Aluminum Hydroxide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

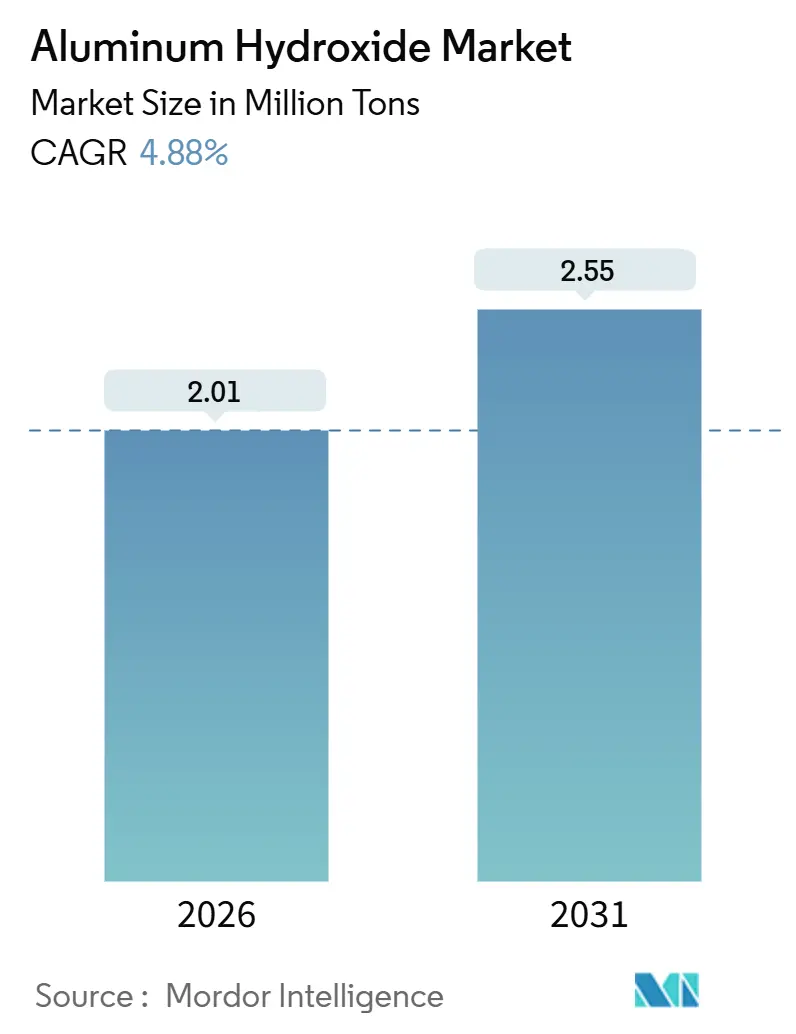

| Market Volume (2026) | 2.01 Million tons |

| Market Volume (2031) | 2.55 Million tons |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminum Hydroxide Market Analysis by Mordor Intelligence

The Aluminum Hydroxide Market size is estimated at 2.01 million tons in 2026, and is expected to reach 2.55 million tons by 2031, at a CAGR of 4.88% during the forecast period (2026-2031). The aluminum hydroxide market is anchored by its twin roles as a halogen-free flame retardant in polyolefin cable compounds and as an active pharmaceutical antacid ingredient. Industrial-grade volumes dominate because fire-safety rules in electric-vehicle battery enclosures and building cables favor mineral flame-retardant systems over brominated chemistries, whereas pharmaceutical demand, though smaller, yields higher margins on the back of aging populations in Japan, Germany, and the United States. Accelerated urban water projects in India and Southeast Asia are further supporting coagulant usage that begins with aluminum hydroxide feedstock. Simultaneously, solid-surface countertops with high filler loadings and lithium-ion battery separator coatings that require nano-scale grades are widening the application field of the aluminum hydroxide market.

Key Report Takeaways

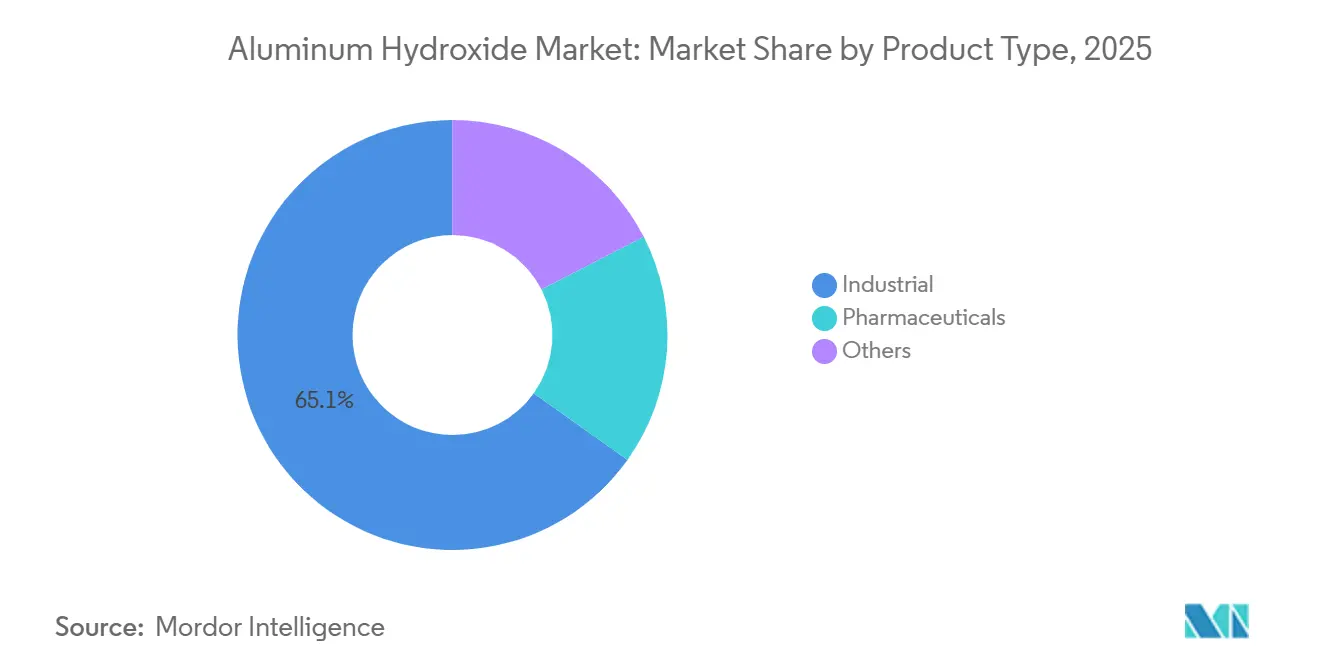

- By product type, industrial grade commanded 65.12% of the aluminum hydroxide market share in 2025 and is forecast to expand at a 5.11% CAGR to 2031.

- By application, flame-retardant and smoke-suppressant uses held 40.26% of volume in 2025; antacid formulations are advancing at a 5.02% CAGR through 2031.

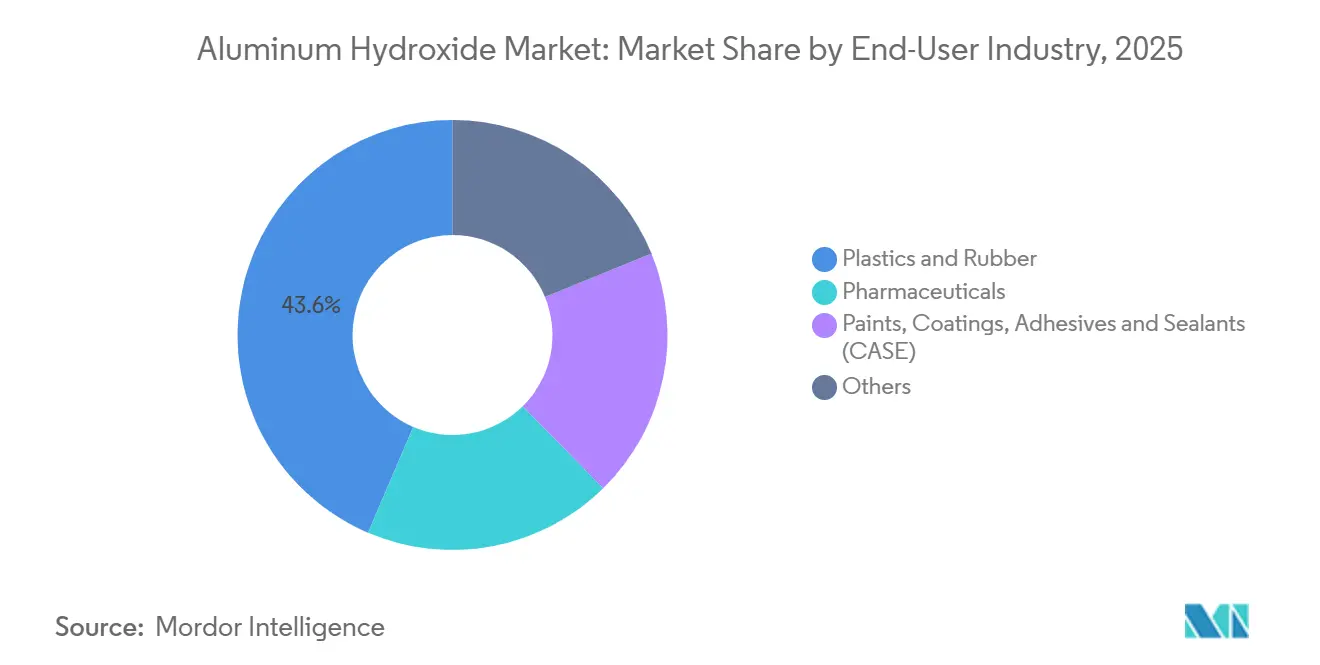

- By end-user industry, plastics and rubber captured 43.56% of the aluminum hydroxide market size in 2025 and are progressing at a 5.14% CAGR to 2031.

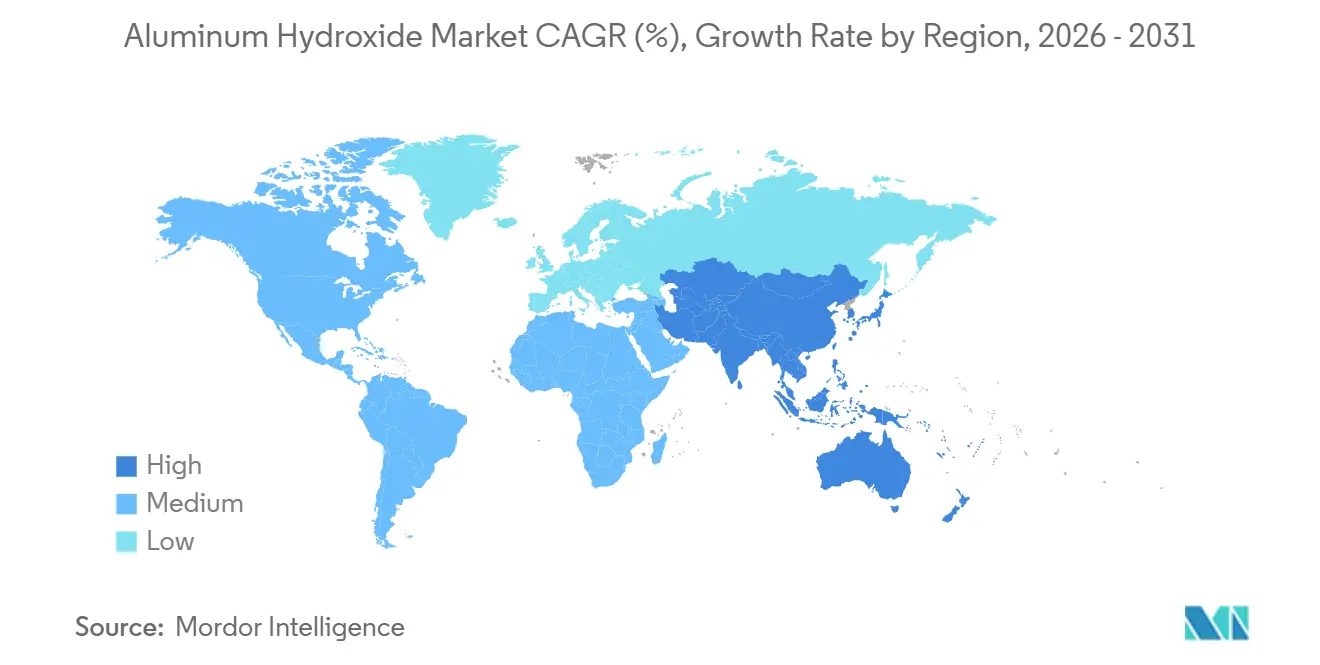

- By geography, Asia-Pacific represented 54.22% of global volume in 2025 and is projected to post a 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aluminum Hydroxide Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fire-safety regulations driving ATH in polyolefin cable compounds | +1.2% | Global, especially EU and North America | Medium term (2 - 4 years) |

| Halogen-free flame-retardant demand in EV battery enclosures | +1.0% | China, India, South Korea; spill-over to North America | Short term (≤ 2 years) |

| Rising OTC antacid consumption in aging economies | +0.6% | North America, Europe, Japan | Long term (≥ 4 years) |

| Rapid adoption of ATH in solid-surface countertops | +0.4% | North America, Europe, Middle East | Medium term (2 - 4 years) |

| Water-treatment infrastructure expansion in emerging nations | +0.8% | India, Southeast Asia, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fire-Safety Regulations Driving ATH in Polyolefin Cable Compounds

Stricter fire-safety regulations, including the EU's Construction Products Regulation EN 50575 and UL 94 V-0, are driving a transition from brominated additives to aluminum trihydrate fillers. Teknor Apex's Halguard low-smoke cable formulations have secured halogen-free certification under UL 2885, underscoring the rising demand for mineral solutions. Launched in April 2025, Benvic's Linkflex HF series, designed for data-center sheathing, boasts enhanced oil resistance. In transit and tunnel installations, aluminum hydroxide's endothermic water release at 180 °C proves beneficial, diluting combustible gases and cooling substrates. While compounders are pushing filler loadings for Class B flame ratings, the resulting high viscosity necessitates twin-screw extruders - a costly investment for smaller players in South America. With tightening standards, the aluminum hydroxide market is poised for steady growth in the global wire-and-cable sector [1]Teknor Apex, “Flame Retardant Wire and Cable Compounds Receive Halogen-Free Assessments,” teknorapex.com.

Halogen-Free Flame-Retardant Demand in EV Battery Enclosures

Demand for aluminum hydroxide-filled sheet-molding compounds is surging, driven by UNECE R-100 and proprietary OEM tests that simulate thermal runaway. Hindalco underscored the volume potential by delivering aluminum battery casings to Mahindra Electric. While premium European models prioritize glass-fiber SMCs infused with aluminum hydroxide for underbody shields - valuing dimensional stability up to 150 °C despite a mass penalty over bare aluminum - Huber's Martinal grades, treated with silane, mitigate moisture uptake. This preservation of mechanical properties post-humidity aging aligns with the eight-year warranties mandated for EVs. In Asia, the aluminum hydroxide market is further buoyed as Chinese cell manufacturers, by co-locating module assembly with vehicle plants, secure local supplies.[2]Hindalco Industries, “Hindalco Industries Ltd.,” hindalco.com.

Rising OTC Antacid Consumption in Aging Economies

The FDA’s OTC Monograph M001 allows elemental aluminum per antacid tablet. Japan’s 65+ cohort hit a significant percentage in 2024, fueling gastroesophageal reflux cases. Pharmaceutical-grade aluminum hydroxide meets USP heavy-metal limits and commands a premium over industrial material. Tablets retailing for a 30-day course in India still undercut proton-pump inhibitors by two-thirds, supporting steady consumption. Safety agencies cap daily aluminum intake; thus, formulators often blend with magnesium hydroxide to offset constipation risks without breaching intake limits.

Rapid Adoption of ATH in Solid-Surface Countertops

In 2024, U.S. remodeling spending saw a resurgence, driving up the demand for vanity tops. Meanwhile, hospitality projects in the Middle East are opting for thermoformable, non-porous cladding. Solid-surface composites, utilizing aluminum trihydrate, not only achieve the UL 94 V-0 standard but also offer a seamless aesthetic appeal. Surface-treated 5-µm grades from Sibelco are enhancing the industry, as they reduce resin viscosity and elevate polishing standards, enabling fabricators to attain a Class A gloss finish. While engineered quartz commands a dominant share of the countertop volume, solid surfaces carve out a niche in the healthcare sector, where joint-free installations and chemical resistance are non-negotiable. As a result, specialty grades are propelling the aluminum hydroxide market, particularly in lucrative construction applications.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bauxite-supply volatility | -0.9% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Health concerns on chronic aluminum intake | -0.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| High energy cost of precipitated ATH output | -0.7% | Europe, secondary in North America | Medium term (2 - 4 years) |

| Source: Mordor Intelligence | |||

Bauxite-Supply Volatility

In 2023, Guinea exported bauxite, setting its sights on increased exports by 2025. However, port congestion at Kamsar, coupled with monsoon disruptions, has hampered export consistency. This unpredictability has nudged Chinese buyers to pivot towards Australia, even if it means shouldering higher costs. In 2024, spot bauxite prices fluctuated. This volatility has put pressure on European aluminum hydroxide producers, who are bound by annual downstream contracts. Meanwhile, Rio Tinto's 2024 revival of its Gove refinery bolsters supply for Western smelters. Yet, the refinery grapples with elevated energy and labor expenses. As a result, the aluminum hydroxide market finds itself vulnerable to raw material shocks, leading to pronounced price fluctuations.

Health Concerns on Chronic Aluminum Intake

ATSDR has established a conservative oral minimal risk level, a stance echoed by WHO with its weekly tolerable intake. In Europe, some utilities have reduced alum dosing and switched to ferric coagulants to minimize residuals. Meanwhile, consumer advocacy groups are advocating for aluminum labeling on over-the-counter antacids, posing a reputational challenge for pharmacy brands. This heightened scrutiny in the aluminum hydroxide market might dampen long-term growth in established regions, despite a boost in near-term volumes driven by aging demographics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Grade Anchors Volume Growth

Industrial grade represented 65.12% of volume in 2025, owing to cost-effective flame retardancy in plastics and rubber. This slice of the aluminum hydroxide market is forecast to rise at 5.11% through 2031 as cable makers swap brominated additives for mineral fillers. Converters can now balance mechanical strength with flame performance, thanks to Huber's Martinal range, which spans from 1 to 80 µm. While smaller in size, the pharmaceutical-grade variant commands a price premium. This is due to USP's stringent limit on heavy metals, ensuring the purity essential for antacid tablets and vaccine adjuvants. Specialty nano-scale grades, measuring below 200 nm, are being utilized for lithium-ion separator coatings. In a bid to boost its financials, Sumitomo's NXA series is targeting a revenue increase in FY 2025. Meanwhile, reclaimed aluminum hydroxide, sourced from refinery waste, is making waves in Europe, aligning with the region's circular-economy aspirations.

Industrial demand is on the rise, driven by the need for halogen-free cable compounds to achieve filler loading for UL 94 V-0 compliance. Additionally, fine grades are enhancing opacity in cast-polymer countertops, and stearate-treated particles are improving flow in powder paints. The pharmaceutical sector is witnessing steady growth, as an aging population increasingly opts for OTC remedies over pricier proton-pump inhibitors. The stringent ultra-high-purity requirements are narrowing the supplier pool, thereby bolstering profit margins. While specialty segments present lucrative opportunities, they remain niche. For instance, nano grades are commanding a higher price compared to standard industrial material, yet their volumes are modest in the broader aluminum hydroxide market.

By Application: Flame Retardancy Leads, Antacids Accelerate

Flame-retardant uses delivered 40.26% of volume in 2025, primarily due to high loadings in cable jacketing and thermoplastic elastomers. Given that a single kilometer of low-voltage cable can absorb aluminum hydroxide, it's evident that construction activities play a pivotal role in shaping the aluminum hydroxide market. Tests are steering compounders towards aluminum hydroxide, favoring it over brominated flame retardants, which are known to emit corrosive gases. While aluminum hydroxide's brightness and refractive index make it a preferred choice for fillers and pigments in paints and engineered stones, competition from titanium dioxide ensures pricing remains disciplined.

Antacid formulations, despite modest tonnage, post the fastest 5.02% growth. Each tablet contains elemental aluminum and retails in bulk packs, ensuring visibility in the pharmaceutical sector. Water-treatment chemicals utilize a similar precursor chemistry: aluminum hydroxide's reaction with sulfuric acid produces aluminum sulfate, establishing a direct link between municipal budgets and the aluminum hydroxide market. While catalysts and other niches, such as alumina precursors for refinery FCC units, are influenced by global oil throughput, they tend to be stable yet slow-moving.

By End-User Industry: Plastics and Rubber Dominate

Plastics and rubber captured 43.56% of 2025 demand and are growing at the fastest rate of 5.14% because automakers and builders prefer halogen-free systems that meet UL 94 and EN 50575. To manage thermal events, EV battery shields now incorporate aluminum hydroxide into glass-fiber SMCs. In a nod to the multi-sector reliance on the aluminum hydroxide market, rubber conveyor belts used in underground mines have added filler to meet MSHA flame criteria. While pharmaceutical buyers represent only a small fraction of the overall volume, their stringent GMP requirements bolster price resilience, preventing commoditization.

Paints, coatings, adhesives, and sealants employ aluminum hydroxide as an intumescent additive in fire doors and structural steel primers, competing with expandable graphite and ammonium polyphosphate on cost-performance grounds. Paper coatings and specialty ceramics share a niche canvas, reflecting digitalization’s drag on printing grades. Nevertheless, the breadth of end-use keeps the aluminum hydroxide market diversified across economic cycles.

Geography Analysis

Asia-Pacific accounted for 54.22% of volume in 2025 and is set to post a 5.23% CAGR to 2031. In 2023, China imported bauxite, fueling its low-cost alumina plants. This strategic move allowed China to export aluminum hydroxide at prices lower than its European counterparts. Meanwhile, India's ambitious Jal Jeevan Mission, which is setting up rural water plants, is heavily reliant on aluminum sulfate, ensuring a steady demand for its precursor. In Japan, a significant portion of the population is seniors who drive consistent antacid consumption. At the same time, South Korea's leading battery manufacturers are opting for nano-grade aluminum hydroxide in their separators, citing its thermal stability benefits.

North America commands a significant share of the aluminum hydroxide market. While Huber and Martin Marietta capitalize on short lead times, they grapple with energy cost surges. Europe faces constraints due to power costs. This has led Nabaltec to contemplate shifting capacities to clusters in the gas-abundant Middle East. South America and the combined regions of the Middle East and Africa account for a smaller share of the market volume. While Brazil's automotive components and Saudi Arabia's hospitality projects drive growth, both regions still find themselves as net importers, hindered by limited alumina refining capabilities.

Competitive Landscape

The aluminum hydroxide market is moderately consolidated. Strategies revolve around upstream bauxite ownership, downstream masterbatch compounding, and regional diversification to offset energy and logistics risk. Technological differentiation includes surface coatings that reduce water absorption in polymer matrices and particle-size control that tailors rheology. ISO 9001 and ISO 14001 certification have become table stakes for automotive and pharmaceutical supply, yet REACH compliance costs give non-EU producers an advantage. Reclaimed aluminum hydroxide is emerging, but the lack of consistent quality standards limits penetration. Overall, regional energy economics and environmental regulation form the key battlegrounds in the aluminum hydroxide market.

Aluminum Hydroxide Industry Leaders

Huber Engineered Materials

Almatis

Nabaltec AG

Hindalco Industries Ltd

Alteo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Chengdu Yurong Chemical reported factory prices for 99.5%-grade aluminum hydroxide rising from CNY 3,200 per ton in Jun 2024 to CNY 4,600 per ton by Nov 2024.

- August 2023: Sumitomo Chemical outlined a 30% revenue expansion target for its ultra-high-purity alumina line by FY 2025 after scaling technology that derives α-alumina from calcined aluminum hydroxide.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the aluminum hydroxide market as the global trade and consumption of freshly produced aluminum trihydrate powder and related slurry grades that serve as flame-retardant fillers, antacid actives, water-treatment coagulants, and catalyst precursors across plastics, construction, electronics, and pharmaceutical manufacturing.

Scope exclusion: recycled alumina residues and downstream calcined alumina derivatives such as alumina hydrate-based fillers are not included.

Segmentation Overview

- By Product Type

- Industrial

- Pharmaceuticals

- Others (Specialty Nano Grade and Reclaimed / Recycled Grade)

- By Application

- Flame-Retardant and Smoke-Suppressant

- Filler and Pigment

- Antacid

- Water-Treatment Chemicals

- Catalyst and Others

- By End-User Industry

- Plastics and Rubber

- Pharmaceuticals

- Paints, Coatings, Adhesives and Sealants (CASE)

- Others (Paper and Others)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with alumina refiners, polymer compounders, cable makers, and regional distributors across Asia-Pacific, North America, and Europe enabled us to calibrate utilization rates, typical selling prices, and upcoming capacity additions, thereby closing gaps left by public data.

Desk Research

We began by mapping production and utilization footprints using open data sets issued by the United States Geological Survey, China Non-ferrous Metals Association, Eurostat Comext trade cubes, and International Trade Centre shipment codes. Policy drivers were traced through regulations published by the EU's REACH portal and flame-retardant guidelines from the National Fire Protection Association, while antacid consumption trends were benchmarked with World Health Organization pharmaceutical statistics. Company 10-K filings and investor decks enriched the demand narrative, and subscription databases such as D&B Hoovers and Dow Jones Factiva helped us vet corporate revenue splits. This list is illustrative; many additional public and proprietary sources were tapped during cross-checks.

Market-Sizing & Forecasting

A top-down production and trade reconstruction establishes the baseline volume.

Results are balanced against selective bottom-up roll-ups of refiner output, sampled average selling prices, and distributor channel checks to fine-tune regional splits. Key model variables include:

1. Plastic resin output and halogen-free flame-retardant penetration share. 2. New building floor-space completions under updated fire codes. 3. Pharmaceutical antacid demand per capita. 4. Municipal water-treatment capacity additions. 5. Electric vehicle battery housing production.

Multivariate regression, informed by expert consensus on the above indicators, projects volumes through the forecast period, with price scenarios layered to derive value where needed. Data voids in bottom-up estimates are addressed by applying weighted regional utilization factors that were validated during interviews.

Data Validation & Update Cycle

Our analysts iterate triangulation tests that compare model outputs with customs flows, quarterly earnings clues, and pricing dashboards before senior review. The model is refreshed each year, and material events, such as plant outages, policy shifts, and large contract wins trigger interim updates so clients always receive the latest vetted view.

Credibility Cornerstone - Why Mordor's Aluminum Hydroxide Baseline Stands Firm

Published figures often diverge because firms pick different units, include adjacent derivatives, or apply unvetted price curves.

Key gap drivers in our space revolve around (i) value versus volume reporting, (ii) whether alumina trihydrate used in non-flame-retardant applications is counted, (iii) exchange-rate assumptions, and (iv) refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 1.99 million tons, 2025 | Mordor Intelligence | - |

| USD 12.50 billion, 2025 | Global Consultancy A | Reports value not volume; blends ATH with downstream calcined alumina. |

| USD 12.32 billion, 2024 | Industry Association B | Uses list-price ASPs and omits pharmaceutical antacid demand. |

| USD 1.9 billion, 2025 | Regional Consultancy C | Covers only precipitated grades and stops at select Asia-Pacific geographies. |

In short, because Mordor's scope, dual-unit approach, and annual refresh capture the full spectrum of aluminum hydroxide flows, our baseline offers decision-makers a balanced, transparent yardstick they can retrace and update with ease.

Key Questions Answered in the Report

What is the current volume of the aluminum hydroxide market?

Global demand reached 2.01 million tons in 2026 and is forecast to grow to 2.55 million tons by 2031, registering a CAGR of 4.88%.

Which product grade dominates consumption?

Industrial grade held 65.12% of the 2025 volume due to widespread flame-retardant use in plastics and rubber.

Which application segment is growing fastest?

Antacid formulations are expanding at a 5.02% CAGR as aging populations drive OTC demand.

Why does Asia-Pacific lead regional demand?

Competitive feedstock costs, large cable and construction sectors, and India’s water-infrastructure build-out push Asia-Pacific to 54.22% of global volume.

What are the key growth restraints?

Bauxite-supply volatility, high European energy costs, and health concerns over chronic aluminum exposure restrain long-term expansion.

Page last updated on: