Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.89 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.01 Billion |

| Growth Rate (2026 - 2031) | 2.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Carpet Tile Market Analysis by Mordor Intelligence

The Europe carpet tile market size was valued at USD 0.89 billion in 2025 and estimated to grow from USD 0.91 billion in 2026 to reach USD 1.01 billion by 2031, at a CAGR of 2.05% during the forecast period (2026-2031). Maturation accompanies this steady trajectory as extended-producer-responsibility rules, healthy-building labels, and digital design tools reshape procurement patterns across the region. Commercial landlords favor modular flooring because selective tile replacement shortens vacancy periods and limits maintenance outlays, enhancing rental yields in a soft office market. Hybrid-workspace adoption also boosts demand for cushion-backed products that combine acoustic comfort with rapid installation, especially in the United Kingdom, Germany, and the Nordics. EU carbon-footprint disclosure has accelerated investment in recyclable backings such as Interface’s CQuest Bio and Tarkett’s EcoBase, giving suppliers with proven take-back schemes a pricing premium [1]Interface, “Modular Carpet Tile,” interface.com. . Meanwhile, digital dye-injection systems allow designers to order low-MOQ custom patterns for boutique hotels and co-working hubs, unlocking incremental revenue streams in the premium tier.

Key Report Takeaways

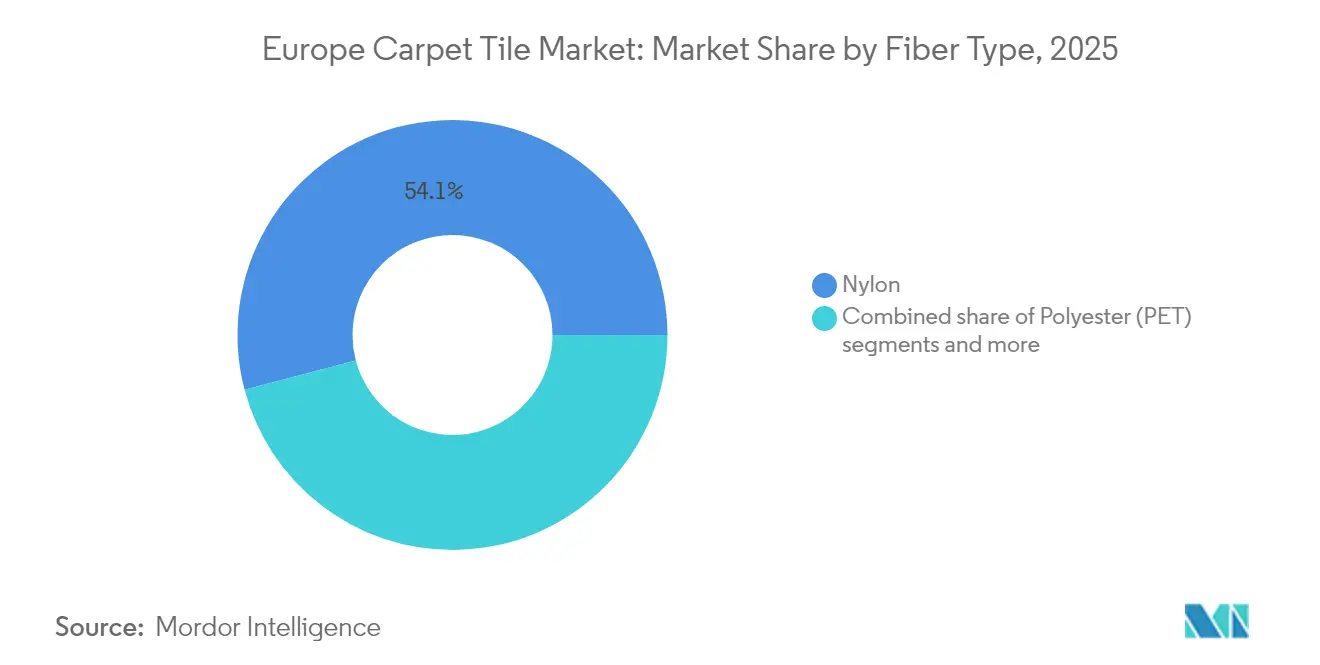

- By fiber type, nylon led with 54.10% of Europe carpet tile market share in 2025, bio-based fibers are projected to post the fastest 10.38% CAGR and lift their portion of the Europe carpet tile market size through 2031.

- By end user, the commercial segment accounted for 63.05% of Europe carpet tile market share in 2025, while hospitality and leisure are advancing at a 9.05% CAGR through 2031.

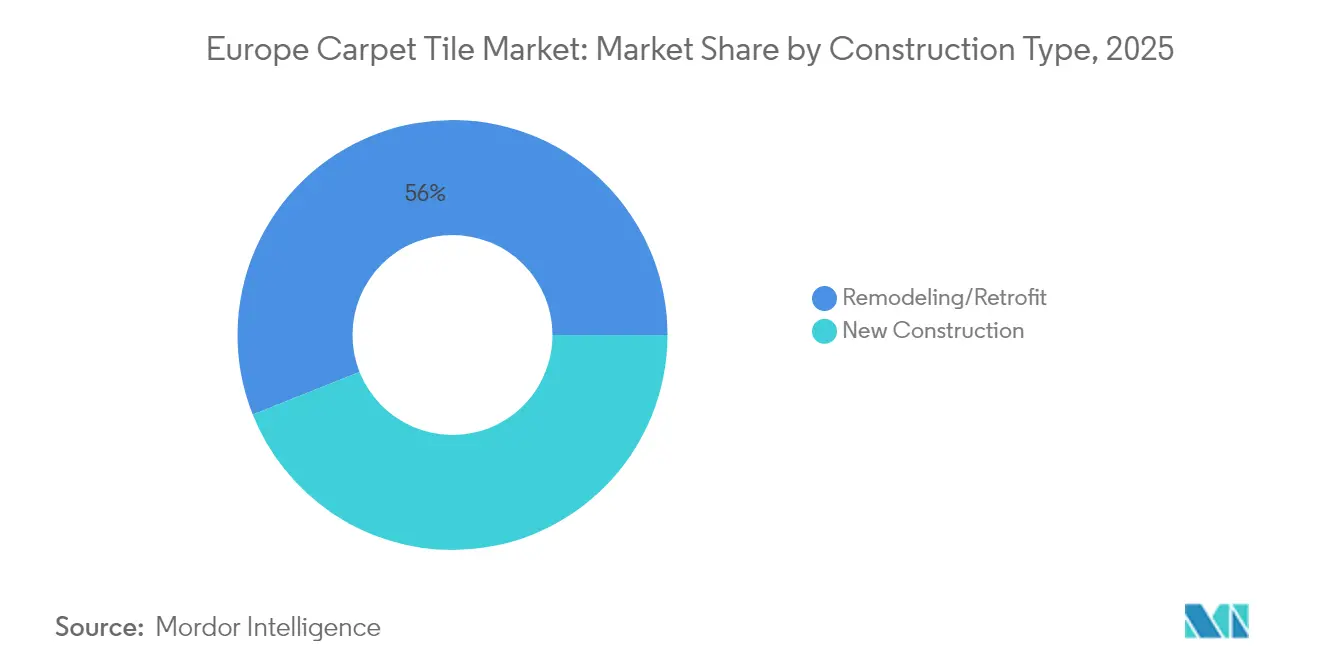

- By construction type, remodeling and retrofit projects held 56.02% of Europe carpet tile market share in 2025 while new construction is poised to register a 7.18% CAGR to 2031.

- By distribution channel, B2B contractors captured 51.10% of Europe carpet tile market share in 2025, yet online channels are on track for a 12.35% CAGR by 2031.

- By geography, the United Kingdom dominated with a 22.10% of Europe carpet tile market share in 2025; Spain is forecast to grow at 8.31% CAGR, the fastest within Europe carpet tile market dynamics.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Carpet Tile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for modular, low-maintenance flooring in commercial refurbishments | +0.8% | UK, Germany, France, Netherlands | Medium term (2-4 years) |

| Surge in post-pandemic office fit-outs & hybrid-workspace redesigns | +0.6% | Global, strongest in UK, Germany, Nordics | Short term (≤ 2 years) |

| EU-wide carbon footprint disclosure boosting demand for recyclable tile backings | +0.4% | EU-wide, particularly Germany, Netherlands, France | Long term (≥ 4 years) |

| Digital dye-injection enabling low-MOQ bespoke patterns for designers | +0.3% | UK, Germany, France, Italy, Spain | Medium term (2-4 years) |

| Accelerated shift toward healthy-building certifications requiring low-VOC materials | +0.2% | Global, strongest in Nordics, UK, Germany | Long term (≥ 4 years) |

| Expansion of flexible co-working chains across tier-2 European cities | +0.1% | Spain, Italy, Central & Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Modular, Low-Maintenance Flooring in Commercial Refurbishments

Commercial landlords now specify carpet tiles to limit tenant disruption and keep maintenance budgets low. Interfaces that allow selective tile exchange mean high-traffic zones can be refreshed overnight, reducing downtime and improving tenant satisfaction. Tarkett indicated that carpet tiles represented more than 62% of its commercial carpet sales in 2025, with EcoBase-backed modules enabling up to 84% CO₂ savings compared with incineration. This operational flexibility has become a core value driver in lease negotiations, especially in jurisdictions where fit-out costs are borne by landlords. The Europe carpet tile market therefore benefits from a structural shift toward modularity as property owners align flooring decisions with portfolio yield management. Pre-cut tiles also generate less installation waste, further supporting ESG objectives under tightening EU disclosure rules [2]Carbonfact, “Overview of Textile EPR Laws,” carbonfact.com..

Surge in Post-Pandemic Office Fit-Outs & Hybrid-Workspace Redesigns

Hybrid-work adoption pushed firms to re-zone offices into collaboration clusters, quiet pods, and touchdown points. Carpet tiles offer acoustic attenuation and permit fast reconfiguration when occupancy patterns change. In Prague, 2024 fit-out budgets averaged EUR 1,235/m² (USD 1,350/m²), and developers increasingly chose tiles to compress installation schedules and limit labor costs [3]EurobuildCEE, “Office Fit-Out Costs in Prague,” eurobuildcee.com.. Hospitality venues mirrored this strategy by using modular flooring to flip meeting rooms into banquet spaces within hours. The flexibility theme has now entrenched itself in specification guides across corporate real-estate and facility-management teams, cementing a demand floor for Europe carpet tile market products over the next two years.

EU-Wide Carbon Footprint Disclosure Boosting Demand for Recyclable Tile Backings

From January 2025, the Waste Framework Directive obliges member states to arrange separate textile collection, while Extended Producer Responsibility schemes assign disposal costs to manufacturers. Interface’s CQuest Bio backing and Tarkett’s closed-loop EcoBase platform provide compliance head-starts, enabling price premiums in green-building projects. Hungary’s EPR framework now levies HUF 145/kg (USD 0.40/kg) fees on non-recyclable carpet products, sharpening the cost gap between conventional and circular designs. Manufacturers with reclamation sites, such as Tarkett’s Waalwijk plant, are better positioned to absorb logistics and processing expenses. As disclosure norms extend to carbon labeling on product data sheets, recycle able tiles gain additional pull through ESG-oriented procurement policies in Germany, France, and the Netherlands.

Digital Dye-Injection Enabling Low-MOQ Bespoke Patterns for Designers

High-resolution print heads now apply color directly onto tufted substrates, removing the minimum-order hurdle that once forced designers to compromise on aesthetics. Milliken’s PrintWorks platform supplies samples within four days and full orders inside three weeks, accelerating design-to-build cycles for boutique hotels and creative agencies. The technology complements Europe’s strong interior-design culture, letting small projects specify unique palettes without incurring surplus inventory. Manufacturers gain higher average selling prices by monetizing personalization, while distributors reduce inventory carrying costs. Digital print will likely lift premium-segment value in the Europe carpet tile market through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront cost versus broadloom carpet | -0.3% | Price-sensitive markets, Central & Eastern Europe | Short term (≤ 2 years) |

| Volatility in crude-derived nylon & bitumen raw-material prices | -0.2% | Global, manufacturing-intensive regions | Medium term (2-4 years) |

| Take-back obligations raising reverse-logistics expenses | -0.25% | Western Europe, markets with circular mandates | Medium term (2–4 years) |

| Limited installer skill pool in Central & Eastern Europe | -0.15% | Central & Eastern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost Versus Broadloom Carpet

Carpet tiles typically command 15-25% price premiums over equivalent broadloom installations, constraining adoption in cost-sensitive commercial segments and residential applications. This pricing gap persists despite lifecycle cost advantages from selective replacement capabilities and reduced installation waste. The premium reflects higher manufacturing complexity, specialized backing systems, and precision cutting requirements that increase production costs per square meter. Price-conscious specifiers in Central and Eastern European markets often default to broadloom solutions despite carpet tiles' operational benefits, particularly in large-scale installations where upfront budget constraints outweigh long-term maintenance considerations. However, manufacturers increasingly offer entry-level tile ranges with simplified backing systems to address price sensitivity while maintaining core modular benefits.

Volatility in Crude-Derived Nylon & Bitumen Raw-Material Prices

Nylon 6 and bitumen price fluctuations directly impact carpet tile manufacturing costs, with energy-intensive production processes amplifying raw material volatility. European manufacturers face additional pressure from reduced Russian energy supplies and carbon pricing mechanisms that increase production costs for petroleum-derived inputs. Shaw Industries, EF, and Mohawk implemented price increases of 5-15% in April 2022 due to inflationary pressures on raw materials, labor, and logistics costs. Supply chain diversification and alternative material development help mitigate these risks, with increasing adoption of recycled nylon fibers like ECONYL reducing dependency on virgin petroleum-derived inputs while supporting sustainability objectives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Bio-Based Materials Drive Innovation

Nylon held a dominant 54.10% Europe carpet tile market share in 2025 owing to its durability and stain resistance. Bio-based fibers, however, are forecast to expand at a 10.38% CAGR, the highest among all fiber categories. This momentum stems from corporate carbon targets and regulatory pushes toward circularity. The Europe carpet tile market size for regenerated nylon is rising in parallel as Aquafil’s ECONYL, made from fishing nets and post-consumer carpet, now supplies more than half of the company’s fiber output.

Manufacturers also promote PET derived from recycled bottles and wool for boutique applications. These substitutions lower Scope 3 emissions and appeal to hotel brands pursuing eco-label differentiation. The ongoing materials shift requires supply-chain realignment but unlocks pricing headroom for premium sustainable SKUs, reinforcing top-line resilience even in low-growth macro environments.

By End User: Hospitality Sector Leads Growth

Commercial premises commanded 63.05% of 2025 demand in the Europe carpet tile market. Offices, healthcare campuses, and education facilities collectively dominate through specifications that reward durability and acoustic performance. Hospitality and leisure are projected to log a 9.05% CAGR, the quickest among end-user groups. Hotel refurbishments postponed during lockdowns are now underway, and operators prefer carpet tiles for their speed of installation and design flexibility.

Corporate office briefs increasingly require zoning for collaboration, privacy, and social interaction, encouraging modular flooring that can be rearranged without full rip-outs. Education projects adopt cushion-backed tiles to tame reverberation in classrooms, while hospitals use low-VOC collections to support infection-control programs. The diversity of use cases cushions the Europe carpet tile market against cyclical shocks in any single vertical.

By Construction Type: Retrofit Projects Dominate

Remodeling and retrofit activity represented 56.02% of 2025 revenue as Europe’s aging building stock demanded interior upgrades . Building owners favor renovation over demolition to cut embodied-carbon emissions and comply with taxonomy-aligned financing. The Europe carpet tile market size attached to new-construction projects will still grow at a solid 7.18% CAGR, buoyed by data-center builds, selective high-rise offices, and logistics warehouses.

In retrofits, carpet tiles’ peel-and-stick or adhesive-free formats reduce downtime. Builders avoid moisture barriers and minimize waste, supporting tenant retention and ESG metrics simultaneously. In new developments, specifiers integrate access-floor panels with modular tiles to future-proof layouts for technological upgrades, embedding carpet tiles into the core design language of modern workplaces.

By Distribution Channel: Online Sales Accelerate

B2B contractors and builders made up 51.10% of 2025 distribution, reflecting the project-driven character of flooring procurement. Digital channels are expected to post a 12.35% CAGR, the fastest across all sales routes. Manufacturers have deployed configurators that show 3D room renderings and instantly calculate bills of materials, cutting design lead times.

Dealers now operate hybrid showrooms where architects sample textures physically before finalizing colorways online. Direct-to-site logistics bypass regional warehouses, shrinking carbon footprints and transport costs. Online growth therefore complements, rather than cannibalizes, established contractor networks, expanding the overall reach of the Europe carpet tile market.

Geography Analysis

The United Kingdom led the Europe carpet tile market with a 22.10% share in 2025. Specifiers there emphasize BREEAM credits, driving demand for recyclable backings and low-VOC fibers that align with corporate ESG disclosure mandates. In London, employers use premium modular flooring to support hybrid-work fit-outs, and public-sector refurbishment programs add steady baseline volume.

Germany ranks second, bolstered by a strong manufacturing base and stringent environmental laws that accelerate adoption of circular products. Producers operate regional reclamation hubs that recycle collected tiles into new backings, reducing carbon intensity. France maintains similar scale through ongoing corporate office renovations and accelerated hotel investment ahead of major sporting events.

Spain outpaces all peers with an 8.31% forecast CAGR. Tier-2 cities welcome co-working chains that value swift installation and stylish customization. The hotel sector’s rebound also favors carpet tiles for speed of refurbishment between booking seasons. Italy follows with solid penetration in fashion-driven hospitality projects and corporate headquarters that demand high acoustic performance.

BENELUX countries benefit from policy incentives for material recovery and close access to Interface and Tarkett plants, creating short lead times and low freight emissions. Nordic nations, though smaller by volume, exert influence on product development through advanced health-based building criteria. Central and Eastern Europe, including Poland, Hungary, and Romania, show incremental uptake as quality-of-fit-out rises in new office towers and logistics hubs. Installer skill shortages and budget constraints still temper growth, but EU grant funding and foreign direct investment are narrowing the adoption gap each year.

Competitive Landscape

In 2024, the Europe carpet tile market showed moderate concentration, with the five largest suppliers collectively generating the majority of total revenue. Interface led the market, driven by its carbon-negative CQuest Bio platform and its widely recognized Mission Zero sustainability milestones. Tarkett followed closely, capitalizing on its Desso brand and a closed-loop facility in Waalwijk that recycles used tiles into EcoBase backings. Shaw Industries also held a strong position, supported by its Patcraft and Shaw Contract labels, known for advanced acoustic cushion systems and extensive color offerings.

Competition increasingly centers on recycling infrastructure and bio-based content rather than traditional durability metrics. Smaller specialists focus on digital customization and secondary-market sales. Belgium-based Composil processes 250,000 m² of reclaimed tiles annually, repurposing them at roughly half the price of new products and extending the useful life of installed flooring. Rising compliance costs under Extended Producer Responsibility rules are driving consolidation, as illustrated by Beaulieu’s closures in Belgium and Poland in 2025.

Strategic moves highlight sustainability leadership. Interface marked 25 years of its i2 modular platform with new carbon-negative collections in February 2025. Tarkett unveiled an EU-funded Carpet Recycling Centre targeting 95-97% material recovery by 2028. Shaw inked a distribution deal with PPG to add resinous floors to its Patcraft channel, broadening cross-sell opportunities. These initiatives underscore a pivot toward cradle-to-cradle models and portfolio diversification, themes that will shape competitive advantage through the forecast horizon.

Europe Carpet Tile Industry Leaders

Interface, Inc.

Tarkett S.A.

Shaw Industries (Patcraft)

Mohawk Industries (IVC, Karastan

Milliken & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Interface celebrated 25 years of i2 and launched new carbon-negative collections. The company also launched new carpet tile collections claiming carbon-negative credentials.

- January 2025: Tarkett introduced an EU-funded Carpet Recycling Centre to close the material loop.

- October 2024: Composil announced expanding its second-hand carpet tile business internationally. The initiative extended its reuse and recycling operations into Luxembourg and France.

- July 2024: Tapi Carpets acquired Carpetright’s brand and 54 UK stores for GBP 15 million (USD 20.15 million).

Europe Carpet Tile Market Report Scope

Carpet tiles, also known as modular carpets or square carpets, are squares cut from wall-to-wall rolls which can be fitted together to make a carpet. Carpet tiles are popular as a flooring option for commercial environments, such as bars, restaurants, and other relatively uncomplicated projects. A complete background analysis of the European Carpet Tile market, which includes an assessment of the emerging trends by segments and regional markets, significant changes in market dynamics, and market overview, is covered in the report. By-products type, the market is segmented into square and rectangle, by end-user into residential and commercial, by distribution channel into offline stores and online stores, and by geography into Germany, the United Kingdom, France, Spain, and Rest of Europe.

By Fiber Type

| Nylon |

| Polyester (PET) |

| Polypropylene |

| Wool |

| Bio-based Fibres |

| Other Fiber Types |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Remodeling / Retrofit |

By Distribution Channel

| B2C / Retail Consumers | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Contractors / Builders |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Fiber Type | Nylon | |

| Polyester (PET) | ||

| Polypropylene | ||

| Wool | ||

| Bio-based Fibres | ||

| Other Fiber Types | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Remodeling / Retrofit | ||

| By Distribution Channel | B2C / Retail Consumers | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Contractors / Builders | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe carpet tile market in 2026?

The market is valued at USD 0.91 billion in 2026 and is projected to reach USD 1.01 billion by 2031.

Which fiber type leads sales?

Nylon accounts for 54.10% of 2025 revenue due to durability and stain resistance.

Why are hospitality projects adopting carpet tiles quickly?

Hotels value modular tiles for rapid room turnover, acoustic comfort, and custom design options, supporting a 9.05% CAGR in this segment.

What regulation is shaping product design?

EU Extended Producer Responsibility schemes require textile take-back programs from 2025, pushing investment in recyclable backings.

Which country is growing fastest?

Spain is forecast to record an 8.31% CAGR through 2031, driven by co-working expansion and hotel refurbishments.

Page last updated on: