Cerebral Somatic Oximeters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

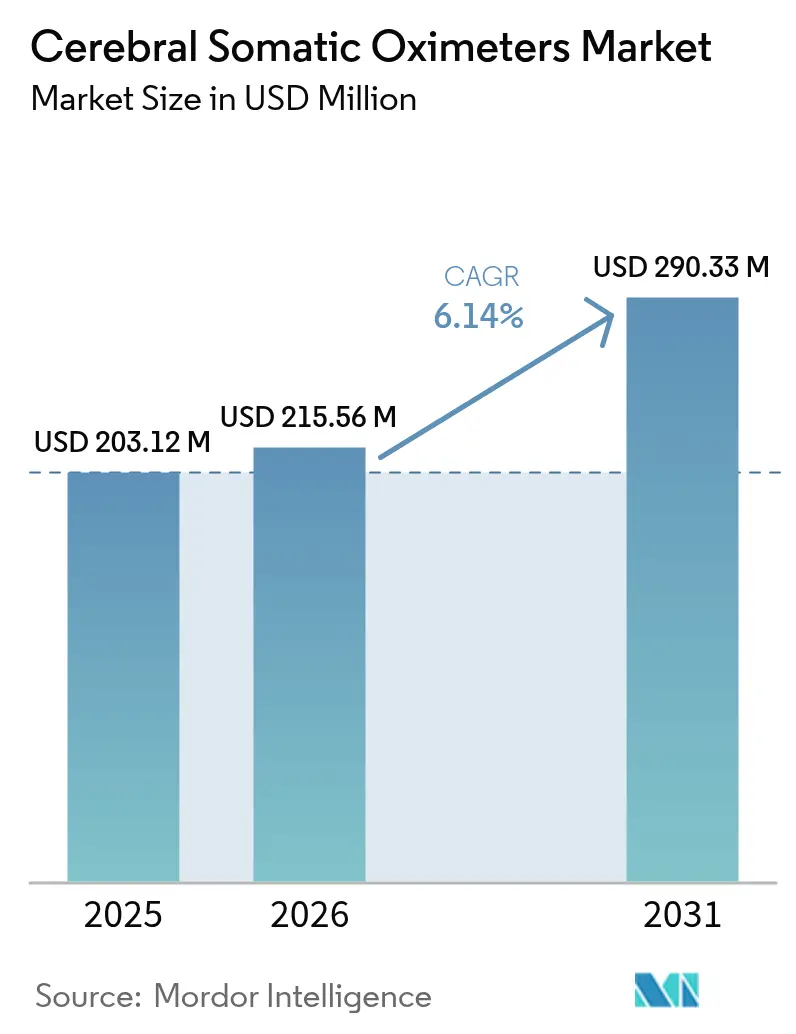

| Market Size (2026) | USD 215.56 Million |

| Market Size (2031) | USD 290.33 Million |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

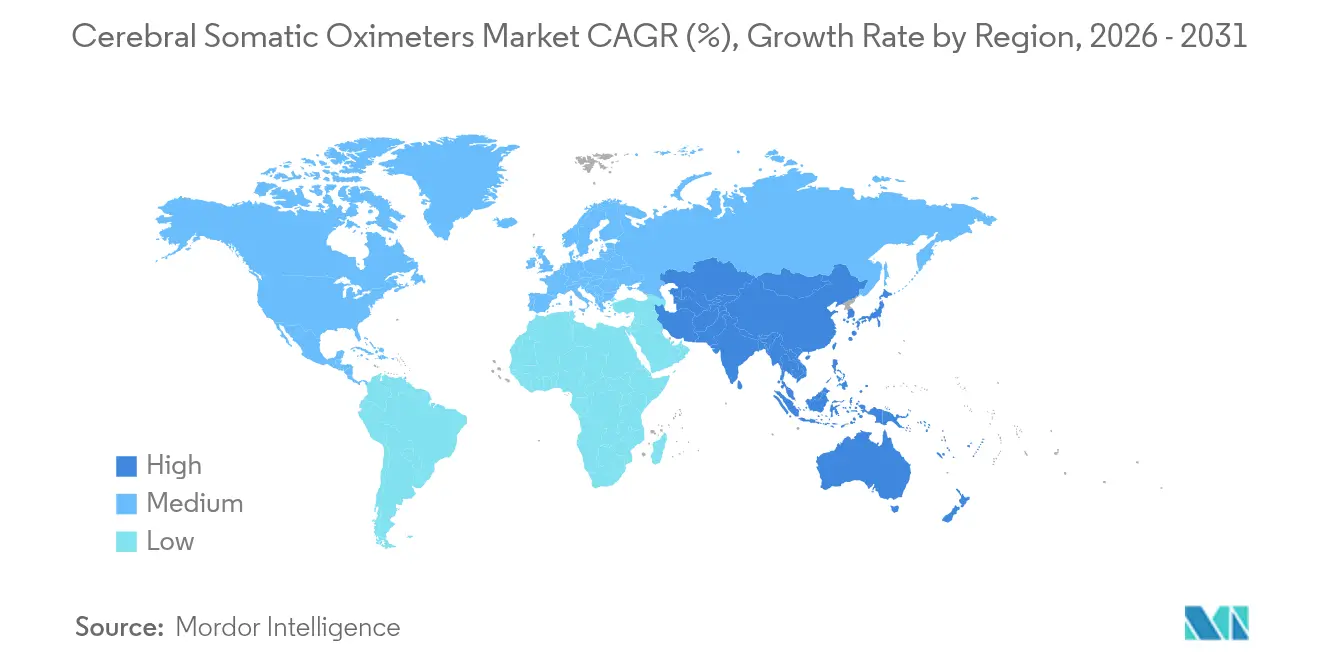

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cerebral Somatic Oximeters Market Analysis by Mordor Intelligence

The cerebral somatic oximeters market size was valued at USD 203.12 million in 2025 and estimated to grow from USD 215.56 million in 2026 to reach USD 290.33 million by 2031, at a CAGR of 6.14% during the forecast period (2026-2031). This expansion stems from converging forces: aging populations that increase surgical demand, rising global procedure volumes in cardiac, vascular, and neurological specialties, and sustained breakthroughs in near-infrared spectroscopy that enable real-time monitoring of brain and somatic tissue oxygenation. Consolidation among device makers deepens technology portfolios and broadens their geographic reach, while favorable reimbursement in high-income nations shortens the payback periods for hospitals investing in advanced monitoring. At the same time, emerging markets are increasing capital spending on perioperative infrastructure, thereby reinforcing long-term volume growth. Ultimately, multivariable algorithms that integrate cerebral oximetry with hemodynamic and electrophysiological signals enhance decision support and strengthen the clinical value proposition of integrated monitoring platforms.

Key Report Takeaways

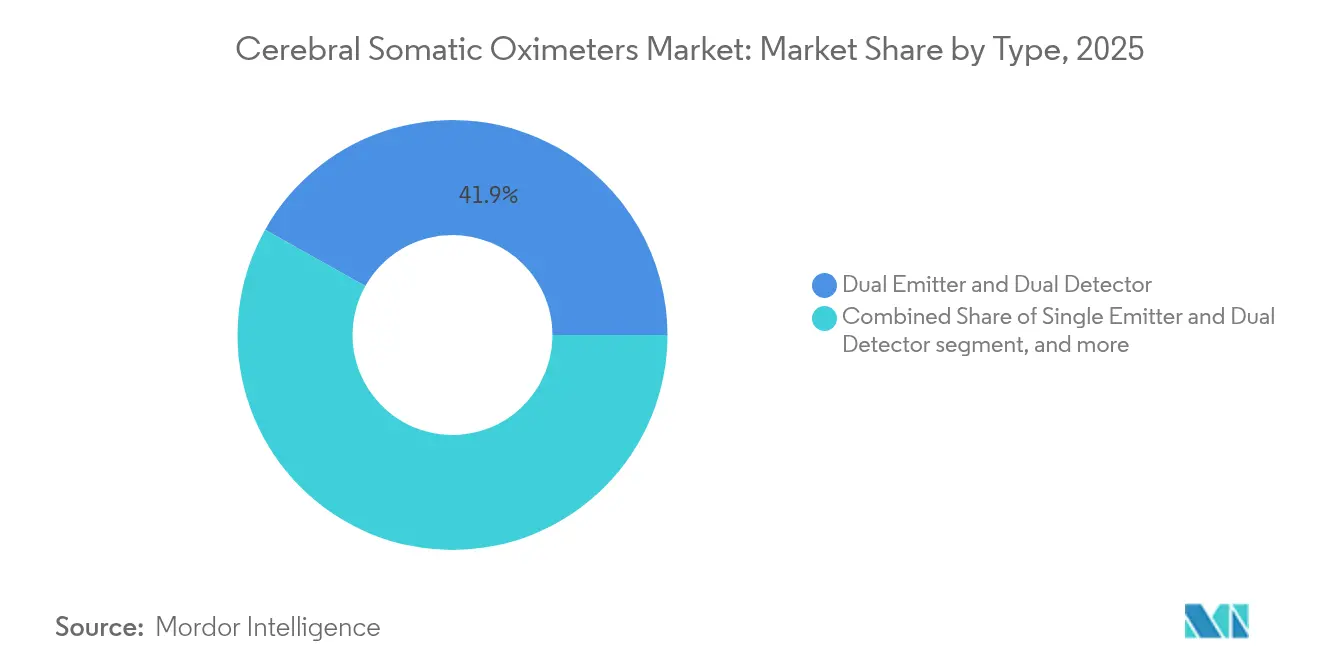

- By type, dual emitter and dual detector configurations held 41.85% of the cerebral somatic oximeters market share in 2025, while other emerging types posted the fastest 8.02% CAGR from 2025 to 2031.

- By application, cardiac surgery accounted for 44.90% of the revenue in 2025, while neurosurgery and traumatic brain injury applications grew at an 7.63% CAGR through 2031.

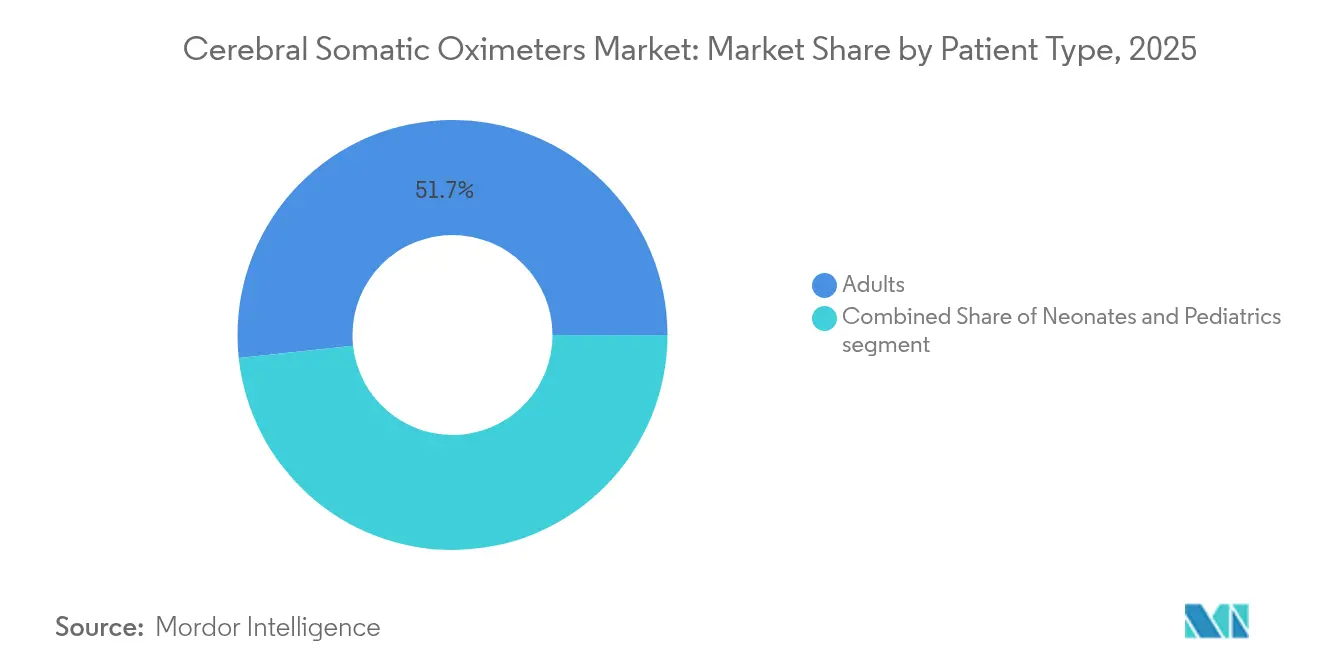

- By patient type, adult procedures accounted for 51.70% of 2025 demand, whereas neonatal monitoring registers the highest 8.19% CAGR thanks to purpose-built sensors for premature infants.

- By end user, hospitals and clinics captured 54.85% of the revenue in 2025, while ambulatory surgical centers are projected to exhibit a robust 8.88% CAGR to 2031.

- By geography, North America led with 41.10% revenue in 2025, but the Asia-Pacific region recorded the strongest 7.10% CAGR, driven by high cardiovascular disease prevalence and rapid infrastructure expansion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cerebral Somatic Oximeters Market Trends and Insights

Drivers Impact Analysis*

| Driver | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of cardiovascular and neurological disorders | +1.2% | Global, stronger in North America and Europe | Long term (≥ 4 years) |

| Increasing adoption of advanced perioperative monitoring standards | +1.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising demand for minimally invasive and point-of-care devices | +1.1% | Global, led by developed markets | Medium term (2-4 years) |

| Expanding surgical procedure volumes in emerging economies | +0.9% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Technological advancements in near-infrared spectroscopy sensors | +0.8% | Global, with innovation hubs in U.S., EU, Japan | Short term (≤ 2 years) |

| Favorable government initiatives and reimbursement policies | +0.5% | North America, selective EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Cardiovascular and Neurological Disorders

Cardiovascular disease remains the top global killer, driving consistent demand for perioperative brain oxygenation monitoring during cardiac bypass and valve repair. Stroke and traumatic brain injury add further volume, with the CDC reporting 2.8 million brain-injury cases and 795,000 strokes annually in the United States[1]Centers for Disease Control and Prevention, “Traumatic Brain Injury & Stroke Statistics,” cdc.gov. Elderly patients often present multiple comorbidities that heighten the risk of cerebral hypoxia, making real-time monitoring indispensable in complex surgeries. Advances in dual-wavelength NIRS now provide depth-resolved quantitative data that reduce extracranial contamination. As health systems aim to curb postoperative cognitive dysfunction, clinical guidelines increasingly position cerebral oximetry as standard of care.

Increasing Adoption of Advanced Perioperative Monitoring Standards

Clinical societies embed brain oximetry in updated perioperative checklists, citing evidence that early detection of cerebral desaturation cuts complication rates. The 2024 AHA/ACC guidelines endorse comprehensive neuromonitoring for high-risk cardiac cases[2]American Heart Association, “2024 AHA/ACC Guideline for the Management of Cardiac Patients,” ahajournals.org. ELSO recommends NIRS for ECMO management, while the I-PROTECT consensus supplies reference ranges that simplify bedside interpretation. The FDA’s Breakthrough Devices and Safety & Performance Based Pathway accelerate clearances for innovative sensors, shrinking time-to-market[3]U.S. Food & Drug Administration, “Breakthrough Devices Program,” fda.gov. Hospitals in Scandinavia pioneer multimodal neuromonitoring bundles that pair cerebral oximetry with BIS and processed EEG, setting replicable global templates.

Rising Demand for Minimally Invasive and Point-of-Care Devices

Outpatient procedural shifts propel requirements for portable monitors that match in-hospital accuracy. Ambulatory centers prefer compact consoles connected to wireless, adhesive sensors that shorten turnover times. Wearable fore-head bands now stream brain oxygen data to cloud dashboards, allowing anesthetists to supervise multiple rooms. Point-of-care uses extend to emergency departments, where rapid cerebral saturation readings inform resuscitation and intracranial pressure control. Contactless optical architectures in development aim to eliminate disposable costs and infection risk, paving entry into home-care stroke rehabilitation programs.

Expanding Surgical Procedure Volumes in Emerging Economies

Asia-Pacific overtakes Europe in total cardiovascular surgeries as China, India, and Japan finance hospital expansions and population screening. Governments allocate budgets for perioperative quality metrics, and local champions introduce value-priced oximeters configured for high-volume environments. Multinational suppliers localize consumables to meet procurement thresholds, leveraging public-private partnerships that bundle devices with digital training. Rising health insurance coverage in these nations further cushions capital hurdles, sustaining uptake of premium brain monitoring systems.

Restraints Impact Analysis*

| Restraint | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and consumable costs of devices | –1.4% | Global, more acute in emerging markets | Medium term (2-4 years) |

| Limited clinical evidence linking monitoring to improved outcomes | –0.8% | Global, especially cost-sensitive regions | Long term (≥ 4 years) |

| Reimbursement gaps in low- and middle-income countries | –0.6% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Competitive pressure from alternative neuro-monitoring modalities | –0.4% | Global, highest in tertiary centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs of Devices

Advanced cerebral oximetry consoles retail between USD 15,000 and USD 50,000, a sizeable investment for secondary hospitals. Single-use sensors add USD 25-75 per case, pressuring budgets in high-volume centers. Purchasing committees often favor multipurpose imaging gear over specialized monitors, delaying adoption even when clinical teams advocate for brain saturation tracking. Emerging markets feel cost barriers most acutely, although tiered sensor portfolios and re-use-validated probes begin to lower run-time expenses.

Limited Clinical Evidence Linking Monitoring to Improved Outcomes

While observational studies suggest fewer neurological events when cerebral oximetry guides perfusion, large randomized trials remain scarce. Meta-analyses report mixed findings on reduced stroke or mortality, prompting payers to request stronger proof before broad reimbursement. Device makers co-fund multicenter registries to capture real-world outcome data, and societies such as STS collaborate on standardized endpoints. As forthcoming trials publish, evidence gaps may narrow, but current uncertainty tempers procurement in price-sensitive health systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dual Emitter Configurations Lead Technology Evolution

Dual emitter and dual detector systems generated the largest revenue slice in 2025, reflecting 41.85% of the cerebral somatic oximeters market. These platforms optimize signal-to-noise ratio, granting surgeons stable readings despite patient motion and electrocautery interference. In value terms, the cerebral somatic oximeters market size for dual emitter technology is forecast to grow at 5.92% CAGR to 2031, mirroring steady capital refresh cycles in tertiary centers. Other emerging architectures, including wireless and wearable variants, post an 8.02% CAGR as battery efficiency and Bluetooth privacy protocols mature.

Complementary trends include integrated multimodal solutions that merge NIRS with EEG and electromyography, as demonstrated by Artinis Medical Systems’ acquisition of TMSi. Time-domain NIRS prototypes progress toward commercial launch, offering depth-resolved data that mitigate extracranial contamination. FDA Breakthrough designations shorten market entry for novel laser-diode arrays, and intellectual property clustering intensifies around optical coupling algorithms. Collectively, such innovations expand addressable use cases beyond the operating room into neuro-rehab and sports physiology, broadening the cerebral somatic oximeters market.

By Application: Cardiac Surgery Dominance Faces Neurological Challenge

Cardiac surgery retained 44.90% revenue in 2025, underpinned by mandated brain perfusion monitoring during cardiopulmonary bypass. At segment level, the cerebral somatic oximeters market size for cardiac surgery is projected to reach USD 123.36 million by 2031, with a steady 5.18% CAGR as valve repair and aortic procedures climb in older populations. Neuro-surgery and traumatic brain injury applications accelerate at 7.63% CAGR as ICUs adopt cerebral oximetry to guide ventilator and vasoactive management.

Beyond these core indications, vascular interventions, pediatric cardiac arrest resuscitation, and ECMO circuits integrate brain saturation targets into perfusion algorithms. Guideline endorsements from ELSO and the AHA bolster clinical confidence, while software updates overlay autoregulation indices on live trend screens. As outcome registries collect comparative data, neuro-focused growth may narrow the gap with cardiac usage, reshaping application mix by the decade’s end.

By Patient Type: Adult Procedures Drive Volume While Neonatal Innovation Accelerates

Adult cases composed 51.70% of global procedures in 2025, anchoring baseline demand. Revenue concentration aligns with high cardiac and vascular caseloads in seniors, a cohort prone to cognitive deficits from cerebral hypoxia. The cerebral somatic oximeters market size for adult monitoring is estimated to expand 5.62% CAGR on procedure growth and console replacement.

Neonatal use, while smaller today, charts the fastest 8.19% CAGR on the back of purpose-built probes like OxyPrem’s NOAH sensor. Prematurity affects 10% of global births, and clinicians now track brain oxygen continuously to prevent intraventricular hemorrhage. Pediatric algorithms tailored to small blood volume and higher heart rates strengthen accuracy, reinforcing adoption. Mid-sized manufacturers partner with children’s hospitals to refine form factors and build reference databases, supporting the long-run rise of neonatal revenue.

By End User: Hospital Dominance Challenged by Ambulatory Surge

Hospitals and clinics captured 54.85% of 2025 sales, leveraging established infrastructure and staff proficiency. These sites absorb premium multi-parameter consoles that network with electronic health records. The cerebral somatic oximeters market size for hospital settings is projected to rise 5.33% CAGR to 2031, with growth driven by surgical complexity and quality-metric reimbursement.

Ambulatory surgical centers register a 8.88% CAGR as payers steer low-risk procedures out of hospital walls. Portable all-in-one monitors suit ASC needs for quick turnover, small footprint, and simplified consumables. Some vendors offer subscription bundles where capital cost folds into per-case sensor pricing, easing ASC cash flow constraints. Emergency medical services and home telemonitoring form niche but rising demand nodes as health systems pursue decentralized care pathways.

Geography Analysis

North America accounted for 41.10% of the revenue in 2025, supported by CMS add-on payments and FDA pathways that expedite the approval of novel devices. High procedural volumes in cardiac and vascular surgery sustain regular sensor consumption, and large integrated delivery networks adopt enterprise-wide contracts that bundle disposables at scale. Clinician familiarity with cerebral oximetry, combined with malpractice‐risk mitigation, underpins continued purchasing.

Europe ranks second in value, with mature healthcare systems emphasizing patient safety. CE-marked multimodal platforms dominate university hospitals, and public procurement often rewards suppliers that present cost-effectiveness data tied to shortened ICU stays. Nordic countries set leading practice, using cerebral saturation targets during anesthesia induction and in post-operative step-down units. Pan-EU research consortia, such as EuroNIRS, develop uniform outcome metrics that guide further reimbursement alignment.

Asia-Pacific delivers the fastest 7.10% CAGR, propelled by China’s hospital capacity expansion and Japan’s optical sensor R&D leadership. Regional makers localize production to qualify for tender programs, and private cardiac specialty chains in India adopt brain oximetry to differentiate service quality. Government insurance schemes across ASEAN broaden coverage for complex surgeries, indirectly boosting monitor demand. In parallel, joint ventures with domestic electronics firms accelerate the commercialization of wireless sensors, bringing cost-optimized units to mid-tier hospitals. South America and the Middle East & Africa show incremental uptake as training programs disseminate perioperative neuromonitoring standards.

Regulatory Landscape

Cerebral somatic oximeters are regulated as moderate-risk devices in major markets, with the United States using FDA Class II controls for cerebral/tissue oxygenation monitoring (including product codes used for cerebral oximetry and tissue saturation oximetry clearances). In practice, most market entry activity continues to proceed through the FDA 510(k) pathway, and manufacturers typically align testing and documentation to FDA-recognized consensus standards for electrical safety and performance.

In Europe, classification under Regulation (EU) 2017/745 (MDR) is driven by Annex VIII rules for active diagnostic and monitoring devices (commonly assessed under Rule 10). Risk-based classification can move products into Class IIa or IIb depending on intended use and clinical context. On the standards side, ISO 80601-2-85:2021 remains the key device-specific benchmark for cerebral tissue oximeter equipment. April 2026 also brought an update to ISO 80601-2-61:2026 for pulse oximeter equipment, reinforcing the broader compliance environment for optical oxygenation monitoring platforms used across perioperative and acute care settings.

Value Chain Analysis

The value chain begins with specialized optical and electronics inputs, including NIR light sources, photodetectors, analog front ends, and adhesives and biocompatible materials for single-use sensors. It then shifts to device design, algorithm development, and the manufacturing of consoles and disposable probes. Standardization requirements, anchored by ISO 80601-2-85:2021 for cerebral tissue oximeter safety and essential performance, shape supplier qualification, verification testing, and quality-system documentation before products and consumables scale through hospital procurement channels.

Downstream, distribution is dominated by direct sales and group purchasing contracts into hospitals and integrated delivery networks. Recurring revenue is supported by per-case disposable sensors and service agreements. Recent regulatory wins also show how product and software updates propagate through the chain: Masimo received FDA 510(k) clearance in August 2025 to expand delta hemoglobin parameters on its O3 Regional Oximetry platform across cerebral and somatic applications and patient populations, and Casibrain (Beijing) Technology Co., Ltd. received NMPA approval in October 2025 for a non-invasive multi-channel whole-brain cerebral oxygen monitor. Together, these approvals highlight parallel routes for global suppliers and domestic entrants to reach operating rooms and ICUs through local compliance, tender readiness, training, and integration with bedside monitoring workflows.

Competitive Landscape

The market reflects moderate concentration, with Masimo, Medtronic, and Edwards Lifesciences anchoring global share positions yet leaving room for agile innovators. BD’s USD 4.2 billion purchase of Edwards’ Critical Care division and Edwards’ prior USD 100 million acquisition of CASMED illustrate strategic moves to secure proprietary tissue oximetry portfolios. Incumbents invest in machine-learning algorithms that forecast cerebral desaturation minutes ahead, enabling proactive perfusion adjustments.

Emerging firms leverage solid-state lasers, silicon photomultipliers, and flexible circuit substrates to create lighter wearables. Partnerships between optics specialists and electrophysiology developers, like the Artinis–TMSi merger, lay foundations for combined fNIRS-EEG headsets. Intellectual-property walls around depth-resolved NIRS and sensor calibration software raise entry barriers, while mature players exploit global service networks to lock in long-term disposable contracts. Value-tier competitors, particularly from China, pivot on affordable wireless patches that address price-sensitive markets without undermining core quality.

Artificial intelligence increasingly differentiates offerings: predictive models integrate real-time FiO2, MAP, and temperature feeds to suggest personalized perfusion targets. Cloud dashboards benchmark saturation trends against anonymized cohorts, providing surgeons with comparative analytics. Over the forecast period, competition is expected to center on holistic perioperative ecosystems rather than stand-alone devices, pushing vendors to secure interoperability certifications with leading anesthesia information systems.

Cerebral Somatic Oximeters Industry Leaders

Medtronic Plc

Edwards Lifesciences

Nonin Medical, Inc.

ISS Inc.

Masimo Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is forming around software-defined differentiation and protocol-driven adoption in high-acuity workflows where cerebral and somatic rSO2 trends influence perfusion and ventilation decisions. This is most apparent in cardiac surgery, ICU, and ECMO management, where clinical teams increasingly use rSO2 to guide monitoring-driven actions. FDA clearance activity also points to vendor focus on algorithmic and parameter expansion, not just hardware refresh cycles, including Edwards Lifesciences clearance (October 2024) for a Cerebral Autoregulation Index (CAI) Algorithm under tissue saturation oximetry classification. Related updates to add delta hemoglobin parameters help clinicians interpret whether rSO2 changes reflect oxygen delivery versus consumption.

Another opportunity sits in multisite monitoring and workflow integration for decentralized care delivery, including ambulatory surgical centers that favor compact systems and simplified consumables. Clinical standardization at the hospital level supports adoption beyond early adopters, illustrated by the NHS Greater Glasgow and Clyde (NHS GGC) publishing a Near-Infrared Spectroscopy (NIRS) guideline (Right Decisions platform). In regions where evidence generation can gate purchasing, manufacturers and hospitals use registries, protocol bundles, and interoperable monitoring stacks to strengthen cost-effectiveness narratives tied to perioperative safety metrics.

Recent Industry Developments

- March 2026: Medtronic entered a definitive agreement to acquire Scientia Vascular for USD 550 million, adding neurovascular access technologies to its portfolio. While not a cerebral oximeter transaction, the deal strengthens Medtronic’s neurovascular procedural footprint and supports broader workflow integration across neuro care and acute monitoring environments where INVOS cerebral/somatic oximetry is used.

- April 2025: Medtronic signed an exclusive US distribution agreement for Retia Medical’s Argos cardiac output monitor as an addition to its Acute Care Monitoring portfolio. The pairing complements INVOS cerebral oximetry use cases by supporting combined hemodynamic and regional oxygenation management protocols in operating rooms and ICUs.

- October 2024: The FDA cleared Edwards Lifesciences’ Cerebral Autoregulation Index (CAI) Algorithm (K240596) under tissue saturation oximetry classification. The clearance reinforces the market shift toward software and algorithm upgrades that add clinical decision support on top of existing near-infrared spectroscopy monitoring platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers devices used in clinical settings to non-invasively measure regional oxygen saturation in cerebral and somatic tissue, typically using near-infrared spectroscopy sensors and related monitoring units. The market size is stated in value terms based on sales into care sites.

Scope exclusions: We exclude standard pulse oximeters, pure capnography or EEG systems, consumables not used for cerebral or somatic rSO2 sensing, and patient monitoring services that do not generate device revenue.

Segmentation Overview

- By Type

- Dual Emitter & Dual Detector

- Single Emitter & Dual Detector

- Other Types

- By Application

- Cardiac Surgery

- Vascular Surgery

- Neuro-Surgery & Traumatic Brain Injury

- Other Applications

- By Patient Type

- Neonates

- Pediatrics

- Adults

- By End User

- Hospitals and Clinics

- Ambulatory Surgical Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand context and set practical bounds before speaking with the market. We referred to public sources such as the US FDA device databases, the US Centers for Medicare and Medicaid Services for procedure and site-of-care signals, the World Health Organization health statistics, and the World Bank population and health spend series. PubMed-indexed clinical literature was also used to see where cerebral and somatic oximetry is commonly used and how adoption has shifted over time.

On the commercial side, company annual reports, investor presentations, and credible healthcare trade coverage helped us map product presence, typical channel structures, and broad pricing direction. Select paid subscriptions that cover company financials and patent databases were used to cross-check ownership changes and technology focus when public disclosures were thin. The sources listed here are illustrative rather than exhaustive, and additional public references and subscriptions were used to collect, validate, and clarify the final dataset.

Primary Interviews and Surveys

Primary work focused on interviews and structured questionnaires with hospital procurement stakeholders, clinicians in OR and ICU environments, distributors, and device-side product or commercial managers, so assumptions could be tested against day-to-day operational constraints. For a global market, inputs were validated across mature and developing healthcare systems, with questions centered on procedure mix, typical attach rates of sensors, replacement cycles, and pricing practices that vary by tendering and contracting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 43% |

| Mid tier: 56% | Functional/Unit leaders: 38% | EMEA: 34% |

| Smaller Players: 14% | Managers: 48% | Americas: 23% |

Market-Sizing & Forecasting

The sizing model starts with a top-down build where procedure volumes in key application areas (such as cardiac surgery and vascular surgery) are translated into an addressable monitoring pool using expected adoption and usage intensity. Once the demand pool is formed, it is converted into value using typical system pricing and sensor utilization patterns, then adjusted by end-user mix across hospitals, clinics, and ambulatory surgical centers.

To keep outputs grounded, we run selective bottom-up approximations as a check, including channel feedback on unit placements, sampled average selling prices, and inferred consumption of disposable sensors tied to the installed base. Inputs tracked in the model include surgical case volumes by region, ICU and OR bed availability signals, neonatal and pediatric procedure share where relevant, replacement and upgrade cycles for monitors, and regional pricing differences driven by contracting and currency movements. Forecasts are built using scenario analysis, with a base case tuned based on what primary respondents expect for procedure recovery, adoption in new care sites, and pricing pressure. Where bottom-up checks are incomplete in smaller regions, we use proxy indicators and then rebalance so regional totals align with the global demand logic.

Data Validation & Update Cycle

Outputs are validated through cross-checks against independent signals such as procedure trend direction, device adoption references in clinical guidelines or literature, and consistency across patient-type and end-user splits. Outliers are reviewed through multiple analyst steps, and when a number appears too high or too low, we trace the assumptions back to the specific input variable and re-test with follow-up outreach.

The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory actions, pricing shocks, or meaningful changes in clinical practice patterns. Before delivery, a final review pass is completed so the market size, assumptions, and near-term forecasts reflect the most recent information available to us.

Mordor Intelligence's Cerebral Somatic Oximeters Market Size Versus Other Published Estimates

Different market sizes are often published for the same device category, even when the growth direction appears similar. The main drivers are what is counted as revenue, how closely the product set is defined, and whether the estimate is tied to clinical activity or extended from broader industry narratives.

The table shows a visible spread across published values, and in Mordor Intelligence's model the total is restricted to cerebral and somatic oximeter monitoring equipment and directly associated sensing components used for rSO2 measurement, instead of bundling general patient-monitoring platforms or standard pulse oximetry revenues. Differences also come from how sources handle base-year alignment, whether they apply faster adoption ramps for new care sites, and how they carry forward prices without consistently cross-checking procedure mix, end-user purchasing cycles, and regional currency timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 215.56 M (2026) | |

| Global Research Publisher A | USD 232.84 M (2025) | Uses a broader cerebral oximetry monitoring framing with a different base year, and the scope may include adjacent monitoring revenues beyond cerebral and somatic rSO2 device sales, which shifts the starting value upward. |

| Industry Bulletin B | USD 239.40 M (2024) | Value is anchored to an earlier year and is typically presented as a high-level market value, with limited visibility on how procedure volumes, sensor usage intensity, and currency timing were validated across regions. |

Looking across the three figures, most of the gap is explained by year alignment and how tightly the product and revenue scope are defined, followed by how adoption and pricing are carried forward. By keeping assumptions traceable to procedure-led demand signals and then checking them with supplier and channel inputs, the final number stays practical to replicate and easier to explain in planning discussions.

Key Questions Answered in the Report

What is the current value of the cerebral somatic oximeters market?

The cerebral somatic oximeters market is valued at USD 215.56 million in 2026.

How fast will cerebral somatic oximeter demand grow through 2031?

Sales are forecast to rise at a 6.14% CAGR, reaching USD 290.33 million by 2031.

Which application generates the biggest revenue?

Cardiac surgery leads with 44.90% of global revenue in 2025.

Which patient group is expanding quickest?

Neonatal monitoring posts the highest 8.19% CAGR, powered by specialized sensors.

Which region offers the strongest growth prospects?

Asia-Pacific records a 7.10% CAGR, driven by rising procedure volumes and infrastructure spending.

Who are the leading suppliers?

Masimo, Medtronic, and Edwards Lifesciences headline the competitive field, with specialized innovators such as Artinis and NIRx gaining momentum.

Page last updated on: