Magnetic Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

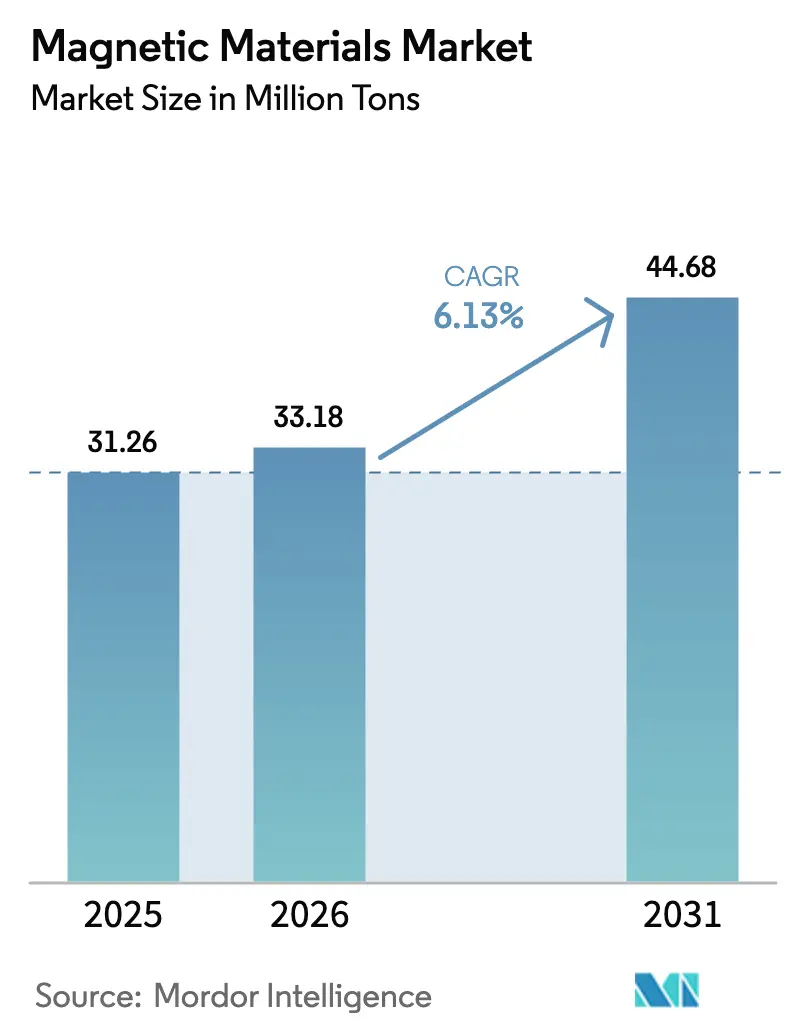

| Market Volume (2026) | 33.18 Million tons |

| Market Volume (2031) | 44.68 Million tons |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

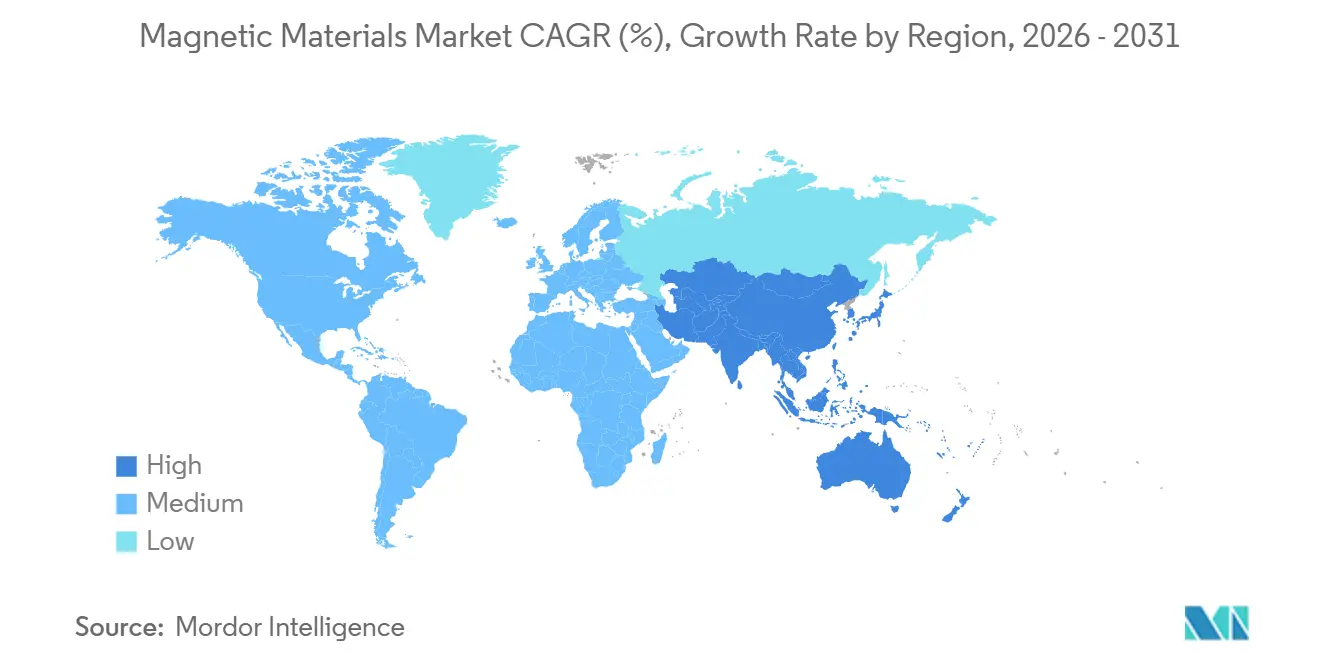

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

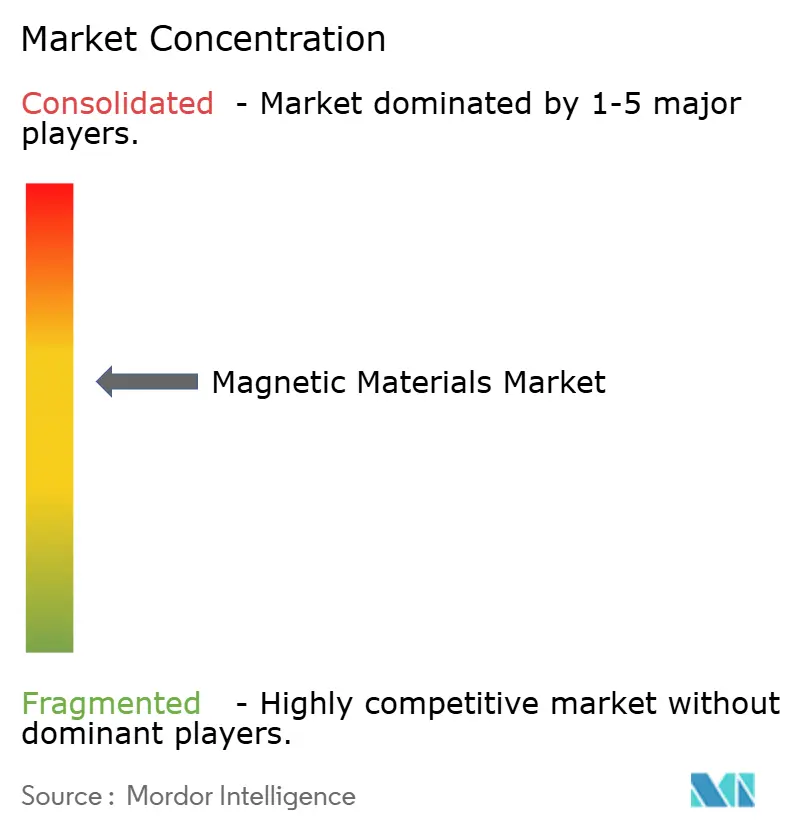

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnetic Materials Market Analysis by Mordor Intelligence

The Magnetic Materials Market size was valued at 31.26 Million tons in 2025 and is estimated to grow from 33.18 Million tons in 2026 to reach 44.68 Million tons by 2031, at a CAGR of 6.13% during the forecast period (2026-2031). Demand is rising as automakers shift from induction drives to permanent-magnet traction motors, wind-turbine OEMs embrace direct-drive architectures, and hyperscale data centers adopt nanocrystalline cores for high-frequency power conversion. Each end-use prefers a different alloy—NdFeB for torque density, ferrite for cost-sensitive gadgets, and amorphous ribbons for switching speed—so headline growth masks margin pressure in specialty grades. Asia-Pacific dominates because China owns most sintering capacity, Japan leads grain-boundary diffusion know-how, and South Korea scales MRAM fabs that consume high-purity targets. Western buyers are reacting to export-control risk by dual-sourcing and exploring recycling, yet oxide prices remain elevated, reinforcing the region’s cost advantage.

Key Report Takeaways

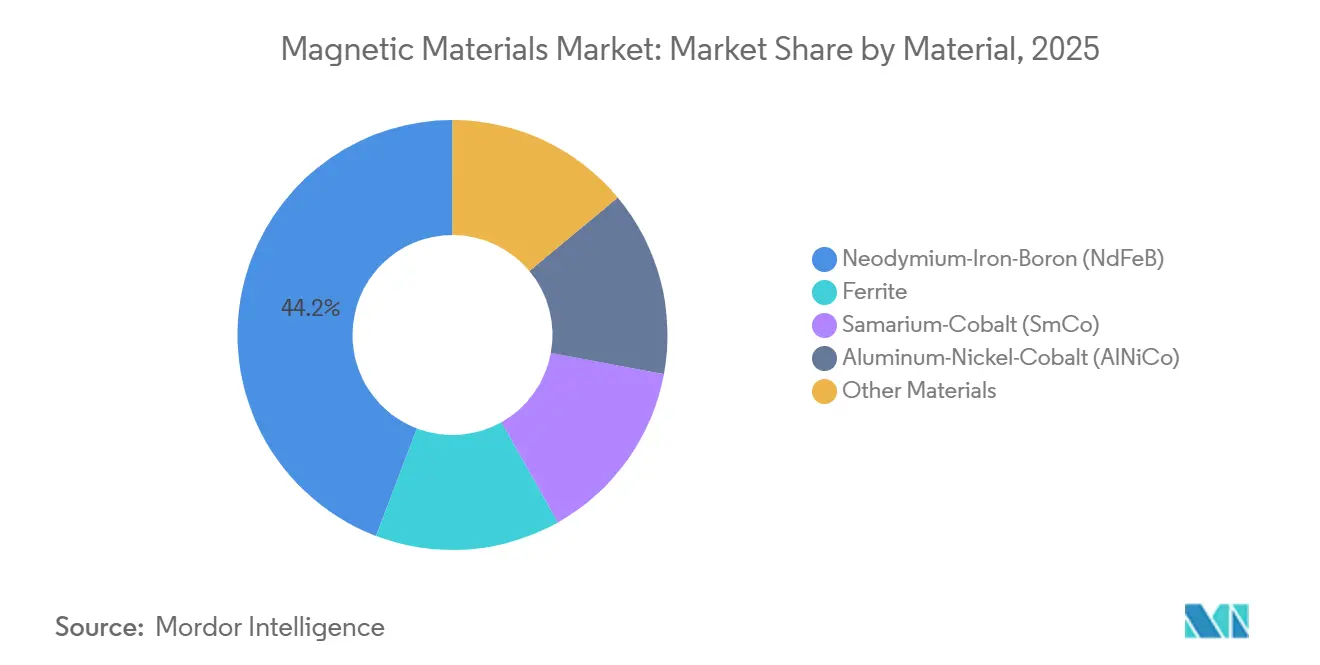

- By material, Neodymium-Iron-Boron (NdFeB) led with 44.21% Volume share in 2025; ferrite is projected to expand at a 6.28% CAGR to 2031.

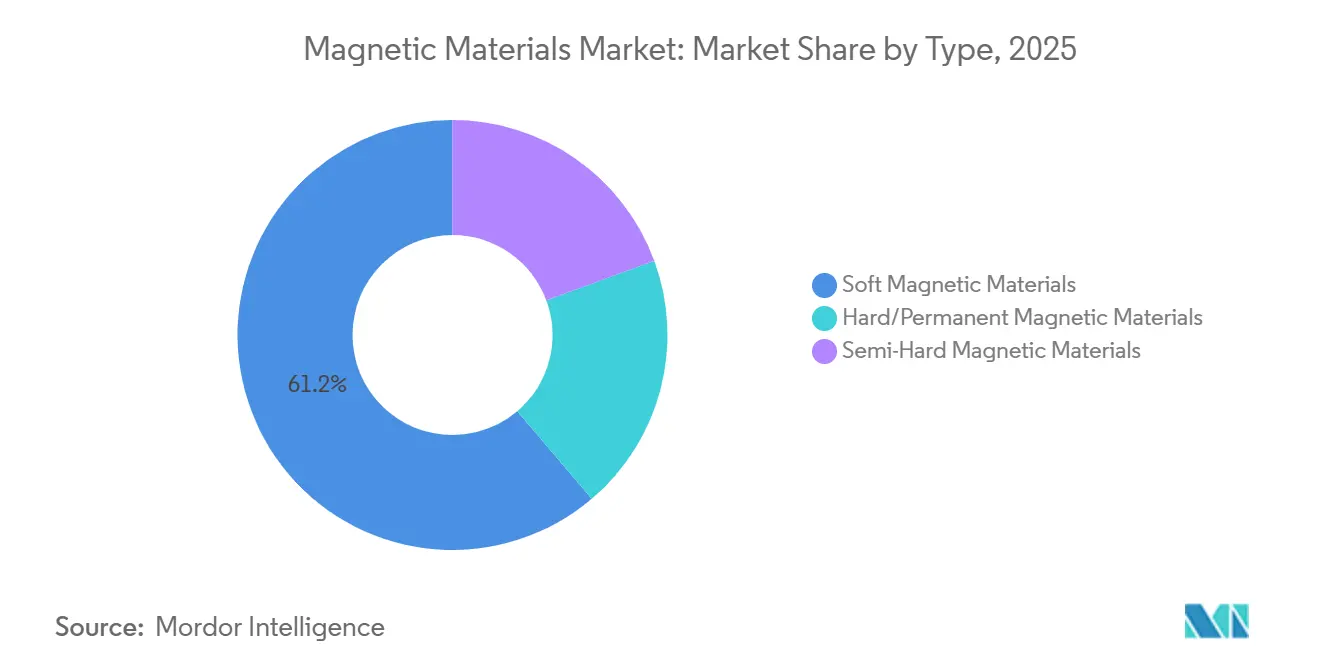

- By type, soft magnetic materials held 61.23% share of the magnetic materials market size in 2025, while hard/permanent magnets are advancing at a 6.98% CAGR through 2031.

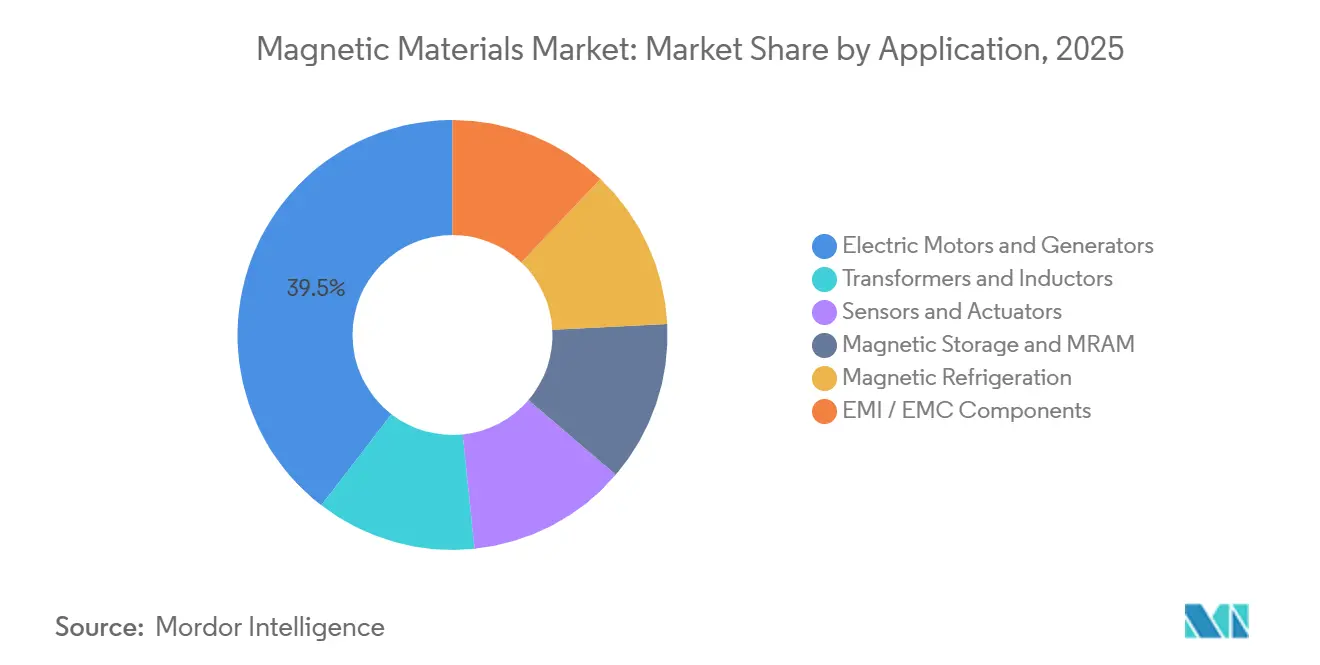

- By application, electric motors and generators commanded 39.55% share in 2025 and are forecast to grow at a 6.78% CAGR to 2031.

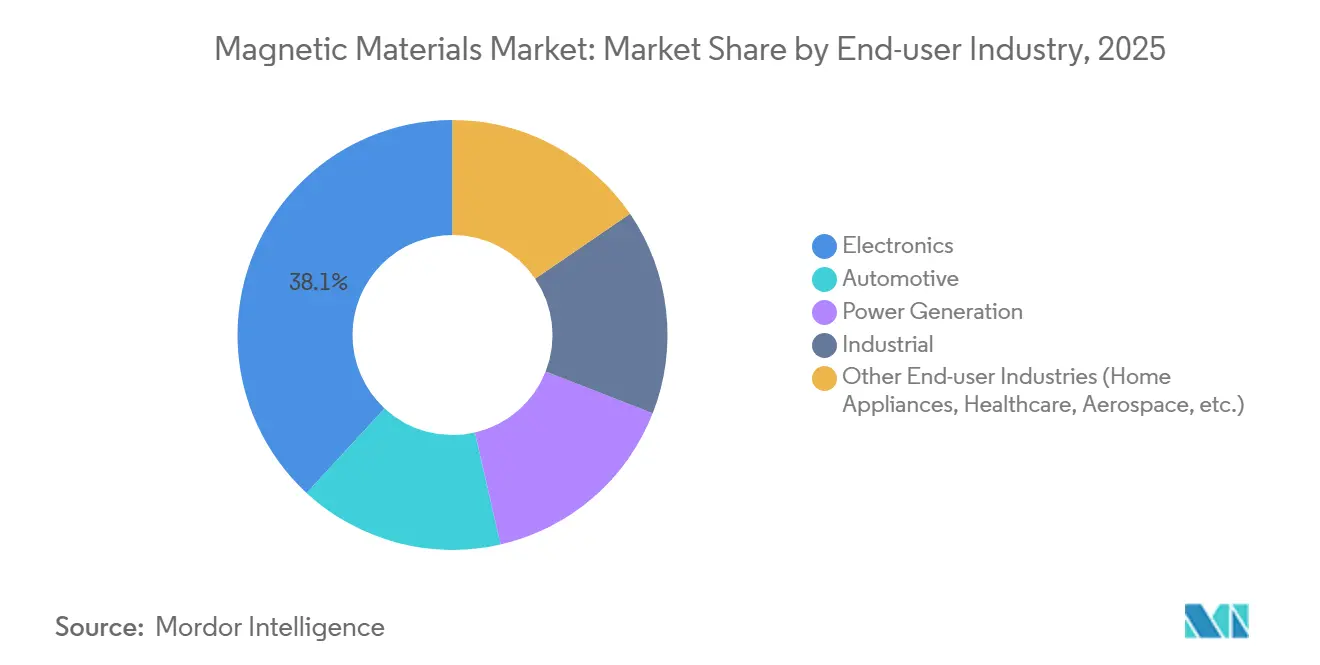

- By end-user industry, electronics accounted for 38.13% share in 2025, whereas automotive is expected to register a 7.95% CAGR through 2031.

- By geography, Asia-Pacific captured 67.23% of magnetic materials market share in 2025 and is expanding at a 7.77% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Magnetic Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Electric Vehicle Adoption Fuels Demand for Magnetic Materials | +1.8% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| Grid-Scale Wind-Turbine Gearless Generators Adoption | +1.2% | Global, concentrated in China, US, Europe offshore markets | Long term (≥ 4 years) |

| AI-Enabled Factory Automation Boosts Sensor Magnets | +0.9% | APAC core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Growing Robotics and Automation Usage Accelerates Magnetic Materials Demand | +0.7% | Global, with early gains in Japan, South Korea, Germany | Medium term (2-4 years) |

| High-Frequency Power Electronics Need Nanocrystalline Cores | +0.6% | North America and Europe data-center hubs, APAC manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Electric Vehicle Adoption Fuels Demand for Magnetic Materials

Battery-electric vehicles consumed 2,800 tons of NdFeB magnets in 2024 and are projected to exceed 8,000 tons by 2030 as annual EV sales approach 30 million units[1]International Energy Agency, “Global EV Outlook 2025,” iea.org . Permanent-magnet synchronous motors achieve peak efficiencies above 96%, prompting OEMs to spend on rare-earth grades to extend driving range without larger batteries. Tesla’s 4680-cell design and BYD’s Blade pack both use multi-motor layouts that double magnet content per vehicle versus single-motor cars. China built 9.5 million EVs in 2025, absorbing most domestic sintered-magnet output and tightening export supply. European platforms moving to 800-volt architectures require high-coercivity magnets able to withstand thermal demagnetization, which lifts dysprosium demand in the magnetic materials market.

Grid-Scale Wind-Turbine Gearless Generators Adoption

Direct-drive turbines remove gearboxes and cut mechanical losses by 2-3 percentage points, extending service intervals from six to eighteen months. Goldwind’s 16 MW offshore unit contains about 12 tons of NdFeB, and 2026 offshore additions of 40 GW could draw roughly 30,000 tons of magnets. China supplies 60% of global turbines, so most magnet demand originates domestically even for projects installed abroad. Siemens Gamesa and Vestas trial recycled NdFeB, yet closed-loop material remains under 5% of consumption because reprocessing degrades flux up to 15%. North Sea operators now specify corrosion-resistant coatings that add USD 2-3 per kilogram but cut crane-vessel repair costs over 25-year lifecycles.

AI-Enabled Factory Automation Boosts Sensor Magnets

Collaborative robots shipped 50,000 units in 2025, each embedding 8-12 magnetic encoders for sub-degree joint control. Sensor magnets are usually samarium-cobalt or bonded NdFeB because they must stay calibrated from -40 °C to 150 °C, a range ferrite cannot handle. Rising labor costs in China’s coastal provinces are accelerating adoption of pick-and-place robots that need miniature magnets for linear actuators. Japan’s FANUC and Germany’s KUKA demand ISO 9001-certified magnet traceability, an edge for established suppliers like TDK and Proterial in the magnetic materials market. Short replacement cycles in electronics manufacturing keep annual sensor-magnet demand climbing even when handset volumes plateau.

High-Frequency Power Electronics Need Nanocrystalline Cores

AI inference clusters run power supplies switching at 500 kHz to 1 MHz, frequencies where silicon-steel cores suffer prohibitive eddy losses. Nanocrystalline ribbons with sub-20 nm grains slash core loss to below 10 W/kg at 100 kHz—one-fifth that of conventional steel—making them the default in 48 V bus converters. VACUUMSCHMELZE’s VITROPERM and Hitachi Metals’ FINEMET are sold out through mid-2026 as AI capex tops USD 200 billion annually. Hyperscalers prioritize footprint and thermal margins, so they pay the premium for nanocrystalline even when amorphous alloys are cheaper. Amorphous ribbon therefore sticks to lower-frequency distribution transformers, leaving high-frequency dominance to nanocrystalline grades in the magnetic materials market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| REE Mining ESG Backlash Intensifies in OECD Nations | -0.8% | North America, Europe, Australia | Medium term (2-4 years) |

| China Export-Control Risk on Nd and Dy Oxides | -1.1% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Slow Scale-Up of Closed-Loop NdFeB Recycling | -0.4% | Global, with pilot projects in Japan, EU, US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

REE Mining ESG Backlash Intensifies in OECD Nations

Permitting for new rare-earth mines in the United States and Australia now averages 7-10 years, double the 2015 timeline, because regulators require perpetual tailings-water treatment bonds. Lynas paused its Kalgoorlie refinery expansion for 18 months while negotiating residue-disposal terms, proving even brownfield projects face social-license delays. Environmental groups have sued MP Materials over radionuclide discharge at Mountain Pass, elevating compliance costs in the magnetic materials market. The EU’s Critical Raw Materials Act demands 10% local supply by 2030, yet no new European mine is online, forcing the bloc to rely on toll refining in Asia. These headwinds are nudging OEMs toward magnet-free motor designs that trade 3-5% efficiency for rare-earth independence when neodymium oxide tops USD 80/kg.

China Export-Control Risk on Nd and Dy Oxides

Beijing imposed licensing on gallium, germanium, and antimony in 2023 and has signaled rare-earth oxides could follow if geopolitical frictions intensify. Although Nd and Dy are not quota-bound yet, voluntary shipment cuts during past disputes spiked prices 40-60% in weeks. Japanese magnet giants Shin-Etsu and TDK hold six-month oxide stocks, tying up working capital worth 15-20% of annual revenue to buffer shocks. The U.S. CHIPS and Science Act earmarked USD 3 billion for domestic separation, but no plant can yet deliver battery-grade neodymium oxide, leaving defense primes dependent on federal stockpiles. South Korea’s POSCO and Australia’s Iluka plan a USD 1.2 billion refinery by 2027, yet feedstock hinges on stable monazite exports from Western Australia, itself vulnerable to policy shifts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: NdFeB Dominance Meets Ferrite’s Cost Advantage

Neodymium-Iron-Boron (NdFeB) commanded 44.21% of 2025 volume, reflecting its unmatched energy product that lets motor makers halve rotor size without losing torque. That dominance locks in premium pricing, yet rising dysprosium cost keeps OEMs searching for alternatives in the magnetic materials market. Ferrite is slated to grow at a 6.28% CAGR through 2031 as handset makers replace bonded NdFeB with injection-molded ferrite in haptic and charging modules, trading 20% performance for zero rare-earth risk. Samarium-cobalt serves niche aerospace and downhole-tool markets above 200 °C, where NdFeB loses flux; volumes stay under 3,000 tons, but prices above USD 100/kg keep profitability intact. AlNiCo is useful mainly in legacy sensors and musical pickups, while electrical steel drives high demand thanks to transformers and motor laminations, anchoring the magnetic materials market. Premium nanocrystalline ribbons win high-frequency slots in data-center PSUs, a pocket of outsized margin amid commodity tonnage.

By Type: Soft Materials Lead Volume, Hard Magnets Lead Growth

Soft magnetic materials held 61.23% tonnage in 2025, buoyed by transformer cores, inductors, and stator laminations that cycle magnetization thousands of times per second. Grain-oriented electrical steel is enjoying fresh investment because utilities target lower no-load losses in distribution transformers. Hard/permanent magnets, however, are expanding at a 6.98% CAGR through 2031, because each electric vehicle, wind turbine, or industrial robot adds multiple permanent-magnet motors, accelerating growth in the magnetic materials market. Semi-hard grades, with intermediate coercivity, are being squeezed out as designers either jump to NdFeB for permanent bias or retreat to ferrite for switchable fields. Global efficiency rules (IE4/IE5) almost require permanent magnets to meet regulatory thresholds, reinforcing the tilt toward hard materials. Meanwhile, USB Power Delivery chargers drive more soft-ferrite demand for high-flux inductors in consumer electronics.

By Application: Motors and Generators Anchor Demand

Electric motors and generators absorbed 39.55% of the 2025 volume and are set to grow 6.78% to 2031 because motors consume 45% of global electricity, so each efficiency gain saves gigawatt-hours at the grid scale. Direct-drive wind turbines and multi-motor EV platforms magnify unit magnet usage, entrenching this application as the magnetic materials market’s demand bedrock. Transformers and inductors’ demand is fuelled by renewable-energy inverters and grid-modernization programs that swap out aging equipment. Sensors and actuators proliferate in vehicles and smart factories—modern cars host 80-100 magnetic sensors—yet their sub-gram mass means smaller tonnage despite exploding unit counts. Magnetic storage is shifting from HDDs to MRAM sputter targets—tiny in mass but strategic for chipmakers—while magnetic refrigeration stays pre-commercial, awaiting cost breakthroughs. EMI filters round out demand with billions of ferrite beads yearly, although volume impact remains modest.

By End-user Industry: Automotive Electrification Outpaces Electronics

Electronics retained 38.13% of 2025 volume, anchored by 1.2 billion smartphones that each carry several grams of ferrite and NdFeB. Growth, however, is flattening as handset shipments plateau, leaving automotive as the fastest riser in the magnetic materials market. Battery-electric vehicles are forecast to jump from 14 million units in 2025 to 35 million in 2030, lifting automotive demand at a 7.95% CAGR because every BEV embeds 3-5 kg of permanent magnets versus none in combustion powertrains. Power-generation uses—including wind turbines and hydro generators—will spike again as offshore projects ramp in 2026. Industrial machinery is converting to variable-frequency drives that pair permanent-magnet motors with silicon-carbide inverters to cut energy use 20-30%. Home appliances and medical devices round out end uses, with samarium-cobalt holding critical niches in defense and aerospace actuators where thermal and radiation resilience are mandatory.

Geography Analysis

Asia-Pacific captured 67.23% of 2025 tonnage and is on track for a 7.77% CAGR to 2031, reflecting China’s 180,000-ton NdFeB output, Japan’s high-coercivity specialties, and South Korea’s MRAM scale-up. China produced major magnetic materials in 2025 across ferrite, electrical steel, and sintered NdFeB, with vertically integrated majors controlling oxide through machining, which sustains low cost and rapid lead times. Japan’s Shin-Etsu and TDK dominate premium grades above 50 MGOe and 30 kOe coercivity, securing 30-40% price premiums over commodity blocks. India is emerging as a ferrite hub for domestic smartphones and two-wheelers, but still imports 95% of rare-earth oxides, exposing it to Chinese policy shifts[2]India Ministry of Mines, “Annual Report 2024-25,” mines.gov.in .

North America held a moderate share, and MP Materials’ Stage II alloy line will shave import dependence to 70% by 2027, yet Canada’s pilot separation capacity remains under 1,000 tons, insufficient for even one automaker. In Europe, local magnet capacity covers barely 5% of need; VACUUMSCHMELZE and Proterial feed data-center cores yet rely on Chinese ribbon, showing the difficulty of onshoring full supply chains. South America and the Middle East and Africa's shares are driven by mining equipment and grid upgrades, with Brazil exploring rare-earth extraction from iron-ore tailings that may not commercialize before 2028.

Competitive Landscape

The magnetic materials market shows moderate concentration: the top 5 producers control roughly 37% of production capacity. Chinese leaders Hengdian and DMEGC practice mine-to-magnet integration to secure oxide streams, Japanese peers Shin-Etsu and TDK lean on grain-boundary diffusion for high-margin grades, and Western newcomers MP Materials and Lynas back-integrate into separation lines to meet defense sourcing rules. Recycling remains white space; Urban Mining Company and Noveon Magnetics run pilot selective-leach plants that recover dysprosium at 90% purity, a capability that will gain value if export quotas tighten. Technology is the key lever: Proterial’s diffusion process drops dysprosium use 30% without losing coercivity and now licenses to NEO Performance Materials and Daido Steel, creating royalty streams that insulate earnings from raw-material shocks. Patent filings in nanocrystalline alloys surged above 200 in 2024-2025, with VACUUMSCHMELZE, Hitachi Metals, and Advanced Technology & Materials racing for core-loss leadership. Standards bodies such as IEC TC 68 are drafting recycled-magnet traceability rules, which could favor producers holding ISO 14001 certification and transparent supply chains in the magnetic materials industry.

Magnetic Materials Industry Leaders

Proterial, Ltd.

Shin-Etsu Chemical Co., Ltd.

TDK Corporation

Ningbo Yunsheng Co., Ltd.

VACUUMSCHMELZE GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Researchers at the University of New Hampshire harnessed artificial intelligence to expedite the discovery of new functional magnetic materials. This effort resulted in the creation of a searchable database containing 67,573 magnetic materials, including 25 previously unidentified compounds that retained their magnetic properties at high temperatures.

- October 2024: Arnold Magnetic Technologies established a new manufacturing facility in Thailand to increase the production capacity of high-reliability magnetic components. This development is anticipated to bolster the company's market position and support growth in the magnetic materials market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the magnetic materials market as the global supply, measured in metric tons, of soft, semi-hard, and permanent magnet alloys such as ferrites, electrical steels, neodymium-iron-boron, samarium-cobalt, and Alnico that are sold to magnet fabricators and component makers serving automotive, electronics, energy, and general industrial end uses.

Scope Exclusions: Finished consumer devices, biomedical powders used exclusively for drug delivery, and recycled scrap traded outside formal channels are not counted.

Segmentation Overview

- By Material

- Neodymium-Iron-Boron (NdFeB)

- Ferrite

- Samarium-Cobalt (SmCo)

- Aluminum-Nickel-Cobalt (AlNiCo)

- Other Materials (Electrical Steel (GO and NGO), Nanocrystalline and Amorphous Alloys)

- By Type

- Soft Magnetic Materials

- Hard/Permanent Magnetic Materials

- Semi-Hard Magnetic Materials

- By Application

- Electric Motors and Generators

- Transformers and Inductors

- Sensors and Actuators

- Magnetic Storage and MRAM

- Magnetic Refrigeration

- EMI / EMC Components

- By End-user Industry

- Electronics

- Automotive

- Power Generation

- Industrial

- Other End-user Industries (Home Appliances, Healthcare, Aerospace, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We interviewed magnet alloy smelters, EV traction-motor integrators, wind-turbine OEM buyers, and regional distributors across Asia-Pacific, Europe, and North America. Their insights helped us validate utilization rates, capture average selling prices, and stress-test growth drivers that desk work alone could not fully surface.

Desk Research

Our analysts first map the demand pool with production and trade statistics from UN Comtrade, the United States Geological Survey, Eurostat, and China Customs, and then pair these with end-use indicators released by the International Energy Agency, OICA, and the Semiconductor Industry Association. We supplement those public datasets with cost and capacity disclosures in SEC filings, investor presentations, and national patent registries. Proprietary inputs are drawn from D&B Hoovers for company financials and Dow Jones Factiva for price and shipment news. This list is illustrative; many other reputable sources informed the study.

Market-Sizing & Forecasting

A top-down build starts with country-level production plus net exports of each alloy group; these volumes are aligned with end-use penetration ratios for EV builds, offshore wind additions, and smartphone output, which are then adjusted for scrap loss before a selective bottom-up check using sampled ASP × volume from key suppliers. Core variables, including electric vehicle sales, global wind-turbine capacity, consumer electronics production index, rare-earth oxide prices, and magnet intensity per unit, feed a multivariate regression model that projects demand to 2030. Where bottom-up evidence diverges, we revise assumptions rather than force totals to fit.

Data Validation & Update Cycle

Mordor analysts run variance checks against independent trade dashboards, investigate any outlier shifts, and elevate the model for peer review. Reports refresh yearly, with mid-cycle updates triggered by supply chain shocks or policy changes, ensuring clients always get the latest vetted baseline.

Why Mordor's Magnetic Materials Baseline Commands Reliability

Published estimates often differ because research firms choose disparate measurement units, segment scopes, and update cadences.

Key gap drivers include our decision to report in physical volume instead of revenue, a stricter inclusion policy that omits captive recycled feed, and an annual refresh that removes outdated COVID-era distortions. Other studies may convert factory gate prices with undisclosed mark-ups, apply broader material baskets, or rely on static historical averages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 33.01 million tons (2025) | Mordor Intelligence | - |

| USD 33.78 billion (2024) | Global Consultancy A | Combines finished magnets and devices; revenue metric masks volume shifts |

| USD 33.18 billion (2024) | Industry Association B | Uses regional price averages and a static demand share from 2022 |

These comparisons show that while other publishers provide useful viewpoints, Mordor's disciplined scope selection, metric transparency, and timely updates give decision-makers a dependable, easy-to-audit baseline.

Key Questions Answered in the Report

What is the volume of the magnetic materials market?

The market stands at 33.18 million tons in 2026 and is forecast to reach 44.68 million tons by 2031, expanding at a 6.13% CAGR.

Which region leads demand for magnetic materials?

Asia-Pacific holds 67.23% of global volume in 2026 and is growing at a 7.77% CAGR through 2031.

Why are neodymium-iron-boron magnets critical in electric vehicles?

NdFeB offers the highest energy product, enabling smaller, more efficient traction motors that extend EV range.

Which application segment is currently the largest consumer of magnetic materials?

Electric motors and generators account for 39.55% of total volume in 2026.

Page last updated on: