Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

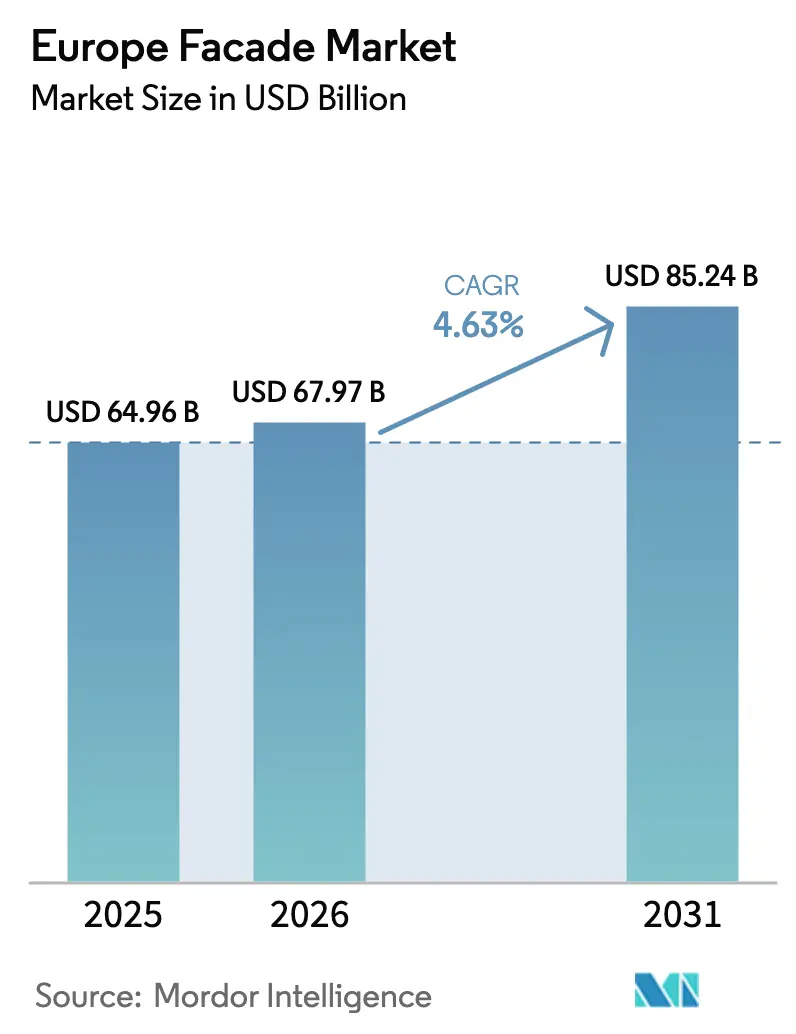

| Base Year Market Size (2025) | USD 64.96 Billion |

| Market Size (2026) | USD 67.97 Billion |

| Market Size (2031) | USD 85.24 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Facade Market Analysis by Mordor Intelligence

The Europe Facade Market size is expected to grow from USD 64.96 billion in 2025 to USD 67.97 billion in 2026 and is forecast to reach USD 85.24 billion by 2031 at 4.63% CAGR over 2026-2031.

Regulatory upgrades under the Energy Performance of Buildings Directive are forcing deep-renovation programs that channel capital toward high-performance envelopes. Rising fire-safety obligations after the 2024 Valencia tower tragedy have shifted specifications toward non-combustible rainscreen systems. Labor shortages across Northern Europe favor unitized off-site panels that cut installation time by up to 30%. Volatile aluminum prices have widened the cost gap between stick-built and prefabricated assemblies, strengthening the value proposition of factory-finished cassettes. Heritage-retrofit activity is also growing because reversible insulation solutions allow protected buildings to meet tightening energy codes without damaging original facades.

Key Report Takeaways

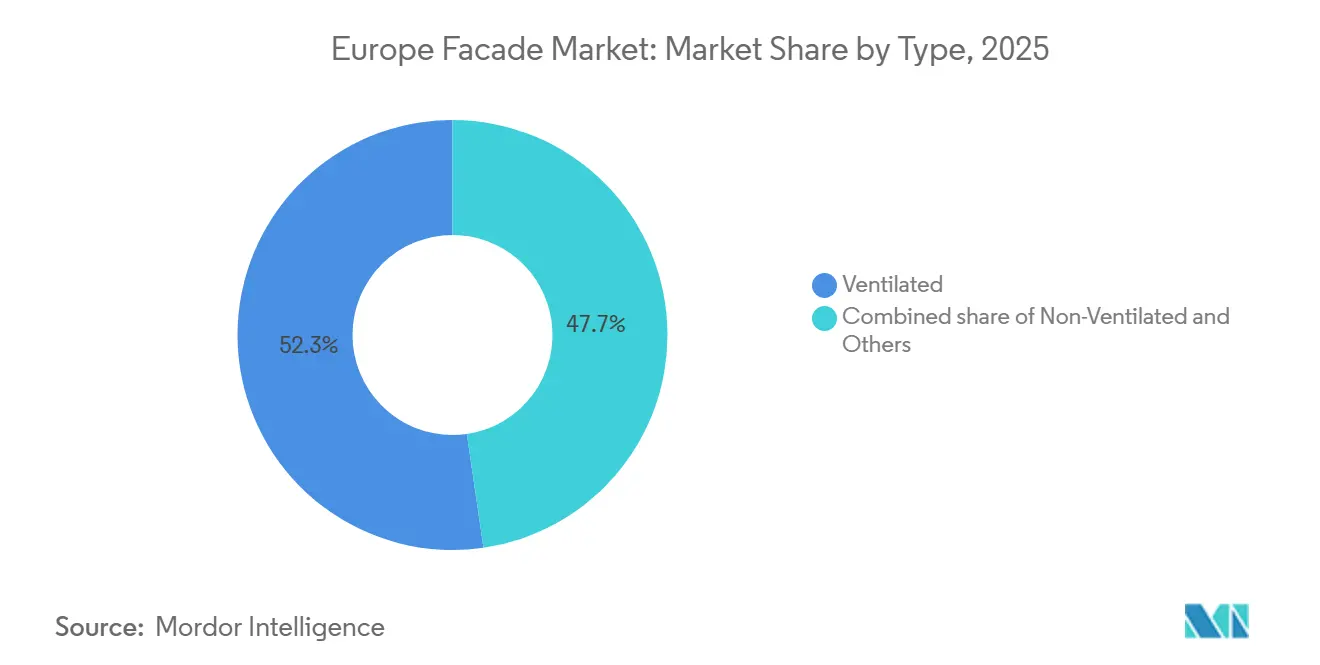

- By type, ventilated facades led with 52.3% market share in 2025 and are projected to post the fastest 5.12% CAGR through 2031.

- By façade system type, curtain-wall systems captured 45.1% share in 2025, while rainscreen cladding is forecast to grow the quickest at a 4.98% CAGR over 2026-2031.

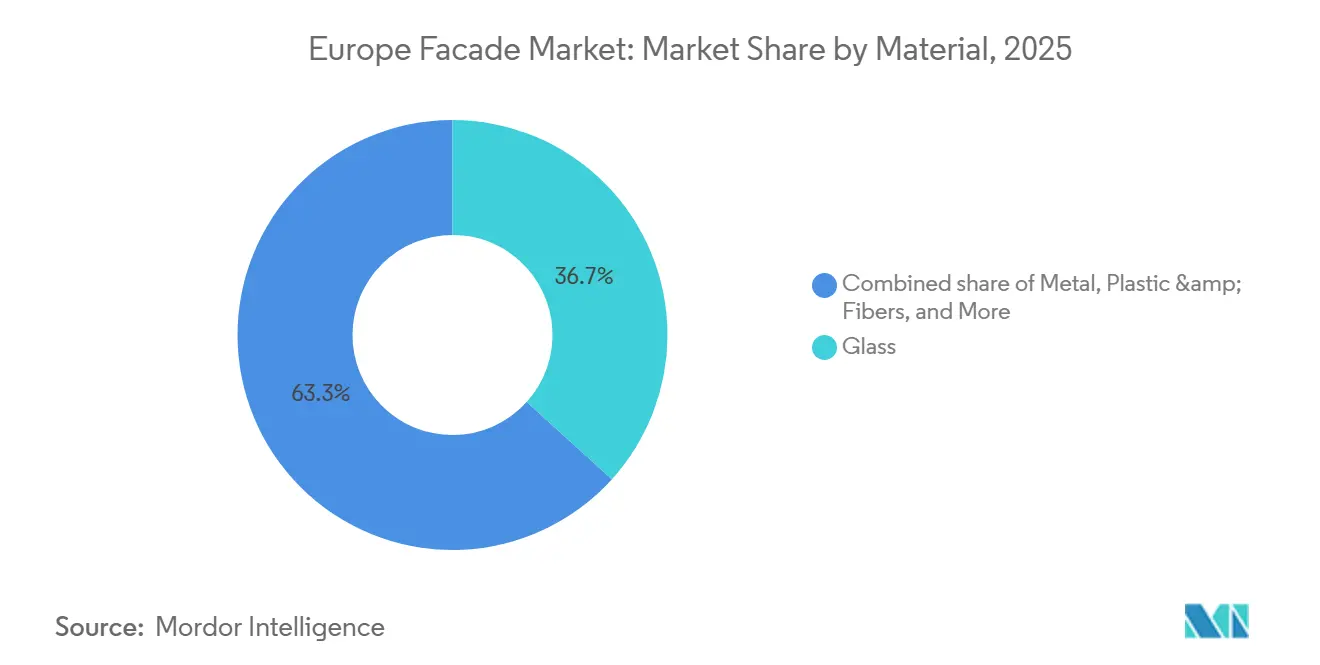

- By material, glass dominated with a 36.7% share in 2025 and also records the top growth outlook, advancing at a 5.22% CAGR to 2031.

- By installation, new construction accounted for 56.9% of 2025 activity, yet renovation and retrofit installations are expected to expand at the leading 5.39% CAGR during the forecast window.

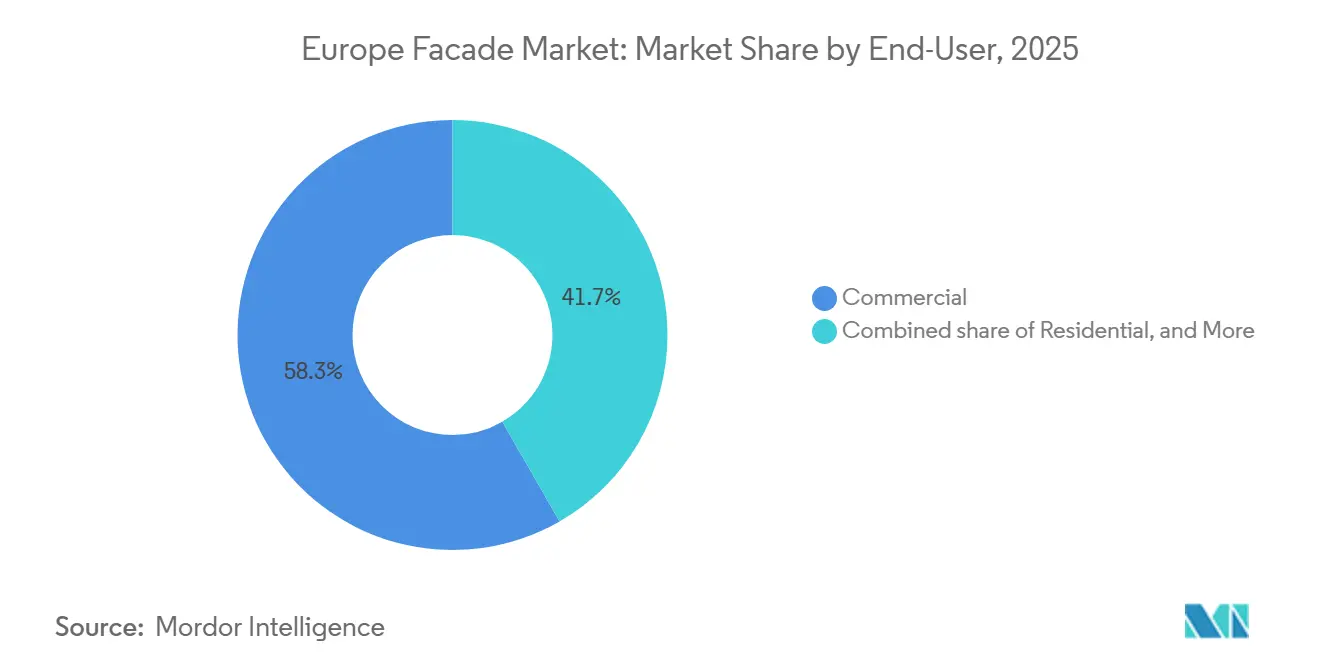

- By end-user, commercial projects contributed 58.3% of 2025 revenue, whereas residential applications show the highest momentum with a 5.01% CAGR to 2031.

- By region, Germany held the largest 22.1% share in 2025, while Sweden is projected to register the fastest 5.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Facade Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter energy-efficiency regulations are increasing the adoption of insulated facade systems | +0.9% | Nordics, Germany, France | Long term (≥4 years) |

| EU renovation programs are driving demand for facade refurbishment and overcladding | +0.8% | Germany, France, the Netherlands | Medium term (2-4 years) |

| Fire-safety compliance is pushing demand for non-combustible facade materials | +0.7% | United Kingdom, Spain, Germany | Short term (≤2 years) |

| Shift toward off-site and unitized facades to reduce construction time | +0.6% | United Kingdom, Germany, Nordics | Medium term (2-4 years) |

| Replacement of aging building envelopes to meet modern performance standards | +0.5% | Germany, France, Italy | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stricter Energy-Efficiency Regulations Increasing Adoption of Insulated Facade Systems

France’s RE2020 tightened lifecycle-carbon thresholds again in 2025, rewarding bio-based insulation and recycled cladding. Germany’s GEG amendment in 2024 forces U-values below 0.20 W/m²K in most walls, aligning with the Nordics, where triple-glazed curtain walls achieve 0.8 W/m²K or better. A 2024 German Energy Agency study showed that upgrading pre-1979 housing stock could avoid 5.3 million t of CO₂ annually. The United Kingdom’s Future Homes Standard, effective 2025, cuts operational carbon by up to 80% compared with the 2013 codes. These policies channel material demand toward high-performance stone wool, thermally broken frames, and electrochromic glass.

EU Renovation Programs Driving Demand for Facade Refurbishment and Overcladding

Mandatory Minimum Energy Performance Standards block the sale or lease of buildings below class F from 2030, so owners are steering capital toward over-cladding that lifts ratings by three classes in a single project. Germany’s BEG grants covered up to 40% of facade-insulation costs in 2025, while France dispersed USD 2.8 billion in MaPrimeRénov’s incentives that required external-wall upgrades for full benefits[1]German Federal Ministry for Economic Affairs, “BEG Funding Statistics 2025,” bmwk.de . The Netherlands targeted 2.5 million homes for insulation by 2030, covering up to half of the material and labor costs. Spain committed USD 7.4 billion for building rehabilitation, with 80% earmarked for envelope improvements. These national programs translate into a steady renovation pipeline that underpins long-run growth of the European facade market.

Fire-Safety Compliance Pushing Demand for Non-Combustible Facade Materials

EU Regulation 2024/1681 now requires Euro class B-s1, d0 or higher on cladding above 18 m, effectively excluding many polymeric cores. The Building Safety Act bans combustible products on residential walls taller than 11 m, expanding to hospitals in 2025. Spain outlawed combustible insulation above 15 m after the Valencia incident. Large-scale fire-test regimes DIN 4102-20 and BS 8414 cost more than USD 160,000 per variant and consolidate demand among established suppliers of stone wool and fiber-cement boards. United Kingdom stone wool volumes jumped by eight points between 2022 and 2025, confirming a structural shift toward mineral solutions.

Shift Toward Off-Site and Unitized Facades to Reduce Construction Time

United Kingdom productivity policy targets one-quarter of new housing via off-site manufacturing by 2030, naming unitized envelopes as a keystone. Factory-built panels cut on-site labor by 20-30%, an advantage as Germany faces a 15% craft-labor shortfall. Schüco’s FWS 60 CV panel places 50–60 units per day on high-rise sites, compressing schedules and reducing weather risk. Dutch public-building guidelines now insist that half of new projects apply industrialized methods by 2030. A 2025 CIRIA study reported 40% fewer facade defects in factory-made units than stick-built alternatives, lowering warranty reserves across the Europe facade market[2]Construction Industry Research and Information Association, “Factory-Built Facades Performance Study 2025,” ciria.org .

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy facade testing and certification timelines | -0.4% | Germany, France, the United Kingdom | Short term (≤2 years) |

| Complexity of retrofitting older and heritage buildings | -0.3% | Italy, France, Spain, the United Kingdom | Medium term (2-4 years) |

| Volatile prices and long lead times for aluminum and architectural glass | -0.3% | Region-wide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Lengthy Facade Testing and Certification Timelines

European Technical Assessments often last 12–18 months and require separate full-scale fire and wind tests for every system variant. Dual CE and UKCA processes since Brexit have doubled the workload for exporters to Britain. Germany’s DIBt recorded a 14-month average decision time in 2025, while France’s fast-track route still needs eight months of data. These delays raise entry costs above USD 250,000 and deter smaller innovators, slowing the refresh cycle of the Europe facade market[3]Deutsches Institut für Bautechnik, “Annual Report 2025,” dibt.de .

Complexity of Retrofitting Older and Heritage Buildings

Many Italian and French landmarks forbid external insulation, forcing internal upgrades that shrink usable floor area and introduce thermal bridges. Reversible mechanical fixings and breathable lime renders add 30–40% to facade budgets, and only a small pool of contractors holds the specialized skills. Approval from heritage bodies can add a year to project timelines, while material limits often cap insulation thickness to 80 mm, compromising thermal gains. These constraints temper the otherwise strong retrofit outlook in historic urban cores.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type – Ventilated Systems Dominate Cold-Climate Demand

Ventilated facades held 52.3% of the Europe facade market share in 2025. Their cavity design allows moisture to escape, preventing freeze–thaw damage and mold in regions that receive more than 800 mm of annual rainfall. Non-ventilated systems are prevalent around the Mediterranean, where cooling loads dominate, and simplified details cut costs. Hybrid concepts that embed photovoltaic laminates in ventilated panels are gaining ground in Germany and the Netherlands for Article 10 solar compliance.

Nordic developers specify ventilated rainscreens because the air gap dampens wind-driven rain and reduces heating demand by up to 15%. Spain and Italy keep favoring direct-bonded systems that require fewer anchors and shorter site programs. Hybrid PV ventilated façades fitted to new Frankfurt offices already trim grid electricity by 20%, pointing to high future uptake as module prices fall.

By Facade System Type – Rainscreen Gains on Fire-Safety Tailwinds

Curtain walls commanded 45.1% of the Europe facade market size in 2025. Rainscreen cladding is advancing at the fastest 4.98% CAGR because regulators now favor inspectable cavities with mineral insulation. Curtain walls stay dominant in towers above 50 m where structural demands and daylight targets prevail. Point-supported and structural glazing serve signature museums and terminals but remain niche.

Fire-test data show rainscreens can cut flame spread risk by 60% compared with closed cavities, which has accelerated adoption in the United Kingdom and Spain residential schemes over 18 m. Curtain-wall technology is evolving, with electrochromic IGUs that lower cooling loads by up to 30% in southern latitudes. Structural glazing and spider systems continue to command premium prices in landmark projects, though their aggregate surface area stays below 5%.

By Material – Glass Leads on Solar Integration and Transparency

Glass captured 36.7% of 2025 demand and is expected to grow at a 5.22% CAGR, the highest among materials, as Article 10 forces solar-ready skins on public and commercial buildings. Metal cladding, largely aluminum composite and zinc, holds mid-rise industrial and residential footholds where durability rules. Fiber-cement and high-pressure laminates serve value markets and deliver Euro class A1 safety. Natural stone keeps a boutique role in hospitality and heritage refurbishments.

Triple-glazed low-e IGUs now account for 60% of new curtain-wall area in Germany and the Nordics. Electrochromic glass in Paris and Milan offices shaves 20–25% from HVAC energy, supporting sustainability certifications. Recycled-content aluminum extrusions reached 75% of Reynaers' output in 2025. Fiber-cement gained 12% volume share in the United Kingdom cladding replacement because of non-combustibility, while thin-cut stone lets heritage sites pair internal insulation with authentic frontage.

By Installation – Renovation Accelerates on Regulatory Pressure

New construction supplied 56.9% of 2025 installations, yet renovation work is advancing at a 5.39% CAGR as energy-class penalties loom in 2030. Retrofit packages usually pair overcladding with triple-glazed windows and cavity fire barriers. Germany, France, and the United Kingdom tower blocks from the 1960s–1980s represent the largest backlog.

Germany dispensed USD 5.7 billion of BEG grants for facade insulation in 2025. France prioritizes 55% energy-savings renovations under MaPrimeRénov’, while the United Kingdom social-housing funds budget USD 1 billion for external wall upgrades on low-income estates. New construction remains strong in Sweden and Denmark, where near-zero-energy permitting is simplified, but life-cycle carbon caps still incentivize factory-made panels that cut waste and on-site hours.

By End-User – Commercial Dominates, Residential Gains on Housing Retrofits

Commercial projects delivered 58.3% of 2025 revenue, reflecting the prevalence of curtain walls in offices, retail centers, and civic buildings. Residential is growing at a 5.01% CAGR because subsidy programs reward landlords who lift Energy Performance Certificates to class C or better. Industrial and public campuses make up the balance and follow capital-budget cycles.

Commercial clients seek column-free interiors and daylighting, which pushes triple-glazed unitized walls with integrated blinds. Residential retrofits in Germany’s Plattenbau estates and the United Kingdom council towers can trim heating bills by 50% when external insulation brings U-values below 0.20 W/m²K. Spain and Italy multifamily schemes turn to ventilated ceramic facades that marry traditional aesthetics with Euroclass A1 fire ratings. Logistics operators favor insulated metal panels that meet 0.25 W/m²K at a 30% lower installed cost than curtain walls.

Geography Analysis

Germany retained 22.1% of the European facade market in 2025 because the amended GEG requires renewable heating coverage and U-values beneath 0.20 W/m²K, forcing investment in high-performance envelopes. Project developers responded even though construction output slipped 1.2% under high interest rates, and facade renovation grew 6.8% as owners raced to avoid class F penalties. The United Kingdom demand pivoted from new build to remediation since GBP 6.5 billion of public money is earmarked for unsafe cladding removal, causing facade activity to jump 22% in 2025 despite a 3.5% fall in residential starts.

France tightened RE2020 embodied-carbon limits in 2025, driving specification of bio-based insulation and recycled cladding, although residential permits dropped 8% while renovation permits rose 14%. Italy and Spain grew more slowly because of financing costs, yet Spain’s USD 7.4 billion rehabilitation plan still steers 80% of funds into energy efficiency. Poland and the Czech Republic use Cohesion Fund grants to back social-housing insulation.

Sweden is the fastest-growing geography at a 5.55% CAGR to 2031, helped by grants that cover half of facade-insulation costs for pre-1980 buildings and a statutory pledge to halve building-sector emissions by 2030. Denmark, Norway, and Finland converge on near-zero energy codes that require curtain-wall U-values of 0.8 W/m²K or lower, which lifts demand for triple-glazed IGUs and thermally broken framing. Finland caps whole-building energy at 90 kWh/m² annually for new dwellings, pushing envelope performance ahead of EU minimums.

Competitive Landscape

Competition is moderately fragmented. Kingspan, Rockwool, and Saint-Gobain hold vertically integrated positions from insulation batch to panel assembly, giving them scale in testing and certification, while Permasteelisa and Lindner specialize in design-build curtain walls for complex towers. Mid-tier metal fabricators compete on regional relationships and rapid turnaround. Entry barriers remain high because full-scale fire and weather testing can exceed USD 250,000 per system and take more than a year, favoring incumbents with CE and UKCA portfolios.

Strategic investment is flowing into automated off-site plants. Kingspan spent USD 93 million to expand German panel capacity by 200,000 m² a year, and Lindner installed robotic lines that trim labor by 35% and shorten lead times from 14 to nine weeks. Schüco’s FWS 60 CV unit integrates photovoltaics and hits 0.7 W/m²K, aligning with Article 10 rules and capturing premium margins. Reynaers pairs cloud configurators with BIM Level 3 tools that output fabrication drawings in hours, compressing design-to-production by 20%.

The innovation focus now lies in bio-based insulation, reversible heritage kits, and integrated PV cladding, though each still accounts for less than 5% of the European facade market. Rockwool is consolidating the stone wool supply in Central Europe after buying Polish and Spanish producers, securing raw material against price swings. Saint-Gobain filed a 2025 patent for a self-healing glazing coating that could stretch curtain-wall life expectancy to 35 years. Smaller disruptors offer parametric design and onsite robotics but struggle with capital intensity and conservative procurement practices.

Europe Facade Industry Leaders

Alliance Facades

Alucraft Ltd

EOS Framing Limited

Saint-Gobain S.A.

Lindner Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Reynaers partnered with a Dutch robotics firm to cut unitized-panel lead times by 35%.

- September 2024: Rockwool opened a 100,000 t stone-wool plant in Romania to serve EU-funded retrofit projects in Eastern Europe.

- June 2025: Schüco released the FWS 60 CV unitized curtain wall with integrated photovoltaics and a 0.7 W/m²K U-value.

- March 2025: Kingspan committed USD 93 million to expand insulated-panel production in Germany by 200,000 m² annually.

Europe Facade Market Report Scope

By Type

| Ventilated |

| Non-Ventilated |

| Others |

By Façade System Type

| Rainscreen Cladding |

| Curtain-Wall Systems |

| Others |

By Material

| Glass |

| Metal |

| Plastic & Fibres |

| Stone |

| Others |

By Installation

| New Construction |

| Renovation & Retrofit |

By End-User

| Commercial |

| Residential |

| Others |

By Region

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Nordics(Sweden, Denmark, Norway, Finland) |

| Rest of Europe |

| By Type | Ventilated |

| Non-Ventilated | |

| Others | |

| By Façade System Type | Rainscreen Cladding |

| Curtain-Wall Systems | |

| Others | |

| By Material | Glass |

| Metal | |

| Plastic & Fibres | |

| Stone | |

| Others | |

| By Installation | New Construction |

| Renovation & Retrofit | |

| By End-User | Commercial |

| Residential | |

| Others | |

| By Region | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Nordics(Sweden, Denmark, Norway, Finland) | |

| Rest of Europe |

Key Questions Answered in the Report

How large will facade spending in Europe be by 2031?

The Europe facade market is forecast to reach USD 85.24 billion by 2031 at a 4.63% CAGR from 2026.

Which facade type currently holds the lead?

Ventilated systems held 52.3% of 2025 demand and remain the largest segment.

What is driving the rise of rainscreen cladding?

Harmonized EU fire-safety rules and post-Grenfell legislation favor non-combustible rainscreen cavities, driving a 4.98% CAGR.

Why is Sweden the fastest-growing national market?

Sweden couples 50% renovation grants with tough emission targets that raise facade-retrofit demand at a 5.55% CAGR.

How are suppliers shortening project cycles?

Automated off-site factories and BIM-linked configurators cut panel lead times up to 35% and reduce on-site labor by 30%.

Which material shows the strongest growth outlook?

Glass, boosted by mandatory solar integration, leads material growth at a projected 5.22% CAGR through 2031.

Page last updated on: