North America Car DVR Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

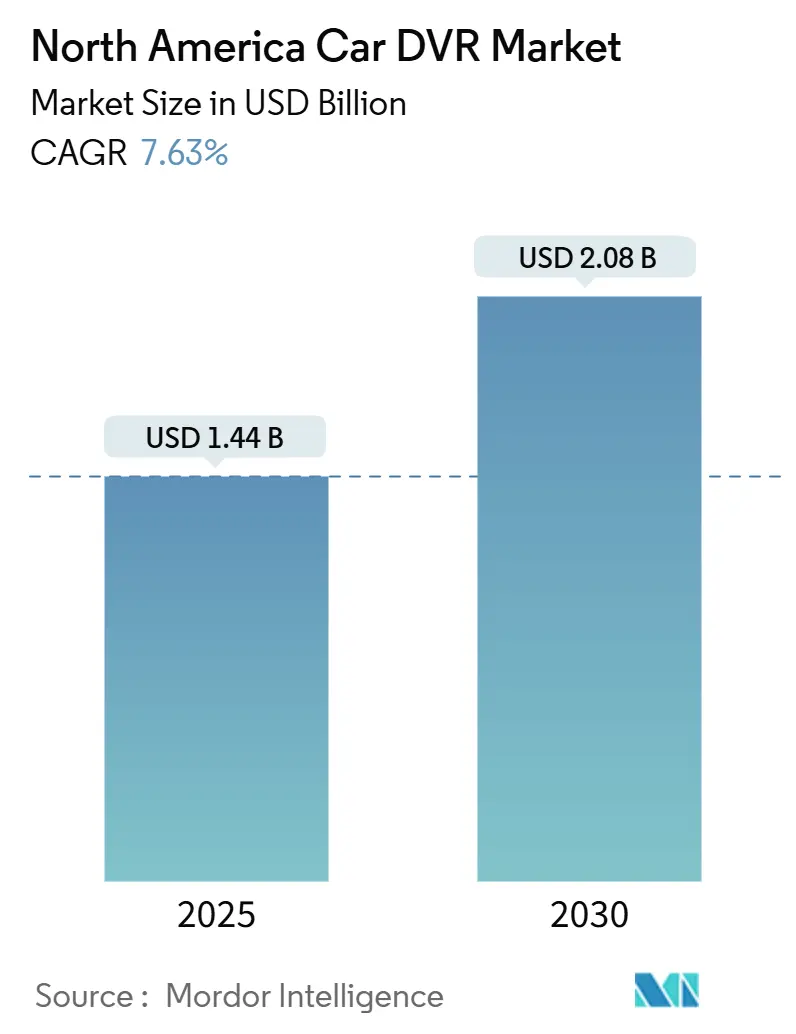

| Market Size (2025) | USD 1.44 Billion |

| Market Size (2030) | USD 2.08 Billion |

| Growth Rate (2025 - 2030) | 7.63% CAGR |

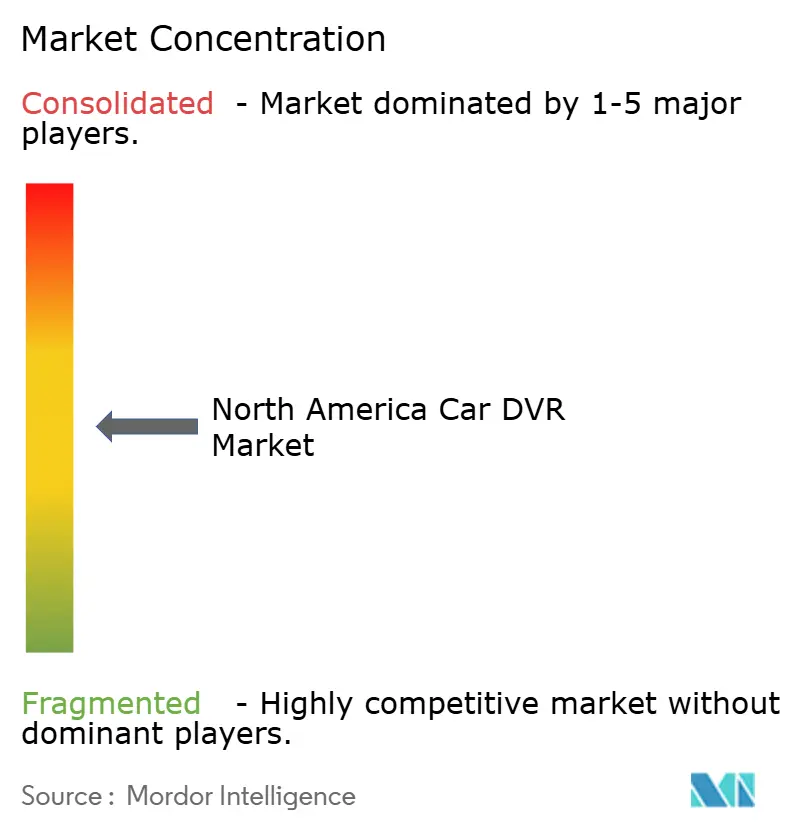

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Car DVR Market Analysis by Mordor Intelligence

The North America car DVR market size stands at USD 1.44 billion in 2025 and is estimated to expand to USD 2.08 billion by 2030, translating into a 7.63% CAGR during the forecast window. Rising state-level camera mandates, insurer subsidies, and the integration of artificial-intelligence video analytics are propelling adoption among both consumers and fleets. Commercial operators are fast-tracking deployments after the Federal Motor Carrier Safety Administration accepted dash-cam footage for every crash category, enabling direct reductions in claims and Compliance, Safety, Accountability (CSA) scores. Insurers such as Progressive pay a USD 20 monthly stipend for telematics-equipped vehicles, showing how underwriting is morphing into a data-driven model anchored in visual evidence. Semiconductor constraints still elevate component costs, yet they also spur vertically integrated suppliers to lock in long-term chip allocations. Software-first competitors leverage AI dashboards and cloud subscriptions to differentiate in a hardware-commoditized arena while privacy litigation in California and Illinois pushes buyers toward vendors with robust redaction and consent frameworks.

Key Report Takeaways

- By product type, single-channel systems led with a 48.18% share of the North America car DVR market in 2024. 360-degree surround-view units are forecast to post the highest CAGR of 5.14% through 2030.

- By vehicle type, passenger cars accounted for 68.37% share of the North America car DVR market size in 2024. Heavy commercial vehicles are projected to grow at a 5.62% CAGR between 2025-2030.

- By sales channel, the aftermarket accounted for 71.61% of revenue in 2024, whereas OEM-installed solutions are projected to advance at a 6.12% CAGR through 2030.

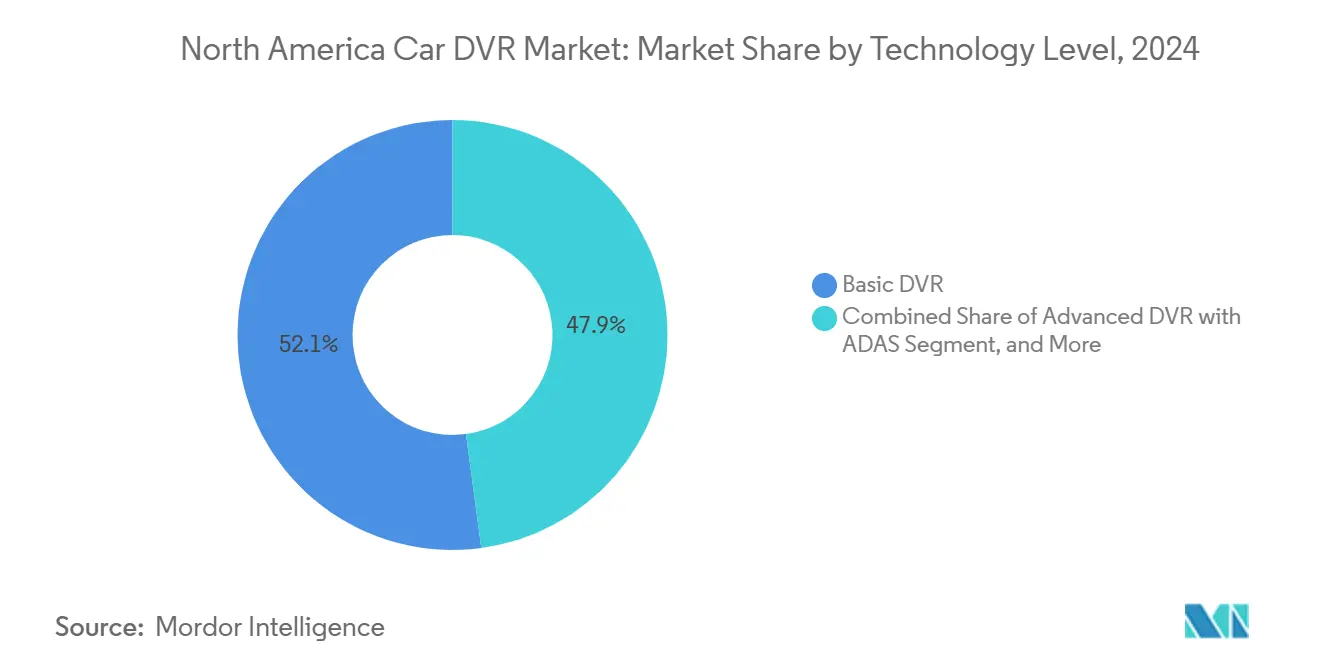

- By technology level, basic DVRs are still expected to hold a 52.14% share in 2024, and smart connected DVR systems are anticipated to register a 6.74% CAGR through 2030.

- By geography, the United States contributed 82.51% of the revenue in 2024, while Mexico is expected to record a 6.21% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on car dvr market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Car DVR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising road-safety awareness and accident rates | +1.8% | Urban corridors across North America | Medium term (2-4 years) |

| Insurance premium discounts for dash-cam equipped vehicles | +2.1% | United States, Canada | Short term (≤2 years) |

| Growing adoption in commercial fleets for driver accountability | +1.5% | Cross-border logistics routes | Long term (≥4 years) |

| OEM infotainment integration unlocking built-in DVRs | +1.2% | U.S. and Canadian assembly hubs | Medium term (2-4 years) |

| AI-driven video analytics monetization with map providers | +0.9% | Tech hubs across North America | Long term (≥4 years) |

| State-level mandates for rideshare in-cab cameras | +0.8% | Select U.S. states | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Road-Safety Awareness and Accident Rates

The FMCSA’s 2024 policy revision elevated dash cameras from optional add-ons to core fleet assets, as video can now overturn crash liability findings, directly improving safety scores and insurance outcomes. Large operators such as Fox Brothers dedicated more than USD 0.5 million to AI dash-cam rollouts as legal defense and duty-of-care measures. The National Transportation Safety Board’s 2024 call for mandatory driver-monitoring systems for passenger vehicles further mainstreamed in-cab cameras.[1]National Transportation Safety Board, “71828,” NTSB, ntsb.gov Insurance datasets show premium cuts of up to 30% for telematics-equipped fleets, solidifying the return-on-investment argument. Collectively, these factors convert safety awareness into quantifiable economic gains that amplify demand across the North America car DVR market.

Insurance Premium Discounts for Dash-Cam Equipped Vehicles

Progressive’s USD 20 per-vehicle monthly credit typifies the shift toward behavior-based pricing, where insurers directly subsidize hardware to harvest risk data. Eighty-two percent of carriers reportedly pull telematics feeds for underwriting, versus 65% only a few years earlier, confirming rapid normalization of video evidence in claims assessment. Nextbase’s U.K. program delivers average annual savings of USD 143 to motorists, offering a template now migrating into North America. Commercial policies increasingly stipulate camera installation as a coverage prerequisite, twisting a once elective upgrade into a compliance mandate that accelerates North America car DVR market penetration.

Growing Adoption in Commercial Fleets for Driver Accountability

AI-enabled cameras from Lytx and Samsara provide real-time driver coaching and auto-tagged incident clips, enabling managers to curb unsafe behavior while reducing litigation exposure. Integration with electronic logging devices satisfies FMCSA hours-of-service rules, bundling compliance features into a single hardware stack. Smartphone-based systems entering the fleet segment offer lower entry costs for small operators; however, privacy settings must adapt to state-specific audio regulations. Over the forecast horizon, cross-border haulers investing in multi-view, AI-rich setups will be notable contributors to the growth of the North America car DVR market.

OEM Infotainment Integration Unlocking Built-In DVRs

General Motors’ OnStar DualCam and Ford Pro’s Lytx-powered packages integrate recording capabilities into factory screens and sensors, eliminating the need for aftermarket wiring while opening up subscription revenue streams. Rostra’s RearSight retrofit kit demonstrates how suppliers can integrate cameras into existing display units without requiring dashboard redesign. Federal rules mandating forward-collision warnings by 2029 encourage OEMs to integrate dash-cam modules with advanced driver-assistance systems, allowing common processing units to cut incremental costs. These trends pull OEMs deeper into the North America car DVR market as integrated features shift from luxury upgrades to mainstream equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and surveillance litigation risks | -1.4% | All-party consent U.S. states | Short term (≤2 years) |

| Upfront cost of multi-channel 4K systems | -0.9% | Price-sensitive segments across North America | Medium term (2-4 years) |

| 12-volt battery drain in cold-weather fleet installations | -0.6% | Canada and northern U.S. markets | Long term (≥4 years) |

| Fragmented cloud storage chain-of-custody standards | -0.5% | Compliance-focused operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Surveillance Litigation Risks

Multiple states require every party in a vehicle to consent to audio capture, exposing fleets to fines of up to USD 5,000 per infraction under Illinois law.[2]Mark Schedler, “Dash-cam state laws: 4 areas to avoid legal pitfalls,” J. J. Keller Compliance Network, jjkellercompliancenetwork.com The resulting patchwork forces large carriers to maintain state-specific recording modes, thereby inflating configuration costs and necessitating additional legal reviews. Funding for privacy-centric startups, such as Pimloc, underlines growing customer anxiety and spurs the adoption of automatic face and license plate blurring technology. Litigation exposure, therefore, tempers but does not derail growth expectations inside the North America car DVR market.

Upfront Cost of Multi-Channel 4K Systems

Professional-grade 4K rigs equipped with AI chips can exceed USD 2,000 per vehicle. Ongoing semiconductor shocks after Taiwan’s supply interruptions continue to elevate image-sensor costs, delaying fleet refresh cycles. Smaller carriers thus stagger purchases or opt for single-channel devices until prices normalize, muting near-term demand for premium SKUs across the North America car DVR market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single-Channel Dominance Faces Multi-View Challenge

Single-channel units led the North America car DVR market in 2024, accounting for a 48.18% share, due to their low price points and ease of windshield installation. Growth, however, is tilting toward 360-degree platforms, which are forecast to outpace the market at a 5.14% CAGR through 2030 as fleets seek comprehensive coverage evidence. Mid-tier dual-channel devices win adopters who want rear views without the wiring burden of four-camera kits. Cabin-view cameras further expand in ride-hail and school transportation, where in-cabin monitoring assists with passenger dispute resolution.

The segment’s competitive field highlights a pivot to 4K sensors and AI copilots. VUEROID’s S1 Infinite, unveiled at CES 2025, illustrates how high-resolution footage supports machine-learning lane detection and driver scoring. Patent filings on fluid-filled housings to dissipate heat suggest a hardware evolution that guarantees durability in heavy-duty settings. As litigation costs rise, fleet managers value broader views over pure capex savings, securing future runway for multi-channel systems inside the North America car DVR market.

By Vehicle Type: Commercial Fleets Drive Premium Adoption

Passenger cars accounted for 68.37% of the North America car DVR market share in 2024, primarily due to insurance credits and increased consumer awareness of safety. Heavy commercial vehicles are set to log the steepest 5.62% CAGR, with cross-border trucking firms upgrading to AI-enabled multi-view rigs that reduce liability and meet customer service SLAs. Light commercial vans ride the e-commerce boom, prompting last-mile operators to blend route optimization with driver coaching via integrated DVR-telematics stacks.

Funding momentum at Driver Technologies, which has secured USD 16.3 million for an AI-powered mobile dash-cam app, underscores the converging needs of users across both personal and professional vehicles. For fleet buyers, direct insurance savings and CSA score gains outweigh higher unit costs, making the commercial cohort the principal catalyst for premium offerings in the North America car DVR market.

By Sales Channel: Aftermarket Leadership Under OEM Pressure

Aftermarket outlets captured 71.61% of the revenue in 2024, as do-it-yourself kits and retail chains supplied fast, low-commitment upgrades. OEM programs are nonetheless climbing at a 6.12% CAGR because factory-embedded cameras piggyback on existing infotainment screens and cloud contracts. Dealers can preload subscriptions to video analytics, building recurring revenue streams that chip away at the aftermarket’s historical edge.

Ford Pro’s expanded Lytx integration and GM’s DualCam package verify automakers’ strategy to lock in customers through bundled telematics, a move that intensifies competition within the North America car DVR market. Aftermarket players counter with short refresh cycles and multi-price tiers, keeping lead times short and the innovation pipeline agile.

By Technology Level: AI Integration Drives Premium Growth

Basic DVRs still hold 52.14% share, targeting budget-focused owners who only need passive recording. Smart connected models, projected at a 6.74% CAGR, combine LTE uplinks, cloud clipping, and AI risk scores, pressing fleets to shift from reactive to predictive safety management. Advanced DVRs layer ADAS alerts on top of learning algorithms, edging the market toward integrated driver-assistance ecosystems.

Samsara’s USD 400 million annual recurring revenue from video safety validates the payback of subscription platforms that pair hardware and analytics. Patent filings for birds-eye-view object models illustrate the drive toward richer situational awareness in a single dashboard. This AI trajectory underpins the competitive moat for premium tiers in the North America car DVR market.

By Video Quality: 4K Adoption Accelerates Despite Full HD Dominance

Full-HD 1080p devices kept 2024’s volume lead, thanks to an optimal balance of clarity and file size. Yet 4K units are forecast to climb at 7.01% CAGR because insurers and courts increasingly require evidence-grade detail, particularly for night incidents. New image sensors from onsemi improve low-light capture at lower power draw, mitigating historical objections on storage and heat.

Product launches like DDPAI’s N5 dual radar dash-cam furthers the blend of high-resolution video with radar cues that feed AI predictors. While cost barriers persist, legal demands continually nudge professional fleets toward ultra-high-definition options inside the North America car DVR market.

Geography Analysis

The United States commanded 82.51% of 2024 revenue, reflecting mature insurance telematics programs, federal fleet mandates, and state-level rideshare in-cab rules. Progressive’s USD 20 monthly subsidy and FMCSA’s open acceptance of dash-cam evidence reshape ROI calculations for both passenger and freight operators. Privacy statutes in California and Illinois complicate cabin audio, yet vendors with auto-redaction and consent workflows still scale quickly.

Canada’s market adopts U.S. norms, with British Columbia weighing compulsory truck cameras after pilot trials. Extreme winter conditions push fleets toward hard-wired, heated rigs, boosting demand for advanced power-management features. Cross-border carriers harmonize equipment across NAFTA corridors, sustaining a consistent baseline for North America car DVR market standards.

Mexico is projected at a 6.21% CAGR to 2030, buoyed by rising manufacturing investment and cross-border freight flows that demand telematics parity with U.S. partners. As logistic firms extend just-in-time deliveries, dashboards with AI alerts counter security threats on long haul routes. Local insurers replicating U.S. telematics rebates further speed acceptance, ensuring Mexico’s role as the fastest-growing geography within the North America car DVR market.

Competitive Landscape

Hardware stalwarts Garmin, Nextbase, and BlackVue still dominate retail shelves, yet subscription-centric fleets gravitate toward Samsara and Lytx, whose AI stacks automate event detection and driver scoring. SureCam’s USD 36 million Series B raise signals investor appetite for mid-market fleet solutions that promise easy installation and simplified coaching workflows.[3]SureCam, “SureCam Secures $36M Fueled by Demand for Simplified AI Fleet Safety,” surecam.com Patent paths on thermal-dissipating camera modules and GPU multi-feed processors demonstrate continuing hardware refinements that support software differentiation.

Start-ups like Pimloc address privacy head-on with Secure Redact AI, enabling blur-on-demand features that appeal to compliance-heavy jurisdictions. Driver Technologies expands beyond mobile to Android Automotive OS, proving software portability across devices.

The net effect is a moderately fragmented arena where competitive edge comes less from lenses and more from cloud analytics, open APIs, and compliance toolkits, all essential to thriving in the North America car DVR market.

North America Car DVR Industry Leaders

Garmin Ltd.

Nextbase Group Ltd.

Pittasoft Co., Ltd. (BlackVue)

Thinkware Corporation

Cobra Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Driver Technologies launched an Android Automotive in-dash application enabling factory-embedded dash-cam functions.

- June 2025: Pimloc secured USD 5 million to scale its Secure Redact AI privacy platform for dash-cam video.

- January 2025: SureCam raised USD 36 million to accelerate North American fleet expansion with AI dash-cam coaching.

- January 2025: VUEROID introduced the S1 Infinite 4K AI dash-cam at CES 2025, targeting consumer and fleet audiences.

North America Car DVR Market Report Scope

| Single-Channel (Front) |

| Dual-Channel (Front + Rear) |

| 360° Surround-View Systems |

| Triple-Channel / Cabin-View |

| Rear-View-Only Dash Camera |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Aftermarket |

| OEM-Installed |

| Basic DVR |

| Advanced DVR with ADAS |

| Smart Connected DVR (AI/Cloud) |

| SD / HD (≤720p) |

| Full HD (1080p) |

| 4K and Above |

| North America | United States |

| Canada | |

| Mexico |

| By Product Type | Single-Channel (Front) | |

| Dual-Channel (Front + Rear) | ||

| 360° Surround-View Systems | ||

| Triple-Channel / Cabin-View | ||

| Rear-View-Only Dash Camera | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| By Sales Channel | Aftermarket | |

| OEM-Installed | ||

| By Technology Level | Basic DVR | |

| Advanced DVR with ADAS | ||

| Smart Connected DVR (AI/Cloud) | ||

| By Video Quality | SD / HD (≤720p) | |

| Full HD (1080p) | ||

| 4K and Above | ||

| By Country | North America | United States |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America Car DVR market in 2025?

The market is valued at USD 1.44 billion in 2025 and is forecast to reach USD 2.08 billion by 2030 on a 7.63% CAGR.

Which product type leads current sales?

Single-channel front-facing dashboards account for 48.18% of all 2024 revenue.

Which vehicle segment is growing the fastest?

Heavy commercial trucks are projected to register a 5.62% CAGR through 2030 as fleets prioritize multi-view AI systems.

Why are insurers subsidizing dash-cam installations?

Carriers like Progressive pay monthly incentives because video evidence lowers claims costs and improves risk scoring.

What compliance trend most affects demand?

FMCSA’s acceptance of dash-cam footage for all crash preventability reviews has turned cameras into essential compliance assets.

Page last updated on: