Catheter Stabilization Devices Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.45 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

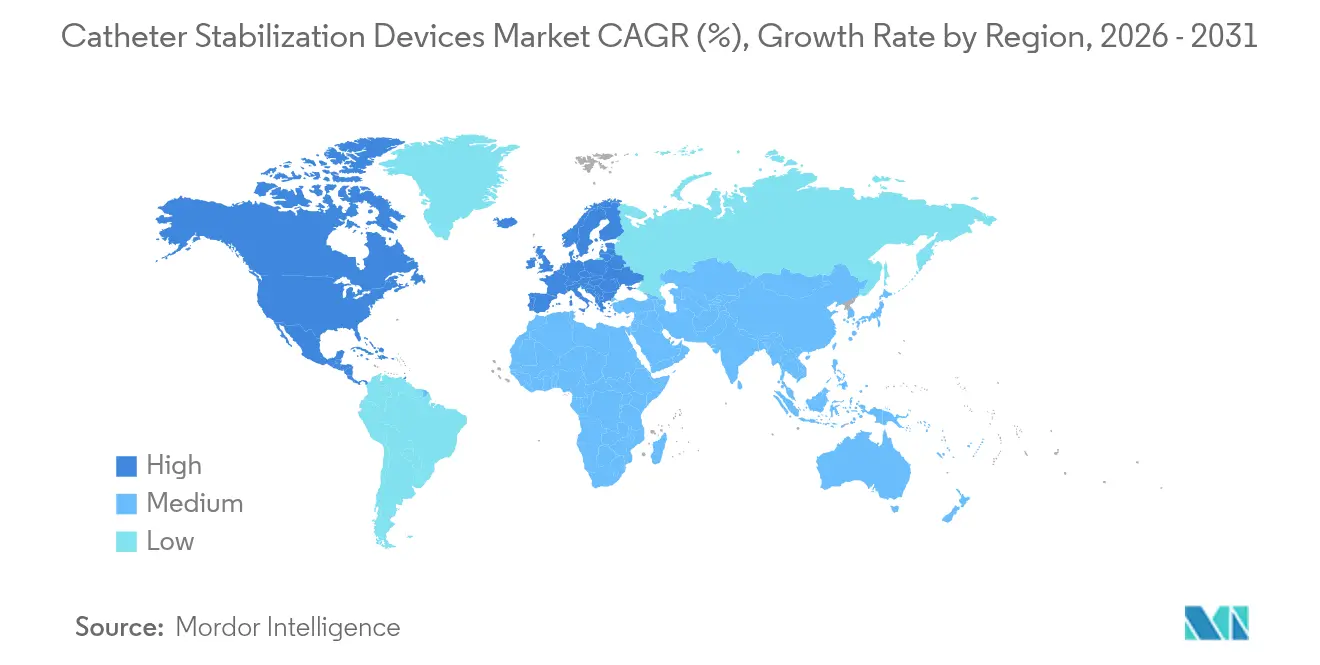

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Catheter Stabilization Devices Market Analysis by Mordor Intelligence

The catheter securement devices market size is expected to grow from USD 1.79 billion in 2025 to USD 1.89 billion in 2026 and is forecast to reach USD 2.45 billion by 2031 at 5.34% CAGR over 2026-2031. Increasing clinical vigilance around catheter-associated infections, the steady expansion of minimally invasive procedures, and stronger demand for hospital-at-home care collectively reinforce the growth outlook. Hospitals intensify spending on infection-control consumables, while ambulatory settings and home-based infusion programs create new use cases that favor portable, easy-to-apply securement formats. Rising oncology caseloads, an aging population that requires frequent vascular access, and innovation in skin-friendly antimicrobial adhesives further sustain the catheter securement devices market trajectory. Manufacturers respond by investing in differentiated designs that reduce dislodgement, lower CLABSI risk, and meet emerging sustainability mandates without compromising performance.

Key Report Takeaways

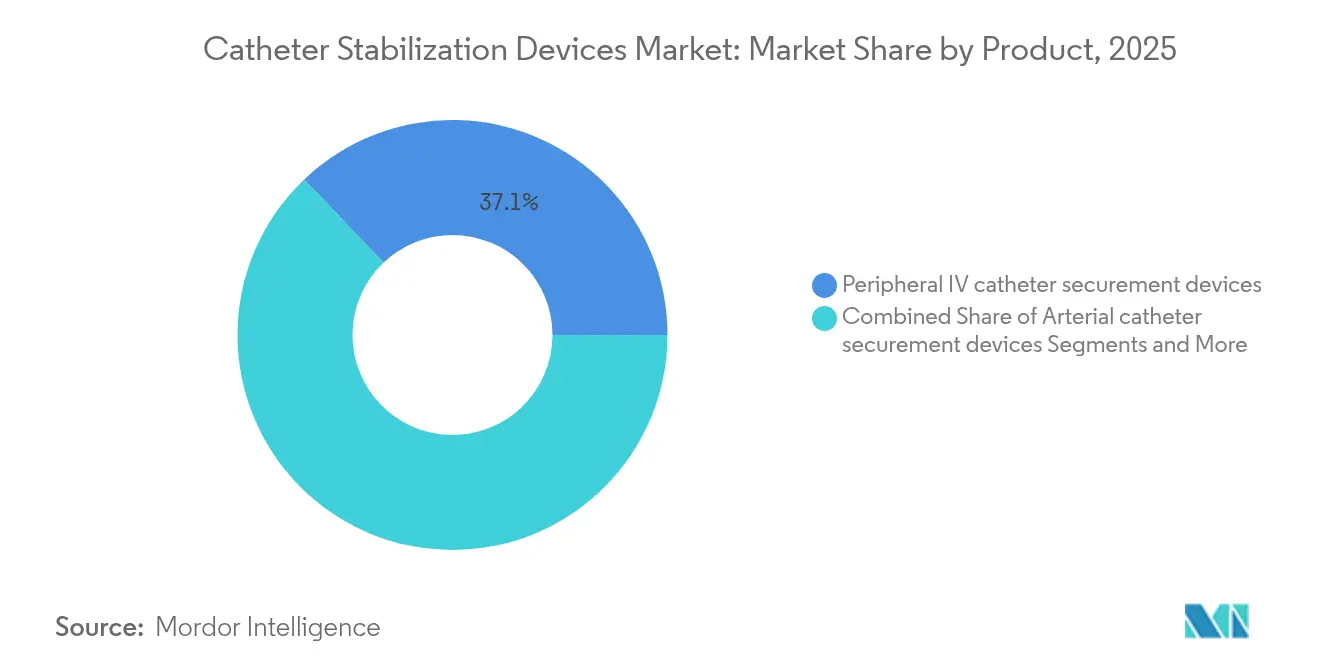

- By product, peripheral IV catheter securement devices led with 37.12% catheter securement devices market share in 2025, whereas central venous catheter securement devices are projected to expand at a 6.05% CAGR to 2031

- By application, cardiovascular procedures accounted for 41.55% of the catheter securement devices market size in 2025 and oncology & chemotherapy applications are advancing at a 6.55% CAGR through 2031.

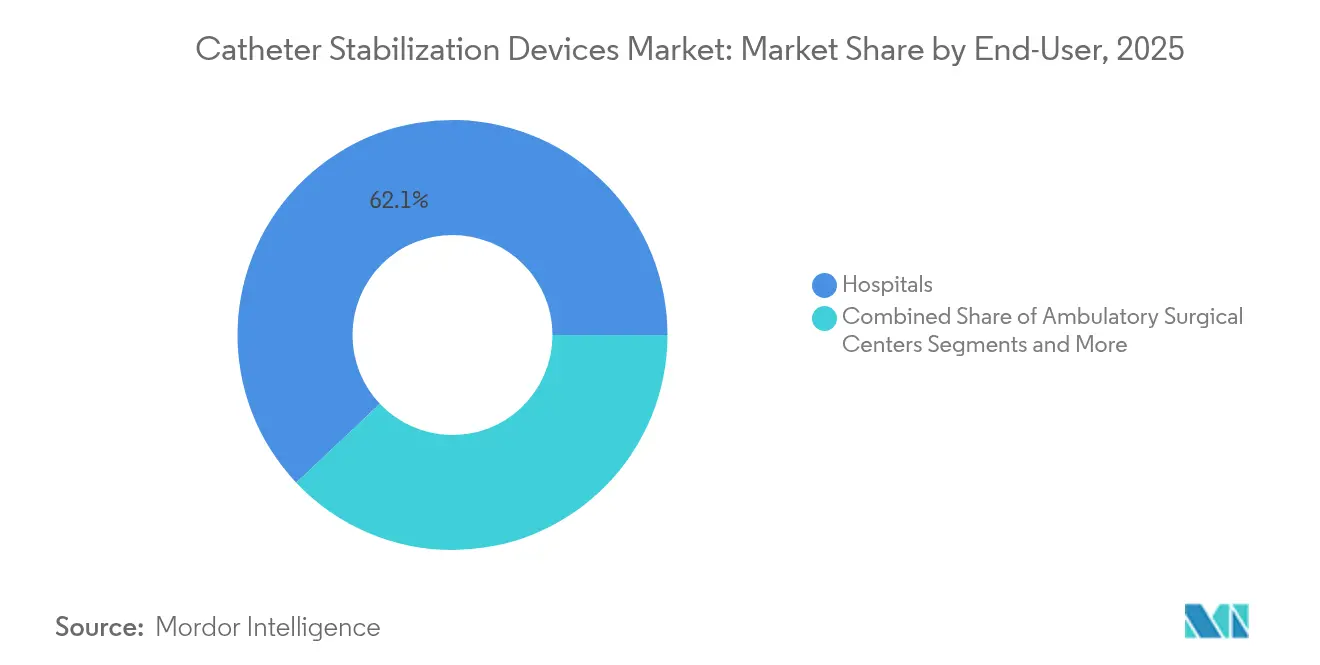

- By end-user, hospitals held 62.05% of the catheter securement devices market in 2025, while ambulatory surgical centers recorded the highest projected CAGR at 6.46% through 2031.

- By geography, North America led with 44.78% catheter securement devices market share in 2025, whereas Asia-Pacific is set to register a 6.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Catheter Stabilization Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic lifestyle diseases | +1.2% | Global; North America & Europe most affected | Long term (≥ 4 years) |

| Expansion of minimally invasive & catheter-based procedures | +1.5% | Global; leadership in North America & APAC | Medium term (2-4 years) |

| Stricter CLABSI & CAUTI prevention guidelines | +1.0% | Global; early uptake in North America & EU | Short term (≤ 2 years) |

| Greater hospital spend on infection-control consumables | +0.8% | Global; priority in developed markets | Medium term (2-4 years) |

| Shift to hospital-at-home & outpatient infusion programs | +1.1% | North America & EU; emerging in APAC | Medium term (2-4 years) |

| Advanced skin-friendly antimicrobial adhesive platforms | +0.6% | Global; R&D hubs in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Lifestyle Diseases

The global rise in diabetes, cardiovascular disease, and cancer drives long-term demand for securement solutions that maintain catheter integrity over extended treatment cycles. Oncology protocols increasingly rely on peripherally inserted central catheters, resulting in a 6.81% CAGR for the segment as clinicians favor devices that cut dislodgement without compromising skin integrity. Seniors now constitute a larger share of hospitalized patients, and their fragile vasculature heightens the need for gentle yet robust securement. Hospitals invest in antimicrobial dressings that lower infection risk, thereby reducing cost of care and readmission penalties. This demographic shift positions the catheter securement devices market as a central component of chronic disease management strategies.

Expansion of Minimally Invasive & Catheter-Based Procedures

Interventional platforms such as transcatheter aortic valve replacement and robotic-assisted vascular therapies rely on precise catheter stability during lengthy procedures. Same-day discharge protocols mean patients leave the hospital sooner, placing a premium on securement devices that continue to perform without continuous monitoring. Device makers respond by engineering low-profile anchors that allow imaging access while resisting accidental pull forces. Premium pricing is achievable when a securement device is purpose-built for a specialized interventional workflow, enhancing revenue diversity within the catheter securement devices market.

Stricter CLABSI & CAUTI Prevention Guidelines

The WHO 2024 standards and the latest CDC guidance identify sutureless securement as best practice for intravascular catheter care [1]World Health Organization, “Guidelines for the Prevention of Bloodstream Infections Associated with Intravascular Catheters,” who.int. Compliance is now tied to reimbursement incentives and public reporting, making infection metrics a board-level priority. Clinical studies demonstrate that stable catheters reduce microbial migration, supporting hospital mandates to switch from sutures to advanced adhesives. Manufacturers that validate infection-reduction claims gain competitive advantage as hospitals standardize purchasing around devices backed by strong evidence.

Greater Hospital Spend on Infection-Control Consumables

Each CLABSI incident can cost a U.S. hospital up to USD 48,108. German data suggest savings of EUR 120–200 per day when infections are prevented. These economics shift securement devices from discretionary to essential spend categories. Procurement teams, incented by value-based care agreements, allocate greater budgets to products that deliver measurable reductions in infection-related costs. The catheter securement devices market thereby benefits from a clear cost-avoidance narrative.

Shift to Hospital-at-Home & Outpatient Infusion Programs

Medicare’s 2025 home health update includes reimbursements for in-home infusion therapy that hinge on safe catheter management. Outpatient antimicrobial therapy programs expand globally, requiring securement systems that empower patient self-care while resisting daily wear. Device features such as clear adhesive windows and color-coded release tabs simplify layperson use. Growth in home-care channels extends the catheter securement devices market beyond hospital walls.

Advanced Skin-Friendly Antimicrobial Adhesive Platforms

Chlorhexidine-impregnated dressings cut central line infection risk by 52% compared with standard dressings. Silicone-based adhesive matrices reduce skin tears and allow pain-free removal, easing adoption among elderly and pediatric patients. These material advances let manufacturers command premium prices while meeting emerging sustainability goals through lower dressing change frequency. Antimicrobial chemistry thus becomes a strategic differentiator in the catheter securement devices market.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Migration to subcutaneous ports / needle-free connectors | –0.7% | Global; leadership in North America & EU | Medium term (2-4 years) |

| Frequent product recalls & adverse-event litigation | –0.4% | Global; strongest effect in regulated markets | Short term (≤ 2 years) |

| Sustainability mandates curbing single-use plastics | –0.5% | EU & North America; expanding worldwide | Long term (≥ 4 years) |

| Hospital reimbursement squeeze on non-revenue disposables | –0.6% | Global; acute in mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Migration to Subcutaneous Ports / Needle-Free Connectors

Needle-free connectors such as BD’s MaxPlus line show CLABSI reductions across more than 3,000 U.S. hospitals, shifting clinician preference toward hub-level infection control [2]Becton, Dickinson and Company, “MaxPlus and MaxZero Needle-Free Connector,” bd.com. Subcutaneous anchors like SecurAcath cut CLABSI risk by 288%, challenging adhesive devices. UV-C disinfection devices further decrease reliance on traditional securement by managing pathogens at the connector site. As integrated alternatives proliferate, sales of standalone surface adhesives may plateau.

Frequent Product Recalls & Adverse-Event Litigation

Securement failures that lead to skin stripping or bloodstream infections trigger recalls and increase liability exposure. Heightened regulatory surveillance in the United States and European Union forces manufacturers to allocate resources to post-market testing and compliance documentation. These costs compress margins and can delay the launch of next-generation devices. The associated brand damage also slows adoption among risk-averse hospital purchasing committees, limiting short-term growth for the catheter securement devices market.

Sustainability Mandates Curbing Single-Use Plastics

The EU Packaging and Packaging Waste Regulation accelerates the shift away from conventional plastics by imposing recycling and material-reduction targets [3]Oliver Healthcare Packaging, “EU Packaging & Packaging Waste Regulation: Impact on Healthcare,” oliverhcp.com. Hospitals favor vendors that offer biodegradable or recyclable components, placing pressure on firms with legacy polyvinyl chloride portfolios. Developing bioplastic options often entails higher raw-material costs and re-validation expenses, squeezing near-term profitability even as it secures longer-term relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Peripheral IV Dominance Amid CVC Innovation

Peripheral IV securement devices accounted for 37.12% of the catheter securement devices market in 2025. Central venous solutions, though smaller, are projected to expand at a 6.05% CAGR due to critical-care complexity and CLABSI prevention mandates. These two categories collectively define the bulk of catheter securement devices market size, with arterial, urinary, and other niche formats serving specialized needs such as dialysis and pediatric care.

Developers enhance peripheral IV products with integrated antimicrobial overlays and transparent, breathable films that allow daily site inspection. In the CVC space, tunneled PICC placements exhibit better infection and dislodgement profiles than non-tunneled lines, prompting vendors to innovate around anchoring mechanisms that accommodate tunneling techniques. Anticipated regulatory clarity for force-activated separation devices should foster additional product differentiation further reinforcing growth prospects for the catheter securement devices market.

By Application: Cardiovascular Leadership With Oncology Acceleration

Cardiovascular interventions represented 41.55% of the catheter securement devices market size in 2025, mirroring the volume of catheter-based cardiac procedures performed globally. Oncology and chemotherapy segments, forecast at a 6.55% CAGR, arise from intensifying cancer treatment regimens that require multi-month central line stability. Critical care and emergency medicine applications benefit from larger ICU footprints, while gastro-urology and nephrology maintain steady demand tied to dialysis prevalence.

Manufacturers tailor securement devices to drug-delivery timescales, sterile-field requirements, and imaging compatibility. Innovations include color-coded adhesive windows for quick inspection during rapid code situations and low-profile assemblies for endoscopic navigation. These refinements enable hospitals to standardize across departments, thereby deepening penetration of the catheter securement devices market.

By End-User: Hospital Dominance Amid ASC Expansion

Hospitals retained 62.05% share of the catheter securement devices market in 2025 owing to their high procedure volumes and complex case mix. Ambulatory surgical centers, projected to rise at 6.46% CAGR, leverage lower overhead and payer incentives for outpatient procedures. Home-care programs gain traction as Medicare and private insurers reimburse in-home infusions, broadening the reach of the catheter securement devices market.

ASC administrators demand quick-apply securement formats that fit fast turnover schedules, while home-care nurses require user-friendly kits with clear instructions. Vendors who offer multi-setting product bundles gain cross-channel efficiencies. Long-term care facilities, though steady, represent a niche growth avenue focused on pressure-injury avoidance and high skin-compatibility materials.

Geography Analysis

North America held 44.78% of catheter securement devices market share in 2025, underpinned by stringent infection-control policies and robust reimbursement pathways. Medicare’s 2025 provisions for home infusion therapy further extend device use into residential settings, reinforcing the regional growth runaway.

Europe shows consistent expansion as hospitals adapt to sustainability regulations that favor recyclable or biodegradable securement components, propelling product redesign and procurement cycles. Clinical research concentration in Germany, France, and the United Kingdom accelerates local adoption of innovative adhesives that satisfy both infection-control and environmental objectives.

Asia-Pacific is set to outpace global averages at a 6.88% CAGR through 2031. Healthcare infrastructure modernization in China and India, combined with aging demographics in Japan and South Korea, steers demand toward advanced vascular access solutions. Regulatory harmonization initiatives streamline approvals, allowing multinational manufacturers to deploy uniform product lines while accommodating local care protocols.

Regulatory Landscape

Catheter stabilization and securement products are regulated as medical devices, primarily under the US FDA framework (including 21 CFR device regulations for catheter-related products) and the EU Medical Device Regulation (Regulation (EU) 2017/745, MDR). A notable 2024 US classification update created a defined Class II pathway for intravenous catheter force-activated separation devices, increasing the emphasis on standardized non-clinical performance testing (for example, separation-force and leak/flow testing) alongside sterility and biocompatibility evidence.

In 2026, compliance expectations tightened in ways that affect securement-device design controls and technical documentation. The FDA Quality Management System Regulation (QMSR) became effective in February 2026, aligning US quality requirements more closely with ISO 13485, while biocompatibility expectations continue to reference ISO 10993, including a shift in ISO 10993-1:2025 toward risk-based biological evaluation with greater reliance on chemical characterization and toxicological assessment. In Europe, MDR implementation continues to expand EUDAMED-related obligations, including guidance for managing Summary of Safety and Clinical Performance (SSCP) information in EUDAMED (MDCG 2026-4), which raises data readiness requirements for manufacturers selling securement systems used with intravascular catheters.

Value Chain Analysis

The value chain begins with specialty inputs such as medical-grade silicones, acrylic and silicone adhesives, antimicrobial chemistries such as chlorhexidine for dressings, polymer films, and release liners, along with sterilization services (commonly ethylene oxide where appropriate). Manufacturers then convert these inputs through precision converting, die-cutting, and injection molding for anchors and clamps, followed by automated adhesive coating and lamination, packaging, sterilization validation, and lot release under QMS controls. Product development and verification remain tightly linked to standards-based testing (biocompatibility under ISO 10993 and device-specific performance verification), which can slow new SKUs and material substitutions.

On the commercial side, hospital procurement and group purchasing organizations dominate distribution, with preferences for supplier consolidation, consistent availability, and reduced SKU complexity. Demand also pulls from ambulatory surgical centers and home-care channels as infusion and hospital-at-home models expand. Post-market surveillance and complaint handling form a feedback loop because dislodgement, skin injury, and infection outcomes are clinically consequential. Regulatory changes, including the 2024 establishment of a specific Class II category for intravenous catheter force-activated separation devices, feed back into the chain by increasing required test evidence and documentation, which can affect supplier qualification, validation timelines, and packaging or labeling workflows for global compliance.

Competitive Landscape

The catheter securement devices market features moderate fragmentation. Established manufacturers such as Becton, Dickinson and 3M rely on R&D scale, broad distribution, and strong clinical evidence to protect share. BD’s USD 4.2 billion acquisition of Edwards Lifesciences’ Critical Care assets builds a platform that integrates monitoring with vascular access, intensifying competitive pressures.

Mid-tier players focus on niche use cases. Teleflex’s purchase of BIOTRONIK’s vascular unit for EUR 760 million improves its coronary portfolio, while Cook Medical’s alliance with Bedal International expands its drainage line with FlexGRIP securement tools. Start-ups leverage AI design to slash bacterial colonization on catheter surfaces by 100-fold, targeting unmet infection-prevention gaps.

Product differentiation centers on antimicrobial activity, skin gentleness, and application speed. Sustainability considerations spur research into bioplastics such as polylactic acid, although scale economics remain uncertain. Companies that demonstrate outcome improvements at competitive price points are positioned to capture incremental share within the catheter securement devices market.

Catheter Stabilization Devices Industry Leaders

Baxter

Becton, Dickinson & Company

Medline Industries Inc.

3M

B.Braun SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

There is a clear whitespace in securement formats that support longer dwell times and simplified maintenance without disrupting the insertion site, particularly for home-care and outpatient infusion programs where catheter management shifts toward patients and visiting nurses. Standards and guidance continue to formalize demand for engineered stabilization rather than improvised methods: the Infusion Nurses Society (INS) Standards of Practice (9th edition, 2024) mandate engineered stabilization devices and exclude non-sterile tape or sutures as acceptable securement, expanding the addressable base across vascular access devices beyond ICU-centric central lines.

Product and workflow innovation is also focused on reducing contamination opportunities during routine care and dressing changes. This supports designs that allow access for maintenance while staying attached to skin, as reflected by USPTO publications in 2026 for securement mechanisms designed for maintenance procedures without removal. Infection-prevention programs are widening their scope from CLABSI to catheter-associated bloodstream infections across vascular access devices, with APIC publishing a 2025 CABSI implementation guide that supports procurement justification for securement tied to measurable reductions in dislodgement and site disruption. On the urinary side, activity around CAUTI-focused securement concepts (for example, Cathetrix and TubeX promoting Foley-Safe and Nephro-Safe) signals ongoing specialization by catheter type and care setting, creating room for vendors to bundle securement with complementary infection-control consumables and protocol-aligned training.

Recent Industry Developments

- June 2026: BD was awarded a Vizient Innovative Technology contract for its CentroVena One Insertion System. The contract designation can accelerate evaluation and uptake across health systems that use Vizient contracting, reinforcing demand for integrated vascular access workflows. It also raises the competitive bar for suppliers selling securement adjacent to insertion by emphasizing procedural standardization and reduced complexity.

- April 2026: BD announced the release of its CentroVena One Insertion System, positioning it as an all-in-one central venous catheter insertion device. The launch highlights continued investment in vascular access platforms that reduce steps and potential contamination points during line placement. Portfolio moves like this can influence downstream securement selection by shifting hospitals toward more standardized kits and compatible accessories.

- February 2024: Cook Medical partnered with Bedal International to add FlexGRIP catheter securement devices to its percutaneous drainage portfolio. The partnership broadened Cook Medicals drainage offering with dedicated securement options intended to improve patient comfort and reduce accidental dislodgement. Adding securement at the portfolio level supports bundled purchasing in interventional and drainage procedures, where device compatibility and supply continuity are important.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the catheter stabilization devices market covers products that secure catheters and related tubes on the patient to reduce movement, dislodgement, and insertion-site complications in clinical and home-care settings.

Scope exclusions: Standalone catheters, needles, insertion kits, and IV fluids are excluded unless the value is explicitly tied to a dedicated stabilization or securement device.

Segmentation Overview

- By Product

- Peripheral IV catheter securement devices

- Central venous catheter (CVC) securement devices

- Arterial catheter securement devices

- Urinary catheter securement devices

- Other niche securement devices

- By Application

- Cardiovascular procedures

- Oncology & chemotherapy

- Critical care & emergency medicine

- Gastro-urology & nephrology

- Pain management & anesthesia

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Home-Care & Hospital-at-Home Programs

- Long-term Care / Skilled Nursing Facilities

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- APAC

- China

- Japan

- India

- Australia

- South Korea

- Rest of APAC

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with understanding procedure volumes and care settings where securement is routinely used, then mapping those signals to product demand. We relied on public sources such as CDC HAI guidance and datasets, the US FDA device database and safety communications, OECD and World Bank health expenditure indicators, UN Comtrade for trade flows linked to relevant HS codes, and peer-reviewed clinical journals that discuss catheter-related complications and securement practices.

To ground the commercial side, we also reviewed annual reports, investor presentations, and product brochures from participating manufacturers and distributors, then checked against reputable medical press coverage. Where needed, we used paid subscriptions for company financials and news intelligence, a patent database, and shipment-level trade datasets to cross-check company exposure and the direction of pricing. These desk research inputs are illustrative, and we also reviewed other public documents to confirm data points and validate assumptions.

Primary Interviews and Surveys

Primary work was used to test what desk sources could not confirm cleanly, including real-world device mix, replacement frequency, and typical purchasing pathways. We spoke with a mix of manufacturers, distributors, and hospital and home-care stakeholders across APAC, EMEA, and the Americas, and we re-contacted stakeholders when a key assumption, such as the average securement sets per patient episode, showed wide variance.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | APAC: 47% |

| Mid tier: 52% | Functional/Unit leaders: 33% | EMEA: 35% |

| Smaller Players: 17% | Managers: 51% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build where procedure volumes and catheter utilization reconstruct the likely number of securement events by setting, then the value is built using typical device mix and pricing. The model is anchored on practical inputs, including central and peripheral line usage rates, urinary catheter prevalence in acute care, the shift toward home infusion and home care, infection-prevention protocol adoption, and the mix between sutureless devices versus tapes and dressings.

After the first pass is built, we corroborate it using selective bottom-up checks, such as sampled company revenue exposure to securement, distributor channel feedback on unit movement, and a simple ASP-to-volume approximation for high-volume product groups. If a country lacks clean procedure statistics, we used proxies like hospital admission volumes and per-capita health spending, then narrowed ranges using interview feedback on local practice patterns.

For forecasting, we used scenario analysis supported by expert views on how catheter days, outpatient migration, and hospital staffing practices may shift. We then applied conservative pricing progression based on observed procurement behavior and inflation signals. The final forecast remains traceable to these variables so adjustments can be repeated when new public data is released.

Data Validation & Update Cycle

Validation is done through multiple checks so outputs do not drift away from realistic care delivery volumes. We compare totals against independent signals like device trade direction, announced capacity or portfolio focus where disclosed, and the implied spend per hospital bed to flag outliers.

When a region shows an unusual jump, the underlying assumptions are reopened, and targeted follow-ups are triggered with respondents who see purchasing patterns closely. Before sign-off, another analyst reviews the logic, units, and conversions, then the report is refreshed annually, with interim updates when material events change pricing, regulation, or procedure volumes. Right before delivery, we run a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Catheter Stabilization Devices Market Size Compared With Other Published Estimates

Published market values for catheter stabilization devices can differ even when the topic looks similar, since sources often choose different product boundaries, different years, and different approaches to pricing and care-setting mix. Currency timing, and whether the numbers reflect manufacturer-level value or wider channel value, also create visible gaps.

The benchmark table shows a spread around the mid-2020s, and in Mordor Intelligence's model the 2026 value is tied to catheter securement and stabilization products, including sutures, sutureless securement, and tapes and dressings, across hospital and home-care use, rather than folding in broader catheter accessory spending or unrelated insertion supplies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.89 B (2026) | |

| Global Research Publisher A | USD 1.95 B (2026) | Uses a longer forecast window and can apply a different split between hospital and home-care demand, which shifts the implied device mix and the weighted ASP in the base year. |

| Industry Research Publisher B | USD 1.51 B (2025) | Anchors sizing on an earlier base year and may apply narrower inclusion around adhesive pad style securement only, which can undercount suture-based and tape or dressing stabilization use cases. |

Looking across the table, most of the difference is explained by what gets counted as a stabilization device and how pricing is averaged across care settings and device types. By keeping the inputs tied to catheter utilization signals and then checking the output against supplier and channel feedback, the estimate stays balanced and can be re-run when procedure or procurement patterns shift.

Key Questions Answered in the Report

Which product category dominates current sales?

Peripheral IV securement devices held 37.12% share in 2025, reflecting their universal use across care settings.

Who are the key players in Catheter Stabilization Devices Market?

Baxter, Becton, Dickinson & Company, Medline Industries Inc., 3M and B.Braun SE are the major companies operating in the Catheter Stabilization Devices Market.

Which is the fastest growing region in Catheter Stabilization Devices Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

How fast is demand for catheter securement solutions growing in ambulatory centers?

Ambulatory surgical centers are projected to post a 6.46% CAGR through 2031, outpacing hospital growth.

Page last updated on: