Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.02 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 3.51 Billion |

| Growth Rate (2026 - 2031) | 9.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Drones Market Analysis by Mordor Intelligence

The Asia-Pacific drones market size reached USD 2.02 billion in 2025, is expected to reach USD 2.21 billion in 2026, and is projected to reach USD 3.51 billion by 2031, at a 9.69% CAGR over 2026-2031. The current growth path reflects stronger policy tailwinds, visible cost declines in survey-grade sensors, and the scaling of precision use cases in fields like agriculture and infrastructure inspection, which convert pilot programs into recurring operations. Broader regulatory pilots in high-density corridors, including BVLOS trials in leading Asia-Pacific cities, are also expanding revenue-generating routes for time-critical logistics. At the same time, resilience measures against GNSS interference and smarter airspace coordination remain priorities for operators, which drives interest in alternative navigation stacks and UTM-aligned deployments in mature regulatory settings.[1]Source: Honeywell Aerospace, “Honeywell Launches New Alternative Navigation Software to Counter Jamming and Spoofing Threats,” honeywell.com The combined effect is a transition phase for the Asia-Pacific drones market, where government incentives, software-led autonomy, and purpose-built payloads work together to improve unit economics across priority missions.

Key Report Takeaways

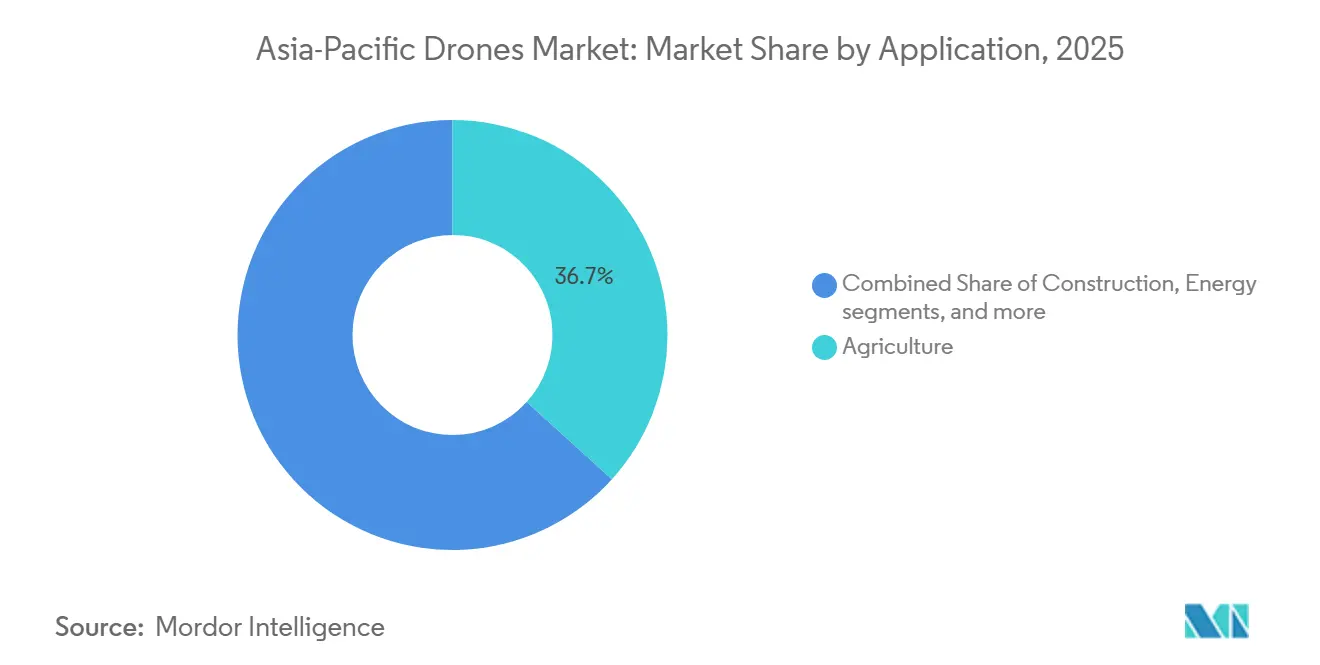

- By application, agriculture led with a 36.70% revenue share in 2025 and is forecast to expand at a 10.55% CAGR through 2031.

- By type, rotary-wing drones accounted for 65.54% of revenue in 2025, while hybrid/VTOL platforms are forecast to grow at a 13.20% CAGR through 2031.

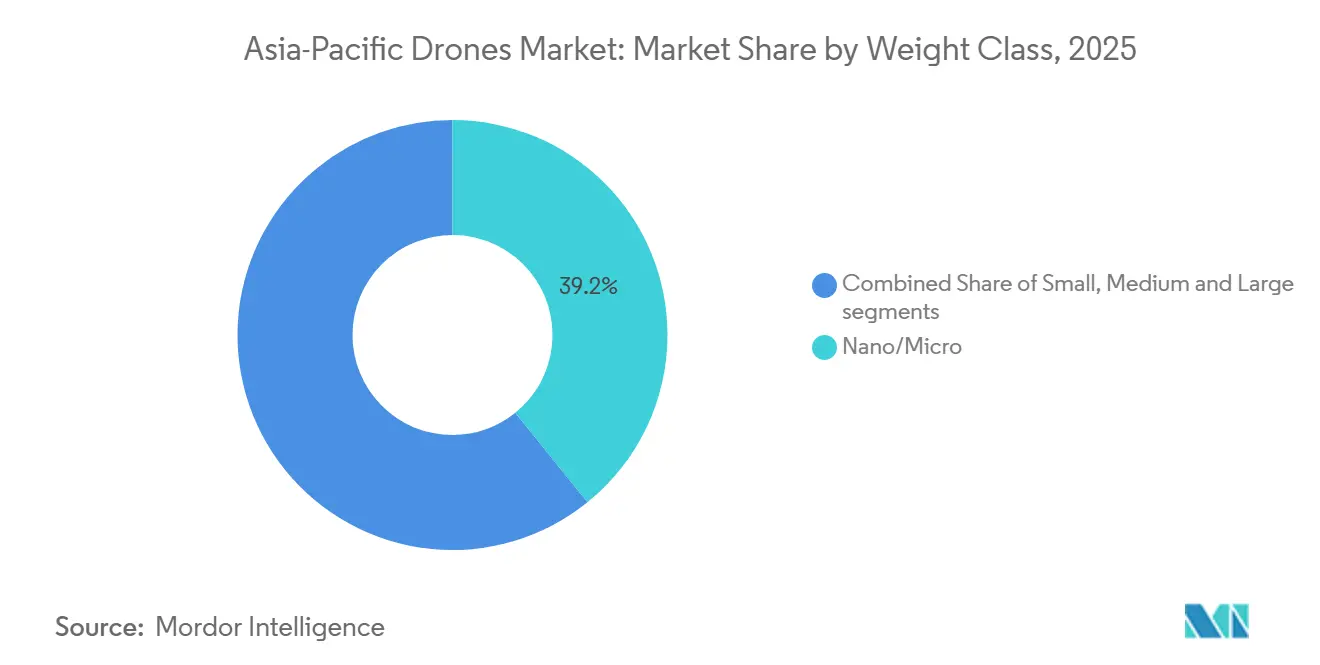

- By weight class, nano/micro platforms captured 39.20% share in 2025 and are projected to lead growth at a 12.54% CAGR through 2031.

- By mode of operation, remotely piloted systems accounted for 67.40% of 2025 deployments, while fully autonomous systems are projected to grow at a 12.70% CAGR through 2031.

- By end user, commercial and consumer/hobbyist users accounted for 70.54% of the 2025 base, while government and civil end users are projected to advance at a 10.20% CAGR through 2031.

- By geography, China led with a 35.40% market share in 2025, while India is projected to register the fastest outlook at a 10.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives for commercial drone adoption | +2.1% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Rapid proliferation of precision-agriculture programs | +1.8% | Global, with Asia-Pacific core (China, India, Southeast Asia) | Medium term (2-4 years) |

| Infrastructure-monitoring demand along Belt and Road projects | +1.3% | China, Central Asia spill-over, ASEAN corridors | Long term (≥ 4 years) |

| Urban e-commerce BVLOS delivery pilots | +0.9% | Singapore, Hong Kong, Shanghai, Tokyo metro | Short term (≤ 2 years) |

| Pay-per-flight insurtech coverage models | +0.7% | India, Southeast Asia, Australia | Short term (≤ 2 years) |

| Falling LiDAR and multispectral sensor costs | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Commercial Drone Adoption

Public policies continue to set demand floors and ease compliance for cross-border deployments in Asia-Pacific. China’s emphasis on a low-altitude economy and dedicated airspace infrastructure is driving faster approvals and a broader set of certified operations across logistics, public safety, and agriculture, thereby lifting addressable demand in the Asia-Pacific drones market. India’s ongoing incentive packages and local-content preferences are reinforcing domestic assembly and parts localization, thereby improving delivery lead times and supporting cost competitiveness for agricultural spraying and mapping providers in the region. South Korea’s reform track has relied on demonstration zones and targeted exemptions that allow BVLOS and complex test cases at the city scale, creating a path for operational data that shortens national authorization cycles thereafter.[2]Source: International Trade Administration, “Korea Drone Regulation Reform,” trade.gov Industry feedback in Australia and Japan also points to clearer pathways for multi-mission certification and interoperability, which reduces engineering rework for fleets moving between adjacent markets in Northeast and Southeast Asia. In parallel, regional coordination around UTM frameworks is gaining ground, signaling a gradual shift toward standardized detect-and-avoid and flight-approval interfaces that matter for scale deployments across Asia-Pacific hubs. Together, these policy signals encourage supplier investments and accelerate the commercialization of autonomy features and payload bundles.

Rapid Proliferation of Precision-Agriculture Programs

Precision agriculture remains the broadest commercial use case in Asia-Pacific, supported by active public programs and enterprise deployments that align drones, imaging payloads, and field analytics. China’s large agricultural drone base provides a steady stream of spraying and imaging missions that normalize drone services for input application, pest detection, and yield forecasting within mainstream farm operations in the Asia-Pacific drones market. India’s policy-led expansion of Drone-as-a-Service models eases access for smallholder farms. At the same time, hardware localization helps reduce the total cost of ownership for cooperatives operating during seasonal windows. Southeast Asian pilots are leveraging agronomy-specific payloads and software workflows to deliver variable-rate spraying and field-health diagnostics with short turnarounds, thereby improving ROI for recurring missions across rice, palm oil, and mixed crops. Japan and South Korea apply similar processes to address labor shortages and terrain constraints, positioning drones as practical tools in fields where ground machinery is less efficient or cannot operate safely. As sensor costs fall and cloud analytics are bundled with service contracts, more operators convert seasonal use into year-round revenue, supporting crop management before and after harvest.

Infrastructure-Monitoring Demand Along Belt and Road Projects

Transmission lines, pipelines, rail corridors, and high-value industrial assets on and near Belt and Road routes require frequent, safe inspection at scale, which favors drones equipped with thermal, LiDAR, and photogrammetry payloads. Utilities and rail operators in Asia-Pacific have shifted a growing share of patrols to unmanned platforms to improve data coverage and reduce downtime risk, helping expand recurring contracts for mapping and anomaly detection. With advancements in payload precision and extended flight endurance in fixed-wing and hybrid VTOL classes, operators can cover longer corridors with fewer sorties while obtaining higher-quality datasets. Upgrades to onboard processing and image-recognition models reduce manual review time and enable faster defect triage, supporting year-on-year growth in contracts for corridor surveillance in the Asia-Pacific drones market. These patterns set a stable demand base that complements cyclical construction cycles and adds resilience to service providers’ revenue mix.

Urban E-commerce BVLOS Delivery Pilots

Asia-Pacific metros are testing and certifying BVLOS delivery in controlled corridors that connect logistics hubs to residential or retail nodes. These efforts prioritize automated deconfliction, reliable command-and-control (C2) links, and standardized landing zones, which together unlock predictable service-level performance at lower cost than ground couriers over specific lanes. Regulatory approvals in advanced ecosystems across East and Southeast Asia have enabled consistent commercial trials for food delivery, pharmaceuticals, and small-parcel transportation. These trials serve as reference models that other cities can adopt following local risk evaluations. Emerging UTM integrations underpin credible safety cases for corridor-based operations that rely on geo-fencing, telemetry health checks, and dynamic rerouting. Underwriting shifts toward data-driven pricing in these lanes also support scale-up by helping small operators match coverage to actual flight counts and mission profiles. As a result, BVLOS logistics remains a visible near-term catalyst for the Asia-Pacific drones market in select cities with mature digital infrastructure and supportive regulatory sandboxes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Air-traffic-management bottlenecks in mega-cities | -1.4% | Seoul, Mumbai, Jakarta, major Asia-Pacific metros | Medium term (2-4 years) |

| Limited pool of certified commercial drone pilots | -0.8% | India, Southeast Asia, rural Asia-Pacific | Medium term (2-4 years) |

| Lithium-cell supply risk from EV sector crowd-out | -0.6% | Manufacturing hubs across Asia-Pacific | Long term (≥ 4 years) |

| Escalating GNSS spoofing and jamming incidents | -0.5% | Contested maritime/border zones, South China Sea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Air-Traffic-Management Bottlenecks in Mega-Cities

Dense urban airspace remains constrained in several Asia-Pacific metros, and legacy ATC processes are not designed for thousands of low-altitude flights per day. Without a mature UTM that automates separation, regulators tend to limit approvals to specific times or narrow corridors, reducing throughput for e-commerce deliveries and asset inspection missions that require a steady cadence. The most advanced cities are trialing integrated systems that fuse telemetry and geofencing data to reduce manual oversight. Yet, large-scale adoption still hinges on common standards and shared interfaces across agencies and operators. Equipment costs also rise when detect-and-avoid compute and sensor suites are added to small airframes, and this can delay scale-up for operators focused on sub-25 kg fleets. These factors collectively slow BVLOS expansion in urban cores and push a higher share of operations toward suburban or peri-urban corridors in the market until UTM coverage and rulesets are harmonized.

Limited Pool of Certified Commercial Drone Pilots

Training capacity has not kept pace with demand in several Asia-Pacific countries, which creates bottlenecks for operators that need mission-specific skills. Licensing requirements often differ by jurisdiction, so cross-border operations still entail incremental compliance and retraining costs for missions that are otherwise similar. Some governments have introduced sandboxes or simplified licenses for sub-25 kg drones to accelerate adoption in agriculture and light logistics. Still, full BVLOS certifications remain tightly controlled and data-heavy in their validation criteria. As a result, many fleets continue to maintain a human-in-the-loop for takeoff, landing, and contingency events even when routes are largely automated. Until training pipelines scale and mutual recognition frameworks mature, pilot supply and licensing complexity will temper near-term growth in the Asia-Pacific drones market, especially in rural or cross-border operations that need flexible staffing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Precision Tasks Propel Diversification Beyond Agriculture

Agriculture held a 36.70% share in 2025 and leads the application outlook at a 10.55% CAGR through 2031, supported by large spraying fleets and standardized imaging workflows that expand contract volumes across key Asia-Pacific farm belts. Construction accounted for a significant portion of revenue with widespread use in topographic surveys, progress tracking, and site safety audits, and adoption is rising as contractors hardwire aerial data into routine project controls. Energy operators continue to scale aerial inspection for transmission lines, wind assets, and utility-scale solar, thereby shortening inspection cycles and feeding predictive maintenance models that improve uptime across distributed assets. Law enforcement and public safety missions are growing on the back of ISR requirements and disaster response, with flight plans that emphasize corridor monitoring and rapid search patterns that complement manned assets. Entertainment use sits at a smaller base yet demonstrates the reliability of swarm software and coordinated flight, which then transfers to industrial use cases that require multi-unit synchronization. As payloads become modular and platforms support quick-swap mounts, operators can deploy the same airframe for NDVI mapping of farms, photogrammetry for construction, and thermal scans for utilities in the drones market in Asia-Pacific, thereby improving asset utilization throughout the year.

The market is supported by regulatory measures that streamline multi-application certification, allowing OEMs and service providers to deliver multiple workflows to the same client base. Public programs in developed markets have reduced compliance barriers for routine flights over familiar terrain, facilitating frequent image captures to maintain up-to-date project twins throughout construction cycles. In agriculture, precision drone usage is evolving into a year-round service, driven by activities such as input planning, mid-season health monitoring, and pre-harvest assessments. This shift helps stabilize operator revenue, which was previously concentrated in limited timeframes. Additionally, BVLOS approvals in select cities are creating opportunities for high-priority medical deliveries and small-parcel logistics, which require reliable time-to-destination and strict thermal control. Over time, the development of standardized regulations and common data protocols is expected to create a more level playing field for smaller service providers that can demonstrate consistent mission quality, thereby broadening the supplier base for diverse applications.

By Type: Hybrid/VTOL Disrupts Rotary Dominance in Logistics

Rotary-wing platforms led with 65.54% of 2025 revenue, driven by hover stability, small landing footprints, and mature supply chains that meet mainstream mapping and spraying needs across the Asia-Pacific drones market. Fixed-wing drones hold a meaningful share due to their long endurance for corridor mapping, where large areas must be covered with a consistent ground sampling distance. Hybrid/VTOL models post the fastest growth at a 13.20% CAGR through 2031 as logistics operators balance vertical takeoff with efficient cruise for routes spanning dozens of kilometers, often with cold-chain payload constraints that reward reliable air time. The 2025 amendments eliminated the need for an SFOC for most VLOS and certain BVLOS operations in the 25–150 kg category, introduced new pilot/operator certifications, and established technical standards. This modernizes Canada’s drone framework, primarily benefiting commercial operators and manufacturers, while recreational pilots remain governed by lighter rules for smaller drones. As more hybrid platforms support modular payloads for agriculture, survey, and cargo pods, operators can amortize airframe costs across multiple revenue streams. This modularity also helps manage inventory with fewer line items and faster turnaround between missions in dense schedules.

Certification advancements matter in this segment because they reduce engineering rework and enable multi-geography rollouts with the same baseline configuration. As UTM frameworks mature in advanced Asia-Pacific cities, hybrid platforms gain a relative advantage for repeat medium-range corridors that need consistent departure and arrival performance at small pads. The Asia-Pacific drones industry is also watching battery improvements and alternative propulsion options that extend endurance without sacrificing payload, which would widen the viable mission set for hybrid designs in logistics and inspection. Given these dynamics, hybrid/VTOL is set to take a growing role in lane-based delivery and long-span inspection. At the same time, rotary platforms continue to dominate short-duration imaging, close-in inspection, and most spraying tasks.

By Weight Class: Nano/Micro Dominance Reflects Regulatory Sweet Spot

Nano/micro drones under 2 kg captured 39.20% share in 2025 and led growth at a 12.54% CAGR, benefiting from user-friendly rules that speed up onboarding for creators, small businesses, and entry-level commercial missions in the Asia-Pacific drones market. Small class platforms from 2–25 kg serve as the professional workhorses across mapping, spraying, and inspection where payload needs exceed Micro capabilities. The medium class (25–150 kg) focuses on law enforcement and heavy-lift missions and requires more stringent certifications. In comparison, the large class (over 150 kg) remains niche and is often associated with eVTOL pilots and emergency logistics. Insurance pricing scales with weight due to risk exposure, which can influence fleet mix in urban use cases where lighter drones can meet most payload needs. As regional regulators refine thresholds, OEMs often target designs just under key cutoffs to compress time-to-market and keep operator training simpler.

The Asia-Pacific drones market continues to see innovation in battery packs and lightweight materials that increase endurance in lighter classes without pushing airframes into higher certification brackets. In agriculture, higher-capacity sprayers and terrain-following features are moving deeper into Small-class fleets to balance payload with regulatory simplicity. For inspection, lighter drones gain onboard processing that supports real-time analysis and anomaly flagging, which reduces the need to fly heavier platforms with large compute footprints. Over time, incremental improvements in energy density and airframe efficiency will keep most commercial activity concentrated below 25 kg, with Medium and Large classes reserved for specialized missions, government programs, and urban air mobility pilots.

By Mode of Operation: RPS’s 68% Share Masks Implementation Gaps

Remotely piloted systems accounted for 67.40% of operational deployments in 2025, reflecting operator and insurer preferences for human-in-the-loop oversight during high-value or complex missions that need flexible retasking. Fully autonomous modes post a 12.70% CAGR through 2031, mainly in applications such as warehouse inventory and agricultural spraying, and in approved BVLOS corridors where detect-and-avoid functions have been field-tested at scale. Optionally piloted configurations serve as a bridge in dense airspace, with manual takeoff and landing paired with autonomous cruise segments to balance compliance with efficiency. Underwriting and waiver pathways continue to reward proven safety cases that tie autonomy stacks to flight-history datasets, which encourages phased adoption rather than immediate full autonomy. These usage patterns explain why remote piloting still dominates installed bases even as autonomy gains share where rules and infrastructure are mature.

Growth in autonomy depends on UTM coverage, reliable, low-latency links, and regulators' acceptance of probabilistic safety cases. As agencies in advanced markets test and validate autonomy stacks at corridor and city scales, approvals for repetitive service lanes expand, accelerating automation in logistics and routine inspection missions. Edge inference engines reduce cloud roundtrips for object detection and compliance logic, thereby tightening control loops and protecting airspace boundaries during complex missions. The Asia-Pacific drones market is expected to see gradual increases in the adoption of autonomous systems as data capabilities and infrastructure improve. However, human oversight will continue to play a critical role in sensitive airspace until redundant systems and standardized verification frameworks are widely implemented.

By End-User: Government Initiatives Drive Security Modernization

Commercial and consumer/hobbyist users represented 70.54% of activity in 2025, with large installed bases in photography, mapping, and spraying that underpin service provider growth across multiple verticals in the Asia-Pacific drones market. Government and civil end-users advance at a 10.20% CAGR as ministries and agencies prioritize ISR, border security, disaster response, and public safety monitoring alongside controlled trials of logistics functions. Procurement tracks in Japan, South Korea, Australia, and India continue to fund both dual-use platforms and mission-tailored payloads, which spill into civilian markets through shared supply chains. Public safety deployments often pair drones with secure communications and encrypted data paths, which expands demand for platforms that meet hardened requirements. A divergence in mission profiles encourages OEMs to maintain dual product lines, with one optimized for civilian compliance and cost, and the other aligned with government-grade specs.

Government investments in UTM and infrastructure have facilitated civilian adoption, particularly benefiting commercial fleets in cities with established 5G networks and robust C2 systems. Additionally, data residency and telemetry safeguards play a significant role in vendor selection for government tenders, influencing local assembly, data hosting, and encryption protocols among suppliers serving both government and civilian clients. In the Asia-Pacific drones market, there is ongoing convergence between hardware and software, as government operational experience influences civilian standards for autonomy and safety. This creates spillover benefits for operators focused on critical infrastructure and logistics applications in regulated environments.

Geography Analysis

China led with a 35.40% share in 2025 on the back of a large registered fleet, public backing for low-altitude economic activity, and deep manufacturing capacity that supplies regional demand at scale, placing the country at the center of the Asia-Pacific drones market. Agricultural programs with sustained subsidies and operational logistics corridors help drive high sortie counts for spraying and delivery where approvals are in place. Expanded inspection use across energy and transport adds stability, and ongoing work on type certification for passenger-grade eVTOLs anchors an ecosystem that can spill into large-cargo platforms over time. Localized compliance frameworks support frequent corridor flights that feed continuous-image datasets for industrial analytics. These features together create a large, diversified demand base that sustains vendors across payload categories and service models.

India is the fastest-growing market, with a 10.80% CAGR through 2031, supported by local manufacturing incentives and streamlined permissions that expand civilian missions in agriculture, mapping, and public services in the Asia-Pacific drones market. Domestic procurement pathways and content preferences also lift demand for indigenous platforms and components, shortening delivery cycles for seasonal operations. State-level programs further drive rural aerial services, while training and sandbox policies expand the pool of pilots for entry-level missions.

Japan remains a critical market with advanced rules that enable BVLOS operations in defined corridors, supporting time-critical deliveries and dense mapping projects. Corporate investment in drones and robotics provides an anchor for software and payload ecosystems that integrate with industrial workflows and ERP systems. South Korea’s policy agenda enables demonstration cities and targeted exemptions for commercial trials, feeding a steady pipeline of operational data that informs national regulations and commercial waivers. Australia’s inspection-heavy use cases across mining and energy continue to grow as regulators expand BVLOS allowances for low-risk operations, which favors fixed-wing and hybrid fleets that can cover large sites in fewer sorties. Southeast Asian markets progress at different speeds as connectivity and rulesets vary, but precision agriculture and corridor logistics continue to gain traction where approvals and operator capacity align. Singapore’s BVLOS pilots and airspace management practices provide reference corridors for long-run commercial use in dense urban settings that other cities can adapt as UTM matures regionally, strengthening the market foundation for scale operations.

Competitive Landscape

The Asia-Pacific drones market features a unique split: high-volume consumer segments are dominated by a handful of global brands. In contrast, the non-consumer commercial segment is more fragmented across applications and services. DJI retains strong positioning in the prosumer and agricultural segments through the integration of airframes, flight controllers, gimbals, and batteries, which enable rapid model updates and a broad accessory ecosystem that appeals to service providers. In public procurement and sensitive verticals, local-content and security-driven preferences in markets like India, Japan, and Taiwan open room for regional OEMs and specialized integrators. Drone's focus on inspection-as-a-service and software reflects a shift in margins as hardware commoditizes and payload analytics drive value for enterprise accounts. Terra Drone was selected for the Project of Supporting Smart Agriculture Verification in Southeast Asia (Indonesia), Japan's Ministry of Agriculture, Forestry and Fisheries (MAFF). The project promotes Japanese smart agriculture technologies in Indonesia. Terra Drone is building networks with local companies for demonstrations and business development.[3]Source: Terra Drone, “Smart Agriculture Verification in Southeast Asia,” terra-drone.net

Strategic moves include expanding autonomy stacks resilient to GNSS interference and refining hybrid/VTOL platforms for medium-range logistics corridors under emerging BVLOS. Honeywell's alternative navigation release reflects a broader push by Tier-1 suppliers to harden autonomy and navigation in contested signal environments. This need applies to both inspection and logistics missions at scale. Regional service providers bundle analytics and data-hosting commitments into their contracts as agencies and industrial clients tighten requirements on telemetry handling and data sovereignty. Partnerships linking payload makers, platform OEMs, and analytics vendors are common as suppliers seek to deliver unified solutions that reduce integration effort for enterprise customers.

Integrated solutions that encompass airframes, payloads, autonomy, and insurance packages enhance customer retention and minimize switching by aligning hardware with operational economics. Major market players continue to invest in datasets to train autonomy and vision models, strengthening their performance in complex environments where safety relies on established field experience. Meanwhile, local companies benefit from policy preferences and customized support for domestic supply chains, enabling them to maintain their market share in government tenders and regulated operations within their home markets.

Asia-Pacific Drones Industry Leaders

SZ DJI Technology Co., Ltd.

Terra Drone Corporation

MicroMultiCopter (MMC) Aero Technology Co. Ltd.

Guangzhou EHang Intelligent Technology Co. Ltd.

Yuneec International (ATL Drone)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Aonic, a drone technology company founded in Malaysia and active throughout Southeast Asia, successfully raised USD 10 million in its latest funding round. Kairous Capital, a regional private equity and venture capital firm, spearheaded the Series A funding. Kairous is backed by Jelawang Capital and Malaysia's National Fund-of-Funds, which is part of its Emerging Fund Managers' Program. This influx of capital will propel Aonic's expansion both regionally and internationally, enhance its research and development efforts, and boost the production of its drones, software, and services, all crafted in Malaysia.

- April 2025: Garuda Aerospace raised INR 100 crore (USD 11.7 million) in Series B funding, valuing the company at USD 250 million. This development underscores the firm's strategic focus on enhancing domestic manufacturing capabilities, with an 85% indigenous content target. The funding positions Garuda Aerospace to strengthen its competitive edge in the drone industry, aligning with government initiatives promoting self-reliance in technology.

- January 2025: Terra Drone Corporation launched the "Terra Xross 1" indoor inspection drone in Japan, marking a strategic move to capture market share in the segment. This development underscores the company's focus on innovation and affordability, potentially reshaping competition in the indoor drone sector.

Asia-Pacific Drones Market Report Scope

The Asia-Pacific drones market encompasses commercial, industrial, and recreational unmanned aerial systems used in applications such as surveying, inspection, logistics, agriculture, cinematography, and environmental monitoring. These drones incorporate AI-based flight control, real-time imaging, and analytics to enable precise operations across various industries. Advancements in infrastructure inspection automation drive market growth, as does the expansion of e-commerce delivery and the adoption of precision agriculture. Key focus areas include regulatory compliance, extended endurance, and sensor integration to improve operational efficiency and safety in civilian and enterprise applications.

The Asia-Pacific drone market is segmented by application, type, weight class, mode of operation, end-user, and geography. By application, the market is segmented into construction, agriculture, energy, entertainment, law enforcement, and other applications. By type, the market is segmented by fixed-wing drones, rotary-wing drones, and hybrid/VTOL drones. By weight class, the market is segmented into nano/micro, small, medium, and large. By mode of operation, it is segmented into remotely piloted, optionally piloted, and fully autonomous. By end-user, the market is segmented into commercial and consumer/hobbyist, and government and civil. The report also provides market size and forecasts for 10 countries across the region. For each segment, the market size and forecast are provided in terms of value (USD).

By Application

| Construction |

| Agriculture |

| Energy |

| Entertainment |

| Law Enforcement |

| Other Applications |

By Type

| Fixed-Wing Drones |

| Rotary-Wing Drones |

| Hybrid/VTOL Drones |

By Weight Class

| Nano/Micro (Less than 2 kg) |

| Small (2-25 kg) |

| Medium (25-150 kg) |

| Large (Greater than 150 kg) |

By Mode of Operation

| Remotely Piloted |

| Optionally Piloted |

| Fully Autonomous |

By End-User

| Commercial and Consumer/Hobbyist |

| Government and Civil |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Indonesia |

| Singapore |

| Malaysia |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Application | Construction |

| Agriculture | |

| Energy | |

| Entertainment | |

| Law Enforcement | |

| Other Applications | |

| By Type | Fixed-Wing Drones |

| Rotary-Wing Drones | |

| Hybrid/VTOL Drones | |

| By Weight Class | Nano/Micro (Less than 2 kg) |

| Small (2-25 kg) | |

| Medium (25-150 kg) | |

| Large (Greater than 150 kg) | |

| By Mode of Operation | Remotely Piloted |

| Optionally Piloted | |

| Fully Autonomous | |

| By End-User | Commercial and Consumer/Hobbyist |

| Government and Civil | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Singapore | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size and growth outlook for the Asia-Pacific commercial drones market?

The Asia-Pacific drones market size was USD 2.02 billion in 2025, is expected to reach USD 2.21 billion in 2026, and is projected to reach USD 3.51 billion by 2031, at a 2026–2031 CAGR of 9.69%.

Which applications are leading and growing fastest in Asia-Pacific?

Agriculture led with 36.70% share in 2025 and also posts the highest growth at a 10.55% CAGR through 2031, supported by large spraying fleets and standardized imaging workflows.

What platform types are most competitive in Asia-Pacific?

Rotary-wing dominates 2025 revenue at 65.54% as the workhorse for mapping and spraying, while Hybrid/VTOL platforms are the fastest growing with a 13.20% CAGR for corridor delivery and long-span inspection.

Which countries are the largest and fastest growing in the region?

China held 35.40% share in 2025, while India has the fastest outlook at a 10.80% CAGR through 2031 on the back of local manufacturing incentives and streamlined permissions.

What are the main bottlenecks to scaling operations in Asia-Pacific cities?

Air-traffic-management constraints and the need for mature UTM limit concurrent BVLOS approvals in dense metros, and pilot licensing differences across jurisdictions increase compliance costs for cross-border fleets.

How are operators addressing GNSS spoofing and jamming risks?

Enterprise fleets are adopting alternative navigation stacks that fuse vision, terrain, and non-GNSS signals to maintain continuity in challenged environments, backed by Tier-1 suppliers releasing resilient software suites.

Page last updated on: