Canada Pension Funds Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

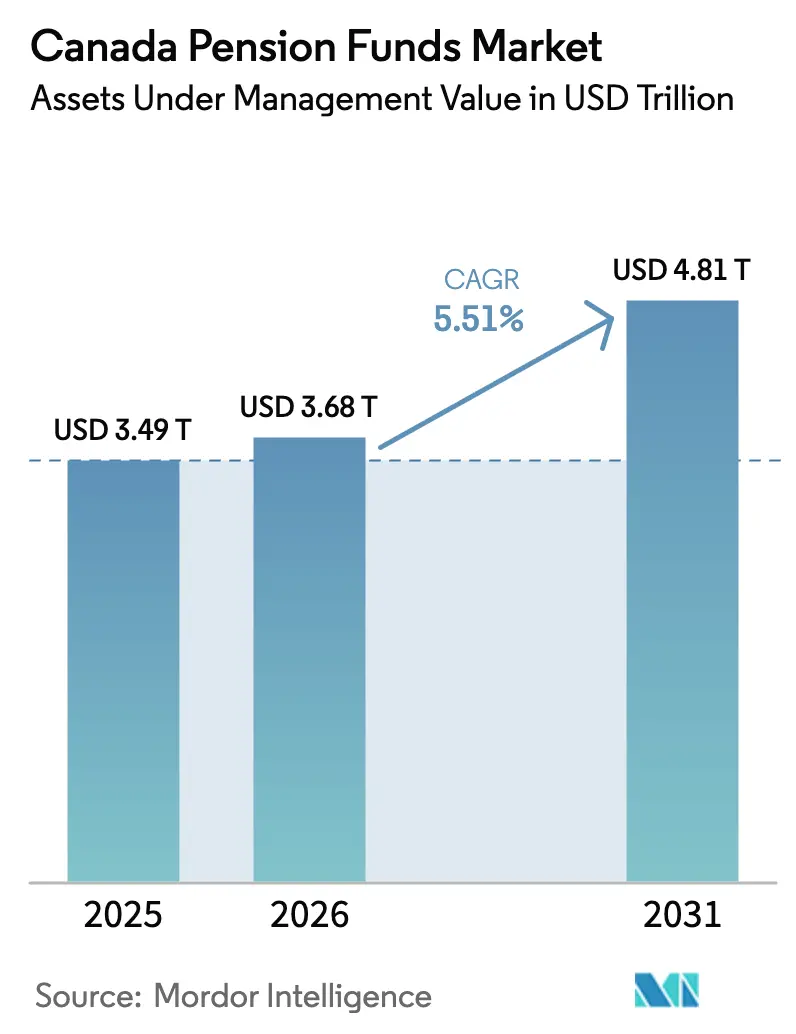

| Base Year Market Size (2025) | USD 3.49 Trillion |

| Market Size (2026) | USD 3.68 Trillion |

| Market Size (2031) | USD 4.81 Trillion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

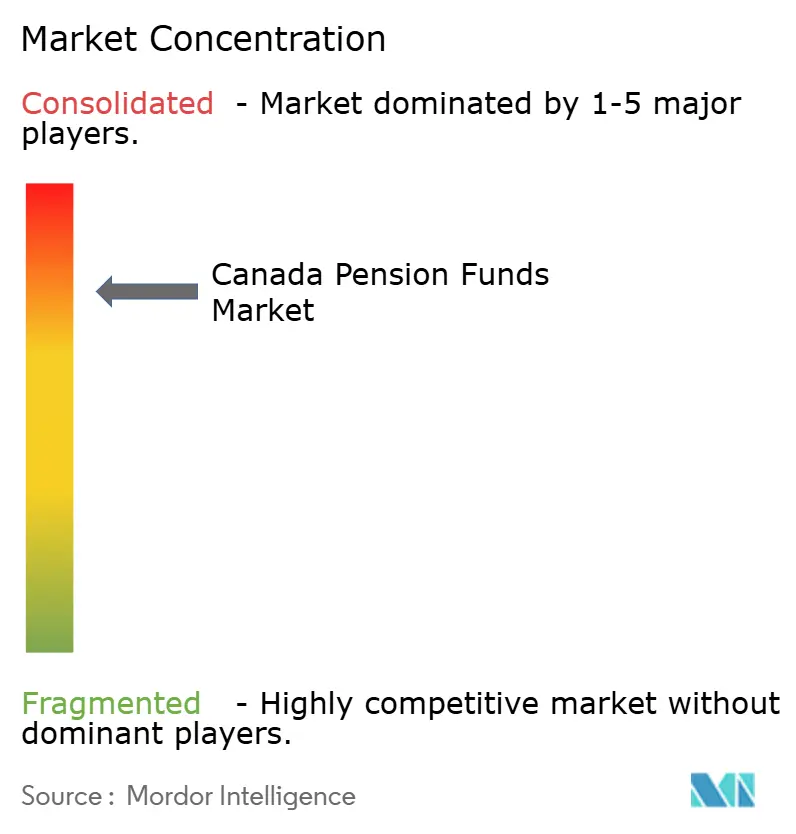

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Pension Funds Market Analysis by Mordor Intelligence

Canada pension funds market size in 2026 is estimated at USD 3.68 trillion, growing from 2025 value of USD 3.49 trillion with 2031 projections showing USD 4.81 trillion, growing at 5.51% CAGR over 2026-2031. Demand for capital-light retirement products, rapid technology adoption, and growing allocations to alternative assets underpin this expansion. Public-sector plans still dominate the Canada pension fund market, yet private-sector sponsors record faster growth as employers migrate to defined-contribution arrangements. Offshore diversification continues to reshape portfolio construction, while the eight largest public plans—the “Maple Eight”—reinforce their global reputation for in-house active management excellence. Persistent demographic pressure, property market write-downs, and liquidity shocks temper the outlook but also accelerate strategic pivots toward infrastructure, renewable energy, and cross-border pension-risk-transfer transactions.

Key Report Takeaways

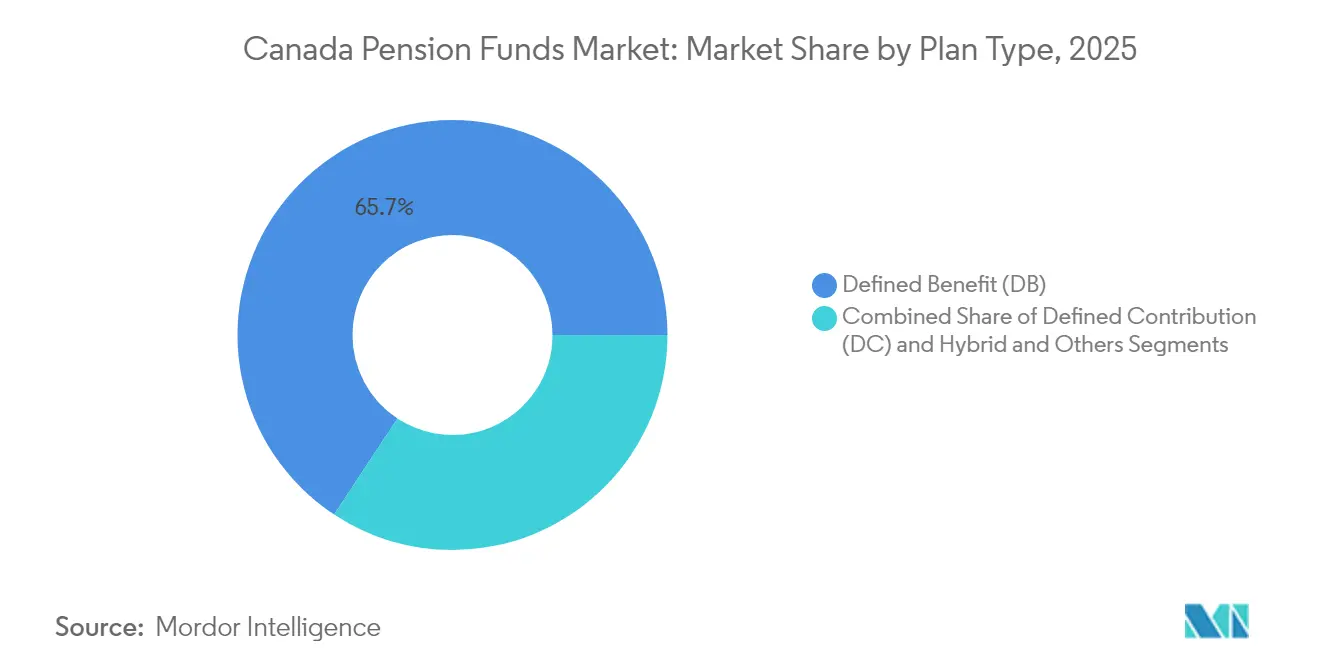

- By plan type, defined benefit schemes held 65.72% of the Canada pension funds market share in 2025, whereas defined contribution plans are expanding at a 6.85% CAGR through 2031.

- By investment strategy, active management retained 62.15% share of the Canada pension funds market size in 2025; passive mandates post the highest projected CAGR of 6.41% to 2031.

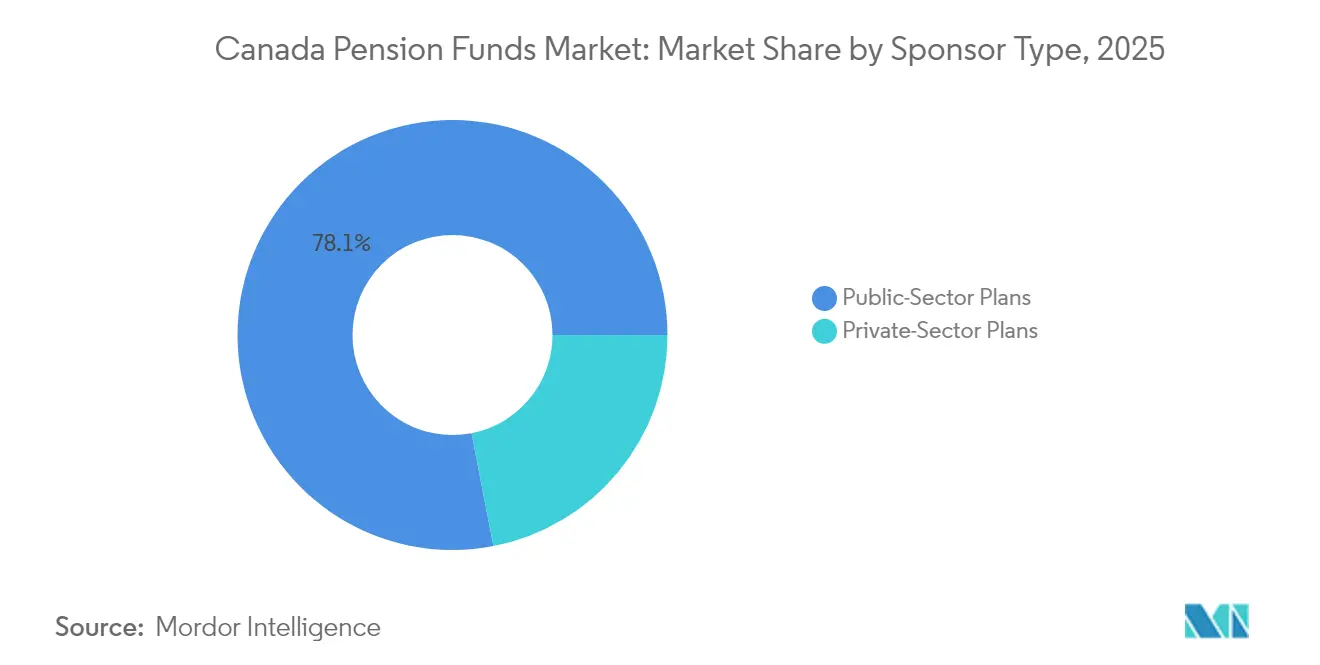

- By sponsor type, public-sector plans commanded 78.05% revenue share of the Canada pension funds market in 2025, while private-sector plans are expected to exhibit the quickest growth at 7.32% CAGR.

- By geography of investment, offshore assets represented 57.05% of Canada's pension funds market allocations in 2025 and are projected to grow at a 6.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Pension Funds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing shift to capital-light retirement products | +1.2% | Global, with early gains in Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Technology-driven member engagement platforms | +0.8% | National, concentrated in major urban centers | Short term (≤ 2 years) |

| Rapid expansion of alternative investments in portfolios | +1.5% | Global, with APAC and North America focus | Long term (≥ 4 years) |

| In-house asset-management cost advantage of “Maple Eight” | +0.9% | National, with spillover to international markets | Long term (≥ 4 years) |

| Climate-aligned infrastructure programs opened by federal government | +1.1% | National, concentrated in renewable-energy corridors | Medium term (2-4 years) |

| Cross-border buy-out deals of closed UK/US DB plans | +0.7% | International, focused on UK and US markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Shift to Capital-Light Retirement Products

Employers continue to exit guaranteed benefit structures, pushing the pension-risk-transfer market toward CAD 10 billion in 2024. Defined contribution plans appeal to organizations looking to curb balance-sheet volatility and streamline compliance expenditures. Insurers meet demand with innovative bulk-annuity offerings that absorb longevity and investment risk, broadening access to mid-market sponsors. Sun Life reports a steady rise in buy-ins as companies view liability transfer as proactive balance-sheet management rather than a last resort. The result is faster asset growth for DC mandates within the Canada pension fund market and improved capital efficiency for corporate Canada.

Technology-Driven Member Engagement Platforms

Artificial-intelligence engines now curate personalized dashboards that guide contribution rates, asset allocation, and retirement income projections [1]CFA Institute, “AI in Public-Sector Pension Funds,” cfainstitute.org. CAAT Pension Plan’s cloud migration with DXC and ServiceNow shows how digital workflows can scale to 100,000+ participants while cutting administrative overhead. Predictive analytics refine actuarial assumptions, helping trustees calibrate contribution schedules. Yet regulators urge vigilance on data privacy and algorithmic bias. Successful adopters therefore balance innovation, cybersecurity, and fiduciary accountability—elements that sharpen competitive positioning in the Canada pension fund market.

Rapid Expansion of Alternative Investments in Portfolios

Infrastructure, private equity, and venture capital now absorb growing slices of aggregate assets as conventional public-market yields remain compressed. CDPQ’s Verene Energia acquisition of a 124-kilometer Brazilian transmission asset illustrates the search for long-duration, inflation-protected cash flows. PSP Investments and KKR’s purchase of American Electric Power’s transmission units highlights the scale advantage Canadian funds wield in competitive auctions [2]Charles Émond, “CDPQ 2024 Sustainable Investing Progress Update,” cdpq.com. Alternative allocations defend funded status against demographic strain and heighten the appeal of the Canada pension fund market to global project sponsors seeking sovereign-grade co-investors.

In-House Asset-Management Cost Advantage of “Maple Eight”

CPPIB generated CAD 16 billion in excess value over five years, even after incurring CAD 5.5 billion in annual operating costs on an asset base of CAD 714.4 billion. Internal teams negotiate lower deal fees, retain proprietary expertise, and accelerate decision cycles. International observers increasingly benchmark against this model, but its upkeep demands relentless talent recruitment and high-performance data architecture. For smaller plans, partnering with or merging into larger peers offers a path to similar economics, intensifying consolidation themes within the Canada pension fund market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market volatility and liquidity shocks | -1.8% | Global, with concentrated exposure in emerging markets | Short term (≤ 2 years) |

| Adverse demographic dependency ratio | -2.1% | National, with acute pressure in Atlantic provinces | Long term (≥ 4 years) |

| Greater solvency-funding disclosure requirements | -0.6% | National, affecting federally regulated plans | Medium term (2-4 years) |

| Office-real-estate write-downs pressuring returns | -1.3% | Global, concentrated in major metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Market Volatility and Liquidity Shocks

Geopolitical friction drives CPPIB to pare emerging-market exposure from 22% to 20% and lift US holdings from 36% to 42% by March 2024. Such defensive tilts cushion short-term downside but concentrate assets in crowded trades, compressing future return potential. Liquidity protocols now incorporate stress testing for sudden collateral calls linked to private-credit drawdowns or secondary-market freezes. Boards monitor these dynamics closely, knowing that sustained shocks could derail performance targets for the Canada pension fund market.

Adverse Demographic Dependency Ratio

The support ratio slide toward 59% by 2027, threatening to inflate provincial healthcare liabilities to CAD 2 trillion and eat into fiscal room for pension top-ups. Higher contributions or trimmed benefits loom, especially in Atlantic regions facing steep out-migration. Ottawa eyes targeted immigration to replenish the workforce, but accelerated population growth strains housing and public services. These demographic forces weigh heavily on actuarial projections and long-range asset-liability models throughout the Canada pension fund market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plan Type: Defined Benefit Resilience amid DC Acceleration

Defined benefit assets accounted for 65.72% of the Canada pension funds market size in 2025, as decades of compounded contributions locked in a formidable capital base. High-profile sponsors such as CPPIB and CDPQ continue to leverage scale for negotiated deal access, cushioning the impact of funding volatility. Still, defined contribution pools clock a 6.85% CAGR to 2031 as employers embrace risk transfer strategies and younger workers prioritize portability. The Canada pension fund market now balances mature DB liabilities against a fresh influx of DC cash flows, shifting service-provider economics and sparking product innovation.

DC momentum is reinforced by capital-light accounting treatment and lower regulatory burden. Hybrid designs that splice DB guarantees with DC flexibility gain niche appeal among industries with cyclical earnings. Consultants increasingly recommend lifecycle and target-date solutions to streamline asset choices for participants. As DC balances rise, passive index funds absorb greater inflows, creating competitive tension between low-cost structures and the Maple Eight’s high-touch active approach.

By Investment Strategy: Active Management under Pressure

Active mandates controlled 62.15% of the Canada pension funds market in 2025, yet fee-aware sponsors are steering incremental cash to passive vehicles at a 6.41% CAGR through 2031. Smaller plans often lack the scale to justify bespoke private-market teams and therefore gravitate toward indexed building blocks. Conversely, the Maple Eight keep internal deal pipelines humming, defending their alpha narrative by highlighting five-year outperformance versus blended benchmarks.

Technology dissolves rigid style boundaries: smart-beta ETFs fold factor tilts into passive wrappers, while quantitative managers automate research that once required armies of analysts. These cross-currents reshape talent requirements and drive cooperative platforms where large funds share data lakes or AI engines to cut duplicative spend. Regulatory focus on value-for-money reporting amplifies scrutiny, nudging trustees to articulate clear performance thresholds for retaining active strategies within the Canada pension fund market.

By Sponsor Type: Public-Sector Strength versus Private-Sector Growth

Public plans, anchored by statutory contribution inflows and sovereign backing, represented 78.05% of total assets in 2025. Their expansive time horizons support multidecade infrastructure bets and patient capital alliances that private peers rarely match. Nonetheless, private-sector plans notch the swiftest expansion at 7.32% CAGR as SMEs adopt group RRSPs and capital-accumulation platforms to compete for talent.

Policy tweaks that simplify governance and permit broader investment menus lower entry barriers for mid-market employers. Insurance-company record-keepers seize the opportunity, bundling education, wellness, and robo-advice features that resonate with digitally savvy employees. Together, these trends broaden the stakeholder base for the Canada pension fund market and diversify cash-inflow sources beyond the public sphere.

By Geography of Investment: Offshore Dominance Drives Returns

Foreign holdings made up 57.05% of portfolios in 2025 and are projected to expand at a 6.05% CAGR to 2031. The Canada pension funds market benefits from APAC infrastructure pipelines, European logistics, and US data-center builds that offer scalable, inflation-linked cash flows. CPPIB now allocates roughly 90% of its assets outside Canada to mitigate domestic commodity-cycle volatility.

Onshore deployments still appeal where government co-investment de-risks early-stage climate ventures. Ottawa’s removal of the 30% rule and new transparency standards aim to entice greater domestic capital without constraining funds’ fiduciary latitude. Trustees, therefore, weigh political optics against risk-return calculus, refining portfolio-mix triggers that guide home-bias adjustments across the Canada pension fund market.

Geography Analysis

Offshore allocations held 57.05% share of aggregate assets in 2025 and remain the fastest-growing slice of the Canada pension fund market. Asia-Pacific absorbs a rising proportion, led by Australia, which captures over half of regional inflows. India overtakes China at 25% of APAC exposure as funds seek regulatory stability and demographic vibrancy . Heightened geopolitical tension prompts trimming of Chinese equities, while resilient rule-of-law jurisdictions attract incremental capital.

North America still anchors overall exposure. CPPIB lifted its US weighting from 36% to 42% by March 2024, favoring energy infrastructure, digital-utility platforms, and high-grade real estate. PSP’s CAD 300 million hospitality partnership with Eurazeo amplifies European diversification and taps post-pandemic travel recovery tailwinds. European green-field renewables and mature toll-road concessions also draw Canadian bids, underscoring the global reach of the Canada pension fund market.

Domestic investments remain substantial but face opportunity-cost scrutiny. Federal authorities encourage “buy Canada” alignment through matched-funding for clean-tech ventures and advanced manufacturing corridors. The Maple Eight responds selectively, prioritizing climate-aligned infrastructure, digital backbone assets, and affordable housing that match liability timelines. While political stakeholders press for deeper home-market engagement, portfolio managers emphasize that fiduciary duty mandates globally optimized, risk-adjusted returns.

Competitive Landscape

Canada’s pension ecosystem is concentrated, with the Maple Eight controlling a significant share of the assets. CPPIB leads at CAD 714.4 billion, followed by CDPQ at CAD 473 billion and OTPP at CAD 247.5 billion. Each pursues distinct mandates: CPPIB maximizes long-term returns for contributors and beneficiaries nationwide; CDPQ balances returns with Quebec economic development; OTPP tailors to Ontario educators. Their heft assures seat-at-table status in multi-billion-dollar global deals, giving the Canada pension fund market a disproportionate presence in cross-border transactions.

Active direct-investment models, bolstered by data science and AI tools, remain central to competitive strategy. CPPIB’s North American energy purchase of California Resources Corporation stock through the Aera Energy merger demonstrates ambition to scale traditional energy alongside transition-ready assets. PSP’s entry into Highway 407 ETR signals rising domestic-infrastructure appetite as valuations stabilize. CDPQ’s private takeover of fintech Nuvei, where it retains a 12% stake post-LBO, advances the fund’s digital-economy thesis.

Smaller provincial plans weigh collaboration or consolidation to unlock comparable scale efficiencies. Shared-service models and pooled-asset vehicles help reduce fee drag and broaden alternative-asset access. Regulatory transparency mandates raise the bar on cost disclosure, nudging underperforming outfits to benchmark against Maple Eight results. Technology investment, talent recruitment, and climate-risk integration form the next arena of competitive differentiation across the Canada pension fund market.

Canada Pension Funds Industry Leaders

Canada Pension Plan Investment Board (CPPIB)

Caisse de dépôt et placement du Québec (CDPQ)

Ontario Teachers’ Pension Plan (OTPP)

Public Sector Pension Investment Board (PSP Investments)

Healthcare of Ontario Pension Plan (HOOPP)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CPPIB announced its intention to acquire common stock in California Resources Corporation through the Aera Energy merger.

- March 2025: PSP Investments joined CPPIB and Ferrovial in the ownership group of Highway 407 ETR, marking PSP’s largest Canadian infrastructure investment.

- February 2025: CDPQ completed the sale of 2.5 million common shares of Intact Financial Corporation, generating liquidity for new opportunities.

- January 2025: PSP Investments and Eurazeo formed a dedicated joint venture for European hospitality investments with initial capital of €300 million.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canadian pension fund market as the combined assets under management of registered defined-benefit, defined-contribution, and hybrid employment pension plans that pool contributions and invest across capital markets to generate retirement income for members. Values are reported in U.S. dollars and capture both on-shore and internationally deployed assets held by public-sector and private-sector sponsors.

Scope exclusion: Group RRSPs, individual retirement savings accounts, and non-regulated wealth products are not counted.

Segmentation Overview

- By Plan Type

- Defined Contribution (DC)

- Defined Benefit (DB)

- Hybrid and Others

- By Investment Strategy

- Active

- Passive

- By Sponsor Type

- Public-Sector Plans

- Private-Sector Plans

- By Geography of Investment

- Onshore

- Offshore

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed plan administrators, provincial regulators, actuaries, and asset-consulting partners across Ontario, Quebec, Alberta, and British Columbia. These conversations clarified hidden cash-flow assumptions, liquidity buffers, and expected alternative-asset write-downs, allowing us to fine-tune model sensitivities that public data alone cannot reveal.

Desk Research

We began with Statistics Canada's quarterly trusteed-plan tables, the Office of the Chief Actuary's CPP actuarial reports, Bank of Canada monetary statistics, OECD 'Pensions at a Glance,' and guidance from the Canadian Association of Pension Supervisory Authorities. Company filings housed in D&B Hoovers and news archived in Dow Jones Factiva enriched sponsor-level insights such as asset-mix shifts, fee structures, and foreign-allocation ceilings.

Annual reports from the 'Maple Eight,' federal budget notes, and parliamentary committee transcripts helped us cross-reference contribution inflows, solvency ratios, and policy levers that materially influence asset growth.

The sources listed illustrate our approach; many other authoritative datasets were reviewed for validation and context.

Market-Sizing & Forecasting

A top-down and bottom-up construct was adopted. Total trusteed assets and CPP balances were first reconstructed from regulator filings, which are then corroborated with sampled sponsor roll-ups and average-asset-per-member checks. Key variables such as active-to-retiree ratios, statutory contribution rates, nominal GDP, five-year equity returns, real bond yields, and offshore allocation trends feed a multivariate-regression forecast through 2030, before scenario analysis adjusts for policy or liquidity shocks. Where sponsor disclosures were incomplete, interpolation used peer averages capped by statutory funding limits.

Data Validation & Update Cycle

Outputs pass variance screens against macro indicators, peer quartiles, and prior editions; anomalies prompt re-contacts. Reports refresh each year, with interim updates released when legislation, actuarial valuations, or market dislocations materially move the baseline.

Why Mordor's Canada Pension Fund Baseline Deserves Trust

Because definitions, currency translation points, and refresh cadences differ, published market values rarely align. We observe that some publishers cite only trusteed plans, others fold in retail retirement products, while a few project aggressive equity returns that inflate 2030 totals.

Key gap drivers include scope breadth, treatment of offshore assets, assumed contribution escalation, and whether sponsor-level write-downs are netted or grossed. Our disciplined inclusion criteria, annual refresh, and triangulation with primary respondent insights reduce these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.49 T (2025) | Mordor Intelligence | - |

| USD 3.49 T (2024) | Global Consultancy A | excludes small private plans; uses fixed 6 % equity return throughout forecast |

| USD 3.86 T (2024) | Research Publisher B | counts group RRSPs and PRPPs, inflating base pool |

| USD 2.50 T (2024) | Government Statistical Office C | covers only top 250 trusteed funds and reports in CAD without currency adjustment |

Taken together, the comparison shows that when scope is harmonized and inputs are stress-tested, Mordor's balanced, transparent baseline offers decision-makers the most dependable starting point for scenario planning.

Key Questions Answered in the Report

What is the current size of the Canada pension fund market?

The Canada pension fund market stands at USD 3.68 trillion in 2026 and is projected to reach USD 4.81 trillion by 2031.

Which plan type is growing fastest?

Defined contribution schemes are expanding at a 6.85% CAGR as employers seek capital-light retirement solutions.

How much of Canadian pension capital is invested abroad?

Offshore assets account for 57.05% of total allocations, with APAC and North America absorbing the bulk of new flows.

Why are Canadian funds increasing alternative investments?

Infrastructure, private equity, and renewables offer long-duration, inflation-linked returns that better match pension liabilities.

What role does technology play in member engagement?

AI-powered platforms personalize retirement planning, cut administrative costs, and enhance actuarial precision across the pension value chain.

How concentrated is the market among top players?

The five largest public plans hold a significant share of assets, giving the market a concentration score of 8.

Page last updated on: