Spain Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

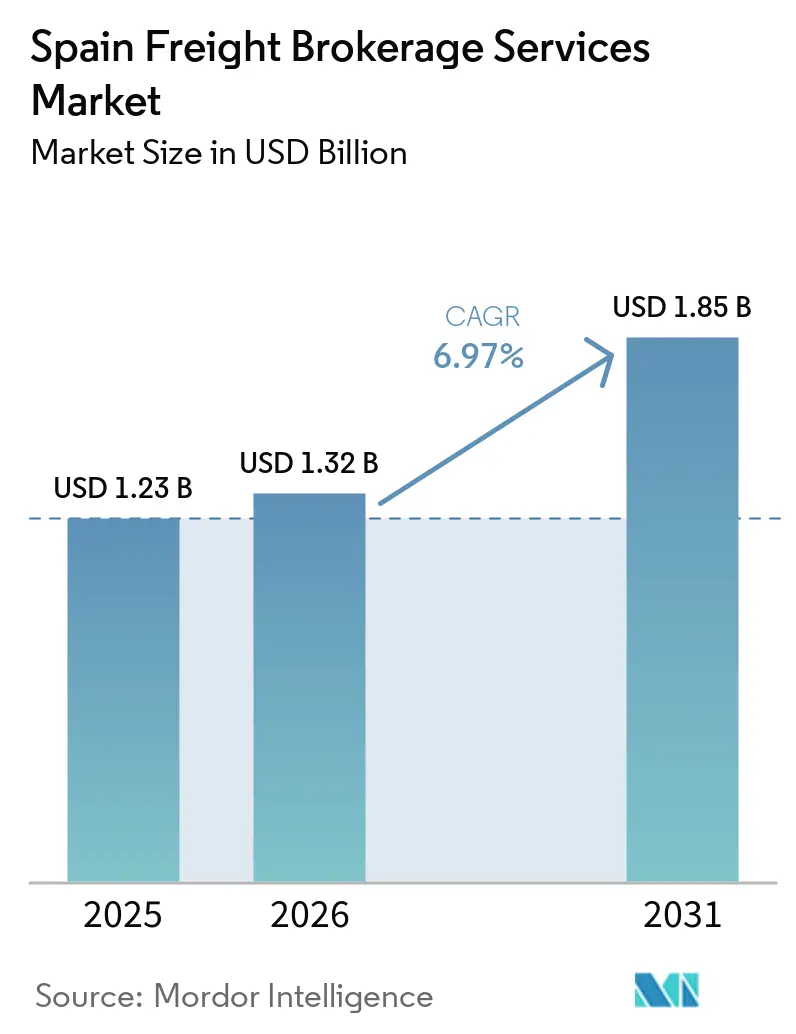

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Freight Brokerage Services Market Analysis by Mordor Intelligence

The Spain freight brokerage services market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.32 billion in 2026 to reach USD 1.85 billion by 2031, at a CAGR of 6.97% during the forecast period (2026-2031).

Digital-document mandates, automated warehouses, and expanding short-sea loops are reshaping competition, rewarding brokers that embed API-ready workflows and real-time capacity matching. Platform providers exploit these structural shifts by integrating eCMR issuance, electronic invoicing, and load-consolidation algorithms that lower compliance costs for shippers. Temperature-controlled capacity remains the anchor of the Spain freight brokerage services market, reflecting the country’s role as Europe’s fresh-produce gateway. Meanwhile, EU carbon-pricing rules and hydrogen-corridor subsidies are pushing early adoption of low-emission equipment, positioning brokers with green-lane offerings for premium growth.

Key Report Takeaways

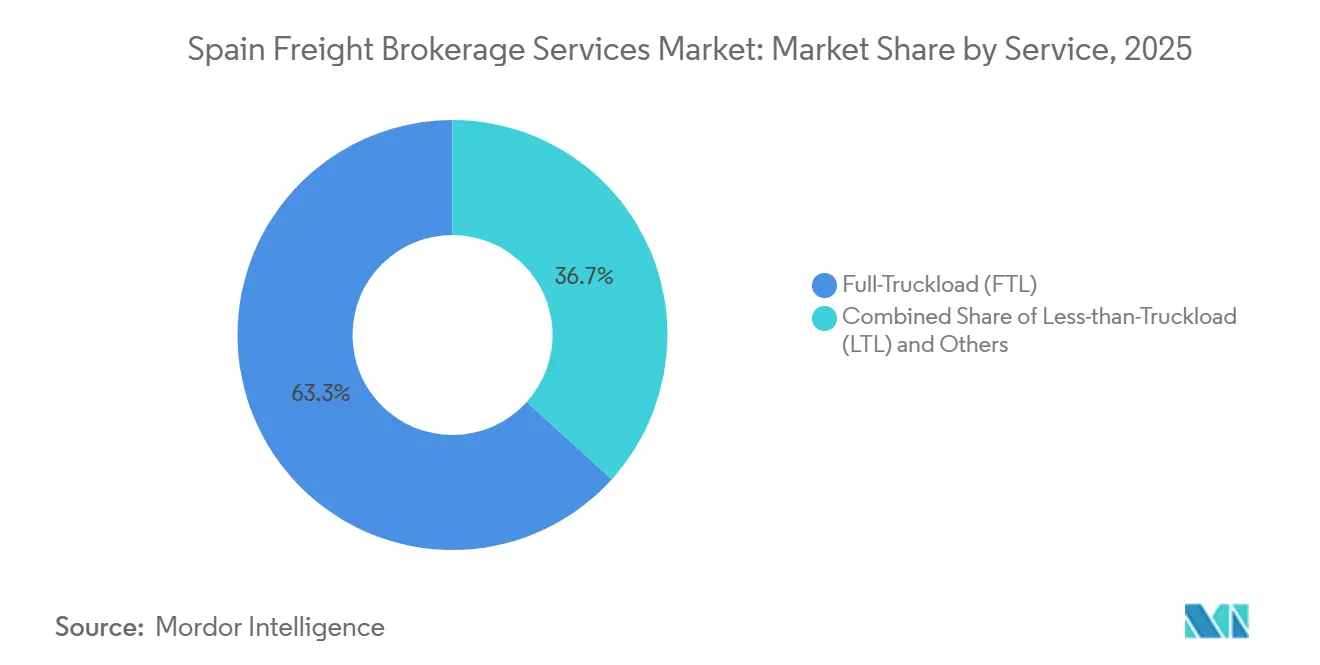

- By service, full-truckload held 63.29% of the Spain freight brokerage services market share in 2025, while Less-than-truckload services are projected to expand at an 8.76% CAGR to 2031.

- By equipment, refrigerated van capacity captured 48.39% of the Spain freight brokerage services market share in 2025, and is forecast to grow at a 9.60% CAGR through 2031.

- By haul length, long-haul operations accounted for 56.35% of the Spain freight brokerage services market size in 2025, whereas local haulage is advancing at an 11.00% CAGR during the same horizon.

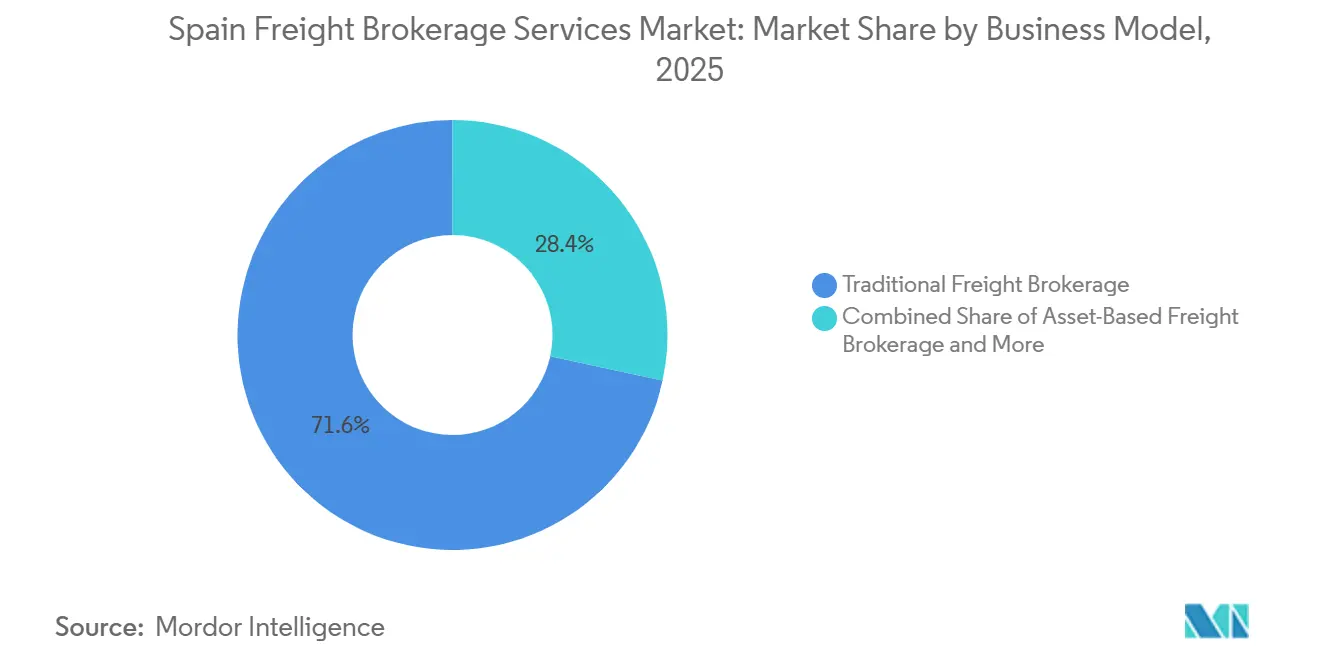

- By business model, traditional brokerage retained 71.60% of 2025 revenue, while digital platforms are scaling at a 26.04% CAGR.

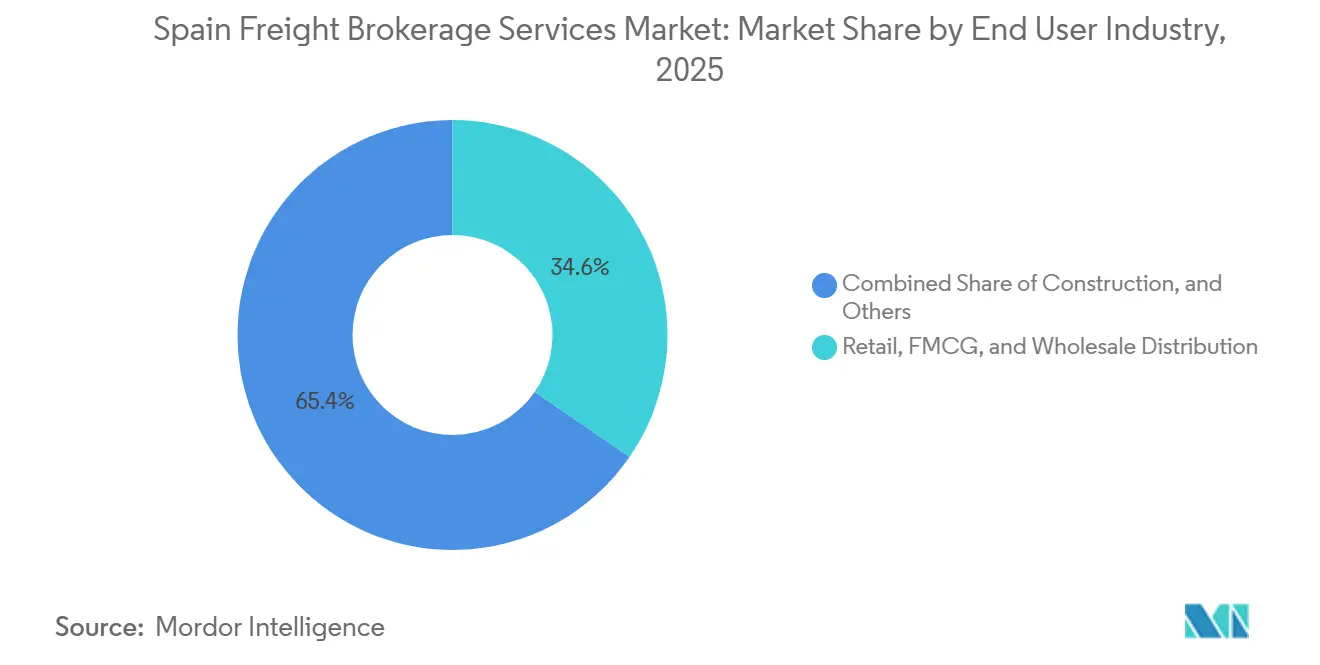

- By end user industry, retail, FMCG & wholesale distribution represented 34.60% of 2025 value, while e-commerce & 3PL fulfilment is expanding at an 18.56% CAGR.

- By customer size, large enterprises controlled 58.57% of spending in 2025; whereas small businesses will rise fastest at a 13.17% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with Spain contributing to the overall trajectory. The outlook on worldwide freight brokerage services market reflects how these are expected to evolve collectively.

Spain Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Warehouse-automation race amplifying intra-Spain same-day freight needs | +1.5% | Madrid, Barcelona, Zaragoza hubs | Short term (≤ 2 years) |

| Mandatory e-freight documents accelerating platform uptake | +1.3% | National and EU cross-border | Medium term (2-4 years) |

| ETS-2 carbon pricing boosting load-consolidation algorithms | +0.9% | National and international routes | Medium term (2-4 years) |

| Growth of Spain-Maghreb short-sea loops | +1.1% | Southern Spain-Morocco corridors | Long term (≥ 4 years) |

| Hydrogen corridor spurring green-lane products | +0.7% | Catalonia, Basque, Aragon | Long term (≥ 4 years) |

| AI-driven public–private logistics data space | +0.8% | National TEN-T integration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Warehouse-Automation Race Amplifying Intra-Spain Same-Day Freight Needs

Automated storage and retrieval systems now shrink dwell time from days to hours, forcing shippers to secure outbound trucks inside 30-minute windows. Digital brokers that ingest warehouse-management signals via API and dispatch carriers in real time monetize this velocity premium. Zaragoza’s PLAZA hub and Barcelona’s Zona Franca concentrate robotics deployments, enabling profitable same-day moves for loads above 300 kg. Traditional call-center brokers lose share as shippers pivot toward platforms offering electronic proof-of-delivery and auto-billing. Same-day expectations ripple across retail, pharma, and high-tech verticals, driving double-digit order growth for time-definite lanes.

Mandatory E-Freight Documents Accelerating Platform Uptake

Spain’s “Ley Crea y Crece” enforces e-invoices in B2B trade, and the EU eCMR framework digitizes consignment notes for cross-border trips[1]“Electronic Freight Transport Information,” European Commission, transport.ec.europa.eu. Platform brokers hard-wire both requirements, letting shippers auto-generate compliant paperwork inside their TMS. Adoption already tops 40% of carrier trips on France and Portugal corridors, versus 15% on purely domestic lanes. Compliance convenience is tipping mid-market exporters toward digital vendors, boosting onboarding rates by triple digits year over year. Paper-based operators face integration costs that erode margins and delay invoice cycles, widening the performance gap.

EU Green-Logistics and Digital-Corridor Funding

From 2027, ETS-2 will impose carbon charges that add 8-12% to diesel costs, intensifying pressure to cut empty miles[2]“El comercio de derechos de emisión de la UE para edificios, transporte por carretera y otros sectores,” Ministerio para la Transición Ecológica y el Reto Demográfico, miteco.gob.es. Algorithmic brokers that batch compatible loads can reduce deadhead by up to 40%, delivering direct cost relief and Scope 3 emission cuts. XPO’s LESS® program, launched with Repsol, previews the premium some shippers already pay for low-carbon lanes. LTL consolidation gains new relevance as carbon pricing narrows the cost differential with dedicated FTL. Platform dashboards that translate route choices into CO₂ metrics become a differentiator during procurement tenders.

Growth of Spain-Maghreb Short-Sea Loops Creating First/Last-Mile Brokerage Opportunities

Vehicle crossings between Spain and Morocco climbed 9.3% in 2024 to 847,429 units. Brokers able to stitch ferry bookings, customs filings, and local drayage into one order workflow are winning new automotive and agrifood accounts. API connectivity to ferry operators trims 12-18 hours from total transit, unlocking just-in-time flows for Tangier-Med component exports. Southern hubs such as Algeciras and Tarifa thus evolve into test beds for integrated sea-land quoting tools. Rising near-shoring by EU manufacturers further expands northbound capacity demand, stabilizing seasonal volatility typical of produce trade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NIS-2 cyber-security compliance raising operating costs for digital brokers | -0.9% | National, EU-wide compliance requirement | Short term (≤ 2 years) |

| Pending 2026–2027 national road-user charge debate creating tariff uncertainty | -0.7% | National, cross-border corridors | Short term (≤ 2 years) |

| OEM-captive logistics and retailer insourcing shrinking accessible spot volumes | -1.2% | National, concentrated in automotive and retail sectors | Medium term (2-4 years) |

| Persistent equipment imbalance at Iberian ports disrupting back-haul availability | -0.8% | Coastal regions, Mediterranean and Atlantic ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

NIS-2 Cybersecurity Compliance Raising Operating Costs for Digital Brokers

By October 2024, digital freight platforms classified as essential will file 24-hour breach reports and undergo yearly audits or risk fines of up to EUR 10 million (USD 11.7 million)[3]“The NIS2 Directive,” European Commission, digital-strategy.ec.europa.eu. Mid-size brokers must allocate EUR 200,000–500,000 (USD 23,508-58,770) annually for SOC tools, penetration testing, and staff training. These outlays accelerate consolidation as smaller entrants sell portfolios to capital-rich rivals. Traditional phone-based firms stay outside the directive’s scope yet lose customers seeking full digital visibility. The compliance burden, therefore, reshapes market structure even while slowing overall growth.

Pending 2026-2027 National Road-User Charge Debate Creating Tariff Uncertainty

Madrid’s plan to replace tolls with nationwide distance-based truck fees could add EUR 0.10-0.15 (USD 0.12-0.18) per km, equal to 15-20% of end-to-end cost on long-haul France corridors. Brokers hesitate to lock multi-year rates, inserting volatile surcharge clauses that clients resist. Contract cycles shorten, and price benchmarking becomes difficult, limiting investment in dedicated assets. Some shippers shift predictable volumes to rail or captive fleets to hedge against the unknown levy, diverting revenue from spot brokerage channels in the interim.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: LTL Gains Momentum Amid FTL Stability

Full-truckload shipments dominated with 63.29% of the Spain freight brokerage services market share in 2025, as large exporters still prefer direct point-to-point moves that simplify border transit. At the same time, less-than-truckload volumes are growing at an 8.76% CAGR because warehouse automation and omnichannel retail break orders into sub-pallet consignments. Digital route-building engines lower per-stop costs, making multi-drop tours viable on dense Madrid-Barcelona-Valencia lanes.

Rapid LTL uptake is diversifying the Spain freight brokerage services market. Brokers able to merge partial loads into full trailers capture higher revenue per mile while offering shippers carbon-efficient options. FTL brokers respond by launching hybrid services that guarantee a base trailer but monetize unused floor space through spot inserts, blurring traditional segment boundaries.

By Equipment/Trailer Type: Cold Chain Dominance Extends

Refrigerated vans held 48.39% of the Spain freight brokerage services market size in 2025, and will expand at a 9.60% CAGR as Spain’s fruit, veg, and vaccine exports require tight temperature control. Electric self-charging reefers introduced in 2025 cut diesel genset use and unlock urban low-emission zones, attracting premium payloads from pharma and grocery chains. Dry-van boxes remain essential for consumer staples but grow more slowly, while tankers and flatbeds cycle with chemicals and construction output.

Within the Spain freight brokerage services market size, cold-chain lanes exhibit the lowest price elasticity, letting brokers pass on fuel surcharges without losing share. Those managing validated GDP lanes add analytics on temperature excursions, creating stickiness with life-science customers. As produce seasonality shifts, brokers redeploy reefers into frozen seafood and confectionery, smoothing asset utilization year-round[4]“Report of the Scientific Committee on Time-Temperature Combinations for Food Safety,” Agencia Española de Seguridad Alimentaria y Nutrición, aesan.gob.es.

By Haul Length: Urbanization Drives Local Surge

Long-haul corridors above 500 miles kept 56.35% of the Spain freight brokerage services market share in 2025, owing to France, Germany, and Benelux exports that sustain high-capacity trunk lines. Yet local trips under 100 miles post the fastest 11.00% CAGR, mirroring micro-fulfillment buildouts around Spain’s top metro areas. Same-day expectations convert regional depots into city-edge cross-docks, cutting line-haul distances and boosting trip frequency.

For brokers, local runs mean thinner margins per load but higher commission velocity. The Spain freight brokerage services market size therefore skews toward platforms that can aggregate hundreds of urban drops into coherent driver schedules. Long-haul specialists hedge by opening satellite offices inside Madrid and Barcelona to capture this fast-growing micro-segment before new entrants dominate.

By Business Model: Digital Platforms Narrow Traditional Gap

Traditional brokerage still controlled 71.60% of the Spain freight brokerage services market size in 2025, reflecting decades-deep carrier ties and regional know-how. However, digital platforms logged a 26.04% CAGR by automating quoting, eCMR, and settlement, slashing transaction time from hours to minutes. Asset-based brokers hold ground in temperature-controlled and hazardous lanes where dedicated fleets assure compliance.

Convergence is under way. Traditional houses invest in white-label portals while pure-play platforms hire former carrier reps to improve human support. The resulting hybrid designs expand the Spain freight brokerage services industry toolkit without diluting digital margins. Success hinges on balancing algorithmic precision with sector-specific expertise, particularly in post-Brexit customs and North-African ferry links.

By End-User Industry: E-Commerce Reshapes Demand Mix

Retail, FMCG & wholesale distribution generated 34.60% of 2025 market share, but e-commerce & 3PL fulfilment is sprinting ahead at an 18.56% CAGR. Reverse-logistics volumes rise in lockstep, compelling brokers to add return-management and quality-check nodes. Automotive and heavy industry retain steady flows yet face insourcing that limits brokerage penetration.

Pharma, fresh food, and high-tech verticals demand GDP-compliant handling and GPS temperature feeds, raising service complexity and margin potential. E-grocers adopt weekly tender models where algorithms auto-award lanes based on historic on-time metrics, a shift that favors data-driven entrants. Consequently, diversification across verticals insulates brokers from cyclical shocks in any single sector.

By Customer Size: Platform Democratization Benefits SMEs

Large enterprises still commanded 58.57% of 2025 market size, but small businesses under USD 10 million revenue are growing at a 13.17% CAGR thanks to self-service portals that drop entry barriers. Instant quoting, credit-card settlement, and pay-per-load visibility levels the playing field against volume-tied contracts once restricted to big shippers.

Within the Spain freight brokerage services market, SMEs collectively form a fragmented but fast-scaling pool that stabilizes broker revenue during enterprise tender lulls. Platforms gamify carrier feedback to reassure first-time shippers, while AI chatbots resolve routine queries, keeping service costs low. Mid-market firms, meanwhile, seek blended support automated booking paired with named account managers nudging brokers to tier service packages by customer size.

Geography Analysis

Spain’s dual-coast port network processed 557.8 million tons of cargo in 2024, anchoring first-mile and last-mile brokerage flows that extend inland toward Madrid’s logistics belt. The Mediterranean Corridor links Algeciras to the French border, transmitting import pulses to produce packing houses in Murcia and export surges from Catalonia’s factories. Investments under the EU TEN-T scheme digitize these arteries, letting brokers issue electronic transit documents and tap rail capacity without manual interchange.

The Madrid-Barcelona-Valencia triangle hosts dense consumption and modern fulfilment centers, making it the epicenter of the Spain freight brokerage services market. Zaragoza’s crossroads location attracts Amazon, Kuehne+Nagel, and DSV, which funnel steady outbound loads that fuel LTL growth. Southern Andalusia leverages Morocco-bound ferry loops to diversify away from traditional agrifood exports into automotive and textile shuttle runs.

Iberian integration with Portugal unlocks bilateral consolidations that shave empty legs, while Basque and Catalan hydrogen valleys pilot zero-emission lanes, attracting sustainability-minded multinationals. Geographic diversification thus cushions brokers from regional slowdowns and spreads network risk across coastal, central, and cross-border corridors, underpinning long-term resilience of the Spain freight brokerage services market.

Analysis of the freight brokerage services market by Mordor Intelligence spans multiple other regional evaluations across Europe and North America, supported by country-level insights for Poland, Russia, Canada, Brazil, South Africa, South Korea, and Mexico, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Competition is moderately fragmented, with digital disruptors scaling through M&A and traditional players defending niches that prize human expertise. Sennder’s purchase of C.H. Robinson’s European surface unit vaulted the start-up into the top tier, proving that technology platforms can buy carrier relationships rather than build them over decades. GXO, XPO, and Logista differentiate through value-added warehousing and green-fleet investments, integrating brokerage with contract logistics for stickier revenue streams.

Cyber-security mandates and carbon pricing raise capital requirements that smaller brokers cannot shoulder alone, accelerating consolidation. Still, service specialization pharma GDP compliance, oversized machinery escort, or Morocco customs brokerage creates defensible moats where scale is secondary to know-how. Digital entrants courting these verticals recruit veteran operators to bridge credibility gaps.

Technology remains the great equalizer. AI load-matching, IoT trailer sensors, and blockchain-verified PoD narrow information asymmetry, compressing price variance across brokers. Survivors will be those that marry tech fluency with sector fluency, offering configurable service layers that match shipper sophistication. This dynamic keeps the Spain freight brokerage services market vibrant even as top-five concentration edges upward.

Spain Freight Brokerage Services Industry Leaders

Ontruck

Trucksters

Sennder

DHL Group

XPO, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: GXO began operating a 36,000 m² automated facility for Hisense in Valencia, cutting order-to-dispatch time to two hours.

- March 2025: Cargobot launched Planimatik in Spain, delivering AI route optimization to mid-market shippers.

- March 2025: Logista added self-charging electric reefers, lowering cold-chain emissions by 25%.

- February 2025: Sennder acquired C.H. Robinson Europe’s surface business, adding 1,600 staff across 20 sites.

Spain Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid and Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing and Automotive |

| Construction and Infrastructure Projects |

| Oil, Gas, Mining and Chemicals |

| Agriculture and Food / Beverage |

| Retail, FMCG and Wholesale Distribution |

| Healthcare and Pharmaceuticals |

| E-commerce and 3PL Fulfilment |

| Others |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid and Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing and Automotive |

| Construction and Infrastructure Projects | |

| Oil, Gas, Mining and Chemicals | |

| Agriculture and Food / Beverage | |

| Retail, FMCG and Wholesale Distribution | |

| Healthcare and Pharmaceuticals | |

| E-commerce and 3PL Fulfilment | |

| Others | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How large will Spain’s freight-broker revenue pool be by 2031?

It is forecast to reach USD 1.85 billion, rising from USD 1.32 billion in 2026 at a 6.97% CAGR.

Which equipment type is expanding quickest?

Refrigerated vans, reflecting cold-chain demand, are projected to grow at a 9.60% CAGR to 2031.

What business model is gaining the most share?

Digital freight brokerage is advancing at 26.04% CAGR, chipping away at traditional dominance.

How will ETS-2 influence freight costs?

Carbon charges could raise diesel expenses 8-12%, motivating shippers to favor consolidation algorithms.

Why are local haul lanes attractive?

Urban micro-fulfillment and same-day delivery targets push local (Less-Than 100 mile) moves to an 11.00% CAGR.

What is the primary regulatory hurdle for digital brokers?

NIS-2 cybersecurity rules mandate audits, incident reporting, and board accountability, lifting compliance costs.

Page last updated on: