Lithium Hydroxide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

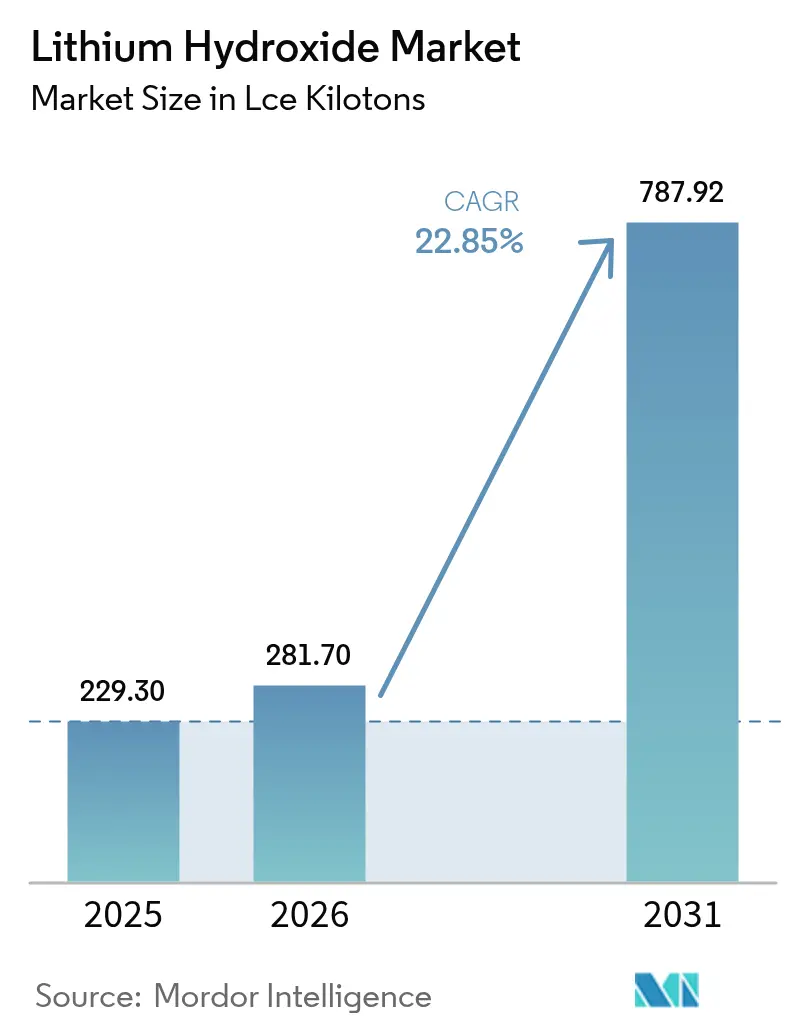

| Market Volume (2026) | 281.7 LCE kilotons |

| Market Volume (2031) | 787.92 LCE kilotons |

| Growth Rate (2026 - 2031) | 22.85% CAGR |

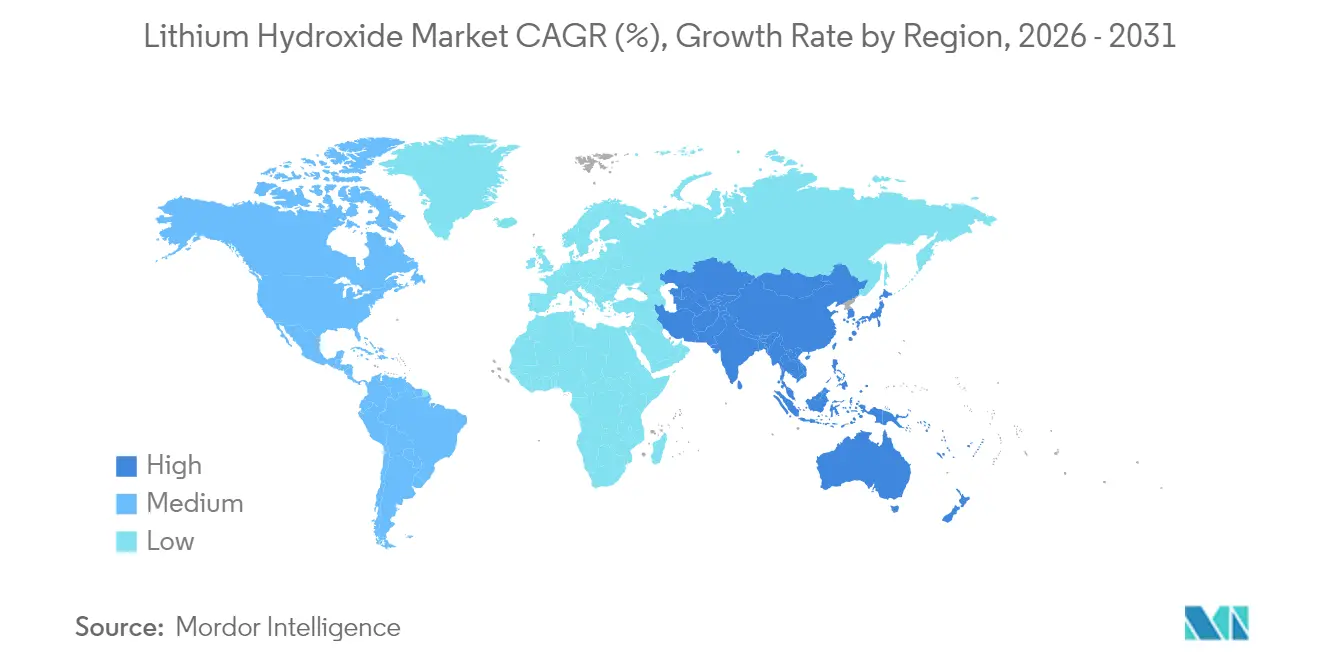

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lithium Hydroxide Market Analysis by Mordor Intelligence

Lithium Hydroxide market size in 2026 is estimated at 281.7 LCE kilotons, growing from 2025 value of 229.30 LCE kilotons with 2031 projections showing 787.92 LCE kilotons, growing at 22.85% CAGR over 2026-2031. Intensifying competition for battery-grade chemicals, fast-rising electric vehicle (EV) sales, and the rapid scale-up of direct lithium extraction (DLE) technologies are reshaping supply networks worldwide. Asia-Pacific commands the largest regional position with 40% of global consumption, delivering the fastest growth rate of 27.66% through 2030. Automakers locked in long-term procurement contracts in 2024 to secure high-purity feedstock, and several battery manufacturers accelerated vertical-integration strategies to hedge price swings. At the same time, stark feedstock price volatility—from USD 81,500/t to USD 22,500/t during 2023—continues to challenge project finance models.

Key Report Takeaways

- By application, lithium-ion batteries held 62.40% of 2025 revenue and are projected to expand at a 26.05% CAGR to 2031.

- By grade, battery-grade material captured 69.30% 2025 share; the same segment advances at a 24.90% CAGR through 2031.

- By form, monohydrate led with 64.20% of 2025 output; anhydrous records the fastest 25.10% CAGR over 2026-2031.

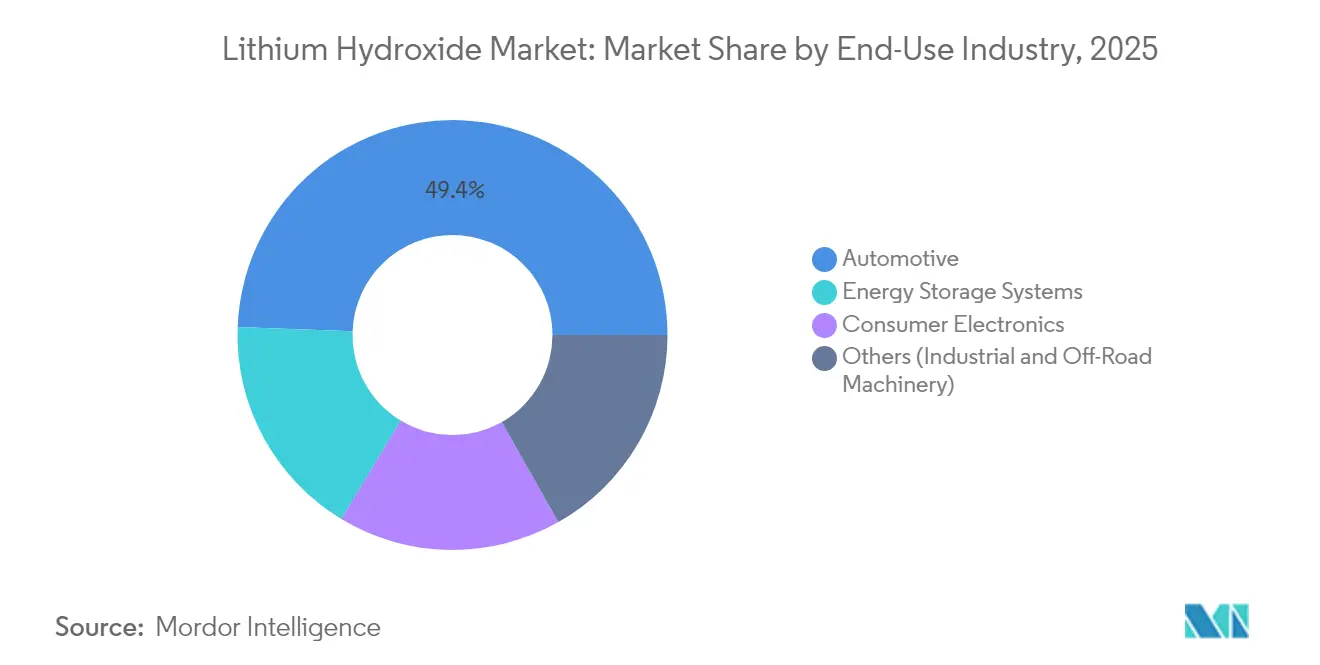

- By end-use industry, automotive accounted for 49.40% of the 2025 total; energy-storage systems grow fastest at 24.60% CAGR.

- By geography, Asia-Pacific commanded 39.60% 2025 share and also posts the highest 26.80% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lithium Hydroxide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Electric Vehicles | +8.50% | China, Europe, North America | Medium term (2-4 years) |

| Increasing Demand for Power Tools | +2.30% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Commercialisation of Direct Lithium Extraction (DLE) Unlocking Low-Cost Hydroxide Feedstock | +6.80% | Latin America, North America | Medium term (2-4 years) |

| OEM-Backed Long-Term Contracts De-Risking New Hydroxide Capacity in Latin America | +3.20% | Latin America (global supply chain effect) | Medium term (2-4 years) |

| Government Policies Supporting Battery Supply Chains | +5.70% | North America, Europe, India, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Power Tools

Cordless power tools are replacing corded alternatives in construction and industrial maintenance because lithium-ion packs deliver longer run-time and a superior power-to-weight ratio. Manufacturers have launched cell formats optimized for high-discharge cycles, a profile that favors lithium hydroxide-rich nickel–cobalt–manganese cathodes. Uptake is strongest among professional contractors in North America and Europe, where tight labor markets place a premium on productivity gains. Continuous adoption of building-information-modeling workflows further accelerates cordless tool penetration because crews require untethered mobility on-site. Though smaller than EV demand, this niche yields above-average price realization for hydroxide producers supplying specialty cathode blends.

Commercialization of Direct Lithium Extraction (DLE) Unlocking Low-Cost Feedstock

Field-scale success at IBAT’s Utah plant, utilizing modular adsorption columns, demonstrated 80-90% lithium recovery in hours versus the months needed for conventional pond evaporation. Project ATLiS in California secured a USD 1.36 billion conditional loan guarantee to deliver 20,000 t/y of lithium hydroxide from geothermal brine, affirming lender confidence in DLE scalability[1]U.S. Department of Energy, “Conditional Commitment for Project ATLiS,” energy.gov . Higher yields cut capital intensity per ton and enable operations in water-stressed regions because many ion-exchange and membrane variants consume less make-up water than pond systems. These economics bolster the long-run supply outlook for the lithium hydroxide market while reducing environmental footprints.

OEM-Backed Long-Term Contracts De-Risking New Capacity in Latin America

Automakers expanded direct participation in upstream deals during 2024 to lock in volumes and cost visibility. Hyundai’s multi-year offtake with Ganfeng, Rio Tinto’s USD 6.7 billion acquisition of Arcadium Lithium, and its subsequent USD 2.5 billion investment in an Argentine mine illustrate the strategic pivot. Binding commitments improve project-finance bankability, shorten payback periods, and underpin larger trains capable of achieving economies of scale—factors that collectively expand the lithium hydroxide market.

Government Policies Supporting Battery Supply Chains

Public-sector funding has shifted decisively toward localized battery ecosystems. The US Department of Energy earmarked USD 725 million for battery-materials processing grants and a separate USD 88 million for advanced-vehicle research in 2025. India’s Scheme for Manufacturing of Electric Cars grants concessional import duties to automakers investing USD 500 million in new EV plants on the condition of 50% domestic value addition[2]Investment Policy Monitor, “Incentives for EV Infrastructure,” investmentpolicy.unctad.org . Conversely, China’s draft export restrictions on battery and lithium processing technologies underscore geopolitical sensitivities and may reinforce regional supply diversification. Overall, these policy moves encourage upstream investment and accelerate the lithium hydroxide market’s installed capacity curve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Costs | -4.20% | Global | Medium term (2-4 years) |

| Feedstock Price Volatility Hindering Project Financing | -3.80% | Global (higher in emerging markets) | Short term (≤ 2 years) |

| Rising concern About the Toxicity | -2.10% | Europe, North America, developed APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Costs

Battery-grade lithium hydroxide plants demand sophisticated impurity control and costly crystallization circuits. Albemarle halted expansion of its Kemerton facility in Australia, slicing planned nameplate capacity in half and reducing onsite headcount by 40%. Multiyear payback periods, strict environmental licensing, and a limited pool of hydro-metallurgical talent maintain high entry barriers and slow new-build momentum, especially in regions with elevated energy tariffs.

Feedstock Price Volatility Hindering Project Financing

Lithium hydroxide prices fell 72% during 2023. Albemarle’s capex guidance dropped from USD 2.1 billion in 2023 to USD 1.6-1.8 billion for 2024, and the firm reported a USD 188 million net loss in Q2 2024 versus a USD 650 million profit a year earlier. Such swings translate into wider discount rates used by lenders and force developers to delay final investment decisions. If the investment gap persists, the lithium hydroxide market could confront supply shortfalls mid-decade when EV penetration accelerates again, creating another feedback loop of price spikes and project rushes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Battery segment cements dominance

Lithium-ion batteries generated 62.40% of 2025 demand and are forecast to expand at 26.05% CAGR through 2031. This segment alone accounts for the largest slice of the lithium hydroxide market size and delivers the highest incremental tonnage. Range-oriented chemistries such as nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminum (NCA) require lithium hydroxide for synthesis rather than carbonate, anchoring structural demand. In contrast, lubricating greases, purified-air systems, and specialty synthesis remain steady but modest contributors. Growing recycling mandates in the European Union are expected to generate a secondary supply channel later in the forecast period, tempering but not displacing primary demand.

Energy storage deployments form the fastest-rising sub-application. Large-scale battery farms linked to renewable assets need long cycle-life chemistries. Projects such as California’s multi-gigawatt-hour installations increasingly specify nickel-rich cathodes, reinforcing hydroxide consumption. As costs decline, smaller commercial and industrial behind-the-meter systems join the opportunity set, ensuring the lithium hydroxide market retains a diversified growth engine across stationary and mobile domains.

By Grade: Battery-grade purity premiums widen

Battery-grade material held a commanding 69.30% share in 2025 and posts a forecast 24.90% CAGR, the highest within this segmentation. Stringent impurity controls on sodium, calcium, and heavy metals underpin price differentials over technical grade. Manufacturers such as Livent have invested in additional recrystallization and ion-exchange modules to achieve less than 100 ppm aggregate impurity limits. That investment raises capital intensity but also deepens competitive moats. Technical grade serves grease and ceramic markets where tolerance thresholds are looser, while industrial grade addresses water treatment and select synthesis routes.

The lithium hydroxide market share for battery-grade will keep rising as OEM specification sheets lengthen. Next-generation solid-state and high-silicon-anode designs rely on precise stoichiometry and ultra-low moisture content, factors that amplify quality premiums. Producers with vertically integrated brine or hard-rock feedstock plus in-house purification are best placed to capture this margin pool.

By Form: Monohydrate maintains lead; anhydrous accelerates

Monohydrate (LiOH·H₂O) controlled 64.20% output in 2025 due to its relative stability and nondeliquescent nature during shipping. Production typically involves reacting lithium carbonate with calcium hydroxide, yielding crystals with about 57% active LiOH content. Anhydrous material, free of structural water, contains higher LiOH per unit weight and is preferred for moisture-sensitive cathode or electrolyte recipes. Although more challenging to produce, it grows at 25.10% CAGR through 2031, outpacing monohydrate as demand for advanced cell chemistries rises.

Process innovations facilitate flexible conversion between forms, enabling plants to pivot output mix in line with order books. Over 2025-2027 several Chinese and South Korean refineries plan debottlenecking projects aimed at higher anhydrous yields, broadening supply options for the lithium hydroxide market.

By End-Use Industry: Automotive leads, energy storage races ahead

Automotive OEMs consumed 49.40% of 2025 tonnage, reflecting soaring EV unit sales and rising average battery capacities. Vehicle makers are embedding lithium supply in overall electrification strategies, with Albemarle, SQM, and Ganfeng all striking multi-year supply agreements with global brands. Consumer electronics, spanning smartphones, laptops, and wearables, remains the next largest end user but posts slower growth as battery pack energy density rises faster than device sales volumes.

Grid-level energy storage systems record the strongest 24.60% CAGR through 2031, supported by government tender pipelines and renewable integration targets. Off-highway equipment manufacturers are beginning to electrify mining trucks and agricultural machinery, a trend that will add another demand leg in the back half of the decade. Together these shifts maintain strong multi-segment fundamentals for the lithium hydroxide market.

Geography Analysis

Asia-Pacific, with a 39.60% lithium hydroxide market share in 2025, benefits from unrivaled cell-manufacturing capacity and a dense cluster of downstream cathode, anode, and pack assemblers. Chinese policy directives now favor domestic sourcing, prompting active development of inland salt-lake brine as well as overseas equity stakes, while Japan and South Korea leverage long-standing material science expertise to stay competitive. India entered the fray with a National Manufacturing Mission and duty exemptions for critical minerals under the 2025-26 Union Budget, stimulating local hydroxide conversion proposals.

North America’s expansion rests on large-scale funding packages. The DOE’s USD 150 million grant to Albemarle supports a spodumene concentrator at Kings Mountain capable of feeding 1.6 million EVs annually. Hyundai Motor Group and SK On approved a USD 5 billion battery cell plant in Georgia, anchoring regional cathode demand for locally produced hydroxide. These initiatives aim to cut reliance on Asian supply chains and meet US Inflation Reduction Act sourcing thresholds.

South America remains the primary feedstock hub. Chile’s National Lithium Strategy invites private participation while safeguarding state oversight, and new geological surveys lifted estimated reserves by 28%. Argentina attracted Rio Tinto’s USD 2.5 billion mine investment and multiple OEM offtakes. Brazil saw EV sales jump 85% in 2024, led by BYD with 70% share, hinting at future domestic hydroxide conversion requirements.

Europe accelerates capacity with stringent CO₂ regulations and comprehensive recycling mandates. Germany spearheads R&D on next-generation cathodes, while the EU Battery Regulation sets minimum lithium recovery quotas from 2025 onward. Several greenfield conversion plants in Finland, France, and Portugal are scheduled for commissioning by 2027, adding diversity to the lithium hydroxide market supply base. The bloc’s push for strategic autonomy may reshape trade flows, especially if China enacts proposed technology export restrictions.

Regulatory Landscape

Policy is increasingly shaping where lithium hydroxide is extracted, processed, and qualified for downstream battery supply chains. In the European Union, the Batteries Regulation (Regulation (EU) 2023/1542) and the Critical Raw Materials Act (Regulation (EU) 2024/1252) reinforce localization objectives: the CRMA sets 2030 benchmarks including 40% of strategic raw material processing and 25% of recycling to be done within the EU, which directly encourages regional conversion and recycling capacity for lithium salts used in cathode supply.

In the United States, the Inflation Reduction Act Section 30D EV credit ties eligibility to critical-minerals sourcing, with a 70% threshold in 2026 for the value of critical minerals in an EV battery to be extracted or processed in the US or a free-trade-agreement partner. US Treasury final regulations issued in 2024 also shifted compliance toward a traced qualifying value approach (with a transition that allows the prior value-added test until January 1, 2027), increasing documentation and chain-of-custody requirements for battery-grade lithium hydroxide. Separately, hazard and chemical-management scrutiny is tightening in Europe, where lithium salts face potential reproductive-toxicity reclassification pathways that would increase CLP/REACH compliance obligations for manufacturers and users handling lithium hydroxide.

Value Chain Analysis

The lithium hydroxide value chain starts with lithium-bearing feedstocks (hard-rock spodumene concentrates and brines), followed by extraction and concentration, chemical conversion to lithium hydroxide (commonly via carbonate intermediates or integrated conversion routes), and purification and crystallization to battery-grade monohydrate or anhydrous forms. The product then moves through bulk and specialty logistics, including controlled moisture handling for battery-grade material, to cathode active material producers and cell makers. Demand concentrates in Asia-Pacific, where downstream battery and cathode ecosystems are densest. Typical participants include upstream miners and brine producers (Australia, Chile, Argentina, Brazil, and emerging African sources), converters and refiners (with heavy concentration in China), distributors, and OEM-linked procurement desks that increasingly require traceability and specification compliance.

Recent events reflect both diversification efforts and operational bottlenecks. Albemarle announced idling of Train 1 at its Kemerton lithium hydroxide plant in Western Australia in February 2026, highlighting utilization and cost-curve pressures in ex-China conversion. New conversion and processing nodes are also being developed to broaden feedstock and midstream options, including commissioning of a 6,000 metric tonne per day lithium processing plant in Nasarawa, Nigeria (July 2026) and announced plans for the United Kingdoms first lithium hydroxide refinery at the Billingham Chemical Complex by Tees Valley Lithium (June 2026, 25,000 tpa, targeted startup 2028). Across the chain, commissioning timelines, technical complexity in sustaining battery-grade quality outside established hubs, and shifts in cathode chemistry mix remain key constraints that shape contracting structures and inventory strategies.

Competitive Landscape

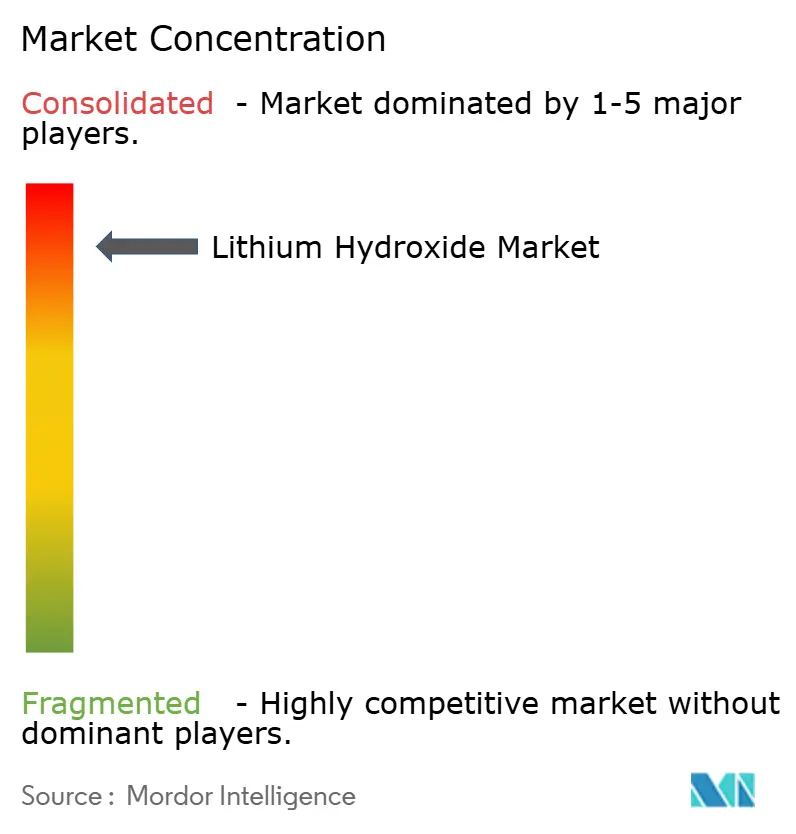

The lithium hydroxide market exhibits highly consolidated concentration, with the top five producers controlling over half of global conversion capacity. Albemarle implemented an integrated functional structure in late 2024 and reprioritized capex to assets with strong cost curves, particularly in the US and Chile.

Consolidation momentum intensified when Rio Tinto offered USD 6.7 billion for Arcadium Lithium, combining hard-rock and brine assets and projecting a 130% capacity lift by 2028. Vertical integration is another defining theme: several cathode manufacturers now co-invest in upstream hydroxide lines to secure quality and volumes. Chinese mid-tier firms such as Yahua Industrial and Chengxin Lithium inked multiyear contracts with Korean battery assemblers, reflecting a pivot toward regionalized supply relationships.

Innovation remains a key differentiator. Producers are piloting low-carbon process heat using renewable power and exploring sodium-sulfate by-product valorization. Select players are trialing hybrid DLE–conversion flowsheets blending brine extraction and conventional refining to cut energy intensity, signaling that technological leadership will shape long-run margins across the lithium hydroxide market.

Lithium Hydroxide Industry Leaders

Albemarle Corporation

SQM S.A.

Ganfeng Lithium Group Co. Ltd.

Tianqi Lithium Corporation

Arcadium Lithium

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are centered on compliant, localized, and lower-carbon lithium hydroxide supply that aligns with evolving EV-battery sourcing rules and European raw-material resilience programs. The EU Critical Raw Materials Act (Regulation (EU) 2024/1252) sets 2030 targets for in-region processing (40%) and recycling (25%) of strategic raw materials, creating whitespace for European conversion and recycling-linked hydroxide supply, especially where projects can build on existing chemical infrastructure. In Germany, Vulcan Energy commenced construction in April 2026 on its Lionheart central lithium chemical plant at Infraserv Industrial Park Hochst in Frankfurt, targeting 24,000 tonnes of lithium hydroxide monohydrate capacity, as an example of integrated, in-region conversion capacity being developed for European cathode and cell demand.

Qualification and traceability requirements are also becoming a commercial differentiator for battery-grade suppliers. In the United States, IRA Section 30D requirements reach 70% qualifying critical-minerals content in 2026, and the 2024 Treasury rules emphasize traced qualifying value, reinforcing demand for auditable supply chains and long-term offtakes that can be defended in procurement compliance. On the supply side, recent capacity actions and investments show continued reshaping of the global conversion footprint: POSCO completed a second lithium hydroxide plant at the Yulchon Industrial Complex in Gwangyang in November 2025, lifting total capacity to 43,000 tonnes per year, while Albemarle moved to idle its Kemerton hydroxide operations in February 2026, tightening focus on assets that fit cost and demand realities. These shifts increase opportunities for flexible converters (monohydrate and anhydrous capability), projects with secured feedstock and binding offtakes, and suppliers that can document emissions and provenance attributes sought by OEM and battery customers.

Recent Industry Developments

- June 2026: Alkemy Capital Investments PLC signed a five-year binding offtake agreement with a Glencore plc subsidiary for supply of 25,000 to 50,000 tonnes of battery-grade lithium hydroxide from the planned Tees Valley Lithium refinery in the United Kingdom. The contract structure links upstream financing and project credibility to a committed downstream counterparty, supporting bankability for new ex-China conversion capacity. It also reinforces the trend toward contracted, regionally anchored supply for battery-grade chemicals.

- February 2026: Albemarle announced plans to idle its Kemerton lithium hydroxide processing plant in Western Australia, after earlier suspension of operations, to improve financial flexibility and align output with market conditions. The move highlights the operational leverage converters face when lithium chemical pricing and demand mix shift. It also increases the strategic value of low-cost, reliably qualified capacity for battery-grade customers seeking continuity of supply.

- January 2024: Livent and Allkem merged to form Arcadium Lithium, creating a larger integrated lithium producer with expanded lithium chemicals capabilities across multiple regions. The combination strengthened access to diversified feedstocks and conversion assets, supporting more integrated contracting with battery and automotive customers. It also contributed to higher market concentration among leading lithium hydroxide suppliers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the lithium hydroxide market covers the sale and consumption of lithium hydroxide (including monohydrate) as a chemical input across battery materials and industrial uses, measured on a consistent lithium carbonate equivalent (LCE) basis and tracked across major producing and consuming regions.

Scope exclusions: This sizing does not count upstream lithium mining value, or downstream battery cell and cathode material value, beyond the lithium hydroxide portion.

Segmentation Overview

- By Application

- Lithium-ion Batteries

- Lubricating Greases

- Purification

- Other Application (Polymer and Specialty Chemical Synthesis)

- By End-use Industry

- Automotive

- Consumer Electronics

- Energy Storage Systems

- Others (Industrial and Off-Road Machinery)

- By Grade

- Battery Grade (Greater than or equal to 56.5% LiOH·H₂O)

- Technical Grade

- Industrial Grade

- By Form

- Monohydrate

- Anhydrous

- By Geography

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a fact base around lithium supply, conversion, and demand signals that can be checked year by year. Public sources that help anchor these checks include data and publications from the US Geological Survey, the International Energy Agency, UN Comtrade, and OECD trade statistics, followed by peer-reviewed work on lithium conversion chemistry and refining yields.

We also review company filings and investor decks for producers and converters, along with customs and port commentary carried by business press sources, which we use to spot commissioning delays, utilization changes, and contract behavior. Where needed, paid subscriptions for company financials and intelligence, import-export shipment-level records, and patent databases are used to confirm timelines and test directional claims. The specific examples listed here are not exhaustive, and additional public sources were referenced to collect, cross-check, and clarify the data.

Primary Interviews and Surveys

Primary work is used to translate public signals into realistic operating assumptions, especially on conversion yields, product mix (technical versus battery grade), and near-term supply availability. We speak with a balanced mix of producers, converters, distributors, and large end users, and we validate regional differences across APAC, EMEA, and the Americas so the model does not over-apply one region's pricing or ramp-up pattern to another.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 47% |

| Mid tier: 57% | Functional/Unit leaders: 30% | EMEA: 34% |

| Smaller Players: 14% | Managers: 57% | Americas: 19% |

Market-Sizing & Forecasting

The core sizing is built from a top-down demand pool that reconstructs lithium hydroxide consumption using battery and industrial pull factors, and then converts the outcome into LCE kilotons for consistency across countries. In practice, we track indicators such as EV and battery production ramp-ups, cathode chemistry shifts toward high-nickel formulations, lithium hydroxide conversion capacity additions, typical plant utilization ranges, and observable import-export movements that indicate where material is being sourced.

Once these totals are formed, they are corroborated with selective bottom-up approximations, such as sampling supplier volumes in key corridors, checking realized pricing ranges against contract commentary, and running volume times ASP reasonableness checks for major applications. Where a region appears overstated, we adjust the final number by reconciling these checks with trade and capacity timing. When a country-level data gap exists, proxy logic is applied using trade flows and known demand centers, before being filtered through interview feedback. Forecasts are developed using scenario analysis tied to commissioning schedules, utilization ramp curves, and battery demand outlooks, with explicit assumptions so they can be re-run as new capacity or demand information emerges.

Data Validation & Update Cycle

Validation is handled through multiple checks so single-source noise does not drive the final market size. Model outputs are compared against independent signals such as announced conversion capacity, trade direction, and demand growth markers, and then outliers are reviewed to confirm whether they reflect a real shift or a timing issue.

Before sign-off, a separate analyst review is performed, and follow-up calls are triggered when a large variance appears in a key input such as utilization, conversion yield, or a major project start date. The report is refreshed annually, and interim updates are made when material events occur, such as a major capacity commissioning change or a sharp movement in lithium chemical pricing. Right before delivery, a final refresh pass is done so clients receive the latest consistent view.

Mordor Intelligence's Lithium Hydroxide Market Size Measured Against Other Published Estimates

Published market sizes for lithium hydroxide can look far apart because the underlying unit of measure, boundary, and timing are not always aligned. Some sources report value in USD, while others size the market in volume terms like LCE, and the choice alone can widen the spread.

By tracking conversion capacity, utilization, and LCE-based demand checks, Mordor Intelligence keeps the estimate tied to physical consumption signals instead of price-led swings, which can shift USD market values sharply even when tonnage growth is steady.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.28 B (2026) | |

| Global Consultancy A | USD 1.44 B (2024) | The estimate is value-based and can be heavily influenced by lithium chemical pricing in the chosen base year, and the scope may bundle adjacent lithium chemicals or grades without a clear LCE normalization. |

| Industry Publisher B | USD 1.70 B (2025) | A longer-range outlook is presented with broad assumptions, and the value series can differ due to currency timing and a higher reliance on averaged prices rather than plant ramp-ups and regional trade checks. |

Looking at the table, the differences mainly come from whether the market is expressed in physical volume versus USD value, and how each source treats price volatility, grade mix, and timing. A model that stays traceable to capacity additions, utilization, and demand pull indicators is easier to refresh and repeat, which helps teams compare scenarios without mixing incompatible scopes.

Key Questions Answered in the Report

What is the current size of the lithium hydroxide market?

The market is valued at 281.7 LCE kilotons in 2026 and is projected to rise to 787.92 LCE kilotons by 2031, reflecting a 22.85% CAGR.

Why is lithium hydroxide preferred over lithium carbonate in batteries?

High-nickel cathodes such as NCM and NCA require lithium hydroxide to achieve higher energy density and faster charging, which is why automakers increasingly favor it.

How will direct lithium extraction affect supply?

Commercial DLE plants achieve up to 90% recovery and shorter processing times, lowering costs and unlocking resources previously considered uneconomic, thereby expanding global supply.

Which region leads lithium hydroxide demand growth?

Asia-Pacific leads both in 2025 consumption share (39.60%) and growth rate (26.80% CAGR to 2031) due to its extensive battery manufacturing base.

What are the main challenges facing lithium hydroxide producers?

High capital costs for battery-grade purity and extreme price volatility complicate project financing and can delay capacity expansions.

How are governments supporting domestic lithium hydroxide production?

Measures include the US DOE’s multi-hundred-million-dollar grants for processing plants and India’s duty incentives for EV manufacturers, while some countries, notably China, contemplate technology export restrictions.

Page last updated on: