France Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

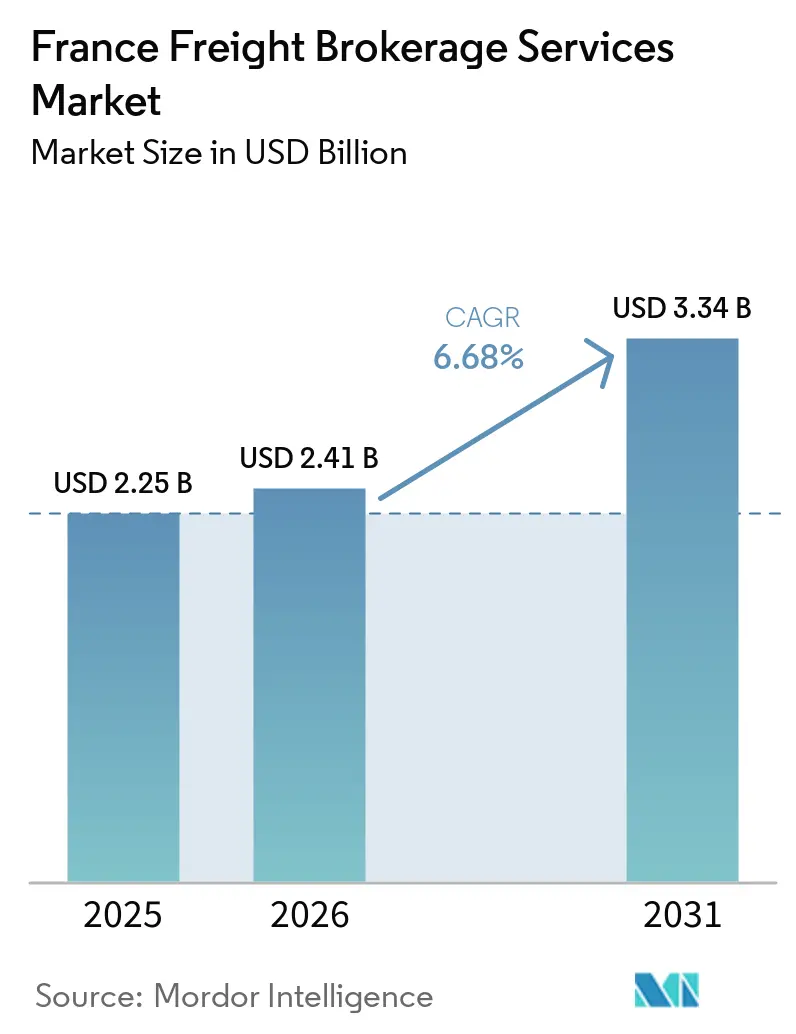

| Base Year Market Size (2025) | USD 2.25 Billion |

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

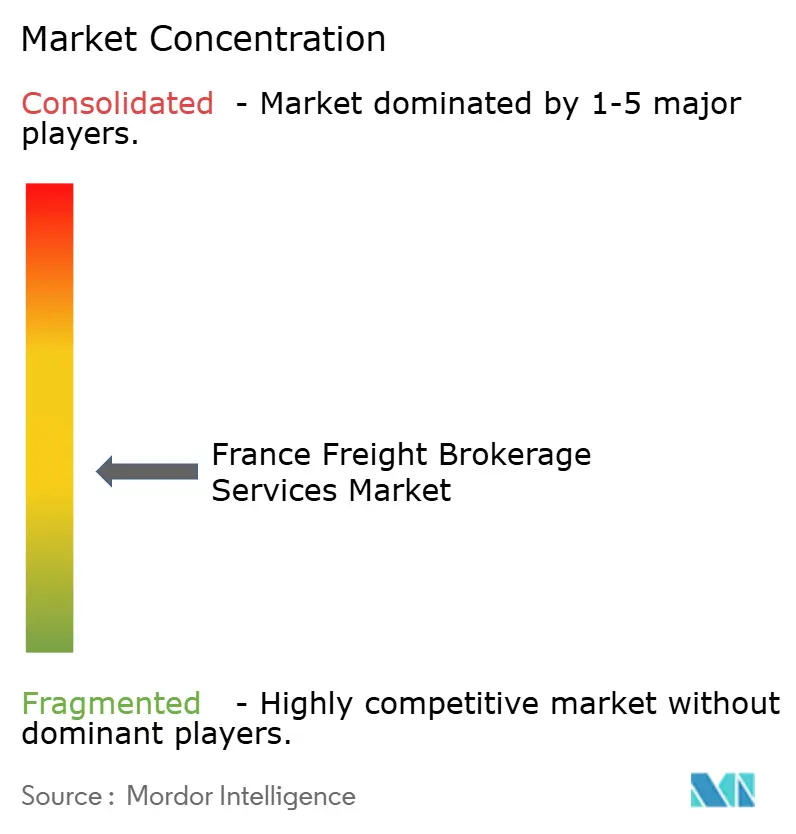

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Freight Brokerage Services Market Analysis by Mordor Intelligence

The France freight brokerage services market size is expected to increase from USD 2.25 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.34 billion by 2031, growing at a CAGR of 6.68% over 2026-2031. Demand climbs as shippers outsource Scope 3 emissions reporting, customs processes move online after Brexit, and hydrogen-truck subsidies widen low-carbon capacity pools. Digital platforms embed AI pricing to cut empty miles and speed quoting, while consolidation hubs inside zero-emission zones unlock profitable less-than-truckload backhauls. Tight driver supply and rising insurance premiums squeeze small carriers, creating opportunities for brokers who can aggregate fragmented capacity and underwrite credit risk. Macro factors such as Fit-for-55 decarbonization targets, EU infrastructure funding, and resilient household consumption sustain freight volumes despite fuel and electricity price swings.

Key Report Takeaways

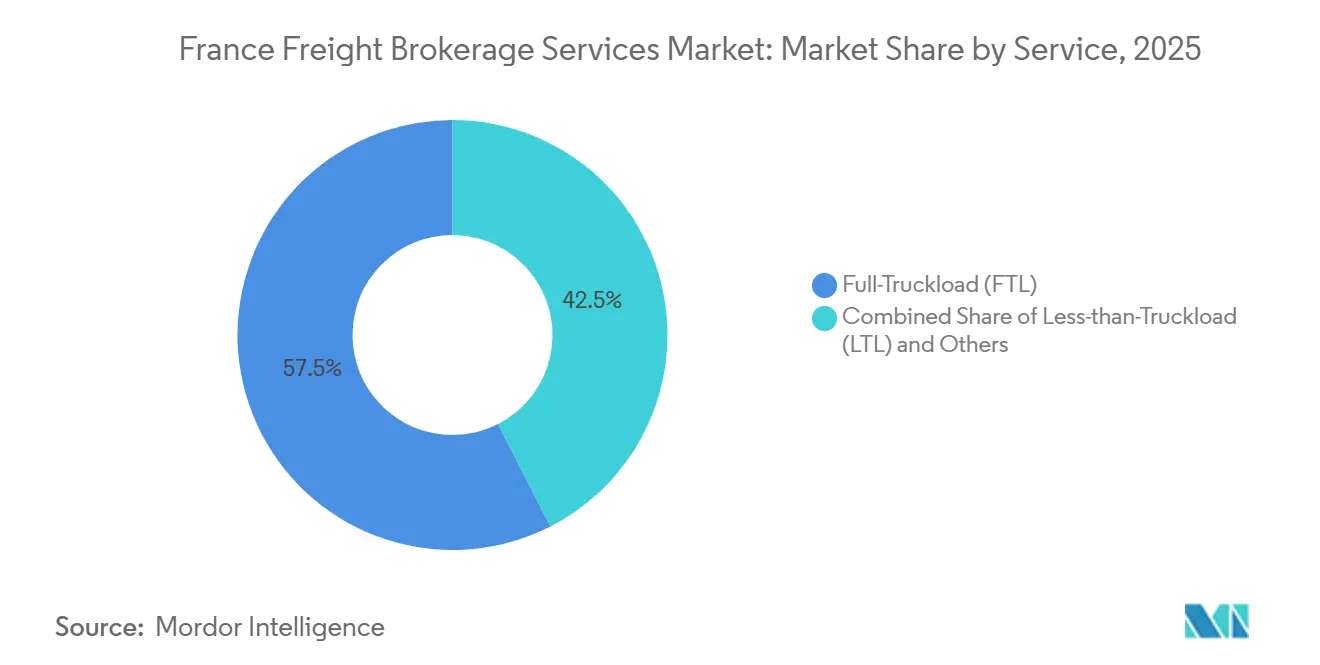

- By service, full-truckload led with 57.53% of the France freight brokerage services market share in 2025, and less-than-truckload is advancing at an 8.06% CAGR through 2031.

- By equipment type, dry vans accounted for 40.68% of the France freight brokerage services market size in 2025, whereas refrigerated vans are expected to grow with the fastest 8.68% CAGR to 2031.

- By haul length, long-haul captured 43.79% of the France freight brokerage services market size in 2025, while local delivery under 100 miles expands at 10.16% CAGR.

- By business model, traditional brokerage retained 61.08% of the France freight brokerage services market share in 2025, yet digital platforms are forecast at a 22.43% CAGR.

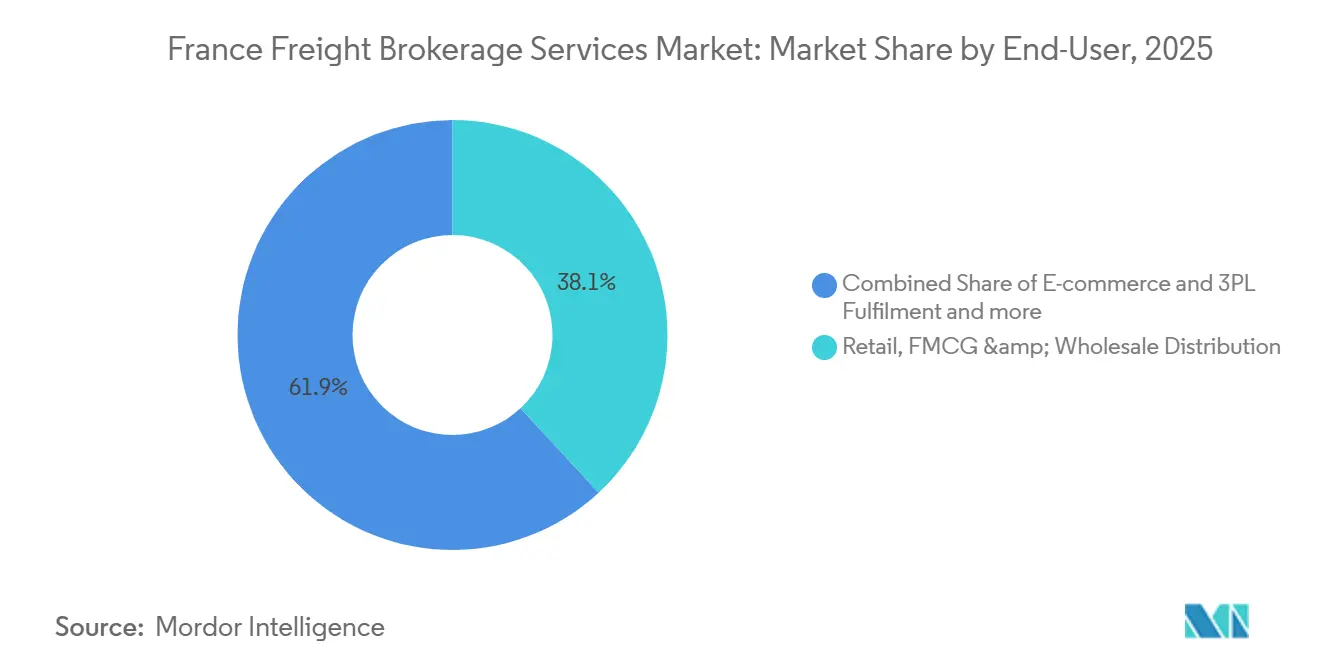

- By end-user, retail, FMCG, and wholesale held a 38.10% share in 2025; e-commerce and 3PL fulfillment grew the fastest at a 18.89% CAGR.

- By customer size, large enterprises contributed 63.81% of 2025 revenue, but small businesses rose at 12.60% CAGR as platforms democratize procurement.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Spain includes both locally based firms and those operating across multiple regions. The market landscape in the global freight brokerage services industry research shows how these players are arranged internationally.

France Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain-visibility mandates under CSRD drive broker adoption | +1.5% | National, concentrated in the Paris corporate headquarters | Short term (≤ 2 years) |

| Expansion of urban consolidation hubs boosts cross-docking brokerage | +1.1% | Metropolitan areas – Paris, Lyon, Marseille, Lille | Medium term (2-4 years) |

| Hydrogen-truck subsidy scheme enlarges green capacity pools | +0.8% | National, early deployment in industrial corridors | Long term (≥ 4 years) |

| Post-Brexit digital customs clearance stimulates cross-Channel volumes | +1.3% | Northern France, Calais-Dover corridor | Short term (≤ 2 years) |

| AI-enabled dynamic-pricing engines improve load matching | +1.2% | National, led by digital adopters | Short term (≤ 2 years) |

| Circular-economy reverse-logistics flows create backhaul lanes | +0.7% | National, packaging-intensive sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain-Visibility Mandates Under CSRD Drive Broker Adoption

CSRD obliges around 50,000 companies to disclose Scope 3 transport emissions from January 2025, pushing shippers to partner with providers that deliver ISO 14083-aligned carbon data and real-time tracking. Compliance penalties and average annual reporting costs of EUR 1.2 million (USD 1.42 million) encourage outsourcing to brokers with automated dashboards. French multinationals now rank environmental reporting among their three top procurement criteria, expanding the France freight brokerage services market as brokers translate complex audit rules into simple shipper interfaces. The directive’s extraterritorial reach draws non-EU suppliers into the same reporting net, enlarging cross-border brokerage demand. Early adopters differentiate through blockchain proofs of emission calculations and API connectivity with enterprise resource planning systems.

Expansion of Urban Consolidation Hubs Boosts Cross-Docking Brokerage

Fifteen micro-hubs in Paris and eight in Lyon feed zero-emission delivery zones by 2026, letting brokers aggregate palletized loads from multiple shippers and raise truck fill rates to 80-85%. Municipal rules already bar Euro 5 diesel above 3.5 tons from key downtown districts, so brokers charge premiums for value-added cross-docking and time-window services. Consolidation centers also shorten courier routes, lowering last-mile travel time by 30-40% and supporting same-day e-commerce commitments. Public grants from the European Investment Bank and local authorities de-risk private hub investment, further lifting urban LTL brokerage volumes[1]European Investment Bank, “Transport,” eib.org.

Hydrogen-Truck Subsidy Scheme Enlarges Green Capacity Pools

France funds up to 40% of the purchase price of fuel-cell trucks under the H2 Mobility program, targeting 1,000 heavy-duty units by 2030. The planned deployment of 100 refueling stations by TotalEnergies and Air Liquide improves range certainty along the Atlantic-Mediterranean corridors. Brokers gain first-mover advantage by pre-booking hydrogen capacity for sustainability-minded shippers, though a 20-25% ownership cost premium requires tailored surcharge models. Early green lanes already see tender acceptance rates 15% higher than diesel equivalents, indicating shipper willingness to pay for low-carbon credentials.

Post-Brexit Digital Customs Clearance Stimulates Cross-Channel Brokerage Volumes

Automated platforms slash Calais-Dover clearance from up to 6 hours to under 2 hours, reversing the 18% post-Brexit traffic drop. France’s DELTA-G exchanges 60 million declarations yearly and syncs with the UK Customs Declaration Service, but 47% of filings still contain errors that brokers are hired to correct. Volume gains of 25-30% in 2025 underpin robust cross-Channel revenue growth for specialists in UK-EU paperwork. Further simplification is planned through the EU Single Window by 2028, extending the addressable lane mix and adding resilience to the France freight brokerage services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antitrust scrutiny on broker fee transparency raises compliance costs | -0.9% | EU-wide | Medium term (2-4 years) |

| Volatile rail and EV-truck electricity prices erode multimodal parity | -0.7% | National, electrified corridors | Short term (≤ 2 years) |

| Escalating cyber-attacks on freight platforms dampen shipper trust | -0.6% | National | Short term (≤ 2 years) |

| Spike in carrier insurance premiums tightens independent capacity | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Antitrust Scrutiny on Broker Fee Transparency Raises Compliance Costs

EU competition authorities probe hidden margins of 12-25% on spot loads, pressing brokers to unbundle carrier pay from service fees. The French Competition Authority now requires itemized invoices, forcing IT upgrades, legal reviews, and customer re-education that together trim EBITDA for mid-sized firms. Potential fines of up to 10% of revenue heighten risk, slowing geographic expansion and technology spending in the France freight brokerage services market[2]European Union Agency for Cybersecurity, “Transport sector cybersecurity,” enisa.europa.eu.

Volatile Rail and EV-Truck Electricity Prices Erode Multimodal Cost Parity

Industrial electricity averaged EUR 0.18 (USD 0.21) per kWh in late 2024, 50% above 2023, wiping out the diesel-to-electric operating gap. Rail traction power faced similar price spikes, undermining cost cases for intermodal conversions. Brokers must renegotiate fixed-rate contracts or accept thinner margins until renewable supply stabilizes. Some shippers postpone modal shift commitments, opting for carbon offsets rather than physical decarbonization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: LTL Consolidation Benefits From Parcel Fragmentation

Less-than-truckload accounted for a rising slice of the France freight brokerage services market size as its revenue grows at 8.06% CAGR to 2031, while full-truckload still commands 57.53% share in 2025. Consolidation hubs inside Paris and Lyon lift LTL truck utilization and support same-day delivery promises that attract e-commerce merchants. In contrast, FTL serves steady factory-to-warehouse corridors but is pressured by driver shortages and higher insurance.

Improved load pooling through AI cuts LTL pairing time to three hours, enhancing on-time performance. Hybrid solutions that stitch an FTL trunk with LTL urban legs blur segment lines, enabling brokers to upsell bundled services. Specialized offerings for hazardous and oversized cargo remain niche but stable, anchored by construction and chemical demand.

By Equipment Type: Refrigerated Demand Rises With Pharma Growth

Dry vans delivered 40.68% of the France freight brokerage services market size, yet refrigerated units expand at 8.68% CAGR as vaccine and biologic volumes climb. Temperature-controlled capacity shortages during Q1 health campaigns allowed brokers to charge 15-20% premiums, boosting the France freight brokerage services market. IoT probes in trailers now alert on compressor faults, cutting spoilage and raising carrier service levels.

GDP compliance and end-to-end serialization for medicines intensify demand for visibility, prompting brokers to invest in blockchain logs that verify temperature integrity. Flatbeds and tankers keep a steady share tied to construction and chemical shipments, while their growth lags the headline market due to cyclical exposure.

By Haul Length: Local Delivery Outpaces Long-Haul

Long-haul exceeded 500 miles secures 43.79% of the France freight brokerage services market size but edges up slowly because of driver retention issues and toll inflation. Local delivery under 100 miles grows 10.16% CAGR as zero-emission zones in metropolitan areas reward electric vans and micro-hub models. Regional hauls supply spoke-and-hub networks linking fulfillment centers to cities, giving brokers options to balance cost and speed.

Real-time route optimization reduces urban delivery costs by nearly 15%, offsetting higher EV acquisition costs. Brokers experimenting with relay models on lengthy lanes keep drivers closer to home, slightly easing labor constraints while adding operational complexity.

By Business Model: Digital Platforms Accelerate SMB Onboarding

Traditional operators held 61.08% of 2025 turnover, yet digital entrants expand at a 22.43% CAGR by offering instant booking to cash-constrained merchants. AI price engines inside apps drive 95% quote automation and raise acceptance. Some incumbents now layer white-label platforms on top of legacy systems to protect their house accounts and diversify.

Asset-based hybrids use owned fleets to guarantee peak-season capacity and charge resiliency mark-ups. Agent networks quickly fill geographic gaps, though stricter EU rules on worker classification increase compliance burdens. The France freight brokerage services market thus blends personal relationship depth with rising algorithmic speed.

By End-User Industry: E-Commerce Returns Lift Reverse Logistics

Retail-FMCG-wholesale held 38.10% of the France freight brokerage services market share, still benefiting from in-store and online replenishment rhythms. E-commerce and 3PL fulfillment grow at a 18.89% CAGR, fueled by apparel return rates that double the number of shipment touches per sale. Brokers monetize reverse legs through refurbish routing and packaging loops, magnifying overall lane revenue.

Pharma and healthcare benefit from cold-chain upgrades and just-in-time hospital delivery contracts, which command surcharges for GDP certification. Construction, automotive, and agri-food continue to rely on specialized trailers and seasonal calendars, supporting a diverse freight mix that stabilizes cyclicality in the France freight brokerage services market[3]European Commission, “Infrastructure and investment,” transport.ec.europa.eu .

By Customer Size: Platforms Level the Playing Field for SMBs

Large enterprises accounted for 63.81% of 2025 revenue, driven by high shipment volumes and stringent CSRD reporting requirements. Small businesses, however, expand at a 12.60% CAGR once apps remove paperwork hurdles and offer credit card settlement rather than 30-day terms. Mid-market firms adopt blended models, combining contract lanes for core SKUs with spot bookings for promotional spikes.

Shippers with turnover under USD 10 million previously lacked bargaining clout but now tap pooled capacity at near-enterprise rates, eroding incumbents’ historical advantage. Brokers lure SMBs by bundling freight with duty calculation widgets and carbon dashboards, widening user stickiness across growth stages.

Geography Analysis

Northern France dominates cross-Channel volumes thanks to streamlined customs at Calais, while lle-de-France remains the single largest consumption and distribution hub in the France freight brokerage services market. Automated border systems cut clearance to under two hours, drawing manufacturers to reshore inventory close to UK demand and raising broker bookings on Dover ferries. Meanwhile, Auvergne-Rhone-Alpes injects heavy industrial output, feeding steady dry-van and flatbed activity toward Germany and Italy.

TEN-T funding of EUR 3.2 billion (USD 3.78 billion) upgrades Atlantic-Mediterranean rail and road links, enhancing intermodal competitiveness despite short-term energy price hurdles. Port projects at Le Havre and Marseille improve ocean-road handoffs, though labor unrest occasionally diverts traffic to Antwerp, compelling brokers to maintain alternative routings. Hydrogen refueling locations cluster along the same corridors, positioning industrial belts for early adoption of fuel-cell trucks.

Urban zones in Paris, Lyon, and Marseille tighten diesel restrictions, accelerating local electric van brokerage. European Investment Bank loans subsidize consolidation hubs that aggregate e-commerce parcels, raising LTL penetration. Rural regions such as Nouvelle-Aquitaine provide seasonal agri-food loads, requiring flexible carrier rosters to handle harvest spikes. Geographic diversity thus underpins market stability, with regulatory heterogeneity demanding localized brokerage expertise.

Mordor Intelligence tracks the freight brokerage services market across other major regions such as Europe and North America, with additional country-level coverage spanning Netherlands, Poland, Canada, Brazil, South Africa, South Korea, and Russia, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The France freight brokerage services market sits in the middle of the fragmentation scale, with global 3PLs, regional mid-caps, and pure-play tech platforms sharing clients. Incumbents like Kuehne+Nagel, DHL, and Geodis invest in blockchain customs tools, hydrogen fleets, and AI pricing to defend share against digital upstarts offering transparent apps and rapid onboarding[4]Wall Street Journal, “Geodis partners with TotalEnergies on hydrogen,” wsj.com . Start-ups target SMBs by stripping out phone calls and paperwork, converting price inquiries to confirmed bookings in under five minutes.

Sustainability reporting prowess acts as a deciding factor for enterprise tenders. Brokers boasting ISO 14083 audits, live carbon trackers, and hydrogen truck access win premium contracts. Fee-transparency debates add cost layers favoring scale economies, while cybersecurity mandates under NIS2 raise the bar for platform resilience. M&A remains active: Transporeon bought a French AI pricing specialist, and DSV finished absorbing DB Schenker’s local network, consolidating volumes and data pools that feed smarter algorithms.

Niche specialists carve out space in GDP-compliant pharma, reverse-logistics, and customs advisory. Asset-light agents leverage local ties but face capital gaps to meet ESG and digital requirements, prompting partnerships with tech vendors. Overall, technological capability, regulatory fluency, and green capacity access define competitive advantage more than fleet ownership, reshaping the long-term trajectory of the France freight brokerage services market.

France Freight Brokerage Services Industry Leaders

DHL Group

DSV

Geodis

C.H Robinson

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Kuehne + Nagel enhanced AI-driven customs and freight visibility tools across European trade lanes. Improved automation in cross-border documentation and compliance workflows.

- February 2026: DHL Global Forwarding expanded deployment of hydrogen-powered trucks in selected European freight corridors, including France.

- December 2025: GEODIS expanded low-carbon logistics initiatives across French transport corridors with energy partners. Focused on electrified and alternative-fuel-ready freight infrastructure in Europe.

- June 2025: XPO Logistics expanded contract logistics and road freight operations across Western Europe. Strengthened automotive and retail distribution capabilities in key EU markets.

France Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid & Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing & Automotive |

| Construction & Infrastructure Projects |

| Oil, Gas, Mining & Chemicals |

| Agriculture & Food / Beverage |

| Retail, FMCG & Wholesale Distribution |

| Healthcare & Pharmaceuticals |

| E-commerce & 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid & Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing & Automotive |

| Construction & Infrastructure Projects | |

| Oil, Gas, Mining & Chemicals | |

| Agriculture & Food / Beverage | |

| Retail, FMCG & Wholesale Distribution | |

| Healthcare & Pharmaceuticals | |

| E-commerce & 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How large is the France freight brokerage services market in 2026?

The France freight brokerage services market size is projected at USD 2.41 billion in 2026.

What is the expected growth rate through 2031?

Revenue is forecast to rise at a 6.68% CAGR between 2026 and 2031.

Which service segment is growing the fastest?

Less-than-truckload booking expands at 8.06% CAGR due to parcel fragmentation and urban micro-hubs.

Why are digital platforms gaining share?

AI-driven load matching and instant booking help digital brokers grow at 22.43% CAGR, especially among small businesses.

How will hydrogen trucks influence brokerage?

Subsidies and new refueling stations add low-carbon capacity that brokers can sell at premium rates to CSRD-compliant shippers.

What key challenge could slow market expansion?

Volatile electricity prices for rail and EV trucks may delay modal shift economics, restraining some multimodal growth.

Page last updated on: