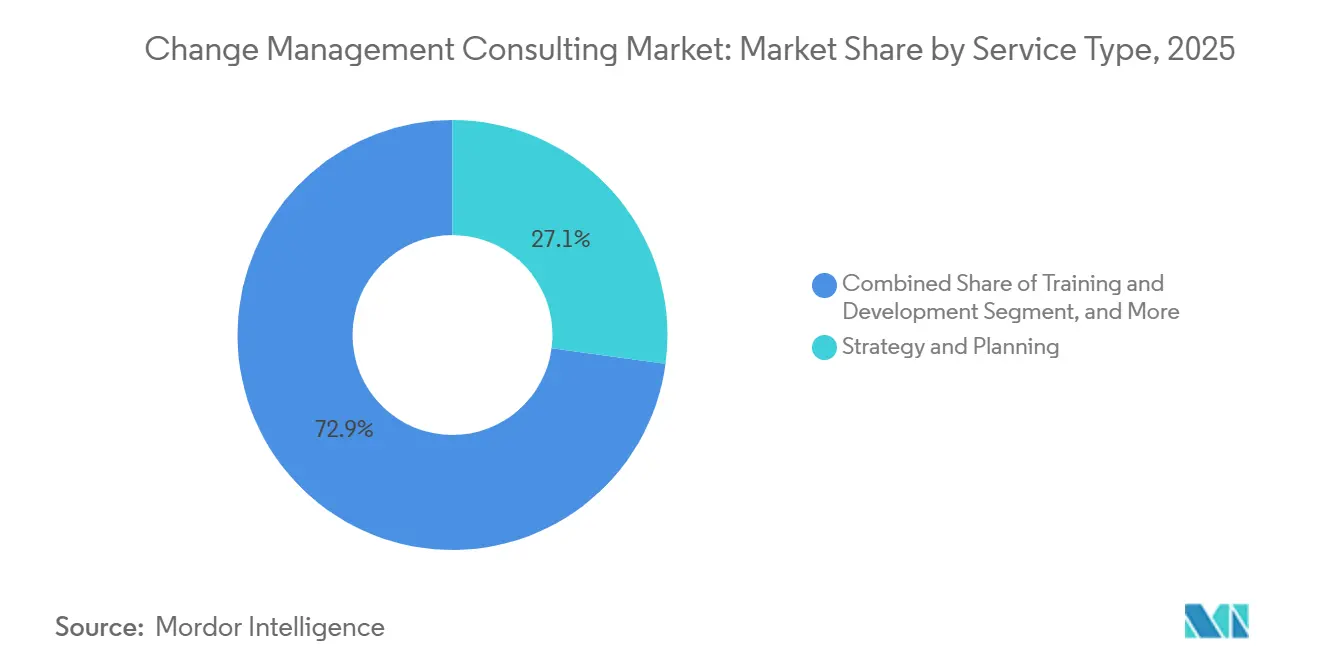

- By service type, the strategy and planning services held 27.13% of the change management consulting market share in 2025, whereas change analytics and measurement is advancing at a 10.43% CAGR through 2031.

- By organization size, large enterprises accounted for 60.86% of the change management consulting market share in 2025, yet small and medium enterprises are expanding at a 9.32% CAGR.

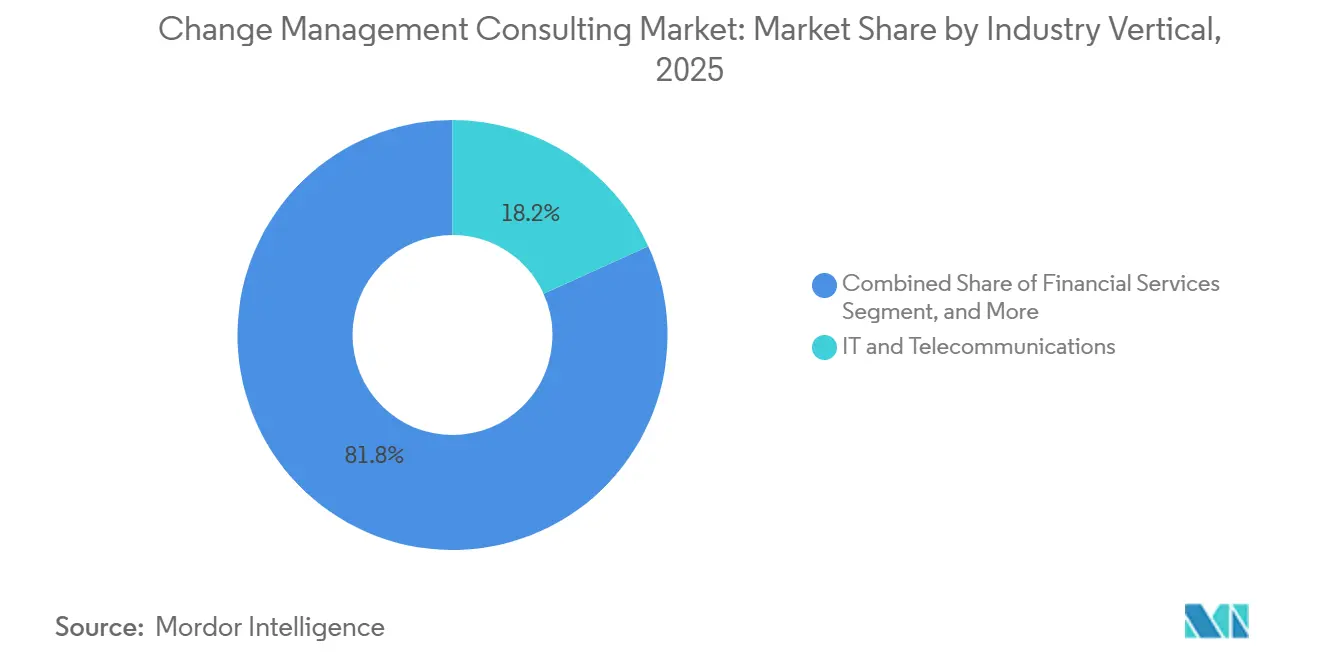

- By industry vertical, IT and telecommunications accounted for 18.23% of the change management consulting, while retail and e-commerce leads vertical growth at a 10.71% CAGR, overtaking the financial services segment in speed, although finance remains the largest revenue contributor.

- By consulting delivery mode, remote, hybrid consulting captured 44.21% of revenue in 2025, whereas remote/virtual consulting is growing at a 9.68% CAGR, while on-site delivery is slowing as clients prioritize cost agility.

- By geography, North America contributed 38.43% of global demand in 2025, while Asia-Pacific is the fastest-growing region at a 10.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Change Management Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Change Analytics Enhancing ROI Visibility | +1.8% | Global, early uptake in North America and Western Europe | Medium term (2-4 years) |

| Post-Pandemic Hybrid Work Models Requiring Cultural Shift | +1.5% | Global, pronounced in major urban centers | Short term (≤ 2 years) |

| Rise of ESG-Driven Organizational Change | +1.4% | Europe leading, expanding worldwide | Medium term (2-4 years) |

| Increasing Pace of Digital Transformation in SMEs | +1.3% | Asia-Pacific core, spill-over globally | Long term (≥ 4 years) |

| Workforce Transformation and Talent Management | +1.2% | Manufacturing-heavy regions | Medium term (2-4 years) |

| Widespread Adoption of New Technologies | +1.0% | Global technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Change Analytics Enhancing ROI Visibility

Enterprises now deploy machine-learning models that predict change readiness, map resistance patterns, and quantify financial impact with precision impossible under manual surveys. Microsoft embedded sentiment analytics into Teams in 2025, enabling leaders to correlate engagement scores with productivity shifts.[1]Microsoft, “Work Trend Index 2024,” microsoft.com JPMorgan Chase applied similar tools to its core modernization program, translating training investments into measurable error reductions. These dashboards have shifted budget approvals from faith-based to evidence-based, yet data quality and governance remain hurdles. Organizations that embed analytics into decision-making cycles see faster course corrections, while laggards treat dashboards as after-action reports. In regulated sectors, audit-ready analytics also satisfy compliance teams demanding traceable links between interventions and outcomes.

Post-Pandemic Hybrid Work Models Requiring Cultural Shift

Hybrid work brought flexibility but also meeting overload and collaboration fatigue. Microsoft reported that remote employees now sit through 42% more meeting hours than in 2019, prompting leaders to redesign synchronous routines. Consultants are crafting asynchronous workflows, decision-rights matrices, and culturally tuned rituals to balance autonomy with alignment. The International Labour Organization released hybrid-work guidelines in 2024 that stress equitable access to career development, pushing firms to hard-wire inclusion metrics into performance systems.[2]International Labour Organization, “Guidelines on Hybrid Work Arrangements,” ilo.org Asia-Pacific corporations face a tougher climb, as hierarchical norms clash with distributed decision making, demanding localized change playbooks. Successful adopters couple process redesign with targeted leadership coaching, avoiding resistance that stalls hybrid strategies.

Rise of ESG-Driven Organizational Change

The European Union’s Corporate Sustainability Reporting Directive took full effect in 2024, forcing roughly 50,000 firms to disclose detailed ESG metrics.[3]European Commission, “Corporate Sustainability Reporting Directive,” europa.eu Compliance alone has spawned a wave of change engagements, yet frontrunners treat ESG as a source of competitive advantage rather than a box-ticking exercise. Unilever documented that embedding sustainability targets into incentive plans across 58,000 workers accelerated carbon-reduction milestones. Consultants now integrate supply-chain redesign, capital allocation shifts, and cultural interventions into unified ESG programs. Social imperatives, such as diversity and inclusion, ride the same wave, requiring sustained behavior change rather than policy rewrites. Governance updates on board composition and executive pay further broaden the mandate, turning ESG into an enterprise-wide transformation driver.

Increasing Pace of Digital Transformation in SMEs

Cloud affordability and fintech competition push small and medium enterprises to digitize or exit. Google Cloud found that 72% of small businesses planned to lift tech spending in 2025, but only 34% had formal change processes. Government subsidies amplify the trend: India’s Digital India program reimburses cloud and cybersecurity investments, catalyzing consulting demand among resource-constrained manufacturers. Consultants respond with pre-packaged toolkits that compress timelines and cost, translating enterprise-grade methodologies into lean playbooks. Prosci launched a simplified framework in 2025 tailored to firms with change teams of one or two people. As digital merchants scale, structured change accelerates retention gains, proving that formal methods pay dividends even in the mid-market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resistance to Change Among Middle Management | -1.1% | Global, stronger in hierarchical cultures | Short term (≤ 2 years) |

| Shortage of Certified Change Practitioners in Emerging Markets | -0.9% | Africa, South America, Southeast Asia | Medium term (2-4 years) |

| Complexity of Organizational Structures | -0.6% | Global conglomerates | Long term (≥ 4 years) |

| Data Privacy Concerns in Change Analytics Tools | -0.5% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Resistance to Change Among Middle Management

Middle managers juggle day-to-day targets while implementing future-state models, often viewing transformation as a threat to authority. Siemens experienced a four-month delay in its digital-factory rollout until it guaranteed roles and launched reskilling tracks for supervisors. Role ambiguity, fear of automation, and limited visibility into long-range benefits spark covert resistance that spreads through informal networks. Consultants increasingly embed career-pathing and recognition systems to win buy-in, yet budget-constrained clients may underrate these soft costs. Without tangible incentives, even well-designed change programs stall at the execution layer. Continuous communication loops and early involvement of supervisory layers mitigate pushback but require executive resolve.

Shortage of Certified Change Practitioners in Emerging Markets

The supply of accredited consultants trails demand across Africa and South America. The Association of Change Management Professionals noted that only 8% of global certification applications originated from these regions in 2025. Talent scarcity inflates fees and elongates project timelines, placing structured transformation out of reach for local firms. Banking regulators in Nigeria linked several digital-banking setbacks to limited change capability within project teams.[4]Central Bank of Nigeria, “Financial Stability Report 2024,” cbn.gov.ng Tata Consultancy Services set up a training hub in 2025 to create 5,000 certified practitioners by 2027, yet similar initiatives remain rare. Without broader capacity-building, organizations turn to generalist advisors, raising execution risk and diluting outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Analytics Reshaping Traditional Advisory

Strategy and Planning services held 27.13% of market share in 2025, reflecting their foundational role in defining transformation roadmaps, securing executive sponsorship, and establishing governance frameworks that guide implementation. However, Change Analytics and Measurement is expanding at 10.43% CAGR as organizations demand quantifiable evidence that change investments deliver promised returns, shifting budget allocation from upfront planning toward continuous monitoring and optimization. Training and Development remains essential for building employee capabilities, particularly in digital transformation initiatives where skill gaps represent the primary adoption barrier, while Communication and Engagement services are evolving from one-way messaging to interactive platforms that solicit feedback and enable peer-to-peer learning.

Process Implementation services are growing as organizations recognize that sustainable change requires embedding new behaviors into workflows, performance metrics, and technology systems rather than relying on awareness campaigns alone. Digital Adoption Platforms Integration emerged as a distinct service category in 2024-2025, as vendors like WalkMe and Pendo partnered with consulting firms to combine in-application guidance with change management methodologies. Change Sustainability Support addresses the reality that most transformations regress within 18 months without ongoing reinforcement, creating demand for multi-year engagements that extend beyond initial implementation. The shift toward analytics-driven services reflects a broader maturation of the market, as buyers move from purchasing change management as a compliance checkbox to viewing it as a strategic capability that drives competitive advantage.

By Organization Size: SMEs Closing the Adoption Gap

Large enterprises commanded 60.86% of market share in 2025, driven by complex transformation portfolios that span multiple geographies, business units, and technology platforms. These organizations typically maintain internal change management centers of excellence supplemented by external consultants for specialized expertise or surge capacity during peak implementation periods. However, small and medium enterprises are growing at 9.32% CAGR as cloud-based tools and virtual delivery models reduce the cost and complexity barriers that previously limited access to professional change management services. The COVID-19 pandemic accelerated this trend by normalizing remote consulting and demonstrating that effective change management does not require on-site presence for every engagement.

SME adoption is particularly strong in retail and e-commerce, where digital transformation is existential rather than optional, and in manufacturing, where automation and Industry 4.0 initiatives require workforce reskilling at scale. Shopify's 2025 Commerce Trends Report found that SME merchants using change management support during platform migrations experienced 47% lower cart abandonment rates and 28% higher customer retention compared to those implementing technology changes without structured change processes. The challenge for consultants serving SMEs is delivering value within compressed budgets and timelines, requiring standardized methodologies and leveraging technology to automate routine tasks like stakeholder mapping and communication planning. Large enterprises continue to drive absolute revenue growth, but SMEs represent the market's future as digital transformation becomes universal rather than the domain of industry leaders.

By Industry Vertical: Retail Leading Digital-Driven Transformation

In 2025, the IT and telecommunications sector commanded the largest market share at 18.23%. This dominance was fueled by ongoing technology refresh cycles, cloud migration efforts, and the launch of digital products, all of which necessitated workforce adaptability and strategic customer communication. The sector grapples with distinct change management challenges, including the adoption of DevOps, agile transformations, and a pivotal shift from product-centric to platform business models. These shifts not only redefine organizational structures but also their incentive systems. Highlighting the scale of these changes, Ericsson's 2024 annual report revealed that its move to a cloud-native 5G infrastructure mandated change management for 95,000 employees across 180 countries. This extensive effort encompassed role redesigns, skill certification programs, and a cultural pivot in software development practices. Moreover, technology firms are at the forefront of change management, often piloting AI-driven analytics and digital adoption platforms long before they become mainstream.

Retail and e-commerce, growing at a robust 10.71% CAGR, leads all sectors. Companies in this space are grappling with omnichannel integration, inventory optimization, and personalization engines. These advancements necessitate upskilling employees and familiarizing them with new workflows. A significant challenge arises from engaging the frontline workforce, where high turnover and part-time roles complicate training and communication. Walmart's 2024 annual report underscored the magnitude of these challenges, detailing the company's store modernization program. This initiative spanned 10,500 locations and impacted 1.6 million associates, necessitating role redesigns, technology training, and a cultural shift in customer service expectations. Meanwhile, the financial services sector remains buoyed by regulatory compliance, digital banking transformations, and core system modernizations. These initiatives touch every customer interaction. In parallel, healthcare and life sciences are adopting electronic health records, value-based care models, and telehealth platforms, fundamentally reshaping clinical workflows.

By Consulting Delivery Mode: Hybrid Models Balancing Flexibility and Presence

In 2025, hybrid consulting delivery dominated the landscape, capturing 44.21% of the market share. Organizations are increasingly drawn to this model, which adeptly marries the cost benefits and geographic flexibility of remote engagements with the depth of relationships and cultural nuances that on-site interactions offer. Typically, this approach utilizes remote delivery for routine tasks, such as training, monitoring progress, and communicating with stakeholders, while reserving on-site presence for pivotal moments. These include executive workshops, activating change networks, and providing go-live support. According to Deloitte's 2025 Consulting Trends Report, hybrid engagements outperformed both remote and on-site models, boasting 18% higher client satisfaction scores. This success is attributed to optimized resource allocation and the flexibility to scale practitioner involvement based on the specific needs of the transformation phase.

Remote and virtual consulting is witnessing a robust expansion, growing at a 9.68% CAGR, the fastest among delivery modes. This surge is largely due to the maturation of technology platforms and a growing organizational comfort with distributed collaboration for intricate advisory services. The post-pandemic landscape has seen a normalization of tools like video collaboration, digital whiteboards, and asynchronous communication. This shift has dispelled the long-held belief that change management necessitates a physical presence for relationship-building and adoption. PwC's 2025 analysis highlighted a significant milestone: remote change management engagements matched the effectiveness of their on-site counterparts for the first time. This parity was largely driven by advancements in virtual facilitation techniques and the emergence of specialized platforms tailored for distributed transformation tasks. The pivot towards remote delivery not only broadens consulting firms' access to global talent but also allows them to cater to clients in secondary markets, where local expertise in change management might be scarce. However, this shift also heightens competition, as the diminishing of geographic barriers becomes evident.

Geography Analysis

North America generated 38.43% of global revenue in 2025, underpinned by deep practitioner ecosystems and enterprise spending across finance, technology, and healthcare. U.S. multinationals embed change gating into program management offices, ensuring steady baseline demand. Growth is moderating as large buyers insource repeatable activities and automate analytics, yet advisory needs persist for frontier topics such as generative AI governance. Canada leans on change expertise for public service digitization and resource-sector decarbonization, keeping the regional pipeline stable. Economic headwinds could delay discretionary initiatives, but regulatory requirements in healthcare and finance provide a counterweight.

Asia-Pacific is the fastest-growing territory at a 10.22% CAGR. China’s industrial upgrading pushes state-owned conglomerates to adopt lean, software-defined production lines, which in turn requires large-scale workforce reskilling. India’s IT services champions integrate change management into global delivery, while domestic enterprises embrace formal frameworks to win export contracts. Southeast Asian economies turn to consultants as governments digitize tax, licensing, and welfare systems, increasing the sophistication of local demand. Japan and South Korea pose cultural challenges for Western methodologies, prompting localization of stakeholder engagement models that respect consensus decision making. Across the region, stringent data localization laws shape tool choices, favoring providers with region-specific cloud offerings.

Europe shows medium-paced growth, driven by ESG legislation, demographic shifts, and post-pandemic productivity drives. Germany’s Industrie 4.0 accelerates factory transformations, and the United Kingdom’s financial houses overhaul operations to navigate post-Brexit regulatory divergence. Southern Europe sees public-sector modernizations funded by NextGenerationEU grants, broadening the addressable market. GDPR compliance complicates analytics rollouts, but firms that offer privacy-by-design solutions gain a competitive edge. South America, led by Brazil, registers nascent yet accelerating uptake, especially in banking, energy, and retail. Currency volatility and budget cycles create project pacing risks, yet digital payments and e-commerce expansion spur necessary overhauls. The Middle East, propelled by national diversification programs, invests in culture change to support private-sector competitiveness. Africa remains small but promising, as mobile banking and public-sector digitization open greenfield opportunities; nonetheless, practitioner scarcity and funding constraints temper near-term prospects.

Competitive Landscape

The change management consulting market exhibits a moderate fragmentation, with the top ten providers collectively accounting for approximately 45-50% of the revenue. The Big Four accounting networks adeptly cross-sell change services, leveraging their established audit relationships. This strategy not only capitalizes on the trust they've built with clients but also underscores their compliance credentials. Meanwhile, strategy houses, armed with board-level access and in-depth industry research, position change management as a pivotal component of strategy execution. This positioning often secures them projects that intertwine enterprise-wide redesigns with essential cultural realignments. On another front, technology service giants seamlessly weave change enablement into their digital transformation portfolios. This integration allows them to present comprehensive solutions, covering everything from software selection and implementation to ensuring user adoption. Specialized firms, like Prosci, carve out a niche by monetizing training and certification, thereby cultivating ecosystems of in-house practitioners who champion and propagate their methodologies.

In this competitive landscape, strategies are increasingly centered around toolset differentiation. Providers are channeling investments into advanced technologies, harnessing AI-driven sentiment analytics, predictive adoption models, and digital adoption platforms to ensure tangible outcomes. The trend of acquisitions is evident, with a keen focus on boutique specialists boasting ESG expertise or proprietary software. This is underscored by a flurry of deals announced during 2024-2025. New entrants, particularly software vendors, are innovatively bundling advisory services to expedite license renewals, effectively blurring the traditional boundaries between consultancy and product offerings. The challenge of talent scarcity looms large, prompting firms to forge partnerships with universities and establish internal academies, all in a bid to cultivate and expand their pool of practitioners.

Regional boutique firms carve out their niche by leveraging deep cultural insights and vertical specializations. Often, they find themselves subcontracted within broader global frameworks. However, as the market evolves, price pressures mount, especially for services perceived as commoditized. This has led many incumbents to pivot towards value-based pricing models, directly linked to adoption KPIs. Looking ahead, while moderate consolidation seems probable, the enduring significance of relationship-centric purchasing and the influence of local regulations ensure that there's still ample space for niche players to thrive.

Change Management Consulting Industry Leaders

Deloitte Touche Tohmatsu Limited

International Business Machines Corporation

PricewaterhouseCoopers International Limited

Ernst and Young Global Limited

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Accenture expanded its change practice by acquiring an ESG-focused European advisory that added 450 practitioners and proprietary frameworks.

- December 2024: Deloitte launched an AI-driven analytics platform that predicts resistance patterns and transformation outcomes with 78% accuracy.

- November 2024: PwC formed an alliance with Microsoft to embed change services into Microsoft 365 and Dynamics 365 deployments.

- October 2024: Prosci partnered with five Indian universities to certify 5,000 practitioners by 2027, easing South Asian talent shortages.

Global Change Management Consulting Market Report Scope

The Change Management Consulting Market Report is Segmented by Service Type (Strategy and Planning, Training and Development, Process Implementation, Communication and Engagement, Change Sustainability Support, Digital Adoption Platforms Integration, Change Analytics and Measurement), Organization Size (Small and Medium Enterprises, Large Enterprises), Industry Vertical (IT and Telecommunications, Healthcare and Life Sciences, Manufacturing, Financial Services, Retail and E-commerce, Government and Public Sector, Energy and Utilities, Education, Transportation and Logistics), Consulting Delivery Mode (On-site Consulting, Remote/Virtual Consulting, Hybrid Consulting), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Strategy and Planning |

| Training and Development |

| Process Implementation |

| Communication and Engagement |

| Change Sustainability Support |

| Digital Adoption Platforms Integration |

| Change Analytics and Measurement |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Manufacturing |

| Financial Services |

| Retail and E-commerce |

| Government and Public Sector |

| Energy and Utilities |

| Education |

| Transportation and Logistics |

| On-site Consulting |

| Remote/Virtual Consulting |

| Hybrid Consulting |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Service Type | Strategy and Planning | |

| Training and Development | ||

| Process Implementation | ||

| Communication and Engagement | ||

| Change Sustainability Support | ||

| Digital Adoption Platforms Integration | ||

| Change Analytics and Measurement | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | IT and Telecommunications | |

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Financial Services | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| Energy and Utilities | ||

| Education | ||

| Transportation and Logistics | ||

| By Consulting Delivery Mode | On-site Consulting | |

| Remote/Virtual Consulting | ||

| Hybrid Consulting | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the change management consulting market by 2031?

It is forecast to reach USD 3.29 billion by 2031.

How fast is the North American market growing?

North America is expected to expand at a slightly lower rate than the global 9.02% CAGR due to higher maturity but remains the largest regional contributor.

Which service category is growing the fastest?

Change Analytics and Measurement is growing at a 10.43% CAGR as clients demand real-time ROI tracking.

Why are hybrid work models driving consulting demand?

Hybrid arrangements require cultural realignment, meeting redesign, and inclusive performance systems that most firms lack internally.

What is the biggest barrier to successful transformation?

Resistance from middle management, driven by role uncertainty and competing priorities, remains the leading execution challenge.

How are small and medium enterprises accessing change expertise?

Providers offer modular toolkits, virtual coaching, and subscription pricing that lower cost thresholds and support 9.32% CAGR adoption among SMEs.

Page last updated on: