Canada Data Center Processor Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

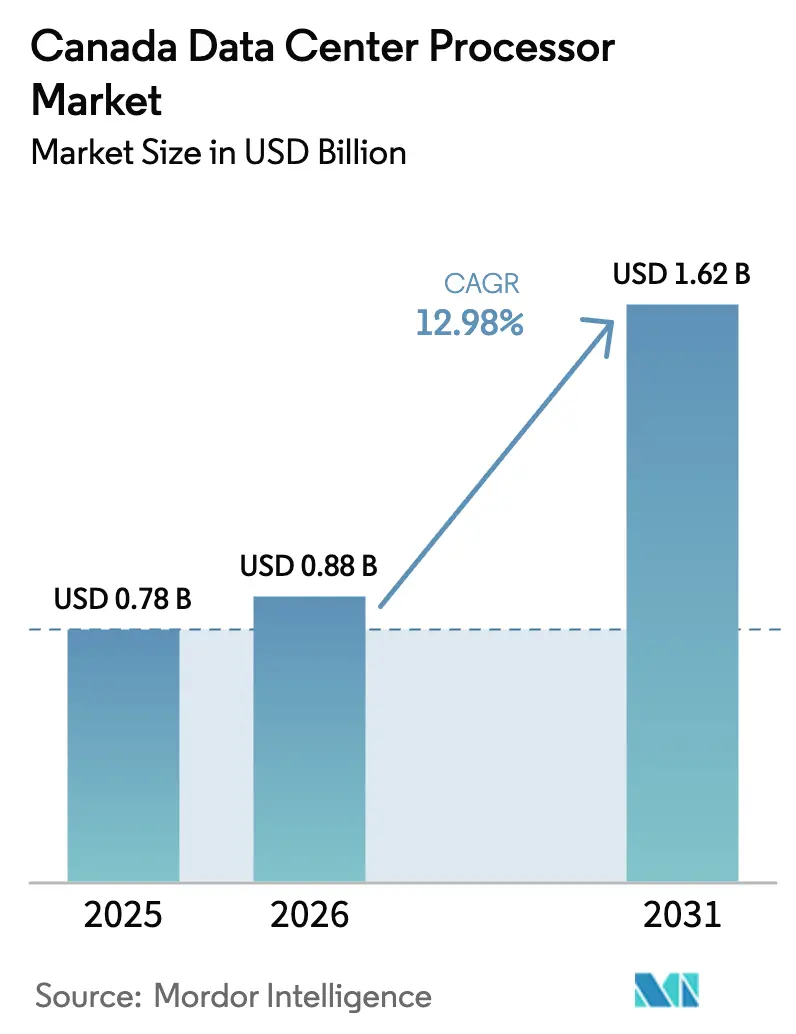

| Base Year Market Size (2025) | USD 0.78 Billion |

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 12.98% CAGR |

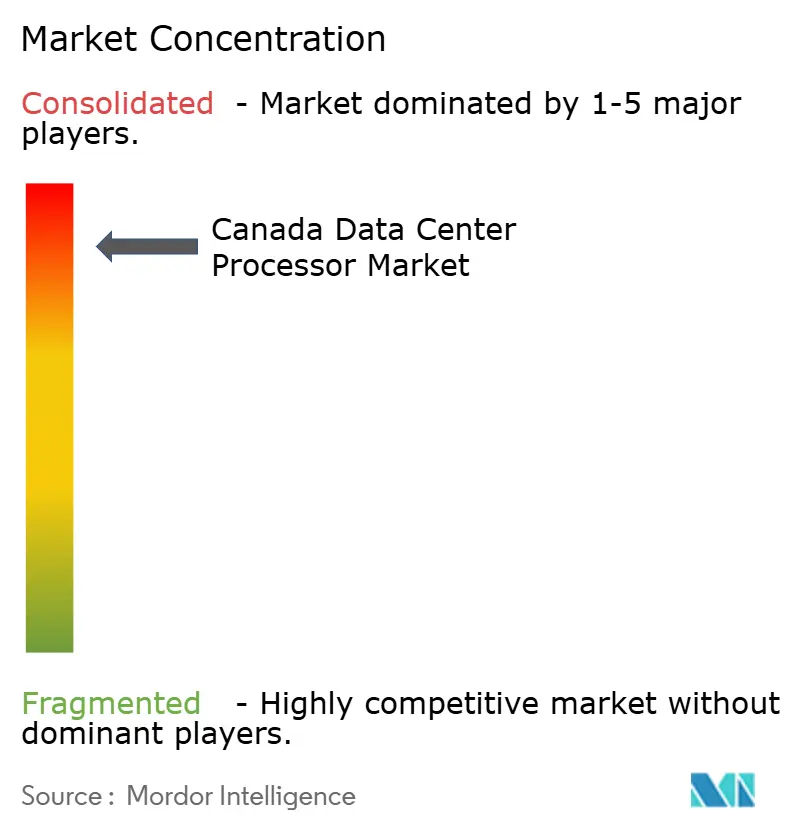

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Data Center Processor Market Analysis by Mordor Intelligence

Canada data center processor market size in 2026 is estimated at USD 0.88 billion, growing from 2025 value of USD 0.78 billion with 2031 projections showing USD 1.62 billion, growing at 12.98% CAGR over 2026-2031. Canada’s CAD 2 billion (USD 1.47 billion) Sovereign AI Compute Strategy, generous clean-power tax incentives, and seamless access to advanced GPUs under the U.S. AI Diffusion Framework’s Tier 1 designation together underpin sustained processor demand across hyperscale, colocation, and enterprise venues. Federal and provincial fast-track permitting has already condensed project lead times in Ontario and Quebec, while remote provinces are attracting edge-colocation builds that extend AI and analytics workloads closer to end users. Multicloud GPU leasing marketplaces emerging in Montreal, Toronto, and Vancouver are further raising utilization, and open-source RISC-V clusters at leading universities are seeding a domestic ecosystem around heterogeneous compute design. Continued resilience in clean-power supply and aggressive investment in liquid-cooling capacity will be decisive in turning this momentum into long-term scale.

Key Report Takeaways

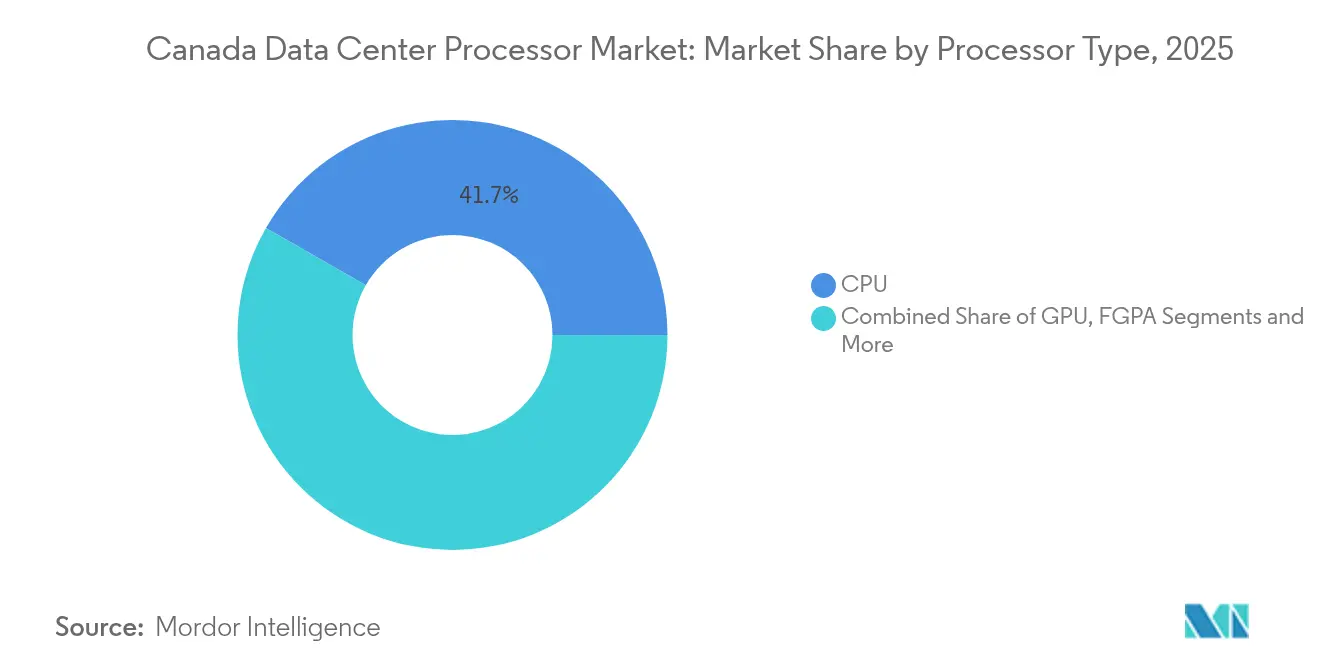

- By processor type, CPUs accounted for 41.72% share of Canada's data center processor market size in 2025, while AI accelerators and ASICs are on track for a 14.36% CAGR to 2031.

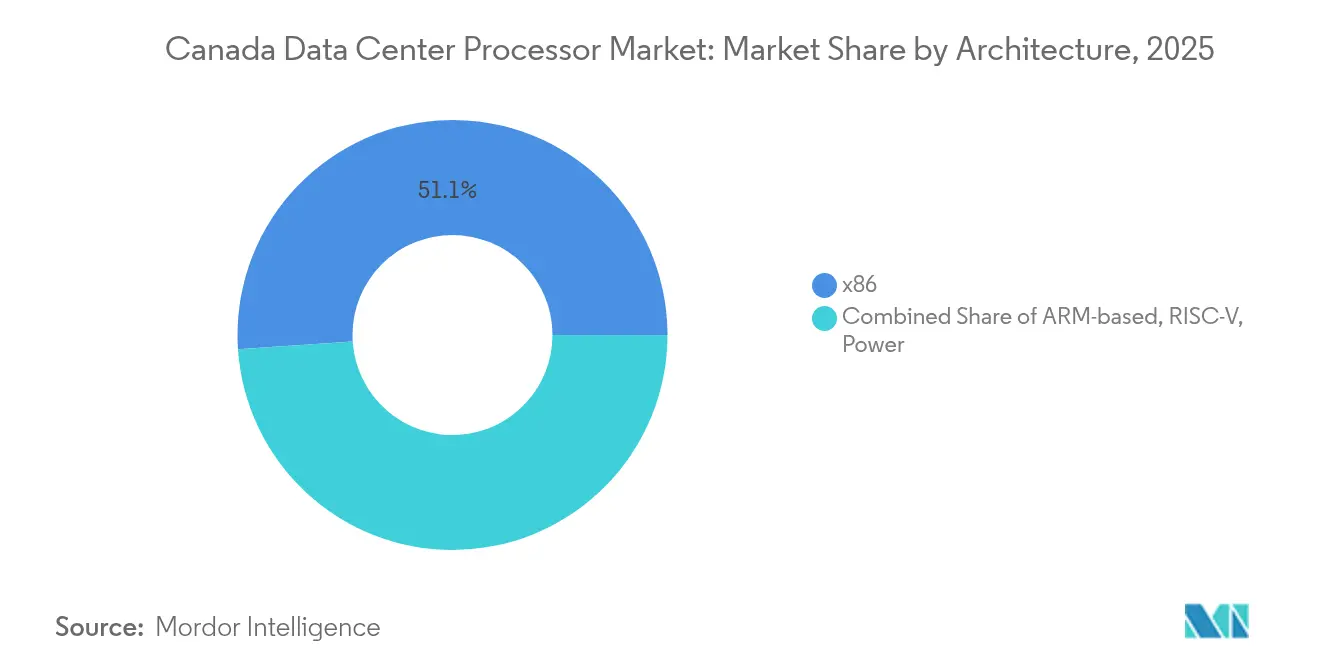

- By architecture, x86 led with 51.05% Canada data center processor market share in 2025; RISC-V is the fastest-growing architecture at a 14.88% CAGR.

- By application, AI/ML training and inference captured 34.12% share of Canada data center processor market size in 2025, and advanced data analytics is advancing at a 14.18% CAGR to 2031.

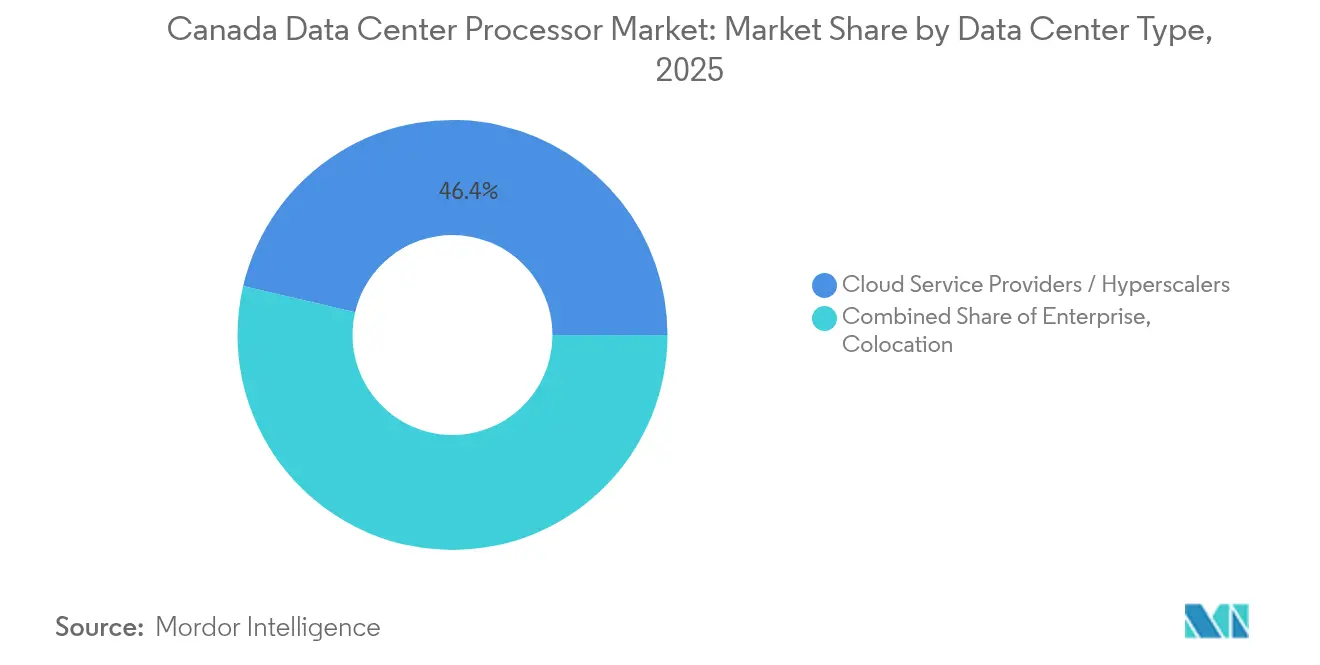

- By data center type, cloud service providers held 46.35% of Canada data center processor market share in 2025, whereas colocation facilities are forecast to expand at a 15.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada contributes to a system defined not by any single country or region but by the interaction of many. The global data center processor market data by Mordor Intelligence represents that combined structure.

Canada Data Center Processor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)(%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first digital-government mandate accelerates hyperscale build-outs | +3.5% | National; early gains in Ontario, Quebec | Medium term (2-4 years) |

| Gen-AI training surge from Sovereign AI Compute Strategy | +4.2% | National; concentrated in Toronto, Montreal | Long term (≥ 4 years) |

| Edge-colocation tied to 5G roll-out in remote provinces | +2.1% | Northern Canada | Medium term (2-4 years) |

| Tax credits for clean-power colocation lower GPU TCO | +1.8% | Quebec, Ontario, Alberta | Short term (≤ 2 years) |

| Multicloud GPU leasing marketplaces | +1.2% | Montreal, Toronto, Vancouver | Medium term (2-4 years) |

| Open-source RISC-V university clusters | +0.7% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-first Digital-Government Mandate Accelerates Hyperscale Build-Outs

Canada’s 2024 Fall Economic Statement earmarked CAD 2.4 billion to deepen the federal cloud-first agenda, spurring hyperscalers to deploy high-density GPU racks for public-sector workloads. Accelerated permitting in Ontario and Quebec has already shortened build cycles by several months, enabling healthcare, tax, and defense agencies to migrate latency-sensitive applications to sovereign facilities.[1]Government of Canada, “Fall Economic Statement 2024,” canada.ca

Gen-AI Training Surge from Canada’s Sovereign AI Compute Strategy

The Sovereign AI Compute Strategy channels CAD 700 million (USD 514.42 million) toward private AI data center projects and CAD 1 billion (USD 0.74 billion) into public supercomputers, prompting cloud providers to pre-order next-generation GPUs and AI accelerators for local deployment. Cohere’s Toronto campus, anchored by NVIDIA DGX clusters, illustrates how domestic AI model training is reshaping processor demand profiles.[2]TELUS, “TELUS to Open Sovereign AI Factory in Quebec,” telus.com

Edge-Colocation Projects Tied to 5G Roll-Out in Remote Provinces

5G coverage across northern provinces is encouraging micro-colocation facilities that minimize backhaul latency for mining, telemedicine, and logistics applications. Partnerships such as Cologix-Consensus Core are equipping compact edge pods with liquid-cooled GPU shelves, reducing data transport costs while improving compliance with data-sovereignty rules.

Tax Credits for Clean-Power Colocation Lower TCO of High-Density GPU

The Clean Electricity Investment Tax Credit of 15% and the companion Clean Technology Manufacturing Credit of 30% lower capital costs for energy-efficient sites leveraging Quebec hydropower and Ontario nuclear baseload. Operators are channeling these savings into 80 kW-per-rack GPU configurations that meet both carbon and cost targets.[3]Government of Canada, “Fall Economic Statement 2024,” canada.ca

Restraints Impact Analysis*

| Restraint | (~)(%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-year utility-grid bottlenecks in Quebec & Ontario | -2.7% | Quebec, Ontario | Medium term (2-4 years) |

| Tight immigration caps slow semiconductor talent inflow | -1.4% | National; acute in Ontario, BC | Long term (≥ 4 years) |

| Export-control risks on U.S. AI accelerators limit supply | -1.1% | National | Short term (≤ 2 years) |

| Insufficient liquid-cooling supply chain | -0.9% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-Year Utility-Grid Bottlenecks in Quebec & Ontario

Rapid uptake of AI compute has outstripped local grid upgrades, forcing operators to secure multi-megawatt interconnections years in advance. Delays in transmission expansion threaten to stall large GPU cluster rollouts and could push demand to provinces with spare capacity.

Tight Immigration Caps Slow Semiconductor Talent Inflow

Despite a new LMIA-exempt Innovation Stream visa, skilled-worker quotas remain tight, slowing recruitment of chip designers and data-center engineers. Domestic players have increased reliance on cross-border project teams and remote work arrangements to close skill gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processor Type: AI Accelerators Reshape Compute Demand

CPU shipments dominated Canada data center processor market in 2025 with a 41.72% share, but heterogeneous architectures are shifting the balance. The segment that bundles AI accelerators and ASICs is growing at a 14.36% CAGR as hyperscalers deploy AMD Instinct MI300X and NVIDIA Blackwell GPUs for large-language-model training. In parallel, custom ASICs optimized for low-latency inference in fintech and e-commerce are capturing new sockets once served by standard CPUs. Canada data center processor market size for AI accelerators is therefore poised to overtake standalone CPU spend in high-density racks before 2031. Energy-efficiency goals are accelerating the pivot toward accelerators equipped with on-package HBM and advanced cooling plates, allowing rack power envelopes to remain within grid constraints.

CPUs are not disappearing; rather they are being repurposed as orchestration cores that manage GPU-rich nodes. Telco edge sites in remote provinces still favor high-core-count CPUs for packet processing and virtualization, while financial regulators mandate deterministic performance for select workloads best handled by x86. Nevertheless, the CAGR gap is widening, reinforcing a procurement shift where operators reserve more budget for accelerator cards than general-purpose sockets. Canada data center processor industry participants that offer integrated CPU-GPU boards and software toolchains are best positioned to capture this evolving mix.

By Application: Advanced Data Analytics Drives New Investment

AI/ML workloads accounted for 34.12% of Canada's data center processor market share in 2025, but advanced data analytics is the fastest-growing slice at a 14.18% CAGR. Real-time fraud detection at Canadian banks and large-scale simulation in logistics now demand dense GPU clusters with mixed-precision compute. The Canada data center processor market size flowing into analytics is expanding as enterprises adopt data-mesh architectures that pool compute-hungry queries across shared accelerator farms.

Security and encryption workloads are also rising, propelled by stricter federal privacy regulations and a forthcoming AI & Data Protection Act. That backdrop is fostering demand for cryptographic accelerators and confidential-compute CPUs that can isolate sensitive workloads in trusted enclaves. The resulting heterogeneity pushes data-center operators to fine-tune resource allocation, often leasing idle GPUs to third parties via multicloud marketplaces to maximize yield.

By Architecture: RISC-V and ARM Challenge x86 Dominance

x86 maintained 51.05% Canada data center processor market share in 2025, but open-hardware momentum is shifting industry sentiment. RISC-V is growing at 14.88% CAGR due to SiFive’s 256-core P870-D, which demonstrates power-efficient AI inference in university clusters and select colocation labs. ARM architectures, led by AWS Graviton-class CPUs, are gaining in hyperscale facilities that prioritize low-watt, high-thread performance. Combined RISC-V and ARM sockets could eclipse one-third of Canada's data center processor market size by 2031 if current adoption curves hold.

x86 vendors are responding with chiplet-based refreshes and integrated AI coprocessors to defend share, while RISC-V players court sovereign-compute initiatives that prize open ISA governance. The outcome is a competitive equilibrium where each architecture carves out niches: x86 for broad software compatibility, ARM for power-sensitive scaling, and RISC-V for customizable AI accelerators.

By Data Center Type: Colocation Surges Amid Hyperscaler Expansion

Cloud service providers led with 46.35% share in 2025, yet colocation sites are the headline growth story, advancing at 15.92% CAGR. Enterprises pursuing hybrid IT are pre-leasing GPU cages in facilities like eStruxture MTL-7, while hyperscalers expand in parallel to serve federal workloads under the digital-government mandate. Canada data center processor market size flowing into colocation will therefore outgrow that of enterprise-owned halls, even as regulated industries maintain on-premise clusters for compliance reasons.

Edge-colocation nodes in northern Alberta and Saskatchewan showcase modular designs that integrate liquid immersion tanks, enabling GPU densities previously confined to urban hubs. Hyperscalers remain committed to sustainability; several have locked in long-term hydropower and nuclear PPAs to guarantee renewable supply for multi-megawatt expansions.

Geography Analysis

Ontario and Quebec dominate spend, jointly accounting for more than two-thirds of Canada data center processor market. Both provinces combine abundant clean electricity with accelerated permitting, drawing hyperscale and colocation investments that demand the newest CPUs, GPUs, and AI accelerators. Quebec’s low-carbon hydropower allows operators to advertise near-net-zero footprints, a critical win for customers under ESG mandates. Ontario, meanwhile, fast-tracks data-center zoning and interconnection, shortening build cycles for government and healthcare projects that require sovereign processing.

Remote provinces are the frontier for edge-colocation, where 5G roll-out and resource-sector digitization compel micro-modular racks equipped with mid-range GPUs. Northern Alberta mines now stream sensor data to local edge nodes for real-time analytics, slashing backhaul latency and bandwidth costs. Similar deployments in Saskatchewan support tele-medicine imaging, translating into incremental processor demand outside the core provinces.

The data center processor market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia. This is complemented by country-specific insights for Chile, Brazil, South Korea, China, Japan, Netherlands, France, and Germany, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Canada’s processor supply chain is fragmented, with global incumbents, domestic startups, and service providers all vying for relevance. TELUS is partnering with NVIDIA to co-locate a Sovereign AI Factory in Quebec, creating a vertically integrated stack that spans GPUs, networking, and AI software frameworks. AMD’s 2025 product slate emphasizes adaptive computing; its MI300X GPU and Ryzen AI series aim to secure sockets across hyperscale and enterprise clusters alike.

Open-hardware disruptors SiFive and AheadComputing leverage RISC-V to pursue custom accelerator IP, targeting workloads where performance per watt trumps decades-old software libraries. Their reference designs are already present in university proof-of-concept clusters funded under the Sovereign AI program. GPU-as-a-Service operators such as CoreWeave and Consensus Core monetize surplus accelerator capacity via multicloud exchanges, squeezing procurement cycles and intensifying competition for utilization.

Canada Data Center Processor Industry Leaders

Intel Corporation

Advanced Micro Devices Inc.

NVIDIA Corporation

Arm Holdings plc

Ampere Computing

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BCE announces six AI data centers across Canada to extend GPU cloud services.

- March 2025: TELUS and NVIDIA launch a Sovereign AI Factory in Quebec powered by 99% renewable energy.

- January 2025: AMD introduces Ryzen AI Max, AI 300, and AI 200 processors at CES, targeting high-performance AI PCs and enterprise servers.

- December 2024: Cohere secures federal backing for a multibillion-dollar AI data center in Toronto, anchored by NVIDIA GPUs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Canada data center processor market as all CPU, GPU, FPGA, and AI-accelerator integrated circuits procured by colocation, hyperscale-cloud, and enterprise facilities for in-rack compute workloads.

Scope exclusion: discrete memory, networking, and power-management chips remain outside this assessment.

Segmentation Overview

- By Processor Type

- GPU

- CPU

- FPGA

- AI Accelerator/ASIC

- By Application

- Advanced Data Analytics

- AI/ML Training and Inference

- High-Performance Computing

- Security and Encryption

- Network Functions Virtualisation

- Others

- By Architecture

- x86

- ARM-based

- RISC-V

- Power

- By Data Center Type

- Enterprise

- Colocation

- Cloud Service Providers / Hyperscalers

Detailed Research Methodology and Data Validation

Primary Research

Conversations with hyperscale capacity planners, colocation operators in Ontario and Québec, semiconductor product managers, and provincial energy-policy officials validated power-cost assumptions, typical refresh cycles, and emerging ARM/RISC-V penetration.

Desk Research

Mordor analysts began with open datasets such as Statistics Canada's ICT hardware import codes, Innovation Science & Economic Development Canada's semiconductor road-maps, Natural Resources Canada's "Clean Electricity Investment Tax Credit" filings, and Uptime Institute's annual Canadian capacity survey; these helped size installed rack count, average processor density, and feasible power envelopes. Trade association notes (AI Canada, Digital Supercluster) and Tier-1 media coverage gathered through Dow Jones Factiva rounded out demand triggers, while D&B Hoovers filings provided vendor revenue splits for Canada. Patents mined from Questel and customs records from CBSA clarified shipments of AI-accelerator boards, which anchored our growth-rate assumptions for emerging chip types. The sources cited here illustrate the mix we use; many additional references supported data vetting but are not listed exhaustively.

Market-Sizing & Forecasting

A top-down reconstruct built total processor spend from imported server volumes, average socket counts, and blended ASPs, then aligned with installed MW capacity. Select bottom-up checks, supplier revenue roll-ups and sampled hyperscale purchase orders, tempered any variance. Key model drivers include average rack density, clean-power tax incentives, Gen-AI training demand, sovereign AI compute budgets, and x86-to-accelerator migration pace. Multivariate regression, run on a five-year history of these indicators, extends forecasts to 2030; missing bottom-up datapoints are gap-filled by applying validated penetration ratios from neighboring quarters.

Data Validation & Update Cycle

Outputs face sequential peer review; variance thresholds (>5 %) trigger re-checks against new customs or vendor filings, and we refresh the file each year or sooner when material events (e.g. abrupt GPU tariff) surface.

Why Mordor's Canada Data Center Processor Baseline Commands Reliability

Published figures often diverge because firms mix broader chip classes, wider geographies, or untested pricing curves. Our disciplined Canada-only lens, clear processor definition, annual refresh cadence, and dual research loops produce a value decision-makers can lean on.

One external publisher cites US$1.19 billion for a wider "chip" basket in 2024. Another places North America CPU spend at US$3.68 billion for the same year, blending U.S. capex with Canadian demand.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| US$0.78 billion (2025) | Mordor Intelligence | - |

| US$1.19 billion (2024) | Global Consultancy A | Includes memory and networking chips; limited Canada-specific primary input |

| US$3.68 billion (2024) | Industry Journal B | Covers entire North America; extrapolates from server capex rather than processor ASPs |

Taken together, the comparison shows how Mordor's Canada-focused definition and mixed-method validation deliver a balanced, transparent baseline that can be replicated and confidently defended on client calls.

Key Questions Answered in the Report

What is the current value of Canada data center processor market?

The market is valued at USD 0.88 billion in 2026 and is forecast to reach USD 1.62 billion by 2031 at a 12.98% CAGR.

Which data center type is expanding the fastest?

Colocation facilities are the fastest-growing segment with a 15.92% CAGR through 2031, driven by hybrid-IT adoption and edge deployments.

Why are AI accelerators gaining share over CPUs?

Explosive AI/ML and analytics workloads require high-throughput compute; AI accelerators offer superior performance per watt, leading to a 14.36% CAGR for the segment.

What regions outside Ontario and Quebec show potential?

Northern Alberta and Saskatchewan are emerging edge-colocation hubs, while British Columbia and Atlantic Canada focus on sustainable builds and advanced cooling.

Page last updated on: