Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

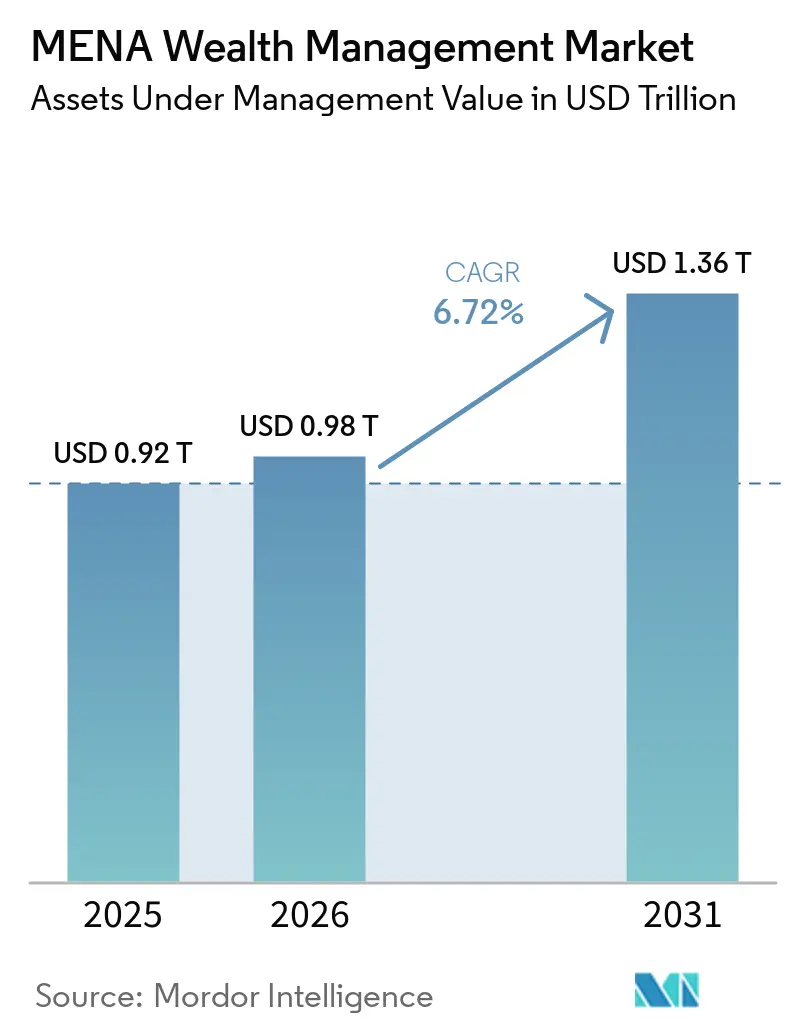

| Base Year Market Size (2025) | USD 0.92 Trillion |

| Market Size (2026) | USD 0.98 Trillion |

| Market Size (2031) | USD 1.36 Trillion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

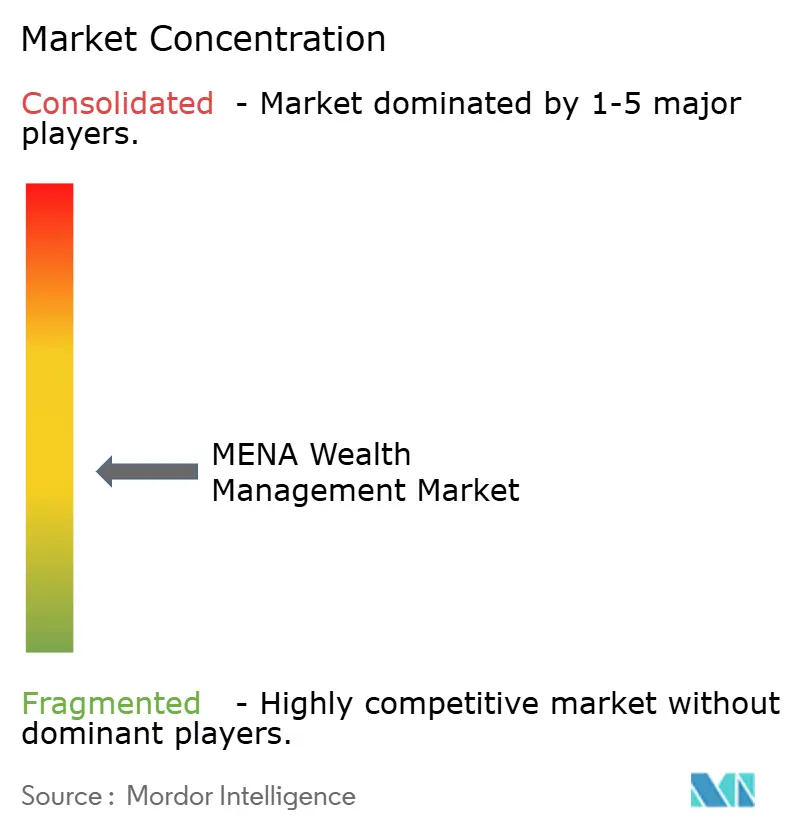

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MENA Wealth Management Market Analysis by Mordor Intelligence

The MENA wealth management market size is expected to grow from USD 0.92 trillion in 2025 to USD 0.98 trillion in 2026 and is forecast to reach USD 1.36 trillion by 2031 at 6.72% CAGR over 2026-2031. The outlook benefits from sovereign-wealth diversification mandates that funnel hydrocarbon earnings into structured advisory products, policy frameworks that levy zero personal tax in UAE and Saudi Arabia, and regulatory sandboxes that fast-track tokenized investment funds. Intensifying millionaire migration to economic zones in Dubai, Abu Dhabi, and Riyadh fortifies the regional asset base while Shariah-compliant robo-advisory tools expand coverage among mass-affluent savers. Competitive behavior centers on hybrid advisory models that merge human expertise with automated screening and portfolio construction. The rise of environmental, social, and governance mandates plus gender-inclusive entrepreneurship programs broadens the potential client pool and supports strong revenue momentum over the forecast horizon.

Key Report Takeaways

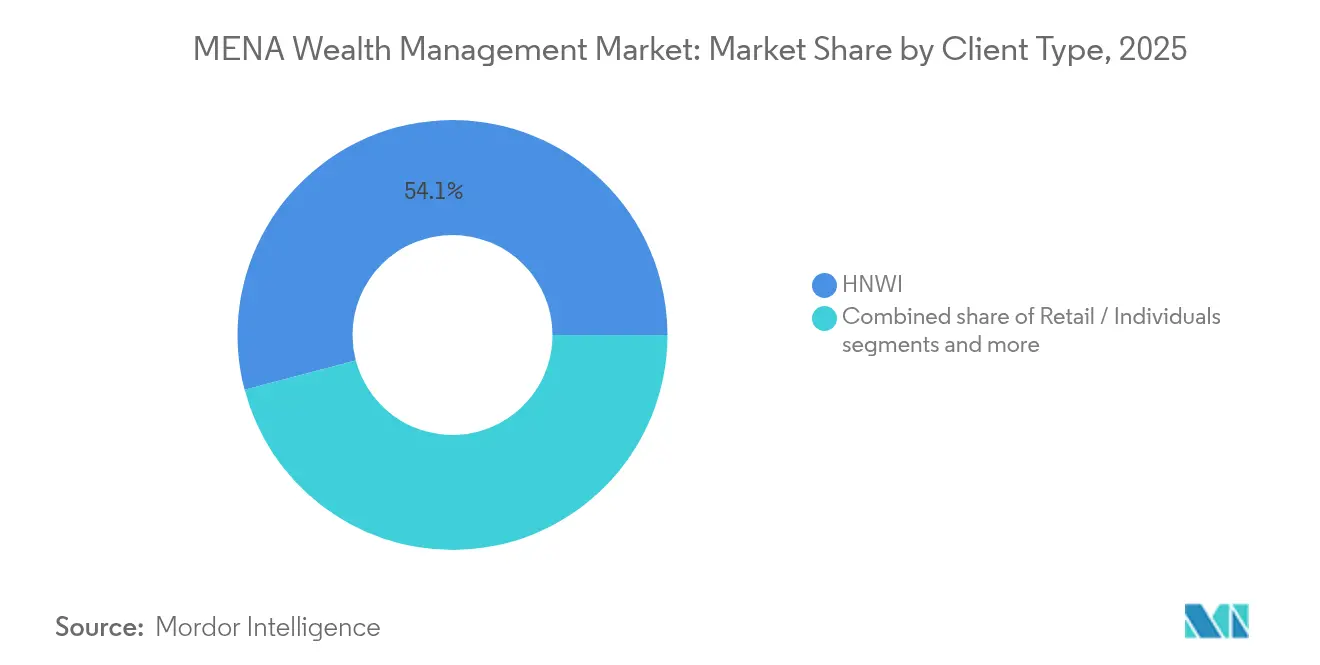

- By client type, high-net-worth individuals held 54.10% of the MENA wealth management market share in 2025, while retail investors are advancing at a 11.78% CAGR to 2031.

- By provider, private banks controlled 42.80% of the MENA wealth management market size in 2025 and fintech advisors (under others) are expanding at a 18.70% CAGR through 2031.

- By geography, the GCC captured 38.90% of the MENA wealth management market share in 2025 and North Africa is forecast to post a 9.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MENA Wealth Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gulf HNWI in-migration to UAE & Saudi economic zones | 1.8% | UAE, Saudi Arabia, with spillover to Qatar, Bahrain | Medium term (2-4 years) |

| Sovereign-wealth diversification boosting on-shore AUM | 1.2% | GCC core, expanding to Kuwait, Oman | Long term (≥ 4 years) |

| Rapid rise of Islamic digital-wealth platforms | 0.9% | Global MENA, strongest in UAE, Saudi Arabia, Malaysia | Short term (≤ 2 years) |

| Inter-generational USD 2 trillion GCC wealth transfer wave | 0.7% | GCC core, with early concentration in Dubai, Riyadh | Medium term (2-4 years) |

| Female entrepreneurship and rising women-controlled assets | 0.6% | Saudi Arabia, UAE, with gradual expansion to Qatar | Medium term (2-4 years) |

| DIFC/ADGM sandbox pipelines for tokenised funds | 0.5% | UAE concentrated, with regulatory spillover to Bahrain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gulf HNWI In-Migration Accelerates Onshore AUM Growth

Zero-tax residency programs in the UAE and Saudi Arabia drive unprecedented millionaire migration, with the UAE expected to attract 9,800 high-net-worth individuals in 2025 alone[1]Gulf News, “UAE to Attract 9,800 Millionaires in 2025,” gulfnews.com. . This influx creates immediate demand for sophisticated wealth structuring services, family office establishment, and cross-border tax optimization strategies that local private banks are rapidly scaling to capture. The Dubai International Financial Centre processed over 200 new family office applications in 2024, representing a 40% increase from the previous year[2]DIFC, “Family Offices Surge 40% in 2024,” difc.ae. . Saudi Arabia's Riyadh International Financial District similarly targets 500 licensed financial services firms by 2030, creating competitive pressure on established UAE hubs. This geographic arbitrage fundamentally reshapes regional AUM distribution patterns as wealth managers establish dual-hub strategies to serve mobile HNWI clients.

Sovereign Wealth Diversification Mandates Reshape Private Banking

Gulf sovereign wealth funds increasingly mandate private banking relationships for their diversification strategies, moving beyond traditional asset management toward structured products and alternative investments. The Saudi Public Investment Fund's allocation to private markets reached 30% in 2024, while ADIA expanded its private wealth co-investment programs with regional family offices. This institutional-to-private wealth crossover creates new revenue streams for private banks that can bridge sovereign capital with HNWI investment opportunities. Abu Dhabi Investment Authority's partnership with local private banks for co-investment vehicles demonstrates how sovereign capital increasingly flows through private banking channels rather than direct institutional mandates. The trend accelerates as oil-dependent economies seek to create sustainable wealth management ecosystems beyond hydrocarbon revenues.

Islamic Digital Wealth Platforms Democratize Shariah-Compliant Investing

Shariah-compliant robo-advisory platforms experienced 180% user growth in 2024, with Sarwa and StashAway leading digital wealth democratization across MENA markets. These platforms address the critical gap in mass-affluent Islamic investment options, offering automated portfolio construction that adheres to Islamic finance principles while maintaining cost structures 60% lower than traditional private banking. The Dubai Financial Services Authority approved 12 new Islamic fintech licenses in 2024, while Saudi Arabia's Capital Market Authority launched its fintech sandbox specifically for Shariah-compliant investment platforms[3]Dubai Financial Services Authority, “2024 Islamic Fintech Licenses,” dfsa.ae. . Regulatory frameworks under DIFC and ADGM now provide clear pathways for Islamic robo-advisors to scale across GCC markets. This technological disruption forces traditional private banks to develop hybrid advisory models that combine human relationship management with automated Shariah screening capabilities.

Inter-Generational USD 2 Trillion Wealth Transfer Reshapes Advisory Demand

The largest inter-generational wealth transfer in GCC history accelerates through 2030, with an estimated USD 2 trillion transitioning from first-generation entrepreneurs to tech-savvy heirs who demand ESG-aligned and technology-enabled investment solutions. Next-generation wealth holders show 70% higher preference for sustainable investing compared to their parents, while requiring digital-first advisory interfaces that traditional relationship managers struggle to provide. Family offices in Dubai and Riyadh increasingly hire chief investment officers with technology backgrounds rather than traditional banking experience, signaling a fundamental shift in advisory service expectations. The Abu Dhabi Global Market reported a 45% increase in family office registrations specifically focused on next-generation wealth management in 2024. This generational transition creates opportunities for fintech-enabled advisory firms while challenging incumbent private banks to modernize their service delivery models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical flashpoints & sanctions spill-over risk | -1.1% | MENA-wide, with concentration in Levant, Iran, Iraq | Short term (≤ 2 years) |

| Oil-price volatility affecting liquidity creation | -0.8% | GCC core, spillover to oil-dependent MENA economies | Short term (≤ 2 years) |

| Fragmented Shariah & cross-border regulatory regimes | -0.6% | MENA-wide, with particular complexity in multi-jurisdictional structures | Medium term (2-4 years) |

| Shortage of Arabic-speaking certified wealth advisers | -0.5% | GCC, North Africa, with acute shortages in Saudi Arabia, UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Flashpoints Create Compliance Cost Escalation

Regional conflicts and sanctions regimes impose escalating compliance costs on MENA wealth managers, with some institutions reporting 40% increases in anti-money laundering and sanctions screening expenses during 2024. Enhanced due diligence requirements for clients with regional business interests create onboarding delays averaging 45 days compared to 15 days for European clients, according to HSBC Private Bank's regional compliance reports. The U.S. Treasury's Office of Foreign Assets Control expanded secondary sanctions risks for financial institutions serving certain Middle Eastern markets, forcing some global private banks to restrict services to regional clients. Swiss private banks operating in DIFC implemented additional client screening protocols that increased operational costs by 25% while reducing client acquisition rates. These compliance burdens disproportionately affect smaller regional players who lack the technology infrastructure to efficiently manage complex sanctions screening requirements.

Regulatory Fragmentation Impedes Cross-Border Islamic Finance Scaling

Divergent Shariah interpretations across GCC jurisdictions create operational complexity for Islamic wealth management platforms seeking regional scale, with some products approved in the UAE but rejected in Saudi Arabia due to different religious authority standards. The lack of harmonized Islamic finance regulations forces wealth managers to maintain separate product offerings and compliance frameworks for each market, increasing operational costs by an estimated 30% compared to conventional products. Malaysia's Securities Commission and the UAE's Emirates Securities and Commodities Authority maintain different sukuk structuring requirements, preventing regional Islamic investment funds from achieving economies of scale[4]Securities Commission Malaysia, “Updated Sukuk Guidelines,” sc.com.my. . Cross-border Shariah-compliant wealth management products face approval delays averaging 8 months across multiple jurisdictions, compared to 3 months for conventional products. This regulatory fragmentation particularly constrains fintech platforms that rely on standardized product offerings to achieve profitability across multiple markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Client Type: HNWI Dominance Faces Retail Digitization

High-net-worth individuals maintain commanding market leadership with a 54.10% share in 2025, yet retail investors emerge as the transformation catalyst with a 11.78% CAGR through 2031. The HNWI segment benefits from the UAE's golden visa program and Saudi Arabia's premium residency scheme, which attracted over 15,000 millionaire families to the region in 2024. Traditional relationship-driven advisory models serve this segment through private banking arms of Emirates NBD, FAB, and international players like UBS and Julius Baer. However, next-generation HNWI clients increasingly demand technology-enabled solutions, forcing private banks to invest heavily in digital advisory platforms and ESG-compliant investment products.

Retail investors represent the market's digital frontier, with platforms like Sarwa and StashAway democratizing wealth management access through Shariah-compliant robo-advisory services that require minimum investments as low as USD 500. The Dubai Financial Services Authority's regulatory sandbox enabled 12 new retail-focused Islamic fintech platforms in 2024, while Saudi Arabia's Capital Market Authority streamlined licensing for mass-market advisory services. Other institutional clients, including pension funds and insurance companies, maintain steady growth patterns but face regulatory constraints that limit cross-border investment mandates. The segmentation shift reflects broader financial inclusion initiatives across GCC economies seeking to reduce oil dependency through diversified savings and investment behaviors.

By Provider: Fintech Disruption Challenges Banking Incumbents

Private banks command 42.80% market share in 2025 through established relationship networks and regulatory advantages, yet fintech advisors (under others) surge at 18.70% CAGR as digital-native platforms capture mass-affluent segments. Emirates NBD Private Banking and First Abu Dhabi Bank leverage their domestic market positions and regulatory relationships to maintain HNWI client loyalty, while international players like HSBC and UBS provide cross-border wealth structuring expertise. Traditional private banks benefit from established trust relationships and sophisticated product capabilities, particularly in family office services and alternative investment access. However, these incumbents face margin pressure as clients demand fee transparency and digital service delivery comparable to fintech competitors.

Family offices experience 14.65% CAGR growth as inter-generational wealth transfer accelerates and regulatory frameworks in DIFC and ADGM streamline establishment procedures. The Abu Dhabi Global Market processed 200+ new family office applications in 2024, representing 40% year-over-year growth as wealthy families seek direct investment control and tax optimization structures. Fintech advisors like Sarwa, StashAway, and emerging Islamic robo-platforms capture market share through lower fees, transparent pricing, and Shariah-compliant automated portfolio management. Other providers, including independent asset managers and boutique advisory firms, maintain niche positions but struggle to achieve scale without technology investments or regulatory advantages that larger competitors possess.

Geography Analysis

The Gulf Cooperation Council maintains a 38.90% market share in 2025 through concentrated wealth accumulation and favorable regulatory environments, while North Africa emerges as the fastest-growing region at a 9.85% CAGR, driven by Morocco's millionaire immigration policies and Egypt's banking liberalization. UAE and Saudi Arabia anchor GCC growth through zero-tax residency programs and sovereign wealth diversification mandates that create onshore AUM demand. The Dubai International Financial Centre and Abu Dhabi Global Market provide regulatory frameworks that attract international wealth managers seeking regional expansion platforms. Qatar and Kuwait maintain steady growth patterns supported by hydrocarbon revenues, while Bahrain positions itself as an Islamic finance hub with specialized Shariah-compliant wealth management services.

Morocco's economic liberalization and new residency programs for foreign investors drive North African expansion, with the kingdom attracting over 2,500 millionaire families in 2024. Egypt's banking sector reforms and currency stabilization create opportunities for wealth accumulation among the country's expanding entrepreneurial class, while regulatory frameworks under the Financial Regulatory Authority streamline wealth management licensing. The Levant region faces geopolitical constraints that limit growth potential, while Turkey maintains modest expansion despite economic volatility. Iran and Iraq remain largely excluded from international wealth management networks due to sanctions regimes, though domestic Islamic banking systems serve local high-net-worth populations. North African growth reflects broader economic diversification trends and regulatory modernization efforts that create favorable conditions for wealth management industry development.

Competitive Landscape

The MENA wealth management market is moderately concentrated, with a handful of top providers managing a significant share of the region’s assets. Local leaders such as Emirates NBD Private Banking and First Abu Dhabi Bank maintain their dominance by leveraging strong domestic foundations and favorable regulatory environments. Emirates NBD oversees USD 134 billion in regional assets, benefitting from its position in the UAE and DIFC’s regulatory framework. First Abu Dhabi Bank manages USD 102 billion through its ADGM platform, offering advanced cross-border wealth structuring services. Meanwhile, global firms like HSBC, UBS, and Julius Baer are expanding aggressively in the region to win cross-border advisory mandates and tap into growing private wealth.

Key strategic trends include the establishment of dual operational hubs in Dubai and Riyadh, aimed at serving regional high-net-worth individuals more efficiently. Wealth managers are also increasingly investing in digital platforms to meet the evolving needs of next-generation clients who expect seamless, tech-enabled service delivery. Islamic finance has become a critical differentiator, with both global and regional firms introducing Shariah-compliant offerings to compete more effectively. These strategies reflect a broader shift toward personalization, digital agility, and regulatory alignment across markets. The combination of local expertise and global best practices is shaping the competitive dynamics of the MENA wealth landscape.

White-space opportunities are emerging in underserved segments such as mass-affluent digital advisory, tokenized Islamic investment products, and North African markets undergoing regulatory reforms. Fintech disruptors like Sarwa and StashAway are capturing market share by offering transparent, low-cost, and Shariah-compliant robo-advisory solutions. Traditional banks often struggle to replicate these models without undermining their high-margin, relationship-driven services. Regulatory initiatives such as the DIFC’s sandbox and ADGM’s compliance frameworks are encouraging innovation while offering protective barriers for licensed players. Furthermore, fragmented Shariah interpretations across jurisdictions give an edge to institutions with multi-market regulatory expertise and standardized Islamic finance offerings.

MENA Wealth Management Industry Leaders

Emirates NBD Private Banking

First Abu Dhabi Bank (FAB)

HSBC Global Private Banking

UBS Global Wealth Management

Julius Baer Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Emirates NBD Private Banking launched its tokenized sukuk platform in partnership with DIFC Innovation Hub, enabling fractional ownership of Shariah-compliant bonds with minimum investments of USD 10,000. The platform represents the first regulated tokenized Islamic investment offering in the Middle East and targets mass-affluent investors seeking diversified fixed-income exposure through blockchain-enabled fund structures.

- December 2024: Emirates NBD Private Banking launched its tokenized sukuk platform in partnership with DIFC Innovation Hub, enabling fractional ownership of Shariah-compliant bonds with minimum investments of USD 10,000. The platform represents the first regulated tokenized Islamic investment offering in the Middle East and targets mass-affluent investors seeking diversified fixed-income exposure through blockchain-enabled fund structures.

- November 2024: Emirates NBD Private Banking launched its tokenized sukuk platform in partnership with DIFC Innovation Hub, enabling fractional ownership of Shariah-compliant bonds with minimum investments of USD 10,000. The platform represents the first regulated tokenized Islamic investment offering in the Middle East and targets mass-affluent investors seeking diversified fixed-income exposure through blockchain-enabled fund structures.

- October 2024: Julius Baer Middle East received regulatory approval to expand its Dubai operations with a dedicated family office services division, targeting the growing population of European and Asian millionaires relocating to the UAE. The Swiss private bank invested USD 50 million in regional technology infrastructure and hired 25 relationship managers with multi-lingual capabilities to serve diverse client bases.

MENA Wealth Management Market Report Scope

Wealth management is a type of financial Advisory service. A wealth advisor often works with wealthy people to develop a personalized investment plan to assist them in managing their assets. Additionally, thorough financial counseling, tax advice, estate planning, and even legal support are typically included in wealth management. A complete background analysis of the MENA Wealth Management Market, including the assessment of the economy, market overview, market size estimation for critical segments and emerging trends in the market, market dynamics, and key company profiles, are covered in the report. The MENA Wealth Management Market is segmented by client type (HNWI, Retail/ Individuals, Mass Affluent, and others), by provider (Private Bankers, Fintech Advisors, Family Offices, and others), and by geography (Saudi Arabia, Algeria, Egypt, United Arab Emirates, and Other Countries).

By Client Type

| HNWI |

| Retail / Individuals |

| Other Client Types (Pension Funds, Insurers, etc.) |

By Provider

| Private Banks |

| Family Offices |

| Others (Independent/External Asset Managers) |

| By Client Type | HNWI |

| Retail / Individuals | |

| Other Client Types (Pension Funds, Insurers, etc.) | |

| By Provider | Private Banks |

| Family Offices | |

| Others (Independent/External Asset Managers) |

Key Questions Answered in the Report

What is the current value of the MENA wealth management market?

The market stands at USD 0.98 trillion in 2026.

How fast is the market projected to grow?

It is expected to increase to USD 1.36 trillion by 2031 at a 6.72% CAGR.

Which client segment is expanding the quickest?

Retail investors lead growth at a 11.78% CAGR through 2031.

Which provider type shows the highest growth rate?

Fintech advisors are expanding at 18.70% CAGR by leveraging digital Shariah-compliant solutions.

Which geography is forecast to be the fastest-growing?

North Africa is projected to grow at a 9.85% CAGR to 2031.

What recent move highlights tokenization in the region?

In Jan 2025 Emirates NBD introduced a regulated tokenized sukuk platform through DIFC.

Page last updated on: