Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

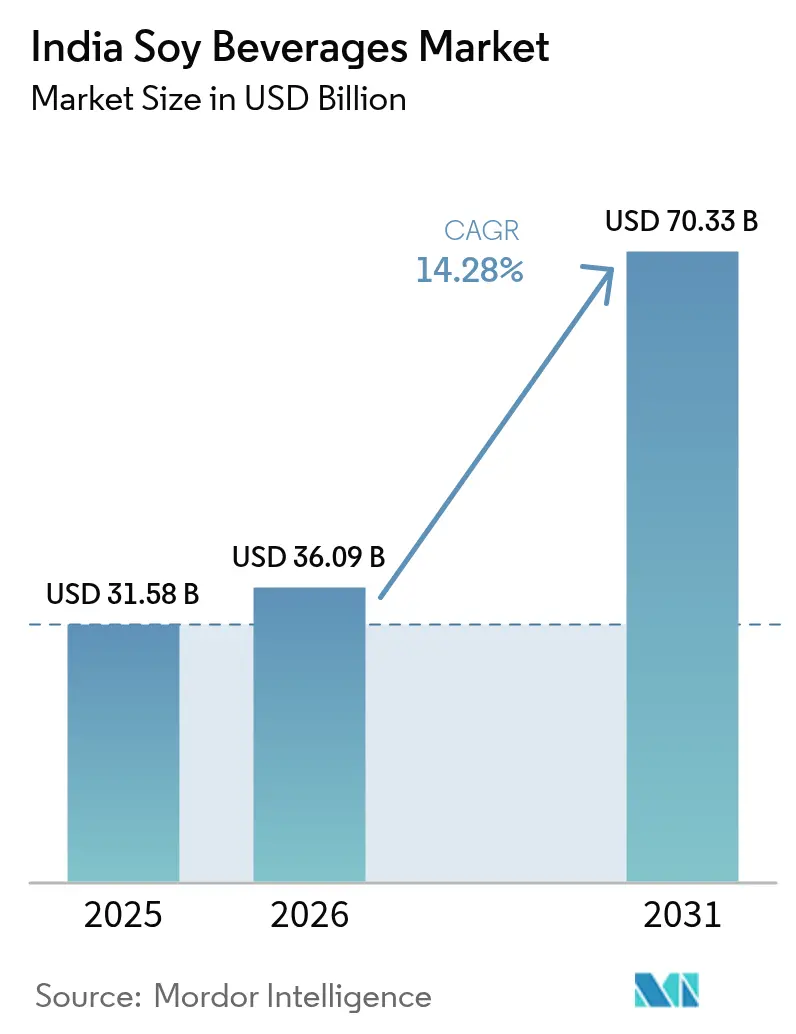

| Base Year Market Size (2025) | USD 31.58 Billion |

| Market Size (2026) | USD 36.09 Billion |

| Market Size (2031) | USD 70.33 Billion |

| Growth Rate (2026 - 2031) | 14.28% CAGR |

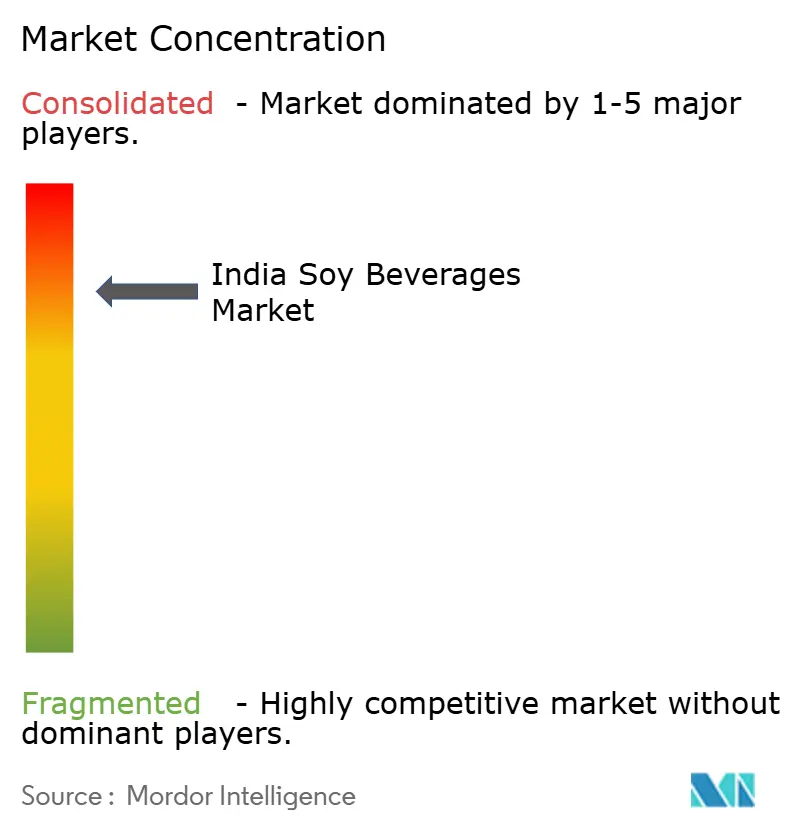

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Soy Beverages Market Analysis by Mordor Intelligence

India soy beverages market size in 2026 is estimated at USD 36.09 million, growing from 2025 value of USD 31.58 million with 2031 projections showing USD 70.33 million, growing at 14.28% CAGR over 2026-2031. This growth is driven by heightened health awareness, a surge in lactose intolerance, and the rising allure of plant-based diets. Government initiatives, notably food-processing PLI schemes, are fostering a conducive environment for soy beverage producers. While soy milk dominates the market, soy protein smoothies are witnessing the swiftest adoption among health-conscious consumers. Consumption is led by North India, yet South India is experiencing the most rapid growth, signaling a shift in dietary habits among urban populations. Off-trade retail channels hold the majority share, but on-trade quick-commerce platforms are swiftly gaining traction in urban locales. The competitive landscape remains fragmented, offering niche players a chance to carve their niche, especially with India's substantial soybean output. However, challenges persist with deep-rooted dairy preferences and the need for cost parity. The burgeoning health-beverage sector presents soy brands with strategic opportunities to resonate with protein-focused millennials and Gen Z as they seek functional alternatives. Key players in India's soy beverages arena include Nutrela, So Good, Sofit, Vitasoy, Amul Soy Milk, Soyvita, and Pristine Organics. These brands offer a spectrum of formulations, from fortified and flavored to organic and sustainable, catering to diverse consumer tastes.

Key Report Takeaways

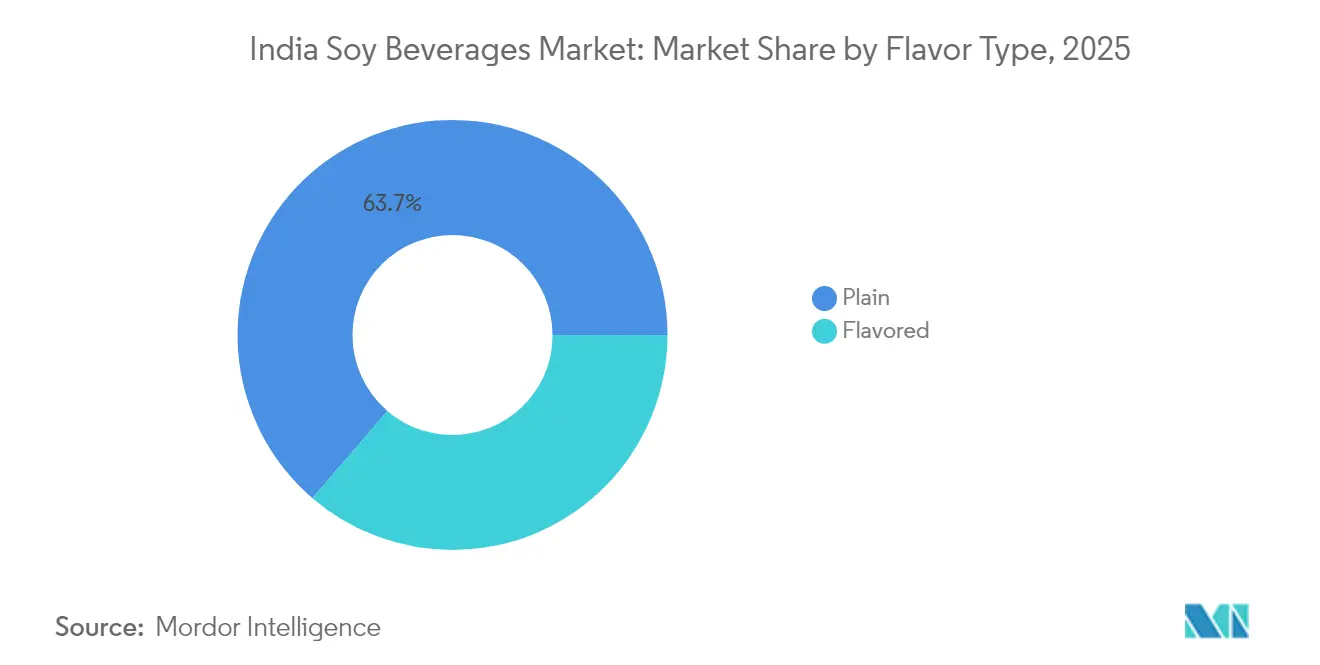

- By flavor, plain soy beverages held 63.71% of the India soy beverages market share in 2025, while flavored variants are projected to grow at a 15.74% CAGR through 2031.

- By category, conventional liquid products captured 88.64% share of the India soy beverage market size in 2025; free-form formats are forecast to expand at 16.95% CAGR to 2031.

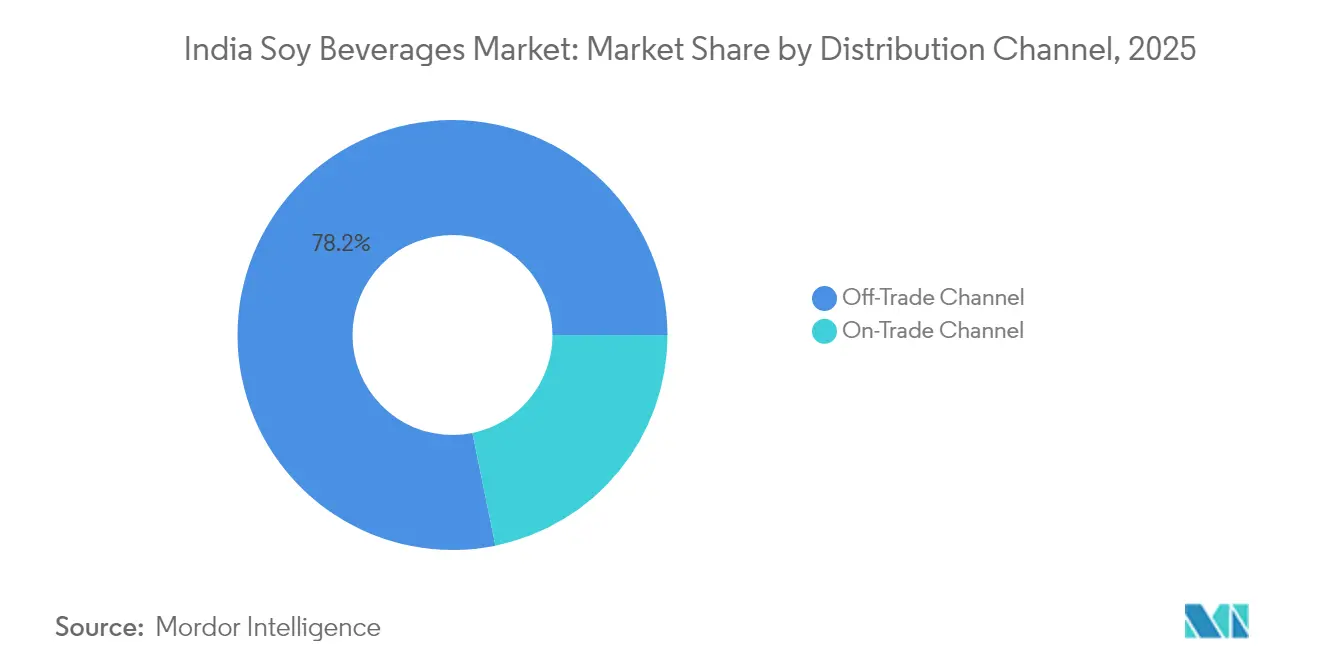

- By distribution channel, off-trade retail accounted for 78.20% of the India soy beverage market size in 2025, whereas on-trade channels led by quick commerce are advancing at a 15.88% CAGR through 2031.

- By packaging type, tetra packs commanded 92.10% revenue share in 2025; PET/glass bottles are poised to rise at 14.35% CAGR between 2026-2031.

- By region, North India remained the largest consuming region in 2025, while South India is posting the fastest growth trajectory through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Soy Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Consciousness and Plant-Based Dairy Demand | +3.2% | National; early adoption in North and West India | Medium term (2-4 years) |

| Growth of Vegan Population and Lactose Intolerance Awareness | +2.8% | Urban centers nationwide; strongest in South India | Long term (≥ 4 years) |

| Product Innovation in Packaging and Flavors | +2.1% | National; manufacturing hubs in North and West India | Short term (≤ 2 years) |

| Aggressive Marketing and Promotional Strategies | +1.9% | Metro and Tier 1 cities | Short term (≤ 2 years) |

| Government Policies and Support for Plant-Based Alternatives | +1.7% | National; implementation focus in major states | Medium term (2-4 years) |

| Rising Functional Beverage Demand | +1.5% | Urban North, West, South India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Consciousness and Plant-Based Dairy Demand

Indian consumers, driven by rising health consciousness and the increasing availability of plant-based dairy options, are gravitating towards soy-based beverages, with soy milk taking the lead. A survey by the Good Food Institute India reveals that 82% of individuals who sampled plant-based milk plan to buy it again, underscoring a swift transition from health-driven trials to consistent demand [1]Source: GFI India, “The Next Course: Mapping India’s Smart Protein Sector,” gfi-india.org. Soy milk stands out with the highest recognition among dairy alternatives, and nearly 25% of consumers have given it a try, marking it as the segment's gateway. Brands are keenly attuned to these consumer trends. Sofit leads in brand recall with its flavored soy milks that marry indulgence with nutrition. Meanwhile, So Good has rolled out unsweetened, protein-fortified variants targeting the fitness-savvy crowd. Amul’s soy milk, emphasizing affordability, has broadened the category's appeal, reaching beyond its initial urban niche. Notably, many users cite "healthier" and "ethically sourced" as primary reasons for their plant-based milk preference, with a significant number willing to pay up to 20% more than for traditional dairy, highlighting a robust value perception. This fusion of health awareness, ethical considerations, and brand innovation is seamlessly integrating soy milk into daily routines, be it in tea, coffee,solidifying its role as a pivotal growth driver in India's shifting dairy scene.

Growth of Vegan Population and Lactose Intolerance Awareness

In India, a burgeoning vegan population and heightened awareness of lactose intolerance are steering beverage preferences, with soy milk emerging as the go-to choice for health-conscious consumers. The World Population Review 2025 indicate that 9% of India's 1.46 billion populace, roughly 132 million individuals, will identify as vegan, positioning India as a global frontrunner in the plant-based beverage market [2]Source: World Population Review, “Veganism by Country 2025,” worldpopulationreview.com. For many, soy milk stands out as the primary protein-rich alternative to dairy, seamlessly fitting into daily rituals like tea, coffee, and shakes without sacrificing flavor or nutrition. A 2024 survey by GFI India underscores this trend, highlighting soy milk's status as the most recognized plant-based dairy, boasting a strong repeat purchase intent, indicative of deepening consumer loyalty. Brands are tailoring their offerings: Sofit lures families with chocolate and vanilla flavors, while So Good targets the fitness-savvy youth with its protein-packed, low-sugar options, reflecting shifting dietary trends. Concurrently, rising lactose intolerance awareness is reshaping family choices, with parents opting for soy milk as a digestible alternative for both children and adults. Amul's affordable soy milk bolsters its mainstream acceptance, and the endorsement from cafés and quick-service restaurants, which now routinely offer soy milk as a non-dairy option, further cements its status. Collectively, these dynamics are elevating soy milk from a niche health product to a staple in India's beverage arena.

Government Policies and Support for Plant-Based Alternatives

In India, government policies are reshaping consumer behavior by enhancing the taste, affordability, and nutritional appeal of soy products in the country's soy beverage market. A policy brief from GFI-India emphasizes that bolstering "smart protein" options, such as soy milk, demands systemic public support, extending beyond mere private investment. This public backing encompasses upgrades to food-processing infrastructure and technological interventions, enabling producers to refine flavors, cut costs, and boost nutritional quality priorities that resonate with consumers. Such a supportive policy landscape empowers established brands like Sofit and So Good to craft tastier, fortified soy milk variants, appealing to health-conscious consumers and families. At the same time, emerging players like Alt Co. leverage capacity-building incentives, allowing them to introduce high-quality soy products at competitive prices. Concurrently, government-backed messaging promoting sustainable and modern diets is bolstering consumer trust, positioning soy milk not merely as an alternative but as a mainstream choice in line with national health and food-tech aspirations. These developments are expected to drive further innovation and competition in the market, creating a dynamic ecosystem for soy-based beverages. Additionally, the increasing awareness of plant-based diets and their environmental benefits is likely to further accelerate the adoption of soy milk.

Aggressive Marketing and Promotional Strategies

In India’s soy beverage market, aggressive marketing and promotional strategies are reshaping consumer behavior, elevating soy milk from a niche product to a mainstream staple. A notable instance occurred in 2024 when L’Opéra India, a premium French bakery chain, rolled out soy milk at all its outlets. This move seamlessly integrated plant-based beverages into the daily café culture, normalizing their presence in social settings. In a parallel effort, Sofit revamped its branding, spotlighting soy milk’s wholesome and indulgent attributes through fresh packaging and messaging. Meanwhile, So Good and Alt Co. harnessed the power of influencer-driven campaigns and digital storytelling, positioning soy beverages at the intersection of fitness, wellness, and ethical living. These strategies not only elevate soy milk's aspirational status but also anchor it in everyday routines, from tea and coffee to shakes. On a broader scale, global plant-based marketing trends bolster these changes. The Veganuary 2025 campaign, for instance, motivated 25.8 million individuals worldwide to explore veganism in just a month, leading to the debut of over 1,480 new vegan products and menu items [3]Source: Veganuary, “Veganuary End Of Campaign Report 2025 UK,” veganuary.com. This surge of innovation and heightened visibility is making waves in the Indian market, reshaping perceptions of soy milk as a contemporary, forward-thinking choice.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural Preference for Traditional Dairy | -2.4% | Nationwide; strongest in rural and East India | Long term (≥ 4 years) |

| Higher Price Compared to Dairy Milk | -1.8% | Price-sensitive markets nationwide | Medium term (2-4 years) |

| Competition from Other Plant-Based Beverages | -1.2% | Urban centers with diverse offerings | Short term (≤ 2 years) |

| Limited Reach in Rural and Tier 2 Areas | -0.9% | Rural and small-city markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cultural Preference for Traditional Dairy

In India, a cultural preference for traditional dairy products hampers the growth of soy beverages. Deep-rooted habits and trust in dairy overshadow the appeal of plant-based alternatives. Established dairy cooperatives, like Amul and Mother Dairy, bolster the cultural significance of milk. They consistently promote products like fresh milk, paneer, butter, and ghee in national campaigns, especially during festive seasons. These campaigns not only celebrate dairy's rich heritage but also reinforce consumer loyalty, making it challenging for soy milk to be viewed as a genuine substitute. In daily life, products like Amul Taaza and Mother Dairy Full Cream Milk are staples in households, chai stalls, and sweet shops. Fresh milk is indispensable for tea, coffee, and mithai. This deep-rooted integration into daily and cultural rituals sidelines soy beverages, which are often perceived as "functional" rather than traditional. Even when brands like Sofit and So Good introduce flavored or fortified soy milk variants, they encounter skepticism from consumers who equate dairy with authenticity and comfort. Furthermore, restaurants and street-food vendors predominantly rely on dairy for items like lassi, kulfi, and paneer dishes, leaving scant opportunity for soy alternatives. These strong cultural and emotional ties to dairy hinder the widespread adoption of soy beverages, confining their appeal mainly to niche, health-conscious consumers.

Competition from Other Plant-Based Beverages

In India, soy beverages are facing mounting competition as consumers increasingly gravitate towards almond, oat, and coconut milk. These alternatives are being marketed as premium, trendy, and versatile choices. For instance, Epigamia's almond and oat milk range has made waves, thanks to its robust retail presence and collaborations with coffee chains. This strategy has particularly resonated with urban millennials who prioritize clean-label and lifestyle-oriented products. Meanwhile, RAW Pressery is championing almond milk, promoting it as the go-to choice for smoothies, shakes, and fitness diets, branding it as a lighter, more appealing alternative to soy. Coffee giants like Starbucks India and Third Wave Coffee Roasters have also taken note, prominently featuring oat and almond milk on their menus. Soy, while listed as an alternative, doesn't receive the same spotlight, resulting in diminished consumer trials and preferences. Adding to the competition, the rise of coconut-based options is hard to ignore. Brands such as Only Earth are tapping into this trend, launching coconut and oat milk beverages with a strong emphasis on sustainability, appealing to the environmentally conscious demographic. Despite its high-protein content, soy struggles to attain the aspirational allure of these newer alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Plain Varieties Lead While Innovation Drives Growth

In 2025, plain soy beverages command a dominant 63.71% share of India's soy beverage market. Their affordability and versatility make them a staple choice for daily consumption. Widely embraced as dairy substitutes in tea, coffee, and cooking, they cater especially to cost-conscious households. While their neutral flavor profile appeals to families prioritizing functional nutrition, concerns about taste have somewhat limited their broader acceptance.

On the other hand, flavored soy beverages are on a rapid ascent, projected to grow at a 15.74% CAGR through 2031. This surge is largely attributed to innovations that tackle taste concerns and draw in new consumers. Brands like Sofit have cultivated a loyal following with their chocolate and vanilla soy milk, resonating with families and children who find these flavors more appealing. Meanwhile, So Good has ventured into indulgent flavors like mango and strawberry, specifically targeting urban millennials who prioritize both taste and nutrition. Additionally, new entrants like Alt Co. are delving into functional, ready-to-drink soy beverages, catering to the fitness-conscious demographic. Such innovations underscore the significance of flavor and format diversification in broadening consumer adoption, positioning this segment as a pivotal driver for the market's future growth.

By Category: Conventional Products Dominate Despite Free-Form Innovation

In 2025, conventional soy beverages command a dominant 88.64% share, thanks to their established processing methods and consumer familiarity. These beverages serve as daily dairy substitutes, making them the top choice, particularly for households that favor ready-to-drink packs. Brands like Sofit have solidified their market presence, offering both plain and flavored liquid soy milk, catering to families seeking convenience. Meanwhile, So Good has broadened its reach, partnering with retail and quick-service outlets, solidifying conventional soy beverages as the preferred choice for mainstream consumers valuing accessibility and consistency.

Free-form soy beverages, capturing a 11.36% market share in 2025, are emerging as a niche segment, driven by a rising demand for organic, clean-label, and non-GMO products. Leading the charge, brands like Health on Plants and Silk offer organic, non-GMO soy drinks, resonating with health-conscious millennials and young professionals. These consumers prioritize transparency, sustainability, and premium nutrition. Such a strategic positioning not only draws in newcomers shifting from dairy but also fortifies loyalty among current plant-based enthusiasts. This underscores the expanding allure of soy in India, propelled by clean-label and organic innovations that transcend traditional formats.

By Distribution Channel: Off-Trade Dominance Meets On-Trade Innovation

In 2025, off-trade channels claimed a commanding 78.20% share of the soy beverages market. This dominance is bolstered by the pivotal roles of supermarkets, hypermarkets, convenience stores, and quick-commerce platforms like Blinkit and Zepto, which enhance last-mile delivery. Supermarkets and hypermarkets are emphasizing premium positioning through dedicated health and wellness aisles, while convenience outlets adeptly capture impulse purchases. Additionally, online and subscription-driven retail bolster brand loyalty. Brands such as Sofit and So Good are strategically partnering with both modern trade and e-commerce platforms, ensuring heightened accessibility and sustained dominance in the market.

On-trade channels, set to grow at a robust 15.88% CAGR through 2031, are being fueled by the burgeoning café culture and the increasing adoption of soy beverages in foodservice. Restaurants, quick-service chains, and cafés are now prominently featuring soy beverages on their menus, especially in lattes, smoothies, and as functional drink alternatives to dairy. This trend underscores a growing willingness to experiment and try soy beverages outside the home, cementing their status as lifestyle choices. While on-trade channels are witnessing the fastest growth, their interplay with off-trade channels highlights the critical need for omnichannel strategies, ensuring products remain visible and engaging to consumers across both retail and foodservice platforms.

By Packaging Type: Tetra Packs Lead While Sustainable Formats Emerge

In 2025, Tetra Packs command a dominant 92.10% share of the soy beverages market, owing to their superior shelf stability, efficient distribution, and well-established supply chains. Their convenience and extended shelf life make Tetra Packs the go-to choice for both retail and home consumption. Brands such as Sofit, So Good, and Staeta utilize Tetra Pack packaging to guarantee consistent quality and ensure widespread availability in supermarkets, hypermarkets, and e-commerce platforms, bolstering consumer trust and accessibility.

PET bottles, forecasted to expand at a robust 14.35% CAGR through 2031, are the market's fastest-growing segment. Their rise is attributed to premium positioning, transparency, and a growing consumer preference for recyclable or visually distinctive packaging. Brands including Alt Co., Sofit, Homesoy, and V-Soy are turning to PET bottles for their organic, non-GMO, and premium soy beverages, targeting health-conscious and environmentally savvy consumers. Meanwhile, flexible formats like pouches and sachets cater to trial-size and convenience-driven purchases, seamlessly integrating into the broader packaging strategy for both retail and on-the-go consumption.

Geography Analysis

In 2025, North India commands the soy beverages market, holding a dominant 35.45% share. This leadership is largely attributed to its proximity to India's primary soybean-producing regions, notably Madhya Pradesh, which boasts an annual output of 5.47 million tonnes. Such proximity not only ensures affordable access to raw materials but also benefits from a well-established processing infrastructure. Major metropolitan areas, including Delhi and Gurgaon, fuel robust consumer demand. Furthermore, developed cold chain networks and established FMCG hubs facilitate efficient distribution. While rural areas exhibit a cultural inclination towards traditional dairy, North India's blend of production prowess, urban consumption, and a streamlined supply chain cements its market leadership.

South India emerges as the region with the most rapid growth, boasting an 17.85% CAGR through 2031. This surge is driven by urban populations that prioritize health, possess higher disposable incomes, and are influenced by global dietary trends. Cities such as Bangalore and Hyderabad, bolstered by a tech-savvy workforce and a populace that's both educated and health-conscious, are particularly receptive to functional and plant-based beverages. Additionally, government incentives in food processing, combined with a skilled labor force, are propelling manufacturing investments, positioning South India as a burgeoning hub of innovation and growth.

While West and East India experience steady growth, it's on a smaller scale. West India, home to industrial powerhouses and cities like Mumbai and Pune, capitalizes on its port connectivity and FMCG infrastructure, establishing itself as a pivotal manufacturing and distribution center. Meanwhile, East India, with Kolkata at the forefront, is slowly warming up to plant-based beverages. This shift is spurred by increasing urbanization and health consciousness. However, cultural preferences and a limited number of metropolitan centers have tempered this adoption. Both regions must navigate localized strategies, balancing their infrastructural strengths with the evolving consumer landscape.

Competitive Landscape

In the consolidated Indian soy beverages market, companies carve out niches through targeted marketing. Brands like AltCo: establish trust across soy, oats, and almond milk; So Good champions unsweetened, lactose-free options; Sofit offers flavored, naturally sugar-free drinks; while Nourish You and Plant Yum cater to online vegan and specialty grocery shoppers. These players harness social media, influencer partnerships, and in-store tastings to foster loyalty and boost adoption among discerning consumers. The market's competitive landscape encourages innovation and differentiation, driving brands to continuously refine their strategies.

Technology plays a pivotal role, with methods like ultrasonic treatment, fermentation, and flavor-masking enhancing taste and nutrition. Brands such as AltCo and Sofit invest in aseptic packaging and cold chain systems, ensuring product integrity in Tetra Packs and PET bottles, and reliable delivery to retailers and online shoppers. Meanwhile, niche players like Nourish You leverage e-commerce to connect with health-focused consumers, navigating past traditional distribution hurdles. These advancements not only improve product quality but also enhance consumer trust and satisfaction.

Beyond product quality, these brands amplify their market presence through premium positioning, functional expansions, and lifestyle-driven promotions. Partnerships with cafés, vegan stores, and online platforms boost visibility. By honing in on segments like protein, immunity, and digestion, these brands tap into rising consumer trends, solidifying their foothold in India's expanding soy beverage landscape.

India Soy Beverages Industry Leaders

Alt Co. Pvt. Ltd

The Hershey Company

Nourish You Private Limited

Danone S.A.

Sanitarium Health and Wellbeing Company Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Danone committed EUR 20 million over three years to scale its Alpro plant-based beverage range in India, signaling intensifying multinational competition.

- August 2024: 1.5 Degree unveiled a diverse portfolio of products including soy milk at the India Expo Centre, Greater Noida, the emerging plant-based food segment received a significant boost with the debut of 1.5 Degree’s innovative range of plant-based dairy products.

- April 2024: Tetra Pak introduced recycled polymer aseptic cartons in the Indian market, addressing consumer sustainability concerns while preserving shelf-life advantages.

India Soy Beverages Market Report Scope

Soy beverage is a plant-based drink produced by soaking and grinding soybeans, boiling the mixture, and filtering out remaining particulates. It is a stable emulsion of oil, water, and protein The Indian soy beverages market is segmented by product type and distribution channel. By product type, the market is segmented into soy milk, soy-based drinkable yogurt; by flavor into flavored and plain/unflavored; and by distribution channel into supermarkets/hypermarkets, pharmacies, retail stores, convenience stores, and other channels. The report offers market size and forecast in value terms in USD million for all the above segments.

By Flavor

| Plain |

| Flavored |

By Distribution Channel

| On Trade Channel | |

| Off Trade Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Others |

By Packaging Type

| Tetra Packs |

| PET /Glass Bottles |

| Others |

By Region

| North India |

| West India |

| South India |

| East India |

| By Flavor | Plain | |

| Flavored | ||

| By Distribution Channel | On Trade Channel | |

| Off Trade Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Packaging Type | Tetra Packs | |

| PET /Glass Bottles | ||

| Others | ||

| By Region | North India | |

| West India | ||

| South India | ||

| East India | ||

Key Questions Answered in the Report

How big is the India Soy Beverages Market?

The India Soy Beverages Market size is expected to reach USD 36.09 million in 2026 and grow at a CAGR of 14.28% to reach USD 70.33 million by 2031.

What is the current India Soy Beverages Market size?

In 2026, the India Soy Beverages Market size is expected to reach USD 36.09 million.

Who are the key players in India Soy Beverages Market?

Pacific Foods Of Oregon, Llc., NESTLÉ, pearl soymilk, Danone and Sanitarium are the major companies operating in the India Soy Beverages Market.

What years does this India Soy Beverages Market cover, and what was the market size in 2025?

In 2025, the India Soy Beverages Market size was estimated at USD 31.58 million. The report covers the India Soy Beverages Market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the India Soy Beverages Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: