Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 1.75 Billion |

| Growth Rate (2026 - 2031) | 3.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Ceramic Tiles Market Analysis by Mordor Intelligence

The Thailand ceramic tiles market size was valued at USD 1.42 billion in 2025 and estimated to grow from USD 1.47 billion in 2026 to reach USD 1.75 billion by 2031, at a CAGR of 3.57% during the forecast period (2026-2031). The growth path stems from sustained infrastructure spending under the Eastern Economic Corridor (EEC), a strengthening housing rebound, and tourism-led hospitality construction that together expand demand for premium tiling solutions. Government budget acceleration, notably in transport and utility upgrades, is reviving construction materials consumption after prior contractions, while hospitality developers race to add capacity ahead of a 40 million foreign-arrivals goal for 2025. Larger-format porcelain products and antimicrobial glazes are gaining share as architects prioritize aesthetics, hygiene, and durability, and thin-tile overlays are unlocking fast-track refurbishment projects in Bangkok’s dense urban fabric. Import pressure from China and Vietnam persists, yet stricter customs scrutiny and rising environmental standards offer quality-focused Thai manufacturers room to defend pricing.

Key Report Takeaways

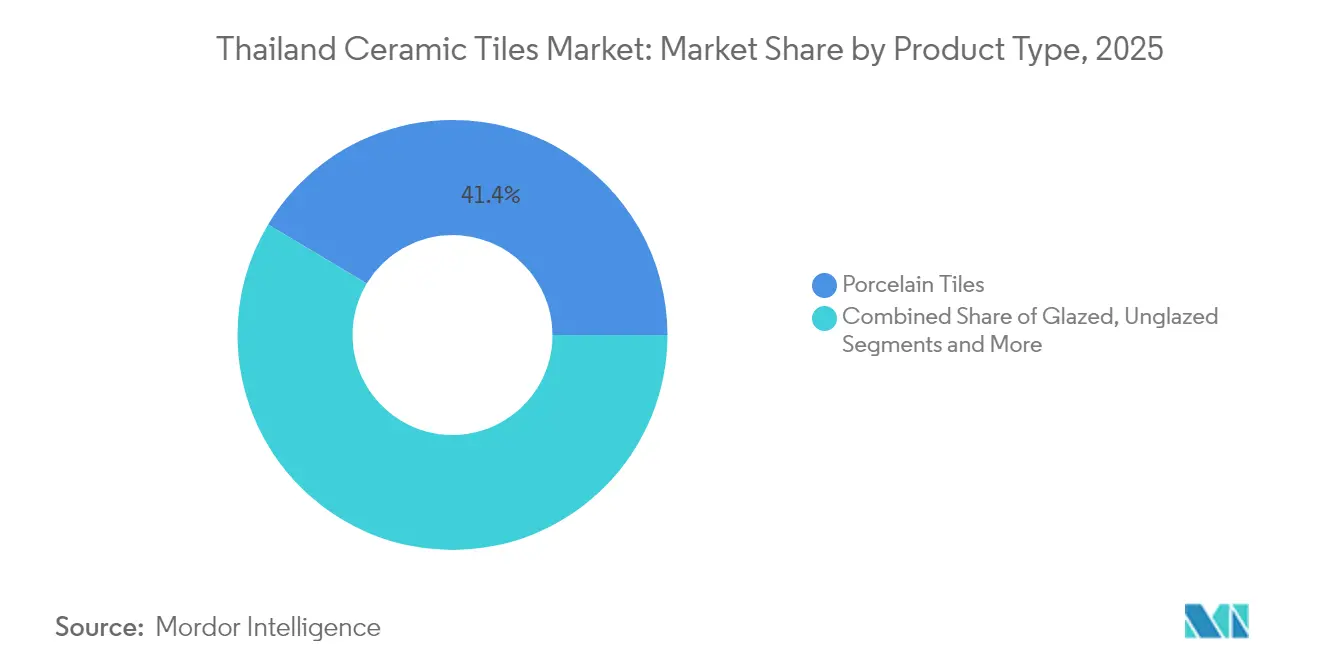

- By product type, porcelain led with 41.40% of Thailand's ceramic tiles market share in 2025, while mosaic tiles are projected to advance at a 4.33% CAGR through 2031.

- By application, floor installations accounted for a 58.50% share of the Thailand ceramic tiles market size in 2025; wall applications hold the fastest growth outlook at 4.65% CAGR.

- By end-user, the residential sector dominated with a 70.20% share in 2025 and is growing at a 4.38% CAGR on the back of stimulus-supported housing demand.

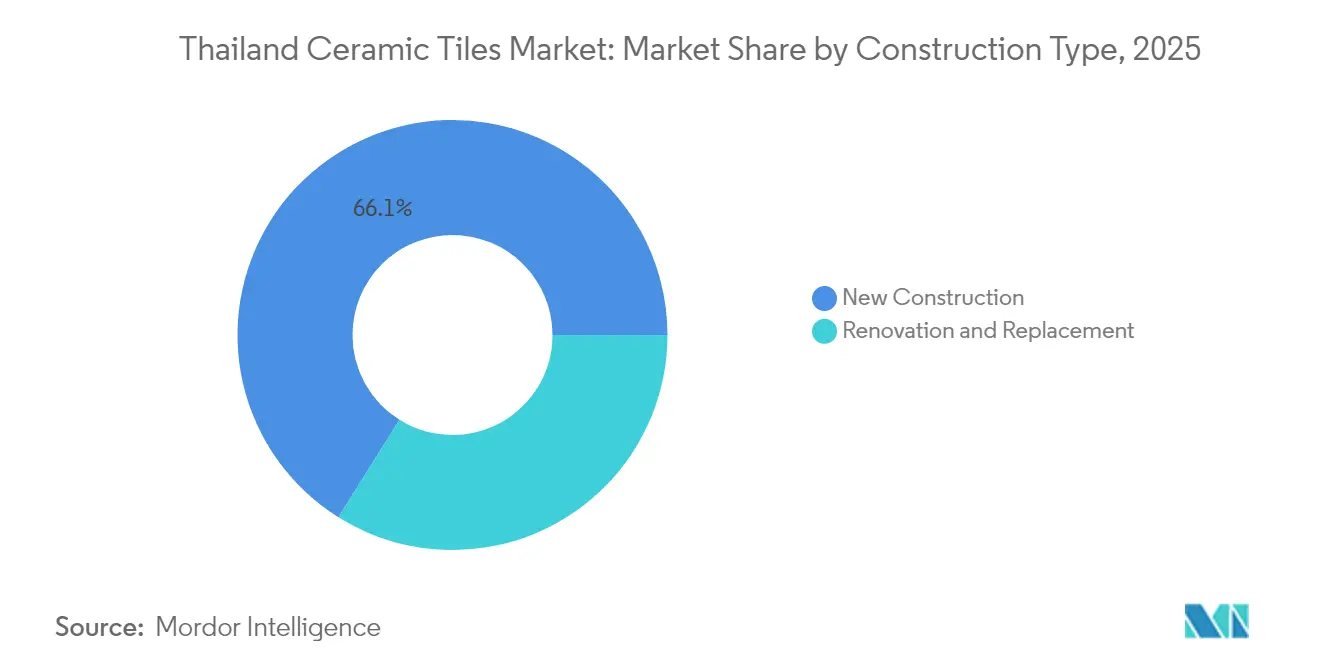

- By construction type, new builds supplied 66.10% of 2025 revenue, yet renovation and replacement activities posted the quickest expansion at 4.49% CAGR through 2031.

- By geography, Bangkok Metropolitan commanded a 34.60% share in 2025, whereas the EEC-focused Eastern Seaboard is set to rise at a 5.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban residential construction rebound | +0.8% | Bangkok Metropolitan, Eastern Seaboard, Central Thailand | Medium term (2-4 years) |

| Tourism-led expansion of hospitality projects | +0.6% | Bangkok Metropolitan, Southern Thailand, Eastern Seaboard | Short term (≤ 2 years) |

| Government EEC infrastructure build-out | +0.7% | Eastern Seaboard, Central Thailand | Long term (≥ 4 years) |

| Shift toward premium porcelain & large-format tiles | +0.5% | Bangkok Metropolitan, Central Thailand | Medium term (2-4 years) |

| Adoption of antimicrobial & easy-clean glazes | +0.3% | National, with early gains in Bangkok, Chonburi, Phuket | Short term (≤ 2 years) |

| Thin-tile overlay solutions boosting renovation demand | +0.4% | Bangkok Metropolitan, Central Thailand, Northern Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Residential Construction Rebound

New-home launches are climbing as the government sustains mortgage incentives and transfers fees reductions to stimulate demand. In the EEC, developers unveiled 400 projects worth THB 157 billion, pushing land prices up more than 50% in Chon Buri and satellite provinces. Leading builders such as Pruksa Holding and Sansiri are accelerating groundbreaks, which amplifies tile procurement cycles for both mid-market and luxury units. Foreign investors from China and Japan are co-developing mixed-use estates, adding higher-spec finish schedules that favor premium porcelain. Policy support for first-time buyers and rapid mass-transit extensions underpin steady residential demand through 2027. The residential construction rebound represents a fundamental shift from the pandemic-era slowdown, with developers now focusing on quality and sustainability features that require advanced ceramic tile solutions.

Tourism-Led Expansion of Hospitality Projects

Thailand targets 40 million foreign arrivals in 2025, pressuring hotel pipelines to add keys and refurbish legacy stock. Central Pattana opened five new hotels in 2024 and reported revenue of THB 46.8 billion, signaling strong sector recovery[1]Source: Central Pattana, “2024 Investor Presentation,” cpn.co.th. Boutique resorts are specifying antimicrobial, slip-resistant tiles that comply with international chains’ brand standards. Large-format porcelain slabs are favored to craft seamless lobby aesthetics while reducing grout maintenance in high-traffic zones. The tourism upswing therefore channels incremental volumes into specialized commercial-grade tile categories. The hospitality construction boom is also driving demand for large-format tiles and sophisticated surface treatments that can create distinctive visual experiences while maintaining operational efficiency in commercial settings.

Government EEC Infrastructure Build-Out

The EEC has attracted USD 39.0 billion in applications since 2016 and is mapping THB 500 billion more projects through 2027, including high-speed rail, deep-sea ports, and smart-city hubs. Foreign approvals surged 37% in 2024, with the corridor taking 54% of pledged investment. Industrial estates sold 8,063 rai in H1 2024, 60% of which lay inside the corridor, confirming construction momentum. These capital projects require durable floor and wall systems for terminals, factories, and logistics hubs where porcelain and technical ceramics outperform commodity options. Long build-out timelines ensure multi-year demand visibility for tile producers positioned in the region.

Shift Toward Premium Porcelain & Large-Format Tiles

Consumers are migrating from small-format ceramics to value-rich porcelain that delivers enhanced stain resistance and upscale aesthetics. SCG Decor’s X-PORCELAIN line is doubling exports in 2025, confirming appetite for high-strength, thin-profile slabs across ASEAN. Commercial architects prefer panels exceeding 1.2 meters to minimize joints and create contemporary visuals. Manufacturers are scaling kiln technology to fire larger bodies at tighter tolerances, elevating average selling prices. The move to premium formats is redefining competition away from price wars toward design leadership and performance assurance. The premium segment's growth is supported by Thailand's improving economic conditions and increasing disposable income among target consumer segments, enabling greater willingness to invest in high-quality building materials. This trend represents a fundamental market evolution from price-driven competition toward value-based differentiation through product innovation and design excellence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge of low-cost imports from China & Vietnam | -0.9% | National, with highest impact in price-sensitive segments | Short term (≤ 2 years) |

| Volatile natural-gas & electricity kiln costs | -0.6% | National, concentrated in manufacturing regions | Medium term (2-4 years) |

| Shortage of skilled tile installers | -0.4% | Bangkok Metropolitan, Eastern Seaboard, major urban centers | Long term (≥ 4 years) |

| ESG-driven kiln decarbonisation cap-ex burden | -0.3% | National, affecting all major manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge of Low-Cost Imports from China & Vietnam

Imports captured share by undercutting local ex-factory prices by up to 30%, forcing several Thai kilns to halve output in 2024. E-commerce platforms expedite direct consumer access to cheaper foreign tiles, bypassing traditional distributor vetting. The Federation of Thai Industries lobbies for safeguard duties and quality audits to restore competitive balance. Domestic firms respond by emphasizing design complexity, faster logistics, and warranty service impossible to replicate for overseas sellers. The dispute accelerates industry consolidation as sub-scale producers exit. The government is considering policy interventions including review of tax waivers on low-value imports and enforcement of stricter quality standards to level the competitive playing field for domestic producers. The import pressure is forcing industry consolidation and efficiency improvements as smaller manufacturers struggle to achieve economies of scale necessary for competing against large-scale Chinese and Vietnamese producers.

Volatile Natural-Gas & Electricity Kiln Costs

Energy constitutes roughly 35.0% of porcelain production costs, making Thai kilns sensitive to LNG import swings and spot electricity tariffs. Price jumps in late 2024 eroded margins, prompting temporary furnace shutdowns among smaller plants. Leading players invest in cogeneration and rooftop solar arrays to hedge volatility. The Energy Regulatory Commission is reviewing peak-time tariffs, yet relief remains uncertain. Cost instability complicates long-range cap-ex planning for capacity or format upgrades. Energy cost management is becoming a critical competitive factor as manufacturers with more efficient operations or better energy sourcing arrangements can maintain pricing flexibility during volatile periods. The volatility also complicates long-term planning and investment decisions as manufacturers must account for uncertain energy cost scenarios when evaluating capacity expansion or technology upgrade projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Drives Innovation

Porcelain tiles claimed 41.40% of Thailand's ceramic tile market share in 2025 on the back of superior density, water absorption below 0.5%, and design versatility. Glazed ceramic remains relevant for budget-focused builds, whereas unglazed technical bodies fill industrial floors requiring R-12 slip standards. Mosaic variants enjoy a 4.33% CAGR tailwind as boutique hotels and high-end condos specify statement backsplashes and pool linings through 2031. Decorative “others” such as handmade terracotta gain visibility through social-media-driven interior trends. Investments pivot toward pressing technology capable of 1600-ton compaction and digital inkjet lines that widen aesthetic offerings, cementing porcelain’s premium status.

Growing disposable income and imported design references accelerate consumer migration to large-format porcelain panels that slash grout lines and visually enlarge rooms. Thin-tile technology enables façade retrofits without adding excessive dead load, opening new commercial frontiers. Mosaic’s growth benefits from customizable mesh-mounted sheets simplifying complex layouts. Unglazed bodies align with EEC factory expansions where abrasion and chemical resistance outweigh aesthetics. Altogether these dynamics propel Thailand ceramic tiles market toward higher value mix despite volume pressure from imports.

By Application: Floor Leadership with Wall Growth

Floor installations represented 58.50% of the Thailand ceramic tiles market size in 2025 thanks to heavy commercial foot traffic and residential wear demands. Shopping malls, mass-transit hubs, and industrial corridors specify 600×600-millimeter porcelain pieces to balance load-bearing with cost. Wall cladding posts a 4.65% CAGR as designers push feature walls in living rooms and hotel lobbies that mimic marble and wood through 2031. Roofing applications, though niche, rely on traditional clay tiles for thermal insulation suited to tropical climates. The application split underscores diversification from purely functional flooring toward decorative vertical surfaces.

Wall expansion owes to technological leaps in inkjet realism, enabling stone-look veneers without maintenance burdens. Developers embrace full-height bathroom clads to reduce leak points and cleaning labor. Roofing sees incremental uplift in coastal resorts where salt-spray resistance is prized. Floor segments remain resilient via public-sector station builds and condominium corridors requiring PEI IV wear ratings. The evolving balance means manufacturers must tailor surface finishes, slip coefficients, and installation accessories per use case to sustain differentiation within Thailand ceramic tiles market.

By End-User: Residential Strength Sustains Growth

Residential buyers consumed 70.20% of 2025 volume, indicating homebuilding’s anchor role in Thailand's ceramic tiles industry evolution. Mortgage incentives and urban migration maintain steady condominium pipelines, while landed housing recovers in Bangkok fringes. Commercial demand spans hospitality, retail, healthcare, and education, each demanding specialized slip, stain, and hygiene credentials. Hospitality alone adds thousands of keys in Phuket and Pattaya, accelerating high-traffic porcelain uptake. Institutional build lean on easy-clean and antimicrobial surfaces to satisfy public-health guidelines.

Homeowners increasingly favor slim porcelain planks that replicate timber without termite risk, boosting renovation throughput. Commercial landlords pursue bold lobby statements and durability for return-to-office campaigns. Healthcare expansions under universal-care upgrades require low-VOC, chemical-resistant tiles. Education ministries specify vandal-resistant wall clads for new STEM campuses. Thus, diversified functional needs secure multi-segment resilience for the Thailand ceramic tiles market.

By Construction Type: New Projects Lead with Renovation Acceleration

New builds generated 66.10% of 2025 turnover as highway links, mass-transit extensions, and industrial parks trigger greenfield demand. Yet renovation posts a 4.49% CAGR, reflecting maturing building stock and owner preference for asset-life extension over raze-and-rebuild through 2031. Overlay porcelain lets malls refresh without shuttering, critical for rent continuity. Residential refurbishments adopt click-lock ceramic planks that fast-track weekend DIY makeovers. This dual-track growth hedges the sector against macro cycles, ensuring steady tile offtake.

Government condo-retrofit subsidies targeting energy efficiency spur the replacement of dated ceramic flooring with reflective, light-colored porcelain. Office landlords revamp washrooms with antimicrobial walls to lure tenants. Retail chains pilot overnight thin-tile installations to minimize downtime. Industrial floor overlays with 8 millimeter unglazed tiles rejuvenate logistics centers while resisting forklift abrasion. Consequently, the renovation’s rising share stabilizes Thailand's ceramic tiles market across volatile new-build cycles.

By Distribution Channel: Digital Disruption Accelerates

Specialty tile and stone stores captured 40.60% of 2025 revenue by offering curated showrooms, design advice, and installer matchmaking. Home-improvement chains cater to price-driven DIYers and small contractors through bulk discounts. Direct contractor sales enable volume deals on tower projects, bolstering manufacturer margins. Online marketplaces, expanding at a 5.42% CAGR, leverage 3D visualization tools and last-mile delivery to entice millennials comfortable with e-purchases through 2031. Omnichannel hybrids emerge as brick-and-mortar showrooms integrate virtual catalogs and click-and-collect services.

Digital uptake benefits rural customers previously underserved by physical outlets, broadening the geographic reach of the Thailand ceramic tiles market. Manufacturers invest in augmented-reality apps allowing homeowners to preview patterns at 1:1 scale. Specialty retailers layer subscription-based design studios for architects, deepening loyalty. Home-center chains add in-store kiosks linked to extended online assortments. Direct contractor portals streamline RFQs and specification downloads, shortening tender cycles and fortifying supplier-installer relationships.

Geography Analysis

Bangkok Metropolitan held 34.60% of Thailand ceramic tiles market share in 2025 due to dense high-rise activity, premium retail, and the capital’s high purchasing power. New sky-train lines and mixed-use megaprojects intensify tile demand across floors, walls, and façades. Central Thailand outside Bangkok benefits from spill-over industrial estates and affordable housing clusters feeding continuous mid-market consumption. The Eastern Seaboard records a 5.18% CAGR, buoyed by EEC incentives that spawn factories, ports, and smart cities requiring robust porcelain solutions through 2031. Northern and Southern regions leverage tourism renaissance to renovate resorts and build boutique lodgings, lifting mosaic and large-format sales.

Western Thailand sees incremental adoption due to border-trade logistics parks and eco-tourism circuits along the Myanmar frontier. Northeastern provinces (Isan) catch up as provincial capitals upgrade civic centers and hospitals, integrating easy-clean tiles into public facilities. Coastal southern cities such as Phuket and Krabi prioritize slip-resistant pool decks and salt-resistant roof tiles suited to humid maritime climates. Chiang Mai’s creative community spurs decorative and handmade tile uptake across cafés and guesthouses. Overall, national demand migrates from Bangkok dominance toward multi-regional growth nodes under infrastructure decentralization.

The continuing urbanization of secondary cities fosters retail complex development, stimulating premium wall cladding orders. Provincial universities erect STEM laboratories, specifying chemical-resistant unglazed flooring. Cargo-driven inland ports in Isan update logistics terminals using heavy-duty porcelain to withstand pallet jack traffic. Rail double-tracking across west and northeast stimulates station refurbishments demanding vandal-resistant glazed tiles. Regional diversification thus cushions Thailand ceramic tiles market against localized construction slowdowns.

Competitive Landscape

Thailand's ceramic tiles market exhibits moderate fragmentation with established domestic players maintaining strong positions through integrated supply chains, brand recognition, and distribution network advantages, while facing intensified competitive pressure from low-cost imports and emerging digital distribution channels. SCG Ceramics leads via its COTTO, Campana, and Sosuco lines, leveraging in-house raw-material quarries, a nationwide dealer network, and R&D labs advancing thin-body porcelain. Dynasty Ceramic and Royal Ceramic Industry maintain regional strongholds through mid-priced glazed offerings and contractor loyalty. RAK Ceramics Thailand and Johnson Tiles import global design catalogues and pursue hospitality and corporate fit-outs demanding international certifications. Importers of Chinese commodity tiles disrupt low-end segments, prompting Thai brands to elevate service and design differentiation.

Sustainability emerges as a strategic yardstick; SCG reported 80% of cement volumes as low-carbon in H1 2024 and is retrofitting kilns to cut CO₂ intensity, a template local ceramic units follow. Firms automate glazing lines and deploy AI for defect detection, boosting yield and reducing scrap. Digital marketing accelerates, with Instagram-ready room-set photography influencing consumer decisions and steering footfall to experience centers. Partnerships with Italian press and kiln vendors such as KEDA Industrial underscore technology transfer and capacity to produce 2 × 3 meter slabs showcased at Tecna 2024[2]Source: KEDA Group, “Tecna 2024 Press Release,” kedagroup.com. Government customs tightening on sub-quality imports positions compliant local producers for margin recovery.

M&A prospects loom as mid-tier players seek scale to fund ESG retrofits and branding. Private-equity interest surfaces around export-oriented niche makers of handmade tiles attractive to boutique hospitality clients. Regional expansion drives strategy; SCG Decor eyes Vietnam, the Philippines, and Indonesia’s THB 180 billion market to diversify revenue and optimize kiln utilization[3]Source: SCG, “Sustainability Report 2024,” scg.co.th. Brand collaborations with interior influencers promote limited-edition patterns, heightening consumer engagement. Overall, competition tilts toward innovation, green credentials, and omnichannel reach rather than price alone.

Thailand Ceramic Tiles Industry Leaders

SCG Ceramics

Dynasty Ceramic Public Co.

Royal Ceramic Industry

Kenzai Ceramic

Casa Tiles

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SCG Decor announced a plan to double exports of X-PORCELAIN tiles across ASEAN markets, citing demand for high-strength thin panels.

- February 2025: Ratanarak Group raised its stake in Siam City Cement to 71.88% after purchasing 25.54% from Jardine Cycle & Carriage, consolidating its influence in Thai construction materials.

- September 2024: KEDA Industrial Group highlighted expanded partnerships with SCG at Tecna 2024 to advance large-format ceramic technology and global collaboration initiatives.

Thailand Ceramic Tiles Market Report Scope

Ceramic tiles are a mixture of clays and other natural materials, such as sand, quartz, and water. They are primarily used in houses, restaurants, offices, shops, and so on, as bathroom walls and kitchen floor surfaces. They are easy to fit, easy to clean, easy to maintain, and are available at reasonable prices.

The Thailand ceramic tiles market is segmented by product, construction type, and end-user. By product, the market is subsegmented into glazed, porcelain, scratch-free, and other products. By application, the market is subsegmented into floor tiles, wall tiles, and other applications. By construction type, the market is subsegmented into new construction, replacement, and renovation. By end-user, the market is sub-segmented into residential and commercial. The report offers market size and forecasts for Thailand's ceramic tiles market in terms of revenue (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Bangkok Metropolitan |

| Central Thailand (ex-Bangkok) |

| Northern Thailand |

| Northeastern (Isan) |

| Eastern Seaboard |

| Western Thailand |

| Southern Thailand |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Bangkok Metropolitan | |

| Central Thailand (ex-Bangkok) | ||

| Northern Thailand | ||

| Northeastern (Isan) | ||

| Eastern Seaboard | ||

| Western Thailand | ||

| Southern Thailand | ||

Key Questions Answered in the Report

What is the current value of Thailand ceramic tiles market?

The market is valued at USD 1.47 billion in 2026 and is projected to reach USD 1.75 billion by 2031.

Which segment holds the largest share in Thailand ceramic tiles market?

Porcelain tiles hold the largest share at 41.40% in 2025.

Which region in Thailand is growing fastest for ceramic tiles?

The Eastern Seaboard, driven by the EEC, is forecast to grow at 5.18% CAGR.

How are online channels impacting tile sales in Thailand?

Online retail is the fastest-growing channel with a 5.42% CAGR as consumers embrace e-commerce and visualization tools.

What is the key restraint affecting Thai tile manufacturers?

A surge of low-cost imports from China and Vietnam pressures local prices and margins.

Page last updated on: