MEMS Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.24 Billion |

| Market Size (2031) | USD 29.08 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

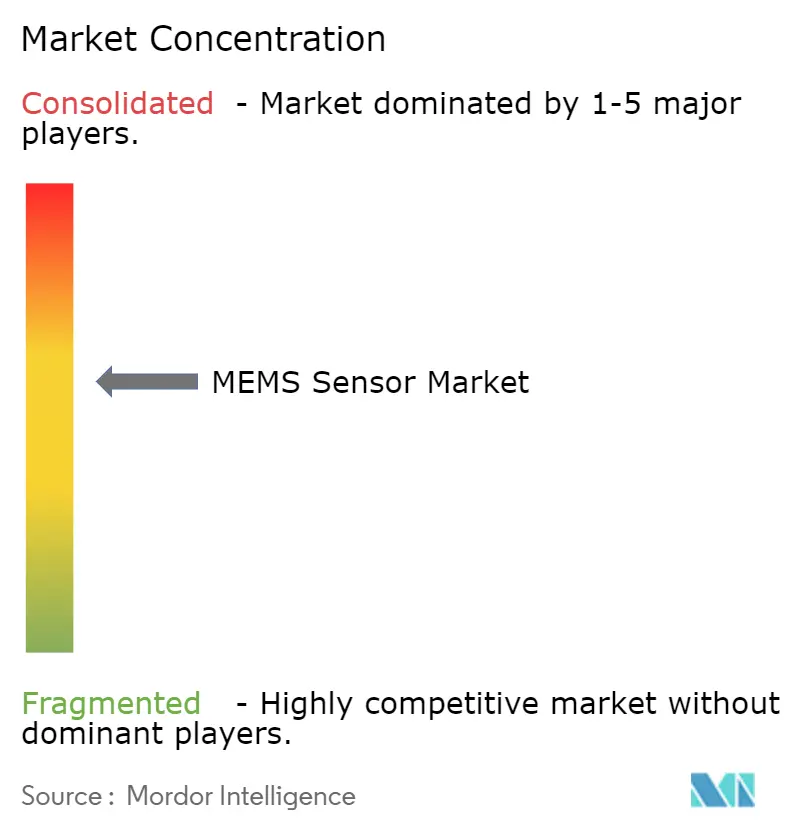

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MEMS Sensor Market Analysis by Mordor Intelligence

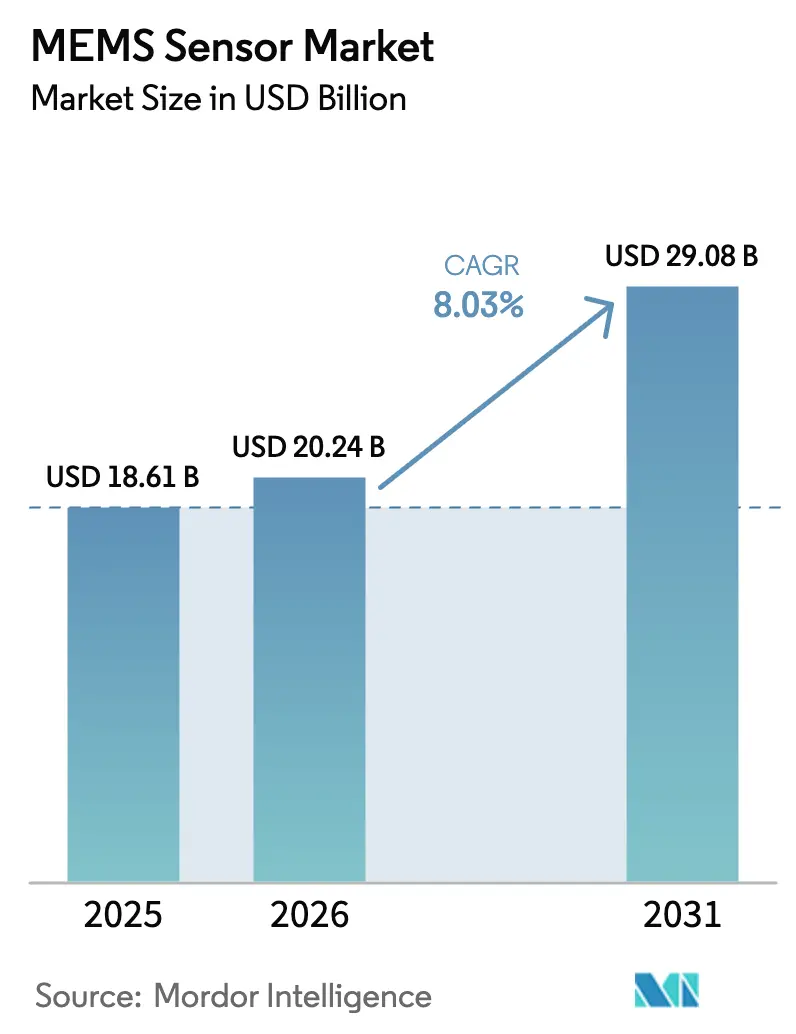

The MEMS Sensor Market size was valued at USD 18.61 billion in 2025 and is estimated to grow from USD 20.24 billion in 2026 to reach USD 29.08 billion by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

This trajectory reflects three powerful themes: mandatory automotive safety electronics, pervasive edge-AI deployment, and rapid miniaturization in health-monitoring wearables. Automakers are raising per-vehicle sensor content to comply with advanced driver-assistance requirements, while smartphone and wearable brands embed multi-axis packages that fuse motion, sound, and pressure data for context-aware services. Semiconductor foundries in Asia Pacific continue to scale 300 mm MEMS processes, lowering die cost and increasing supply resilience, whereas European and North American suppliers differentiate through heterogeneous integration that co-packages MEMS dies with application-specific integrated circuits. Competitive intensity remains elevated as vertically integrated leaders battle fabless challengers that rely on open foundry ecosystems and machine-learning firmware to move up the value chain.

Key Report Takeaways

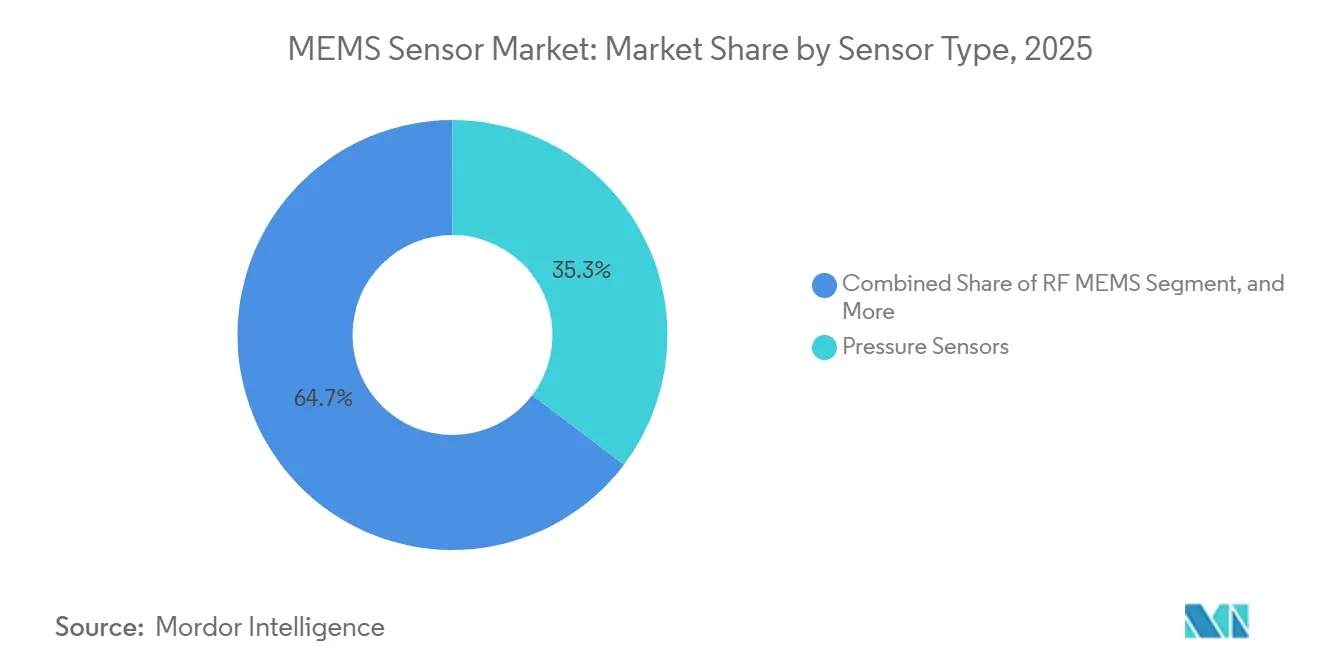

- By sensor type, pressure sensors held 35.25% of the MEMS sensor market share in 2025, while RF MEMS registered the fastest 9.79% CAGR through 2031.

- By technology, capacitive processes captured 46.19% of revenue in 2025; optical MEMS expanded at a 10.53% CAGR to 2031.

- By end-user, automotive led with a 29.44% revenue share in 2025, whereas healthcare posted the highest 10.81% CAGR through 2031.

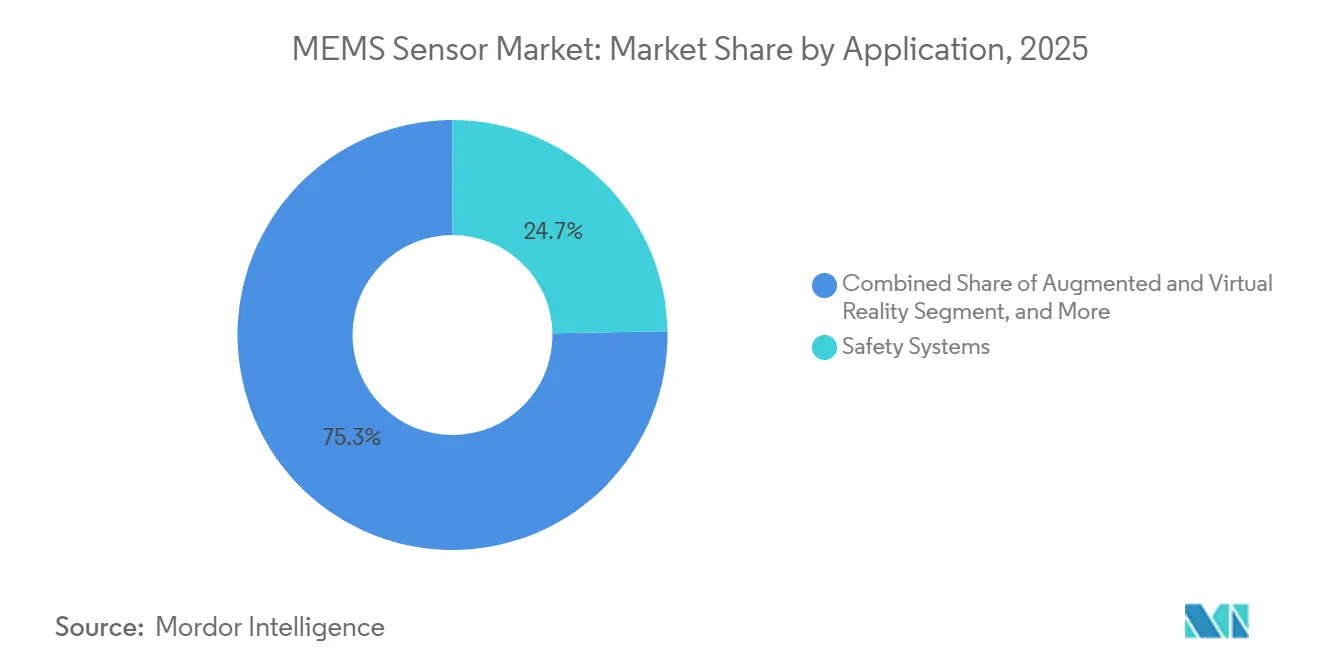

- By application, safety systems commanded 24.72% of 2025 revenue; augmented and virtual reality logged a 10.11% CAGR to 2031.

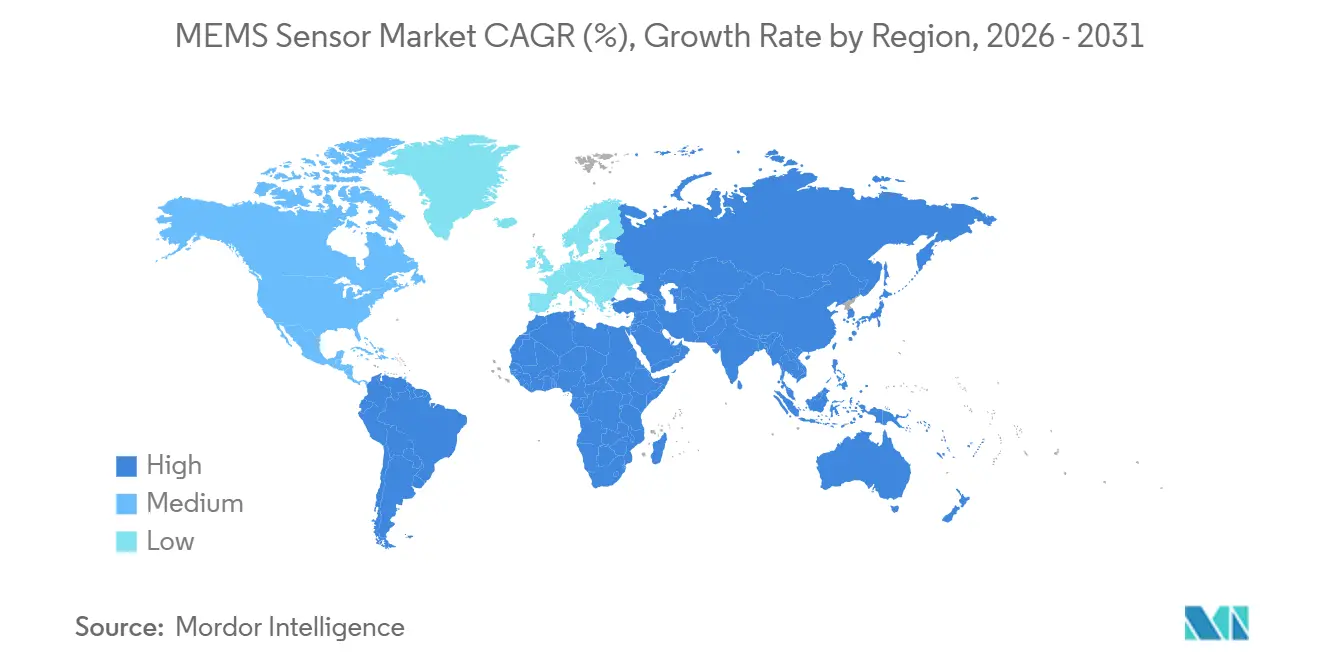

- By geography, Asia Pacific accounted for 38.31% of 2025 sales and advanced at a 9.25% CAGR, the fastest regional pace to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global MEMS Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Safety Concerns in the Automotive Industry | +1.80% | Global, with concentration in North America, Europe, and China | Medium term (2-4 years) |

| Emergence of Automation and Industry 4.0 | +1.50% | Europe and Asia Pacific manufacturing hubs, spillover to North America | Long term (≥ 4 years) |

| Proliferation of Smartphones and Wearables | +1.20% | Asia Pacific production centers, global consumption | Short term (≤ 2 years) |

| Rising Demand for IoT Edge Devices | +1.40% | Global, with early adoption in smart cities across Asia Pacific and Middle East | Medium term (2-4 years) |

| Integration of MEMS Sensors in Microdrones for Last-Mile Delivery | +0.60% | North America and Europe logistics corridors, emerging in Asia Pacific | Long term (≥ 4 years) |

| Adoption of Bio-Compatible MEMS Sensors for Implantable Medical Devices | +0.90% | North America and Europe regulatory markets, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Safety Concerns in The Automotive Industry

Tightening crash-avoidance regulations are translating directly into higher unit volumes of inertial sensors, pressure transducers, and microphones per vehicle. The United States National Highway Traffic Safety Administration finalized an automatic emergency-braking mandate that forces passenger-car makers to integrate multi-sensor suites able to detect obstacles, trigger braking, and record events within 0.1 second latency thresholds.[1]National Highway Traffic Safety Administration, “Federal Motor Vehicle Safety Standards,” NHTSA.GOV Euro NCAP raised the weight of active-safety criteria to 40% of its 2025 five-star protocol, prompting European automakers to add redundant gyroscopes and accelerometers for lane-keeping and stability control.[2]Euro NCAP, “Safety Assessment Protocols,” EURONCAP.COM China NCAP followed with pedestrian-detection rules that require exterior acoustic arrays using MEMS microphones filtered for wind noise. Tire-pressure monitoring systems, mandated worldwide, now transmit combined pressure and temperature data to extend sensor life, while brake-by-wire architectures in electric vehicles depend on sub-millibar MEMS pressure sensors to preserve pedal feel.

Emergence of Automation and Industry 4.0

Manufacturers are embedding vibration, pressure, and environmental MEMS devices into predictive-maintenance frameworks that cut downtime and material waste. Siemens achieved a 23% bearing-failure reduction after fitting 12 000 electric motors with triaxial accelerometers feeding machine-learning models in 2025.[3]Siemens AG, “Industrial Automation Solutions,” SIEMENS.COM The IEC 63278 wireless-sensor standard has created a common interface between MEMS nodes and programmable logic controllers, easing multivendor industrial adoption. Collaborative robots rely on six-axis force-torque sensors for real-time grip control, trimming surface-mount scrap by 18% in electronics assembly lines. Cleanroom managers deploy particulate and volatile-organic-compound MEMS detectors to maintain ISO Class 5 air, reducing wafer contamination risk. Edge compute gateways now process raw vibration data locally, slashing cloud bandwidth costs while enabling sub-10 ms feedback loops for robotic welding controls.

Proliferation of Smartphones and Wearables

Flagship and mid-tier smartphones ship with seven or more MEMS devices, ranging from high-g accelerometers for crash detection to micro-speakers for spatial audio. Apple equipped iPhone 14 with a sensor that triggers automatic emergency calls when 256 g deceleration events persist for 20 seconds. Samsung Galaxy Watch 6 pairs bio-impedance electrodes with MEMS pressure transducers to deliver FDA-cleared blood-pressure estimates suitable for over-the-counter use. Earbuds exploit sub-2 mm MEMS microphones that enable wind-noise-suppressed voice pickup, with Knowles surpassing 500 million units shipped in 2025. Augmented-reality glasses require sub-1-degree heading accuracy, driving magnetoresistive compasses that correct hard-iron distortions in real time.

Rising Demand for IoT Edge Devices

Smart-city planners and industrial operators deploy battery-powered sensor nodes that monitor environmental parameters and structural integrity. Barcelona installed 20 000 air-quality nodes equipped with particulate matter detectors to steer traffic away from pollution hotspots. The George Washington Bridge uses 400 wireless accelerometers to track modal frequency shifts indicating fatigue cracks. Precision-agriculture platforms integrate barometers, humidity transducers, and soil-moisture sensors to cut irrigation water usage by 30% in California orchards. Cold-chain logistics firms embed MEMS temperature and shock sensors in vaccine shipments to maintain compliance with WHO Good Distribution Practice and prevent spoilage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Overall Cost of MEMS Sensors Due to Interface Complexity | -1.20% | Global, with acute impact in cost-sensitive consumer electronics | Short term (≤ 2 years) |

| Lack of Standardised Fabrication Processes for MEMS | -0.90% | Global foundry ecosystem, concentrated in Asia Pacific and North America | Medium term (2-4 years) |

| Packaging Reliability Challenges in Harsh Environments | -0.60% | Automotive and industrial segments, global | Medium term (2-4 years) |

| Supply Constraints of Specialised SOI Wafers | -0.50% | Global, with supply concentrated in Japan and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increase in Overall Cost of MEMS Sensors Due to Interface Complexity

Modern multi-sensor platforms combine accelerometers, gyroscopes, and magnetometers within a single package, yet each axis still needs dedicated gain stages, anti-alias filters, and multi-kilohertz ADCs. Designers must therefore select microcontrollers with abundant SPI and I²C ports or add protocol bridges, adding USD 0.50 to USD 1.20 per node in bill-of-materials. Sensor-fusion firmware requires floating-point DSP blocks that raise power budgets by up to 25 mW and introduce thermal-management challenges in slim wearables. Factory calibration rigs must execute multi-axis rotation sequences, extending test time 30% and lifting per-unit manufacturing cost for high-g and precision inertial sensors. Absent standardized mechanical footprints, each new sensor generation triggers PCB reroutes that delay consumer-device launches.

Lack of Standardized Fabrication Processes for MEMS

Capacitive accelerometers rely on deep reactive-ion etching of high aspect-ratio combs, piezoresistive pressure sensors need ion-implanted strain gauges, and piezoelectric gyroscopes deposit aluminum-nitride thin films - three fundamentally different process flows unlikely to converge soon. Device makers running parallel lines therefore lose economies of scale and face yield variability that remains higher than in digital CMOS. Particle contamination during wafer bonding and release etch commonly drives 5-15% die rejection in pressure-sensor batches, forcing expensive inline inspections. Without unified design rules, electronic-design-automation coverage is limited, so MEMS engineers rely on manual finite-element simulation, stretching development cycles and non-recurring engineering outlays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Pressure Dominance Coupled With RF MEMS Momentum

Pressure sensors captured 35.25% of the MEMS sensor market share in 2025, primarily because every new passenger car sold in North America, Europe, China, and India now carries direct tire-pressure monitoring modules. These piezoresistive transducers withstand -40°C to 125°C, meet stringent accuracy requirements, and communicate over ultra-high-frequency links to in-dash diagnostics. Industrial pressure sensors fabricated on silicon-on-insulator wafers extend operating life in hydraulic systems, pneumatic actuators, and chemical reactors by resisting media corrosion.

Inertial sensors dominate consumer devices: six-axis motion tracking now ships in mid-tier smartphones priced below USD 300, enabling augmented-reality photo filters and game control without external beacons. MEMS microphones supply 90% of handset audio inputs, and dual-microphone beamforming has improved call clarity by 20 dB. Environmental sensors measuring humidity, temperature, and gases are increasingly built into HVAC thermostats and air-quality monitors to meet indoor-air regulations.

At the frontier, RF MEMS switches and tunable capacitors are gaining speed. Telecom OEMs embed these devices in 5G base stations to enable frequency-agile phased arrays. Qorvo’s latest RF MEMS switch handles 50 W across 24-44 GHz and exhibits sub-1 dB insertion loss, demonstrating parity with GaAs solutions while offering lower drive voltage. As operators densify millimeter-wave networks, the RF subset is positioned to outpace the broader MEMS sensor market, sustaining its 9.79% CAGR.

By Technology: Capacitive Maturity Meets Optical Expansion

Capacitive MEMS technology enjoyed a 46.19% revenue share in 2025 on the strength of refined process control, widespread foundry availability, and economical wafer-level packaging. STMicroelectronics alone shipped more than 2 billion capacitive accelerometers and gyroscopes for smartphones, automobiles, and industrial robots. Piezoresistive devices continue to serve harsh industrial and medical niches where strong linearity and wide temperature range outweigh temperature drift.

Optical MEMS is expanding at 10.53% CAGR through 2031 thanks to market pull from LiDAR sensors in autonomous vehicles and micro-mirror arrays in augmented-reality headsets. MicroVision’s 100 Hz beam-steer micro-mirror assembly enables centimeter-level object detection at 200 m, critical for Level-3 autonomy. Meanwhile, silicon photonics foundries have begun integrating optical MEMS scanners with laser drivers and signal-processing chips on single substrates via through-silicon vias, trimming parasitic capacitance and improving scan speed.

Piezoelectric resonators are dethroning quartz in timing applications. SiTime’s MEMS oscillators are 20 times more shock resistant than quartz, offering programmable frequencies without mechanical trimming, and already supply 15% of automotive Ethernet ports. Thermal and magnetic-tunnel devices fill smaller but growing niches in flow sensing and geomagnetic navigation. Despite process diversity, heterogeneous integration is advancing: sensor dies now stack atop ASICs using oxide-bonded wafers to cut height below 0.6 mm for ultra-thin wearables.

By End-User Industry: Automotive Scale With Healthcare Velocity

Automotive remained the largest buyer at 29.44% of 2025 revenue. Electronic stability control modules depend on high dynamic-range gyroscopes, while direct tire-pressure modules attach to every wheel. Battery-electric vehicles add brake-by-wire pressure transducers and inertial packages for sophisticated torque-vectoring. The MEMS sensor market size for automotive will continue to expand in absolute terms, yet its share is stable as other sectors accelerate.

Healthcare is the standout growth vertical, advancing at 10.81% CAGR to 2031. Continuous glucose monitors place electrochemical sensors on flexible patches, sampling interstitial fluid every five minutes and sending data to insulin pumps. FDA-cleared blood-pressure wearables integrate MEMS strain and pressure sensors, promising medical-grade accuracy without cuffs. Implantable pressure and flow sensors coated with biocompatible polymers now monitor hydrocephalus and cardiac output for a decade, reducing hospital readmissions.

Consumer electronics continues its volume leadership in unit terms. Apple’s crash-detect accelerometer illustrates how a single high-g axis can unlock life-saving differentiation in a crowded market. Industrial users push specification envelopes rather than unit counts, embedding vibration and environmental sensors to achieve predictive maintenance on rotating machinery. Aerospace and defense specify radiation-hardened inertial measurement units capable of 20 000 g shocks for missile guidance, whereas telecom operators install MEMS timing and RF switches inside 5G base stations.

By Application: Safety Systems Reign While Immersive Media Accelerates

Safety systems generated 24.72% of MEMS sensor revenue in 2025. Satellite accelerometers mounted at multiple vehicle points sense impact signatures and coordinate airbag deployment within 15 ms. Redundant gyroscopes in stability-control algorithms apply selective braking when yaw rates exceed threshold values. Brake-pedal emulation in electric vehicles relies on sub-millibar pressure sensors to deliver familiar pedal feel across regenerative and friction braking modes.

Navigation and positioning applications blend MEMS inertial data with GNSS to maintain sub-meter accuracy when satellite signals drop. u-blox dead-reckoning algorithms fuse accelerometer and gyroscope inputs to cap drift within 1 % of distance travelled over 60 s. Structural health monitoring arrays listen for modal-frequency changes in real time, protecting bridges and high-rise buildings. Environmental monitoring nodes map urban air quality, feeding municipal dashboards.

Augmented and virtual reality is the fastest-expanding application segment at 10.11% CAGR. Six-degree-of-freedom tracking depends on nine-axis inertial measurement units aided by optical inside-out vision algorithms. Meta’s latest headset fuses accelerometer and gyroscope output at 1 kHz to achieve sub-10 ms motion-to-photon latency. Microdrones for package delivery integrate barometric altimeters and attitude sensors, enabling autonomous waypoint navigation cleared by aviation regulators. The MEMS sensor market size for immersive-media devices therefore rises faster than the overall average through 2031.

Geography Analysis

Asia Pacific dominated the MEMS sensor market with 38.31% revenue share in 2025 and posted the fastest 9.25% CAGR through 2031. Taiwan Semiconductor Manufacturing Company boosted 300 mm MEMS capacity by 30% in 2025, cutting per-die cost for capacitive inertial sensors by one-fifth. South Korea’s vertically integrated cluster pairs Hyundai Mobis with domestic sensor fabs, yielding annual production of 15 million electronic stability control units. China’s smartphone assemblers shipped more than 700 million handsets in 2025, each embedding multiple microphones and motion sensors tailored for augmented-reality functions. Japan uses MEMS vibration sensors in industrial condition-monitoring to prolong tool life at automotive and electronics plants. India’s 2025 regulation mandating tire-pressure monitoring on new passenger cars generated demand for 20 million sensors, encouraging local content under its phased-manufacturing program.

North America and Europe together accounted for 45% of 2025 revenue. The NHTSA crash-avoidance mandate adds USD 150-300 of sensor content per U.S. passenger vehicle, while Euro NCAP’s 2025 scoring weight on active safety drives multi-axis inertial installs in Europe. Siemens rolled out triaxial accelerometers across 12 000 motors in German plants, confirming a 23% bearing-failure cut. FDA clearance of over-the-counter glucose monitors and blood-pressure wearables expanded addressable sensor units in 2025. Honeywell Aerospace sells radiation-hardened gyroscopes to U.S. low-Earth-orbit satellite integrators. Canadian unmanned-air-system developers integrate high-temperature-resistant inertial units for beyond-visual-line-of-sight operations.

South America, the Middle East and Africa contribute smaller shares but display localized surges. Brazil produced 2.3 million vehicles in 2025, equipping each with tire-pressure modules to meet Mercosur safety rules. Dubai installed 10 000 MEMS-based air-quality nodes in 2025, supporting congestion-management initiatives. Saudi Arabia’s Vision 2030 projects retrofit bridges and tunnels with wireless accelerometer arrays to detect fatigue cracks. South Africa’s precision-agriculture sector uses barometric and soil-moisture sensors to cut vineyard water consumption 25%. Nigeria’s network operators added 5 000 base stations in 2025, installing MEMS timing devices for synchronization.

Competitive Landscape

The five largest suppliers, STMicroelectronics, Bosch Sensortec, TDK InvenSense, Analog Devices, and Infineon Technologies, held roughly 55% of global revenue in 2025, leaving a long competitive tail of niche specialists. Vertically integrated leaders control proprietary wafer fabrication, improving yield and protecting intellectual property, while fabless challengers tap open foundry capacity to conserve capital and focus engineering on analog front ends and sensor-fusion firmware. Technology roadmaps converge on heterogeneous integration: sensor dies bond face-down to ASICs through oxide layers, shrinking package height and boosting bandwidth beyond 10 kHz. Capacity investments underline this trend: STMicroelectronics opened a 10 000-wafer-per-month MEMS line in Italy in October 2025, targeting automotive inertial packages with TSV interconnects.

Strategic moves also involve consolidation and certification. TDK acquired InvenSense’s automotive unit for USD 1.3 billion in September 2025 to embed radar-on-chip modules alongside inertial sensors and challenge Bosch in the premium ADAS segment. NXP won ISO 26262 ASIL-D approval for a triaxial accelerometer that self-tests signal-path health, cementing its role in safety-critical braking and airbag modules. SiTime displaced quartz oscillators in automotive Ethernet ports by delivering rugged MEMS resonators with programmable frequencies, seizing 15% share in 2025. Patent filings concentrate on wafer-level hermetic packaging that eliminates wire bonds and lowers z-height below 0.6 mm, crucial for implantable and earbuds.

Smaller entrants specialize: MicroVision commercialized optical MEMS scanners for LiDAR, Qorvo released kilowatt-class RF switches for 5G phased arrays, and Sensirion introduced indoor-air-quality modules combining humidity, temperature, and gas detection. Fragmented fabrication standards mean OEMs qualify multiple vendors for a single function, enhancing supply security but tempering pricing leverage. Energy-harvesting MEMS, quantum-scale force detectors, and bio-compatible implantables remain challenge-rich avenues expected to shape the post-2031 horizon.

MEMS Sensor Industry Leaders

STMicroelectronics NV

Invensense Inc. (TDK Corp)

Bosch Sensortec GmbH (Robert Bosch GmbH)

Analog Devices Inc.

Murata Manufacturing Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Knowles Corporation won the CES 2026 Innovation Award for its SiSonic MEMS microphone featuring a 75 dB signal-to-noise ratio and wind-noise suppression, targeting premium smartphones and voice-assistant devices.

- October 2025: STMicroelectronics inaugurated a 300 mm MEMS line in Italy with 10 000 wafers per month of capacity, integrating through-silicon vias to shrink automotive inertial modules by 40%.

- September 2025: Bosch Sensortec introduced the BMI323 six-axis inertial measurement unit with an on-chip machine-learning core that adapts to user motion patterns while consuming 1.2 mA in active mode.

- August 2025: TDK acquired InvenSense’s automotive sensor division for USD 1.3 billion, gaining inertial and radar-on-chip modules to supply Level 3 autonomous programs.

Global MEMS Sensor Market Report Scope

The MEMS Sensor Market Report is Segmented by Sensor Type (Pressure, Inertial, Microphones, Environmental, Microfluidic, RF MEMS, Others), Technology (Capacitive, Piezoresistive, Piezoelectric, Optical, Thermal, Magnetic Tunnel, Others), End-User Industry (Automotive, Consumer Electronics, Industrial, Healthcare, Aerospace and Defense, Telecommunications, Agriculture, Others), Application (Safety Systems, Navigation, Health Monitoring, Structural Health Monitoring, Environment Monitoring, AR and VR, Others), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Pressure Sensors | |

| Inertial Sensors | Accelerometers |

| Gyroscopes | |

| Magnetometers | |

| Microphones | |

| Environmental Sensors | |

| Microfluidic Sensors | |

| RF MEMS | |

| Other Sensor Types |

| Capacitive |

| Piezoresistive |

| Piezoelectric |

| Optical |

| Thermal |

| Magnetic Tunnel |

| Other Technologies |

| Automotive |

| Consumer Electronics |

| Industrial |

| Healthcare |

| Aerospace and Defense |

| Telecommunications |

| Agriculture |

| Other End-User Industries |

| Safety Systems |

| Navigation and Positioning |

| Health Monitoring |

| Structural Health Monitoring |

| Environment and Climate Monitoring |

| Augmented and Virtual Reality |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Taiwan | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Sensor Type | Pressure Sensors | |

| Inertial Sensors | Accelerometers | |

| Gyroscopes | ||

| Magnetometers | ||

| Microphones | ||

| Environmental Sensors | ||

| Microfluidic Sensors | ||

| RF MEMS | ||

| Other Sensor Types | ||

| By Technology | Capacitive | |

| Piezoresistive | ||

| Piezoelectric | ||

| Optical | ||

| Thermal | ||

| Magnetic Tunnel | ||

| Other Technologies | ||

| By End-User Industry | Automotive | |

| Consumer Electronics | ||

| Industrial | ||

| Healthcare | ||

| Aerospace and Defense | ||

| Telecommunications | ||

| Agriculture | ||

| Other End-User Industries | ||

| By Application | Safety Systems | |

| Navigation and Positioning | ||

| Health Monitoring | ||

| Structural Health Monitoring | ||

| Environment and Climate Monitoring | ||

| Augmented and Virtual Reality | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the MEMS sensor market expected to grow through 2031?

The market is forecast to post an 8.03% CAGR, rising from USD 20.24 billion in 2026 to USD 29.08 billion by 2031.

Which application currently generates the most revenue?

Safety systems, including airbag accelerometers and stability-control gyroscopes, accounted for 24.72% of 2025 sales.

What is driving the rapid rise of MEMS use in healthcare devices?

Biocompatible pressure and biochemical sensors enable continuous glucose monitors and cuff-less blood-pressure wearables, pushing healthcare to a 10.81% CAGR through 2031.

Why is Asia Pacific growing faster than other regions?

Regional fabrication scale, smartphone assembly volumes, and automotive electronics adoption produce a 9.25% CAGR, outpacing all other geographies.

Which technology segment is expanding the quickest?

Optical MEMS, propelled by LiDAR scanners and micro-mirror arrays for augmented reality, is accelerating at a 10.53% CAGR to 2031.

What strategic move is shaping competitive dynamics?

Heterogeneous integration that co-packages MEMS dies with ASICs via through-silicon vias reduces module size and cost while raising bandwidth beyond 10 kHz.

Page last updated on: