Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

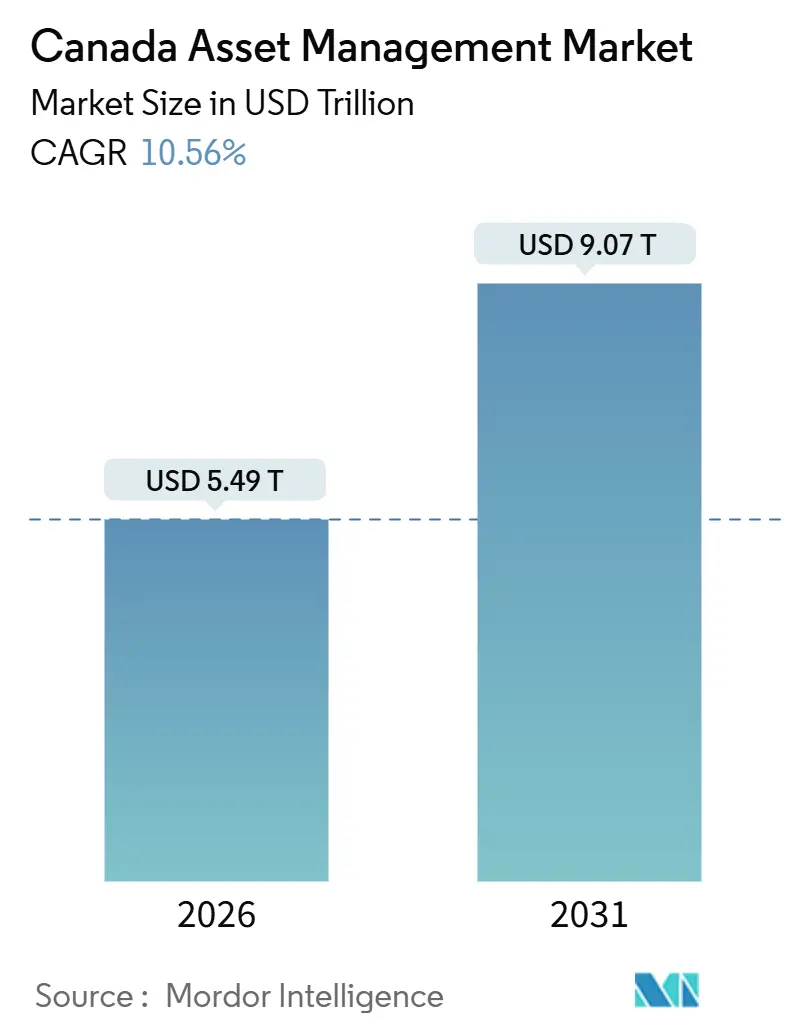

| Market Size (2026) | USD 5.49 Trillion |

| Market Size (2031) | USD 9.07 Trillion |

| Growth Rate (2026 - 2031) | 10.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Asset Management Market Analysis by Mordor Intelligence

The Canada asset management market size is USD 5.49 trillion in 2026 and is projected to reach USD 9.07 trillion by 2031 at a 10.56% CAGR. The expansion aligns with rising household net worth, which increased through Q3 2025, and with deeper penetration of investment vehicles across both retail and institutional channels.[1] Strong equity market performance in 2025 lifted portfolio values and supported flows into listed products such as ETFs, while money market funds benefited from higher short-term rates that improved cash yields. Regulatory modernization and supervisory focus on risk management have increased emphasis on liquidity, disclosure, and climate-related governance, shaping product design and asset allocation across the Canada asset management market. Digital access points, especially broker-led and advisor-integrated platforms, continue to broaden participation and lower friction for investors across age cohorts in the Canada asset management market.

Key Report Takeaways

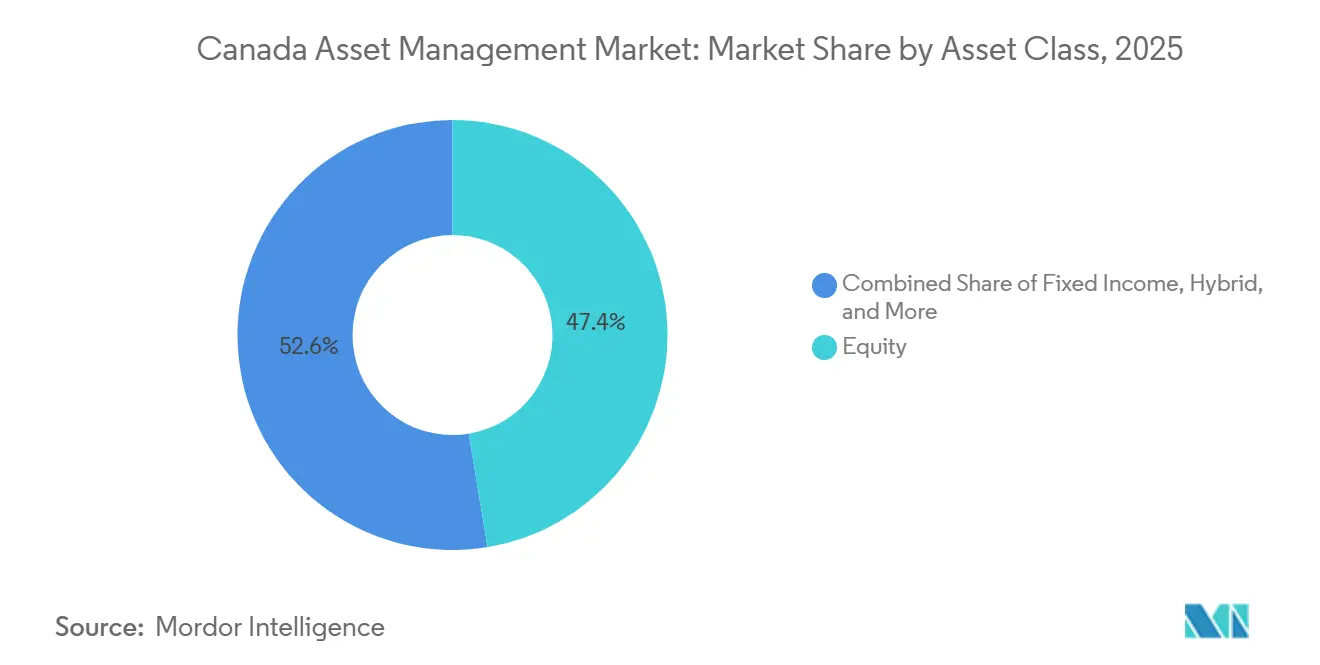

- By asset class, equity held the largest share at 47.39% of the Canada asset management market share in 2025, while alternatives are projected to record the fastest growth at 11.72% CAGR through 2031.

- By source of funds, pension funds and insurance companies accounted for 39.39% of the Canada asset management market share in 2025, while individual investors are forecasted to grow the fastest at 13.24% CAGR to 2031.

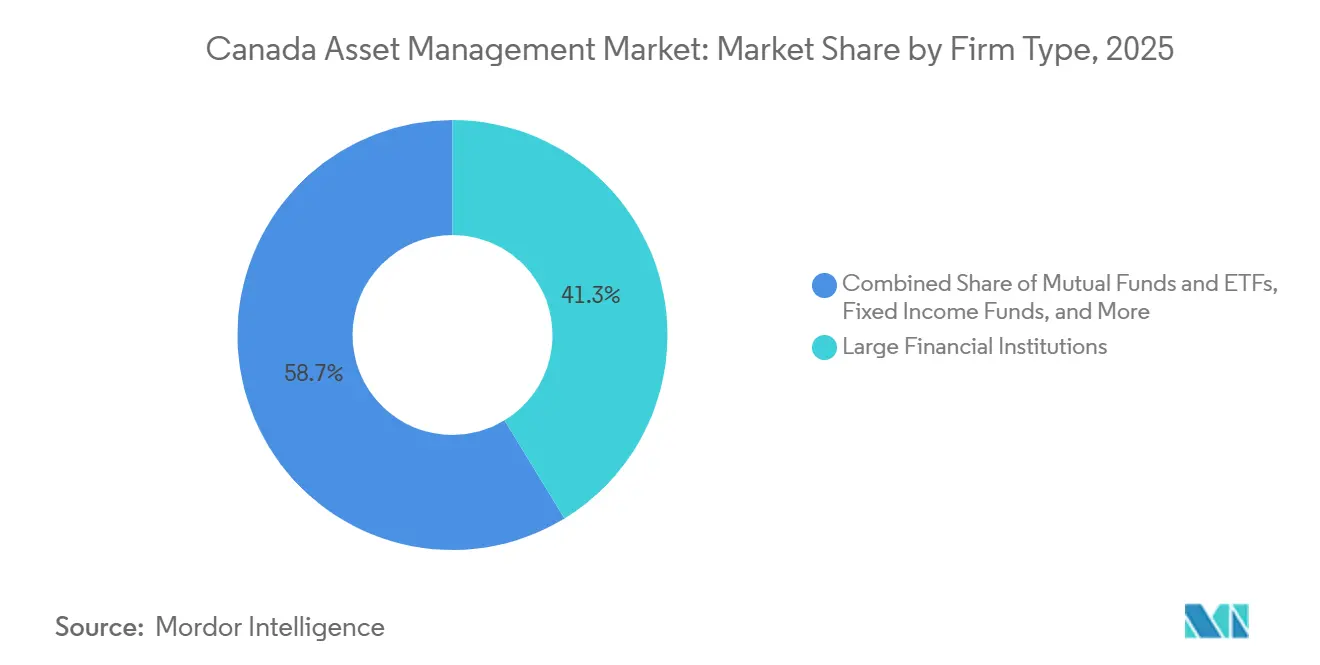

- By firm type, large financial institutions commanded 41.28% of the Canada asset management market share in 2025, while digital-only ETF platforms are expected to expand at a 15.36% CAGR through 2031.

- By geography, Ontario led with 49.39% of the Canada asset management market share in 2025, while British Columbia is projected to advance at 11.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from DB to DC pension plans | +1.8% | National, strongest in Ontario and Alberta (private sector concentration) | Medium term (2-4 years) |

| Growing adoption of low-fee passive & ETF products | +2.3% | National, with early gains in Ontario, British Columbia | Short term (≤ 2 years) |

| Rising demand for ESG & impact-focused mandates | +1.4% | National, led by Quebec (La Caisse), Ontario (major pensions) | Long term (≥ 4 years) |

| AI-driven portfolio analytics improving alpha generation | +1.2% | National, concentrated in Toronto (RBC, TD), Calgary (AIMCo) | Long term (≥ 4 years) |

| Consolidation of provincial pension funds (e.g., AIMCo expansion) | +0.9% | Alberta-centric, spillover to British Columbia, Saskatchewan | Medium term (2-4 years) |

| Digital-only neo-brokers are broadening retail participation | +2.6% | National, strongest penetration in Ontario, British Columbia, among the under-40 cohort | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift from Defined Benefit to Defined Contribution Pension Plans Propelling Asset Growth

Shifts in retirement plan structures are expanding the investable base in the Canada asset management market, as defined contribution membership has grown faster than defined benefit membership across the private sector. Statistics Canada’s most recent pension survey confirms that plan membership continues to rise nationally, with the mix evolving toward plans that rely on participant-level investment decisions and diversified fund menus. This evolution channels ongoing contributions to pooled strategies and multi-asset defaults offered through employer plans, strengthening recurring flows into core equity and fixed-income vehicles managed by leading firms in the Canada asset management market. Large institutions continue to steward defined benefit pools, but the increased prevalence of defined contribution plans widens the addressable retail and advisory segments that select mutual funds and ETFs as core allocations. Regulatory work on climate and risk management, including expectations for decision-useful climate disclosures by federally regulated financial institutions, is reinforcing a trend toward systematic oversight of investment risks that influences asset selection within retirement programs.

Growing Adoption of Low-Fee Passive and ETF Products Driving Market Democratization

Low fees and scalable wrappers are accelerating asset capture across the Canada asset management market as investors respond to improved transparency and convenience. ETF activity and listings have increased on Canadian exchanges, and trading value remained elevated through 2024 and 2025 as providers pushed new launches into both passive and active categories to meet income, equity, and cash management goals. The combination of bank-affiliated ETF platforms and global managers has driven economies of scale, with RBC iShares growing assets and retaining a leading share of the Canadian ETF segment within an integrated distribution ecosystem. Providers continue to enhance ETF lineups with balanced, dividend, and systematic tilts that offer predictable pricing and simple access, as reflected by multi-asset and rotation strategies launched in 2025.[2]Mackenzie Investments, “2025 ETF year in review: Active ETFs take the lead,” Mackenzie Investments, mackenzieinvestments.com The net result is greater accessibility for cost-conscious investors, which supports asset growth across passive products and reinforces fee-based advisory models in the Canada asset management market.

Rising Demand for ESG and Impact-Focused Mandates Reshaping Product Development

Sustainability policies and evolving disclosure standards are standardizing expectations for climate and ESG data in the Canada asset management market. Federal guidance on sustainable investment, paired with work by securities regulators to calibrate climate-related reporting, is prompting asset managers to refine frameworks and align product labelling with credible, verifiable claims. The Canadian Securities Administrators updated the market in April 2025 on the approach to climate and diversity disclosure projects, signalling that issuers should consider voluntary Canadian sustainability standards in the interim while policy development continues.[3]Canadian Securities Administrators, “CSA updates market on approach to climate-related and diversity-related disclosure projects,” CSA, securities-administrators.ca Major institutional allocators in Quebec and Ontario maintain visible climate strategies, with CDPQ reporting robust progress on portfolio decarbonization and long-term green asset targets, reinforcing the momentum behind sustainable mandates. These policy and institutional signals influence asset selection across equities, fixed income, and private markets in the Canada asset management market, and they support the integration of ESG data into mainstream risk processes. They also steer the development of labelled strategies and stewardship practices that align with long-term capital allocation goals in core pension and retail channels.

AI-Driven Portfolio Analytics Improving Alpha Generation and Operational Efficiency

Artificial intelligence is enhancing research, risk oversight, and client engagement across the Canada asset management market. The Bank of Canada has adopted AI to support forecasting, sentiment analysis, and data cleaning, reflecting the broader institutionalization of AI in financial analysis and policy work. Supervisors are advancing a dialogue on AI-related systemic risks, with OSFI highlighting autonomous systems, third-party concentration, and governance needs as priorities for collaboration with industry. Leading institutions are targeting measurable value from AI through fraud detection, credit decisioning, and personalized insights, while also investing in platform capabilities that can scale across wealth and capital markets businesses. These applications contribute to improved alpha generation, more precise risk limits, and streamlined operations in the Canada asset management market. They also elevate expectations for data governance and transparency to meet supervisory standards and investor trust thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression is squeezing margins | -2.1% | National, most acute in passive equity and fixed-income segments | Short term (≤ 2 years) |

| An aging population is lowering household risk appetite | -1.3% | National, with a concentration in the Atlantic Canada provinces | Long term (≥ 4 years) |

| High concentration of distribution through bank branches | -0.8% | National, legacy channel dominance in Quebec, rural areas | Medium term (2-4 years) |

| Heightened OSFI liquidity-stress rules | -1.0% | National, federally regulated plans spill over to provincial jurisdictions. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fee Compression Squeezing Margins Across Traditional Product Lines

Price competition continues to weigh on profit pools in traditional strategies as investors migrate to low-cost vehicles. Providers have launched fee-conscious multi-asset products to support advice-led models, adding mutual fund versions of proven ETF portfolios to meet advisor preferences on account administration and billing in the Canada asset management market. Large banks have also reduced management fees across select fixed income and equity funds to defend share and respond to evolving cost expectations. Enhanced total cost reporting and fee transparency under evolving rules will make headline pricing more visible and will likely reinforce migration to lower-cost wrappers in the Canada asset management market. Budget 2025 proposed a prohibition on account transfer fees, which, if implemented, will further reduce friction for investors to move assets toward lower-cost providers. These trends collectively pressure margins for managers without scale or differentiated capabilities in alpha, solutions, or private markets.

Aging Population, Lowering Household Risk Appetite, and Shifting Demand Toward Guaranteed Products

Demographics are shifting risk preferences toward income and capital preservation, which shapes asset allocation choices in the Canada asset management market. The Old Age Security maximum benefit levels in early 2026 reflect the growing fiscal footprint of retirement programs and the need for predictable income solutions as longevity improves. The 32nd Actuarial Report on the Canada Pension Plan highlights how funding status is sensitive to return assumptions, underscoring the importance of prudent risk management for long-term sustainability. Distribution of wealth across cohorts shows older households hold a large share of financial assets, which supports demand for fixed-income, dividend, and insurance-linked solutions in the Canada asset management market. Providers are scaling products that blend market exposure with guarantees, including segregated fund structures with principal protection features for decumulation needs. This demand profile moderates equity risk-taking and strengthens flows into lower-volatility strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Equity Leadership Challenged by Surging Alternative Allocations

Equity investments held the largest slice at 47.39% of the Canada asset management market share in 2025, supported by a strong domestic equity rally and risk-on sentiment. The S&P/TSX Composite delivered a 2025 surge and hit new valuation highs, which buoyed portfolio values and lifted flows into listed strategies in the Canada asset management market. Bond markets stabilized with tighter spreads into late 2025, and investors rotated toward income solutions that preserved capital while maintaining upside convexity where possible. Alternative assets are positioned as the fastest-growing class at 11.72% CAGR, reflecting institutional demand for private equity, infrastructure, and real assets to diversify public market volatility within the Canada asset management market. Within cash management, policy rate dynamics encouraged the use of money market mutual funds and high-interest ETFs as tools for liquidity management.

In 2025, product development targeted systematic responses to the cycle and enhanced income, including tilt-based ETFs and covered call strategies that help meet yield targets while managing total return variability. Managers brought new rotation tools that adjust exposures as macro conditions evolve, allowing advisors to implement disciplined allocation frameworks in the Canada asset management market. Providers also scaled multi-asset wrappers that package equity and fixed income with transparent fees and simple rebalancing rules, reinforcing the operational advantages of ETFs and related mutual fund clones. In alternatives, institutional allocators added exposure across private credit and infrastructure to complement public fixed income, and returns from real estate varied by segment, with office still weighing on performance in 2024. These dynamics kept the Canada asset management market focused on outcome-oriented portfolio construction that balances equity growth with income, diversification, and capital preservation.

By Source of Funds: Individual Investors Surging as Digital Access Expands Retail Reach

Pension funds and insurance companies accounted for the largest pool at 39.39% in 2025, reflecting the scale of national plans and public-sector sponsors that underpin stable allocations across asset classes in the Canada asset management market. The Canada Pension Plan reported net assets of 714.4 billion at fiscal 2025 year-end with a 9.3% net annual return, illustrating the significant anchor role of national retirement savings in investment flows [4]CPP Investments, “CPP Investments Net Assets Total $714.4 Billion at 2025 Fiscal Year End,” CPP Investments, cppinvestments.com, and it maintained a strong funded status while recording a solid 2024 investment return, reinforcing the stability of large defined benefit plans in supporting capital markets and fixed-income liquidity in Canada. Alberta’s AIMCo generated a double-digit balanced return in 2024, supported by equities and private markets, which highlights the role of provincial consolidators in deploying long-dated capital within the Canada asset management market. These institutional sources provide multi-decade horizons that complement more tactical retail flows and expand demand for alternative assets and solutions strategies.

Individual investors are the fastest-growing source at 13.24% CAGR, supported by digital platforms, low-cost product access, and advisor-integrated solutions that simplify onboarding and portfolio construction in the Canada asset management market. Direct investing businesses within large banks are scaling clients and assets while benefiting from internal referrals and integrated mobile experiences that serve younger savers and self-directed investors. Regulatory changes that lower switching costs, such as the proposed prohibition on account transfer fees, can further support competition and accelerate asset movement to low-cost channels. This environment is also expanding the use of ETFs and model portfolios in advisory practices, which firms are aligning with household goals across tax-advantaged accounts in the Canada asset management market. Over time, digital adoption and hybrid advice should sustain retail contributions while institutional allocations continue to drive the asset base.

By Firm Type: Large Institutions Defending Share Amid Digital Platform Disruption

Large financial institutions and bulge-bracket banks controlled 41.28% in 2025, leveraging scale, technology, and distribution to retain leadership in the Canada asset management market. RBC iShares held a leading share of the Canadian ETF landscape while RBC’s wealth platform continued to expand assets and direct investing penetration through cross-sell across a huge retail customer base. TD Asset Management broadened its lineup with a Global Private Credit Strategy and introduced advisor series capabilities for ETF portfolios to deepen penetration in fee-based advice models. Managers launched new ETFs with systematic tilts and dividend focus to match demand for income and diversification in the Canada asset management market. Fidelity expanded with global small-mid cap equity and its first multi-strategy liquid alternative to broaden the solution set for risk-managed equity exposure.

Digital-only ETF platforms are projected to be the fastest-growing firm type at 15.36% CAGR as self-directed and hybrid advisory models scale in the Canada asset management market. Bank-owned direct investing arms continue to add tools, education, and research access for DIY clients while keeping a pathway to full-service advice for complex needs. Fee reductions across select fund families illustrate ongoing competition to serve price-sensitive investors and to match the low-cost expectations set by ETFs. In private markets access, regulatory innovation is opening channels for retail to participate in long-term asset vehicles under new oversight arrangements, which will influence how firms structure products and education in the Canada asset management market. The overall result is a landscape where scaled incumbents defend share through technology, pricing, and product breadth, while digital-first challengers shape user experience standards.

Geography Analysis

Ontario accounted for 49.39% in 2025, reflecting Toronto’s role as the financial nerve centre for exchanges, banks, and large institutional allocators in the Canada asset management market. Exchange statistics show elevated ETF trading value and a healthy pace of new listings, which support liquidity and innovation for product issuers and advisors across the province. Pension membership gains in 2023 were strongest in Ontario in absolute terms, which expands the base of long-term savers participating in professionally managed vehicles. The Ontario Securities Commission has advanced work to expand retail access to long-term assets through a regulatory sandbox, which may broaden alternatives participation in the Canada asset management market. Large Ontario-based plans maintained strong funded positions into 2025 while contributing to domestic market liquidity through sizeable government bond holdings and multi-asset portfolios.

Quebec represents the second-largest provincial base, anchored by CDPQ and a deep cooperative network that powers product manufacturing and distribution in the Canada asset management market. CDPQ reported net assets of 473.3 billion as of December 2024 and continued to invest across Quebec with a sustained focus on infrastructure, growth capital, and sustainable finance. The province’s regulatory framework is modernizing, with Bill 92 setting the path to harmonize mutual fund representative oversight with CIRO while enhancing enforcement tools at the AMF and the Financial Markets Administrative Tribunal. Desjardins agreed to acquire Guardian Capital Group in a transaction expected to close in early 2026, creating a combined platform of meaningful scale to compete nationally and internationally within the Canada asset management market. Provincial funds and government vehicles, such as Quebec’s Generations Fund, further shape the investment landscape by sustaining long-term capital deployment to lower funding costs.

British Columbia is projected to be the fastest-growing region at 11.38% CAGR through 2031, supported by technology entrepreneurship, immigration-led population gains, and resource-linked investment opportunities that align with decarbonization goals in the Canada asset management market. Pension membership increased in 2023, which adds to the pool of long-term savers who contribute through workplace plans and personal accounts. The Rest of Canada includes Alberta, Saskatchewan, Manitoba, and the Atlantic provinces, with region-specific drivers such as energy exposure, infrastructure needs, and demographic profiles shaping product demand and allocation. Alberta’s institutional ecosystem, including AIMCo’s management of public-sector assets, remains a significant node for public markets and private asset investment in the Canada asset management market. Ongoing legislative changes around pension governance in Alberta will influence how stakeholders evaluate risk and legal protections for asset owners and beneficiaries.

Competitive Landscape

Innovation and Adaptation Drive Future Success

The Canada asset management market features a moderate level of concentration, with large bank-owned platforms holding a majority of retail assets through integrated models that link banking, wealth, and capital markets. RBC maintains leadership positions across mutual funds and ETFs through RBC iShares and a broad advice and direct investing footprint that spans millions of retail clients. TD Asset Management has expanded into private credit and refined fee schedules to remain competitive in core fixed income and equity categories for advisors and institutions. Product sponsors continue to bring systematic ETFs and liquid alternative wrappers to market, which deepens the menu available to advisors seeking income, diversification, or volatility management in the Canada asset management market.

Competitive strategy centres on three themes. First, fee alignment with investor expectations, including reductions in fund management fees at bank-owned complexes, keeps pressure on pricing while preserving shelf breadth in the Canada asset management market. Second, product innovation in higher-value segments such as active ETFs, private markets access funds, and liquid alternatives expands solutions tailored to specific outcomes or risk tolerances. Third, digital distribution and hybrid advice enhance user experience and broaden the funnel for retail participation while preserving pathways to more comprehensive planning as needs become complex in the Canada asset management market. Platform investments in AI and analytics underpin these strategies by improving research, risk, and client personalization.

Mergers and acquisitions are reshaping competitive positions. CI Financial entered into a take-private transaction with Mubadala Capital in August 2025, providing scale capital and strategic flexibility to pursue growth in Canada and the United States. Desjardins’ agreement to acquire Guardian Capital Group is expected to create a larger manager with diversified capabilities and distribution reach in 2026, strengthening competition in Quebec and nationally in the Canada asset management market. New listings and product types, including a Bitcoin ETF listed on Cboe Canada, signal ongoing expansion of accessible exposures through regulated vehicles that fit within advisor and retail workflows. Infrastructure improvements at the exchange group level, including post-trade modernization initiatives, support efficient settlement and market plumbing for growing ETF and equity activity in the Canada asset management market.

Canada Asset Management Industry Leaders

RBC Global Asset Management

TD Asset Management

BlackRock Asset Management Canada

BMO Global Asset Management

CI Global Asset Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: TD Asset Management introduced a Global Private Credit Strategy and added an Advisor Series for MAP ETF Portfolios to broaden access to private credit within advice-led channels.

- November 2025: Manulife Canada expanded its segregated fund lineup with four index funds managed by BlackRock, combining broad market exposures with insurance features aimed at income and estate planning.

- October 2025: Mackenzie Investments and Northleaf launched a multi-asset private markets fund for accredited investors, offering diversified exposure to private equity, private credit, and infrastructure.

- October 2025: Fidelity Investments Canada launched the Fidelity Global Small-Mid Cap Equity Fund and ETF Series and introduced its first multi-strategy liquid alternative equity fund with an ETF series.

Canada Asset Management Market Report Scope

Asset management is one of the most widely demanded markets as people are adopting digitalization. A complete background analysis of the Canadian asset management market includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles in the report.

The Canadian asset management market is segmented by asset class (equity, fixed income, alternative investment, hybrid, cash management), source of funds (pension funds and insurance companies), individual investors (retail+ high net worth clients), corporate investors, other sources (government, trust funds, and others), and type of asset management firms (large financial institutions/bulge bracket banks, mutual funds and ETFs, private equity and venture capital, fixed income funds, hedge funds, and other types).

The report offers market sizes and forecasts in value (USD) for all the above segments.

By Asset Class

| Equity |

| Fixed Income |

| Alternative Investment |

| Hybrid |

| Cash Management |

By Source of Funds

| Pension Funds and Insurance Companies |

| Individual Investors (Retail + High Net Worth Clients) |

| Corporate Investors |

| Other Sources (Government, Trusts, Others) |

By Type of Asset Management Firms

| Large Financial Institutions / Bulge-Bracket Banks |

| Mutual Funds and ETFs |

| Private Equity and Venture Capital |

| Fixed Income Funds |

| Hedge Funds |

| Other Types of Asset Management Firms |

By Geography

| Ontario |

| Quebec |

| British Columbia |

| Atlantic Canada |

| Rest of Canada |

| By Asset Class | Equity |

| Fixed Income | |

| Alternative Investment | |

| Hybrid | |

| Cash Management | |

| By Source of Funds | Pension Funds and Insurance Companies |

| Individual Investors (Retail + High Net Worth Clients) | |

| Corporate Investors | |

| Other Sources (Government, Trusts, Others) | |

| By Type of Asset Management Firms | Large Financial Institutions / Bulge-Bracket Banks |

| Mutual Funds and ETFs | |

| Private Equity and Venture Capital | |

| Fixed Income Funds | |

| Hedge Funds | |

| Other Types of Asset Management Firms | |

| By Geography | Ontario |

| Quebec | |

| British Columbia | |

| Atlantic Canada | |

| Rest of Canada |

Key Questions Answered in the Report

Which asset class leads and which is growing the fastest in the Canada asset management market?

Equity leads with a 47.39% share in 2025, while alternatives are projected to grow the fastest at 11.72% CAGR through 2031.

Who are the primary funding sources in the Canada asset management market?

Pension funds and insurance companies represent the largest pool at 39.39% in 2025, while individual investors are the fastest-growing source at 13.24% CAGR to 2031.

Which province has the largest share in the Canada asset management market?

Ontario holds the largest share at 49.39% in 2025, supported by Toronto’s exchange activity, bank headquarters, and large pensions.

What themes define competition in the Canada asset management market?

Scale pricing, product innovation in ETFs and alternatives, and digital distribution define competition, with banks defending share while digital-first platforms expand.

Page last updated on: