Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.36 Billion |

| Market Size (2026) | USD 4.62 Billion |

| Market Size (2031) | USD 6.42 Billion |

| Growth Rate (2026 - 2031) | 6.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Dairy-Based Beverages Market Analysis by Mordor Intelligence

The Africa dairy-based beverages market size was valued at USD 4.36 billion in 2025 and is estimated to grow from USD 4.62 billion in 2026 to reach USD 6.42 billion by 2031, at a CAGR of 6.80% during the forecast period (2026-2031). This growth is driven by factors such as rapid urbanization, the premiumization of fermented products, and advancements in retail infrastructure, which are encouraging a shift in consumer preferences from commoditized fresh milk to higher-margin functional beverages. Products like probiotic drinks fortified with live cultures, lactose-reduced formulations enabled by in-line lactase dosing, and on-the-go yogurt smoothies are gaining popularity and outpacing fluid milk in modern trade channels. On the supply side, challenges such as raw milk seasonality, disease outbreaks in South Africa and North Africa, and rising feed costs are encouraging processors to invest in aseptic technology and longer-shelf-life packaging solutions. Multinational companies, including Danone, Nestlé, and Lactalis, are leading innovation in the category, while regional players are focusing on strengthening farmer networks and cold-chain infrastructure to ensure quality and maintain margins. Despite structural challenges such as widespread lactose intolerance and increasing competition from plant-based alternatives, these factors support resilient volume growth, positioning the Africa dairy-based beverages market for sustained expansion over the coming years.

Key Report Takeaways

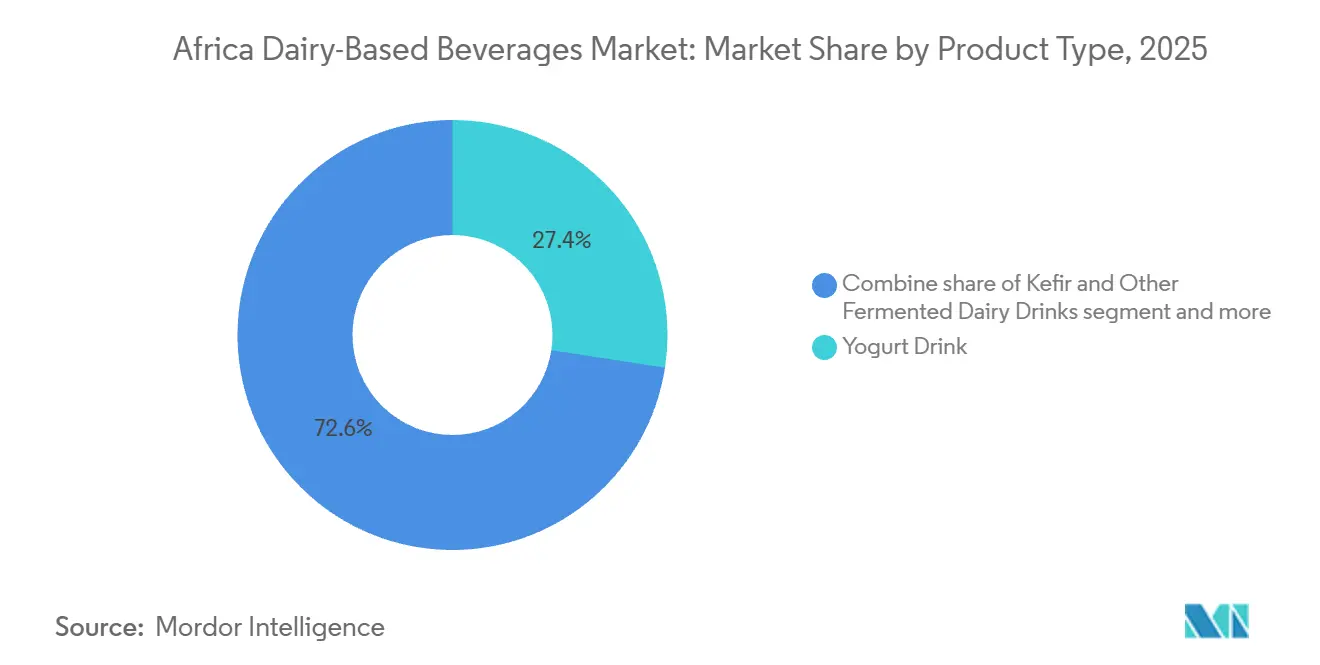

- By product type, yogurt drink captured 27.43% revenue share in 2025, whereas kefir and other fermented dairy drinks are forecast to grow at a 7.04% CAGR through 2031.

- By fat content, whole-fat beverages accounted for 55.21% of 2025 sales, while low-fat variants are projected to advance at a 7.49% CAGR to 2031.

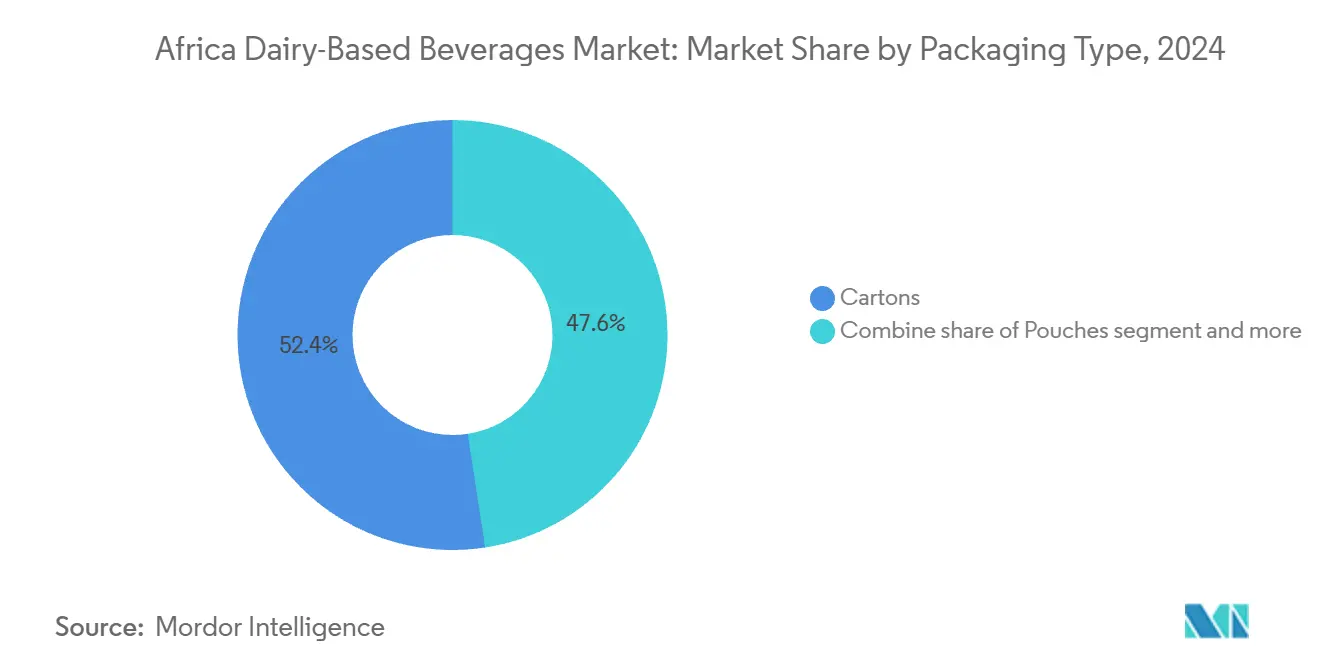

- By packaging type, cartons dominated with 52.43% share in 2025; pouches are expected to expand at a 7.72% CAGR during the outlook period.

- By distribution channel, off-trade held 64.54% of 2025 revenue, whereas on-trade outlets will post the fastest growth at 7.73% CAGR to 2031.

- By geography, South Africa led with 29.21% market value in 2025, while Nigeria is poised for the highest regional CAGR of 7.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Dairy-Based Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional and probiotic beverages | +1.5% | Global, with early traction in South Africa, Egypt, Kenya | Medium term (2-4 years) |

| Innovation in flavored and value-added milk | +1.2% | Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Emergence of lactose-reduced and easier-to-digest dairy drinks | +1.0% | Kenya, South Africa, urban Nigeria | Medium term (2-4 years) |

| Adoption of ready-to-drink formats for on-the-go lifestyles | +1.3% | Urban centers across South Africa, Nigeria, Egypt | Short term (≤ 2 years) |

| Expansion of modern retail and refrigerated shelves | +0.9% | South Africa, Kenya, Nigeria, Egypt | Long term (≥ 4 years) |

| Growing popularity of drinkable yogurt and yogurt smoothies | +1.4% | Egypt, South Africa, Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for functional and probiotic beverages

Across Africa, consumers are increasingly viewing dairy beverages as products that deliver live cultures offering digestive and immune health benefits, rather than simply as sources of protein and calcium. Research published in the Journal of Dairy Science highlights that lactic acid bacteria and bifidobacteria strains can survive gastric transit and colonize the gut when included in fermented milk at concentrations exceeding 107 colony-forming units per milliliter. De Novo Dairy's precision-fermentation platform, which produces dairy proteins without relying on cows, secured partnerships in 2024 to supply African co-packers seeking clean-label probiotic bases. In Egypt, Juhayna's Greek and stirred yogurt lines have successfully leveraged this trend, contributing to the company's 59 percent market share in drinkable yogurt and 30 percent share in spoonable yogurt during fiscal 2024. Additionally, urban retailers in Nairobi and Johannesburg have reported that probiotic-labeled stock-keeping units (SKUs) command price premiums of 15 percent to 25 percent over standard yogurt drinks, reflecting a growing consumer willingness to pay for perceived health benefits.

Innovation in flavored and value-added milk

Flavored milk products, enriched with vitamins, minerals, or plant extracts, are steadily replacing plain white milk on supermarket shelves as manufacturers aim for higher profit margins and cater to younger consumers. The Dairy Standard Agency of South Africa reported that the production of sweetened, flavored, or colored milk increased by 9% during the first nine months of 2024 compared to the same period in the previous year, surpassing the growth rate of plain fluid milk. In 2024, Nestlé Nigeria expanded its NIDO fortified milk powder range and introduced ready-to-drink MILO. Furthermore, Kerry Group launched lactase enzyme solutions in East African dairies, which allow the production of lactose-free chocolate and strawberry milk without compromising sweetness or texture. A pilot project conducted by the International Livestock Research Institute in Kenya demonstrated that lactose-hydrolyzed milk achieved a 92% consumer acceptability score while effectively addressing digestive discomfort in lactose-intolerant participants [1]Source: International Livestock Research Institute, “MoreMilk: More milk for lives and livelihoods in Kenya,” ilri.org.

Emergence of lactose-reduced and easier-to-digest dairy drinks

Genetic studies show that lactase persistence, which refers to the ability to digest lactose into adulthood, remains uncommon across sub-Saharan Africa, with prevalence rates below 20% in most populations outside pastoralist communities [2]Source: National Institute of Diabetes and Digestive and Kidney Diseases, “Definition & Facts for Lactose Intolerance,” niddk.nih.gov. This physiological characteristic has encouraged processors to focus on developing lactose-free or lactose-reduced formulations that maintain the nutritional benefits of dairy while addressing gastrointestinal discomfort. In 2023, Brookside Dairy in Kenya introduced a lactose-free fresh milk line and expanded its product range with almond milk variants, aiming to cater to the 42% of Kenyans who experience lactose malabsorption. Tetra Pak's processing solutions, implemented across Africa in 2024 and 2025, include in-line lactase dosing technology that hydrolyzes lactose during ultra-high-temperature treatment, resulting in products with less than 0.1 gram of lactose per 100 milliliters. Research conducted by the International Livestock Research Institute in Kenya, Tanzania, and Uganda confirmed that lactose-reduced milk can increase daily dairy consumption by 30% to 40% among previously intolerant consumers, thereby unlocking latent demand.

Adoption of ready-to-drink formats for on-the-go lifestyles

Urbanization and the increasing duration of daily commutes are significantly influencing consumer behavior, leading to a shift from traditional sit-down breakfasts to more convenient mobile snacking options. This change has driven a growing preference for single-serve packaging formats such as bottles, pouches, and cans, as opposed to bulk cartons. Tiger Brands, a South African food conglomerate, reported that its Snacks, Treats, and Beverages segment generated revenue of South African Rand (ZAR) 6.0 billion (USD 333 million) in fiscal year 2025. This represents a growth of 3.1 percent compared to the previous year. Within this segment, beverage dilutables achieved a positive volume market share over the 12 months ending September 2025. Tetra Pak's ambient drinking-yogurt solutions, which do not require a cold chain for storage or transportation, have enabled processors in Nigeria and Egypt to distribute probiotic beverages to inland towns where reliable refrigeration is often unavailable. These innovative solutions have also extended the shelf life of such products to 12 months, effectively addressing logistical challenges in these regions. In addition, SIG Combibloc Group's spouted pouches and bag-in-box packaging formats, introduced to African contract packers in 2024, have reduced packaging weight by 30 percent compared to rigid bottles. This reduction in weight has also lowered transportation costs, making ready-to-drink yogurt a more economically viable option for rural markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of lactose intolerance and dairy allergies | -1.2% | Nigeria, Ethiopia, Uganda, Tanzania, Kenya | Long term (≥ 4 years) |

| Competition from plant-based and non-dairy alternatives | -0.8% | South Africa, Kenya, urban Egypt | Medium term (2-4 years) |

| Volatility in raw milk supply and quality | -0.9% | Kenya, Ethiopia, Rwanda, Uganda, Zambia, Tanzania | Short term (≤ 2 years) |

| Disease outbreaks in dairy herds | -0.6% | South Africa, North Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High prevalence of lactose intolerance and dairy allergies

Approximately 68% of the global population experiences some level of lactose malabsorption, with rates surpassing 80% in countries such as Nigeria, Ethiopia, and Uganda, according to data from the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK). Lactose malabsorption refers to the body's reduced ability to digest lactose, a sugar found in milk and dairy products, due to insufficient production of the enzyme lactase. A 2024 study published in *Nutrients* found that 52% of Tanzanian adults and 42% of Kenyan adults exhibited lactose intolerance in breath-hydrogen tests, which measure the amount of hydrogen in the breath as an indicator of undigested lactose. This condition limits their ability to consume conventional fluid milk without experiencing gastrointestinal discomfort, such as bloating, diarrhea, or abdominal pain. Genetic research has identified specific variants of the lactase (LCT) gene, commonly found in African populations, that reduce lactase production after weaning. This genetic trait creates a structural barrier to dairy consumption, making it challenging for individuals to include traditional dairy products in their diets. While lactose-free and lactose-reduced products provide a solution to this issue, they require additional processing steps and enzyme inputs, which increase production costs by 8% to 12%. These higher costs compress profit margins for dairy processors, particularly in price-sensitive markets where affordability is a key concern. Additionally, dairy allergies, which are distinct from lactose intolerance, affect a smaller portion of consumers. Unlike lactose intolerance, which is related to enzyme deficiency, dairy allergies involve immune system reactions that can trigger severe symptoms, further narrowing the addressable market for dairy products.

Competition from plant-based and non-dairy alternatives

Oat, almond, soy, and coconut beverages are increasingly gaining shelf space in African supermarkets, particularly in South Africa and Kenya. Urban consumers in these regions perceive plant-based options as healthier, more sustainable, or aligned with vegan lifestyles. In 2023, Brookside Dairy introduced an almond milk product line, acknowledging that some consumers are unlikely to return to conventional dairy products, even with lactose-free formulations. Similarly, Juhayna's Nature and Goodness (N&G) brand in Egypt offers almond-based beverages, targeting health-conscious millennials who associate plant proteins with benefits such as weight management and environmental sustainability. While plant-based alternatives currently represent a low single-digit share of total beverage volume in Africa, growth trends in developed markets suggest that adoption in Africa will likely accelerate as local production scales up and import tariffs are reduced. Dairy processors face a strategic challenge: investing in plant-based product lines risks cannibalizing core dairy revenues, but ignoring this segment allows startups and multinational competitors to capture market share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fermented Formats Outpace Conventional Milk

Yogurt Drinks accounted for 27.43% of market revenue in 2025, reflecting consumer demand for tangy, probiotic-rich beverages that serve as both snacks and meal replacements. Kefir and Other Fermented Dairy Drinks, while smaller in overall volume, are projected to grow at an annual rate of 7.04% through 2031. This growth is driven by urban consumers' interest in traditional fermentation methods and higher live-culture content. Probiotic Milk, which includes fortified fluid milk with added Lactobacillus or Bifidobacterium strains, appeals to health-conscious households willing to pay a premium for functional health benefits.

The Others category includes flavored milk, sweetened condensed milk drinks, and hybrid products that combine dairy with fruit juice or plant proteins. Juhayna's drinkable yogurt portfolio, which holds a majority market share in Egypt, demonstrates how manufacturers can dominate a segment by offering Greek-style, stirred, and fruit-blended variants to meet diverse consumer preferences. Tetra Pak's ambient drinking-yogurt solutions, introduced in Nigeria and Egypt in 2024 and 2025, provide a 12-month shelf life without refrigeration. This innovation enables distribution to inland areas and helps reduce spoilage-related losses.

By Fat Content: Whole-Fat Dominance Yields to Health-Conscious Shifts

Whole-fat or full-fat dairy beverages are projected to account for 55.21% of volume in 2025, driven by consumer preferences for taste, satiety, and cultural norms that associate richness with quality. However, low-fat formulations are expected to grow at an annual rate of 7.49% through 2031, as urban consumers increasingly adopt calorie-conscious diets and respond to public health messaging regarding cardiovascular risks. Skimmed or non-fat variants remain a niche category, primarily appealing to fitness enthusiasts and diabetic patients who prioritize protein intake over fat content.

According to South Africa's Dairy Standard Agency, retail sales of ultra-high-temperature milk increased by 1.6% in the 12 months ending July 2024, with low-fat and skimmed SKUs accounting for a significant share of the incremental volume. Nestlé Nigeria's beverage portfolio, which generated NGN 342.3 billion (USD 228 million) in 2024, includes both full-cream and reduced-fat NIDO variants, enabling the company to cater to diverse consumer segments.

By Packaging Type: Pouches Challenge Carton Supremacy

In 2025, cartons accounted for 52.43% of the packaging volume. This was supported by well-established supply chains, consumer familiarity, and their suitability for both refrigerated and ambient distribution. Pouches are expected to grow at an annual rate of 7.72% through 2031, driven by benefits such as lower material costs, reduced transport weight, and convenience for on-the-go consumption.

Bottles, primarily made of plastic or glass, cater to premium segments where features like transparency and resealability justify higher packaging costs. Cans remain a niche option, mainly used for sweetened condensed milk drinks and energy-fortified dairy beverages. The "Others" category includes bag-in-box formats and bulk dispensers, which are primarily utilized in food-service channels. SIG's spouted pouches, introduced to African co-packers in 2024, reduce packaging weight by 30% compared to rigid bottles and offer single-handed consumption, making them appealing to commuters and schoolchildren.

By Distribution Channel: Off-Trade Leads, On-Trade Accelerates

Off-Trade channels, which include supermarkets, hypermarkets, convenience stores, specialty stores, and online retail, accounted for 64.54% of sales in 2025. This reflects the strong preference for take-home consumption. On-Trade outlets, such as cafés, quick-service restaurants, and hotel breakfast buffets, are expected to grow at an annual rate of 7.73% through 2031. This growth is driven by factors such as increasing urbanization and rising disposable incomes.

Within the Off-Trade sub-segments, supermarkets and hypermarkets continue to dominate due to their wide product assortments, promotional pricing, and availability of refrigerated displays that encourage impulse purchases. Convenience stores and fuel stations are adding cold vaults to meet the growing demand for grab-and-go products. Online retail, however, remains in its early stages outside South Africa and Kenya, primarily due to challenges in last-mile logistics and consumer preferences for inspecting perishables before purchase. Specialty stores, such as health-food boutiques and organic grocers, serve niche markets by offering products like lactose-free, probiotic, or plant-based options.

Geography Analysis

South Africa led the market in 2025, capturing 29.21 percent of the market value. This performance was supported by a dairy sector with a gross value of approximately ZAR 25 billion (USD 1.39 billion) in 2023 and around 984 commercial milk producers [3]Source: U.S. Department of Agriculture, “Nigeria: Overview of the Dairy Market and US Export Opportunities,” fas.usda.gov. About 10 processors, including Clover, Lactalis, Danone, Nestlé, and Woodlands, controlled 70 percent of the volume, creating a moderately consolidated competitive landscape. Ultra-high-temperature (UHT) and sterilized milk accounted for 28 percent of unprocessed milk utilization, while fermented products such as maas and yogurt represented 15 percent. Retail sales of UHT milk increased by 1.6 percent in the 12 months ending July 2024, and the production of sweetened, flavored, or colored milk rose by 9 percent in the first nine months of 2024. A foot-and-mouth disease outbreak in 2024 affected 37 farms in KwaZulu-Natal and Eastern Cape, leading to the culling of approximately 430 cattle and temporary movement restrictions that delayed deliveries. Lactalis South Africa introduced its Parmalat Protein range in 2024, offering protein yogurt and protein milk aimed at fitness-oriented consumers.

Nigeria is expected to be the fastest-growing segment, with an annual growth rate of 7.87 percent through 2031. This growth is driven by the National Dairy Policy launched in June 2024, which aims to scale domestic production and reduce the country's USD 1.5 billion annual dairy import bill. Domestic production reached 600,000 tonnes in 2024, leaving a significant supply gap filled by imports of fat-filled milk powder and UHT milk. In 2025, UAC of Nigeria acquired Chi Limited, the owner of the Hollandia yogurt drink and Chivita juice brands, from The Coca-Cola Company, signaling consolidation and increased investment in local manufacturing.

Other notable developments include Egypt's market, where drinkable yogurt holds a 59 percent share of the category and is supported by exports to over 40 international markets. The company operates 39 distribution centers and serves 243,000 retail outlets, combining modern retail chains with traditional grocers. Juhayna's product portfolio includes fresh milk (58 percent plain milk share, 51 percent flavored milk share), Greek and stirred yogurt (30 percent spoonable yogurt share), and plant-based almond beverages under the N&G brand. In Kenya, Brookside Dairy, in which Danone holds a 40 percent stake, commands 40 to 45 percent of processed milk volume. The company sources milk from more than 200,000 farmers across 27 counties.

Competitive Landscape

The Africa dairy beverages market is moderately concentrated. Multinational companies, including Danone, Nestlé, and Lactalis, compete with notable regional players such as Juhayna, Brookside, Clover, and FrieslandCampina WAMCO. In South Africa, approximately 10 processors account for 70% of the market volume. Conversely, in Nigeria and Kenya, the market is more fragmented, with informal traders and artisanal dairies holding substantial shares, especially in rural areas.

Vertical integration has become a key strategy in the market, covering farm-level cooling infrastructure to retail distribution networks. For example, Juhayna operates four plants and 39 distribution centers, while Brookside sources from over 200,000 farmers and invested Kenyan Shilling (KSh) 112 million (USD 867,000) in cooling tanks in July 2025. Aseptic packaging technology, licensed from Tetra Pak and SIG Combibloc, enables ambient distribution and eliminates reliance on unreliable cold chain systems. This provides a competitive advantage in regions where refrigeration infrastructure is insufficient to meet demand.

Opportunities remain in the lactose-free and plant-based segments, where local production capacity struggles to meet growing consumer demand. This gap forces retailers to import premium-priced alternatives from Europe and Asia. Brookside's 2023 launch of almond milk and Juhayna's N&G plant-based brand highlight how established players are diversifying to address structural constraints in the dairy market. Smaller players, such as Inyange Industries in Rwanda and Pearl Dairy Farms in Uganda, are leveraging local sourcing and catering to regional taste preferences to compete with larger multinational firms. However, limited access to capital and advanced technology continues to pose significant challenges for these smaller companies. Regulatory compliance also plays a critical role in shaping competitive dynamics. Adherence to Codex Alimentarius standards, including microbial limits and aflatoxin thresholds, is essential. For example, the Kenya Dairy Board's 2023 to 2025 import-permit restrictions on Brookside's Ugandan milk illustrate how regulatory standards can act as non-tariff barriers within the market.

Africa Dairy-Based Beverages Industry Leaders

Danone S.A.

Nestlé S.A.

Clover Industries Ltd

Lactalis Group

Brookside Dairy Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: CoolMilk launched a groundbreaking rural dairy innovation initiative in Bloemfontein, South Africa, in partnership with an agri‑business network. The programme targets smallholder farmers, improving access to dairy production resources, technical support, and market linkages to strengthen rural livelihoods and dairy sector productivity in the region.

- October 2025: Danone launched the Danone Milk Academy, a global farmer-upskilling initiative designed to improve milk quality, animal welfare, and sustainable practices across its supply chains, with modules tailored to African smallholders in Kenya, South Africa, and Morocco

- November 2024: Clover S.A. Proprietary Limited launched two new dairy beverages in South Africa: Clover 1L UHT Flavoured Milk (Chocolate and Strawberry variants) with added Vitamin D and calcium, and no added sugar, plus Tropika Drinking Yoghurt combining tropical fruit flavours with yoghurt goodness.

Africa Dairy-Based Beverages Market Report Scope

Dairy-based beverages are drinks made by combining milk fat and other milk-derived solids. The African dairy-based beverages market is segmented by type into Probiotic Milk, Yogurt Drinks, Kefir and Other Fermented Dairy Drinks, and Others. The market is further segmented by fat content into Whole/Fat, Low-Fat, and Skimmed/Non-Fat. Based on packaging type, the market is categorized into Cartons, Bottles, Pouches, Cans, and Others. Distribution channels are divided into On-Trade and Off-Trade. The Off-Trade segment is further sub-segmented into Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, and Others. Additionally, the study examines key regions, including South Africa, Egypt, Nigeria, and the Rest of Africa. The market sizing has been done in value terms in USD and Volume in Liters for all the abovementioned segments.

By Product Type

| Probiotic Milk |

| Yogurt Drink |

| Kefir and Other Fermented Dairy Drinks |

| Others |

By Fat Content

| Whole/Fat |

| Low-fat |

| Skimmed/Non-fat |

By Packaging Type

| Cartons |

| Bottles |

| Pouches |

| Cans |

| Others |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Others |

By Geography

| South Africa |

| Egypt |

| Nigeria |

| Kenya |

| Rest of Africa |

| By Product Type | Probiotic Milk | |

| Yogurt Drink | ||

| Kefir and Other Fermented Dairy Drinks | ||

| Others | ||

| By Fat Content | Whole/Fat | |

| Low-fat | ||

| Skimmed/Non-fat | ||

| By Packaging Type | Cartons | |

| Bottles | ||

| Pouches | ||

| Cans | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Africa dairy-based beverages market in 2031?

It is forecast to reach USD 6.42 billion by 2031, growing at a 6.8% CAGR.

Which country is expected to record the fastest growth rate through 2031?

Nigeria is projected to advance at a 7.87% CAGR, supported by its 2024 National Dairy Policy.

Which product category currently leads revenue contributions?

Yogurt Drink held 27.43% of 2025 revenue, making it the largest category.

How significant is lactose intolerance to market strategy?

With intolerance rates above 80% in several African countries, processors increasingly launch lactose-free and plant-based lines to capture sensitive consumers.

What packaging format is gaining share most rapidly?

Pouches are forecast to grow at 7.72% CAGR, driven by lower cost and on-the-go convenience.

Page last updated on: