Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

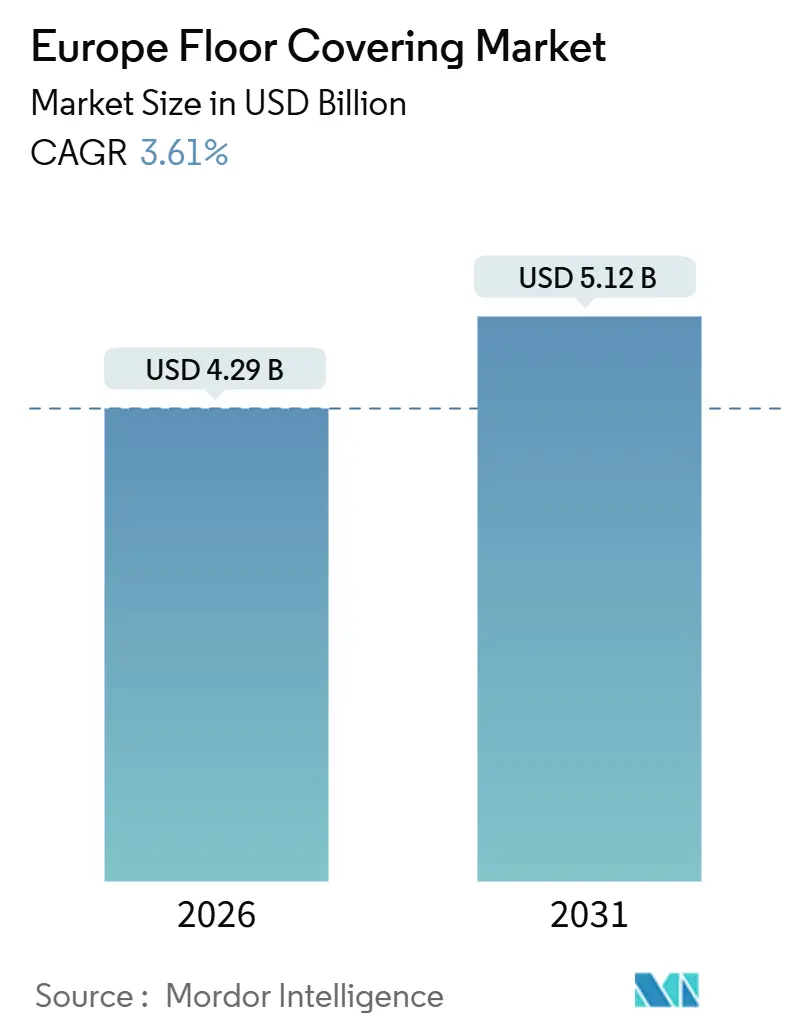

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 5.12 Billion |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Floor Covering Market Analysis by Mordor Intelligence

The Europe floor covering market size is estimated at USD 4.29 billion in 2026, and is expected to reach USD 5.12 billion by 2031, at a CAGR of 3.61% during the forecast period (2026-2031). Growth is supported by the EU Renovation Wave and the Energy Performance of Buildings Directive, which channel retrofit activity toward performance-driven materials and verified environmental data through 2030[1]Efficient Buildings Europe, “Energy Performance of Buildings Directive Implementation Guide 2024,” Efficient Buildings Europe, efficientbuildings.eu. Circular procurement in the Nordics and Benelux, including tender weighting for recycled content and documented end-of-life pathways, pushes manufacturers to scale take-back and recycled-content programs. Energy costs, though off crisis highs, continue to influence kiln-fired categories while resilient formats gain from faster installation and installer scarcity across several member states. Suppliers emphasize vertical integration, closed-loop collection, low-emission certifications, and transparent life cycle data to meet public-sector requirements and ESG-minded private demand across the European floor covering market.

Key Report Takeaways

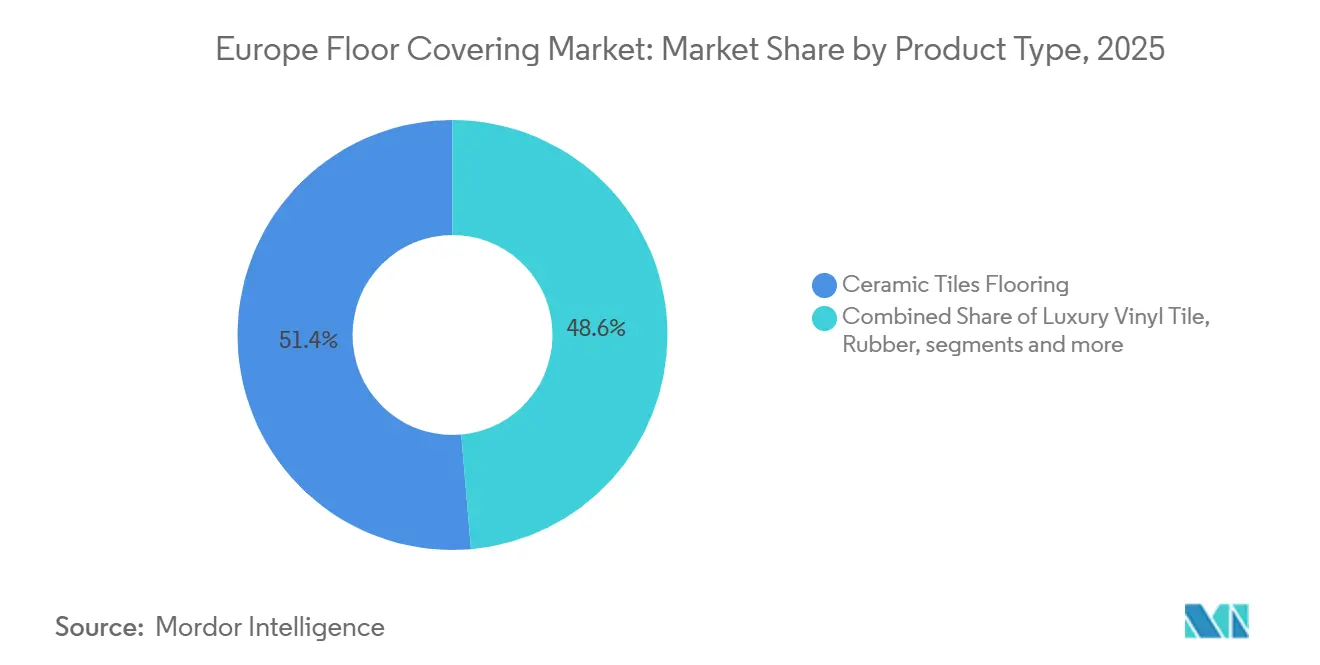

- By product type, ceramic tiles led with 51.38% of the European floor covering market size in 2025. Vinyl flooring is projected to expand at a 7.65% CAGR through 2031.

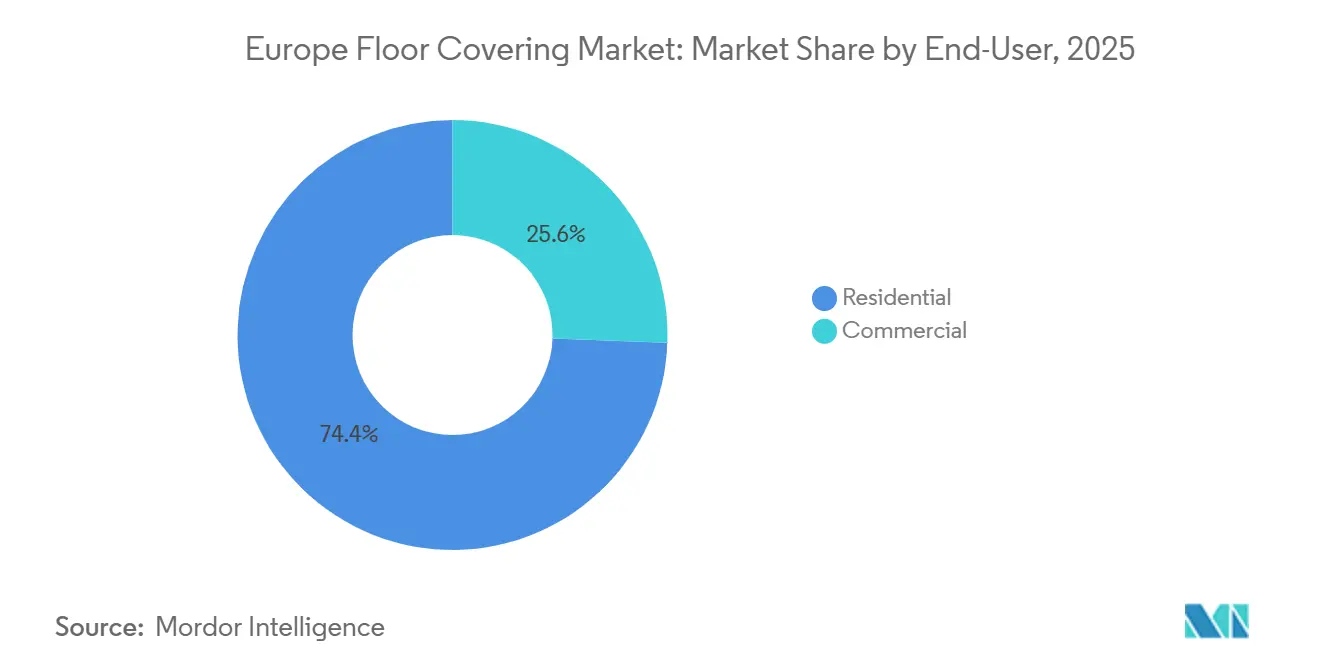

- By end-user, the residential segment held 74.43% of the European floor covering market size in 2025. The commercial segment is forecast to record the highest CAGR at 8.36% through 2031.

- By distribution channel, B2C retail accounted for 71.37% share of the European floor covering market size in 2025. B2B contractors and builders are projected to grow at a 9.65% CAGR through 2031.

- By construction type, remodelling or retrofit commanded a 64.44% market share of the European floor covering market in 2025. New construction is projected to grow at a 9.63% CAGR through 2031.

- By geography, Germany accounted for a 31.76% share of the European floor covering market size in 2025. France is projected to expand at a 9.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Renovation Wave boosting retrofit in Germany, France, Italy | +1.2% | Germany, France, Italy | Medium term (2-4 years) |

| Circular materials under the EU Green Deal favour recyclable flooring | +0.8% | Global, strongest in Nordics and Benelux | Long term (≥ 4 years) |

| DIY-led penetration of LVT and SPC in Western Europe | +1.5% | Western Europe, including the United Kingdom, Germany, France, Benelux | Short term (≤ 2 years) |

| Hybrid work model driving office redesign in Nordics and Benelux | +0.6% | Nordic countries, Benelux | Medium term (2-4 years) |

| Healthcare infrastructure expansion in CEE is lifting resilient flooring | +0.9% | Central and Eastern Europe | Medium term (2-4 years) |

| Premium upgrades in the United Kingdom homes are raising engineered wood adoption | +0.7% | United Kingdom | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU "Renovation Wave" Stimulating Retro-Fit Demand in Germany, France, and Italy

The Energy Performance of Buildings Directive aligns the region toward deep renovation outcomes and requires minimum performance standards to lift the worst energy classes, which converts flooring components into compliance-critical elements in retrofit scopes. Buildings account for a large share of energy use and emissions in the region; therefore, measures such as floor insulation and acoustic underlayment move from optional to expected where thermal gains are measured at the building level. Germany’s multi-year renovation ambition catalyzes demand for moisture-resistant subfloors and rigid, resilient products that can meet acoustic targets without complex assemblies. France’s subsidy framework that supports compliant low-emission installations redirects purchases toward engineered formats with verified emission claims. This environment shifts procurement toward multi-attribute specifications, where performance, embodied carbon, and verifiable declarations are evaluated together in public and commercial tenders.

Shift to Circular Materials under EU Green Deal Raising Demand for Recyclable Flooring

Public-sector tenders in the Nordics and Benelux incorporate recycled-content weighting and documented pathways for material recovery, which strengthens demand for flooring that can be disassembled and retrieved at the end of life. The Ecodesign for Sustainable Products Regulation and the revised Construction Products Regulation extend product-level requirements and environmental declarations, making EPDs and material passports central to market access and bid eligibility. Sector initiatives prove the viability of recycling methods for PVC and elevate post-consumer content in backings without performance loss, which supports circular procurement[2]Plastics Europe, “The Circular Economy for Plastics, A European Analysis,” Plastics Europe, plasticseurope.org. Manufacturers respond with bio-based and climate-positive ranges, including linoleum lines with agricultural byproducts and high biogenic carbon storage documented across the life cycle. These policies and practices weave circularity into product design and procurement decisions and lift the appeal of closed-loop programs in the European floor covering market.

Rapid Penetration of LVT and SPC in Western Europe Driven by DIY Retail Chains

Click-lock resilient formats reduce labour dependencies and align with DIY retail strategies in large Western European markets that face installer scarcity and schedule constraints. The category’s premium growth is supported by embossing-in-register visuals, antimicrobial wear layers, and dimensional stability that suits underfloor heating and frequent cleaning cycles. VOC restrictions on adhesives and floor coverings in Belgium, and related emission testing requirements, further advantage low-odor resilient systems in occupied renovations. These traits reinforce the shift toward resilient within the European floor covering market as renovation activity remains the primary driver of installed volumes through the forecast period.

Growth of Hybrid Work Models Triggering Office Re-Design Cycles in the Nordics and Benelux

Hybrid work strategies prompt office reconfigurations that segment collaboration and focus zones, raising demand for acoustic performance and modularity in floor systems. Modular carpet tiles and loose-lay resilient products allow reconfiguration without disruptive adhesive removal, which fits shorter leases and frequent refresh cycles in these markets[3]Interface, “2024 Interface Impact Report Highlights Continued Climate Progress,” Interface, investors.interface.com. Corporate buyers prioritize verified carbon and recycled-content attributes alongside functional performance, including slip, fire, and indoor-air criteria that align with well-being objectives. Smart readiness assessments in non-residential buildings encourage adaptable systems that integrate with sensor-ready subfloors and building automation, increasing the value of modular flooring designs. This pattern supports premium commercial specifications and influences higher-end residential preferences within the European floor covering market as people carry office design cues into the home.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated European gas and power costs are raising ceramic and kiln costs | -0.7% | EU-wide, strongest in Italy, Spain, Portugal | Short term (≤ 2 years) |

| Tight VOC norms are increasing carpet compliance costs | -0.4% | Germany, Nordics, Benelux | Medium term (2-4 years) |

| Installer shortages are delaying large fit-outs | -0.9% | EU-wide, construction-heavy economies | Long term (≥ 4 years) |

| Volatile timber supply from Russia and Belarus is disrupting wood chains | -0.5% | EU-wide, importers of birch plywood | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soaring European Gas and Electricity Prices Inflating Ceramic and Kiln-Fired Tile Costs

Industrial energy prices eased in 2025 versus crisis peaks but remain above pre-pandemic baselines, which challenges energy-intensive kiln-fired categories[4]Eurostat, “Electricity price statistics,” Eurostat, ec.europa.eu. Gas and electricity costs vary by country, with several markets facing higher-than-average rates for non-household users, which affects margins and pricing decisions. These dynamics explain why ceramic’s large installed base grows more slowly than resilient in renovation-focused geographies. Geopolitical supply rebalancing and sanction regimes add uncertainty around future contracts and risk premiums that manufacturers must manage in planning horizons. As a result, specifiers lean toward materials with lower production energy intensity in projects with tight budgets and schedules across the European floor covering market.

Skilled Installer Shortages in the EU Labor Market Delaying Large-Scale Fit-outs

Persistent labour shortages across many trades complicate scheduling and raise the appeal of flooring systems that require fewer installation steps. Upskilling initiatives progress, yet reported participation rates are not sufficient to close gaps at the scale required for renovation targets in the near term. These constraints influence specifiers to choose click-lock, loose-lay, and acclimation-light products that shorten on-site times and reduce dependencies on scarce trades. Coordinating trades for smart-ready non-residential buildings increases complexity and amplifies the need for modular flooring that can integrate with sensor-ready subfloors. These dynamics tilt decisions toward resilient and engineered options in the European floor covering market, where installer availability is uncertain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vinyl Leads Fastest Growth as Rigid-Core Technologies Displace Ceramics

Ceramic tiles held 51.38% of the European floor covering market share in 2025, leading in Southern Europe. Growth has slowed in renovation-driven markets favoring faster installation and lower embodied energy. Vinyl flooring is expected to grow at a 7.65% CAGR through 2031, supported by rigid-core formats meeting acoustic, hygiene, and underfloor heating needs without extensive subfloor work. Resilient flooring with enhanced embossing and antimicrobial layers has expanded into healthcare, education, and food service sectors, where cleaning protocols and indoor air standards are critical. Low-emission adhesives and restricted-VOC lists further drive adoption of loose-lay and click-fit systems in residential remodels, addressing installer shortages and project delays. These trends position resilient flooring as a key growth segment, aligning with renovation budgets and compliance requirements.

Waterproof laminate and engineered wood remain competitive for residential upgrades, valued for acoustic underlayment and indoor air quality claims. Innovations in recycled content, take-back programs, and verified EPDs enhance public-sector eligibility. Rubber and linoleum flooring, backed by life cycle data, attract education and healthcare buyers seeking durable, low-maintenance, and environmentally friendly options. Investments in European resilient flooring capacity and digital printing technology improve availability, lead times, and regional aesthetic alignment, supporting compliance with emission and circularity standards.

By Construction Type: Remodelling Surges Ahead of New Construction Amid Regulatory Push

Remodeling and retrofit held a 64.44% market share in 2025, driven by policies and financing frameworks targeting upgrades to existing buildings. These efforts emphasize minimum performance standards and energy labeling. New construction is expected to grow at a 9.63% CAGR through 2031, addressing housing shortages in urban areas. Retrofits focus on flooring products with low emissions, acoustic performance, and underfloor heating compatibility to enhance comfort and energy efficiency. Low-profile resilient options are ideal for heritage buildings, minimizing floor elevation changes and avoiding door or threshold modifications. These preferences support faster installation and compliance with European floor covering market requirements.

Underfloor heating and efficient building services in new housing influence demand for dimensionally stable surfaces and thermally rated adhesives. Rigid-core resilient flooring and engineered wood with verified emission performance are preferred for balancing comfort and maintenance. Expanding environmental reporting obligations, such as life cycle declarations, affects product selection to ensure market access and faster permitting. Procurement teams prioritize recovery options to improve circularity ratios, aligning with updated construction product guidelines. These factors shape finishing choices and direct supply toward compliant systems in the European floor covering market.

By End-User: Commercial Segment Outpaces Residential Growth on Office Redesigns and Healthcare Mandates

Residential applications dominated 74.43% of the European floor covering market size in 2025, driven by large housing stocks and retrofit programs integrating flooring into thermal and acoustic upgrades. The commercial segment is expected to grow at a CAGR of 8.36% through 2031, with offices, healthcare, and education projects adopting modular and resilient systems for reconfiguration and maintenance efficiency. Corporate interiors focus on acoustic comfort, underfoot resilience, and low-emission credentials supporting well-being and ESG targets. Healthcare procurement prioritizes seamless, antimicrobial surfaces resistant to frequent disinfection, increasing demand for homogeneous sheet products and advanced rubber. Verified low-emission and circular-ready products meet these needs, with public tenders enforcing strict documentation standards.

Hospitality, retail, and education sectors balance durability and design, favoring long-format visuals with reduced pattern repetition and resilient performance under heavy traffic. Loose-lay systems and high-recycled-content carpet tiles enable quick installations with low-odor materials. Universities and schools prioritize acoustic performance and low fire and slip classifications, often specifying linoleum and rubber for corridors and classrooms to optimize lifecycle costs. Commercial buyers also consider material passports and take-back programs to meet circularity goals and regulatory standards. These functional, regulatory, and sustainability priorities shape adoption trends in the European floor covering industry during commercial remodeling cycles.

By Distribution Channel: B2B Contractors Surge as Renovation Wave Fuels Project-Based Sales

The B2C retail segment held a 71.37% share of the European floor covering market in 2025, supported by home centers, specialty stores, and online platforms offering DIY-friendly inventory and quick purchasing. The B2B segment, growing at a 9.65% CAGR through 2031, benefits from renovation aggregators and accredited installers managing subsidy-linked retrofits requiring documentation and multi-trade coordination. Bundling projects like HVAC, insulation, fenestration, and flooring enables scale pricing and streamlined procurement under qualified contractors. Online tools for visualization and sample logistics enhance omnichannel retail, while physical samples remain preferred for high-value purchases. Channels combining technical guidance, compliance support, and product availability drive market growth.

Specialty dealers excel in advisory services and regulatory compliance, addressing EPD registration, VOC testing, and chain-of-custody requirements. Manufacturer-builder partnerships integrate flooring into standard packages for new housing and multifamily retrofits, ensuring schedule adherence. Industry associations train installers on adhesives, substrates, and sensor-ready assemblies to meet automation and smart-readiness demands. Digital displays and curated showroom assortments help consumers balance performance and sustainability considerations without delays. These practices boost confidence and efficiency, supporting the European floor covering market amid strong renovation activity.

Geography Analysis

Germany held 31.76% of the European floor covering market size in 2025, supported by renovation goals and financing that stabilized retrofit volumes in housing and public buildings. France is expected to grow at a 9.37% CAGR through 2031, driven by incentives for low-emission installations and embodied-carbon thresholds guiding material choices. Southern European producers face elevated energy costs, influencing ceramic tile pricing and production capacity. Renovation regulations and public procurement criteria, emphasizing environmental declarations and circularity, shape bidding processes and product strategies across the market.

The United Kingdom focuses on premium renovations, favoring engineered wood and resilient flooring compatible with underfloor heating and low-emission standards. Benelux markets prioritize circular procurement, using material passports and recycled-content weighting to favor suppliers with take-back programs. The Nordics emphasize heating-compatible, resilient, and engineered wood flooring that withstands temperature fluctuations. Central and Eastern Europe allocate funds to healthcare and institutional projects requiring antimicrobial and washable surfaces under strict procurement standards. These trends drive diverse product mixes and compliance expectations across the market.

Steady growth continues in accession-related markets and regions with expanding housing supply, where residential space per capita lags Western norms. Value-oriented ceramic and laminate materials remain popular in budget-constrained areas, while public frameworks focus on recovery and recycling targets. Variations in VOC enforcement and emissions documentation require localized formulations and labeling to meet national regulations. Suppliers adjust operations and distribution to serve tender-heavy segments and address reporting needs, shaping go-to-market strategies across Europe’s diverse regulatory landscapes.

Competitive Landscape

Supply in the European floor covering market remains fragmented, with national and global players competing in procurement, R&D, and compliance to meet rising standards in tenders. Companies focus on low-emission adhesives, bio-based backings, and PVC-free alternatives to comply with indoor air quality requirements. Circular collection and recycling programs are increasingly prioritized, driving investments in logistics and processing to recover post-installation and post-use materials. Investor communications emphasize energy management, emissions reduction, and recycled content, influencing capital access and corporate positioning. These strategies are essential for competitive differentiation where performance and compliance intersect.

Manufacturers are enhancing European resilient capacity and high-definition printing to localize aesthetics and reduce design cycle times. Product launches target lower cradle-to-gate carbon footprints and antimicrobial properties, addressing hygiene and sustainability goals in education and healthcare projects. Verified carpet tiles, rubber solutions, and modular vinyl products are positioned for reconfigurable commercial spaces and premium residential markets. Partnerships with builders integrate flooring specifications into housing packages, simplifying choices for buyers and developers. These efforts align production and market strategies with evolving demand and regulatory requirements, strengthening the market.

Corporate disclosures show progress in renewable energy use, carbon reduction, and recycled-content adoption, helping suppliers meet qualification criteria and improve procurement scores. Companies with take-back programs and Environmental Product Declarations (EPDs) are prepared for stricter regulations and circularity goals. Capital allocation and restructuring focus on cost reduction and asset efficiency while maintaining European production footprints for resilient categories. This positions market leaders to serve public and private projects as the market evolves under stricter specification and reporting standards.

Europe Floor Covering Industry Leaders

Mohawk Industries

Tarkett Group

Forbo Holding AG

Gerflor Group

Interface Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Karndean has launched Karndean Design Aesthetics, a tool designed to enhance personalized, boutique-style retail experiences. The company has also expanded its Knight Tile range by introducing new wood and stone designs. Additionally, it showcased its latest products at The Flooring Show, highlighting its commitment to innovation and design.

- March 2025: Unilin, part of Mohawk Industries, plans to invest EUR 40 million in a PIR insulation panel factory in Leśnica, Poland. The construction is set to begin in 2025, with operations anticipated by late 2026. This investment aims to enhance production capabilities and meet growing market demand for insulation solutions in the region.

- January 2025: Interface has introduced a carbon-negative rubber flooring prototype under its nora by Interface brand. Designed for healthcare and other performance-critical environments, the product is expected to be commercially available by late 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe floor covering market as the sales value of finished surface materials, carpet and rugs, resilient formats such as LVT and linoleum, and non-resilient options including ceramic/porcelain tile, laminate, stone, and wood that are permanently installed over structural sub-floors in residential and commercial buildings. According to Mordor Intelligence, the market reached USD 4.12 billion in 2025 and is forecast to touch USD 4.78 billion by 2030.

Scope exclusion: We exclude loose mats, area rugs below 1 m², unfinished lumber, sub-floor panels, adhesives, and installation labor.

Segmentation Overview

- By Product Type

- Carpet and Area Rugs

- Wood Flooring

- Ceramic Tiles Flooring

- Laminate Flooring

- Vinyl Flooring

- Stone Flooring

- Other Products

- By Construction Type

- New Construction

- Remodelling/Retrofit

- By End-User

- Residential

- Commercial

- Hospitality & Leisure

- Retail & Shopping Centers

- Healthcare Facilities

- Education

- Corporate Offices

- Public & Government Buildings

- Other Commercial Users

- By Distribution Channel

- B2C Retail

- Home Centres

- Specialty Flooring Stores

- Online

- Other Distribution Channels

- B2B / Contractors / Builders

- B2C Retail

- By Geography (Europe)

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed distributors, DIY chains, installers, and procurement leads across Germany, Italy, Poland, and the Nordics, followed by surveys of residential remodelers. These conversations validated unit penetration, click-lock adoption rates, and pricing spreads that secondary data alone could not capture.

Desk Research

We began with Eurostat building permit series, EU Construction Observatory briefs, and trade association portals such as the European Resilient Flooring Manufacturers' Institute, Fédération Européenne des Fabricants de Parquets, and Cerame-Unie, which provide shipment and price indices. Country customs records, patent filings via Questel, and listed company 10-Ks further clarified brand mix and channel shifts.

Supplementary insight came from D&B Hoovers company financials, Dow Jones Factiva news flows, and national renovation grant databases. These sources guided base-year splits and verified product average selling prices. The desk sources named here are illustrative, and many additional open and paid datasets were reviewed to cross-check figures.

Market-Sizing & Forecasting

We apply a top-down build using Eurostat floor-area completions and Renovation Wave retrofitting targets, which are then multiplied by material penetration ratios and ASPs gathered from interviews. Supplier roll-ups and sampled project invoices act as bottom-up sense checks. Key variables include ceramic kiln gas price trends, LVT import volumes, housing completion starts, installer wage inflation, and e-commerce share of flooring spend. A multivariate regression with ARIMA overlays projects each driver to 2030, and gaps arising from limited distributor disclosures are bridged with scenario bands approved by interviewees.

Data Validation & Update Cycle

Our team triangulates outputs against independent tile production statistics and vinyl import values, flags anomalies for senior review, and revisits respondents when variances exceed five percent. Reports refresh yearly, with mid-cycle revisions triggered by material regulatory or pricing shocks.

Why Mordor's Europe Floor Covering Baseline Commands Reliability

We observe that published market values often diverge because firms choose wider material baskets, mix labor revenues, or freeze exchange rates differently.

Key gap drivers include the inclusion of adhesives and underlayment, aggregation of EMEA instead of pure Europe, and use of construction spend proxies without on-ground interviews.

Our disciplined scope, annual refresh, and dual-track validation make Mordor's estimate the dependable midpoint for strategic planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.12 billion (2025) | Mordor Intelligence | |

| USD 60.15 billion (2023) | Global Consultancy A | Combines flooring materials, accessories, and Middle East data with Europe figures |

| USD 42 billion (2024) | Industry Database B | Uses producer shipment value plus installation income and lacks ASP verification interviews |

| USD 27.49 billion (2024) | Regional Consultancy C | Relies on construction spending indices and omits resale renovation volumes |

In sum, Mordor's model ties every euro to transparent floor-area metrics, validated prices, and a repeatable update loop, giving decision-makers a balanced baseline they can audit and trust.

Key Questions Answered in the Report

What is the current size and expected growth of the European floor covering market?

The European floor covering market size reached USD 4.29 billion in 2026 and is projected to reach USD 5.12 billion by 2031 at a 3.61% CAGR.

Which product category is growing fastest in the European floor covering market?

Vinyl is the fastest-growing category, projected at a 7.65% CAGR through 2031, supported by rigid-core formats and antimicrobial finishes.

Which end-user segment leads demand within the European floor covering market?

Residential led with 74.43% of value in 2025, while commercial is set to grow fastest at 8.36% CAGR through 2031 due to office redesigns and healthcare projects.

How do regulations influence the European floor covering market today?

Energy performance rules, VOC restrictions, EPD mandates, and circular-procurement criteria drive demand for low-emission, recyclable, and take-back-enabled flooring systems across public and private projects.

Which country holds the largest share of the European floor covering market?

Germany led with 31.76% in 2025 due to renovation programs and financing that sustain high retrofit volumes.

Which sales channel is expected to grow fastest for floor coverings in Europe?

B2B or contractor channels are projected to grow at a 9.65% CAGR through 2031 as subsidy-tied retrofits and project bundling favour accredited installers and project-based procurement.

Page last updated on: