Car DVR Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.5 Billion |

| Market Size (2030) | USD 4.49 Billion |

| Growth Rate (2025 - 2030) | 5.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Car DVR Market Analysis by Mordor Intelligence

The Car DVR market size stood at USD 3.5 billion in 2025 and is projected to climb to USD 4.49 billion by 2030, translating into a 5.11% CAGR. Consistent regulatory pressure for eCall and ADAS compliance, combined with insurance premium incentives and falling component costs, is sustaining double-digit unit growth across developed and emerging regions. Original-equipment integration is accelerating as automakers bundle dash cameras with broader safety suites, while the aftermarket channel remains resilient because hobbyists and fleet operators value installation flexibility and rich feature sets. Rapid adoption of AI-based video analytics is redefining product value, transforming cameras from passive recorders into active risk-mitigation tools. Competitive intensity is strengthening as electronics majors, tier-one suppliers, and fast-moving Asian brands pursue price-performance advantages and global distribution agreements.

Key Report Takeaways

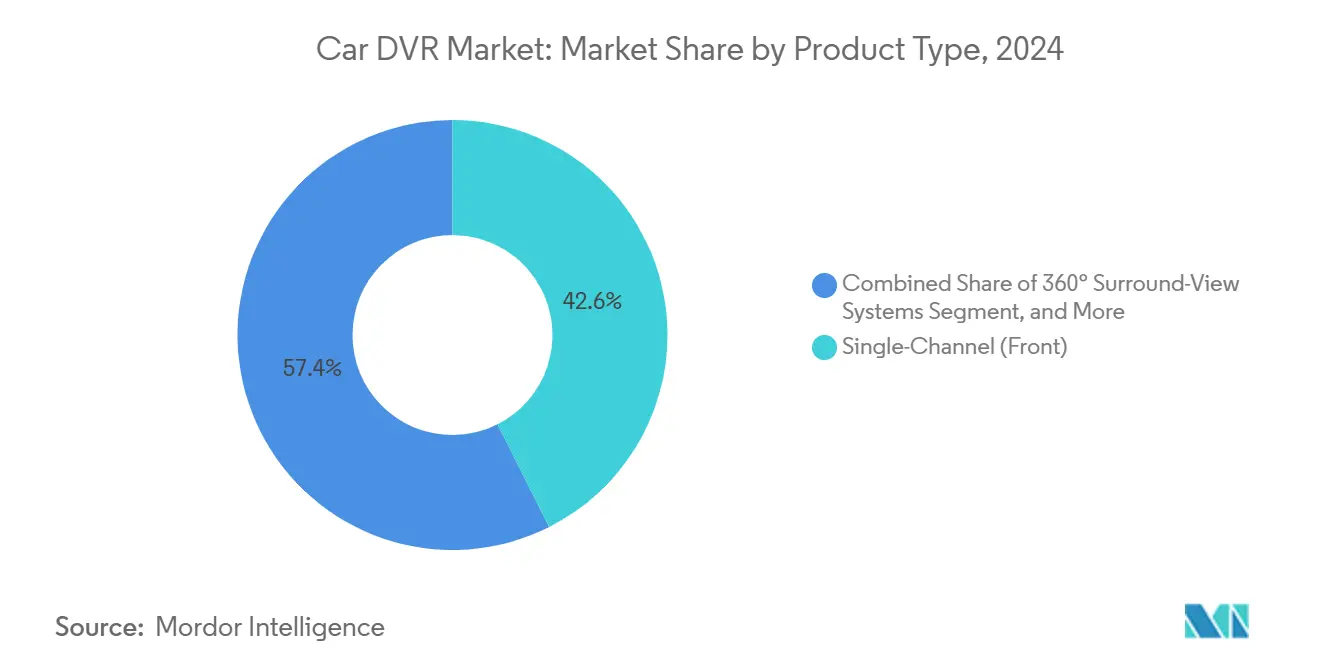

- By product type, single-channel front-facing units led with 42.57% revenue share in 2024, while dual-channel front + rear systems are projected to advance at a 5.33% CAGR through 2030.

- By vehicle type, passenger cars commanded 63.11% of 2024 revenue; light commercial vehicles are forecast to grow at a 6.15% CAGR to 2030.

- By sales channel, the aftermarket held 67.34% share in 2024, whereas OEM installations are set to rise at a 7.24% CAGR through 2030.

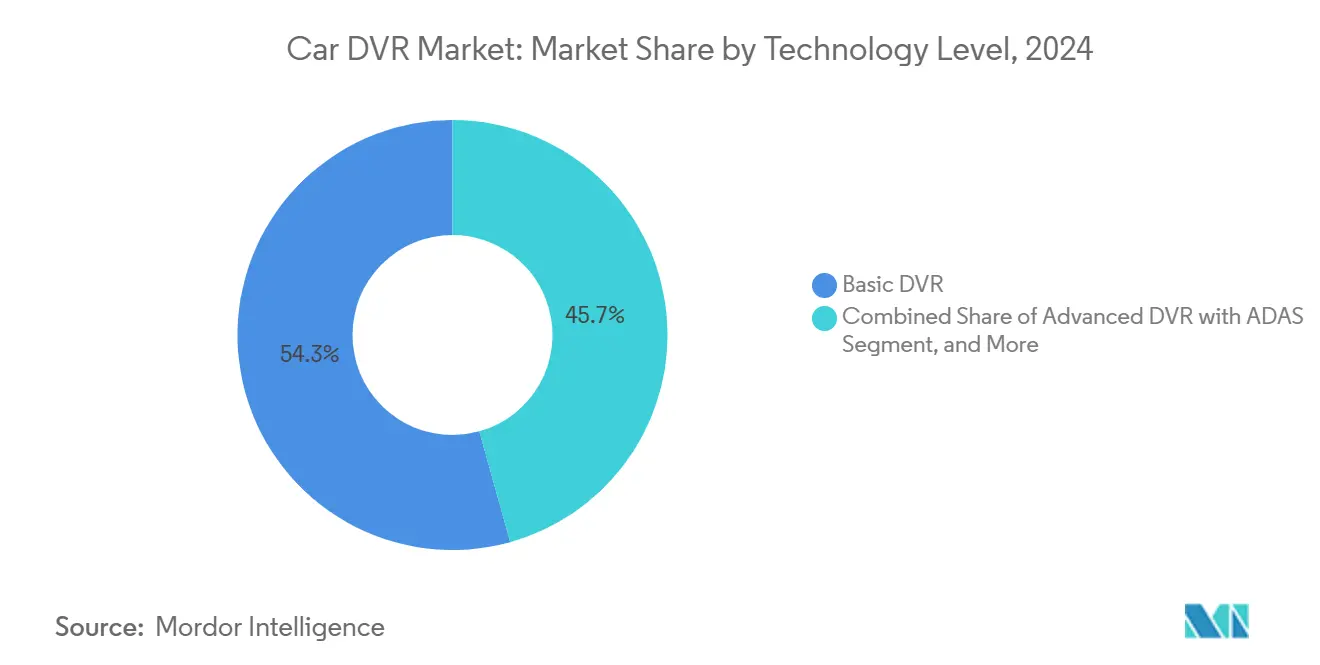

- By technology level, basic DVR systems accounted for 54.32% of 2024 revenue, but smart connected DVRs are expected to expand at a 6.36% CAGR to 2030.

- By video quality, SD/HD units (≤720p) retained 47.84% share in 2024, while 4K-and-above models are poised to grow at a 6.29% CAGR through 2030.

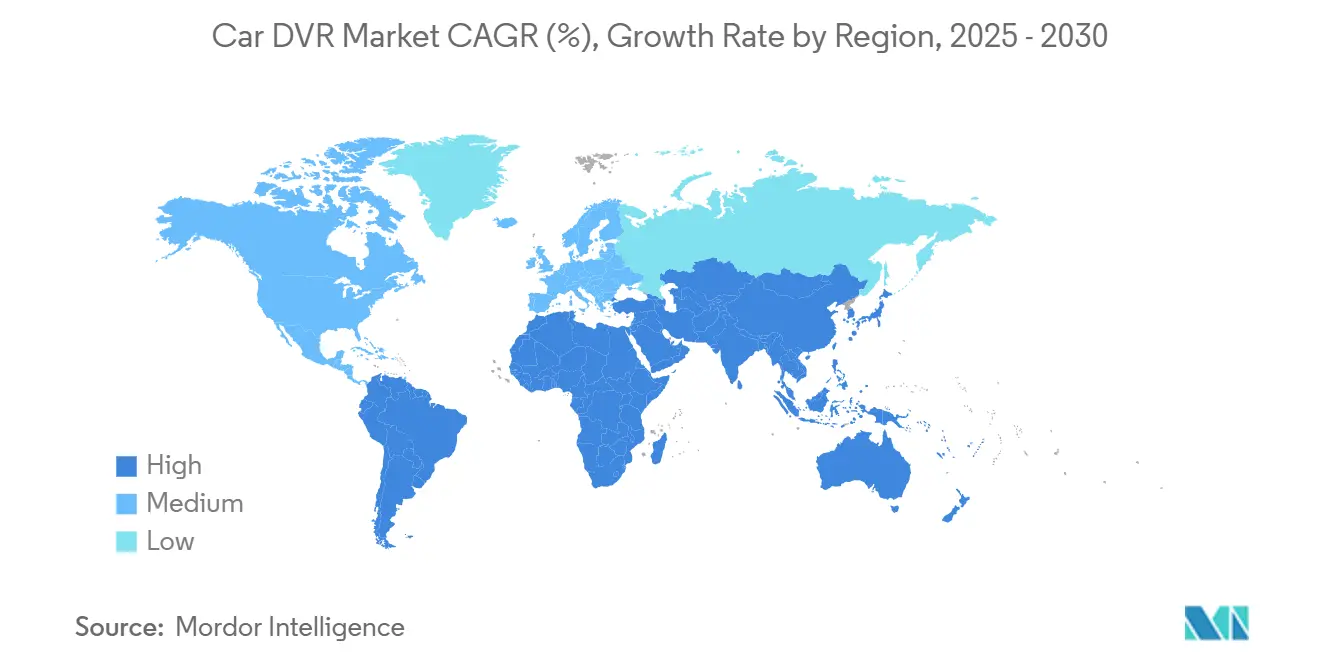

- By geography, Europe led with 31.46% revenue share in 2024 and Asia-Pacific is projected to register a 5.73% CAGR toward 2030.

Global Car DVR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Insurance premium discounts for dash-cam-equipped vehicles | +0.8% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Stricter ADAS / eCall regulations in EU, South Korea and Japan | +1.2% | EU core, expanding to Asia-Pacific markets | Medium term (2-4 years) |

| Fleet-wide video-telematics adoption by ride-hailing and logistics operators | +0.9% | Global, concentrated in urban markets | Short term (≤ 2 years) |

| Integration of AI-powered driver-monitoring and incident-detection analytics | +1.1% | Developed markets initially, scaling globally | Medium term (2-4 years) |

| Falling solid-state storage and CMOS sensor costs | +0.7% | Global manufacturing impact | Long term (≥ 4 years) |

| Embedded 5G / V2X modules enabling real-time cloud uploads | +0.6% | Advanced markets with 5G infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Insurance premium discounts for dash-cam-equipped vehicles

Major insurers now offer 10–15% premium reductions to policyholders who install certified dash cameras. Commercial fleets using video-based driver monitoring cut fuel spend by 16% and accident-related expenses by 22%. The evidentiary value of footage is well established, with driver-facing video exonerating operators in roughly half of claims and litigation cases.[1]Wasson, Thomas, “C.R. England Adopts AI-Powered Driver-Facing Cameras,” freightwaves.com As underwriters embed telematics data into risk models, dash cameras become an indispensable component of usage-based insurance programs that are moving from fleets into private-passenger lines. The financial incentive directly expands the Car DVR market by shortening payback periods for both retail buyers and fleet managers. Momentum is expected to hold because claims-cost containment remains a structural priority for insurers in all major regions.

Stricter ADAS / eCall regulations in EU, South Korea and Japan

The European Union has required eCall functionality in new passenger vehicles since 2018 and is now layering advanced camera-based safety mandates on top of that baseline. South Korea’s roadmap obliges driver-monitoring systems in commercial vehicles by 2025, while Japan has tightened collision-avoidance standards that implicitly demand multi-purpose cameras. New U.S. Federal Motor Vehicle Safety Standard 127 adds automatic emergency-braking requirements that push camera costs an extra USD 200–300 per vehicle. These rules lift the floor for hardware specifications, converting Car DVR market demand from discretionary to compulsory in regulated classes. Suppliers that can certify multi-function systems at automotive-grade reliability secure preferred-supplier status with global OEMs, reinforcing upward volume visibility for the next decade.

Fleet-wide video-telematics adoption by ride-hailing and logistics operators

High-volume carriers such as C.R. England outfitted 3,500 tractors with AI-enabled cameras, showcasing the scale at which fleets seek safety and liability protection. In Australia and New Zealand, installed fleet-management units are forecast to jump from 1.6 million in 2023 to 2.7 million in 2028 as chain-of-responsibility laws tighten.[2]Libatique, Roxanne, “Fleet Tech Boom Expected in Australia and New Zealand by 2028,” insurancebusinessmag.com Investor enthusiasm echoes the operational rationale: Standard Fleet raised USD 13 million to merge digital-key control with video monitoring for mixed fleets. Seventy-five percent of managers surveyed report quantified accident reductions after deploying in-cab video. These metrics reinforce a recurring-revenue model for cloud subscriptions that augments hardware sales, expanding the Car DVR market into a service-oriented ecosystem.

Integration of AI-powered driver-monitoring and incident-detection analytics

Partnerships such as ECARX with FAW deploy AI-powered perception modules that transform dash cameras into real-time behavior analysts. Advanced algorithms now flag distraction, tailgating, or seat-belt non-compliance and deliver instant coaching prompts that improve driving scores on the spot. Verizon Connect’s 2025 technology outlook positions AI video as a cornerstone of personalized safety programs that scale across multi-brand fleets.[3]Mitchell, Peter, “Verizon Connect Fleet Management 2025 Outlook,” fleetmaintenance.com The shift from mere recording to predictive intervention sustains premium ASPs in the Car DVR market because buyers value documented loss-rate improvement more than hardware specs alone. Suppliers that master AI models, edge processing, and secure cloud integration command defensible differentiation even as sensor costs drop.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmentary privacy laws limiting on-road video recording (EU, Brazil) | -0.4% | EU under GDPR, Brazil LGPD, select US states | Medium term (2-4 years) |

| Cyber-security vulnerabilities in connected DVR firmware | -0.3% | Global, concentrated in connected device markets | Short term (≤ 2 years) |

| Up-front cost sensitivity in entry-level vehicles of emerging markets | -0.5% | Emerging markets, price-sensitive segments | Long term (≥ 4 years) |

| Limited OEM standard-fitment outside premium vehicle segments | -0.4% | Global, varying by OEM strategy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmentary privacy laws limiting on-road video recording

GDPR in Europe and Brazil’s LGPD require explicit consent for processing identifiable data, forcing dash-cam makers to implement on-device masking, short retention windows, and opt-in workflows. Twelve U.S. states demand all-party permission for audio capture, so vendors like 70mai ship region-specific firmware that disables microphones by default. Compliance features raise engineering effort and unit cost, slowing deployments among small fleets and private owners who do not perceive the legal nuances. For global brands, overlapping rules mean extended certification cycles that delay product launches and complicate over-the-air update schedules. As lawmakers continue refining data-protection statutes, uncertainty will weigh on near-term adoption rates in privacy-sensitive jurisdictions, tempering otherwise strong Car DVR market momentum.

Cyber-security vulnerabilities in connected DVR firmware

Real-time streaming devices such as DDPAI Z60 Pro and Vantrue S1 Pro rely on 4G or Wi-Fi links that can expose location and video feeds if encryption or access control is weak. Attack-surface expansion increases liability for fleets because compromised video may reveal routing patterns or personal data. The aftermarket character of many units means security patches are user-initiated, and compliance gaps persist when owners ignore update prompts. Manufacturers now invest in secure boot, hardware root-of-trust, and FIPS-compliant encryption to close exploit windows, pushing up bill-of-materials and certification costs. Until best-practice frameworks are standardized across the supply base, perceived cyber risk will dilute purchasing intent in the connected segment of the Car DVR market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dual-channel adoption accelerates comprehensive coverage

Single-channel front-facing units captured 42.57% of the Car DVR market share in 2024, reflecting their value proposition for customers who favor lower prices and simple wiring. The configuration serves insurance-evidence needs for individual drivers and entry-level fleets. Growth persists as first-time buyers enter the Car DVR market, yet its expansion pace is moderating as multi-camera options become more affordable. Dual-channel front-and-rear solutions are advancing at a 5.33% CAGR through 2030, buoyed by claims that rear-end collisions account for one-third of road incidents and require rear footage for fault adjudication.

Demand for 360-degree surround-view and triple-channel cabin-view systems signals a shift toward perimeter perception once limited to premium cars. CES 2025 prototypes revealed multi-sensor sets that merge high-resolution optics with AI object detection to deliver blind-spot alerts and parking guidance. In ride-hailing fleets, inward-facing cameras deter misconduct and support driver-behavior scoring, helping operators negotiate favorable insurance rates. The trend elevates ASPs and encourages chipset vendors to integrate quad-ISP architectures, further enriching the Car DVR market product roadmap.

By Vehicle Type: Commercial uptake leads risk-management agenda

Passenger cars generated 63.11% of 2024 revenue, underpinned by growing consumer awareness and falling price points. Retail adoption benefits from insurance discounts and viral social-media footage that demonstrates evidentiary value. Light commercial vehicles record the fastest 6.15% CAGR as last-mile delivery, field service, and ride-hailing operators institutionalize video telematics for loss prevention and service verification. The Car DVR market size for this segment is projected to widen in tandem with e-commerce logistics expansion.

Heavy commercial vehicles maintain steady purchasing because regulatory mandates and cargo-liability exposure obligate robust recording. Many trucking firms integrate cameras with electronic logging devices to streamline compliance reporting. Sustainability priorities add momentum, as fleet managers use video-assisted coaching to cut idling and aggressive acceleration, trimming fuel and emissions footprints. Consequently, the Car DVR industry sees hardware shifting from basic SD cards toward edge-AI designs that complement telematics gateways found in modern commercial cabs.

By Sales Channel: OEM alignment reshapes distribution economics

Aftermarket products dominated 67.34% of the Car DVR market size in 2024 thanks to broad SKU variety, convenient e-commerce access, and do-it-yourself installation appeal. Independent installers and specialist retail chains maintain strong pull through recurring upgrade cycles. However, OEM factory fitment exhibits a 7.24% CAGR to 2030 as brands add dash-cam lines to safety bundles in response to customer demand and competitive positioning. Toyota’s decision to wire dash cameras into the 2024 4Runner underscores mainstream acceptance among volume automakers.

OEM integration enhances functional cohesion because cameras leverage in-vehicle power, CAN-bus triggers, and infotainment displays. The approach simplifies warranty claims and firmware update logistics, a benefit not always available with aftermarket kits. Tier-one suppliers that already deliver ADAS radars are cross-selling camera modules, further consolidating supplier bases. Regionally, Europe leads OEM penetration because UNECE rules encourage unified safety suites, whereas North America continues to see vibrant aftermarket sales that sustain entrepreneurial brands within the Car DVR market.

By Technology Level: Smart connected systems capture value premium

Basic recorders retain 54.32% share in 2024 by fulfilling minimal evidentiary needs at price points below USD 100. Yet smart connected variants sporting LTE, Wi-Fi, and AI are advancing at a 6.36% CAGR, adding cloud-based auto-backup, driver scoring, and live-stream capabilities. Advanced units with ADAS overlays occupy the middle, appealing to safety-aware users who are not ready to pay subscription fees.

The 70mai Omni 4K employs Sony STARVIS 2 sensors and onboard neural networks to predict collisions and notify emergency contacts. Fleet operators appreciate over-the-air diagnostics that cut service downtime by flagging SD-card issues before recording gaps occur. As mobile-data tariffs decline and edge compute becomes cheaper, connected dash cameras will anchor integrated mobility platforms that fuse video, telematics, and predictive maintenance, reinforcing the recurring-revenue narrative within the Car DVR market.

By Video Quality: 4K resolution elevates forensic accuracy

SD/HD (≤720p) equipment retained 47.84% share in 2024 because entry-level consumers value affordability over pixel granularity. Full-HD 1080p units form the mass-market core, balancing clarity and storage demands. The high-end 4K tier is growing at 6.29% CAGR, driven by falling NAND prices and advanced compression that stream high-bitrate footage economically.

Sony’s 3D-stacked automotive CMOS chips deliver superior dynamic range for nighttime scenes, enabling license-plate recognition at distance without motion blur. Premium fleets use these capabilities to combat cargo theft and verify delivery events. Content creators also post incident footage on social platforms, raising consumer expectations for crystal-clear imagery and indirectly widening the Car DVR market addressable audience.

Geography Analysis

Europe commanded 31.46% revenue in 2024, supported by mandatory eCall, upcoming Euro NCAP driver-monitoring criteria, and mature safety awareness among motorists. Countries such as Germany and the United Kingdom maintain strong spending on premium 4K dual-channel kits, and GDPR compliance has spurred adoption of on-device anonymization that favors sophisticated vendors. Public awareness campaigns by insurers further amplify unit velocity.

Asia-Pacific is the fastest-expanding region at a 5.73% CAGR through 2030. China’s 2024 NCAP update obligates in-cab cameras for commercial vehicles, while South Korea’s autonomous-driving timeline and Japan’s K-MP/K-SAFE standards elevate technical baselines. Local champions including Xiaomi’s 70mai and Hikvision pair aggressive pricing with feature innovations, fueling volume ramp-up. The scale advantages enjoyed by regional optics and memory suppliers feed a virtuous cycle that compresses global bill-of-materials.

North America shows consistent uptake anchored in insurance incentives and fleet telematics convergence. State-level windshield-mount rules vary, but legislative proposals trend toward permissive use coupled with clear disclosure, offering regulatory clarity. The Middle East and Africa are emerging opportunities as logistics corridors expand and governments target road-fatality reductions through Vision 2030-style programs. South America is gradually catching up; Brazil’s LGPD increases compliance costs yet provides a legal framework that reassures enterprise buyers evaluating connected dash-cam deployments.

Mordor Intelligence provides coverage of the car dvr market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The Car DVR market is moderately fragmented. Legacy brands such as Garmin, Nextbase, and BlackVue leverage recognized quality and broad retail footprints to defend share, while 70mai and Thinkware employ competitive pricing and fast iteration cycles to penetrate new geographies. Feature races revolve around AI algorithms, multi-channel support, cloud subscriptions, and 5G connectivity. September 2024 saw Garmin introduce the Dash Cam X series with native vehicle-bus integration, signaling incumbents’ commitment to platform evolution.

Strategic collaborations reflect vertical-integration ambitions. ECARX links chipsets, operating systems, and dash cameras into a single cockpit domain, winning FAW’s Hongqi line as an anchor program. Insurance tie-ups are also prominent; multiple carriers now bundle premium discounts with approved camera brands, aligning vendor roadmaps with actuarial requirements. Start-ups exploit white-space niches, such as solar-powered parking mode modules and AI-based privacy masking, to differentiate themselves in saturated online marketplaces.

Supply-chain vigilance remains crucial because global CMOS sensor shortages and memory constraints can extend lead times. Vendors hedging through multi-foundry arrangements suffer fewer stock-outs, capturing opportunistic demand spikes. Overall, top five players account for a significant share of global revenue, signaling a competitive yet consolidating arena where innovation speed and channel leverage dictate outcomes.

Car DVR Industry Leaders

ABEO Technology Co., Ltd.

Garmin Ltd.

Nextbase Limited

Pittasoft Co., Ltd. (BlackVue)

Thinkware Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Standard Fleet secured USD 13 million in Series A funding to expand mixed-fleet connectivity solutions and roll out an upgraded digital-key platform that integrates real-time video monitoring.

- January 2024: ECARX announced a strategic partnership with FAW to launch the first Hongqi model featuring AutoGPT with DeepSeek-R1 integration

- December 2024: Honda and Nissan signed an MoU to merge operations, creating a potential top-three automaker focused on electric vehicles and integrated camera safety suites

- September 2024: Garmin unveiled the Dash Cam X series, adding enhanced integration features for automotive applications

Global Car DVR Market Report Scope

| Single-Channel (Front) |

| Dual-Channel (Front + Rear) |

| 360° Surround-View Systems |

| Triple-Channel / Cabin-View |

| Rear-View-Only Dash Camera |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Aftermarket |

| OEM-Installed |

| Basic DVR |

| Advanced DVR with ADAS |

| Smart Connected DVR (AI/Cloud) |

| SD / HD (≤720p) |

| Full HD (1080p) |

| 4K and Above |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Single-Channel (Front) | ||

| Dual-Channel (Front + Rear) | |||

| 360° Surround-View Systems | |||

| Triple-Channel / Cabin-View | |||

| Rear-View-Only Dash Camera | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| By Sales Channel | Aftermarket | ||

| OEM-Installed | |||

| By Technology Level | Basic DVR | ||

| Advanced DVR with ADAS | |||

| Smart Connected DVR (AI/Cloud) | |||

| By Video Quality | SD / HD (≤720p) | ||

| Full HD (1080p) | |||

| 4K and Above | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

Dash-cam discounts: what do insurers currently offer?

Leading carriers provide 10–15% premium reductions when certified cameras are installed, and claim processing times drop because video clarifies liability.

Which region is growing fastest in Car DVR adoption?

Asia-Pacific leads with a 5.73% CAGR through 2030 as China, South Korea, and Japan tighten camera-based safety rules.

Why are light commercial fleets investing in multi-channel dash cameras?

Fleet managers see measurable ROI through lower accident rates, fuel savings, and faster claim resolution, supporting a 6.15% CAGR for the segment.

How are AI features changing dash-cam value?

On-device analytics now detect distraction and predict collisions, converting cameras from passive recorders into active safety tools that justify higher prices.

What privacy safeguards do modern dash cameras include?

GDPR-compliant models offer face blurring, adjustable retention windows, and region-specific audio settings to meet diverse data-protection laws.

Are OEM-installed systems overtaking aftermarket units?

Factory fitment is rising at a 7.24% CAGR, yet the aftermarket still holds 68% share because buyers value feature variety and retrofit flexibility.

Page last updated on: