Permanent Magnet Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

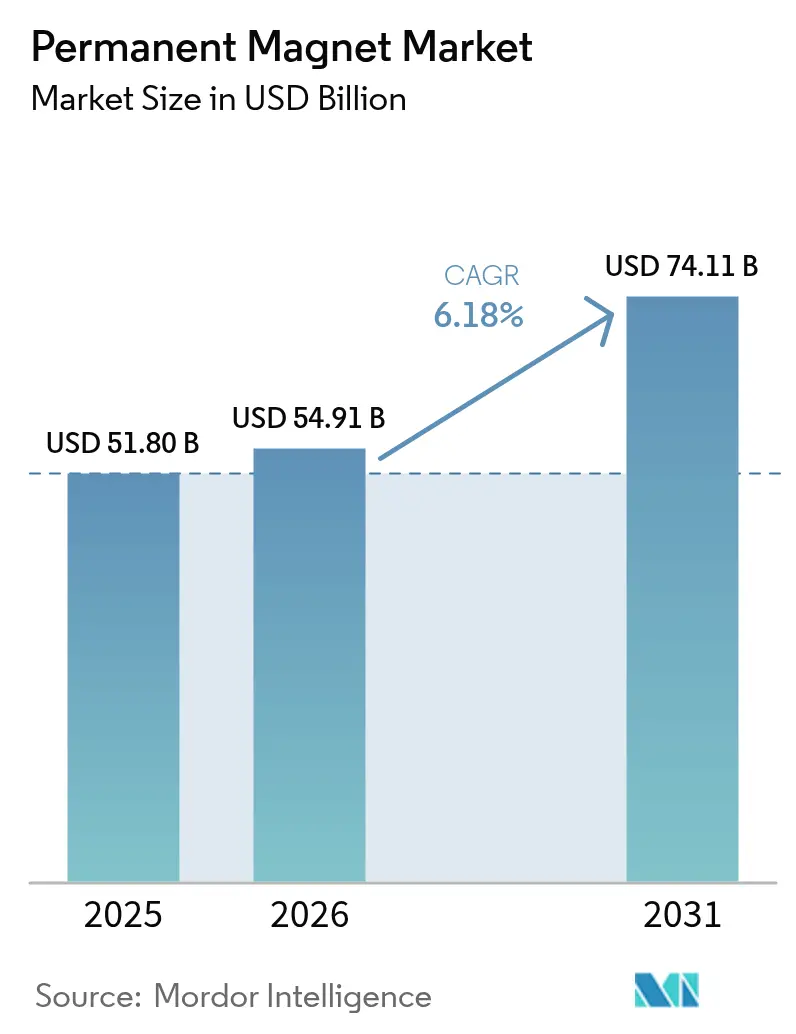

| Market Size (2026) | USD 54.91 Billion |

| Market Size (2031) | USD 74.11 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Permanent Magnet Market Analysis by Mordor Intelligence

The Permanent Magnet Market size is projected to grow from USD 51.80 billion in 2025 to USD 54.91 billion in 2026, and reach USD 74.11 billion by 2031, growing at a CAGR of 6.18% from 2026 to 2031. Electrification requirements in transportation, renewable-energy targets, and precision-manufacturing upgrades are aligning to lift long-term demand for high-energy-density grades, particularly sintered neodymium-iron-boron (NdFeB) magnets. Ferrite magnets still contribute nearly half of 2025 revenue because they are cost-competitive in auxiliary motors and low-power devices; however, designers of traction drives and direct-drive wind generators are migrating toward rare-earth compositions that tolerate higher temperatures and stronger magnetic fields. Magnet suppliers are narrowing dysprosium content through grain-boundary diffusion to cut exposure to volatile heavy rare-earth prices, while downstream buyers invest in recycling loops that reclaim neodymium from end-of-life motors and hard-disk drives. Moderate industry concentration allows regional specialists to succeed in additive manufacturing, grain-boundary-diffused chemistries, and custom small-lot runs that quickly prototype geometrically complex parts for aerospace, robotics, and medical imaging.

Key Report Takeaways

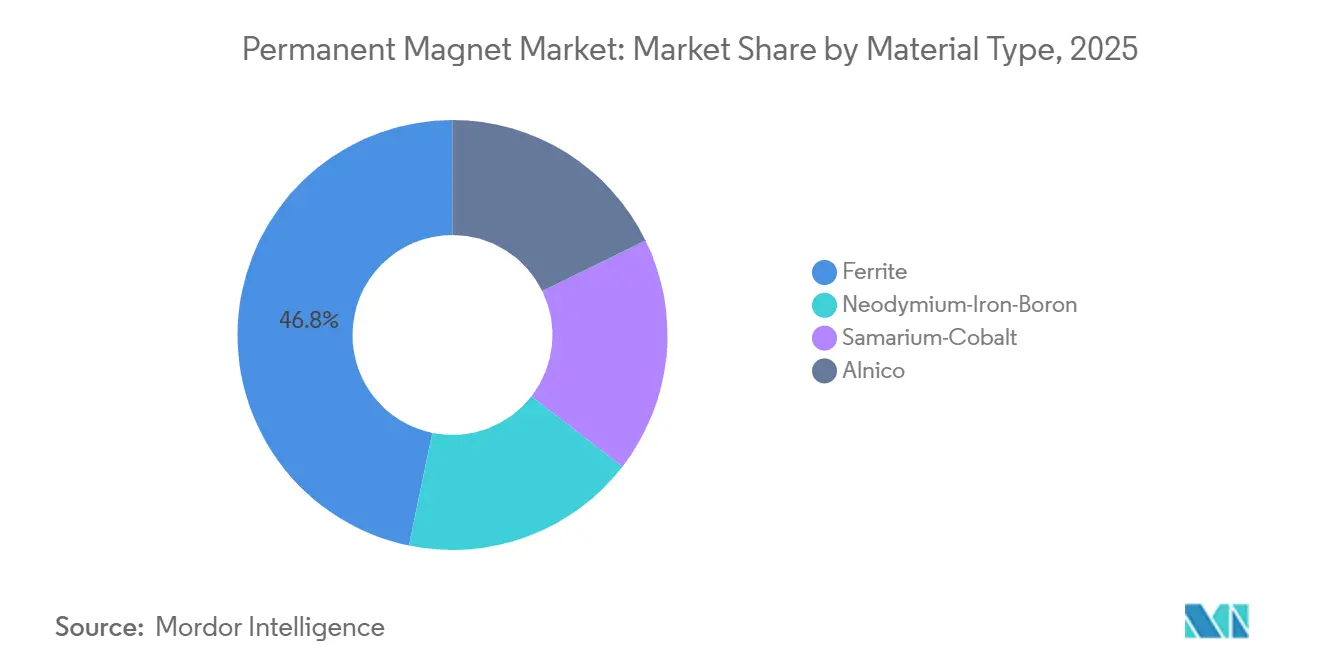

- By material type, ferrite magnets held 46.76% of the permanent magnet market share in 2025, while neodymium-iron-boron grades are forecast to post the fastest 7.18% CAGR through 2031.

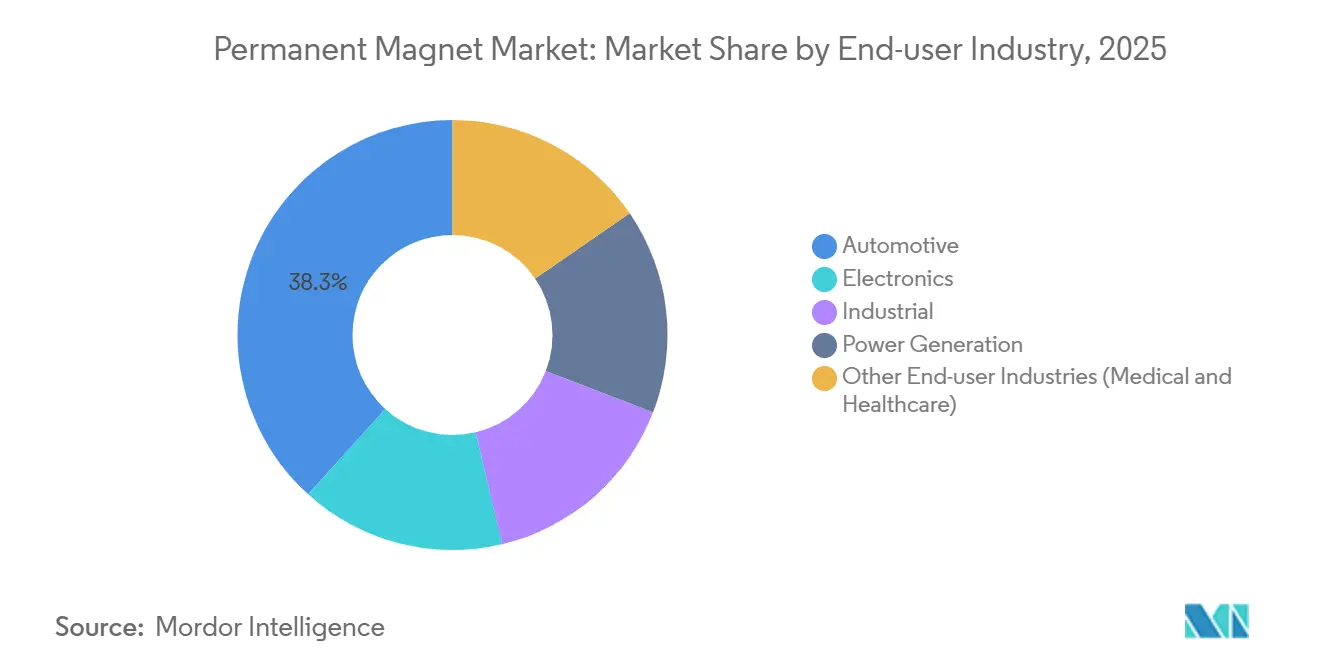

- By end-user industry, automotive led with 38.29% revenue share in 2025; Other end-user industries segment including medical imaging and surgical robotics, are set to grow at an 8.54% CAGR to 2031.

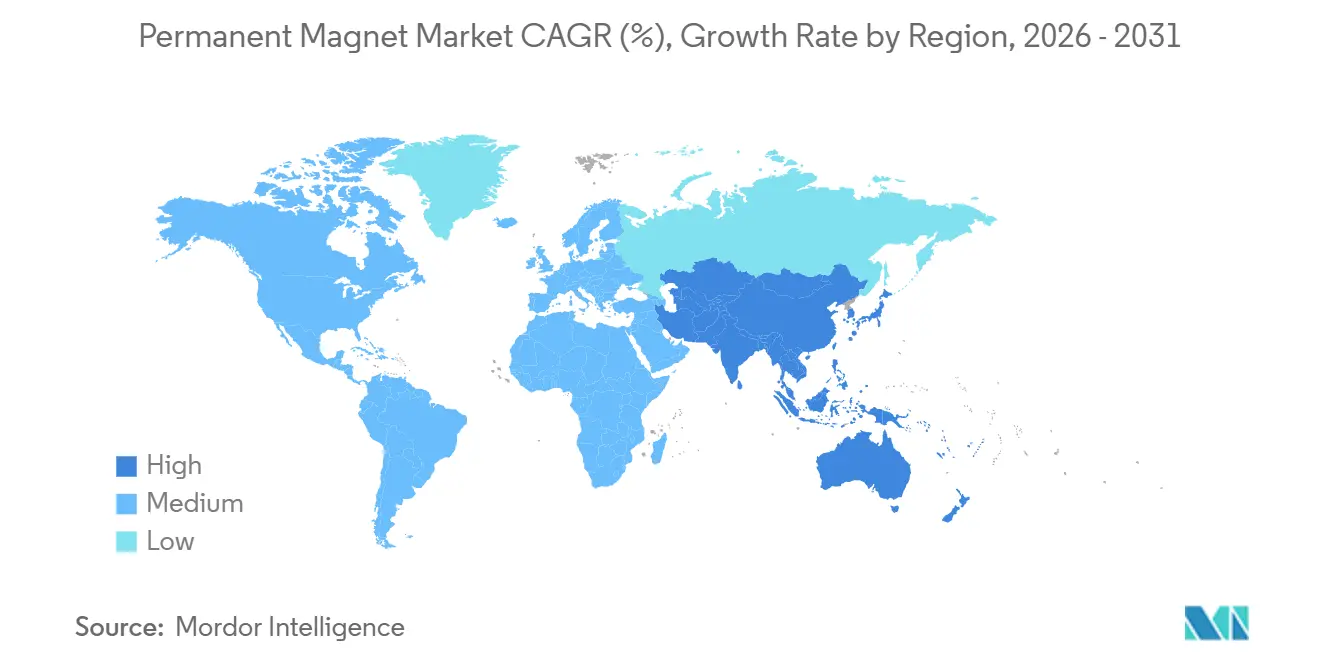

- By geography, Asia-Pacific captured 53.72% of 2025 revenue and is advancing at a 7.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Permanent Magnet Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of passenger and commercial EV fleets | +1.8% | Global, led by Asia-Pacific and Europe | Medium term (2-4 years) |

| Surging direct-drive wind-turbine installations | +1.2% | Offshore Europe, China, US Atlantic Coast | Long term (≥ 4 years) |

| Miniaturization in high-precision consumer electronics | +0.9% | Core Asia-Pacific, spillover to North America | Short term (≤ 2 years) |

| Industrial automation and humanoid-robot investments | +1.4% | North America, Europe, Japan, emerging China | Medium term (2-4 years) |

| Commercialization of 3-D-printed net-shape magnets | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification of Passenger and Commercial EV Fleets

Battery-electric vehicle output hit 14 million units in 2025, with each passenger car averaging 2 kg of sintered NdFeB and heavy trucks using up to 8 kg[1]BYD Co. Ltd., “E-Platform 3.0 Investor Deck Q1 2025,” byd.com. BYD’s e-platform 3.0 specified 180 °C-rated NdFeB rotors, while Daimler Truck and Volvo doubled magnet content in dual-motor drivetrains. The Euro 7 tailpipe rule, effective July 2025, locks in permanent-magnet synchronous machines for new urban buses, embedding long-run demand across a 40,000-unit replacement cycle.

Surging Direct-Drive Wind-Turbine Installations

Offshore wind added 22 GW in 2025, and 68% used direct-drive generators that require 600–1,200 kg of NdFeB per turbine. China’s 42 GW pipeline and recent US lease areas specify the same topology, tightening the supply–demand balance for high-grade rare-earth magnets.

Miniaturization in High-Precision Consumer Electronics

Apple’s iPhone 16 employed ultra-thin sintered NdFeB micro-magnets that raised haptic force by 30% while cutting volume 18%True-wireless earbuds shipped 450 million units in 2025, absorbing 135 tons of NdFeB, a margin-rich niche driven by stringent grinding and coating tolerances. Foldable handsets like Samsung Galaxy Z Fold 6 integrated detent magnets that further lifted ultra-thin demand.

Industrial Automation and Humanoid-Robot Investments

Figure AI’s 28-joint humanoid packs 2.1 kg of high-grade NdFeB, and Series C funding signals intent to reach 500,000 units by 2028. Factory servo-motor shipments in China jumped 19% in 2025 as pneumatic drives were swapped for permanent-magnet frameless motors offering 40% energy savings. Boston Dynamics deployed linear-motor warehouse robots that clock 800 box moves per hour, highlighting throughput gains that justify premium magnet grades.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rare-earth price volatility and export controls | -0.8% | Global, acute for non-Chinese producers | Short term (≤ 2 years) |

| Rise of ferrite/soft-magnetic composite substitutes | -0.6% | Automotive and industrial auxiliaries | Medium term (2-4 years) |

| Patent restrictions on high-grade NdFeB technology | -0.3% | Producers in Southeast Asia and India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rare-Earth Price Volatility and Export Controls

Neodymium oxide spiked 42% in 2025 after Myanmar halted heavy-rare-earth output and China imposed a 15% export tariff, squeezing non-Chinese refiners and trimming Lynas margins to 22%. Spot prices of praseodymium-neodymium alloy averaged USD 68/kg, adding USD 32 to a 2 kg EV motor bill-of-materials.

Rise of Ferrite/Soft-Magnetic Composite Substitutes

TDK’s 0.46-T ferrite launched in 2025 allowed Volkswagen to replace bonded NdFeB in 12-V auxiliaries, displacing 180 tons annually. Soft-magnetic composites climbed to 8% of industrial servo shipments, valued by conveyor and packaging OEMs that prioritize cost stability above peak torque.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: NdFeB Premiumization Reshapes Mix

Neodymium-Iron-Boron (NdFeB) magnets outpace the permanent magnet market at 7.18% CAGR through 2031 as electric-mobility and wind-power designers demand energy products above 35 MGOe. Ferrite retained 46.76% of 2025 revenue because smartphones, loudspeakers, and low-speed motors value low cost per kilogram, yet its share erodes as traction motors standardize on sintered NdFeB. Samarium-cobalt remains a niche for aerospace and oil-and-gas tools thanks to stability beyond 250 °C, while alnico slips under 5% after rare-earth options displaced it in sensors and precision instruments. Shin-Etsu shipped 14% more sintered NdFeB in fiscal 2025, underscoring the shift from bonded forms.

Bonded NdFeB is relegated to thin micro-speaker rings and smartwatch haptics where net-shape molding outweighs energy limits. The permanent magnet market size for NdFeB is therefore projected to capture an outsized share of absolute value gains through 2031 while ferrite largely tracks global GDP.

By End-User Industry: Medical and Automotive Drive Divergent Trajectories

Automotive captured 38.29% of 2025 revenue, with battery-electric platforms averaging 3.5 kg of permanent magnets versus 0.8 kg in internal-combustion vehicles. Tight Euro 7 rules and China’s zero-emission bus mandates support sustained demand for high-grade rotors, steering assist, and brake-by-wire actuators. In contrast, the Other end-user industries’ segment, led by MRI scanners and surgical robots, is expanding at an 8.54% CAGR—higher than any other segment—because 3 T and 7 T machines require large shimming arrays containing 1,800 kg of NdFeB per unit.

Electronics posted a modest rise in 2025 as handset shipments cooled, yet wearables and earbuds partly compensated, maintaining steady ferrite and bonded-rare-earth pull. Industrial machinery growth is driven by servo-motor retrofits that replace hydraulics, while power generation is growing amid offshore wind orders for direct-drive units. Collectively, these dynamics keep the permanent magnet market size expanding even where unit volumes plateau.

Geography Analysis

Asia-Pacific generated 53.72% of global value in 2025 and is rising at a 7.25% CAGR. China alone refined 85% of global rare-earth oxides and produced 187,000 tons of NdFeB magnets, bolstered by low electricity costs and integrated mine-to-magnet clusters[2]China MIIT, “Statistical Bulletin 2025,” miit.gov.cn. Japan maintains technology leadership, but limited domestic raw materials capped output at 31,000 tons. India’s production grew 18% under Production-Linked Incentives that reimburse up to 20% of capital outlay for new plants.

North America plus Europe accounted for significant revenue in 2025. MP Materials’ Stage II refinery produced neodymium-praseodymium oxide in California, marking the first US upstream step toward integrated magnets since 2015. Germany’s VACUUMSCHMELZE lifted Hanau's sintering capacity 30% to supply European EV plants under multiyear take-or-pay contracts.

South America and the Middle East and Africa are witnessing a rising demand for permanent magnets. Brazil’s offshore wind build-out supports local magnet assemblies, and South African mines install permanent-magnet conveyor drives to save 25% energy. South Korea exported 18,000 tons of magnets in 2025, feeding Vietnamese and Thai supply chains. Across Europe, the extended Ecodesign Directive, effective 2025, pushes industrial motor efficiency thresholds that effectively favor permanent-magnet synchronous machines in ratings above 7.5 kW.

Competitive Landscape

The permanent magnet market is fragmented in nature. Miners are integrating forward; Lynas and Blue Line will build a USD 450 million Texas magnet plant leveraging domestic rare-earth feedstock. Automakers such as General Motors and Stellantis invested USD 320 million in minority stakes in magnet fabrication, locking in supply.

Recycling is emerging as a competitive plank. Hitachi Metals recovered 98% of neodymium and dysprosium from retired hard-disk drives in a pilot that yielded 120 tons of oxides at costs 30% below virgin input, projecting 15% recycled feedstock coverage by 2030. Start-ups explore non-rare-earth chemistries; Niron Magnetics piloted iron-nitride magnets at 28 MGOe, suitable for cost-sensitive conveyor drives. Patent activity rose 22% in 2025, two-thirds from Chinese applicants, as firms race to reduce heavy-rare-earth use without violating existing diffusion claims.

Permanent Magnet Industry Leaders

Hitachi Metals, Ltd.

JL MAG Rare-Earth Co., Ltd.

Shin-Etsu Chemical Co., Ltd.

NINGBO YUNSHENG co., Ltd

VACUUMSCHMELZE GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Shin-Etsu Chemical committed JPY 45 billion (USD 310 million) to add 3,000 tons of NdFeB capacity at its Takefu plant, integrating automated coating lines that cut labor costs by 35%.

- December 2025: TDK bought 35% of Vietnam’s Hpmagnetics for USD 78 million, establishing a bonded-magnet hub that can triple capacity by 2028 while reducing US-China trade-route risk.

- November 2025: Lynas started its Kalgoorlie processing plant in Western Australia, adding 4,000 tons of mixed-oxide capacity compliant with free-trade sourcing rules under the US Inflation Reduction Act.

Global Permanent Magnet Market Report Scope

Permanent magnets are manufactured from special alloys such as iron, nickel, and cobalt, several alloys of rare-earth metals, and minerals such as lodestone. They generate a persistent magnetic field without the need for any external source of magnetism or electrical power.

The permanent magnet market is segmented by material type, end-user industry, and geography. By material type, the market is segmented into neodymium-iron-boron, ferrite, samarium cobalt, and alnico. By end-user industry, the market is segmented into automotive, electronics, industrial, power generation, and other end-user industries. The report also covers the market size and forecasts for the permanent magnet market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Neodymium-Iron-Boron |

| Ferrite |

| Samarium-Cobalt |

| Alnico |

| Automotive |

| Electronics |

| Industrial |

| Power Generation |

| Other End-user Industries (Medical and Healthcare) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Neodymium-Iron-Boron | |

| Ferrite | ||

| Samarium-Cobalt | ||

| Alnico | ||

| By End-user Industry | Automotive | |

| Electronics | ||

| Industrial | ||

| Power Generation | ||

| Other End-user Industries (Medical and Healthcare) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How great will global demand for permanent magnets be by 2031?

The permanent magnet market is projected to reach USD 74.11 billion by 2031 by growing with a CAGR of 6.18% during the forecast period.

Which region expands fastest through 2031?

Asia-Pacific leads at a 7.25% CAGR thanks to integrated rare-earth supply in China and rising EV production in India and Japan.

How serious is the risk of rare-earth supply disruption?

Price spikes in 2025 showed neodymium oxide can jump 40% within months when Myanmar or Chinese exports tighten, trimming the market CAGR by 0.8 percentage points.

Are ferrite magnets replacing NdFeB in autos?

Only in low-power auxiliaries; traction drives still need high-flux NdFeB that ferrite cannot deliver within space and weight limits.

What role does recycling play by 2030?

Pilots such as Hitachi Metals’ 98%-recovery plant suggest recycled feedstock could supply 15% of Japan’s magnet needs, easing pressure on virgin rare-earth mining.

When will 3-D-printed magnets become cost-competitive?

Producers estimate break-even near 500 tons annual output, implying commercial parity around 2028 for aerospace and defense volumes.

Page last updated on: