Pension Funds Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

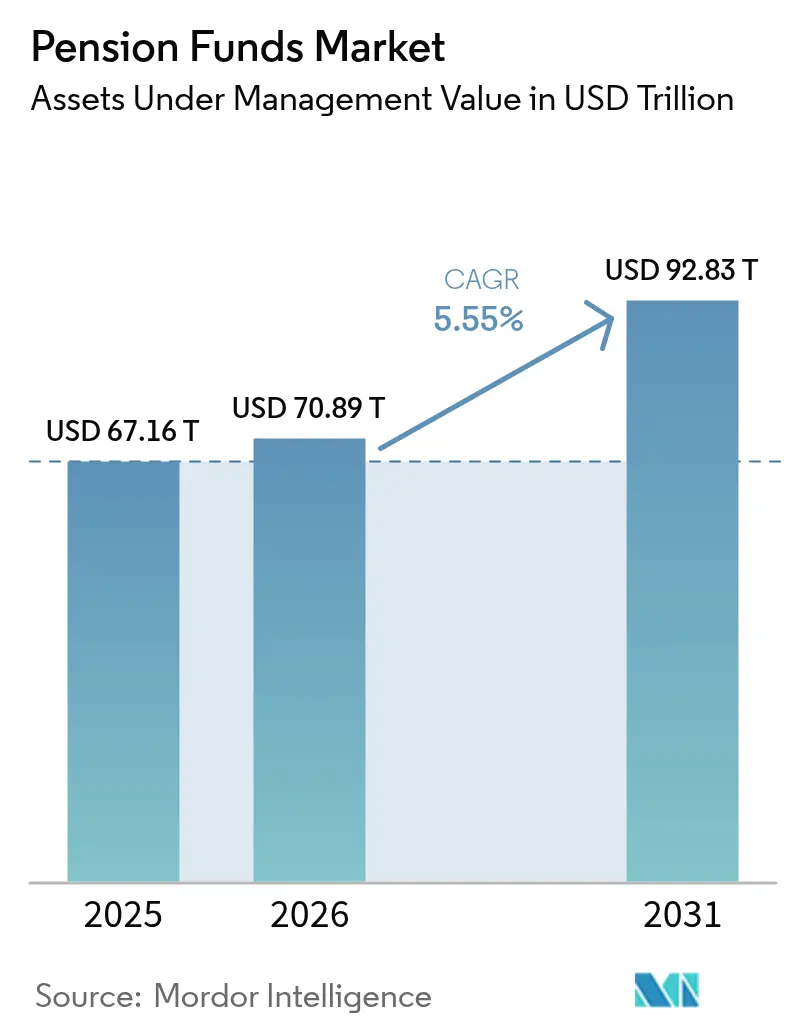

| Market Size (2026) | USD 70.89 Trillion |

| Market Size (2031) | USD 92.83 Trillion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pension Funds Market Analysis by Mordor Intelligence

Pension funds market size in 2026 is estimated at USD 70.89 trillion, growing from 2025 value of USD 67.16 trillion with 2031 projections showing USD 92.83 trillion, growing at 5.55% CAGR over 2026-2031. Gains rest on the decisive global swing from defined benefit (DB) to defined contribution (DC) plans, intensifying regulatory nudges that raise participation and contributions, and steady inflows from ageing workforces seeking secure post-retirement income. Asset-allocation patterns continue to migrate toward equities, infrastructure, and other private-market classes as funds search for yield while contending with low-rate backdrops. Meanwhile, digital tools that automate administration, enable member self-service, and lower back-office costs are allowing even mid-sized plans to replicate the scale advantages once enjoyed only by the largest sponsors. Competitive positioning is shifting from pure asset heft to a blend of cyber-secure operations, data-rich risk management, and credible climate strategies that help trustees meet fiduciary and societal expectations.

Key Report Takeaways

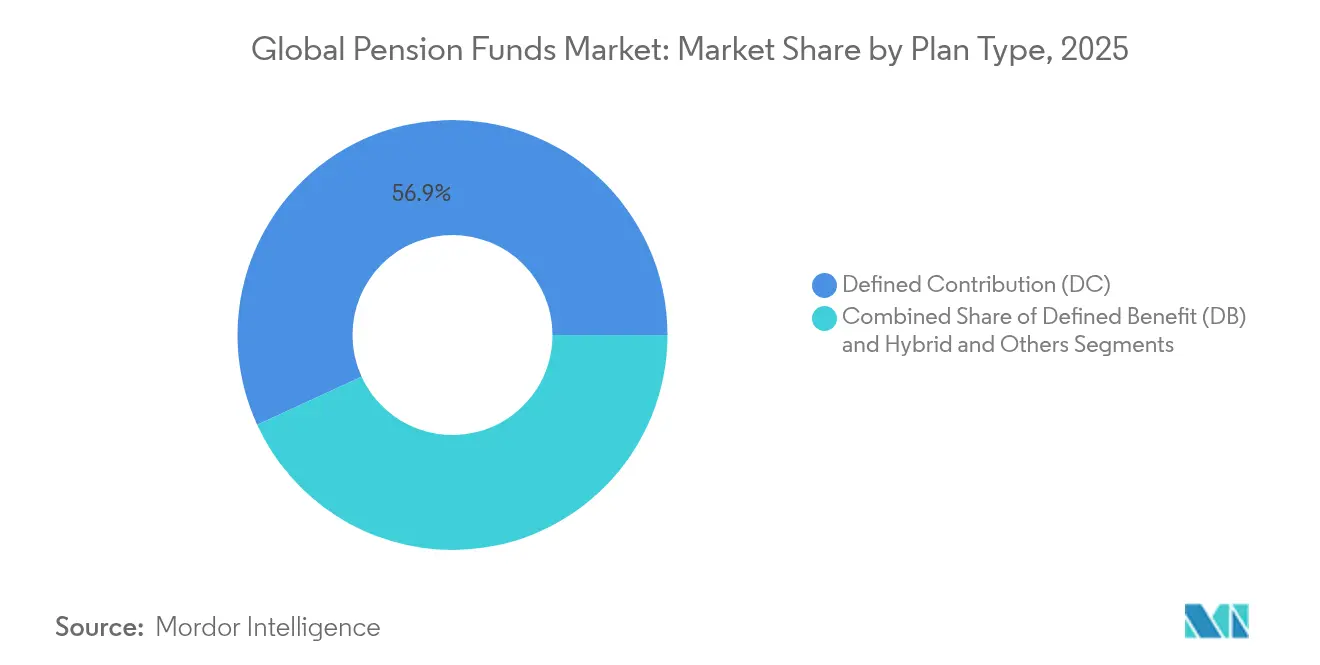

- By plan type, defined contribution schemes led with 56.85% of the global pension funds market share in 2025 and are projected to expand at a 6.32% CAGR to 2031.

- By investment strategy, active management still accounted for 54.35% share of the global pension funds market in 2025, while passive strategies are expected to record the fastest growth at 6.02% CAGR through 2031.

- By sponsor, public-sector plans held 68.75% of the global pension funds market share in 2025, but private-sector plans are projected to advance at a 6.91% CAGR of the pension funds market to 2031.

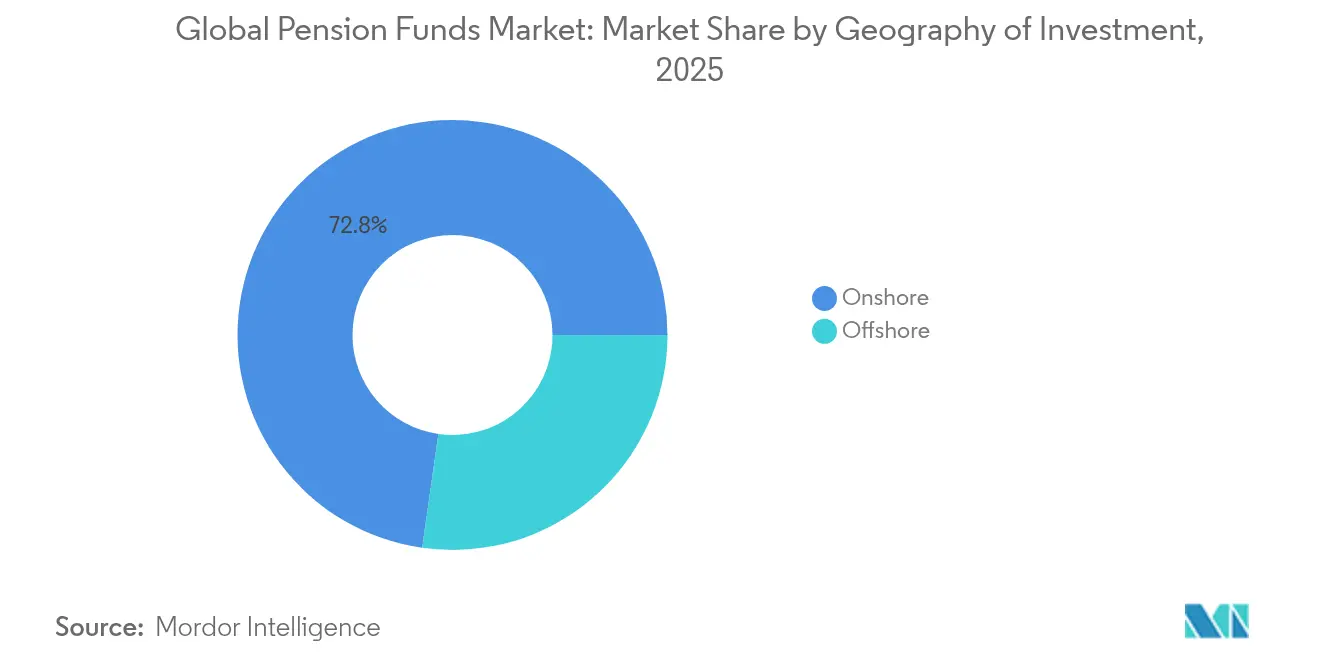

- By geography of investment, onshore assets comprised 72.75% of the global pension funds market size in 2025, yet offshore allocations are projected to grow 5.91% annually between 2026-2031.

- By region, North America commanded 70.65% of global assets of the pension funds market in 2025, whereas Asia-Pacific is forecasted to expand at a 6.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pension Funds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from DB to DC schemes | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Ageing population and longevity risk | +0.9% | Global, especially OECD economies | Long term (≥ 4 years) |

| Regulatory push for auto-enrolment | +0.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Diversification into alternative assets | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Tokenization of real assets | +0.4% | North America and Europe initially, widening globally | Long term (≥ 4 years) |

| Climate-aligned infrastructure demand | +0.6% | Global, early uptake in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift from DB to DC Schemes

Defined contribution plans already hold the majority of global pension savings, and their 6.45% growth rate underscores the systemic reallocation of investment risk from employers to employees. The United Kingdom, the Netherlands, and Germany all enacted pivotal reforms that accelerate DC take-up, compelling sponsors to modernize member portals and adopt robo-advice so individuals can manage personalized glide paths. Asset managers benefit from rising flows into target-date funds, while administrators deploy cloud processing to cut record-keeping costs and enable same-day investment of contributions. Collectively, these moves recalibrate fee structures, shorten settlement cycles, and heighten demand for real-time analytics that guide participants toward adequate retirement outcomes.

Ageing Population & Longevity Risk

Longer life expectancy lifts pension liabilities, prompting funds to recalibrate strategic asset mixes away from low-yield government bonds toward global equities, real estate, and infrastructure. Japan’s allocation pivot amplified listed-equity exposure and added nearly USD 280 billion of net gains in fiscal 2024. South Korea and China now study similar equity weightings as buffers against future benefit obligations. Longevity-linked securities, annuity buy-ins, and bespoke reinsurance solutions are rising as sponsors seek cost-effective hedges against payouts that stretch well beyond actuarial projections. These innovations spur demand for granular mortality data and analytics that can refine liability duration and hedge effectiveness.

Regulatory Push for Auto-Enrolment & Higher Contributions

Legislative packages such as the SECURE 2.0 Act in the United States introduce mandatory enrollment and escalating contribution schedules. Compliance workloads multiply, spurring uptake of specialized software that automates eligibility checks, electronic disclosures, and payroll feeds. Higher inflows also enlarge the investible pool for ESG-screened index funds and thematic private-market vehicles that align with new stewardship codes introduced across multiple jurisdictions. Providers that bundle record-keeping, financial-wellness content, and cyber-secure mobile apps stand to gain share among cost-pressured employers.

Diversification into Alternative Assets

Average pension allocations to alternatives rose to 35% of portfolios by 2024, led by infrastructure, private credit, and renewable-energy projects offering contractual cash flows and inflation-linked income. Canadian and Dutch funds spearhead direct-investment consortiums that bypass traditional intermediaries, lowering fees and sharpening governance. Yet the growing ticket sizes magnify operational due diligence burden, accentuating the premium on in-house expertise across valuation, legal structuring, and responsible investing frameworks. Managers who can furnish transparent fee models and robust ESG reporting gain traction as trustees intensify scrutiny of cost-to-alpha trade-offs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged low-yield environment | -0.8% | Global, greatest pressure in developed markets | Medium term (2-4 years) |

| DB plan under-funding gaps | -0.6% | North America and Europe | Short term (≤ 2 years) |

| Domestic investment mandates | -0.4% | Varies by jurisdiction | Long term (≥ 4 years) |

| Rising cyber-security exposures | -0.3% | Global, highest in digitally advanced economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prolonged Low-Yield Environment

Real yields that remain below assumed returns compress funding ratios and intensify the need for risk assets. U.S. public plans that previously experienced significant returns later faced notable declines, exposing volatility that challenges board risk tolerance. Trustees respond by lengthening duration through private credit, yet must reconcile liquidity constraints with unpredictable benefit-payment schedules. Liability-driven investing mandates expand, and overlays that hedge interest-rate risk receive renewed attention. The environment elevates pressure on fee budgets and underlines the importance of integrated asset-liability modeling tools capable of stress-testing dozens of economic scenarios.

DB Plan Under-Funding Gaps

Corporate sponsors increasingly execute pension-risk-transfer deals. Legal & General’s GBP 785 million transaction covering three Anglo American schemes in 2025 exemplifies the active de-risking pipeline [1]Legal & General Group plc, “Anglo American Pension Buy-in Announcement,” legalandgeneral.com. These moves underscore a robust market for bulk annuity providers and reinsurers that can absorb longevity exposures at scale. Yet they also think asset pools within legacy DB schemes, encouraging asset managers to pivot toward DC, hybrid, and outsourced CIO mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plan Type: DC Schemes Drive Market Evolution

Defined contribution structures captured 56.85% of the global pension funds market in 2025 and are projected to widen their lead at 6.32% CAGR to 2031. Mandatory auto-enrollment rules in major economies funnel fresh payroll inflows, lifting the pension funds market size for DC accounts to more than USD 52.4 trillion by 2031 . Member-directed investment platforms integrate gamified retirement calculators and ESG filters, enhancing engagement while supplying administrators with anonymized behavioral data that bolsters predictive deferral models.

The legacy DB segment still commands sizable pools, but recurring under-funding and volatility accelerate de-risking. Hybrid formats ranging from collective DC in the United Kingdom to wage-linked plans in Germany seek a middle ground, while India’s civil-service hybrid illustrates global experimentation. For insurers, a vibrant market for buy-ins and longevity swaps emerges, supporting scalable hedging products linked to standardized mortality tables.

By Investment Strategy: Active Management Under Pressure

Active mandates accounted for 54.35% of the global pension funds market in 2025, though fee compression and transparency demands are expected to lift passive uptake at 6.02% CAGR. Index-tracking products now embed ESG screens and fractionally integrate smart-beta tilts, allowing trustees to satisfy stewardship codes without incurring full-service active fees. The pension funds market size allocated to passive equity is expected to grow significantly in the coming years, yet boards still reserve carve-outs for high-conviction active approaches in less-liquid arenas such as global small caps and emerging-market debt.

Blended or “hyper-managed” solutions gain traction, fusing passive building blocks with dynamic overlays that harvest factor-based alpha within tightly controlled tracking-error budgets. Artificial-intelligence tools that mine unstructured data for macro sentiment support real-time rebalancing, cutting decision cycles from weeks to hours. Custodians and middleware vendors expand data pipes to feed these engines, creating fertile revenue niches well beyond traditional safekeeping.

By Sponsor Type: Private Sector Accelerates Growth

Despite the public sector’s share of 68.75% in the global pension funds market in 2025, workplace innovation and regulatory carrots place private-sector plans on a faster 6.91% CAGR trajectory. Simplified set-up procedures, pooled employer plans, and low-cost index funds spur medium-sized enterprises to introduce retirement benefits that rival multinational offerings. The pension funds market share for private-sector plans could climb considerably by 2031, supported by digital payroll integration that slashes administrative friction.

Public funds harness scale to negotiate direct infrastructure stakes and drive climate-aligned mandates, exemplified by CalPERS’ USD 100 billion Climate Action Plan that already surpassed USD 53 billion in commitments. Political oversight can slow adoption of novel asset classes, so many appoint external CIOs who pair internal indexing hubs with specialist managers overseeing private-market allocations.

By Geography of Investment: Offshore Allocation Gains Momentum

Domestic holdings dominated with a 72.75% share of the global pension funds market in 2025, but offshore assets are advancing 5.91% a year as fiduciaries hunt diversified returns. The pension funds market size allocated for non-domestic securities is expected to grow significantly if current rules remain permissive. Risk systems capable of consolidating multi-currency exposures and real-time ESG metrics become indispensable to boards that must justify allocation shifts to regulators and beneficiaries alike.

Increased scrutiny of geopolitical risk pushes plans to adopt scenario modeling that gauges the impact of sanctions, trade barriers, and FX volatility. Insurers and custodians ramp up cross-border fund-administration capabilities, while bilateral tax treaties and mutual-recognition pacts between securities regulators simplify operational entry into priority destinations such as the United States or European Union.

By Region: Asia-Pacific Emerges as Growth Engine

North America retained 70.65% share of the global pension funds market in 2025, thanks to entrenched employer-sponsored systems and an extensive universe of investment vehicles. Nonetheless, Asia-Pacific’s 6.65% CAGR positions it as the principal incremental asset-gathering theatre. Mandatory contribution rises in Australia, newly streamlined portable retirement accounts in India, and rapid middle-class expansion across Southeast Asia combine to accelerate funded-asset accumulation. Japan’s GPIF demonstrated regional sophistication by posting record returns of USD 280 billion in fiscal 2024 .

Chinese pension reforms that gradually raise retirement ages from January 2025 widen participant pools, while South Korea studies contribution increases to 13% to avert fund depletion by 2055. Regional authorities continue refining frameworks that open channels for private-pension products, encouraging global managers to establish onshore vehicles that meet local tax and custody rules.

Geography Analysis

North America’s 70.65% share mirrors deep capital markets, tax-advantaged account frameworks, and widely adopted auto-enrolment. Yet public-plan liabilities press sponsors to explore risk-transfer packages, while technology-driven robo-advice reshapes member engagement. The SECURE 2.0 Act broadens coverage through mandatory enrollment and bigger catch-up ceilings, and Canadian funds sustain peer-leading returns via in-house asset teams that pursue direct private deals.

Asia-Pacific remains the fastest-growing region: GPIF’s governance model influences peers, India’s universal-pension initiatives extend coverage, and China’s phased retirement-age uplift places structural support under funded assets. South Korea’s National Pension Service continues to weigh parametric contributions, and Australia’s superannuation rate rises to 12% in 2025.

Europe balances demographic headwinds with reform zeal. Germany’s new EUR 200 billion equity-focused fund underpins its push toward market-based financing, the Netherlands implements its landmark DC shift, and the United Kingdom’s megafund consolidation aims to unlock GBP 80 billion for infrastructure. France’s public sector scheme ERAFP refines tactical asset allocation amid volatility while maintaining long-term ESG commitments.

Competitive Landscape

Competition is moderate and intensifying. The ten largest funds account for a considerable share of global assets, leaving room for mid-tier players that differentiate by domain expertise or technology. Canadian funds illustrate the edge conferred by in-house active capabilities and direct private-market execution. Acquisition momentum remains brisk: Mercer’s 2024 purchase of Cardano added USD 66 billion of assets, while its 2025 acquisition of SECOR bolstered outsourced-CIO bandwidth. Bulk annuity providers such as Legal & General secured multi-scheme buy-ins worth GBP 785 million, signaling an active de-risking pipeline.

Technology vendors that offer real-time data aggregation, cyber-secure cloud platforms, and AI-assisted customer service gain traction. Cyber threats loom large, with 77% of pension executives expecting elevated risk profiles in 2025, prompting stepped-up investment in zero-trust architectures and staff-training programs. Asset managers pivot toward climate-aligned strategies: CalPERS leads with USD 53 billion already deployed toward a USD 100 billion goal.

Emerging disruptors include tokenization start-ups that fractionalize infrastructure equity, reducing ticket sizes and unlocking diversified opportunities. Meanwhile, data providers harness natural-language processing to decode corporate climate disclosures, meeting trustees’ need for transparent ESG metrics while complementing established governance protocols.

Pension Funds Industry Leaders

CalSTRS (US)

Government Pension Investment Fund (Japan)

National Pension Service (South Korea)

ABP (Netherlands)

California Public Employees’ Retirement System (CalPERS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UK Government directed pension schemes to consolidate into default arrangements holding at least GBP 25 billion by 2030 to boost investment in national infrastructure.

- March 2025: Chile enacted a mixed-pillar pension law that lifts employer contributions to 8.5% and introduces a new social-security component.

- February 2025: Mercer closed the acquisition of SECOR Asset Management, adding USD 35 billions of advised and managed assets.

- February 2025: Allianz, BlackRock, and T&D Holdings agreed to acquire Viridium Group for EUR 3.5 billion, adding EUR 67 billions of closed-life assets under management.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global pension fund market as the pool of professionally managed collective investment vehicles that receive, administer, and invest retirement contributions from occupational defined-contribution, defined-benefit, and hybrid plans backed by public-sector and private-sector sponsors. Assets are consolidated in US dollars using prevailing year-end exchange rates.

Scope Exclusions: We intentionally exclude pay-as-you-go social-security systems, individually purchased retirement savings accounts that are not pooled, and sovereign wealth vehicles unrelated to retirement income.

Segmentation Overview

- By Plan Type

- Defined Contribution (DC)

- Defined Benefit (DB)

- Hybrid and Others

- By Investment Strategy

- Active

- Passive

- By Sponsor Type

- Public-Sector Plans

- Private-Sector Plans

- By Geography of Investment

- Onshore

- Offshore

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with fund trustees, investment consultants, and regulators across North America, Europe, and Asia-Pacific helped clarify contribution patterns, asset-allocation shifts, and reform timelines. Insights from these conversations let us challenge desk findings and adjust assumptions where real-world practice diverged.

Desk Research

Our analysts began with authoritative statistics from bodies such as the OECD Pension Markets in Focus, the IMF Global Financial Stability Note, and World Bank demographic tables, which provide historic asset pools and participation ratios. Public regulator filings (for example, Form 5500 in the United States), national fund annual reports, and press archives accessed through Dow Jones Factiva enriched these baselines. Subscription data from D&B Hoovers supplied multi-year balance-sheet details for the largest pension sponsors, while consultation papers from the International Organisation of Pension Supervisors flagged upcoming rule changes. This list is illustrative; many additional open and paid sources were reviewed for confirmation and gap filling.

Market-Sizing and Forecasting

A top-down reconstruction anchored on reported assets, regulator data, and cross-border investment statistics produced the base year value. Selective bottom-up roll-ups of sampled funds, plus channel checks on contribution inflows and withdrawal ratios, validated totals. Key variables in the model include covered workforce size, average contribution rate, funded-status ratios, long-run return expectations, and exchange-rate paths. Multivariate regression, augmented by scenario analysis on real-yield trajectories, projects assets through the forecast period. Where discrete fund data were missing, country-level coverage ratios and historic allocation norms bridged gaps.

Data Validation and Update Cycle

Mordor analysts run variance checks against external macro indicators and automated anomaly alerts. Findings then pass peer review before sign-off. Reports refresh each year and may be updated sooner if material policy or market events occur. Before delivery, one analyst re-verifies every figure so clients receive the latest vetted view.

Why Mordor's Pension Funds Baseline Commands Reliability

Published estimates often diverge because firms vary scope, valuation dates, and currency treatment.

Key gap drivers with other providers include inclusion of insurer annuity reserves, reliance on earlier base years without FX normalization, or focus on only the largest twenty-two markets, leaving emerging economies uncounted.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 67.16 trn (2025) | Mordor Intelligence | - |

| USD 76.54 trn (2024) | Global Consultancy A | Adds insurance retirement products and uses earlier baseline |

| USD 58.50 trn (2024) | Industry Association B | Omits many emerging markets and voluntary third-pillar plans |

These contrasts show how Mordor's clear perimeter selection, blended valuation date, and transparent variable set give decision-makers a balanced baseline that is repeatable and easy to audit.

Key Questions Answered in the Report

What is the current size of the pension funds market?

The market held USD 70.89 trillion in assets in 2026 and is projected to reach USD 92.83 trillion by 2031.

Which plan type is expanding the fastest?

Defined contribution schemes lead growth at a 6.32% CAGR, aided by auto-enrolment mandates and growing payroll contributions.

Why are pension funds increasing allocations to alternative assets?

Persistent low yields in traditional bonds push funds toward infrastructure, private credit, and other alternatives that offer inflation-linked cash flows and diversification benefits.

How are regulators influencing pension savings rates?

Measures such as the SECURE 2.0 Act in the United States introduce mandatory enrollment and higher contribution rates, directly boosting funded assets.

What role does technology play in the pension funds industry?

Digital administration, AI-driven member analytics, and cybersecurity solutions reduce operating costs, enhance engagement, and safeguard sensitive data, becoming critical differentiators among providers.

Which region offers the strongest growth outlook?

Asia-Pacific is forecast to expand at a 6.65% CAGR through 2031, driven by rising contribution rates, regulatory reforms, and rapid middle-class expansion.

Page last updated on: