Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.86 Billion |

| Market Size (2026) | USD 7.14 Billion |

| Market Size (2031) | USD 8.71 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Home Appliances Market Analysis by Mordor Intelligence

The Canada home appliances market size is expected to grow from USD 6.86 billion in 2025 to USD 7.14 billion in 2026 and is forecast to reach USD 8.71 billion by 2031 at a 4.06% CAGR over 2026-2031. The Canada home appliances market is moving on a measured growth path, shaped by steady replacement cycles, energy-efficiency regulations, and a gradual shift toward connected products that promise lower operating costs and better user control. Manufacturers are aligning portfolios to meet stricter minimum performance standards while retailers balance in-store validation with online convenience as e-commerce gains weight in household durables. Household formation tied to immigration supports baseline demand even when mortgage costs and affordability strain discretionary upgrades. Policy harmonization with United States thresholds lowers compliance complexity for multinational brands, which is reinforcing a moderate but durable expansion in the Canada home appliances market[1]Government of Canada, “Regulations Amending the Energy Efficiency Regulations, 2016 (Amendment 18),” Canada Gazette, gazette.gc.ca.

Key Report Takeaways

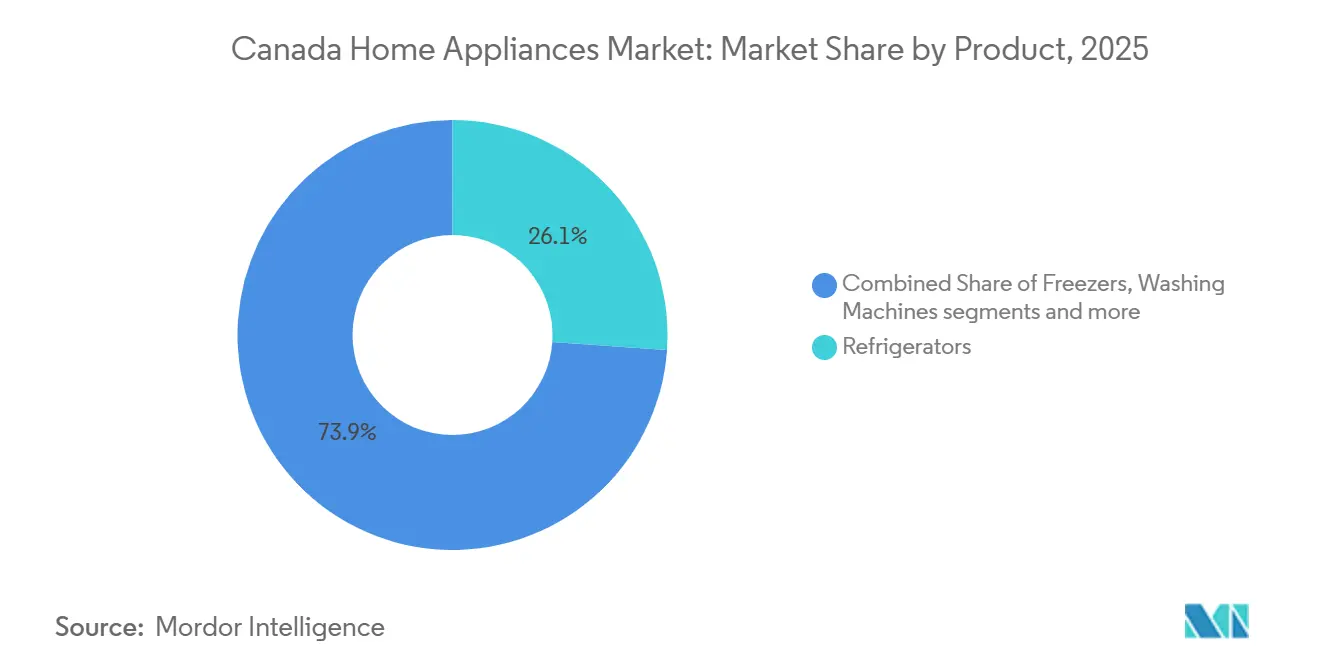

- By product type, refrigerators led with 26.12% of the Canada home appliances market share in 2025, while air fryers are projected to expand at a 4.49% CAGR through 2031.

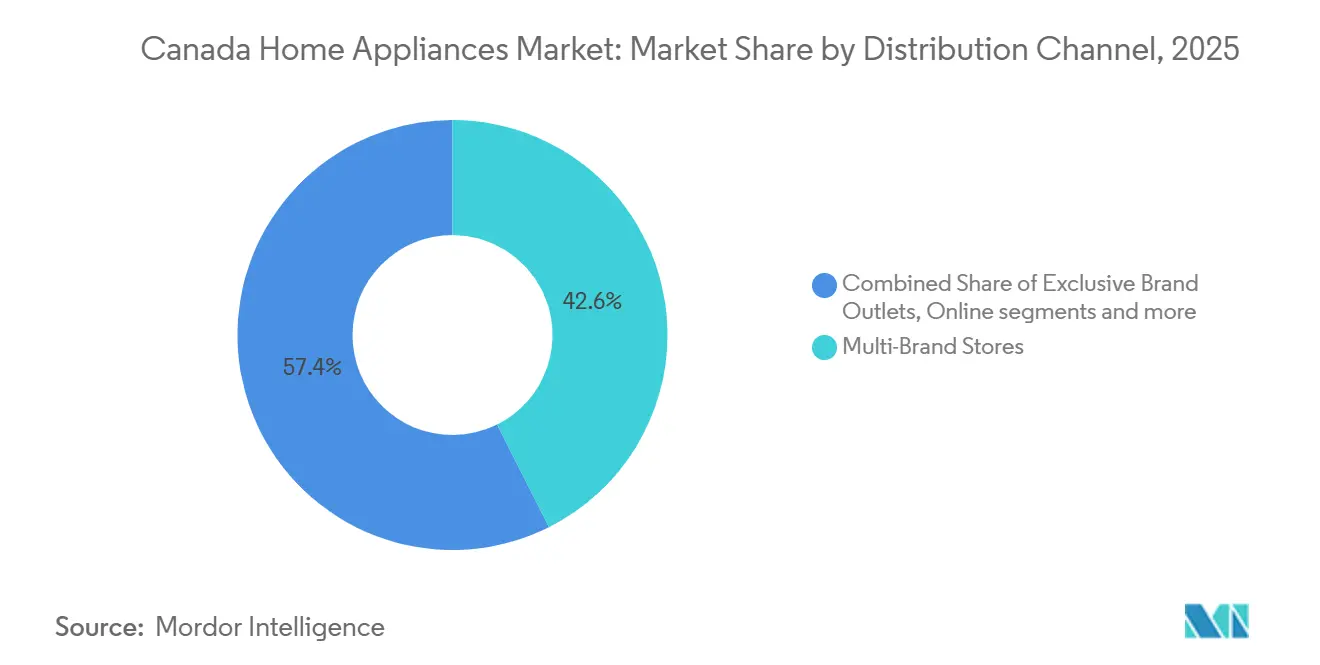

- By distribution channel, multi-brand stores held 42.55% of the Canada home appliances market share in 2025, whereas online retailing is forecast to grow at a 5.22% CAGR through 2031.

- By geography, Ontario accounted for 38.05% of the Canada home appliances market share in 2025, while Alberta is projected to grow at a 4.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Replacement-led demand and renovation cycles in aging housing stock | +1.2% | Ontario and Quebec | Medium term (2-4 years) |

| Energy-efficiency upgrades (ENERGY STAR) and rebate-driven retrofits | +0.8% | Ontario, British Columbia, Prince Edward Island | Short term (≤ 2 years) |

| Smart/connected appliance adoption and ecosystem integration | +0.6% | Toronto, Vancouver, Montreal metros | Long term (≥ 4 years) |

| Population growth and immigration-led household formation supporting incremental appliance demand | +0.7% | National, with higher concentration in GTA, Greater Vancouver, Greater Montreal | Medium term (2-4 years) |

| Electrification push: induction cooking and cold-climate heat pump appliances | +0.5% | British Columbia and Ontario, with spillover to Alberta | Long term (≥ 4 years) |

| Time-of-use electricity pricing spurring demand-response ready features | +0.3% | Ontario and Quebec | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Replacement-led Demand and Renovation Cycles in Aging Housing Stock

Canada’s housing base is sizable and mature, which supports repeat purchase cycles for large appliances on 12-15 year horizons and concentrates spending in repair-or-replace decisions when budgets tighten. Suppressed household formation has built a backlog of families waiting to form independent households as vacancy rates tightened, a condition that defers appliance purchases until supply catches up. Building permits surged to 242,000 net completions in 2023, yet household formation reached 460,000, sustaining a supply-demand imbalance that defers turnover and concentrates spending on repair-or-replace decisions rather than voluntary upgrades. Regional dynamics amplify this trend; Ontario and British Columbia households face shelter-cost-to-income ratios exceeding 55% for the 25-34 age cohort, suppressing headship rates and elongating multi-generational living arrangements that postpone independent household formation and the associated appliance purchases[2]PBO. "Household Formation and the Housing Stock," PBO, pbo-dpb.ca. This mix favors brands that offer reliable core models and step-up configurations that deliver tangible savings in energy and water over the product life.

Energy-Efficiency Upgrades (ENERGY STAR) and Rebate-Driven Retrofits

Provincial and federal rebates remain potent market accelerants. Ontario's November 2025 announcement commits CAD 10.9 billion over 12 years to energy-efficiency programs, including up to CAD 200 per household for energy-efficient refrigerators, freezers, and laundry machines[3]Jones, Allison. "Ontario expands energy efficiency programs to eligible appliances." CBC News, cbc.ca. Ontario requires appliances manufactured from January 1, 2025 onward to meet or exceed federal minimum energy performance standards or equivalent U.S. DOE levels, which raises the baseline and simplifies compliance choices for buyers. Rebates remain an important nudge, with BC Hydro offering instant savings on ENERGY STAR Tier 2 and Tier 3 washers, dryers, and refrigerators, and Prince Edward Island providing instant rebates on efficient laundry and refrigeration products. ENERGY STAR Most Efficient criteria set a clear north star for OEMs, pushing innovations in compressors, insulation, and control systems. Efficiency Canada estimates significant cumulative energy and emissions reductions from updated appliance standards, which unlock meaningful net consumer benefits as more efficient units replace legacy stock.

Smart/Connected Appliance Adoption and Ecosystem Integration

Matter connectivity, launched by the Connectivity Standards Alliance to unify smart-home protocols, reached Canadian shelves in 2025 when BSH Home Appliances shipped the first Matter-enabled refrigerator globally, the Bosch 100 Series French Door Bottom Mount, featuring cross-platform compatibility with Google Home and Amazon Alexa[4]BSH Home Appliances, “BSH Drives Matter Connectivity Standard Forward for Home Appliances,” Bosch Media Service US, us.bosch-press.com. GE Appliances introduced a hybrid heat pump water heater with native demand-response, leak detection, and app-based controls to align hot-water production with off-peak electricity windows. Samsung’s latest Bespoke AI Family Hub integrates on-device and cloud intelligence to streamline kitchen planning and coordination across connected laundry and cooking products. Policy proposals to expand the Energy Efficiency Act to include “energy demand performance” and “interoperability” indicate regulatory tailwinds for grid-aware appliances in the Canada home appliances market. As electric utilities integrate more variable generation into the grid, household devices that automate load-shifting should gain positioning advantages because they help consumers save money without daily micromanagement.

Population Growth and Immigration-Led Household Formation Supporting Incremental Appliance Demand

Household formation remains a bedrock source of incremental demand in the Canada home appliances market, even as affordability constraints delay some purchases. The Parliamentary Budget Officer projects a sizable increase in household count through 2030, which implies an ongoing need for core refrigeration, laundry, and cooking solutions. Newcomers often concentrate in large metro areas where landlords and property managers standardize on efficient, reliable appliances to meet energy codes and reduce service calls. This pattern supports consistent baseline volume in entry and mid-tier price bands while leaving headroom for premium connected models in urban cores. The net effect is a slow but steady expansion supported by demographics, with purchase timing shaped by rental cycles, turnover, and renovation activity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing affordability and high mortgage rates delaying big-ticket purchases | -0.6% | National, most acute in Toronto, Vancouver, Victoria | Short term (≤ 2 years) |

| Input cost volatility and logistics costs keeping ASPs elevated | -0.5% | National, with added friction in remote markets | Short term (≤ 2 years) |

| Retailer concentration and private labels intensifying price competition | -0.3% | Ontario and Quebec | Medium term (2-4 years) |

| Last-mile delivery/service gaps in remote/territorial markets | -0.2% | Northern Territories and remote communities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Housing Affordability and High Mortgage Rates Delaying Big-Ticket Purchases

Elevated borrowing costs and strained affordability are tamping down some large-ticket purchases, which moderates the premium mix in the Canada home appliances market during promotional windows. Retail data for December 2025 shows a monthly decline for electronics and appliance-focused retailers, which underscores consumers’ cautious stance at year's end. Consumers continue to prioritize essential replacements, placing more scrutiny on payback periods for step-up features such as advanced water filtration, AI-enabled cycles, or connectivity. This behavior keeps promotional intensity high while pushing OEMs to communicate total cost of ownership gains more clearly. The restraint is most visible in metros with high shelter-cost-to-income ratios, where move-up purchases that typically trigger appliance turnover are deferred longer.

Input Cost Volatility and Logistics Costs Keeping ASPs Elevated

Tariff policy, freight variability, and materials pricing have added cost pressure that is difficult to pass through fully when demand is uneven. Some categories have seen tariff exposure diminish, which eases margin pressure for certain brands and channels, while other inputs remain volatile. Retailers are shortening contract cycles and sharpening inventory control to reduce over-ordering and to protect margins, especially in seasonal categories that swing with weather and promotions. National assortments continue to prioritize in-line models with reliable supply and factory service coverage, which mitigates stockout risk when logistics fluctuate. The combined effect is a cautious posture on pricing and procurement while brands invest in automation and vertical integration to stabilize cost structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators Anchor Share While Air Fryers Drive Volume Growth

Refrigerators accounted for 26.12% of the 2025 category market size in the Canada home appliances market, reflecting near-universal household penetration and disciplined replacement cycles that sustain steady throughput. ENERGY STAR Most Efficient criteria are encouraging the shift to inverter compressors and advanced insulation, which elevates lifetime savings and supports premium step-ups within the Canada home appliances industry. OEMs have aligned roadmaps with this trend: BSH introduced the first Matter-enabled refrigerator globally to improve cross-platform control, and Samsung’s latest Bespoke AI flagship showcases food-recognition and list automation that deepen kitchen integration. Premium refrigeration now features software and filtration advances, along with flexible configurations that help users reduce food waste and manage energy in real time. Air fryers are forecast to grow at a 4.49% CAGR through 2031 on the strength of countertop convenience and perceived energy savings, which expands the addressable base in small urban kitchens and rental units in the Canada home appliances market.

Dishwashers and laundry continue to benefit from efficiency and water-saving innovations. Efficiency Canada highlights updated energy thresholds for dishwashers and washers that tighten allowable consumption, a signal that the product pipeline is ready for higher baselines. Brands are pairing performance with conservation features, as seen in Beko’s models that reduce water use per cycle through smart reuse of rinse water, paired with sensor-driven cycle optimization. Laundry portfolios lean into heat pump drying and AI cycle management, while hybrid heat pump water heaters sit adjacent to appliance decisions in renovation bundles. The Canada home appliances market share dynamics in large appliances are stable, with innovation centered on efficiency, ease of use, and connected convenience rather than raw capacity growth.

By Distribution Channel: Multi-Brand Stores Retain Leadership as Online Accelerates

Multi-brand stores held 42.55% of the 2025 distribution market size in the Canada home appliances market, supported by showrooms where live demos enable trust for premium categories such as built-in refrigeration and professional-style ranges. Canada’s largest appliance-only chain, Canadian Appliance Source, operates dozens of locations across major provinces and combines in-store validation with online fulfillment, an approach that aligns with how consumers research and buy appliances. Online retail is projected to deliver a 5.22% CAGR through 2031 as visualization tools, delivery scheduling, and seamless returns improve, and as overall retail e-commerce sales advanced in late 2025. Luxury brands are investing in curated experiences and specialized retail to lift conversion on high-consideration purchases, which supports value capture at the top of the category.

The interplay between channels is fluid, and omnichannel continues to strengthen in the Canada home appliances industry. Builders and contractors remain an important route for project-based sales, and industry data indicate that appliances are commonly included in purchase agreements, which stabilizes volumes even when retail foot traffic softens. Promotions, rebates, and loyalty programs connect in-store advice with online price transparency, which keeps share shifting toward retailers that combine strong digital UX with dependable local service. Exclusive brand outlets and showrooms, such as Fisher & Paykel’s space in Toronto, anchor experiential selling that lifts close rates on premium models and complements multi-brand distribution in large metros. Across channels, clear articulation of efficiency benefits and connected features has become central to merchandising in the Canada home appliances market.

Geography Analysis

Ontario accounted for 38.05% of 2025 revenue in the Canada home appliances market, supported by dense urban demand and policies that align appliance standards with national requirements. The province adopted efficiency requirements that anchor purchasing decisions around compliant models and streamline stocking across large retail chains. Retail sales in December 2025 showed a small monthly decline for Ontario, but the resilience of core urban corridors remained visible in major CMAs, which shows steady in-person engagement for high-touch categories. Time-of-use rate structures and emerging demand-response programs set the stage for connected features that optimize operation schedules without day-to-day effort from users. This policy environment and retail footprint sustain leadership for the province within the Canada home appliances market.

Quebec ranks as a large, distinct market with strong public-power programs and consumer protection that supports repairability and longer useful life. Right-to-repair and labeling rules influence product selection and service practices, which lengthen replacement intervals and support a robust service ecosystem. Provincial incentives for peak-shaving and energy savings, together with relatively low-cost electricity, reinforce the appeal of efficient refrigeration, laundry, and connected water heating in multi-family portfolios. December 2025 retail patterns showed variability across Quebec’s urban and rural segments, which underlines the importance of localized assortments and service coverage for the Canada home appliances market.

Alberta is projected to be the fastest-growing large province through 2031 in the Canada home appliances market, supported by migration and energy-sector incomes that sustain household formation. Atlantic Canada benefits from targeted incentives, with Prince Edward Island’s instant rebates exemplifying how well-structured programs can lift adoption for efficient laundry and refrigeration in cost-sensitive households. Remote and territorial communities remain constrained by logistics and service coverage, which tempers penetration of connected models and sustains demand for durable, serviceable designs in the Canada home appliances market.

Competitive Landscape

The Canada home appliances market features moderate fragmentation. The top five companies, Whirlpool, Haier, Samsung, Robert Bosch, and Electrolux, account for roughly over half of unit sales, which leaves room for mid-tier specialists and premium brands to differentiate through service, regional packaging, and focused retail experiences in the Canada home appliances market. Product roadmaps have converged on three pillars: energy efficiency, connected convenience, and premium design, each supported by active launches and platform investments in 2025 and 2026.

BSH extended connected leadership by shipping the first Matter-enabled major appliance and unveiling Bosch Cook AI, a kitchen assistant that coordinates multi-appliance workflows through Home Connect. GE Appliances launched the GE Profile GEOSPRING Smart Hybrid Heat Pump Water Heater with native demand-response, leak detection, and app control, aligning with utility programs and time-of-use pricing strategies. Samsung’s Bespoke AI Family Hub integrated Google’s Gemini to automate pantry tracking and meal planning, while its laundry and floor-care platforms highlighted on-device intelligence focused on convenience and energy savings for the Canada home appliances market.

LG expanded its Signature Kitchen Suite range for North America with AI-enabled laundry and flexible induction, raising competitive stakes in the builder and luxury segments. Miele scaled consumer engagement with its largest-ever Canadian campaign focused on longevity and engineering, which supports premium positioning in key metros. Fisher & Paykel opened a Toronto showroom to create hands-on experiences and added a time-bound promotional incentive to stimulate trial. Hisense broadened its ConnectLife ecosystem and previewed next-wave refrigeration and compact laundry concepts, reflecting innovation in entry and mid-tier price points. Whirlpool signaled continued investment in North American manufacturing and automation through a strategic recapitalization and highlighted portfolio-wide innovations at KBIS 2026. Beko emphasized measurable water savings with new dishwasher features, aligning with conservation priorities that are increasingly central to Canadian buyers in urban regions.

Canada Home Appliances Industry Leaders

-

Whirlpool Corporation

-

Samsung Electronics

-

LG Electronics

-

GE Appliances (a Haier company)

-

Electrolux Group (Frigidaire)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: At CES 2026, Samsung Electronics unveiled its bespoke AI appliance lineup, spotlighting the bespoke AI refrigerator family hub with Google Gemini integration, AI hybrid cooling, the bespoke AI laundry combo, and the Jet Bot Steam Ultra robot vacuum, all tailored for the Canadian audience.

- September 2025: Miele Canada introduced the rumoured for a reason campaign. It was the most significant advertising push in North America, rolled out across major Canadian cities like Toronto, Vancouver, Montreal, and Calgary, transforming heritage into captivating narratives.

- April 2025: Monogram luxury appliances began a two-year partnership with Canadian designer Lauren Kyle McDavid. She was appointed as the official Canadian design ambassador and tasked with heading the Monogram design council to create content targeting affluent renovation enthusiasts.

- January 2025: The Ontario government, under a USD 10.9 billion 12-year initiative, launched expanded energy efficiency programs. A key feature is the home renovation savings program, which offers families rebates of up to 30% on energy-efficient upgrades and appliances to reduce power consumption.

Canada Home Appliances Market Report Scope

Home appliances are machines designed to aid in various household tasks, including cooking, cleaning, and food preservation. These appliances can be broadly classified into three categories, namely major appliances, small appliances, and consumer electronics.

The Canadian home appliance market is segmented by major appliances, small appliances, and distribution channel. By major appliances, the market is segmented into refrigerators, freezers, dishwashing machines, washing machines, and cookers and ovens. By small appliances, the market is segmented into vacuum cleaners, small kitchen appliances, hair clippers, irons, toasters, grills and roasters, hair dryers, and other small appliances. By distribution channel, the market is segmented into multi-brand stores, exclusive stores, online, and other distribution channels. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Counter-top Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Ontario |

| Québec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Counter-top Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Ontario | |

| Québec | ||

| British Columbia | ||

| Alberta | ||

| Rest of Canada | ||

Key Questions Answered in the Report

What is the 2026 size and growth outlook for the Canada home appliances market?

The Canada home appliances market size in 2026 is estimated USD 7.14 billion, and it is projected to reach USD 8.71 billion by 2031 at a 4.06% CAGR.

Which product categories lead demand in Canada home appliances?

Refrigerators lead by revenue with a 26.12% share in 2025, while air fryers are the fastest-growing category through 2031.

How are channel dynamics shifting for appliances in Canada?

Multi-brand stores remain the largest channel, and online is the fastest-growing route as visualization, delivery, and return experiences improve.

Which provinces are the most important for appliance sales?

Ontario leads with 38.05% of 2025 revenue, and Alberta is projected to be the fastest-growing province through 2031.

What policies are shaping energy-efficient appliance adoption?

Amendment 18 to the federal Energy Efficiency Regulations and Ontario’s O. Reg. 399/24 raise performance baselines, while provincial rebates like BC Hydro and PEI programs nudge purchases toward efficient models.

How do connected features influence purchasing decisions in Canada appliances?

Interoperability, demand-response readiness, and app-enabled monitoring are becoming differentiators as policy and rate design reward load-shifting and energy savings.

Page last updated on: