Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

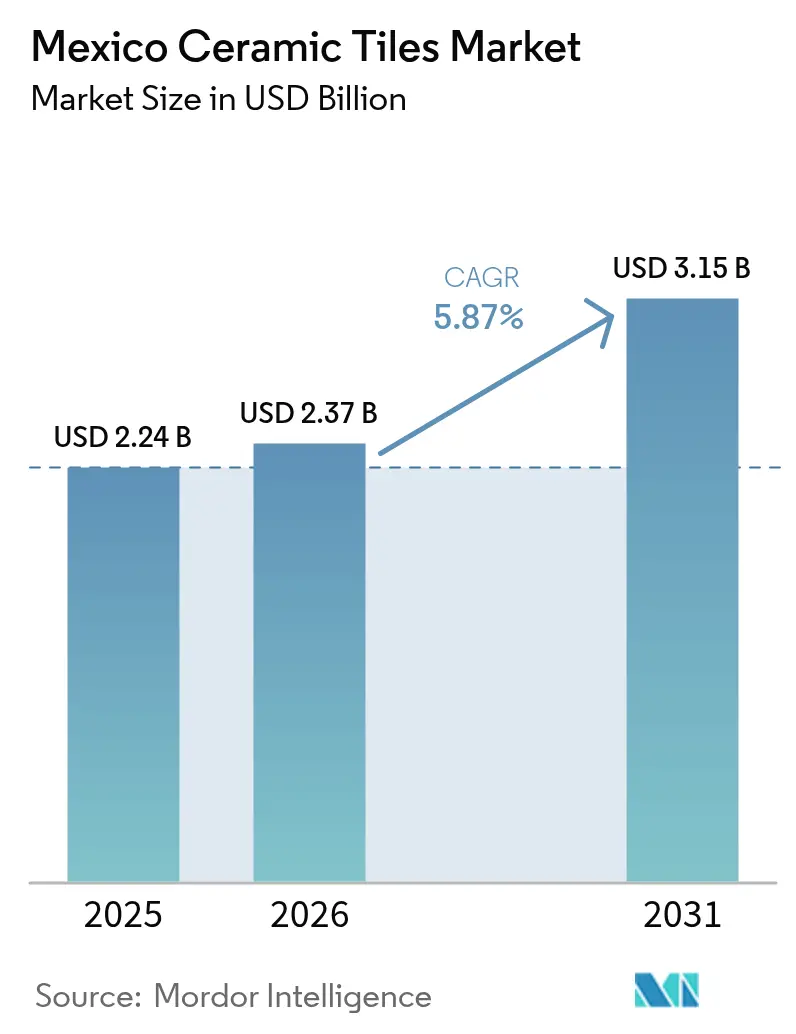

| Base Year Market Size (2025) | USD 2.24 Billion |

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

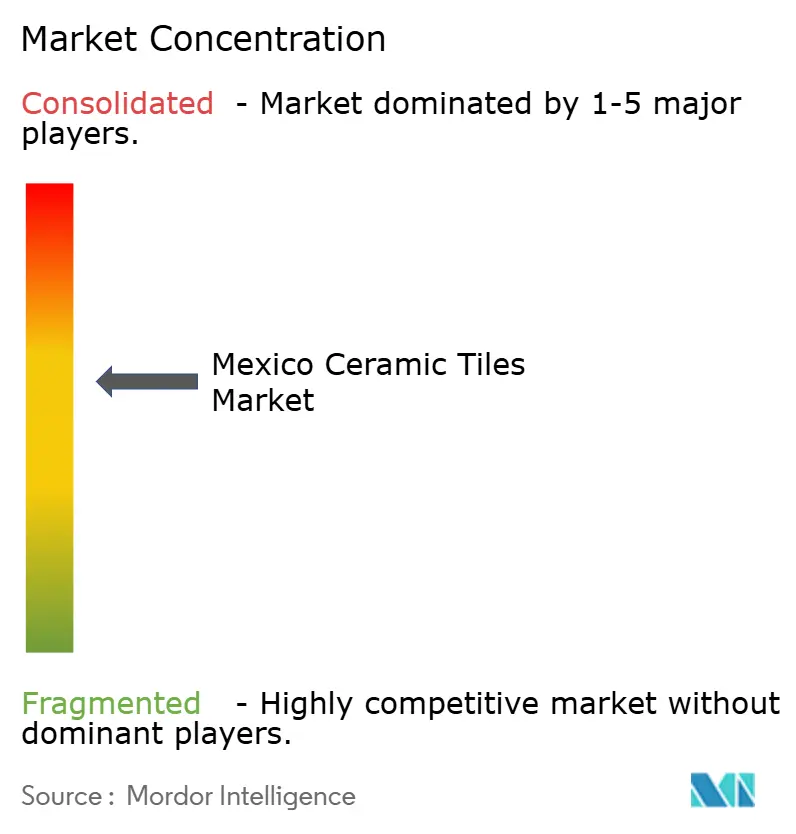

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Ceramic Tiles Market Analysis by Mordor Intelligence

The Mexico ceramic tiles market size was valued at USD 2.24 billion in 2025 and estimated to grow from USD 2.37 billion in 2026 to reach USD 3.15 billion by 2031, at a CAGR of 5.87% during the forecast period (2026-2031). Robust federal housing programs, an expanding tourism footprint, and capacity additions from global producers position the Mexico ceramic tiles market for steady volume gains through the forecast period. Peso cost advantages versus Asian supply, paired with proximity to the United States, continue to draw foreign direct investment into tile manufacturing clusters in Central, Bajío, and Northern Mexico. Energy-efficiency upgrades such as low-NOx kilns and alternative fuel trials are beginning to offset natural-gas volatility, sustaining competitive pricing even as utility costs fluctuate. Strategic acquisitions—including Mohawk Industries’ 2023 purchase of Vitromex—signal accelerating consolidation that will shape technology adoption and distribution reach across the Mexico ceramic tiles market.

Key Report Takeaways

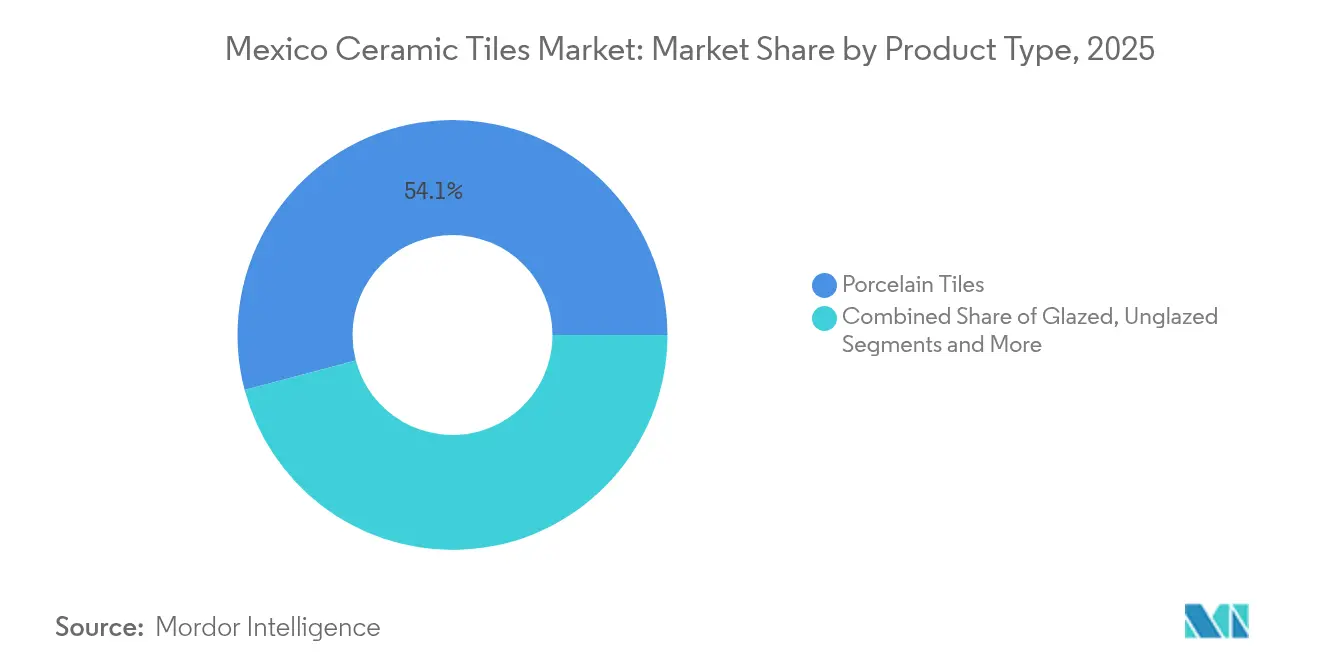

- By product type, porcelain captured 54.12% of the Mexico ceramic tiles market share in 2025, while mosaic tiles are projected to expand at a 6.55% CAGR through 2031.

- By application, floor installations held 60.75% of the Mexico ceramic tiles market size in 2025, whereas wall applications are growing at a 5.88% CAGR to 2031.

- By end-user, residential construction accounted for 61.05% of 2025 revenue, and it remains the fastest-growing segment with a 6.12% CAGR through 2031.

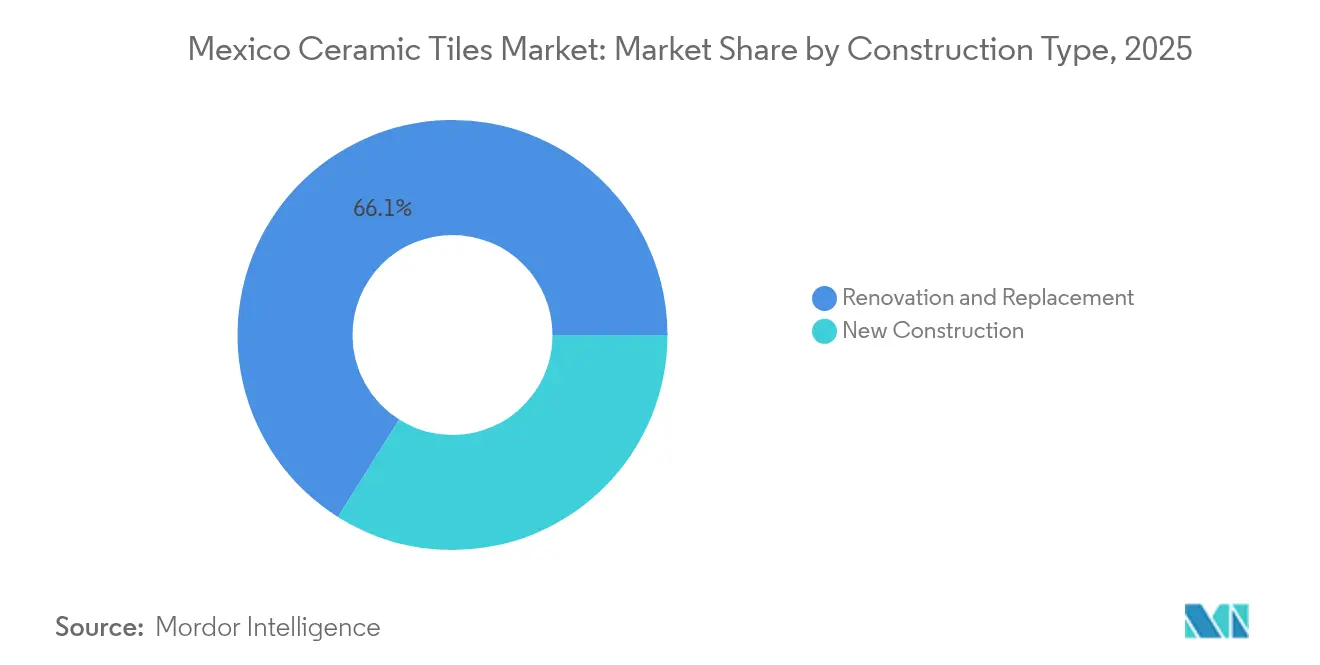

- By construction type, renovation and replacement retained 66.05% share of the Mexico ceramic tiles market in 2025, yet new construction leads growth at a 6.39% CAGR during the forecast horizon.

- By distribution channel, specialty tile and stone stores dominated with 41.55% 2025 share, while online retail is on track for a 7.28% CAGR to 2031.

- By geography, Central Mexico commanded 36.75% revenue in 2025, but the Yucatán Peninsula is forecast to post the quickest regional expansion at a 6.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust growth in residential construction fueled by government affordable-housing initiatives | +1.2% | National, with concentration in Central Mexico and Estado de México | Medium term (2-4 years) |

| Rising consumer preference for durable, low-maintenance flooring materials | +0.8% | National, with premium segments in Central Mexico and Yucatán Peninsula | Long term (≥ 4 years) |

| Expansion of domestic production capacity lowering unit costs and improving availability | +1.0% | Central Mexico, Northern Mexico, Bajío region | Medium term (2-4 years) |

| Increasing adoption of digital ink-jet printing enabling hyper-local design motifs | +0.6% | Central Mexico, Bajío, with export potential to North America | Long term (≥ 4 years) |

| Nearshoring manufacturing shift from Asia to Mexico for North-American supply-chain resilience | +0.9% | Northern Mexico, Bajío, with spillover to Central Mexico | Long term (≥ 4 years) |

| Booming hospitality-sector investments driven by tourism growth fueling premium tile demand | +0.7% | Yucatán Peninsula, Baja California, coastal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Residential Construction via Federal Housing Programs

Federal initiatives targeting 1 million social-housing units through INFONAVIT and CONAVI create a predictable baseline demand that smooths out cyclical slowdowns in private residential building. Early 2025 construction starts on 27 government-owned plots across 12 states, adding immediate volume visibility for ceramic tile suppliers. Expanded social-leasing provisions that prohibit balance updates for unemployed borrowers improve mortgage affordability, broadening the addressable homeowner base. Land banks of more than 2,000 hectares ensure a multi-year pipeline for developers, supporting longer production runs and lower unit costs for large-format floor tiles. As grants prioritize vulnerable populations, mid-range glazed products are likely to benefit most, raising the Mexico ceramic tiles market’s average selling price while preserving affordability.

Rising Preference for Durable, Low-Maintenance Flooring

Urban households are favoring hard-surface solutions that withstand heavy foot traffic, resist moisture, and simplify cleaning in compact living spaces. Ceramic products with antimicrobial glazes introduced by Mohawk Industries directly respond to heightened hygiene awareness in post-pandemic interiors[1].Source: Mohawk Industries, “Antimicrobial Tile Portfolio,” mohawkindustries.com Hospitality operators also gravitate toward matte-finish porcelain that masks scuffs and maintains visual uniformity in high-occupancy corridors. Digital print lines now replicate natural stone grains and handmade motifs without the maintenance burden of porous materials, expanding ceramic share against engineered wood. These lifestyle shifts collectively add 0.8 percentage points to the forecast CAGR for the Mexico ceramic tiles market.

Digital Ink-Jet Printing for Localized Designs

Ink-jet platforms support rapid design turnovers that echo indigenous patterns and regional color palettes in small production runs, something traditional screen printing could not deliver cost-effectively. The MANUFACTURA–Uriarte Talavera collaboration integrates 3D printers to elevate pattern depth while preserving artisanal glazes, expanding export appeal for heritage-styled wall tiles. Flexible printheads lower setup expenses, encouraging producers to chase niche hospitality projects seeking custom statement pieces. Shorter lead times also help Mexican converters react to U.S. fashion shifts without holding excessive inventory. The result is a 0.6 percentage-point lift in long-run CAGR for the Mexico ceramic tiles market as differentiated products command healthy margins.

Nearshoring Shift from Asia to Mexico

Mexico attracted USD 43.9 billion of 2023 foreign direct investment, much of it earmarked for supply-chain realignment away from Asia, reinforcing the need for local building-material inputs[2]Source: Expansión, “Nearshoring: México capta 43.9 mmd de IED,” expansion.mx. Automotive suppliers clustering in the Bajío require production floors, canteens, and worker housing, each demanding high-durability floor tiles. Tile makers gain a 35% landed-cost edge versus Chinese exporters into the U.S. Southwest, opening bilateral sales channels for plants in Coahuila and Nuevo León. The co-location of tile and component factories reduces travel emissions, aligning with OEM sustainability metrics that increasingly factor into supplier awards. As these facilities come online, they contribute 0.9 percentage points to the Mexico ceramic tiles market’s compound growth outlook.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in natural-gas prices elevating kiln operating expenses | -0.8% | National, with highest impact in Central Mexico and Northern manufacturing hubs | Short term (≤ 2 years) |

| Competition from luxury-vinyl tiles and engineered-wood alternatives | -0.6% | National, with premium segments in Central Mexico and Northern regions | Medium term (2-4 years) |

| Regional water-scarcity restrictions hindering clay extraction and processing | -0.5% | Northern Mexico, Central Mexico, with emerging concerns in Bajío region | Long term (≥ 4 years) |

| Peso exchange-rate fluctuations impacting imported glazing-material costs | -0.4% | National, with export-oriented manufacturers in Northern Mexico and Baja California most affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Natural-Gas Price Volatility Raising Kiln Costs

Fired-tile production consumes 25-35% of its factory energy in kilns, making delivered costs vulnerable to spot-market spikes in natural-gas tariffs. Mexican industrial rates fluctuate alongside peso-denominated contracts, complicating budgeting for capacity expansions. Pamesa’s switch to alternative gas suppliers netted EUR 85–90 million in annual savings, proving that procurement agility can mitigate fuel risk. Research into methanol-assisted combustion indicates a 17.4% reduction in firing time and lower CO₂ emissions, offering a long-term hedge against fossil-fuel swings[3]Source: MDPI, “Energy Savings in Methanol-Fired Kilns,” mdpi.com.. Until such conversions scale, gas volatility trims 0.8 percentage points from near-term Mexico ceramic tiles market growth.

Competition from Luxury-Vinyl Tile and Engineered Wood

Low installation costs and click-lock formats enable LVT to capture share in budget-focused renovations, particularly in northern border towns with U.S. design influence. Mohawk’s decision to add LVT output alongside ceramic at its Mexicali complex highlights a defensive diversification strategy. Ceramic retains clear advantages in moisture-prone kitchens and high-traffic hospitality corridors, yet price spreads can prompt consumers to compromise on longevity. Retailers are bundling underlayment and rapid-set adhesives with LVT, lowering installed cost per square meter versus entry-level glazed ceramic. Consequently, alternative surfaces shave 0.6 percentage points off projected CAGR for the Mexico ceramic tiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Strength Meets Mosaic Upswing

Porcelain tiles accounted for 54.12% of the Mexico ceramic tiles market share in 2025 on the strength of high abrasion resistance and large-format offerings that align with modern minimalist design. Mosaic products, although smaller in unit volume, are registering a 6.55% CAGR through 2031 as boutique hotels and premium residential baths specify intricate patterns previously reserved for artisanal hand-cuts. The Mexico ceramic tiles market size for porcelain is forecast to reach USD 1.71 billion by 2031, supported by upgrades to ink-jet lines that broaden wood-look and terrazzo variants without sacrificing dimensional stability. Decorative and handmade categories attract architects seeking authentic Mexican motifs, leveraging Talavera-style glazes and textured finishes to differentiate hospitality lobbies. Unfinished porcelain bodies are also gaining traction in outdoor installations where slip ratings and freeze-thaw performance are critical to warranty compliance.

Rapid-fire kilns in the Dal-Tile Mexicali plant raise porcelain throughput while holding energy intensity below regional benchmarks, underscoring efficiency gains that reinforce segment leadership. Mosaic hits its CAGR targets largely through value-added shower-floor sheets and feature walls that sell at premium price points per square meter. As product catalogs expand, tile distributors bundle trim pieces and coordinating borders, boosting average transaction values. Porcelain suppliers are layering antimicrobial finishes that promise lifetime surface hygiene, an attribute hospital projects elevate in tender scoring. On balance, porcelain remains the anchor of the Mexico ceramic tiles market, but mosaics provide incremental margin lift through 2031.

By Application: Floor Dominance Balanced by Wall Momentum

Flooring commanded 60.75% of 2025 revenue as builders remain inclined toward durable, low-maintenance surfaces for high-traffic residential zones and commercial common areas. The Mexico ceramic tiles market size for floor applications is projected to top USD 1.91 billion by 2031, even as wall installations accelerate at a 5.88% CAGR over the same window. Moisture and impact resistance keep ceramic floors entrenched in kitchens and corridors, displacing laminate solutions that swell under spills. Wall tiles are catching up through decorative feature panels in hotels and urban condos eager for texture and color pops that paint cannot deliver. Digital print technologies allow seamless wraparound murals and metallic accents that support wall-segment premiumization.

Advances in large-format rectified slabs are shrinking grout lines on walls, enhancing aesthetics and easing cleaning regimens demanded by hospitality operators. Flooring still leads replacement cycles in government housing programs due to standardized sizes that streamline procurement logistics. Nonetheless, quick-set mortars now enable same-day wall grouting, making vertical installations more contractor-friendly and bolstering growth rates. Outdoor facades and ventilated cladding systems offer new surfaces for wall-oriented porcelain, especially in hot coastal regions seeking thermal buffering. Overall, floors stay volumetric leaders, but walls deliver faster revenue upside within the Mexico ceramic tiles market.

By End-User: Residential Breadth Sustains Dual Momentum

Residential projects held 61.05% of market value in 2025 and are on track for a 6.12% CAGR, driven by federal homebuilding pipelines and urban family formations. INFONAVIT’s 500,000-unit mandate guarantees baseline ceramic volumes across economic tiers, channeling demand toward mid-gloss glazed floor tiles with high skid resistance. Commercial buyers, notably hotels and retail centers, prioritize premium porcelain with sub-0.5% water absorption rates that minimize maintenance. Healthcare complexes lean on antimicrobial wall panels, while education facilities specify high-albedo tiles to lower artificial-lighting costs. Transport hubs employ extra-thick pavers for concourse durability, carving a stable niche in industrial-grade formats.

Residential kitchen and bath remodels account for more than half of renovation-segment units, underpinning steady pull-through for 30×60 cm and 60×60 cm field tiles. Commercial value nevertheless outperforms in square-meter pricing via large-format slabs and mosaics priced at sizeable premiums. Hospitality’s bounce-back to pre-2020 occupancy recovered capex budgets for resort-style pool decks and rooftop bars demanding slip-rated ceramics. Office developers incorporate polished porcelain in lobby statements that replicate marble veining without natural-stone cost or maintenance. This dual-engine structure secures balanced volume and margin streams within the Mexico ceramic tiles market.

By Construction Type: Renovation Bulk Meets New-Build Velocity

Renovation and replacement accounted for 66.05% of 2025 revenue as Mexico’s aging housing stock cycles through flooring upgrades every eight to ten years. Yet new construction is rising faster (6.39% CAGR) on the back of public housing and nearshoring industrial campuses. Government subsidies for first-home buyers widen eligibility pools, funneling significant ceramic orders into greenfield subdivisions. Manufacturing parks announced in Coahuila and Querétaro embed plant floors, dormitories, and cafeteria fit-outs that each specify hard surfaces compliant with ISO slip standards. Renovation activity remains resilient, with premium mosaics and rectified wall tiles favored in bathroom refurbishments that emphasize quick occupancy turnaround.

Quick-dry self-leveling compounds reduce downtime for occupied renovations, making ceramic replacements less disruptive and retaining share versus floating LVT systems. New-build high-rise residential towers in Mexico City employ lightweight porcelain facades to meet seismic load requirements without exceeding structural limits. The Program for the Development of the Isthmus of Tehuantepec introduces industrial-park shells that will demand large-format factory floors, extending ceramic volume to historically under-tiled southern states. Renovation growth moderates mid-decade as the bulk of post-pandemic remodeling concludes, but ongoing design-refresh cycles keep baseline volumes intact. The Mexico ceramic tiles market thus balances steady renovation flow with spirited new-construction gains.

By Distribution Channel: Stores Lead, E-Commerce Accelerates

Specialty tile and stone stores retained a 41.55% share in 2025 owing to tactile product displays, design consulting, and project-bundled accessory sales. E-commerce, expanding at a 7.28% CAGR, benefits from virtual room-visualizer apps that bolster consumer confidence in online selections. Big-box home-improvement chains capture impulse DIY traffic through weekend promotions and install-in-a-day packages targeting entry-level homeowners. Contractor direct sales leverage volume rebates and just-in-time delivery to major commercial sites, minimizing on-site inventory and capital strain for builders. Hybrid omnichannel models-sampling online with pickup at brick-and-mortar-are bridging the convenience gap, amplifying online conversion rates.

Virtual reality showrooms hosted by leading retailers allow users to experience tile surface textures through haptic feedback accessories, narrowing the sensory deficit that once encumbered digital sales. Logistics partners now offer tail-lift trucks fitted with pallet jacks that deliver directly into high-rise construction elevators, removing a key friction point for online pallet orders. Home-center banners are trials of scan-and-buy QR codes directing shoppers to full SKU ranges online, regaining assortment breadth without expanding shelf space. Contractor portals integrate technical data sheets and adhesive calculators, shortening bid-preparation time and reinforcing loyalty. Collectively, distribution innovations ensure the Mexico ceramic tiles market keeps pace with evolving purchasing behaviors.

Geography Analysis

Central Mexico generated 36.75% of 2025 revenue on the back of dense population centers, mature logistics networks, and entrenched production clusters anchored by Grupo Lamosa’s flagship operations. Government housing grants targeting vulnerable communities in the eastern Estado de México sustain steady tile pull-through in peri-urban projects while leveraging nearby raw-material feedstocks. Central highways and rail spurs expedite shipments to the coast and northern border, keeping freight premiums below 5% of invoice value on cross-regional orders. Local kiln know-how also supports export assignments into the U.S. Sun Belt, reinforcing factory utilization rates even when domestic demand fluctuates. With Plan México pushing a 15% increase in local manufacturing content, Central Mexico remains the hub of the Mexico ceramic tiles market.

Northern Mexico enjoys structural advantages from proximity to U.S. buyers and a wave of nearshoring activity that has doubled automotive component plant announcements since 2023. Industrial parks in Coahuila offer discounted electricity and water tariffs for energy-intensive producers, coaxing ceramic makers to expand kiln footprints in tandem with supplier facilities. Cross-border trucking lanes deliver just-in-time shipments of large-format porcelain to distributors in Texas, Arizona, and California inside 48 hours, outpacing Asian standard lead times by more than six weeks. Peso volatility can compress export margins, yet many factories hedge through U.S.-dollar revenue streams, stabilizing cash flows for reinvestment. Northern Mexico thereby consolidates its role as the export engine of the Mexico ceramic tiles market.

The Bajío macro-region, encompassing Guanajuato, Querétaro, and San Luis Potosí, captures roughly half of automotive FDI and an emerging share of aerospace assembly, both of which spawn demand for industrial floor tiles and worker housing finishes. Freight corridors connecting Bajío to 80% of the national market within three hours strengthen its pull as a distribution crossroads. Skilled labor nurtured by vocational programs supporting automotive painting translates well to precision glaze application and ink-jet line maintenance. Cluster synergies reduce component shortages and downtime, creating a virtuous cycle for ceramic throughput. As such, the Bajío delivers balanced domestic and export contribution to the Mexico ceramic tiles market.

Competitive Landscape

The Mexico ceramic tiles market exhibits moderate concentration, with domestic leaders leveraging established distribution networks while international players pursue strategic acquisitions to capture market share. Grupo Lamosa capitalizes on vertically integrated clay and glaze sourcing, streamlining costs and securing service levels for large housing contracts. Mohawk Industries’ 2023 acquisition of Vitromex doubled its domestic footprint, granting it deeper penetration into builder channels and sparking intensified product-development competition [4]Source: Mohawk Industries, “2023 Acquisition of Vitromex,” mohawkindustries.com.. Dal-Tile differentiates through U.S.–Mexico dual-site logistics and proprietary StepWise slip-resistant surfaces that meet ANSI A326.3 standards without compromising gloss. Pamesa sets a benchmark in energy cost control by renegotiating gas supply contracts and piloting methanol firing, offering a profitability template for peers grappling with utility volatility.

Digital transformation is unfolding as producers deploy IoT sensors inside roller kilns to monitor temperature gradients and flag maintenance needs before costly shutdowns. Augmented-reality design studios in flagship showrooms boost consumer engagement, allowing real-time visualizations of floor-plan layouts using tile SKUs pulled from live inventory feeds. Sustainability imperatives guide R&D toward recycled content bodies and low-lead frits, anticipating tighter environmental standards. Emerging entrants focus on artisanal and decorative niches, leveraging Mexico’s rich heritage to attract premium hospitality customers. Meanwhile, competitive pressure from LVT keeps price competition alive in entry-level residential ranges, nudging ceramic leaders to emphasize value-added coatings and lifetime warranties.

Strategic collaborations upstream and downstream are reshaping bargaining power; for example, kiln-furnace suppliers’ partner with tile makers to co-develop hydrogen-ready burners, sharing R&D costs and accelerating decarbonization roadmaps. Distribution alliances with home-center chains enable nationwide penetration without excessive capital tied up in dedicated retail footprints. Producers are experimenting with franchise models for mono-brand boutiques in secondary cities, capturing aspirational consumers upgrading kitchens and bathrooms. Export platforms remain critical, with U.S. demand accounting for nearly one-quarter of Mexican tile shipments, prompting factories to certify to North American TCNA standards. Overall, technological investment, energy hedging, and channel innovation underpin the competitive dynamics of the Mexico ceramic tiles market.

Mexico Ceramic Tiles Industry Leaders

Grupo Lamosa S.A.B. de C.V.

Interceramic Inc.

Vitromex

Dal-Tile Corporation

Cesantoni S.A. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cemex announced a USD 1.4 billion global capex plan, earmarking USD 45 million for Mexican operations that will bolster cement and aggregate availability critical to tile production.

- March 2025: Mohawk Industries completed a restructuring of its Mexican ceramic tile division, targeting USD 20 million in annual savings through plant consolidation and procurement synergies.

- February 2024: Dal-Tile finalized the acquisition of Ceramica San Lorenzo’s Mexicali facility, adding advanced ink-jet porcelain capacity geared to U.S. West Coast demand.

- January 2024: MANUFACTURA and Uriarte Talavera launched the Talavera Project to blend 3D printing with traditional glazes, elevating precision in artisanal decorative tiles.

Mexico Ceramic Tiles Market Report Scope

Ceramic tiles are made of sand, natural products, and clay, and once they are molded into a shape, they are fired in a kiln. Ceramic tiles are durable, resistant to water, moisture, and fire, and cheap as compared to other flooring products. A complete background analysis of the Mexican ceramic tiles market, which includes an assessment of the parental market, emerging trends in the segments and regional markets, and significant changes in market dynamics and a market overview, is covered in the report. The report also offers a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across various key points in the value chain.

The Mexican Ceramic Tiles Market Is Segmented By Product (Glazed, Porcelain, Scratch-Free, And Other Products), By Application (Floor Tiles, Wall Tiles, And Other Applications), By Construction Type (New Construction, Replacement, And Renovation), And By End User (Residential And Commercial). The Market Size And Forecasts Are Provided In Terms Of Value (USD) For All The Above Segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Central Mexico |

| Northern Mexico |

| Western/Bajio |

| Southern Mexico |

| Yucatan Peninsula |

| Baja California |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Central Mexico | |

| Northern Mexico | ||

| Western/Bajio | ||

| Southern Mexico | ||

| Yucatan Peninsula | ||

| Baja California | ||

Key Questions Answered in the Report

How large is the Mexico ceramic tiles market in 2026?

It stands at USD 2.37 billion and is expected to climb to USD 3.15 billion by 2031.

Which product type leads sales in Mexico?

Porcelain tiles account for 54.12% of 2025 revenue to durability and design versatility.

What is the fastest-growing regional market?

The Yucatán Peninsula is projected to expand at a 6.72% CAGR through 2031 to tourism investments.

How are online channels performing in tile distribution?

E-commerce is the quickest-expanding channel with a 7.28% CAGR as virtual visualization tools gain traction.

Which segment benefits most from federal housing programs?

The residential end-user category, already holding 61.05% share, receives consistent volume from social-housing initiatives.

What risks could slow market growth?

Volatile natural-gas prices and competition from luxury-vinyl tile alternatives could trim aggregate CAGR by 1.4 percentage points.

Page last updated on: