Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

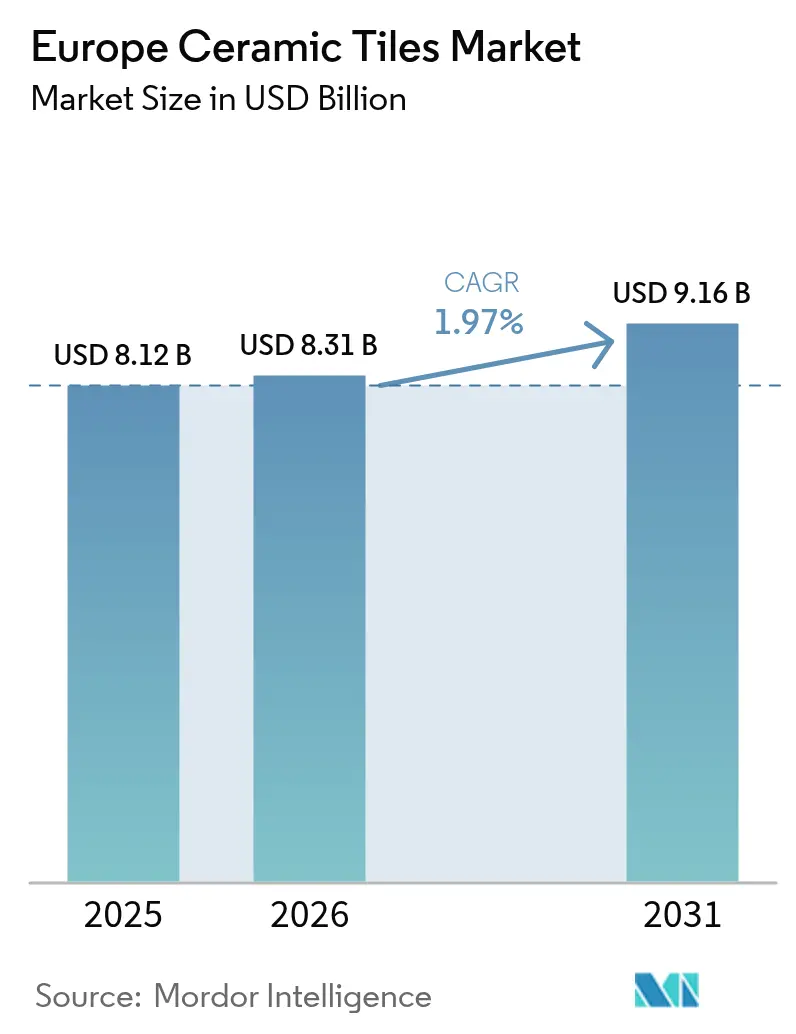

| Base Year Market Size (2025) | USD 8.12 Billion |

| Market Size (2026) | USD 8.31 Billion |

| Market Size (2031) | USD 9.16 Billion |

| Growth Rate (2026 - 2031) | 1.97% CAGR |

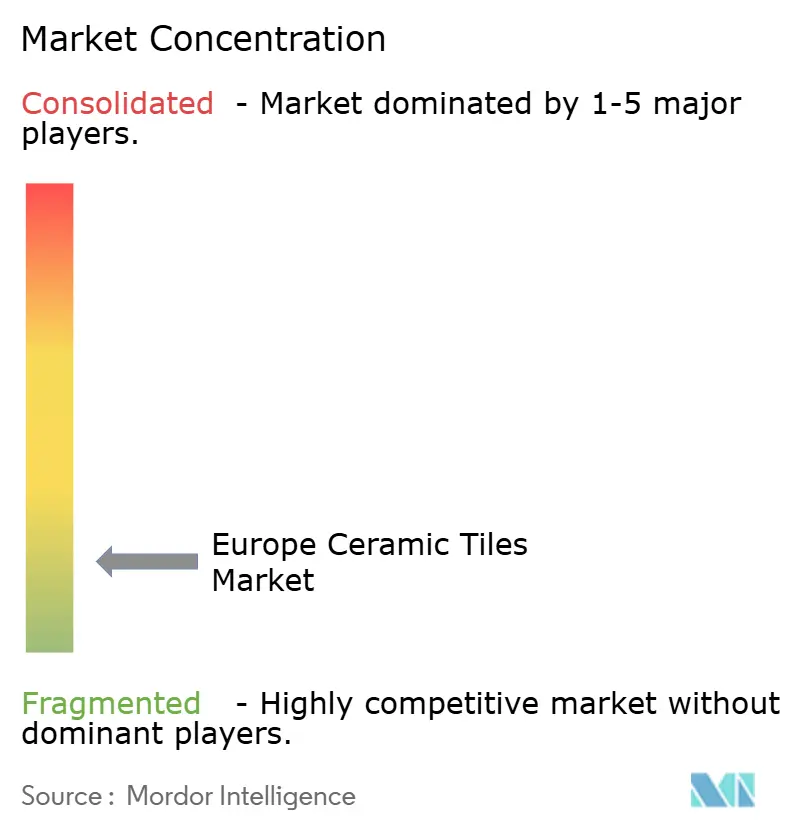

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ceramic Tiles Market Analysis by Mordor Intelligence

The Europe ceramic tiles market size is projected to be USD 8.12 billion in 2025, USD 8.31 billion in 2026, and reach USD 9.16 billion by 2031, growing at a CAGR of 1.97% from 2026 to 2031. Retrofit activity tied to the Energy Performance of Buildings Directive is the primary growth engine as member states finalize national codes and funding frameworks that bring wet-room and high-traffic surface upgrades forward in project timelines. Renovation and replacement work accounts for most installations, and spending priorities favor durable, low-maintenance finishes in public buildings and co-financed housing. Germany leads demand by value, while the fastest growth is unfolding in BENELUX on the back of strict procurement standards and investments in transport and social infrastructure. Product mix tilts toward porcelain for premium and high-traffic spaces, with mosaic gaining momentum as hospitality refurbishments return.

Key Report Takeaways

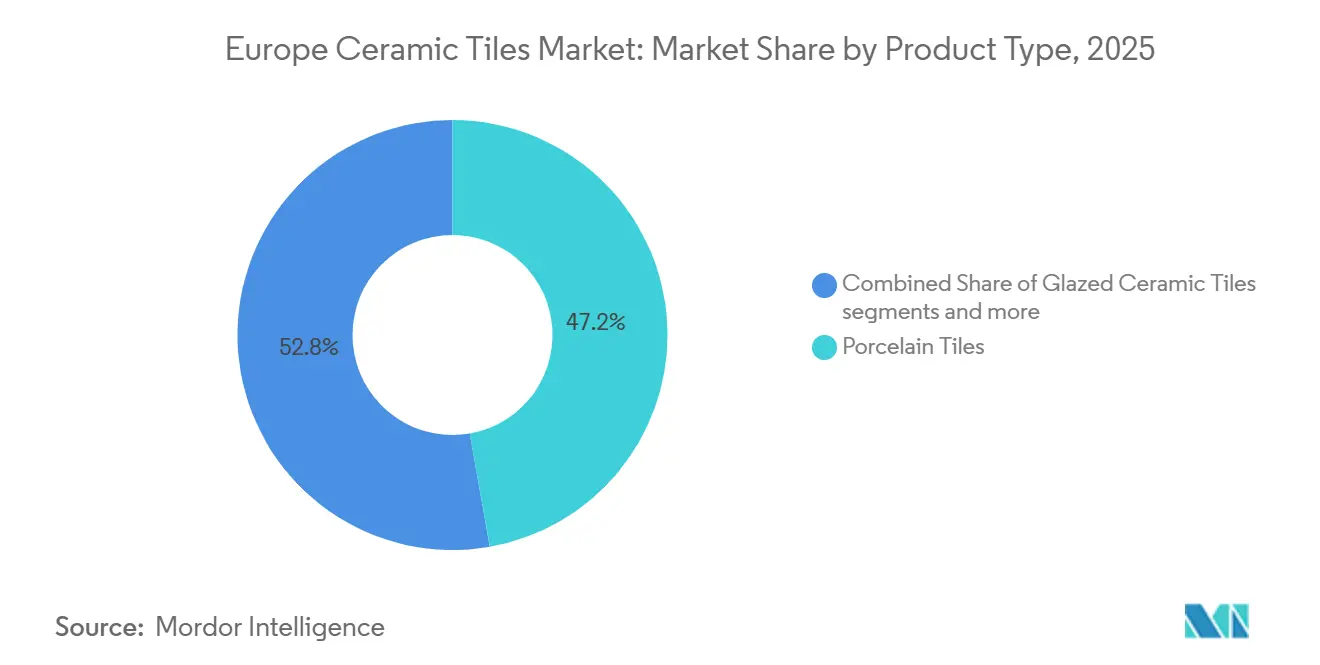

- By product type, porcelain led with 47.23% revenue share in 2025, while mosaic is forecast to expand at a 2.02% CAGR through 2031.

- By application, floor installations accounted for a 60.12% share of the Europe ceramic tiles market size in 2025, while wall applications are advancing at a 2.04% CAGR through 2031.

- By end-user, the residential segment held 43.45% of the Europe ceramic tiles market share in 2025, while the commercial segment recorded the highest projected CAGR at 2.31% through 2031.

- By construction type, renovation and replacement led with 64.12% share in 2025, while new-build is projected at a 2.53% CAGR through 2031.

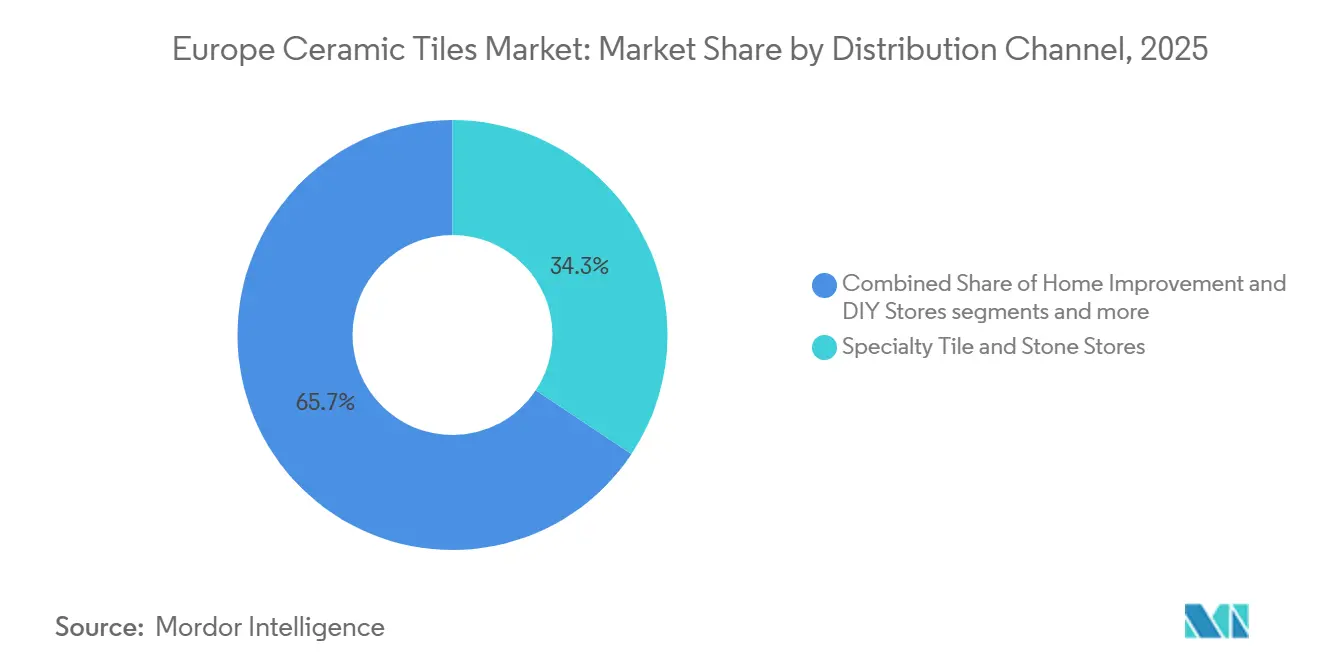

- By distribution channel, specialty tile and stone stores held 34.34% share in 2025, while online retail is forecast to expand at a 4.32% CAGR through 2031.

- By geography, Germany led with 21.34% revenue share in 2025, while BENELUX is projected to post the fastest 4.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Renovation Wave and Codes Accelerating Retrofits | +0.6% | EU-wide, concentrated in Germany, France, the Netherlands, Belgium | Medium term (2-4 years) |

| Porcelain And Large-Format Adoption in Premium Interiors | +0.4% | Germany, Italy, the United Kingdom, Spain, and France | Medium term (2-4 years) |

| Hospitality And Travel Rebound Driving Refurbishments | +0.3% | Spain, Greece, Italy, France, BENELUX | Short term (≤ 2 years) |

| Specialty Retail and Omnichannel Improving Access | +0.2% | Western Europe's core, emerging in Poland and the Czech Republic | Medium term (2-4 years) |

| Antimicrobial, EPD, ISO 17889-1 Tiles Gaining Share | +0.2% | Nordics, BENELUX, Germany, with spill-over to France and Italy | Medium term (2-4 years) |

| Kiln Electrification, Hydrogen Pilots, Waste-Heat Recovery | +0.1% | Spain, Italy, pilots in Germany and Austria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Renovation Wave & EPBD Mandates: Retrofit Surge Lifts Tile Demand

Member states are transposing the revised Energy Performance of Buildings Directive by May 29, 2026, which mandates renovation of the 16% worst-performing non-residential buildings by 2030 and a 16% reduction in average residential primary-energy use, shifting procurement toward durable, easy-to-maintain surfaces in wet rooms and high-traffic corridors[1]European Commission, “Energy Performance of Buildings Directive (EU/2024/1275),” EUR-Lex, eur-lex.europa.eu. Buildings represent a large share of energy consumption in the European Union, and the building stock remains old, which amplifies the scope for bathroom and kitchen upgrades that specify ceramic tiles for hygiene and durability. National renovation plans that slipped from late 2025 into early 2026 will unlock grants and co-financing, creating a concentrated order window in 2027 and 2028 for tile packages linked to insulation, heating, and code compliance. Procurement bodies increasingly require Environmental Product Declarations and ISO 17889-1 documentation, and Italian manufacturers score high on that framework, which tightens access to public-sector tenders across Nordic and BENELUX markets. As these rules scale, the Europe ceramic tiles market benefits from a clear retrofit pipeline and specification standards that reward documented products over undifferentiated imports.

Large-Format Porcelain & Digital Aesthetics: Premium Migration

The ANSI definition updated in 2024 recognizes large-format tiles where at least one side exceeds 23 inches, expanding eligibility to popular 24-by-48-inch formats that reduce grout lines and accelerate installation in busy retrofit schedules [2]Crossville Studios, “Large-Format Tile: What It Is and How To Specify,” Crossville, crossvilleinc.com. Porcelain’s low water absorption below 0.5% supports high-traffic applications in hotels, transport hubs, and offices while retaining visual consistency across large surfaces. Architects specify these panels for minimalist interiors and monolithic wall cladding that align with durability and cleaning standards in commercial and institutional spaces. Digital inkjet printing advances have enabled hyper-realistic stone and wood aesthetics with kiln-fired performance, keeping porcelain competitive against resilient alternatives that fall short on abrasion and fire safety in heavy-use spaces. As capital projects return, premium finishes migrate toward large-format porcelain and design-led mosaics, reinforcing value mix within the Europe ceramic tiles market.

Hospitality Rebound & Transport-Hub Modernization: Commercial Cycle Returns

Europe hotel revenue per available room rose 2.8% year to date in 2025, and hotel property transactions reached EUR 21 billion in 2024, equal to USD 22.7 billion, which revived refurbishment pipelines for lobbies, guest bathrooms, and restaurant spaces[3]CBRE Research, “European Hotels 2025 Midyear View,” CBRE, cbre.com. Spain recorded mid-year RevPAR gains in 2025, and Greece posted double-digit increases, which steered capex toward aesthetic and hygiene upgrades suited to ceramic finishes. Terminal expansions and rail-station modernizations are rising as international air passenger volumes increase, pushing demand for slip-resistant floor systems and non-combustible wall coverings that withstand wheeled traffic and frequent cleaning. Convention and business travel is also normalizing, which encourages hotels and venues to invest in high-durability floor and wall packages. These dynamics favor porcelain slabs and antimicrobial wall solutions, helping the Europe ceramic tiles market tap into the returning commercial cycle.

Omnichannel Distribution & AR Visualization: Democratizing Specification

Online channels post the fastest growth rate among distribution pathways through 2031 as augmented reality tools close design-confidence gaps that once required showroom visits. Specialty showrooms still serve as technical hubs for large-format and custom mosaics, yet contractors now source more directly through digital portals that integrate project pricing and logistics. Western European platforms offer faster delivery and tighter inventory integration, which improves lead times for retrofit programs with compressed schedules. DIY chains continue to broaden assortments, but professional installers in retrofit-heavy markets, including Germany and France, increasingly leverage direct-to-installer online options to meet EPBD-driven timelines. As visualization improves and shipping-friendly thin panels expand availability, omnichannel models extend reach and specification support across the Europe ceramic tiles market.

Restraints Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy And Carbon Cost Inflation Pressuring Kiln Costs | -0.5% | Italy, Spain, and Germany are production hubs | Medium term (2-4 years) |

| Substitution From LVT/SPC And Fast-Install Resilients | -0.4% | Residential segments, Germany, France, United Kingdom | Long term (≥ 4 years) |

| Tightening Crystalline Silica OELs And Dust-Control Costs | -0.1% | EU-wide, focus on the UK, Germany, Netherlands | Medium term (2-4 years) |

| CBAM, Anti-Dumping Shifts, And Low-Cost Import Surges | -0.05% | Import-competing segments, Southern Europe exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Natural Gas Volatility & EU ETS Phase IV: Kiln Economics Under Siege

Natural gas remains a large share of production costs, and ETS allowances averaged EUR 64.74 per tonne in 2024, equal to USD 69.9 per tonne, with the linear reduction factor accelerating to lift the overall emissions cut targeted by the end of the decade[4]International Carbon Action Partnership, “EU ETS Factsheet 2026,” ICAP, icapcarbonaction.com. Ceramic-sector compliance costs are projected to total EUR 8.5 billion by 2030, equal to USD 9.2 billion, while ETS 2 expansion in 2027 brings more small plants into scope with incremental burdens that could reach EUR 148 million per year by 2030, equal to USD 159.8 million. Larger European producers have invested in cogeneration and on-site renewables to defray grid energy, and Spain operates dozens of cogeneration plants at high electrical efficiency. Waste-heat recovery and photovoltaic arrays further reduce exposure to allowance volatility, and projects demonstrate material emissions avoidance across ceramic clusters. Hydrogen kiln pilots by leading equipment suppliers complement electrification, setting a path for low-carbon tile production as incentives and procurement standards gain traction.

LVT/SPC Substitution & Fast-Install Preference: Residential Share Erosion

Stone-polymer composite surged to 75% of European modular flooring in 2024 with shipments up 26.1% to 67.7 million square meters, which diverted share from ceramics in non-wet residential rooms where ease of installation is valued. Traditional LVT click variants declined 35.6% to 9.1 million square meters, but the broader resilient category maintained momentum in living areas and bedrooms. Ceramic producers are responding with thin, six-millimeter panels for direct-over-tile upgrades that limit demolition and speed project completion. Click-enabled tile systems are emerging as pilots to narrow the installation gap relative to resilient flooring. Ceramic continues to defend and expand in high-traffic commercial settings that require superior abrasion resistance and fire performance, which aligns with the growth profile of the commercial end-user segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Commands Scale, Mosaic Artisanship Gains Premium Traction

Porcelain tiles captured a 47.23% share of product-type revenue in 2025, reinforcing their role in premium interiors and heavy-use commercial areas where performance, low porosity, and lifecycle durability are essential. Low water absorption under ISO classifications, combined with digital printing that replicates natural materials, positions porcelain as the first choice for airports, hotel lobbies, and upscale residential kitchens. Large-format slabs reduce grout lines and accelerate installation, which matters in EPBD-driven timelines where building closures are tightly scheduled. Glazed ceramic remains relevant for value-focused residential and light commercial jobs, while unglazed formats hold steady in outdoor and industrial uses. Mosaic tiles, though smaller by volume, show the quickest growth rate due to hospitality and high-end residential designs that favor accent walls and spa aesthetics as tourism and property transactions return across key destinations. These factors keep porcelain at the center of the Europe ceramic tiles market while mosaics deliver incremental premium mix as projects resume.

Comparing recent patterns, porcelain-maintained share stability through disruptions in starts, while mosaic demand moved with discretionary hospitality budgets that were released from 2024 onward. As refurbishments scale, decorative and handmade mosaics benefit from the desire to differentiate guest-facing spaces, and the pipeline of hotel and resort projects supports steady ordering of feature walls and backsplashes. Investment in advanced presses and continuous lines signals confidence in large-format porcelain’s trajectory, and sustained capital flows aim to improve energy efficiency as well. Sector-level Environmental Product Declarations published by leading groups and high ISO 17889-1 scores by Italian producers strengthen qualification in public tenders where documentation is non-negotiable. These documentation advantages favor suppliers ready with product-level and plant-level data packages, especially in the Nordics and BENELUX.

By Application: Floor Dominance Persists, Wall Segment Accelerates on Hygiene Mandates

Floor installations absorbed 60.12% of volume in 2025, yet wall applications are advancing at a 2.04% CAGR through 2031 as public facilities and hospitality assets upgrade vertical surfaces for hygiene, cleaning efficiency, and documentation requirements. Floor demand remains anchored in high-traffic commercial settings and transport hubs where abrasion resistance and non-combustibility drive lifecycle economics. Adoption of large-format panels in busy corridors and concourses streamlines cleaning and reduces visible wear, which aligns with refurbishment timelines in airports and rail networks. Roofing remains a niche for ceramic within broader clay categories, and specification hinges on climate-related standards in colder geographies. As energy retrofits scale, wall lining upgrades are surfacing in plans for hospitals, schools, and eldercare facilities where antimicrobial finishes and environmental declarations are preferred.

Wall systems gain specification from post-pandemic hygiene priorities and green-building frameworks that emphasize verifiable materials data. High ISO 17889-1 scores by Italian producers and sector-level EPDs support procurement in strict jurisdictions, and documented wall slabs secure positions in co-financed public work. Hospitality refurbishments add momentum for decorative walls and shower surrounds, and project schedules are aligning with the 2027 to 2028 wave of EPBD-funded programs. Floor demand should remain stable in commercial hubs due to traffic intensity and fire-safety standards, while wall demand has growing tailwinds from institutional retrofits. This shift supports a broader mix of SKUs and favors suppliers prepared with antimicrobial claims and environmental documentation across both wall and floor lines.

By End-User: Residential Holds Share, Commercial Surges on Delayed Cap-Ex Release

Residential applications held a 43.45% share in 2025, while the commercial segment shows the steepest growth at a 2.31% CAGR through 2031 as hotels, offices, and public buildings renew deferred projects. Hotels are reactivating lobby and guest-room upgrades with porcelain slabs and antimicrobial walls, and investor activity supports renovations in major city hubs. Transport-hub programs are expanding to manage higher passenger traffic, which specifies slip-resistant flooring and robust wall finishes that withstand frequent cleaning. Institutional buildings benefit from EPBD funds that prioritize durable, low-VOC materials backed by environmental declarations and ISO evidence. These trends push the Europe ceramic tiles market toward a larger contribution from commercial projects over the forecast window.

Retail and office footprints are stabilizing under omnichannel and hybrid work patterns, and refresh cycles emphasize ease of maintenance and compliance with indoor air-quality frameworks. Public tenders continue to ask for ISO 17889-1 and EPD documentation as base criteria, awarding an advantage to prepared manufacturers. On the residential side, resilient modular options capture some living-space volume, while ceramic sustains strength in bathrooms, kitchens, and entryways. Thinner panels that permit direct-over-tile application help offset homeowner hesitancy on demolition and labor availability. With discretionary budgets normalizing and funding flows secured for institutional projects, commercial outpaces residential through 2031 within the Europe ceramic tiles market.

By Construction Type: Renovation Dominates, New-Build Recovers on Infrastructure Push

Renovation and replacement projects claimed a 64.12% share in 2025, which reflects the shift from speculative starts to code-driven upgrades funded under the EPBD and national programs. Member states must renovate the worst-performing non-residential cohort by 2030 and cut average primary-energy use across homes, which triggers bathroom, kitchen, and corridor packages where ceramic surfaces meet hygiene and durability needs. Grants and co-financing will concentrate awarding activity in 2027 and 2028, and procurement templates in Northern and Western Europe require ISO 17889-1 and EPD documentation at submission. Germany’s sizable public and institutional stock, along with strict documentation rules, illustrates how retrofit activity sustains steady tile demand across multi-year budgets. This retrofit pipeline anchors volume in the Europe ceramic tiles market across the second half of the decade.

New-built activity is poised to recover from the recent low base as governments address housing shortages and fund transport, education, and health infrastructure. Metro extensions, airport terminal work, and campus upgrades in Central and Western Europe support specifications for ceramic finishes that deliver fire safety, skid resistance, and ease of maintenance. Zero-emission standards coming into force later in the decade will elevate material choices that reduce operating and cleaning burdens, and porcelain fits that profile. Within new residential blocks, durable floor and wall packages are increasingly favored in shared spaces where wear is high. The Europe ceramic tiles market size linked to renovation should remain the largest share by 2031, while new-build grows faster as rates stabilize and procurement budgets turn to delivery.

By Distribution Channel: Specialty Showrooms Retain Edge, Online Surges with AR Tools

Specialty tile and stone stores accounted for 34.34% of revenue in 2025, reflecting the importance of in-person technical advice for large-format and custom designs. Online channels, however, expand at a 4.32% CAGR to 2031 as visualization improves and delivery times compress, enabling contractors to source quickly for tight retrofit schedules. DIY chains maintain sizable assortments for homeowners, yet a growing share of professional orders moves through direct-to-installer platforms in Western Europe. Digital kiosks in showrooms help bridge design exploration with centralized inventory, adding flexibility to procurement paths. Public procurement portals function as quasi-digital channels by prequalifying documentation before quotes, which supports compliant suppliers across multiple routes to market in the Europe ceramic tiles market.

E-commerce penetration for ceramics remains lower than in other building categories because color matching and handling are sensitive issues. Thinner panels reduce shipping constraints, which supports further adoption of online ordering by smaller contractors. Specialty showrooms counter with sample programs, on-site training, and jobsite support that pure-play digital channels find hard to replicate. Direct sales to contractors remain vital in large commercial and institutional jobs where pricing, scheduling, and technical coordination are complex. The Europe ceramic tiles industry therefore operates with a blended distribution model that matches project type and buyer preference across regions.

Geography Analysis

Germany commanded a 21.34% revenue share in 2025, supported by public-sector building stock and commercial hubs that align with EPBD timelines and strict procurement documentation. German buyers often require ISO 17889-1, Environmental Product Declarations, and low-VOC evidence, which favors Italian and Spanish manufacturers with strong sustainability credentials. Italy remains the production and export nucleus, with the sector navigating energy and allowance costs while investing in efficiency and product innovation. Spain’s output expanded in 2024, and the cluster employs extensive cogeneration and growing photovoltaic capacity that reduces electricity from the grid and supports decarbonization targets. France blends premium residential aesthetics with institutional hygiene priorities, which support antimicrobial wall tiles and durable floor packages in co-financed retrofits.

The United Kingdom continues to adjust its trade and standards framework post-Brexit, yet tile demand in London and key regional centers remains anchored by commercial refurbishment cycles. Poland posts healthy momentum on the back of EU-funded transportation and education projects that favor robust ceramic finishes. BENELUX leads the region in growth rate, underpinned by strict public procurement rules that emphasize EPDs and strong sustainability claims. Nordic countries maintain the highest documentation thresholds, which filter suppliers to those with qualified declarations and ISO-backed evidence. Intra-regional flows see Italian and Spanish tiles shipped to Northern European buyers, where compliance and design breadth are decisive.

Comparing recent performance, Germany held steady through market swings because retrofit funding supported baseline volumes in institutions. Italy and Spain adapted to energy-cost cycles by expanding cogeneration and renewables to stabilize production economics. Hospitality recovery in Southern Europe supported design-intensive renovations, while Central Europe gained from infrastructure outlays. Looking ahead, Germany should maintain leadership by value but may grow slightly below the regional average as resilient flooring competes in some residential applications. BENELUX and Poland are likely to outperform through 2031 as infrastructure and documentation-led procurement catalyze projects aligned with EPBD milestones.

Competitive Landscape

The Europe ceramic tiles market remains highly fragmented, with hundreds of mid-sized manufacturers and active import competition across value tiers, especially in price-sensitive segments. Fragmentation persists despite notable production scale in Southern Europe because of aesthetic preferences, export orientation, and differentiated ranges that limit consolidation. Producers focus on energy efficiency and decarbonization to manage ETS-related costs, including cogeneration, photovoltaic installations, and waste-heat recovery, which lower net allowance exposure. Select firms are piloting hydrogen or electrified kilns to further reduce operational emissions and meet emerging low-carbon procurement criteria. Documented sustainability performance under ISO 17889-1 and robust EPD coverage have moved from an advantage to a baseline requirement in public tenders across Northern Europe.

Investment continued in large-format capacity and advanced printing to support premium projects, and targeted acquisitions consolidated capabilities where producers sought resilience against energy volatility and allowance costs. Capital programs in Spain expanded slab production and improved productivity at key plants, directing output to commercial-grade porcelain and specialty formats. Companies that combine energy efficiency with documentation strength are positioned to win tenders in healthcare, education, and transport upgrades tied to EPBD funding windows. Digital sales integration with regional logistics supports faster project delivery, and value-added showroom services such as training and technical support help premium distributors defend their roles in the channel mix.

M&A examples include portfolio expansions in Spain that integrate specialty-tile capabilities, while broader restructuring actions at multinational flooring groups improved operating leverage and freed funds for product and process upgrades. Public disclosures highlight ongoing cost-reduction plans through 2026 that align with decarbonization investments and footprint optimization. These moves strengthen competitive positions during a phase when smaller or undercapitalized producers face rising compliance costs and tighter documentation requirements to participate in public procurement. Over the forecast, cost-structure differentiation and verified sustainability credentials are likely to be key determinants of share gains in the Europe ceramic tiles market.

Europe Ceramic Tiles Industry Leaders

Grupo Pamesa

Mohawk Industries (Marazzi, Ragno)

Porcelanosa Grupo

Gruppo Concorde (Atlas Concorde)

Iris Ceramica Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The European Commission proposed increasing anti-dumping duties on Chinese ceramic tableware to 79% from the current 13.1-36.1% range, a measure backed by industry groups and aimed at countering unfair trade practices that contributed to closures and job losses over the past decade.

- January 2025: Grupo Pamesa completed the acquisition of Natucer, a Castellón-based manufacturer with EUR 32 million in annual revenues, equal to USD 34.6 million, and 158 employees, consolidating regional capacity and expanding its specialty portfolio.

- January 2025: Grupo Pamesa announced EUR 65 million in 2025 capital investments, equal to USD 70.2 million, including two Supera continuous presses at Almassora for slabs up to 360 by 120 centimeters, a third kiln at Ascale to lift productivity, and a 24-bar digital printer to reinforce premium architectural offerings.

Europe Ceramic Tiles Market Report Scope

The ceramic tiles are thin slabs made from clay or other inorganic materials, typically rectangular, that cover surfaces.

The European ceramic tiles market is segmented by product, application, construction type, end user, and geography. By product, the market is segmented into glazed, porcelain, scratch-free, and other products (terracotta tiles). By application, the market is segmented into floor tiles, wall tiles, and other applications (countertops). By construction type, the market is segmented into new construction, replacement, and renovation. By end user, the market is segmented into residential and commercial. By geography, the market is segmented into the United Kingdom, Germany, France, Italy, Russia, Belgium, Poland, and Rest of Europe. The report offers market sizes and forecasts in value terms (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Germany |

| Italy |

| Spain |

| France |

| United Kingdom |

| Poland |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Germany | |

| Italy | ||

| Spain | ||

| France | ||

| United Kingdom | ||

| Poland | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe ceramic tiles market?

The Europe ceramic tiles market size is USD 8.31 billion in 2026 and is projected to reach USD 9.16 billion by 2031 at a 1.97% CAGR.

Which segments are leading and growing fastest within the Europe ceramic tiles market?

Porcelain led product revenue with 47.23% in 2025, while mosaic is the fastest with a 2.02% CAGR to 2031; floors held 60.12% by application, with walls growing at 2.04%; commercial end-user growth is fastest at 2.31%.

How will EPBD-related renovations affect the Europe ceramic tiles market?

EPBD transposition by May 2026 and renovation mandates to 2030 are front-loading public and co-financed retrofit demand, concentrating tile procurement into 2027 and 2028.

What sustainability documentation helps win public tenders in Europe?

ISO 17889-1 and Environmental Product Declarations are widely required by Nordic, BENELUX, and German procurement authorities, favoring documented suppliers.

How is competition structured across the Europe ceramic tiles market?

The landscape is highly fragmented with many mid-sized producers and active import competition, and cost-structure differentiation plus verified sustainability credentials are becoming decisive.

Which regions show the strongest growth within Europe?

BENELUX is the fastest-growing cluster through 2031, while Germany retains the largest national share by value.

Page last updated on: