Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

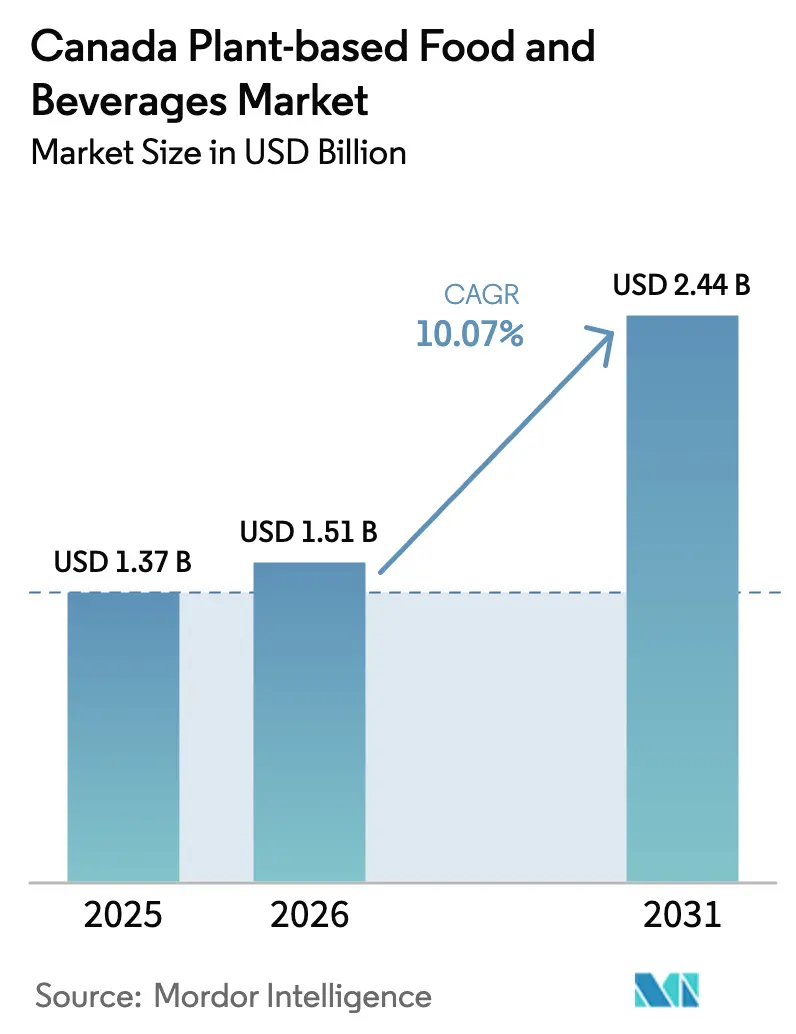

| Base Year Market Size (2025) | USD 1.37 Billion |

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 10.07% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Plant-based Food And Beverages Market Analysis by Mordor Intelligence

The Canada Plant-based Food and Beverages Market size was valued at USD 1.37 billion in 2025 and estimated to grow from USD 1.51 billion in 2026 to reach USD 2.44 billion by 2031, at a CAGR of 10.07% during the forecast period (2026-2031). The market expansion is primarily attributed to the transformation in consumer dietary preferences, heightened health consciousness, and increasing environmental awareness among the Canadian population. Canadian consumers are demonstrating a significant shift toward plant-based alternatives through the systematic adoption of flexitarian dietary patterns. Environmental considerations, particularly regarding the substantial impact of animal agriculture on climate change, have intensified consumer demand for sustainable food alternatives. The market development is facilitated by enhanced retail distribution networks, optimized e-commerce accessibility, and strategic product positioning that emphasizes clean labels, protein content, and allergen-free attributes. Furthermore, governmental policy support, advancements in domestic ingredient innovation, and substantial investments in research and development and processing infrastructure continue to strengthen the industry framework. In conclusion, the Canadian plant-based food and beverages market has successfully transitioned from a specialized segment to a mainstream category, signifying a fundamental transformation in consumer food preferences and establishing a robust foundation for sustained market growth.

Key Report Takeaways

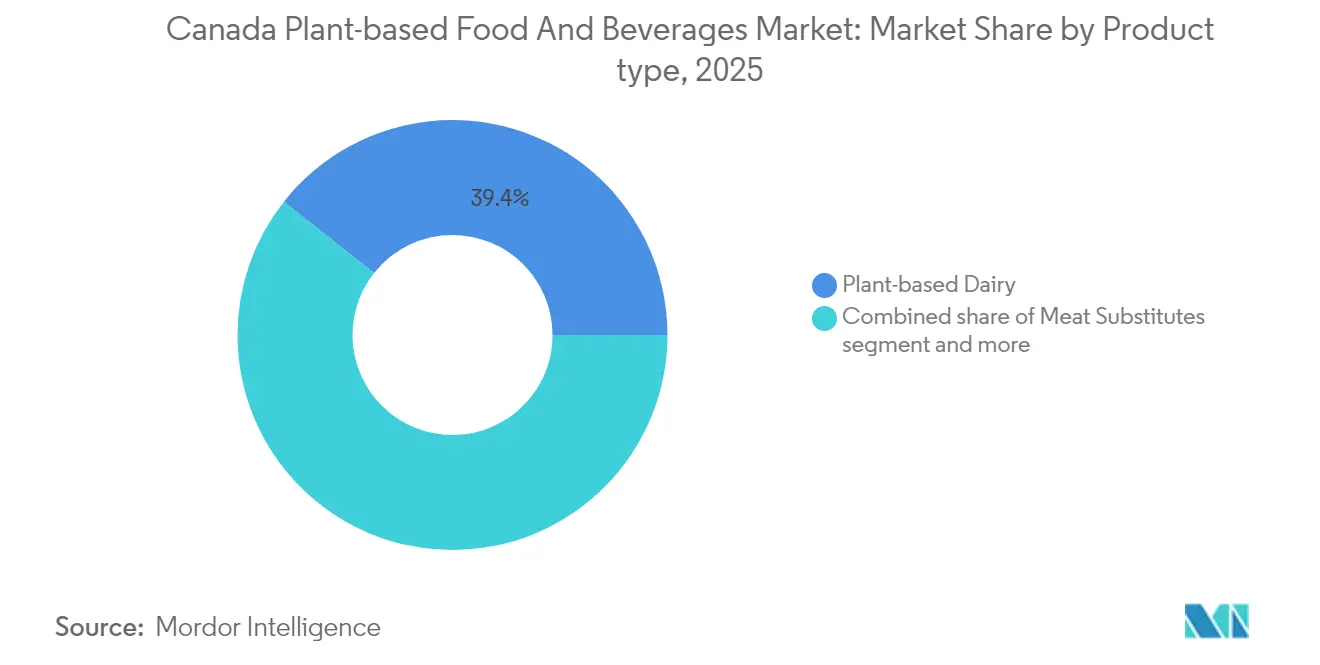

- By type, plant-based dairy led with a 39.35% revenue share in 2025; meat substitutes are on track to post a 13.21% CAGR through 2031.

- By ingredient source, soy captured 30.18% of the Canadian plant-based food market share in 2025, while oat is projected to expand at a 12.03% CAGR.

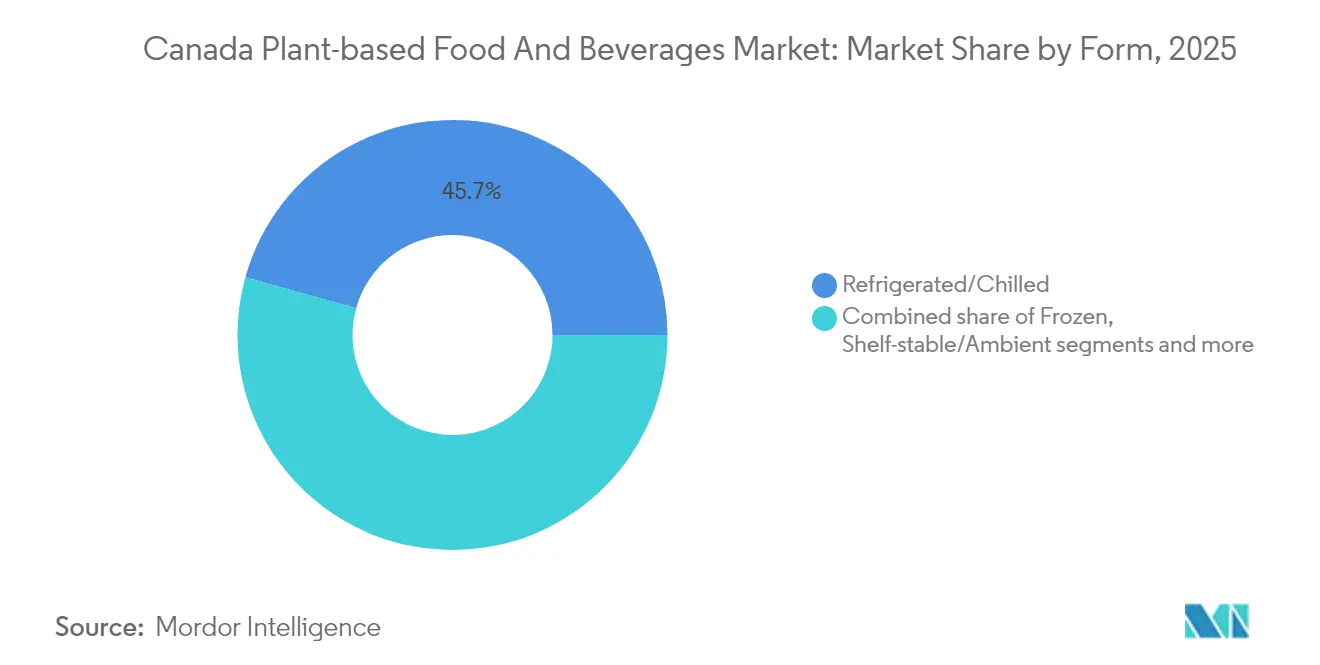

- By form, refrigerated/chilled products accounted for a 45.68% share of the Canada plant-based food market size in 2025, while frozen are advancing at an 11.49% CAGR.

- By distribution channel, off-trade outlets held 77.93% of the Canadian plant-based food market size in 2025, whereas on-trade channels are forecast to grow at an 11.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Plant-based Food And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing vegan and flexitarian populations | +2.1% | National, with higher concentration in urban centers | Medium term (2-4 years) |

| Retail expansion and product availability | +1.8% | National, with stronger impact in Ontario and Quebec | Short term (≤ 2 years) |

| Innovations in plant-based product offerings | +2.3% | National, led by Research and Development hubs in Ontario and British Columbia | Long term (≥ 4 years) |

| Sustainability and environmental concerns | +1.9% | National, with stronger resonance in British Columbia and Quebec | Medium term (2-4 years) |

| Rising allergen concerns | +1.2% | National, with particular relevance in urban markets | Short term (≤ 2 years) |

| Government support and health guidelines | +1.4% | National, with provincial variations in implementation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Vegan and Flexitarian Populations

The Canadian market is experiencing a significant demographic transformation as consumers increasingly adopt plant-based and flexitarian dietary patterns. According to Statistics Canada, in 2023, the country had 2.3 million vegetarians and 850,000 vegans [1]Source: Made in CA, “Veganism and Vegetarianism Statistics in Canada,”madeinca.ca. This dietary shift extends across multiple age demographics, with millennials and Baby Boomers demonstrating substantial engagement in plant-based product trials and repeat purchases. Female consumers are emerging as primary decision-makers in household purchasing, particularly in the selection of plant-based protein alternatives. Statistics Canada's 2024 health data indicates that declining life satisfaction correlates with increased health consciousness, leading consumers to seek dietary options that address both wellness and environmental concerns. This evolving consumer behavior indicates a sustained growth trajectory for the plant-based food and beverage market in Canada, with manufacturers adapting their product portfolios to meet these changing dietary preferences.

Retail Expansion and Product Availability

Major Canadian retailers are implementing systematic plant-based category expansions, with Loblaw Companies leading through its Canadian-first sourcing strategy that prioritizes local plant-based manufacturers to mitigate tariff impacts while supporting domestic innovation. Retail penetration is accelerating through strategic partnerships between Canadian plant-based manufacturers and major grocery chains, creating distribution efficiencies that reduce consumer acquisition costs while improving product accessibility across urban and rural markets. The implementation of the Grocery Code of Conduct, fully operational by January 2026, is establishing transparent supply chain practices that benefit plant-based producers through improved negotiating positions with major retailers. This regulatory framework is particularly advantageous for smaller plant-based companies that previously faced barriers to securing premium shelf placement, creating a more level competitive environment that encourages innovation and consumer choice expansion.

Innovations in Plant-based Product Offerings

Technological advancements in plant-based food and beverage processing have significantly improved product quality and consumer acceptance in the Canadian market. For instance, in June 2025, New School Foods Inc. developed a patented directional freezing technology that created meat-like textures through controlled ice crystal formation. The company secured USD 18 million in funding and established nationwide distribution agreements with Gordon Food Service and Bondi Produce, demonstrating market confidence in processing technologies that addressed texture and mouthfeel challenges. Moreover, in March 2024, the Canadian Food Innovation Network invested USD 464,518 in six foodtech projects, including ProFillet's plant-based fish alternatives, indicating sustained innovation across protein categories beyond conventional meat and dairy substitutes. These technological developments and investments strengthened Canada's plant-based food and beverage market, enabling manufacturers to overcome traditional product quality challenges while aligning with evolving consumer preferences and dietary requirements.

Sustainability and Environmental Concerns

Environmental regulations are transforming the plant-based food and beverage industry in Canada. For instance, in November 2023, the Canadian Government introduced Bill C-59, which requires scientific evidence for environmental claims and imposes penalties of up to CAD 10 million for non-compliance. The legislation requires plant-based manufacturers to conduct life-cycle assessments and document carbon footprints. Companies that demonstrate verified sustainable operations gain competitive advantages in the market. SunOpta exemplifies this regulatory compliance by providing quantified environmental impact data to support its claims about the lower carbon footprint of plant-based beverages compared to dairy products. The Clean Electricity Regulations, which mandate net-zero emissions by 2050, are driving food manufacturers to adopt renewable energy sources. Plant-based producers have an inherent advantage in this transition due to their lower energy requirements compared to traditional animal agriculture operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost inflation of pulse and oilseed inputs | -1.7% | National, with stronger impact on Prairie provinces | Short term (≤ 2 years) |

| Consumer perception of ultra-processing and additives | -1.1% | National, with higher impact in health-conscious urban markets | Medium term (2-4 years) |

| Allergen and ingredient sensitivities | -1.0% | National, with higher impact in allergy-prone demographics | Medium term (2-4 years) |

| Taste and texture barriers | -1.1% | National, with stronger impact among traditional meat consumers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost Inflation of Pulse and Oilseed Inputs

The Canadian plant-based food and beverage manufacturing market confronts substantial operational constraints due to persistent inflation in agricultural input costs, particularly in pulse and oilseed commodities. Global supply chain disruptions and climate-related yield variations have resulted in significant production cost increases throughout the value chain. This financial pressure is demonstrated by Merit Functional Foods' Winnipeg plant, which entered receivership and underwent subsequent sale despite receiving CAD 100 million in government investment. While the lentil cultivation area expanded by 14.8% to 4.2 million acres in 2024, predominantly in Saskatchewan, manufacturers continue to experience severe margin compression due to elevated fertilizer and energy costs, according to Statistics Canada [2]Source: Canada Statistics, "Tofu and lentils", statcan.gc.ca. These sustained cost pressures constitute a fundamental market restraint, adversely affecting operational viability and deterring capital investments in the Canadian plant-based food and beverage manufacturing industry.

Consumer Perception of Ultra-processing and Additives

Growing consumer awareness of ultra-processed foods and artificial additives has intensified scrutiny of ingredient lists and processing methods in the Canadian plant-based food and beverage market. This shift in consumer behavior has compelled manufacturers to adopt natural ingredients and advanced processing technologies that minimize artificial interventions. The Canadian Food Inspection Agency's proposed guidance on plant-based egg alternative labeling demonstrates increased regulatory emphasis on transparency, particularly regarding processing methods and ingredient authenticity. Health Canada's modernized food additive regulations have streamlined approval processes while heightening consumer consciousness about processing aids and functional ingredients in plant-based formulations. The agency's stringent requirements for scientific validation of health claims have necessitated manufacturer investment in clinical studies and nutritional research, increasing development costs but reinforcing product credibility in a market where consumers increasingly prioritize minimally processed, clean-label options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product type: Dairy Alternatives Drive Market Leadership

Plant-based dairy products maintain a dominant market position with a 39.35% share in 2025, primarily attributed to their superior performance in applications such as coffee beverages and cereal consumption. The reduction in organoleptic differences between plant-based and conventional dairy products through technological advancement has reinforced this market position. This advancement is exemplified by Aiya Foods' July 2023 product launch, where the company introduced Goat Cheeze Flavour Crumbles and Feta Cheeze Flavour Crumbles. These products, manufactured utilizing oat flour, demonstrate the industry's capability to deliver optimal texture and creaminess comparable to traditional dairy products, addressing consumer demands for authentic taste experiences.

The meat substitute segment demonstrates substantial growth potential with a projected CAGR of 13.21% through 2031, representing the highest growth rate within plant-based categories. This expansion is facilitated by significant advancements in texture and flavor replication technologies. Plant-based nutrition and snack bars have established a strong market presence among health-conscious consumers seeking efficient protein delivery systems, while bakery products incorporate plant-based formulations to address allergen sensitivity requirements. The beverage category exhibits notable growth in alternative milk products, particularly oat-based formulations, which demonstrate superior functional properties including enhanced frothing capabilities and neutral organoleptic profiles. The strategic expansion of plant-based coffee and tea products through foodservice collaborations has facilitated increased consumption opportunities beyond residential applications, contributing to sustained market expansion.

By Ingredient Source: Soy Leadership Challenged by Oat Innovation

Soy maintains market predominance with a 30.18% market share in 2025. Canadian soybean production demonstrated an 8.4% increase to 7.6 million tonnes in 2024, with Ontario contributing 4.4 million tonnes, according to Canada Statistics . This substantial domestic supply enables plant-based manufacturers to minimize import dependency and operational transportation costs. Manufacturing entities are implementing strategic ingredient source diversification to mitigate supply chain risks and reduce reliance on single protein sources, while addressing documented consumer concerns regarding soy's phytoestrogen content and potential allergenicity.

Oat has established itself as the fastest-growing ingredient source, demonstrating a 12.03% CAGR through 2031, primarily influenced by consumer preferences for allergen-free alternatives with enhanced functional properties. The significant adoption of oat-based ingredients is attributed to their neutral organoleptic profile and superior processing characteristics in dairy alternative applications, particularly in coffee-based beverages, where emulsion stability and frothing performance approximate dairy milk standards. Protein Industries Canada's USD 4.5 million investment in July 2024 in crop quality prediction technologies aims to enhance consistency in protein crop supplies, providing substantial benefits to manufacturers requiring precise ingredient specifications.

By Form: Convenience Drives Ready-to-Eat Growth

Refrigerated and chilled products maintain a substantial 45.68% market share in 2025, demonstrating significant market dominance. This segment's prominent position is attributed to the established consumer perception correlating cold storage with optimal product freshness, particularly critical in plant-based dairy alternatives, where product integrity and organoleptic properties directly influence consumer purchasing behavior. The strategic convergence of meal kit market expansion and increased plant-based product adoption has facilitated the emergence of innovative hybrid product categories that transcend conventional classifications while addressing consumer requirements for nutritionally balanced, efficient meal solutions.

With a projected CAGR of 11.49% through 2031, the frozen segment is emerging as the fastest-growing category. This surge in growth underscores a notable shift in consumer preferences, leaning towards solutions that prioritize convenience, product quality, and extended shelf life. In the realm of plant-based offerings, frozen products are increasingly meeting the demand for ready-to-cook options, striking a balance between time efficiency and sensory appeal. The trend of participatory meal preparation is gaining momentum, highlighted by the rising popularity of pre-marinated and seasoned plant-based proteins. These products provide culinary flexibility while maintaining convenience. Canadian brands like Wholly Veggie, Gardein, and Sol Cuisine are at the forefront of this movement, presenting a wide array of frozen plant-based meals, snacks, and protein alternatives. Their offerings resonate with the consumer demand for nutrition, convenience, and clean-label ingredients.

By Distribution Channel: On-trade Growth Accelerates Despite Off-trade Dominance

In 2025, off-trade channels maintain a commanding position in Canada's plant-based food and beverage distribution landscape, representing 77.93% of the market share. This significant market dominance is attributed to established consumer purchasing patterns that demonstrate a clear preference for controlled home environments when evaluating novel plant-based alternatives. The systematic assessment of product attributes, including organoleptic properties and preparation versatility, occurs without external variables such as price premiums or social considerations. The off-trade segment's market leadership is further substantiated by comprehensive product distribution networks, strategic pricing mechanisms, and the systematic expansion of private-label portfolios across major Canadian retail establishments. For instance, in January 2023, 7-Eleven Canada introduced a vegan breakfast sandwich at 550 locations, featuring an Impossible Sausage patty, Violife cheese, and folded JUST Egg in an English muffin.

The on-trade channel, while holding a smaller market share, is projected to grow at a compound annual growth rate (CAGR) of 11.76% through 2031. Foodservice operators are increasingly incorporating plant-based options to attract younger consumers, particularly Millennials and Gen Z, who seek venues accommodating various dietary preferences, including vegan, flexitarian, and allergen-sensitive options. The growth in on-trade channels is supported by the ability of plant-based menu items to increase customer traffic and average check values, particularly when offered as premium alternatives. The evolving distribution dynamics across both channels demonstrate market maturation and strategic adaptation to diverse consumer preferences, indicating sustained growth potential in Canada's plant-based food and beverage sector.

Geography Analysis

The Canadian plant-based food and beverages market demonstrates significant regional differentiation, primarily influenced by demographic distributions, agricultural resource availability, and regulatory frameworks across provinces. Ontario maintains its position as a market leader through its comprehensive food processing infrastructure and strategic proximity to major metropolitan areas. Quebec exhibits substantial market penetration, attributed to heightened environmental consciousness and cultural receptivity to culinary innovation, further reinforced by robust manufacturing capabilities. This manufacturing strength is exemplified by Danone Canada's USD 9 million investment in June 2025 for the production of individual yogurt cups using polyethylene terephthalate (PET) at their Boucherville facility in Québec.

British Columbia's market shows strong consumer preference for sustainable and health-focused products, particularly in premium segments. This trend reflects the province's environmentally conscious population and supportive regulatory environment. For instance, in March 2023, Daiya invested in fermentation technology at its Burnaby, British Columbia, facility to develop improved plant-based cheese products with enhanced taste, melting, and stretching properties, demonstrating the region's commitment to sustainable food innovation. The Prairie provinces, though having smaller consumer markets, are essential agricultural production hubs for plant-based ingredients. Saskatchewan focuses on lentil cultivation, while Alberta is a major pulse crop producer, according to Statistics Canada.

Atlantic Canada presents emerging market opportunities through its expanding urban populations, particularly in Halifax and surrounding metropolitan regions. However, the region necessitates carefully structured distribution strategies due to logistical considerations and market scale limitations. The geographical distribution of Canada's plant-based market fundamentally reflects the interconnection between agricultural production capabilities, consumer demographic patterns, and infrastructure development. Successful market penetration requires organizations to implement regionally adapted strategies while addressing the distinct market characteristics prevalent across individual provinces.

Competitive Landscape

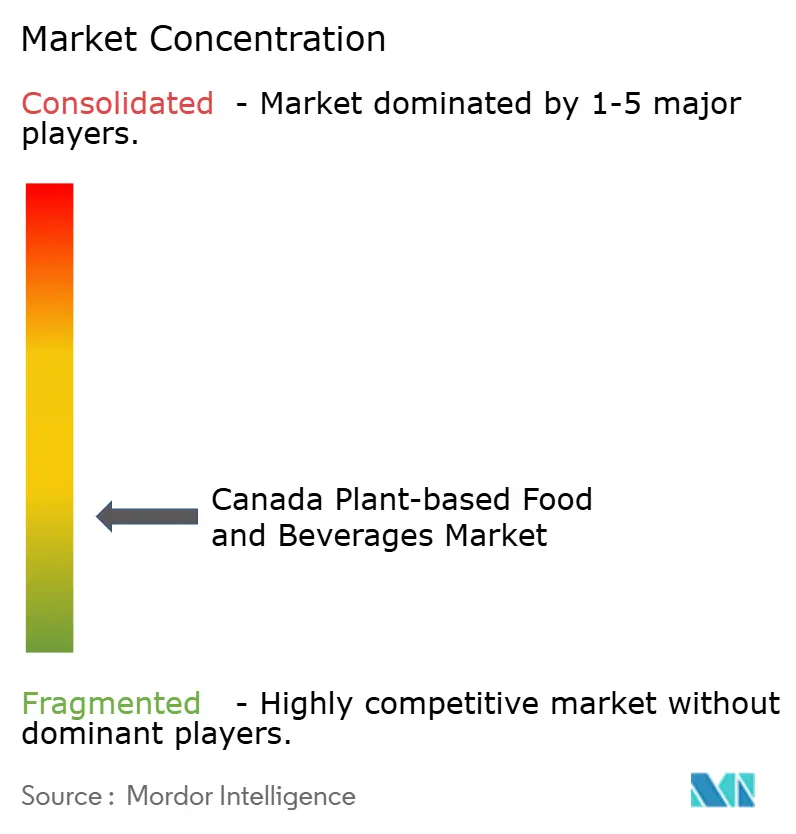

The Canada plant-based food market demonstrates a fragmented market. This market structure creates opportunities for established companies and new entrants to gain market share through product differentiation and technological innovation. The key market participants include Danone S.A., Beyond Meat, Inc., Nestle S.A., Earth's Own Food Company Inc., and SunOpta Inc. Companies are increasingly focusing on local sourcing and Canadian ingredients as competitive differentiators, exemplified by Danone Canada's use of domestic pea protein in its products.

The market presents significant opportunities in premium segments, foodservice channels, and specialized dietary categories where current players have minimal presence. New entrants benefit from Health Canada's modernized regulatory framework, including simplified food additive approval processes and updated compositional standards that support innovation while maintaining safety protocols. Companies that effectively balance product innovation, cost control, and regulatory compliance gain competitive advantages.

Government initiatives, such as Protein Industries Canada's technology leadership projects, help companies reduce development time and commercialization risks. Companies that establish partnerships with Canadian agricultural producers and food service distributors strengthen their market position through secure supply chains and distribution networks, while those without such relationships face increased cost pressures and declining market share.

Canada Plant-based Food And Beverages Industry Leaders

-

Danone S.A.

-

Beyond Meat, Inc.

-

Nestle S.A.

-

Earth’s Own Food Company Inc.

-

SunOpta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Violife launched Canada's first vegan cream cheese block. The product can be whipped, spread, and baked. The Creamy Block is available at retailers across the country, including Save-On-Foods and Longo's.

- May 2024: Bel Group launched The Laughing Cow Plant-Based in the Canadian market, expanding its plant-based product portfolio. The almond-based product maintains the traditional triangular shape of the original dairy version.

- May 2024: Lactalis Canada launched its new plant-based brand Enjoy!, featuring a high-protein line of plant-based beverages. The product range includes Unsweetened Oat, Unsweetened Oat Vanilla, Unsweetened Almond, Unsweetened Almond Vanilla, Unsweetened Hazelnut, and Unsweetened Hazelnut and Oat.

- February 2024: Danone S.A.'s brand Silk introduced a new plant-based yogurt made with Canadian pea protein. The product contains 12g of protein per 175g serving and features a Greek-style thick texture. The yogurt is available in Lime and Vanilla flavors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canada plant-based food and beverages market as the total retail and foodservice sales value of finished foods and drinks that rely primarily on plant ingredients for taste, texture, and nutrition; covering meat substitutes, dairy alternatives, bakery snacks, nutrition bars, and non-alcoholic beverages formulated from soy, pea, oat, almond, coconut, wheat, rice, and similar sources. Products must be commercially packaged, bar-coded, or listed on foodservice menus and must target end-consumers in Canada.

Scope exclusion: Industrial protein ingredients, raw pulses, feed, and nutraceutical capsules are outside this assessment.

Segmentation Overview

-

By Type

-

Plant-based Dairy

- Yogurt

- Cheese

- Frozen Desserts and Ice-Cream

- Other Plant-based Dairy

-

Meat Substitutes

- Tofu

- Tempeh

- Textured Vegetable Protein

- Other Meat Substitutes

- Plant-based Nutrition/Snack Bars

- Plant-based Bakery Products

-

Plant-based Beverages

- Packaged Milk

- Packaged Smoothies

- Coffee

- Tea

- Other Plant-based Beverages

- Other Food and Beverages

-

Plant-based Dairy

-

By Ingredient Source

- Soy

- Almond

- Pea

- Oat

- Wheat

- Rice

- Coconut

- Other Sources

-

By Form

- Refrigerated/Chilled

- Frozen

- Shelf-stable/Ambient

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Stores

- Other Off-Trade Channels

Detailed Research Methodology and Data Validation

Primary Research

We supplement desk work through interviews and structured surveys with Canadian grocery buyers, alt-protein start-ups, contract manufacturers, food scientists, and dietitians across Ontario, Québec, British Columbia, and the Prairies. Feedback helps test adoption rates, average selling prices, and channel mix assumptions and highlights emerging demand pockets such as oat-based coffee creamers in cafés.

Desk Research

Mordor analysts begin with publicly available macro and industry data from Statistics Canada, Agriculture & Agri-Food Canada, Health Canada, and the Canadian Food Inspection Agency. Trade flows are read through Customs Tariff files and the UN Comtrade interface, while consumption shifts come from Euromonitor Passport and Mintel GNPD product-launch trackers. Company filings, investor decks, major grocery banners' annual ESG reports, and reputable news archives accessed through Dow Jones Factiva and D&B Hoovers supply brand-level revenue cues. These sources illustrate volume trends, pricing corridors, and regulatory milestones that set the market context. The list above is illustrative; dozens of additional government portals, trade associations, and press articles are also reviewed to cross-check figures and clarify grey areas.

Market-Sizing & Forecasting

A top-down build links national food retail and foodservice turnover to category-level penetration rates derived from scanner panels, import volumes of key plant proteins, menu-count analytics, household dietary surveys, and flexitarian incidence data. Results are corroborated with selective bottom-up checks; supplier roll-ups and sampled ASP times unit calculations fine-tune totals. Key model variables include per-capita dairy milk reduction, average price premium of plant beverages, soy and pea protein import tonnage, new product launch frequency, and provincial lactose-intolerance prevalence. Forecasts to 2030 employ multivariate regression with scenario analysis around price inflation and protein crop yields, guided by sentiment gathered in primary interviews. Gaps in bottom-up granularity are bridged by weighting factors calibrated against historical variance.

Data Validation & Update Cycle

Every output passes a two-tier analyst review, variance screens against external indices, and anomaly discussions with subject experts. We refresh the model annually and trigger interim updates after material events such as subsidy changes or major product recalls; a final sense-check is performed before each client delivery.

Why Mordor's Canada Plant-Based Food And Beverages Baseline Is Trusted

Published market values often diverge. Differences in product scope, channel coverage, currency treatment, and refresh cadence lead figures from various publishers down separate paths.

Key gap drivers here include: some firms fold ingredient sales into end-product revenue, others exclude foodservice, and a few apply global growth multipliers without validating local price elasticities. Mordor's disciplined scope, dual-source variable set, and yearly refresh keep our baseline tightly aligned with what Canadians actually buy and consume.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.37 billion (2025) | Mordor Intelligence | - |

| USD 2.50 billion (2024) | Regional Consultancy A | Includes cafés RTD drinks and wellness powders outside our scope; relies on global uplift factors. |

| USD 4.62 billion (2023) | Trade Journal B | Blends raw pulse ingredient sales with finished goods; limited primary verification. |

| USD 1.12 billion (2023) | Analytics Publisher C | Focuses solely on retail packaged goods, ignoring restaurant demand. |

In sum, our model anchors to clearly defined product boundaries, Canada-specific demand drivers, and a transparent variable stack, giving decision-makers a balanced, reproducible baseline they can plan against with confidence.

Key Questions Answered in the Report

What is the current size of the Canada plant-based food market?

The Canada plant-based food market is valued at USD 1.51 billion in 2026 and is forecast to reach USD 2.44 billion by 2031.

Which product type leads sales in Canada?

Plant-based dairy holds 39.35% of revenue, benefiting from regular household use in coffee, cereal and smoothies.

Which ingredient source is growing fastest?

Oat-based formulations are projected to expand at a 12.03% CAGR, driven by barista-friendly beverages and allergen-free positioning.

How dominant are supermarkets versus restaurants?

Off-trade retailers maintain 77.93% share, but on-trade foodservice is growing faster at an 11.76% CAGR as menus broaden plant-based options.

Page last updated on: