Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.13 Billion |

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Ceramic Tiles Market Analysis by Mordor Intelligence

The Philippines ceramic tiles market size stood at USD 1.13 billion in 2025, is estimated at USD 1.20 billion in 2026, and is forecast to reach USD 1.57 billion by 2031, reflecting a 5.58% CAGR over 2026 to 2031. Porcelain tiles lead product demand, floor formats dominate functional use, and residential projects hold the largest end-user base, shaping near-term volume visibility across private and public construction programs. Renovation-led activity is anchoring the Philippines' ceramic tiles market as aging condominium stock and provincial housing upgrades progress, while online channels are reducing delivery times to provincial sites through new fulfillment hubs. Public infrastructure pipelines under Build Better More keep institutional tile specifications in focus, especially for high-traffic transport nodes and government assets where porcelain durability and hygiene matter. Hospitality expansion adds structural demand, 158 hotel projects worth PHP 250 billion inject 40,084 new keys, with Ayala Land committing USD 500 million to double its portfolio to 8,000 rooms[1]TTG Asia, “Philippine hotel industry plans manpower roadmap to address labour shortages,” TTG Asia, ttgasia.com. This surge elevates mosaic accents and large-format porcelain slabs in lobbies, spas, and premium suites.

Key Report Takeaways

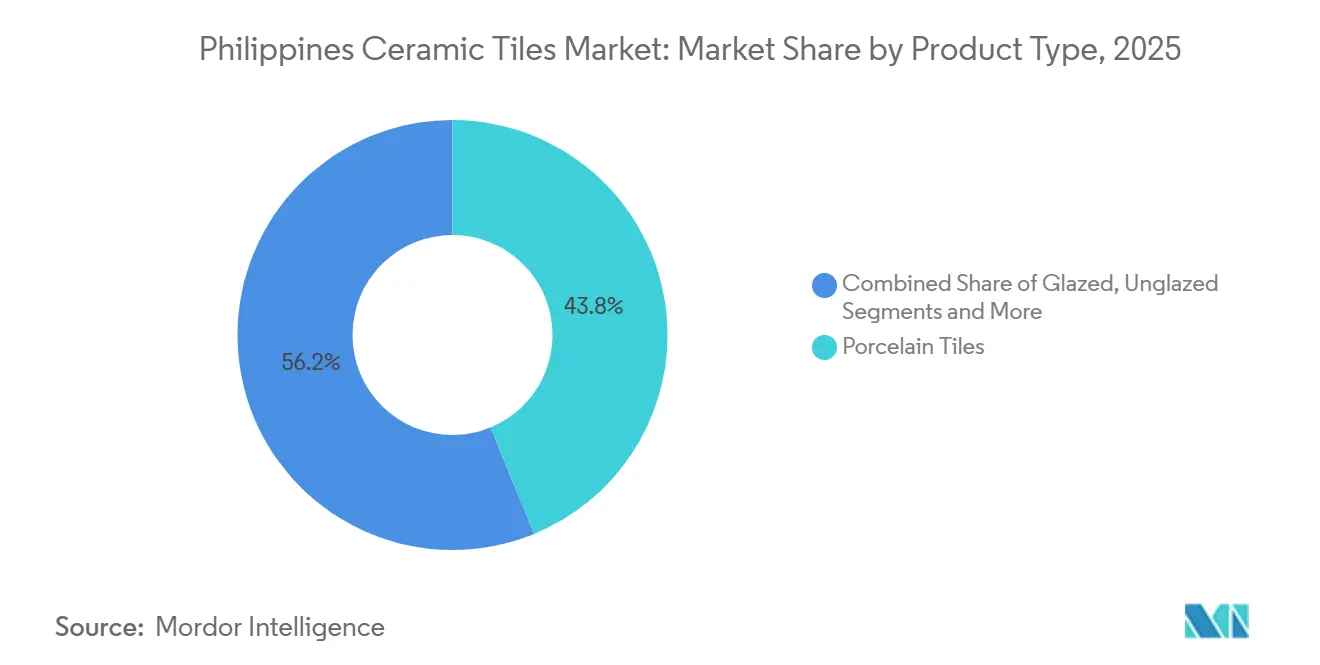

- By product type, porcelain led with 43.78% revenue share in 2025, and mosaic is projected to record the fastest 7.46% CAGR through 2031.

- By application, floor tiles accounted for 61.61% of demand in 2025, and are expected to post the fastest CAGR of 6.24% through 2031.

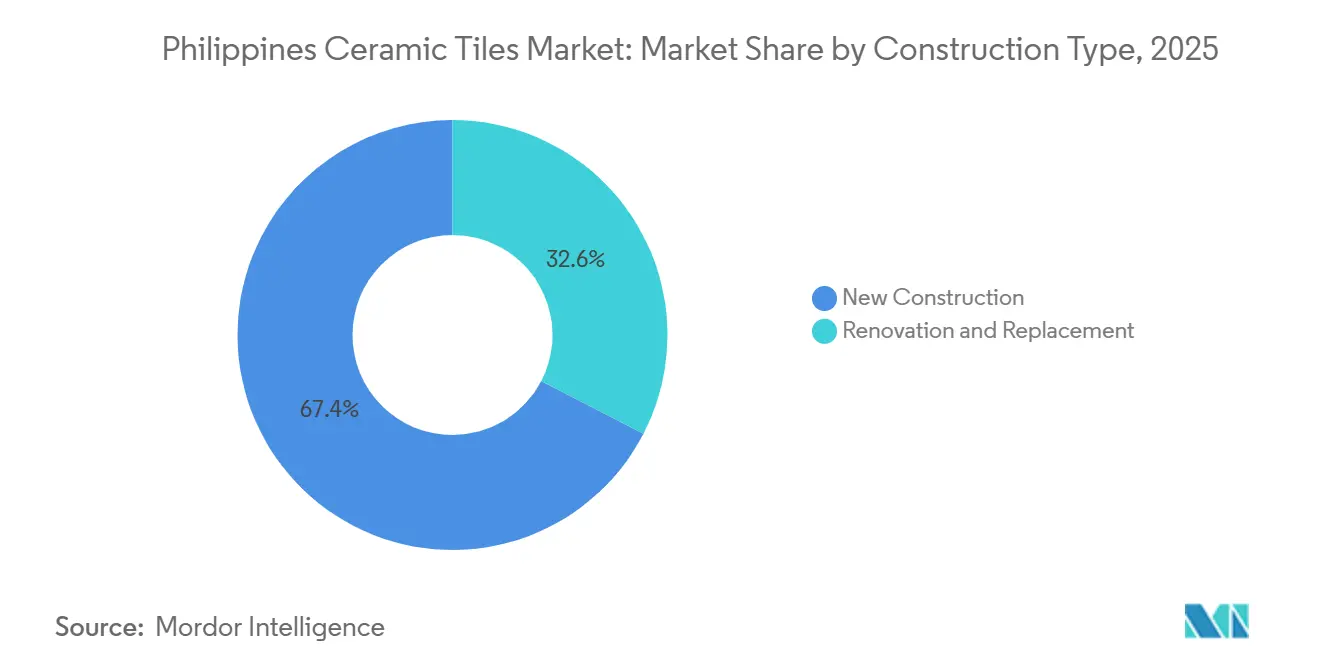

- By construction type, new construction captured 67.42% of the 2025 volume, and replacement and renovation are forecast to grow at the fastest 6.93% CAGR through 2031.

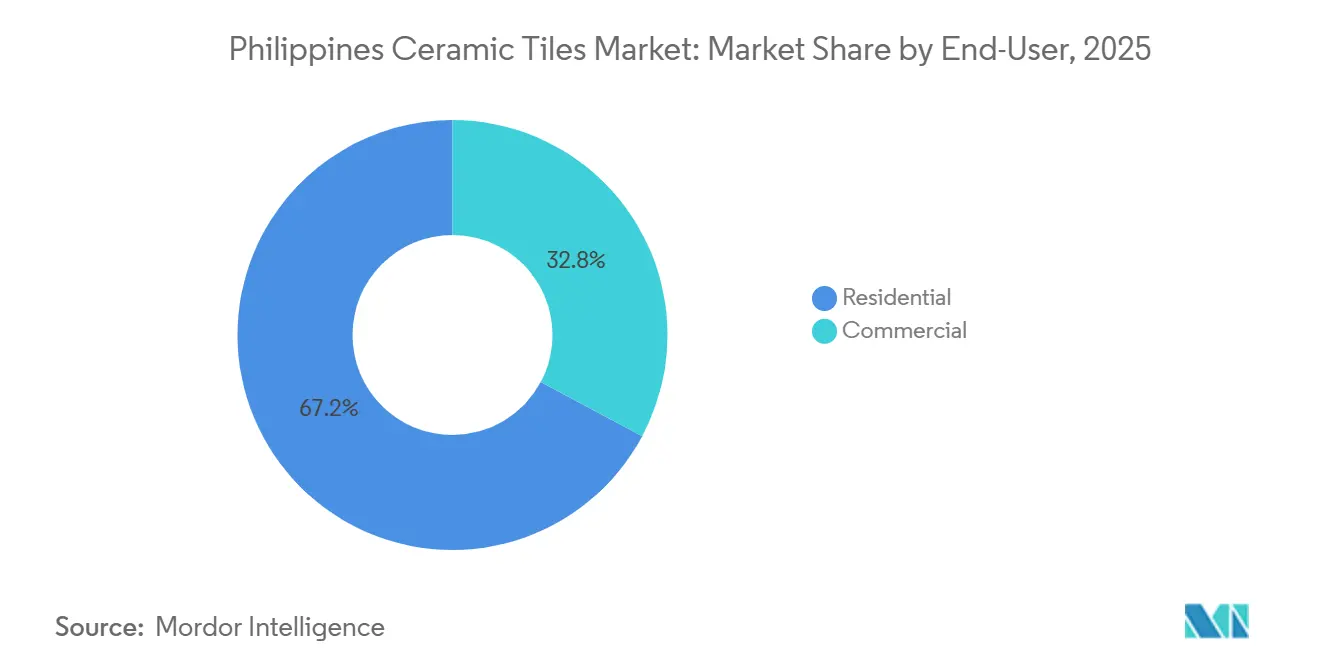

- By end-user, residential construction held a 67.20% share in 2025, and commercial construction is set to expand at the fastest 6.20% CAGR through 2031.

- By distribution channel, specialty tile and stone stores held 22.59% share in 2025, and online retail is projected to deliver the fastest 7.82% CAGR through 2031.

- By geography, Luzon led with 66.08% of 2025 sales, and the Visayas is expected to register the fastest territorial CAGR of 7.36% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steady residential construction recovery and mid-income housing programs | +1.2% | National, with early gains in Metro Manila, Calabarzon, and Central Luzon | Medium term (2-4 years) |

| Omnichannel retail expansion deepens access | +0.6% | National, accelerated adoption in Visayas, Mindanao | Short term (≤ 2 years) |

| Hospitality and resort pipeline supports premium formats | +0.9% | Luzon, Visayas, Mindanao | Medium term (2-4 years) |

| Public and private institutional projects specify durable porcelain and hygienic wall tiles | +0.8% | National, infrastructure corridors in Luzon, Mindanao | Long term (≥ 4 years) |

| Quality compliance push raises formal market share | +0.5% | National | Medium term (2-4 years) |

| Climate-resilient, anti-slip outdoor and roofing tile adoption in flood-prone areas | +0.4% | Typhoon-exposed municipalities in Eastern Visayas, Bicol, and Northern Luzon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steady Residential Construction Recovery and Mid-Income Housing Programs Drive Baseline Tile Consumption

Mid-income housing pipelines have bolstered kitchen, bathroom, and balcony tiling in ongoing projects, which supports steady utilization across porcelain and glazed formats in the Philippines ceramic tiles market. Remittance-supported purchases in regional cities strengthen mid-priced condominium specifications, with durable porcelain favored for wet areas to meet lifecycle cost goals in a tropical climate. Permit momentum softened at various points in 2025, which affected near-term unit launches, yet developers in growth corridors continue to pivot toward horizontal formats to maintain project velocity and tile uptake. Cost discipline is shaping mixed decisions, which sustains mid-tier ceramic options while premium finishes concentrate in targeted units and amenities. Overseas Filipino worker remittances reached USD 34.49 billion in 2024, with an estimated 60% channeled to real estate, particularly mid-priced condominiums in Cebu, Davao, and Pampanga that specify porcelain tiles for durability and resale appeal[2]Global Property Guide, “Philippines's Residential Property Market Analysis 2026,” Delmendo, Lalaine C, globalpropertyguide.com. In aggregate, these dynamics keep the Philippines' ceramic tiles market tied to steady residential handovers while setting a clear baseline for future upgrades.

Omnichannel Retail Expansion Deepens Access (Specialty Chains, Big-Box, E-Commerce)

National chains scaled store footprints and showroom formats to extend reach into provincial cities, which places curated tile assortments and advisory services closer to contractors and homeowners. Wilcon Depot marked a 100-store network by year-end 2024, which broadened omnichannel service coverage and logistics capacity that supports faster tile delivery to tier-2 cities. Despite softer comparable sales, Wilcon reported 6.6% same-store growth in Do-It-Wilcon formats, which points to differentiated demand for targeted tile assortments and advisory-led selling. AllHome’s nationwide presence and push for in-house assortments maintain competitive pressure on mid-tier SKUs and support bundle sales for adhesives, grouts, and waterproofing. Online storefronts compress lead times for remote buyers, which raises the service value of fast-moving adhesive systems that ship with tile orders. The channel mix, therefore, deepens access and widens the customer base for the Philippines' ceramic tiles market.

Hospitality and Resort Pipeline (New Rooms and Refurbishments) Supports Premium Formats

Tourism’s rebound and destination investments sustain demand for high-specification surfaces in hotels and resorts, which favors porcelain slabs and mosaic accents in lobbies, guest rooms, spas, and wet zones. Operators and developers target durability and hygiene features, which support materials that ease maintenance and align with brand standards. Large-format geometry reduces grout lines and shortens cleaning cycles, which appeals to upscale and luxury positioning in new builds and refurbishments. Pipeline activity across Cebu, Boracay, Palawan, and Metro Manila uplifts tile mix quality, with premium imports and design-forward local SKUs featured in flagship properties. Travellers International's USD 700 million casino resorts in Mactan and Boracay, launching construction in 2026, target premium segments with Italian and Spanish tile imports for VIP suites and gaming floors[3].

Public and Private Institutional Projects Specify Durable Porcelain and Hygienic Wall Tiles

Infrastructure Flagship Projects under Build Better More prioritize heavy footfall assets, which align specifications to anti-slip and abrasion-resistant porcelain for stations, airports, and civic facilities. The national pipeline includes 207 flagship undertakings with long-duration construction timetables, which anchor sustained institutional demand for durable ceramic solutions[4]Bangko Sentral ng Pilipinas, “Public-Private Partnerships in the Philippines’ Infrastructure Flagship Projects,” Bangko Sentral ng Pilipinas, bsp.gov.ph. Public-private partnerships are a core delivery model that channels consistent materials standards into tender documents and technical submittals. Healthcare and education facilities maintain emphasis on hygienic wall finishes and easy-to-clean surfaces, which benefits ceramic and porcelain wall systems. Strengthened oversight of material compliance further embeds PNS ISO 13006:2019 benchmarks into institutional procurement, which favors PS- and ICC-certified supply. These factors give the Philippines' ceramic tiles market stable institutional anchors that complement private sector cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High power and fuel costs raise kiln firing and logistics expenses | -0.7% | National, acute impact on domestic manufacturers in Pampanga, Cavite | Short term (≤ 2 years) |

| Tight credit and soft private construction weigh on big-ticket finishes | -0.9% | Metro Manila, major urban centers | Short term (≤ 2 years) |

| Trade-remedy uncertainty creates pricing and procurement volatility | -0.5% | National, import-reliant distributors | Medium term (2-4 years) |

| Stricter PS/ICC enforcement can disrupt the non-compliant import supply | -0.3% | National, transitory compliance window | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Power and Fuel Costs Raise Kiln Firing and Logistics Expenses

Energy intensity in tile manufacturing tightens margins for local producers when electricity and fuel prices trend higher. Utilization discipline becomes critical since suboptimal kiln cycles elevate per-unit costs and can constrain SKU breadth for mid-tier categories. Regional players have expanded renewable and alternative fuels to reduce exposure, with reported gains in biomass-based thermal energy share at the corporate level, which illustrates mitigation paths for heat-intensive operations. Logistics volatility and shipping delays have also pressured import-reliant assortments, which can lengthen lead times for budget formats. The near-term effect is cautious inventory planning by retailers and distributors that serve the Philippines ceramic tiles market, with faster turns for essentials and tighter control of slow-moving designs.

Tight Credit and Soft Private Construction Weigh on Big-Ticket Finishes

High borrowing costs and selective bank lending have moderated private project starts and slowed unit completions, which defer tile-heavy fit-outs in some locations. Home improvement demand skewed toward smaller ticket purchases, as seen in big-box retail results that reflected cautious consumer behavior in 2024. Specialty DIY formats outperformed larger depots on same-store metrics, which indicates targeted product substitution and timing shifts for bath and kitchen upgrades. A leading home improvement chain reported an 18% revenue decline in FY 2024, which it attributed to softer demand in hard categories, including tiles and related materials. Developers and contractors have adjusted procurement schedules to align with financing windows, which has shifted some tile purchasing into later quarters and heightened emphasis on cost control in specifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Leads Through Institutional Mandates, Mosaic Gains in Hospitality Accents

Porcelain tiles accounted for 43.78% of the Philippines ceramic tiles market in 2025, maintaining category leadership due to their durability, moisture resistance, and suitability for high-traffic applications across both residential and commercial construction. Residential developers continue to prefer porcelain for kitchens, bathrooms, and living areas due to its lower maintenance requirements and greater lifecycle value. At the same time, commercial spaces such as malls, offices, and transport facilities prioritize their abrasion resistance and load-bearing performance. Glazed ceramic tiles remain widely adopted in the mid-market residential segment owing to their affordability, broad design options, and compatibility with renovation projects, particularly in provincial housing upgrades. Unglazed ceramic tiles continue to serve niche industrial and utility applications where slip resistance and chemical durability remain important.

Mosaic tiles are projected to register the fastest growth, expanding at a 7.46% CAGR during 2026–2031, supported by rising demand from boutique hospitality projects, premium condominiums, wellness spaces, and decorative interior applications. As urban residential projects increasingly emphasize aesthetics and differentiated interior finishes, mosaic tiles are gaining traction in feature walls, spa zones, backsplashes, and luxury bathroom concepts. Growth is also supported by the expansion of design-led retail showrooms and curated tile display formats that improve consumer exposure to premium and decorative surfaces.

The Philippine ceramic tile market is also witnessing a gradual shift toward more organized, specification-driven procurement. Product standardization requirements, increasing awareness of installation quality, and wider adoption of bundled solutions—including adhesives, grouts, and waterproofing systems—are reinforcing demand for premium porcelain and decorative tile formats. While porcelain continues to dominate volume consumption due to its functional advantages and broad application range, mosaic tiles are expected to outpace overall market growth as developers and homeowners increasingly prioritize visual differentiation and premium interior design.

By Application: Floor Dominance Anchors Market, Roofing Surges Through Climate Codes

Floor tiles accounted for 61.61% of the Philippines ceramic tiles market in 2025, reflecting their dominant use across residential housing, commercial buildings, retail centers, offices, and institutional infrastructure where durability, ease of maintenance, and long service life are critical. Floor tiles remain the preferred application in both new construction and renovation projects due to their suitability for high-footfall areas, moisture resistance, and compatibility with modern interior designs. In residential construction, floor tiles are extensively used in living spaces, kitchens, bathrooms, and outdoor areas, while commercial developments prioritize large-format and abrasion-resistant flooring solutions for malls, transport facilities, hospitality properties, and office complexes. Wall tiles continue to maintain stable demand in bathrooms, kitchens, healthcare facilities, and educational institutions where hygienic surfaces and low maintenance requirements are important.

Floor tiles are also projected to record the fastest growth, expanding at a 6.24% CAGR during 2026–2031, supported by sustained urban housing demand, infrastructure development, and rising renovation activity across mid-income households. Increasing preference for vitrified and porcelain floor solutions, particularly in condominium developments and mixed-use projects, is accelerating replacement cycles and premiumization within the flooring segment. In addition, the expansion of tourism-related construction and commercial real estate projects is driving stronger adoption of decorative and high-performance flooring systems in hospitality and retail environments.

Specification trends increasingly favor large-format floor tiles because they offer visual continuity, easier cleaning, and improved installation efficiency in modern commercial spaces. Organized retail showrooms and contractor-led procurement are also strengthening demand for premium flooring systems bundled with adhesives, grouts, and waterproofing solutions to improve installation quality and lifecycle performance. While wall tiles continue to benefit from stable replacement demand in kitchens and sanitary applications, floor tiles are expected to remain both the largest and fastest-growing application category within the Philippines ceramic tiles market due to their broad applicability across residential, commercial, and infrastructure projects.

By Construction Type: Renovation Dominates Volume, New Builds Post Faster Growth

New construction accounted for 67.42% of the Philippines ceramic tiles market in 2025, supported by sustained residential housing development, mixed-use urban projects, commercial real estate expansion, and ongoing infrastructure investments across the country. Large-scale condominium developments, township projects, retail complexes, hospitality construction, and institutional buildings continue to generate substantial demand for ceramic floor and wall tiles during the initial fit-out phase. Public infrastructure programs, including transport hubs, airports, schools, and healthcare facilities, also contribute significantly to tile consumption, particularly for durable porcelain and commercial-grade ceramic applications. Contractor-led procurement and project-based purchasing further strengthen the dominance of new construction within the market.

Replacement and renovation activities are projected to register the fastest growth, expanding at a 6.93% CAGR during 2026–2031, driven by the aging urban housing stock, increasing condominium refurbishment cycles, and rising consumer spending on home improvement. Renovation demand is particularly concentrated in kitchens, bathrooms, balconies, and living areas where ceramic tiles are frequently upgraded to improve aesthetics, durability, and property value. The growth of mid-income housing upgrades, OFW-funded renovations, and hospitality refurbishment projects is also accelerating replacement demand, especially in Metro Manila, Cebu, and emerging urban centers.

The renovation segment is benefiting from the expansion of organized retail showrooms, contractor-led advisory services, and bundled installation solutions that simplify purchasing and reduce project execution risks for homeowners. At the same time, new construction demand continues to be reinforced by government infrastructure pipelines and private sector investments in residential and commercial developments. While new construction remains the dominant demand base due to the scale of ongoing building activity, replacement and renovation are expected to outpace overall market growth as refurbishment cycles become more frequent and consumers increasingly prioritize modernized interior finishes in the Philippines ceramic tiles market.

By End-User: Residential Leads Share and Growth, Commercial Trails Amid Hotel Pipeline

Residential applications accounted for 67.20% of the Philippines ceramic tiles market in 2025, driven by strong demand from housing construction, condominium developments, and renovation activity across Metro Manila and rapidly urbanizing provincial cities. Ceramic tiles remain a preferred flooring and wall solution in residential buildings due to their durability, moisture resistance, low maintenance requirements, and broad design availability across different price points. Porcelain and glazed ceramic tiles are widely adopted in kitchens, bathrooms, living spaces, and outdoor residential areas, particularly in mid-income and upper-middle-income housing segments. Ongoing urbanization, rising condominium turnover, and OFW-supported home improvement spending continue to reinforce residential dominance within the market.

Commercial applications are projected to register the fastest growth, expanding at a 6.20% CAGR during 2026–2031, supported by increasing investments in hospitality, retail, office developments, healthcare facilities, educational infrastructure, and transport-related construction projects. The recovery of tourism and expansion of mixed-use developments are driving stronger demand for premium porcelain, large-format flooring systems, decorative wall tiles, and mosaic applications in hotels, malls, airports, and commercial spaces where aesthetics and durability are critical. Commercial projects also tend to adopt higher-value tile formats and specification-driven procurement, contributing to faster value growth compared to residential applications.

The residential segment continues to benefit from wider access through specialty tile stores, contractor networks, and organized retail chains that improve product availability and pricing transparency for homeowners and renovators. Meanwhile, commercial demand is increasingly influenced by architect-led specifications, premium interior concepts, and long-lifecycle material requirements in high-footfall environments. Government investments in institutional infrastructure, including schools, hospitals, and transport hubs, further support commercial-grade tile demand. While residential construction remains the largest consumption base in the Philippines ceramic tiles market, commercial applications are expected to outperform overall market growth due to accelerating investments in tourism, retail modernization, and urban infrastructure development.

By Distribution Channel: Specialty Stores Maintain Leadership

Direct Sales to Contractors accounted for 42.33% of the Philippines ceramic tiles market in 2025, making it the leading distribution channel due to the contractor-driven nature of residential, commercial, and infrastructure construction activity in the country. Large developers, fit-out contractors, and construction firms typically procure ceramic tiles in bulk through direct supplier relationships to secure better pricing, standardized specifications, and synchronized delivery schedules for ongoing projects. This channel is particularly dominant in condominium developments, hospitality projects, commercial buildings, and public infrastructure works where procurement is centralized and project timelines require coordinated material supply. Contractor-led sourcing is also prominent in residential renovation activity, as homeowners frequently rely on contractors for both material selection and installation.

Online retail is projected to register the fastest growth, expanding at a 7.82% CAGR during 2026–2031, supported by increasing digital adoption among homeowners, contractors, and small builders. The expansion of e-commerce-enabled construction supply platforms, improved logistics infrastructure, and wider product visibility are helping online channels penetrate secondary cities and provincial markets. Organized retailers and tile distributors are increasingly integrating digital catalogues, virtual showroom tools, and online ordering systems to improve accessibility and reduce procurement lead times. This trend is particularly relevant for standardized tile formats, renovation-focused purchases, and small-scale contractor orders where convenience and pricing transparency are important purchasing factors.

Specialty tile and stone stores continue to play a critical role in premium product selection and specification-driven sales by offering curated showrooms, technical advisory services, and design consultation for architects, contractors, and developers. Meanwhile, home improvement and DIY chains support mid-income renovation demand by bundling tiles with adhesives, grouts, and waterproofing systems to simplify procurement for consumers and installers. Other distribution channels, including independent hardware stores and general trade networks, remain relevant in provincial markets where organized retail penetration is still developing. Overall, the distribution structure of the Philippines ceramic tiles market is increasingly evolving toward a hybrid model combining contractor-led bulk procurement with expanding omnichannel and digital retail capabilities.

Geography Analysis

Luzon accounted for 66.08% of the Philippines ceramic tiles market in 2025, supported by the concentration of population, urban housing developments, commercial real estate activity, and large-scale infrastructure projects across Metro Manila, Calabarzon, and Central Luzon. The region remains the country’s primary construction hub, with strong demand from condominium developments, mixed-use townships, retail centers, office projects, and institutional infrastructure requiring durable ceramic and porcelain tile installations. Major public infrastructure programs, including airports, transport systems, government facilities, and logistics developments, continue to generate significant tile consumption, particularly for high-performance flooring and wall applications. Luzon also benefits from the country’s most developed retail and distribution network, enabling stronger penetration of organized tile suppliers, specialty stores, and contractor procurement channels.

Visayas is projected to record the fastest growth, expanding at a 7.36% CAGR during 2026–2031, driven by accelerating tourism investments, hospitality construction, urban residential expansion, and improving regional infrastructure connectivity. Cebu remains the dominant growth center in the region, supported by hotel developments, mixed-use projects, commercial expansion, and increasing demand for premium tile formats in resorts, retail spaces, and upscale residential properties. Infrastructure improvements across Iloilo, Bacolod, and surrounding urban centers are also strengthening logistics access and supporting broader adoption of imported ceramic and porcelain products. Hospitality-led projects in the Visayas increasingly favor large-format flooring systems, decorative wall tiles, anti-slip outdoor surfaces, and mosaic applications in resort and wellness environments.

Mindanao continues to represent an emerging growth market supported by infrastructure expansion, industrial development, and rising institutional construction activity in healthcare, education, and public facilities. Retail expansion and improving contractor access are gradually increasing organized ceramic tile distribution across major Mindanao cities, reducing procurement lead times and improving product availability. Tourism-driven projects and urban development initiatives in Davao and surrounding growth corridors are also supporting incremental demand for commercial-grade and decorative tile applications. While Luzon remains the dominant consumption center due to its concentration of construction activity and distribution infrastructure, Visayas is expected to outperform other regions over the forecast period as tourism, hospitality, and urban development investments accelerate across the central Philippines.

Competitive Landscape

The Philippines' ceramic tiles market is moderately concentrated, with two domestic manufacturers and a wide array of import brands supplying retailers and project channels. Local players maintain PS-licensed production and serve institutional and residential use cases, while imports diversify designs and price points for big-box and specialty chains under ICC protocols. Specialty chains and large depots curate assortments that span entry to premium tiers, with showroom staging and store-based advisory guiding selection for large-format and feature tiles. Retail performance in 2024 showed mix shifts toward smaller tickets, yet select formats like Do-It-Wilcon posted positive same-store growth, indicating resilient category demand within focused formats.

Big-box chains emphasize in-house assortments to raise margins and control specifications, which, along with adhesives, grouts, and waterproofing bundles, enable complete solutions for contractors and DIY buyers. Strengthened customs enforcement under CMC 15-2025 incentivizes documentation-ready imports and PS-certified local lines, which reduces clearance risks for formal channels and encourages inventory turns in high-volume SKUs. On the manufacturing side, energy management remains a priority due to kiln intensity, with regional producers reporting increased renewable and alternative fuel use to curb exposure.

Strategic moves reflect this environment. Wilcon expanded to 100 stores by year-end 2024, investing in warehouses and branch upgrades to enhance nationwide availability and omnichannel services for the Philippines' ceramic tiles market. AllHome leaned into private-label assortments while optimizing operating costs and piloting energy initiatives across stores to cushion elevated utilities and protect price points in hard categories. Adhesive and construction chemical providers supported these channel strategies through integrated systems that improve installation quality and reduce callbacks, which enhances overall category value for residential and project buyers. Together, these moves signal a continued shift toward formal, compliance-ready, and service-rich distribution models across the Philippines' ceramic tiles market.

Philippines Ceramic Tiles Industry Leaders

Mariwasa Siam Ceramics Inc.

Wilcon Depot, Inc.

Floor Center (FC Tile Depot)

Niro Ceramic Philippines

AllHome Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: MSI Surfaces expanded TileTouch technology across tile collections to better match printed visual patterns with tactile surface relief, enhancing realism in porcelain products.

- August 2025: Artivo Surfaces completed the acquisition of Walker Zanger and Anthology brands, strengthening the distribution of premium surface materials, including tile, through a larger multi-brand platform.

Philippines Ceramic Tiles Market Report Scope

Ceramic tiles are flat, thin, and durable pieces made from clay and other natural materials. They are hardened by firing in a kiln at high temperatures. Commonly used for covering floors, walls, and other surfaces, ceramic tiles are known for their versatility, water resistance, and decorative appeal.

The Philippines ceramic tiles market is segmented by product, application, construction type, and end-user. By product, the market is sub-segmented into glazed, porcelain, scratch-free, and other products. By application, the market is sub-segmented into floor tiles, wall tiles, and other applications. By construction type, the market is sub-segmented into new construction, replacement, and renovation. By end-user, the market is sub-segmented into residential and commercial. The report offers market sizes and forecasts in value (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By Construction Type

| New Construction |

| Renovation and Replacement |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Luzon |

| Visayas |

| Mindanao |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Luzon | |

| Visayas | ||

| Mindanao | ||

Key Questions Answered in the Report

What CAGR is expected for the sector through 2031?

From 2026 to 2031, the market is forecast to grow at a 5.58% CAGR, driven by infrastructure spending and residential upgrades.

Which product segment leads demand in the Philippines ceramic tiles market?

Porcelain leads by share at 43.78% in 2025, supported by durability and low absorption that align with institutional specifications.

Which end-user segment is growing fastest within the Philippines ceramic tiles market?

The residential segment holds a 67.20% share of the Philippines ceramic tiles market in 2025, while the commercial sector is projected to register the fastest growth at a 6.20% CAGR through 2031, driven by ongoing construction completions and renovation activities across major urban corridors and tier-2 cities.

Which regions drive the most demand for tiles in the Philippines?

Luzon accounts for 66.08% of the Philippines ceramic tiles market in 2025, while Visayas is projected to record the fastest growth at a 7.36% CAGR through 2031, supported by accelerating tourism, hospitality, and urban infrastructure development across key regional growth centers.

How are regulations shaping supply in the Philippines ceramic tiles market?

DAO No. 20-09 enforces PS certification for domestic tiles and ICC for imports, while a 2026 customs circular requires BPS clearance prior to cargo release, which strengthens formal channels.

Page last updated on: