ASEAN Mechanical, Electrical, And Plumbing (MEP) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

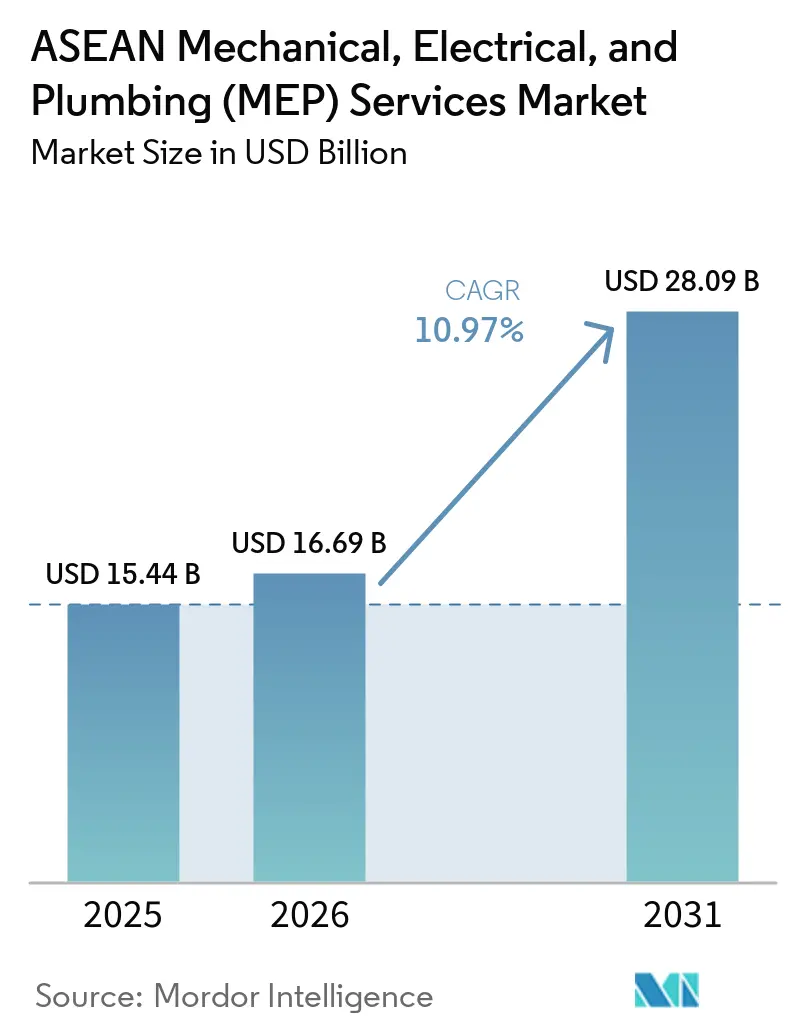

| Base Year Market Size (2025) | USD 15.44 Billion |

| Market Size (2026) | USD 16.69 Billion |

| Market Size (2031) | USD 28.09 Billion |

| Growth Rate (2026 - 2031) | 10.97% CAGR |

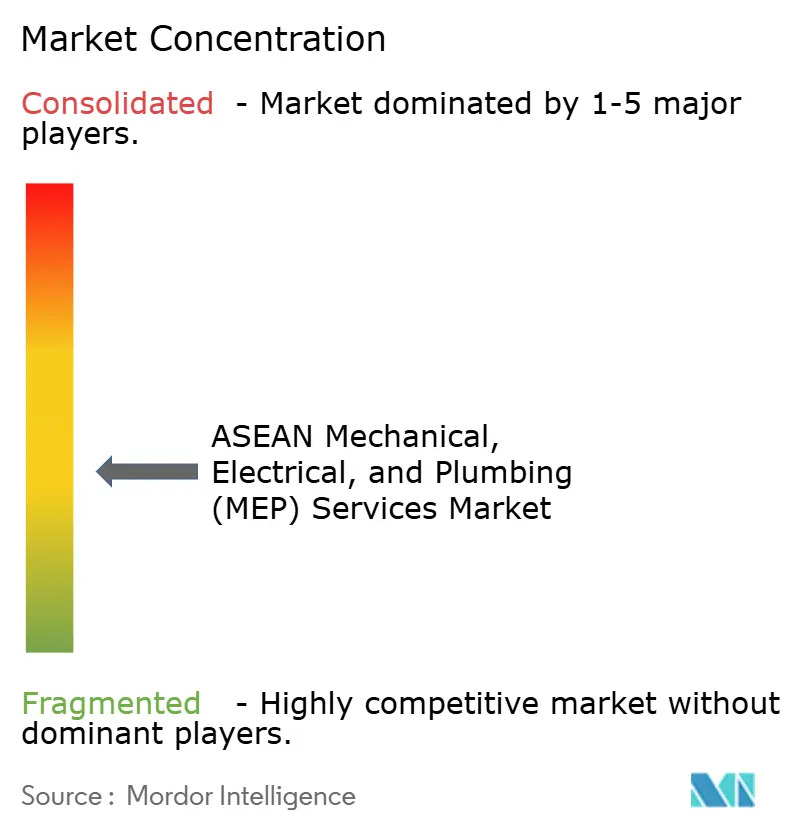

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Mechanical, Electrical, And Plumbing (MEP) Services Market Analysis by Mordor Intelligence

The ASEAN Mechanical, Electrical, And Plumbing Services Market size is expected to grow from USD 15.44 billion in 2025 to USD 16.69 billion in 2026 and is forecast to reach USD 28.09 billion by 2031 at 10.97% CAGR over 2026-2031. The ASEAN Mechanical, Electrical, and Plumbing (MEP) services market is being supported by concurrent infrastructure cycles across the six major ASEAN economies, along with digital infrastructure expansion, industrial estate development, and tighter green-building compliance requirements. Foreign direct investment into ASEAN reached USD 226 billion in 2024, up 8% year on year, and greenfield investment in supply-chain-intensive manufacturing increased to USD 41 billion, which is widening the addressable pipeline for cooling, power, ventilation, water, and building-system design work across the region[1]ASEAN Secretariat and United Nations Conference on Trade and Development, “ASEAN Investment Report 2025: Foreign Direct Investment and Supply Chain Development,” ASEAN Secretariat, asean.org. Semiconductor commitments from Infineon in Malaysia, TSMC in Singapore, and BYD in Indonesia are adding dense project scopes in cleanrooms, high-voltage electrical systems, and precision-cooling environments, which give the ASEAN MEP services market a deeper industrial base than a standard building-services cycle. Public transport expansion, utility modernization, and urban construction in markets such as Vietnam and Indonesia also create demand redundancy, helping the ASEAN MEP services market remain resilient even when one project class slows. Competition remains moderately fragmented across global consultancies, regional contractors, and local specialists, while the clearest operating risk is skilled labor scarcity, which is extending delivery timelines and putting pressure on execution quality in the ASEAN MEP services market.

Key Report Takeaways

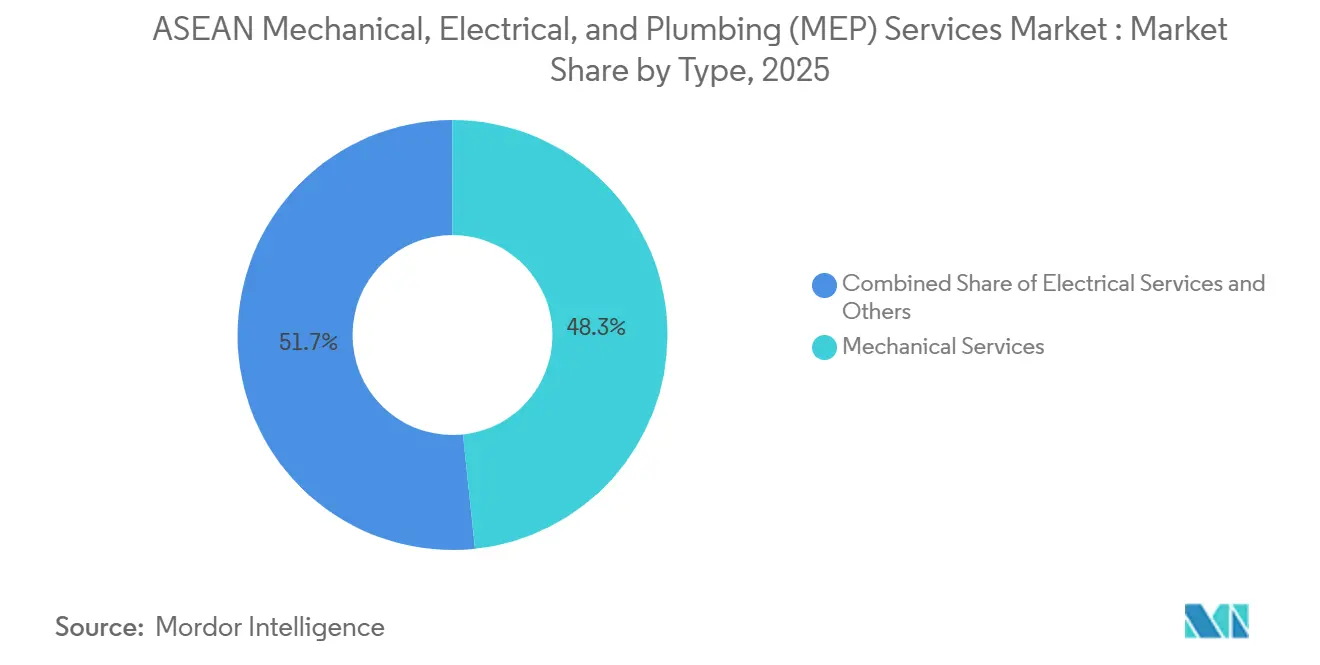

- By type, mechanical services held 48.34% of the ASEAN MEP market share in 2025, while integrated MEP services is forecast to expand at 8.1% CAGR through 2031.

- By service type, design & engineering led with 36.34% of market value in 2025, while other services are projected to grow at 8.82% CAGR through 2031.

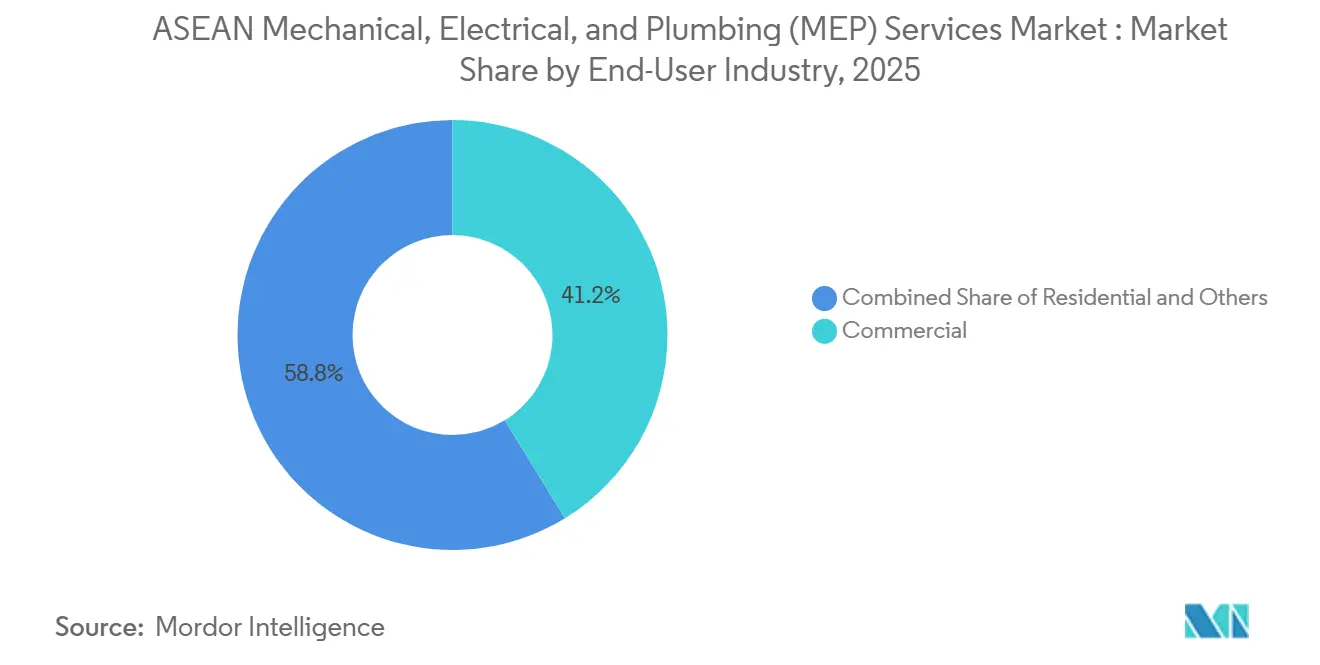

- By end-user industry, the commercial sector accounted for 41.23% of the ASEAN MEP services market size in 2025, while Infrastructure is advancing at a 8.6% CAGR through 2031.

- By geography, Indonesia accounted for 33.22% of regional value in 2025, while Vietnam is expected to record the highest CAGR of 8.19% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Center Capacity Growth Across Malaysia, Indonesia, and Singapore | +2.8% | Malaysia, Indonesia, Singapore | Short term (≤ 2 years) |

| Urban Housing and Transport Infrastructure Expansion | +2.5% | ASEAN-wide, strongest in Indonesia and Vietnam | Medium term (2-4 years) |

| EV, Electronics, and Semiconductor Manufacturing Clusters | +1.8% | Malaysia, Thailand, Indonesia, Singapore | Long term (≥ 4 years) |

| Smart-City and Industrial-Park Development Pipeline | +1.2% | Malaysia, Thailand, Vietnam | Medium term (2-4 years) |

| Green-Building Codes and BIM E-Submission Mandates | +1.0% | Singapore, Malaysia, ASEAN-wide | Medium term (2-4 years) |

| Flood-Resilient Water, Drainage, and Cooling System Design | +0.8% | Indonesia, Vietnam, Thailand, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Center Capacity Growth Across Malaysia, Indonesia, and Singapore

Data-center expansion is one of the most concentrated demand drivers for the ASEAN MEP services market in the near term, as these assets require far denser cooling, power redundancy, fire systems, and water management than conventional offices or hotels. The pattern is visible in Johor and wider Malaysia, where modular and large-format digital facilities are being delivered faster and with more integrated mechanical and electrical coordination than earlier commercial buildings, as shown by Aurecon’s award-winning 60 MW prefab data center project in Johor. It is also evident in Thailand’s ARAYA Eastern Gateway, which is integrating high-voltage power, gas utilities, and 5G connectivity while targeting data center operators among its anchor tenants. AI-ready facilities require high-density electrical distribution, precision thermal control, disciplined water management, and tighter commissioning standards, which means MEP revenue intensity rises much faster than floor area alone would suggest. Developers are therefore favoring integrated delivery structures that can coordinate mechanical, electrical, plumbing, testing, and commissioning packages under a single accountability framework, which directly benefits the ASEAN MEP services market.

Urban Housing and Transport Infrastructure Expansion

The ASEAN MEP services market continues to draw strength from urbanization because city growth creates linked demand for housing, transit stations, tunnels, utilities, and public-service buildings. By 2026, nearly two-thirds of the region’s population will live in cities, and 90 million more people are expected to urbanize across the ASEAN-5 between 2018 and 2030, which keeps the construction pipeline broad and durable across several countries at the same time. This demand is not confined to residential supply, as outward urban expansion also increases the need for ventilation systems, power distribution, water handling, and fire protection on metro, road, and utility projects. Hanoi, Ho Chi Minh City, and Greater Jakarta are all expanding their transport infrastructure, and these programs require specialist electromechanical scopes that general civil contractors cannot take on themselves. Vietnam’s construction sector grew by more than 9% in 2025 and contributed nearly 17% to GDP, underscoring the significant impact of transport and housing investment on the technical workload available to the ASEAN MEP services market.

EV, Electronics, and Semiconductor Manufacturing Clusters

The ASEAN MEP services market is also benefiting from the rising complexity of industrial construction, as semiconductor, electronics, and EV facilities require far more specialized utility systems than standard factories. ASEAN attracted an average of USD 12 billion in semiconductor greenfield investment between 2021 and 2024, and the region accounted for more than 20% of global semiconductor assembly, testing, and packaging activity, reinforcing demand for cleanroom HVAC, high-grade water systems, and advanced electrical infrastructure. Penang’s Silicon Island Green Tech Park moved into the factory-construction phase in 2026 and is targeting semiconductor, medical-device, and advanced-manufacturing tenants, which confirms that industrial MEP demand is broadening within Malaysia’s technology corridor. Thailand’s ARAYA Eastern Gateway was formally declared an industrial estate in September 2025 and includes 115kV power supply, smart energy systems, and integrated digital connectivity, which supports a similar move toward higher-value industrial campuses. These facilities require multiple specialist disciplines within a single project scope, and this shift is giving the ASEAN MEP services market a stronger long-term industrial foundation.

Smart-City and Industrial-Park Development Pipeline

Smart-city and industrial-park development in Malaysia, Thailand, and Vietnam is increasing demand for integrated cooling, power, water, drainage, fire protection, and digital building systems across new project sites. ASEAN’s greenfield investment in supply-chain-intensive manufacturing reached USD 41 billion in 2024, which is supporting new industrial clusters and related demand for building-services design and execution across the region. In Malaysia, Penang’s Silicon Island Green Tech Park moved into the factory-construction phase in 2026 and is targeting semiconductor, medical device, and advanced manufacturing tenants, which raises demand for precision cooling, electrical distribution, and utility-system planning. In Thailand, ARAYA Eastern Gateway was formally declared an industrial estate in September 2025 and includes 115kV electrical supply, natural gas utilities, and 5G connectivity, showing that new parks are being developed as fully serviced engineering environments rather than simple land projects. In Vietnam, the medium-term public investment plan for 2026 to 2030 prioritizes transport, urban development, and energy infrastructure, thereby strengthening the supporting base for industrial zones and smart urban developments. Because these projects are built in phases and rely on coordinated utility networks from the start, they create repeat demand across design, installation, testing, commissioning, and maintenance in the ASEAN MEP services market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Labor Shortages and Certification Gaps | -1.5% | ASEAN-wide, most acute in Indonesia, Vietnam, Philippines | Long term (≥ 4 years) |

| Permitting Complexity and Regulatory Fragmentation | -0.8% | Indonesia, Vietnam, Thailand, moderate in Malaysia | Medium term (2-4 years) |

| Lowest-Bid Procurement Compressing Value-Added Scopes | -0.7% | Indonesia, Philippines, Thailand public sector | Medium term (2-4 years) |

| Power-Quality and Utility-Reliability Constraints Outside Core Hubs | -0.5% | Indonesia outside Java, Vietnam rural provinces, Myanmar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortages and Certification Gaps

Skilled labor shortages are a clear operating restraint for the ASEAN MEP services market because project pipelines are rising faster than the supply of engineers, BIM coordinators, commissioning specialists, and certified site teams. The problem is becoming more visible in digital infrastructure, transport, and advanced industrial projects, where tolerance for errors is low, and documentation burdens are high. It is also becoming more visible in markets moving toward Singapore-style digital submission and building-services compliance standards, as those frameworks raise the baseline for digital coordination and certified engineering sign-off. The result is a two-tier delivery environment where global firms and a limited group of better-capitalized regional contractors can access premium scopes, while many mid-tier local firms remain concentrated in less complex packages. Unless training and accreditation expand faster, labor scarcity will continue to limit the ASEAN MEP services market's efficiency in converting awarded work into on-time project completion.

Permitting Complexity and Regulatory Fragmentation

Permitting complexity remains a consistent drag on the ASEAN MEP services market outside the region’s most streamlined approval environments. The OECD notes that institutional fragmentation, complex land-ownership laws, and rigid approval timelines continue to deter private infrastructure investors across the ASEAN-5, thereby slowing project conversion even when end-user demand is strong. In the OECD sample, only 14 of 129 urban infrastructure projects used private equity, reflecting broader caution about approval risk and execution uncertainty. For MEP contractors, the problem is not only delayed groundbreaking; fragmented approvals also increase the risk of mid-project redesigns to electrical rooms, mechanical layouts, utility interfaces, and fire-safety systems. That pattern raises rework risk, delays commissioning, and compresses margins in countries where regulatory processes still move unevenly across ministries, utilities, and local authorities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mechanical Dominance Driven by Climate and Cooling Intensity

Mechanical services held 48.34% of the market in 2025, reflecting the fact that cooling, ventilation, and indoor environmental control remain the costliest building-system requirements across much of ASEAN countries. Tropical climate conditions keep HVAC central in commercial buildings, hospitality projects, mixed-use towers, and transport infrastructure, while advanced industrial sites add even tighter environmental specifications. Data centers, semiconductor facilities, and large transit assets also depend on high-performance mechanical systems because thermal stability and air quality affect both operations and compliance. Shinryo Indonesia’s project portfolio, spanning Branz Mega Kuningan in Jakarta and the Manyar Smelter in Surabaya, demonstrates the breadth of the mechanical scope across premium real estate and heavy industrial settings.

Integrated MEP services is the fastest-growing sub-segment, with an 8.1% CAGR from 2026 to 2031, and the ASEAN MEP services market for integrated solutions is growing as clients move toward single-point accountability for complex facilities. That shift is especially visible in digital infrastructure and advanced manufacturing projects where mechanical, electrical, plumbing, controls, and commissioning teams must work as one coordinated package. Electrical services continue to expand with industrial estates, transport systems, and utility-heavy buildings, while plumbing services are benefiting from more complex drainage, wastewater, fire-fighting, and water-reuse requirements in urban and infrastructure projects. Green Mark-style compliance structures are also raising the baseline technical standard across the full type landscape, which supports stronger demand for multidisciplinary delivery capability.

By Service Type: Design Anchors Value, But Maintenance Accelerates

Design & engineering commanded 36.34% of market value in 2025 because complex projects across transport, digital infrastructure, utilities, and industrial construction require critical building-services decisions well before physical construction begins. This part of the ASEAN MEP services market benefits from higher-value work, including system planning, code compliance, load analysis, energy modeling, and design coordination. Singapore’s CORENET X mandate has effectively raised the design-phase investment floor for major new projects, as digital coordination now sits within the approval path rather than outside it. Firms that can deliver accurate models, compliant documentation, and coordinated engineering packages, therefore, enter large tenders with a clearer competitive advantage.

Other services is the fastest-growing service sub-segment, with a 8.82% CAGR through 2031, as commissioning verification, performance testing, and energy-audit work become increasingly important as project complexity increases. Installation, testing, and commissioning still account for a large share of billings in the current build cycle because many transport, industrial, and digital assets are still in active construction. Maintenance & repair is also gaining weight as the installed base of complex systems expands and more building owners require planned preventive service rather than reactive repair. Shinryo Corporation’s SGD 436.8 million (USD 323 million) contract for tunnel ventilation and environmental control systems on Singapore’s Cross Island Line Phase 1 and Punggol Extension illustrates how large installation and systems-delivery packages can become on technically demanding transport projects.

By End-User Industry: Commercial Leads, Infrastructure Accelerates

Commercial held 41.23% of the ASEAN MEP services market in 2025 because office, retail, hospitality, mixed-use, and digital assets continue to cluster around Jakarta, Kuala Lumpur, Bangkok, Ho Chi Minh City, and Singapore. This segment remains the deepest source of project variety because it combines urban towers, hotels, shopping centers, airport-linked commercial space, and increasingly data-center campuses within the same regional pipeline. Data centers are now disproportionately influential in commercial work because cooling density, redundancy requirements, and electrical design depth are far above those of typical office fit-outs. Thailand-based ME PRIME describes its scope across offices, condominiums, hotels, and industrial facilities, which reflects the breadth of commercial and adjacent building-services activity that remains active across the region[2]ME PRIME Design and Engineering, “ME PRIME Home,” ME PRIME Design and Engineering, meprime.co.th.

Infrastructure is the fastest-growing segment of the ASEAN MEP services industry, with an 8.6% CAGR from 2026 to 2031, as transport, utility, and public service projects require large, system-heavy electromechanical packages. Vietnam identified 564 key national works in 2025, totaling more than VND 5.14 quadrillion (USD 205.6 billion), supporting a sustained pipeline of ventilation, power distribution, pumping, drainage, and fire-protection systems. Changi Airport Terminal 5 also illustrates the scale of infrastructure-led demand, with Mott MacDonald, SJ Group, and Arup serving as full engineering consultants on a major aviation asset designed to Green Mark Platinum Super Low Energy standards. Residential remains an important base-load segment, and the balance within this part of the market is shifting toward larger, developer-led packages rather than fragmented subcontracting structures.

Geography Analysis

Indonesia accounted for 33.22% of the ASEAN MEP services market in 2025, making it the region’s largest market. Its lead reflects broad construction volume across housing, mining-linked infrastructure, wastewater systems, and digital investment. The Zone 6 sewage treatment plant award in Jakarta highlights the depth of municipal utility need, especially in a city where sewerage coverage was only 12% at the time of contract award.

Indonesia’s digital economy gross merchandise value rose from USD 195 billion in 2022 to USD 263 billion in 2024, helping attract large-scale digital infrastructure and supporting associated cooling and electrical infrastructure. Power-quality constraints outside Java continue to weigh on electromechanical project execution in the outer islands, but the national demand base remains the broadest in the region.

Malaysia and Singapore together anchor some of the highest-value project opportunities in the ASEAN MEP services market because advanced manufacturing, high-spec commercial assets, and stringent compliance frameworks raise engineering intensity per project. Malaysia benefits from semiconductor and related manufacturing commitments, which are expanding demand for cleanroom HVAC, high-current electrical distribution, and specialist utility systems. Singapore’s CORENET X and Green Mark requirements are raising the technical and digital-delivery baseline for all firms that want to compete in the city-state, and that capability often transfers into projects elsewhere in ASEAN. Thailand and the Philippines also contribute meaningful volume, and Thailand’s ARAYA estate shows that integrated industrial utility campuses are widening the region’s pool of higher-spec MEP opportunities.

Vietnam is the fastest-growing geography in the ASEAN MEP services market at 8.19% CAGR from 2026 to 2031. The country’s construction sector contributed nearly 17% of GDP in 2025 and grew by more than 9% in the same year, which shows that volume growth is now being matched by greater project sophistication. Vietnam’s National Assembly approved a VND 8.22 quadrillion (USD 312 billion), medium-term public investment plan for 2026 to 2030 in May 2026, with transport, urban development, and energy infrastructure as core beneficiaries. The expansion of expressways, metro systems, and airport infrastructure will keep the country’s project mix favorable for tunnel ventilation, power systems, water management, and fire protection over the forecast period.

Competitive Landscape

The ASEAN MEP services market is moderately fragmented, with global engineering consultancies competing alongside regional contractors and country-level specialists. AECOM, WSP Global, Arup, Mott MacDonald, Aurecon, Meinhardt Group, Surbana Jurong, Shinryo Corporation, Obayashi Corporation, Gamuda, and Sunway Construction all operate across different parts of the regional opportunity set. AECOM’s appointment as owner’s engineer for Phase 2 of Singapore’s integrated waste management facility in May 2026 demonstrates how international firms continue to target technically complex public infrastructure projects with strong advisory, oversight, and commissioning content[3]AECOM, “AECOM Binnies and Ramboll Joint Venture Appointed for Phase 2 of Singapore’s Integrated Waste Management Facility,” AECOM, aecom.com. Mott MacDonald’s role as lead engineering consultant on the 600 MWac Bulan cross-border solar and battery storage project between Indonesia and Singapore illustrates a similar ability to secure complex multi-system energy work that requires high-confidence engineering coordination. No single player appears to dominate the ASEAN MEP services market, as major awards are distributed across owner’s engineer roles, design consultancies, bundled contractors, and specialist system integrators.

Regional firms are also moving beyond conventional subcontracting roles and using ASEAN delivery capabilities to pursue higher-value, longer-duration positions. Meinhardt Group and Surbana Jurong signed MoUs with Abu Dhabi’s Projects and Infrastructure Centre in November 2025, which showed that ASEAN-rooted engineering firms are increasingly exporting modular MEP, smart-city, and infrastructure planning expertise beyond their home region. Obayashi Corporation’s establishment of PT Obayashi Concession Indonesia and its acquisition of a stake in a central Jakarta toll-road operator in May 2026 point to a strategy that extends beyond pure construction into concession-linked infrastructure participation. These moves suggest that firms are trying to lock in recurring infrastructure exposure and deepen client relationships rather than compete only on one-off project awards.

Specialized execution remains a strong differentiator in the ASEAN MEP services market because high-value scopes increasingly sit in narrow technical categories. Shinryo Corporation’s Singapore rail ventilation contract shows how firms with deep experience in environmental control systems can defend strong positions in critical transport packages. Aurecon’s RICS Southeast Asia Project of the Year recognition for a modular data center in Johor shows that speed, prefabrication, and tight services coordination are becoming more important in winning complex digital-infrastructure work. WSP’s 2025 to 2027 strategy, which includes USD 200 million for research, innovation, and digital partnerships, also signals that major global players will keep investing in capability depth that can be applied to ASEAN’s higher-spec project pipeline.

ASEAN Mechanical, Electrical, And Plumbing (MEP) Services Industry Leaders

Meinhardt Group

Surbana Jurong

WSP Global

AECOM

Jacobs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AECOM, Binnies, and Ramboll JV were appointed by Singapore's National Environment Agency as owner's engineer for Phase 2 of the Integrated Waste Management Facility at Tuas Nexus, covering planning, design, procurement support, construction supervision, and testing and commissioning for a facility processing up to 2,900 tonnes of waste per day.

- May 2026: Obayashi Corporation announced the establishment of PT Obayashi Concession Indonesia (OCI) and the acquisition of a 12.5% stake in PT JTD Jaya Pratama, operator of a 31-km toll road concession in central Jakarta, for approximately JPY 6.8 billion (USD 45 million), with a further acquisition to a 48.8% stake planned for December 2027.

- November 2025: Meinhardt Group and Surbana Jurong signed MoUs with Abu Dhabi's Projects and Infrastructure Center (ADPIC) during the ADIS Roadshows 2025 in Singapore, contributing MEP prefabrication expertise and engineering consultancy capabilities to a USD 54+ billion Abu Dhabi infrastructure pipeline.

- October 2025: A JV comprising Obayashi Corporation, JFE Engineering, PT Wijaya Karya, and PT Jaya Konstruksi was awarded the contract for Zone 6 of Jakarta's Sewage Treatment Plant by the Indonesian Ministry of Public Works, to build a 47,500 m³/day treatment plant addressing Jakarta's approximately 12% sewerage coverage rate.

ASEAN Mechanical, Electrical, And Plumbing (MEP) Services Market Report Scope

The ASEAN MEP Engineering Services Market is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation & Commissioning, Maintenance & Repair, Other Services), and End-User Industry (Residential, Commercial, Infrastructure), and Geography (Indonesia, Malaysia, Thailand, Vietnam, Singapore, Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| Integrated MEP Services |

| Design & Engineering |

| Installation, Testing, and Commissioning |

| Maintenance & Repair |

| Other Services |

| Residential |

| Commercial |

| Infrastructure |

| Indonesia |

| Malaysia |

| Thailand |

| Vietnam |

| Singapore |

| Rest of ASEAN |

| Mainland ASEAN |

| By Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services | |

| Integrated MEP Services | |

| By Service Type | Design & Engineering |

| Installation, Testing, and Commissioning | |

| Maintenance & Repair | |

| Other Services | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| By Geography | Indonesia |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Singapore | |

| Rest of ASEAN | |

| Mainland ASEAN |

Key Questions Answered in the Report

What is the 2026 value of the ASEAN Mechanical, Electrical, and Plumbing services space?

The ASEAN Mechanical, Electrical, and Plumbing (MEP) Services Market is estimated at USD 16.69 billion in 2026 and is projected to reach USD 28.09 billion by 2031, growing at a CAGR of 10.97%.

Which type segment leads revenue across ASEAN MEP services?

Mechanical Services led the regional mix with a 48.34% share in 2025 because cooling, ventilation, and environmental control remain central across commercial, industrial, and transport assets.

Why is commercial demand still the largest source of work in ASEAN?

Commercial captured 41.23% in 2025 because office, retail, hospitality, mixed-use, and data-center assets remain concentrated in the region’s main urban hubs.

Which geography is expanding fastest through 2031?

Vietnam is the fastest-growing geography with an 8.19% CAGR, supported by strong construction growth and a large 2026 to 2030 public investment plan.

Page last updated on: