Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.02 Billion |

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Ceramic Tiles Market Analysis by Mordor Intelligence

The Germany ceramic tiles market size in 2026 is estimated at USD 2.08 billion, growing from 2025 value of USD 2.02 billion with 2031 projections showing USD 2.41 billion, growing at 2.98% CAGR over 2026-2031. Expansion is being powered by post-pandemic household renovation, fast diffusion of large-format porcelain, and government incentives that make tile-laying work eligible for energy-efficiency subsidies. Frost-resistant porcelain, antibacterial glazes, and thin ventilated façade panels are increasingly specified as builders seek durable, low-maintenance finishes that meet tightening carbon rules. Energy-intensive manufacturers are also retrofitting kilns with LPG or waste-heat recovery systems to cushion volatile natural-gas prices. As both supply-side decarbonization and demand-side renovation solidify, the Germany ceramic tiles market is expected to hold its course despite cyclical softness in new housing approvals.

Key Report Takeaways

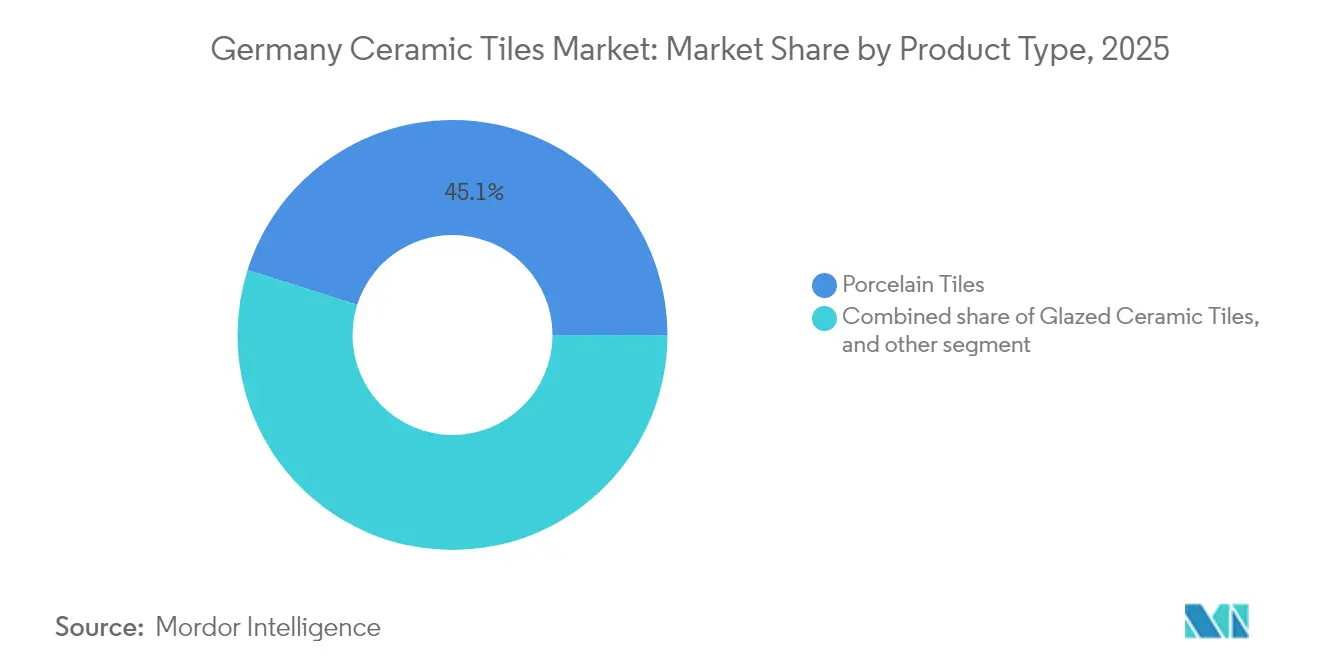

- By product type, porcelain tiles led with 45.12% of the Germany ceramic tiles market share in 2025; thin large-format porcelain is advancing at a 9.18% CAGR through 2031.

- By application, floor coverings captured 70.05% of the Germany ceramic tiles market share in 2025, while façades are projected to expand at an 7.86% CAGR to 2031.

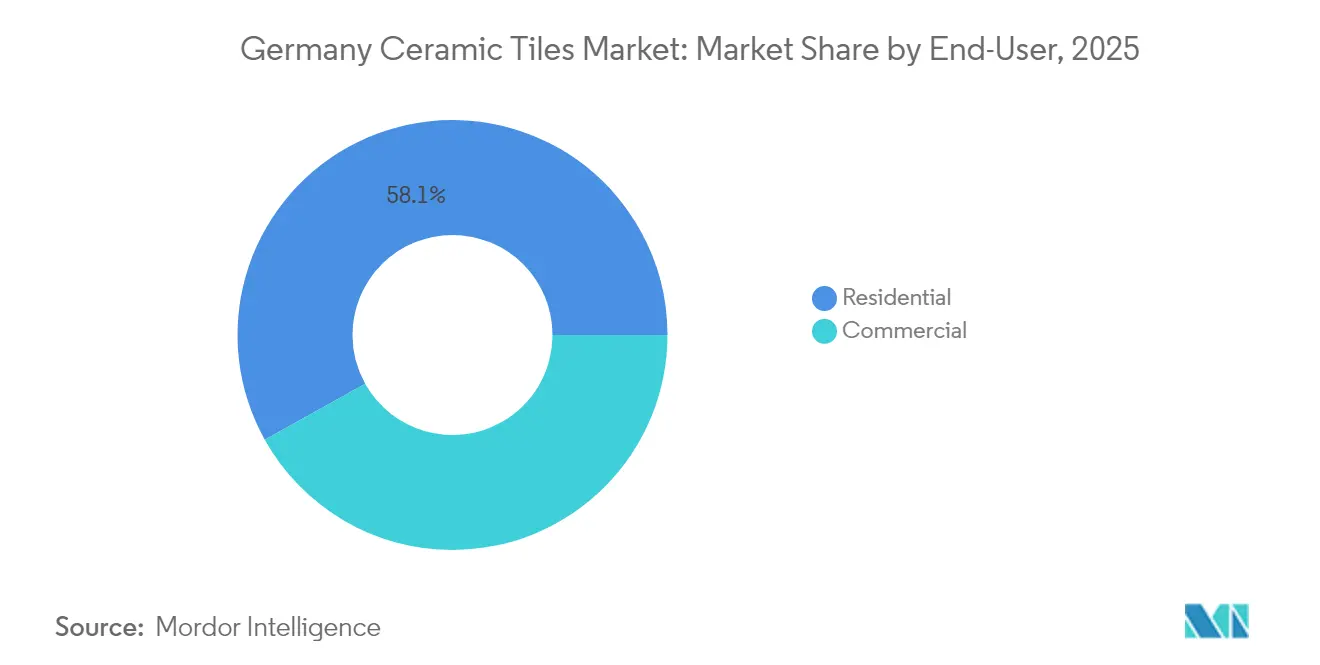

- By end-user, residential renovation accounted for 58.10% of the Germany ceramic tiles market size in 2025 and is projected to advance at a 6.29% CAGR through 2031.

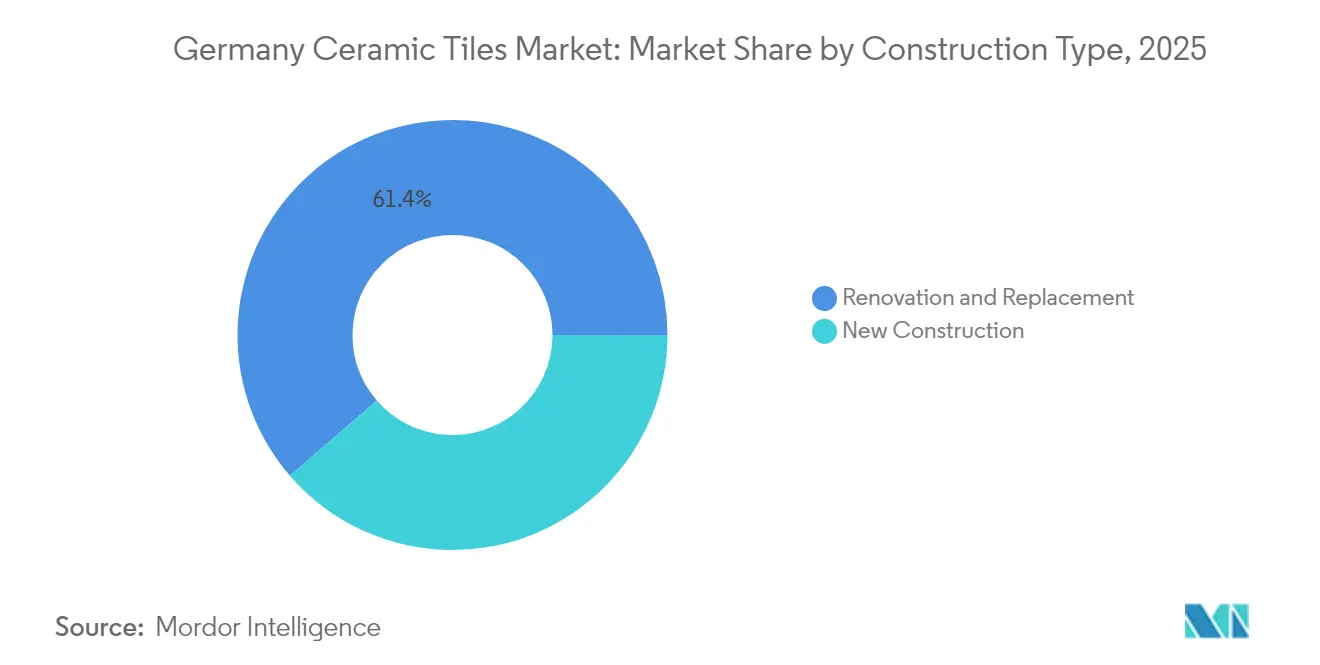

- By construction type, renovation and replacement commanded 61.35% of the Germany ceramic tiles market share in 2025, new construction remains subdued as building permits fell 27% year-on-year.

- By distribution channel, specialty tile stores retained 40.10% of the Germany ceramic tiles market share in 2025, but online retail is on track for a 10.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising renovation demand in post-COVID housing upgrades | +1.2% | National hubs such as Munich, Hamburg, Berlin | Medium term (2-4 years) |

| Shift toward large-format porcelain slabs | +0.8% | Spill-over from Italy and Spain into Germany | Long term (≥ 4 years) |

| Accelerated adoption of thin tiles for façades | +0.6% | Core EU markets | Medium term (2-4 years) |

| Government subsidies for energy-efficient refurbishments | +0.9% | Bavaria, Baden-Württemberg early adopters | Short term (≤ 2 years) |

| Growing preference for antibacterial glazed surfaces | +0.5% | Global demand, strong in healthcare projects | Long term (≥ 4 years) |

| Increasing demand for sustainable, locally sourced ceramic tiles | +0.7% | Germany, especially in Saxony and Thuringia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Renovation Demand in Post-COVID Housing Upgrades

Germany’s retrofit momentum is accelerating as households channel savings into comfort and energy-efficiency measures after an extended time at home. Under the BEG scheme, tile-laying services qualify for a tax reduction of up to EUR 40,000 (USD 42,800) per property, bolstering installations in bathrooms, kitchens, and insulated façades[1]Bundesministerium der Finanzen, “Steuerliche Förderung energetischer Gebäudesanierungen,” bundesfinanzministerium.de.. Renovation now accounts for 61.99% of construction activity, dwarfing new builds as approvals declined sharply in 2024. Academic modeling shows the housing stock must undergo full-scale renovation of 2.5% of floor area annually to align with 2045 climate targets. This regulatory clarity locks in demand visibility for the Germany ceramic tiles market, especially in interior spaces where ceramics deliver durability, hygiene, and aesthetic versatility. As material inflation eases, postponed projects are expected to resume, further underpinning volume growth.

Shift Toward Large-Format Porcelain Slabs

Retailers report surging purchases of XXL formats exceeding 150 × 300 cm, valued for seamless looks and minimal 3 mm joints [2]Fliesen-Kemmler, “Diese Fliesen sind besonders angesagt,” fliesen-kemmler.de. . Digital inkjet systems now replicate wood, stone, and concrete with near-photographic detail, raising design expectations in premium homes and flagship commercial venues. Germany’s first ventilated façade using 3 × 1.5 m maxi-slabs was installed at the Fliesen Thomas showroom, validating exterior suitability of these products. Installer training and specialist handling tools are expanding as slab thickness drops below 6 mm, reducing structural loads yet increasing breakage risk during transport. The premium pricing of large-format porcelain lifts average selling prices, strengthening value growth within the Germany ceramic tiles market.

Accelerated Adoption of Thin Tiles for Façades

Ventilated façade systems employing 4.5-6 mm porcelain help meet EU energy-performance regulations by reducing thermal bridges and enabling rear-ventilation. Lightweight panels cut façade weight by up to 60% compared with conventional ceramics, easing retrofits on older structures constrained by load capacity. German municipalities now encourage façade over-cladding as a pathway to comply with building-envelope standards under the revised EPBD. Manufacturers are pairing thin tiles with proprietary aluminum support rails, boosting installation speed and adjustability. As architects chase monolithic exterior aesthetics, façade demand is forecast to outpace traditional wall cladding within the Germany ceramic tiles market.

Government Subsidies for Energy-Efficient Refurbishments

Federal incentives under BEG and KfW programs reimburse 40% of eligible renovation costs, spurring bathroom updates that often require new waterproofing and tiled surfaces. Subsidy guidelines explicitly recognize tile work as a qualifying skilled trade, shortening return-on-investment periods for homeowners. Banks report loan uptake rising fastest in Bavaria and Baden-Württemberg, regions with high detached-house concentrations. Coupled with declining mortgage rates, stimulus measures act as short-term accelerators for the Germany ceramic tiles market. Builders anticipate a funding wave into 2026 as additional EU climate-fund envelopes reach local governments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas prices inflating kiln firing costs | -0.9% | Industrial clusters in North Rhine-Westphalia and Saxony | Short term (≤ 2 years) |

| Tightening EU carbon regulations on heavy ceramics manufacturing | -1.1% | EU-wide factories | Long term (≥ 4 years) |

| Labor shortages in German construction sector | -0.7% | National, acute in Bavaria and NRW | Medium term (2-4 years) |

| Rising competition from low-cost imports, especially from Turkey and India | -0.8% | National, with stronger effects in price-sensitive markets like Eastern Germany | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Gas Prices Inflating Kiln Firing Costs

Gas supplies cover roughly 85% of energy demand in tile kilns, and recent price swings have driven production-cost spikes of up to 40% quarter-on-quarter. Several German plants now trial LPG conversions that promise steadier pricing but require bulk-storage yards and vaporizer systems. Waste-heat recovery is gaining traction; new thermal-battery installations store surplus exhaust heat for use in drying lines. While these retrofits temper cost volatility, they necessitate capital outlays that smaller producers find difficult to finance. Persistent price instability continues to weigh on margins across the Germany ceramic tiles market.

Tightening EU Carbon Regulations on Heavy Ceramics Manufacturing

Revisions to the EU ETS and Construction Products Regulation mandate 83-87% greenhouse-gas cuts by 2050, pressuring tile makers to pivot toward electrified firing, green hydrogen, or carbon-capture options. Villeroy and Boch’s Eco-Stock heat-storage pilot aims to recover 5.5 GWh yearly and avoid 1,000 t of CO₂. Yet breakthrough alternatives remain commercially uncertain, raising stranded-asset fears for investments in new fossil-based kilns. Compliance costs could erode the price competitiveness of domestic output versus imports, constraining the medium-term growth outlook for the Germany ceramic tiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Generates Premium Value

Porcelain tiles captured 45.12% of the Germany ceramic tiles market size in 2025 as frost resistance and low water absorption allowed them to displace natural stone in upscale projects. Thin large-format porcelain panels are forecast to expand at a 9.18% CAGR, propelled by rising façade applications and minimalist interior trends. Glazed ceramic holds a 38.35% share and continues to serve budget-conscious renovations, while unglazed bodies dominate industrial floors requiring high abrasion resistance. Mosaic tiles remain niche but command elevated prices per square meter in hospitality refurbishments. Growing acceptance of antibacterial porcelain further elevates porcelain’s average selling price, boosting revenue growth ahead of volume gains.

German plants are investing in third-generation digital printers that support up to 12 color bars and texture-mapping, broadening design latitude. Slip-resistant micro-structures and photocatalytic coatings amplify performance in wet environments. Production automation now allows same-line switching between 6 mm panels and classic 10 mm formats, sharpening flexibility. These technical gains anchor porcelain’s premium positioning and reinforce its leadership in the Germany ceramic tiles market.

By Application: Floors Dominate While Façades Accelerate

Flooring represented 70.05% of demand in 2025, reflecting the mechanical loads and frost cycles typical of German climate zones. Large-format porcelain with rectified edges supports near-seamless installations that reduce grout maintenance in open-plan interiors. Wall tiles secured a 21.15% share, fueled by bathroom and kitchen upgrades that leverage antibacterial and easy-clean glazes. Façades recorded the fastest CAGR at 7.86%, driven by thin-tile cladding systems that integrate insulation layers and rain-screen designs. Roofing remains heritage-focused, with ceramic shingles specified on landmark restorations and premium countryside homes.

Energy codes encourage exterior retrofits that combine thermal panels with lightweight ceramics, prompting façade specialists to certify anchor devices and adhesive mortars with DIBt approvals. This engineering progress positions façades as a structural growth pillar for the Germany ceramic tiles market.

By End-User: Residential Renovation Leads, Hospitality Gains

Homeowners generated 58.10% of sales in 2025, as tract housing built before 1990 enters its second major refurbishment cycle. Bathroom overhauls, kitchen backsplashes, and basement conversions underpin steady volumes. Commercial uses, from retail outlets to offices, held a 41.90% share but face budget scrutiny amid slower macro growth. Hospitality projects are on track for a 6.92% CAGR through 2031, with hoteliers adopting large-format antibacterial porcelain to modernize guest-room finishes. Health-care and educational facilities increasingly specify slip-resistant, photo-catalytic surfaces to satisfy hygiene mandates. Case studies such as the 18,000 m² Tinnerbäcksbadet leisure center show German suppliers’ capability to deliver integrated pool-edge and waterline solutions. These high-spec applications reinforce brand credibility and drive differentiation within the Germany ceramic tiles market.

By Construction Type: Renovation Outpaces New Build

Renovation and replacement projects dominate with 61.35% market share in 2025, growing at 6.22% CAGR as Germany's construction sector shifts from new-build focus to existing building upgrades. New construction accounts for a 38.65% share but faces headwinds from reduced building permits, high financing costs, and regulatory complexity that delays project starts. The German construction industry association ZDB reports total construction turnover declined 4% in real terms during 2024, with residential completions falling to 250-255,000 units versus 294,400 in 2023.

Government policy increasingly favors renovation over new construction through BEG subsidies, KfW loan programs, and tax incentives that explicitly include ceramic tile installation as eligible energy-efficiency measures. BAFA grants up to 40% for renewable heating system replacements, often involving bathroom and kitchen renovations that drive ceramic tile demand, while KfW loans up to EUR 150,000 (USD 176,360) per residential unit support comprehensive building envelope upgrades. The regulatory framework creates sustained demand visibility for renovation-focused ceramic tile applications, particularly in bathroom modernization, kitchen upgrades, and façade improvements linked to thermal insulation projects.

By Distribution Channel: Digital and Direct Models Expand

Specialty tile and stone stores maintain a 40.10% market share in 2025, leveraging product expertise, design consultation, and installation services that justify premium positioning. Online retail represents the fastest-growing channel at 10.21% CAGR, driven by digital transformation initiatives and changing consumer research behavior. DIY stores account for a 25% share, serving price-sensitive residential customers and smaller renovation projects, while direct sales to contractors capture 8% share through project-based relationships and bulk pricing advantages.

The digital shift reflects broader retail evolution as consumers increasingly research products online before purchasing, even when final transactions occur through traditional channels. Major German retailers like HORNBACH and Fliesen-Kemmler invest in digital showrooms, augmented reality visualization tools, and e-commerce platforms that bridge online research with in-store consultation. Professional contractors increasingly prefer direct relationships with manufacturers or specialized distributors that provide technical support, project-specific logistics, and installation training. The channel evolution creates opportunities for manufacturers to capture higher margins through direct relationships while requiring investments in digital capabilities and customer service infrastructure.

Competitive Landscape

The top five brands accounted for just over half of the 2024 market revenue, indicating a moderately concentrated landscape that still offers opportunities for niche players. Villeroy and Boch AG led the market, capitalizing on its extensive dealer network and strong premium brand positioning. Deutsche Steinzeug Cremer and Breuer AG followed, with a solid foothold in public pool and civic building projects. Marazzi Group Germany also held a significant share, drawing strength from Italian design expertise and the global scale of its parent company, Mohawk. Sto SE’s acquisitions of STRÖHER Gruppe and GEPADI FLIESEN GmbH illustrate vertical integration that unites façade systems with ceramic production[4]Sto SE, “Presentation for investors,” sto.de..

Italian manufacturers maintain a strong presence through German subsidiaries and distribution partnerships, with Marazzi Group Germany achieving a 10.4% market share through retail penetration and economies of scale via the parent company Mohawk Industries. Technology adoption creates competitive advantages as manufacturers invest in digital printing, large-format production, and antibacterial surface treatments that command premium pricing and specification preference.

Innovation-driven competition focuses on sustainability credentials, energy efficiency, and smart building integration as regulatory requirements and customer preferences evolve. Companies investing in decarbonization technologies, circular economy practices, and digital transformation capabilities position themselves advantageously for long-term market evolution. The competitive landscape rewards technical expertise, regulatory compliance, and customer relationship management rather than pure scale advantages.

Germany Ceramic Tiles Industry Leaders

Villeroy & Boch AG

Deutsche Steinzeug Cremer & Breuer AG (Agrob Buchtal)

Marazzi Group (Germany)

Steuler Fliesen GmbH

Porcelaingres GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Argelith launched updated porcelain stoneware product line emphasizing durability for industrial applications, positioning German manufacturing capabilities in high-performance ceramic segments.

- March 2025: Hansgrohe Group reported fiscal 2024 sales of EUR 1.38 billion (USD 1.62 billion) with domestic German sales of EUR 326.6 million (USD 383 million), indicating stable demand in the sanitary ceramics and integrated bathroom solutions market.

- March 2025: Villeroy and Boch Group reported consolidated revenue of EUR 1.42 billion (USD 1.66 billion) for 2024, up 57.6% following Ideal Standard acquisition, with Bathroom and Wellness Division contributing EUR 1,098.9 million and expanding market presence in fittings and large-scale projects across healthcare, hospitality, and residential sectors.

- February 2025: German Tile Association (Fliesenverband) confirmed German ceramic tile industry participation at BAU 2025, highlighting industry coordination and market presence at Europe's leading construction trade fair.

Germany Ceramic Tiles Market Report Scope

A complete background analysis of the Germany Ceramic Tiles Market, which includes an assessment of the National accounts, economy, and emerging market trends by segments, significant changes in the market dynamics, and the market overview, is covered in the report. German Ceramic Tiles Market is segmented by Product (Glazed, Porcelain, Scratch Free, Other Products), Application (Floor Tiles, Wall Tiles, Other Applications), Construction Type (New Construction, Replacement, and Renovation), and End User (Residential, and Commercial).

Glazed Ceramic Tiles

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices and Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile and Stone Stores |

| Home Improvement and DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

| Glazed Ceramic Tiles | Unglazed Ceramic Tiles | |

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices and Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile and Stone Stores | |

| Home Improvement and DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

Key Questions Answered in the Report

What is the current value of the Germany ceramic tiles market?

The market is valued at USD 2.08 billion in 2026 and is projected to reach USD 2.41 billion by 2031.

Which product type holds the largest share?

Porcelain tiles lead with 45.12% of 2025 revenue, favored for frost resistance and large-format availability.

How fast is online retail growing for ceramic tiles in Germany?

Online sales are forecast to expand at a 10.21% CAGR through 2031 as shoppers embrace digital showrooms and AR tools.

Why are thin porcelain panels gaining popularity in façades?

They reduce structural load, facilitate ventilated rain-screen designs, and help buildings meet EU energy-performance standards.

How do energy subsidies support tile demand?

The BEG program allows homeowners to deduct up to EUR 40,000 (USD 46,880) of renovation costs, with tile-laying explicitly eligible for reimbursement.

Page last updated on: