Canada Data Center Networking Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

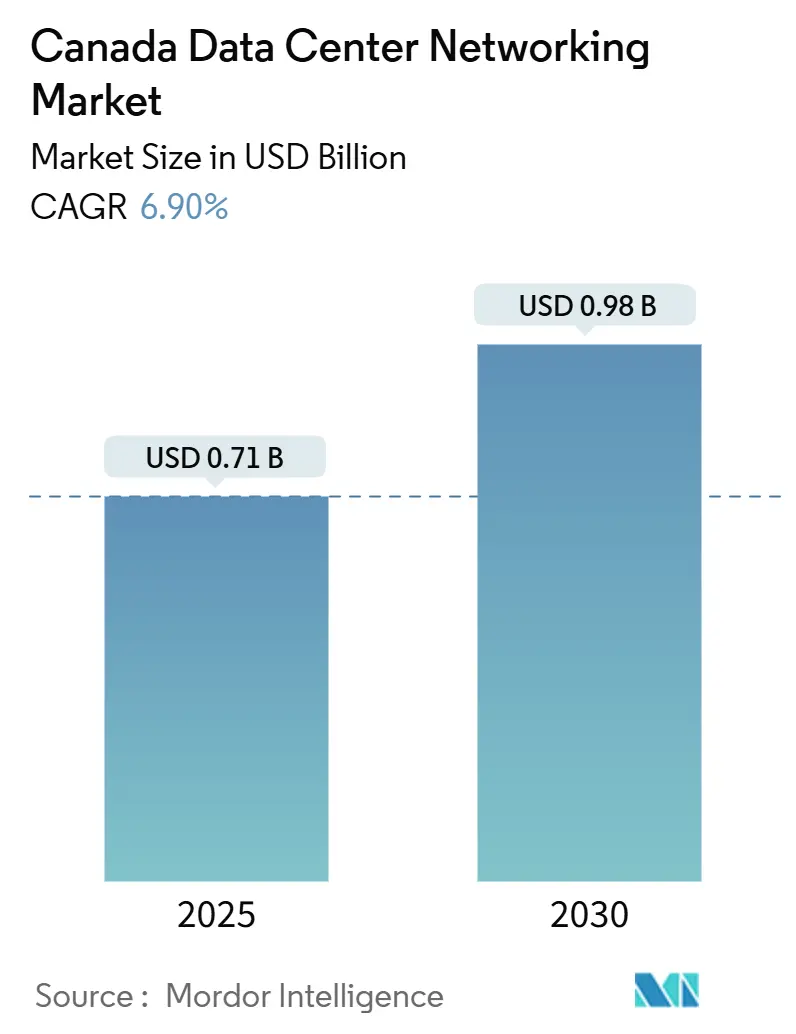

| Market Size (2025) | USD 0.71 Billion |

| Market Size (2030) | USD 0.98 Billion |

| Growth Rate (2025 - 2030) | 6.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Data Center Networking Market Analysis by Mordor Intelligence

The Canada data center networking market stands at USD 710 million in 2025 and is forecast to reach USD 980 million by 2030, expanding at a 6.9% CAGR. Continuous hyperscale cloud region build-outs, rapid 400G/800G Ethernet adoption, generous clean-tech incentives, and the federal AI Sovereign Compute Strategy are combining to reshape capital spending priorities, pushing operators toward low-latency fabrics and energy-efficient hardware. Alberta’s renewable-energy-powered hyperscale projects, Quebec’s hydro-backed colocation clusters, and the Toronto-Montreal financial corridor together drive regional demand for high-performance switches, optical interconnects, and software-defined fabrics. At the same time, removal of Huawei and ZTE gear, lingering optical component shortages, and a bilingual cyber-network talent crunch are inflating project costs and complicating roll-out schedules. Green retrofits supported by investment tax credits, alongside growing interest in liquid-cooled racks, underpin long-term opportunities for vendors that can prove power-efficiency gains. Overall, the Canada data center networking market is entering a scale-up phase where sustainability, sovereignty and speed intersect.

Key Report Takeaways

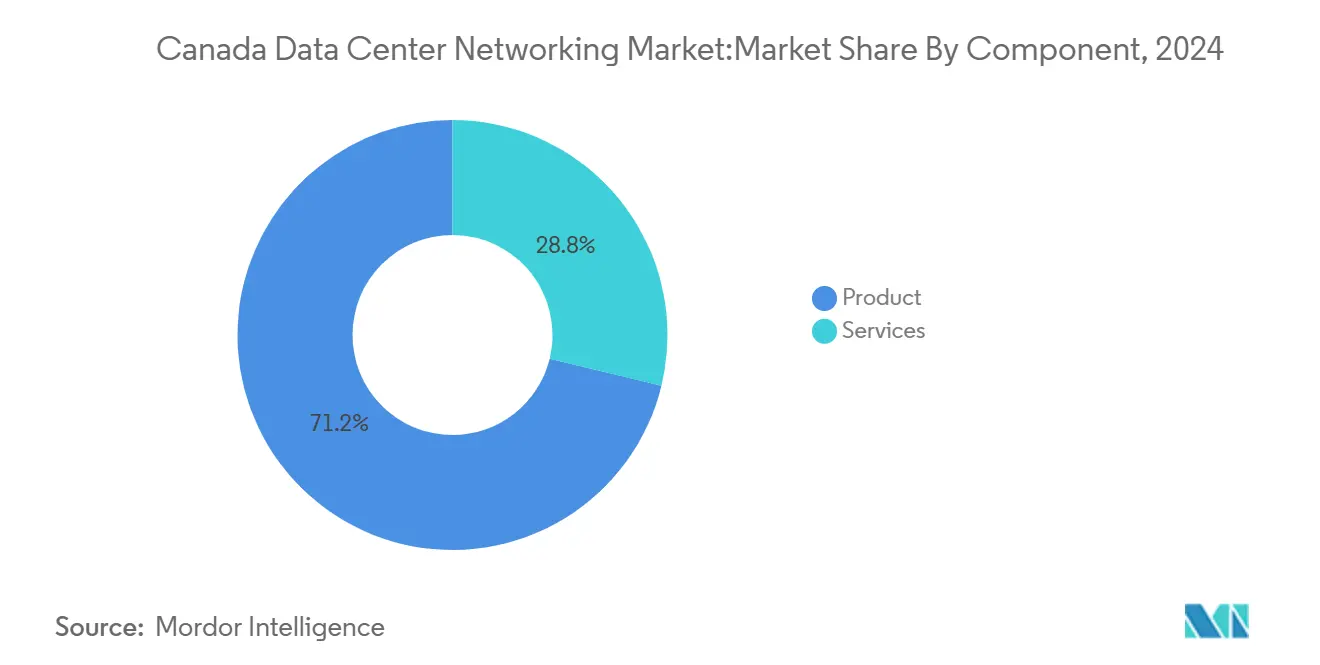

- By component, products led with 71.2% revenue share in 2024, while services are projected to expand at a 7.1% CAGR through 2030.

- By end-user, IT and telecommunications held 38.2% of the Canada data center networking market share in 2024, whereas manufacturing is set to grow at 7.5% CAGR to 2030.

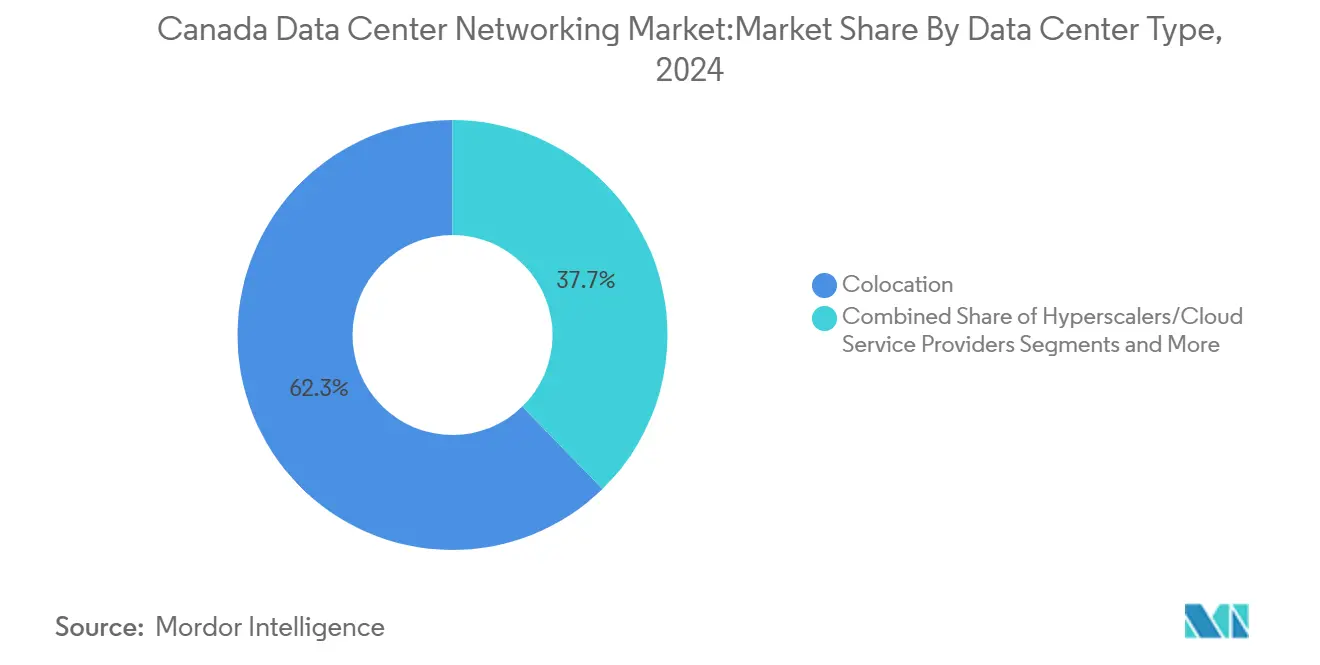

- By data-center type, colocation facilities accounted for 62.3% share of the Canada data center networking market size in 2024, while hyperscaler deployments are advancing at an 8.3% CAGR through 2030.

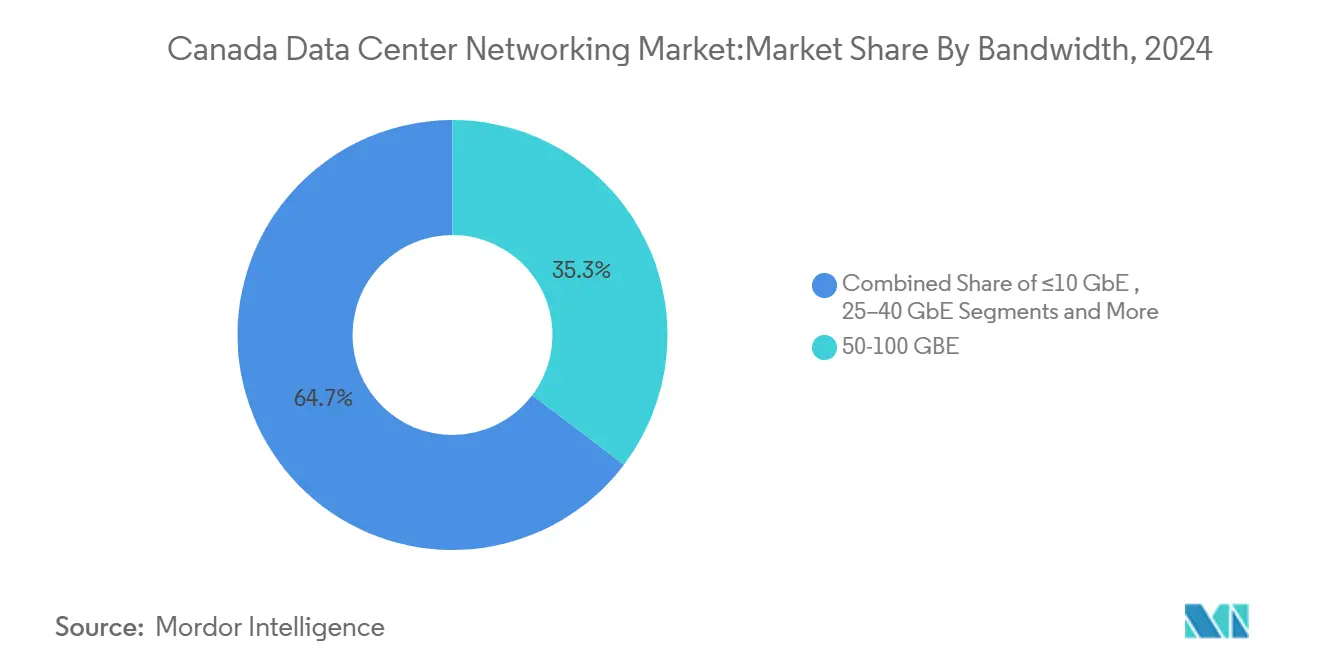

- By bandwidth, 50-100 GbE connections commanded 35.3% share of the Canada data center networking market size in 2024 and greater than 100 GbE links are forecast to rise at an 8.7% CAGR to 2030.

Market participation spans countries and regions, making Canada competition one layer within a larger international field. In its global data center networking industry statistics, Mordor Intelligence maps that multi-region structure.

Canada Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud region build-outs (AWS, IBM, Google) | +1.2% | Alberta, Quebec, Ontario | Medium term (2-4 years) |

| Rapid 400G/800G Ethernet switch adoption | +0.9% | National, major metros | Short term (≤ 2 years) |

| Clean-tech ITCs driving green DC retrofits | +0.6% | National, hydro-rich provinces | Long term (≥ 4 years) |

| Alberta surplus renewables attracting U.S. hyperscalers | +0.8% | Alberta, Saskatchewan | Medium term (2-4 years) |

| Federal AI Sovereign Compute Strategy boosting low-latency fabrics | +0.7% | Toronto-Montreal corridor | Medium term (2-4 years) |

| Liquid-cool-ready network gear enabling ultra-dense racks | +0.5% | National hyperscalers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Expansion and AI Sovereignty

Hyperscaler investment is reshaping the Canada data center networking market as Amazon, Google, and IBM open new cloud regions and align architectures with Ottawa’s CAD 2 billion (USD 1.46 billion) AI Sovereign Compute Strategy. These projects demand leaf-spine fabrics, 400G optics, and zero-trust segmentation that keep sensitive datasets inside national borders. Telecom carriers are pivoting from pure connectivity providers to infrastructure partners by adding sovereign AI clusters powered by hydro-electric energy. Resulting east-west traffic growth drives multi-terabit switch upgrades, cementing a robust outlook for high-bandwidth equipment orders.

Rapid 400G/800G Migration

Accelerating deployment of 400G and test-bed 800G Ethernet switches is moving core data-center links beyond 100G thresholds.[1]Cisco Systems, “400G and Beyond Switching Portfolio,” cisco.comHyperscalers need wider pipes for model training, while enterprises follow suit to future-proof campus backbones and storage fabrics. Vendors that integrate strong telemetry, congestion control and energy-savings features gain advantage, as operators increasingly base decisions on total cost of ownership and sustainability metrics.

Clean-Tech Incentives Spur Green Retrofits

Federal clean-economy investment tax credits covering 15% of eligible electricity assets and 30% of qualifying manufacturing expenditures lower the payback period on efficient, liquid-cool-ready switches.[2]Natural Resources Canada, “Clean Economy Investment Tax Credits,” nrcan.gc.ca Operators retrofit legacy halls with high-density racks, boosting demand for modular, low-loss optical interconnects. Compliance with prevailing wage and apprenticeship rules also prompts collaboration with local integrators and workforce-development partners.

Alberta Renewable Edge and Liquid Cooling Synergy

Abundant wind, solar and natural-gas-firmed power allows Alberta facilities to promise predictable, low-carbon energy. Combined with liquid-cooled GPU clusters, these sites require network gear that tolerates elevated inlet temperatures and dense port configurations. Suppliers able to certify gear for immersion or cold-plate environments secure specification wins as hyperscalers race to build ultra-dense AI pods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Huawei/ZTE equipment ban raising CAPEX and delays | -0.8% | National, rural areas | Short term (≤ 2 years) |

| Global chip and optics shortages elongating lead-times | -0.6% | National | Medium term (2-4 years) |

| Bilingual cyber-network talent crunch | -0.4% | Quebec, New Brunswick | Long term (≥ 4 years) |

| Wildfire-induced fibre outages in rural backbones | -0.3% | West and North | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Equipment Ban and Supply Bottlenecks

Mandatory removal of Huawei and ZTE hardware lifts replacement budgets by 15-25% and forces redesigns, particularly for operators serving Canada’s rural communities. [3]Public Safety Canada, “Secure Equipment List and Deadlines,” publicsafety.gc.ca At the same time, global shortages of coherent optics and high-speed SerDes chips lengthen delivery cycles, slowing hyperscale expansion schedules within the Canada data center networking market.

Talent and Climate-Related Vulnerabilities

A 25,000-person cybersecurity vacancy gap, made tighter by bilingual requirements for federal and Quebec contracts, inflates wage bills and delays go-lives. Meanwhile, wildfire seasons threaten long-haul fibre trunks, prompting new investment in diverse routes and edge-cache nodes that increase overall network complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Signals Market Maturation

The services slice of the Canada data center networking market is projected to grow 7.1% annually through 2030, even though products retained 71.2% share in 2024. Rising complexity from software-defined overlays and AI-optimized fabrics drives demand for design, integration and managed offerings. Ethernet switches, still the revenue anchor, now ship in 400G configurations bundled with telemetry software, while routers migrate toward disaggregated platforms that separate control and data planes. Storage networking benefits from NVMe-over-Fabrics, creating space for integrators skilled in low-latency transport tuning. As organizations target operational resilience, managed service providers upsell proactive monitoring, adding sticky recurring revenue to the Canada data center networking market.

The shift also reflects buyers’ preference for outcome-based contracts over perpetual hardware purchases. Vendors package subscription licensing, lifecycle management and sustainability reporting, enabling CIOs to align spend with cloud-like economics. Consequently, services influence procurement decisions even for core switching hardware, illustrating how the Canada data center networking market has matured beyond a purely box-driven model.

By End-User: Manufacturing Surge Reflects Industry 4.0 Adoption

IT and telecom players still command 38.2% of spending, yet manufacturing’s 7.5% CAGR signals fast catch-up as factories roll out digital twins and predictive maintenance. Real-time control loops require sub-millisecond latency across converged OT-IT networks, turning plant operators into significant purchasers of leaf-spine fabrics and hardened edge switches. Financial institutions remain early adopters of ultra-low-latency architectures for trading, but growth is steadier, driven by compliance refresh cycles rather than new workload types.

Healthcare systems expand tele-diagnostics and genomic analytics, demanding secure, high-bandwidth links from regional hospitals to AI clusters. Media firms shift to cloud-based 8K production pipelines, stretching campus cores. Together these dynamics diversify the Canada data center networking market, reducing reliance on traditional telecom spending and reinforcing the need for multi-industry solution breadth.

By Data-Center Type: Hyperscaler Growth Transforms Infrastructure Requirements

Colocation sites captured 62.3% of 2024 revenue, yet hyperscalers are forecast to log 8.3% CAGR, outpacing every other form factor. Cloud providers scale out four-story halls packed with liquid-cooled GPU trays, necessitating flat, high-radix fabrics. Colocation operators respond by adding build-to-suit hyperscale wings and cross-connect marketplaces, blending neutrality with scale economics to protect their Canada data center networking market share.

Edge and micro-data centers gain traction along 5G corridors and in resource extraction zones, where low-latency analytics cut downtime. These deployments favor compact, temperature-tolerant switches that support remote automation. Consequently, the supply chain must cater to very large-scale and very small-scale builds simultaneously, underscoring the nuanced character of the Canada data center networking market.

By Bandwidth: Ultra-High-Speed Transition Accelerates AI Readiness

Connections above 100 GbE are growing at an 8.7% CAGR as AI model training and east-west traffic skyrocket. The Canada data center networking market size for >100 GbE gear is expected to overtake sub-100 GbE revenue before 2028. 50-100 GbE still holds 35.3% share, primarily in colocation and enterprise refresh projects, offering a bridge for firms moving up from 10 GbE.

Optical integration is pivotal: Ciena’s 1.6 Tb/s coherent pluggables and 448 Gb/s PAM4 modules reduce power per bit and extend reach for inter-metro data-center-interconnect, a segment forecast to triple over five years. Vendors that provide step-wise migration paths and port-speed flexibility protect customer investments and secure long-run loyalty in the Canada data center networking market.

Geography Analysis

Ontario remains the single largest provincial buyer thanks to its concentration of financial services headquarters and proximity to large U.S. markets. High-density campuses in downtown Toronto feed demand for 400G leaf-spine fabrics, while suburban data-center alleyways host inter-cloud exchange hubs. Quebec leverages hydro-electric capacity to attract sustainable AI workloads, anchoring long-haul fibre builds that knit Montreal, Beauharnois and Quebec City into a tri-city digital cluster. French-language procurement rules enable local integrators to capture support contracts, adding services revenue to the Canada data center networking market.

Alberta is emerging as Canada’s hyperscale alternative by pairing renewable energy credits with flexible natural-gas peakers. Projects such as the Wonder Valley AI Park, designed for 1.4 GW off-grid power, accelerate orders for liquid-cool-ready switches and high-capacity optical backbones. Saskatchewan and Manitoba, benefiting from intertie capacity, position themselves as spill-over locations for follow-on builds, thereby broadening the provincial spread of the Canada data center networking market.

Coverage of the data center networking market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Middle East, Asia, and Europe, alongside detailed country-level intelligence for Chile, Brazil, Saudi Arabia, Hong Kong, Norway, and Taiwan, each shaped by local operating conditions.

Competitive Landscape

Vendor rivalry is intensifying as established switch suppliers defend share against cloud-native challengers. Cisco retains leadership through a full-stack portfolio and nationwide channel network, yet Arista’s cloud-grade EOS stack helped it cross USD 2 billion quarterly revenue in Q1 2025, mainly on AI cluster wins. Extreme Networks courts enterprises unsettled by the pending HPE-Juniper merger, positioning ease-of-migration as a differentiator. Nokia’s planned USD 2.3 billion Infinera acquisition underscores optical interconnect’s rising relevance to the Canada data center networking market.

Strategically, vendors bundle network, security and observability into single platforms to reduce operational friction for resource-constrained operators. Co-design partnerships with hyperscalers speed custom ASIC road-maps, while collaboration with colocation providers expands integration services. The Huawei/ZTE ban realigns market share: Ericsson and Nokia win mobile backhaul upgrades, while white-box ODMs gain enterprise traction. Overall, success hinges on demonstrating power efficiency, AI workload readiness and Canadian data-sovereignty compliance to a buyer base that is both cost-sensitive and regulation-aware.

Canada Data Center Networking Industry Leaders

Cisco Systems Inc.

Arista Networks Inc.

VMware Inc.

Huawei Technologies Co. Ltd.

NVIDIA (Cumulus Networks)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TELUS launched Sovereign AI Factories in Kamloops, BC, and Rimouski, QC, delivering 500 MW of hydro-powered capacity across six sites.

- May 2025: Dell Technologies reported record USD 6.3 billion in servers and networking revenue, with USD 12.1 billion in AI orders booked for the quarter.

- May 2025: Arista Networks surpassed USD 2 billion quarterly revenue and unveiled Cluster Load Balancing for AI fabric.

- April 2025: Ericsson and Bell Canada completed AI-native link adaptation tests, boosting downlink throughput by 20%.

Canada Data Center Networking Market Report Scope

Data center networking refers to the set of technologies, protocols, and hardware used to connect physical and network-based devices and manage the network infrastructure, storage, and processing of applications and data. Data center networking is very critical for 100% uptime of data centers. In the current web-connected world, business workloads are executed on single computers, hence leading to the need for data center networking. Networks provide servers, clients, applications, and middleware with a standard plan to stage the execution of workloads and also to manage access to the data produced.

The Canada data center networking market is segmented by product (ethernet switches, routers, storage area network (SAN), application delivery controllers (ADC), and other networking equipment), by services (installation & integration, training & consulting, and support & maintenance), and by end-user (IT & telecommunication, BFSI, government, media & entertainment, and other end users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Products | Ethernet Switches |

| Routers | |

| Storage Area Network (SAN) | |

| Application Delivery Controllers (ADC) | |

| Network Security Appliances | |

| Software-Defined Networking (SDN) Controllers | |

| Optical Interconnects | |

| Services | Installation and Integration |

| Training and Consulting | |

| Support and Maintenance | |

| Managed Network Services |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Defense |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Other End-Users |

| Colocation |

| Hyperscalers/Cloud Service Providers |

| Edge/Micro Data Centers |

| Less than or equal to10 GbE |

| 25-40 GbE |

| 50-100 GbE |

| Greater Than 100 GbE |

| By Component | Products | Ethernet Switches |

| Routers | ||

| Storage Area Network (SAN) | ||

| Application Delivery Controllers (ADC) | ||

| Network Security Appliances | ||

| Software-Defined Networking (SDN) Controllers | ||

| Optical Interconnects | ||

| Services | Installation and Integration | |

| Training and Consulting | ||

| Support and Maintenance | ||

| Managed Network Services | ||

| By End-User | IT and Telecommunications | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Defense | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial | ||

| Other End-Users | ||

| By Data-Center Type | Colocation | |

| Hyperscalers/Cloud Service Providers | ||

| Edge/Micro Data Centers | ||

| By Bandwidth | Less than or equal to10 GbE | |

| 25-40 GbE | ||

| 50-100 GbE | ||

| Greater Than 100 GbE | ||

Key Questions Answered in the Report

What is the current size of the Canada data center networking market?

The market is valued at USD 710 million in 2025 and is projected to reach USD 980 million by 2030 at a 6.9% CAGR.

Which component segment is growing fastest?

Services are expanding at a 7.1% CAGR through 2030, outpacing product revenue growth.

Why are hyperscalers investing heavily in Alberta?

Alberta offers abundant renewable power, supportive provincial incentives and space for liquid-cooled, high-density facilities, attracting U.S. cloud providers.

How does the Huawei/ZTE ban affect networking projects?

Operators face 15-25% higher replacement costs and schedule delays as they shift to alternative vendors and redesign network architectures.

Page last updated on: