Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

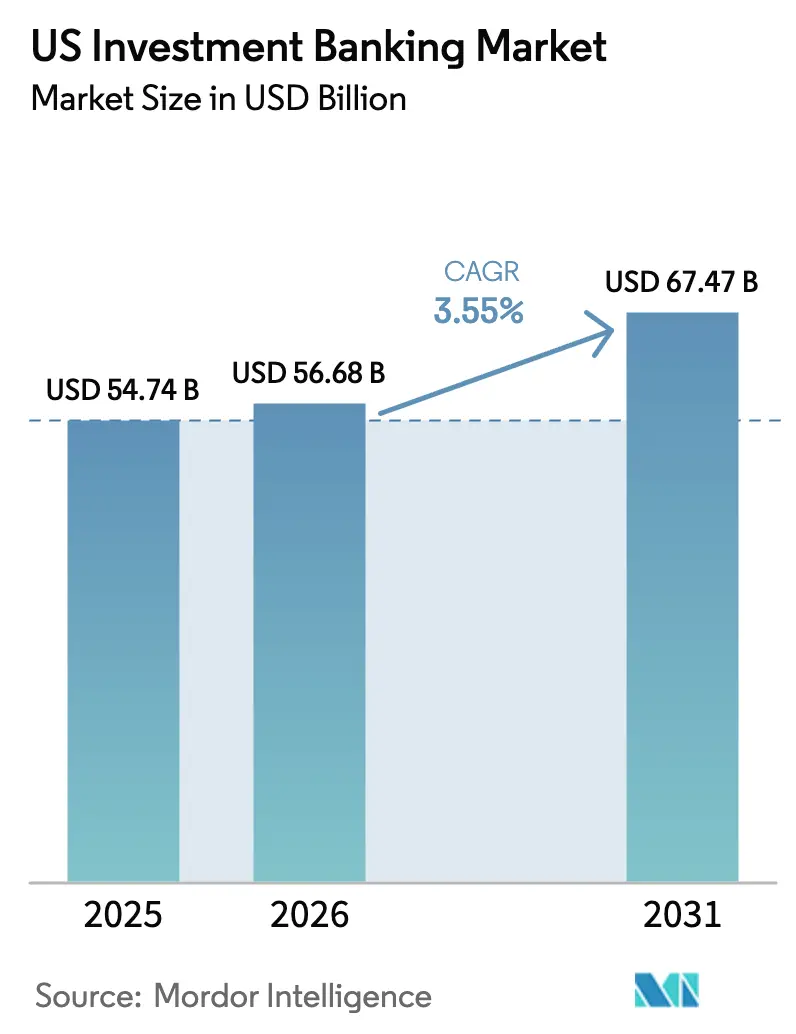

| Base Year Market Size (2025) | USD 54.74 Billion |

| Market Size (2026) | USD 56.68 Billion |

| Market Size (2031) | USD 67.47 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

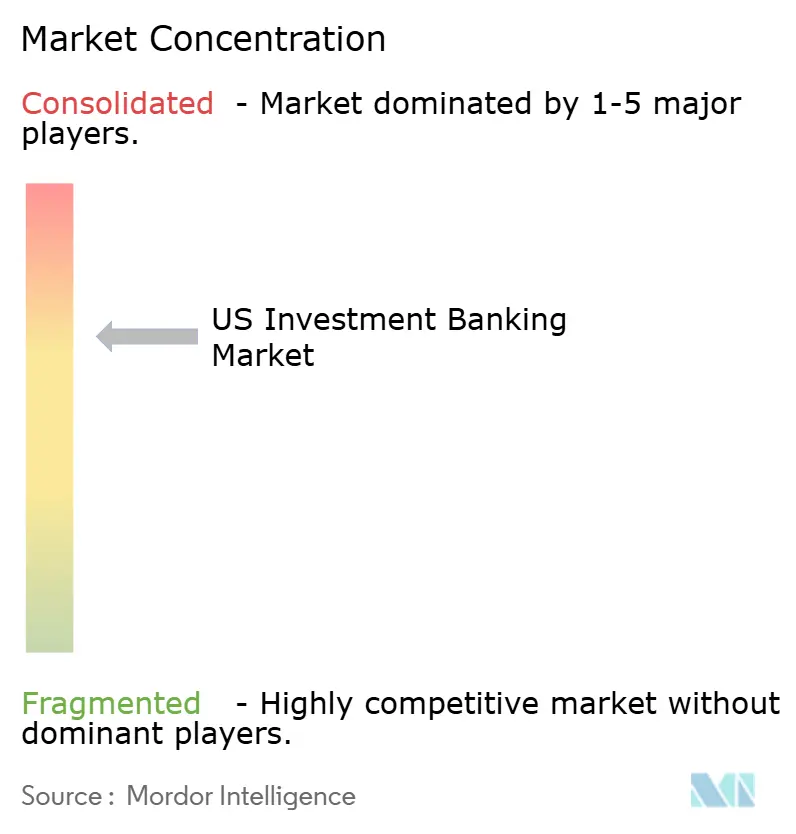

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Investment Banking Market Analysis by Mordor Intelligence

The US investment banking market size is expected to grow from USD 54.74 billion in 2025 to USD 56.68 billion in 2026 and is forecast to reach USD 67.47 billion by 2031 at 3.55% CAGR over 2026-2031. Revenue momentum derives from sponsor-led mergers, a stabilizing IPO calendar, and expanding fee pools tied to energy-transition financing supported by federal incentives. At the same time, higher policy rates, tougher Basel III requirements, and rapid private-credit growth are reshaping profitability models. Banks are building capital-solutions desks that combine private credit, equity, and hedging to deepen client wallet share. Heavy investment in generative AI and analytics is improving pitch efficiency and deal sourcing, reinforcing economies of scale across the US investment banking market.

Key Report Takeaways

- By product type, mergers & acquisitions led with 40.72% share of the US investment banking market in 2025; equity capital markets is projected to expand at a 4.74% CAGR through 2031.

- By deal size, large-cap transactions (USD 1–5 billion) captured 36.95% of the US investment banking market in 2025, whereas mega-cap deals above USD 5 billion are expected to advance at a 4.31% CAGR to 2031.

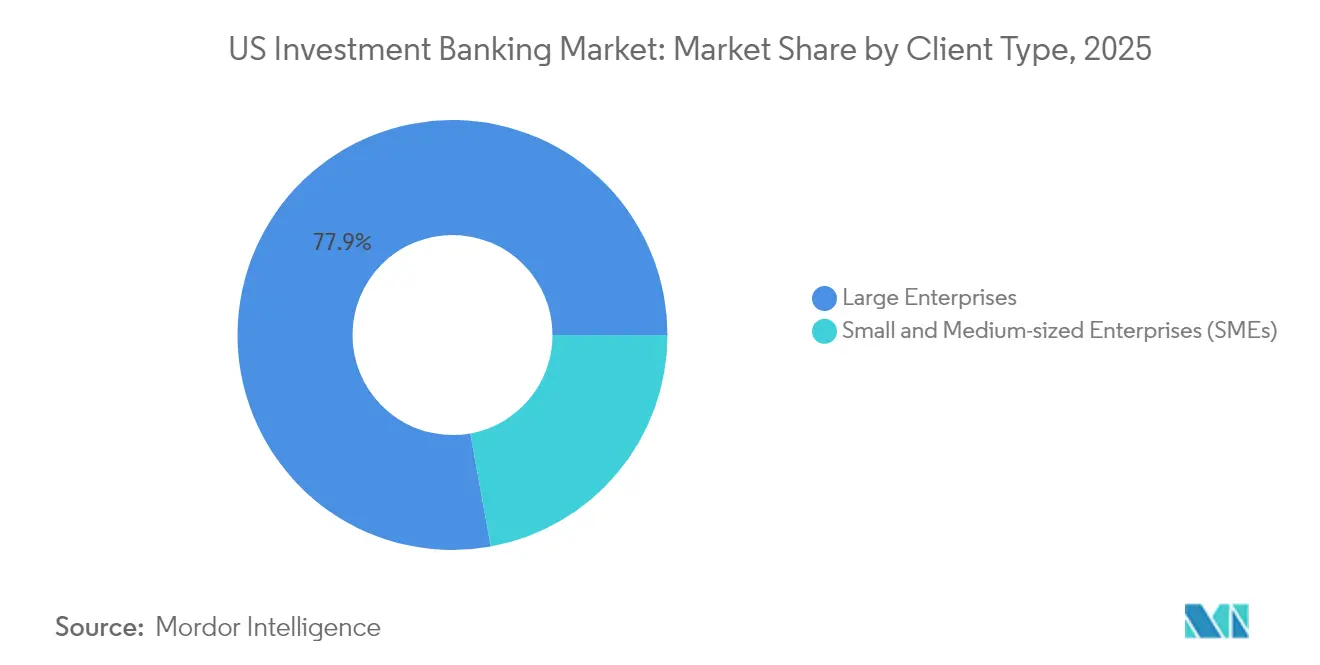

- By client type, large enterprises held 77.85% of the US investment banking market share in 2025; SME mandates are projected to grow at a 5.03% CAGR through 2031.

- By industry vertical, IT & telecommunication accounted for 23.28% of the US investment banking market in 2025; the healthcare & pharmaceuticals segment is set to rise at a 4.88% CAGR through 2031.

- Leading universal and independent platforms continue to invest in technology, sector specialization, and private-credit capabilities to defend advisory margins.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Investment Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in private-equity dry-powder driving sponsor-led M&A | +1.2% | North America-focused | Medium term (2–4 years) |

| Balance-sheet restructuring amid higher rates boosting debt advisory | +0.8% | North America with spillover to Europe | Short term (≤ 2 years) |

| Infrastructure and energy-transition financing momentum | +0.6% | North America with selective international exposure | Long term (≥ 4 years) |

| IPO pipeline rebound in tech and healthcare | +0.7% | Major US financial centers | Medium term (2–4 years) |

| SPAC-to-traditional-deal conversions expanding hybrid fee pools | +0.3% | North America | Short term (≤ 2 years) |

| Tokenization of securities opening new fee structures | +0.4% | Global, early US adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Private-Equity Dry-Powder Driving Sponsor-Led M&A

A record USD 1.6 trillion in uninvested capital is fueling sponsor activity, sustaining fee generation across the US investment banking market despite rate volatility[1]J.P. Morgan Chase & Co., “ESG Report 2025,” jpmorganchase.com. Sponsors facing deployment deadlines are closing mega-cap transactions that typically command 20–30% higher advisory spreads than corporate combinations. The scale of dry powder is also encouraging club deals, where multiple funds partner on a single target, further increasing fee complexity for advisors. Headline examples include ConocoPhillips’ USD 22.5 billion acquisition of Marathon Oil, which required intricate integration plans and bridge financing structures. As these large deals become more common in technology and healthcare, banks with deep sector knowledge and balance-sheet capacity are best positioned to win mandates and protect pricing power in the US investment banking market.

Balance-Sheet Restructuring Amid Higher Rates Boosting Debt Advisory

Policy rates above 5% have raised corporate refinancing costs, driving a surge in demand for liability-management advice. Citigroup’s Q4 2024 debt-advisory revenue spike highlights how issuers are leaning on banks to manage maturities and covenant pressure. Companies with upcoming 2025-2026 rollovers are requesting ESG-linked repricings, exchange offers, and hybrid securities that mitigate earnings risk. Banks able to combine derivatives, private-credit placements, and bond issuance in one proposal are capturing a larger wallet share. This environment turns debt advisory into a strategic entry point for cross-selling, supporting overall fee resilience inside the US investment banking market even while new-money deal flow softens.

Infrastructure & Energy-Transition Financing Momentum

Federal incentives under the Inflation Reduction Act have catalyzed a multi-gigawatt pipeline of renewable projects requiring sophisticated financing solutions[2]U.S. Department of Energy, “Loan Programs Office Monthly Update,” energy.gov. Deutsche Bank’s USD 11 billion SunZia mandate shows the scale at stake as lenders coordinate tax-equity, mezzanine debt, and credit guarantees. Investment banks with strong project-finance pedigrees are forming dedicated clean-energy teams to navigate evolving regulatory frameworks and community stakeholder concerns. Early movers are also advising on green-bond issuance and carbon-capture ventures, diversifying fee streams beyond traditional power-generation assets. As annual US infrastructure spending climbs, these mandates promise a durable, long-term contribution to the US investment banking market.

IPO Pipeline Rebound in Tech & Healthcare

The 2024 issuance calendar featured 154 traditional offerings raising USD 28.6 billion, and early-2025 deals such as Omada Health’s USD 150 million flotation posted a 21% first-day gain[3]Paul Hastings LLP, “2024 U.S. IPO Report,” paulhastings.com. A backlog of venture-backed unicorns in digital health, AI software, and biotech is poised to list once market windows remain open for two consecutive quarters. Underwriters are benefiting from higher gross spreads as issuers prioritize certainty of execution over fee negotiation. Private-equity exit needs and venture-capital liquidity cycles further reinforce demand for equity-capital-markets services. This creates a virtuous loop in which successful IPOs validate valuation benchmarks, attracting more candidates and expanding the US investment banking market’s growth runway.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated interest rates suppressing leveraged-finance volumes | -0.9% | North America-led | Short term (≤ 2 years) |

| Basel III “Endgame” capital charges squeezing returns | -0.7% | Global, phased US rollout | Medium term (2–4 years) |

| Private-credit rise disintermediating syndicated loans | -0.5% | US with global expansion | Long term (≥ 4 years) |

| AI capital-raising platforms eroding mid-market fees | -0.3% | Developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Elevated Interest Rates Suppressing Leveraged-Finance Volumes

All-in yields topping 8% have rendered many private-equity buyouts uneconomical, forcing sponsors to shelve or resize transactions. Loan desks report thinner order books as traditional CLO investors demand wider spreads to absorb duration and credit risk. In response, banks are downsizing bridge commitments and demanding higher market-flex cushions, dampening underwriting fee potential. Although advisory mandates rise for capital-structure optimization, they seldom match the economics of fully underwritten financings. Until benchmark rates fall or EBITDA multiples reset, leveraged-finance softness will continue to weigh on the US investment banking market’s near-term growth.

Basel III “Endgame” Capital Charges Squeezing Returns

Proposed rules could boost common-equity Tier 1 ratios by roughly 16% for large US banks, especially penalizing market-making and OTC derivatives books[4]Arnold & Porter, “Regulatory Approval of Capital One-Discover Deal,” arnoldporter.com. The resulting higher capital density lowers ROE targets for balance-sheet-intensive activities, nudging banks toward fee-only advisory. Compliance investments—ranging from model-validation teams to data-lineage systems—further erode margins in the transition period. Mid-tier institutions without global scale face a disproportionate burden, accelerating consolidation pressure across the sector. As management reallocates scarce capital, overall wallet shrinkage could temper long-term expansion of the US investment banking market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Deal Advisory Strength Offsets Financing Headwinds

Mergers & Acquisitions retained a 40.72% share of the US investment banking market size in 2025. Advisory depth, sector specialization, and sponsor demand keep activity resilient even when capital-market windows narrow. Equity Capital Markets ranks as the fastest riser, projected at 4.74% CAGR, as postponed IPOs and SPAC conversions feed the backlog. Debt Capital Markets faces rate headwinds, yet complex liability-management assignments fetch premium spreads, cushioning revenue declines. Strategically, platforms integrating M&A, private credit, and ECM pitches hold an edge, exemplified by Goldman Sachs’ Capital Solutions Group.

By Deal Size: Fee Weighting Skews Toward Mega-Cap Complexity

Large-cap transactions in the USD 1–5 billion bracket controlled 36.95% share of the US investment banking market size in 2025, but mega-cap deals above USD 5 billion are forecasted to post a 4.31% CAGR, expanding their contribution to the US investment banking market. Bigger deals carry heightened regulatory scrutiny and multi-jurisdictional risk, prompting corporates to hire top-tier advisors such as those coordinating the Capital One–Discover combination. Mid-market activity faces margin compression as AI analytics empower boutiques to compete on price. To protect economics, banks deploy automated diligence, segmenting teams to align resource intensity with potential fees. When mega-cap volumes spike, market size grows disproportionately because headline fees scale non-linearly with consideration value.

By Client Type: Enterprise Relationships Anchor Revenue Streams

Large enterprises accounted for 77.85% of the US investment banking market size in 2025, anchoring the US investment banking market. Multiyear service agreements span M&A, equity, debt, and risk solutions, making churn unlikely. SME mandates are projected to rise at 5.03% annually as digital portals cut ticket-size thresholds for professional advice. Relationship-management software now steers bankers toward cross-sell gaps, improving share of wallet. Over time, this broadens the US investment banking market share base, diversifying revenue streams beyond Fortune 500 clients.

By Industry Vertical: Technology Leadership Amid Healthcare Tailwind

IT & Telecommunication accounted for 23.28% share of the US investment banking market size in 2025, driven by cloud consolidation and semiconductor deals requiring complex IP valuation. Healthcare & Pharmaceuticals, projected at 4.88% CAGR, benefits from aging demographics and biotech breakthroughs. Banks staff cross-functional teams blending regulatory counsel, scientific expertise, and capital-markets depth. Goldman Sachs’ collaboration with the MIT-IBM Watson AI Lab on biodiversity analytics shows how tailored insight differentiates service offerings. Sector-specific expertise remains essential to sustaining premium pricing in the US investment banking market.

Geography Analysis

New York anchors the US investment banking market, concentrating executive leadership, trading floors, and regulatory liaisons that facilitate complex cross-border mandates. Network effects from deep talent pools, specialized legal counsel, and institutional investors reinforce entry barriers for newcomers. San Francisco specializes in technology advisory, Boston in healthcare and asset management, and Chicago in diversified industrial and middle-market coverage, giving banks proximity to sector clusters. Cross-border revenue is meaningful as US advisors guide international issuers through SEC processes and outbound M&A. Federal infrastructure and climate legislation is redirecting coverage teams into clean-energy corridors across Texas, the Midwest, and the Mountain West, enabling banks to build local stakeholder networks that secure repeat mandates in project finance.

Competitive Landscape

The US investment banking market is moderately concentrated, with a handful of systemically important financial institutions capturing a clear majority of advisory and underwriting fees and setting pricing norms for the rest of the industry. These universal banks leverage large balance sheets, integrated capital-markets platforms, and multi-decade client relationships to retain lead-left roles on most marquee transactions, creating high barriers to entry for emerging rivals. Their scale advantage is further entrenched by heavy spending on data infrastructure and regulatory compliance systems that smaller firms struggle to replicate. The resulting fee pool is therefore tilted toward incumbents, allowing them to exercise meaningful negotiating power over syndicate economics and client retainer structures. Industry observers note that this configuration leaves limited room for mid-tier players to break into the top tier without a niche specialization or transformative acquisition strategy.

Independent boutiques counter the dominance of universal banks by emphasizing conflict-free advice, senior-level attention, and sector depth. Although they collectively hold a smaller slice of the market, boutiques frequently win high-profile mandates in technology, healthcare, and energy, where boardrooms value specialization over balance-sheet support. Their success has encouraged larger banks to set up sector-focused pods that mirror boutique intimacy while retaining full-service capabilities. Technology investment is becoming a decisive differentiator across both groups; Goldman Sachs’ deployment of a generative-AI assistant to thousands of bankers illustrates how scale players intend to widen efficiency gaps. Boutiques respond by adopting cloud-based analytics suites, but the capital required to keep pace underscores the structural advantages enjoyed by the largest institutions.

Private-credit capability represents the newest competitive front. Universal banks now pitch loan-to-own, unitranche, and NAV-backed solutions from captive direct-lending arms, offering deal certainty that pure advisory shops cannot match. Boutiques without balance-sheet capacity compensate through alliances with alternative-asset managers, ensuring participation in sponsor processes even when traditional syndication is bypassed. As direct lending gains share, advisory houses that secure reliable capital partners should preserve relevance, while scale banks will consolidate their hold over integrated mandates that bundle financing and strategic counsel.

US Investment Banking Industry Leaders

J.P. Morgan Chase & Co.

Goldman Sachs

Bank of America

Morgan Stanley

Citi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Astris Finance and Colliers formed a partnership, giving Colliers a controlling stake to scale an infrastructure-focused investment banking platform.

- May 2025: Capital One completed its USD 35.3 billion acquisition of Discover Financial Services after securing regulatory approval.

- April 2025: Rocket Companies announced plans to buy Mr. Cooper Group in a USD 9.4 billion all-stock deal expected to close in Q4 2025.

- March 2025: Sycamore Partners moved to acquire Walgreens Boots Alliance for up to USD 23.7 billion, pending approvals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the US investment-banking market as fee and interest income generated inside the United States from advising, underwriting, and arranging mergers & acquisitions, equity capital markets, debt capital markets, and syndicated loans for corporate, institutional, and public-sector clients. Revenues from proprietary trading, asset management, or retail brokerage are outside this boundary.

Scope Exclusions: Activities linked solely to wealth management, prime brokerage, or prop-trading desks are excluded to keep the focus on classical investment-banking mandates.

Segmentation Overview

- By Product Type

- Mergers & Acquisitions

- Debt Capital Markets

- Equity Capital Markets

- Syndicated Loans & Others

- By Deal Size

- Mega-cap ( More than USD 5 billion)

- Large-cap (USD 1-5 billion)

- Mid-market (USD 250 million - 1 billion)

- Small-cap (Less than USD 250 million)

- By Client Type

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Industry Vertical

- Banking, Financial Services, Insurance (BFSI)

- IT & Telecommunication

- Manufacturing

- Retail And E-Commerce

- Public Sector

- Healthcare And Pharmaceuticals

- Other Industry Verticals

Detailed Research Methodology and Data Validation

Primary Research

Several semi-structured interviews with senior dealmakers, syndicate managers, private-equity principals, and finance chiefs across New York, Chicago, San Francisco, and Charlotte validated fee spreads, pipeline health, and client appetite, filling gaps that desk sources left and challenging early model outliers before we finalized assumptions.

Desk Research

We reviewed publicly available tier-1 sources such as SEC 10-K filings, Federal Reserve Z.1 flow-of-funds tables, FDIC Quarterly Banking Profiles, SIFMA capital-markets statistics, and OECD infrastructure-spend datasets, supplemented by industry journals like American Banker and PitchBook league-tables for deal counts. Paid intelligence from D&B Hoovers and Dow Jones Factiva helped map revenue splits by business line while ensuring firm-level consistency. These illustrate inputs only; dozens of additional references were investigated for corroboration, clarification, and historical continuity.

Market-Sizing & Forecasting

Mordor analysts begin with a top-down reconstruction of fee pools by applying observed fee yields to announced deal and issuance volumes captured in regulator releases and league-table feeds; selective bottom-up checks sampling disclosed advisory invoices and average ticket sizes calibrate spreads by deal size and sector. Core variables include announced M&A value, IPO and bond issuance counts, private-equity dry powder, policy-rate path, and Basel III capital buffers; each is forecast through multivariate regression anchored to GDP and corporate profit outlooks, followed by scenario analysis for volatility shocks. Gaps in bottom-up data are bridged using three-year moving averages from comparable cohorts before weighting by historical fee elasticity.

Data Validation & Update Cycle

Outputs pass an anomaly screen versus independent fee indices, after which a senior analyst reviews driver logic line by line. The model refreshes annually and is reopened whenever regulatory, macro, or deal-volume shifts breach predefined variance bands; clients therefore receive a freshly vetted baseline at delivery.

Why Mordor's US Investment Banking Baseline Commands Reliability

Published estimates vary because firms mix divergent revenue streams, refresh at uneven cadences, and apply contrasting scenario levers.

Mordor's disciplined scope, double-lens modeling, and yearly refresh keep our figure balanced and decision ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 54.74 B (2025) | Mordor Intelligence | - |

| USD 32.52 B (2025) | Regional Consultancy A | Counts advisory fees only; omits loan syndication and bridge financing income |

| USD 32.2 B (2023) | Trade Journal B | Snapshots past fee revenue, lacks forward pipeline or macro adjustments |

| USD 134.40 B (2024) | Global Consultancy A | Adds trading and asset management desks then scales down from global totals |

Differences show that narrower scopes understate future opportunity while very broad roll-ups inflate totals; our balanced boundary and transparent driver set give executives a dependable start point for strategy and benchmarking.

Key Questions Answered in the Report

What is the current size of the US investment banking market?

The market is valued at USD 56.68 billion in 2026.

How fast is the US investment banking market expected to grow?

It is projected to expand at a 3.55% CAGR, reaching USD 67.47 billion by 2031.

Which product category leads the market?

Mergers & Acquisitions led with a 40.72% market share in 2025.

What factors are driving growth in equity capital markets?

A recovering IPO window in technology and healthcare, combined with SPAC conversions, supports a 4.74% CAGR for ECM mandates.

How is private credit affecting traditional investment banking?

Private-credit growth disintermediates syndicated loans but enables banks with captive funds to offer new capital-solution services.

Why is infrastructure finance a focus area for banks?

Federal incentives for clean-energy projects require complex tax-equity and project-finance structures, creating durable fee pools for experienced advisors.

Page last updated on: