Germany Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

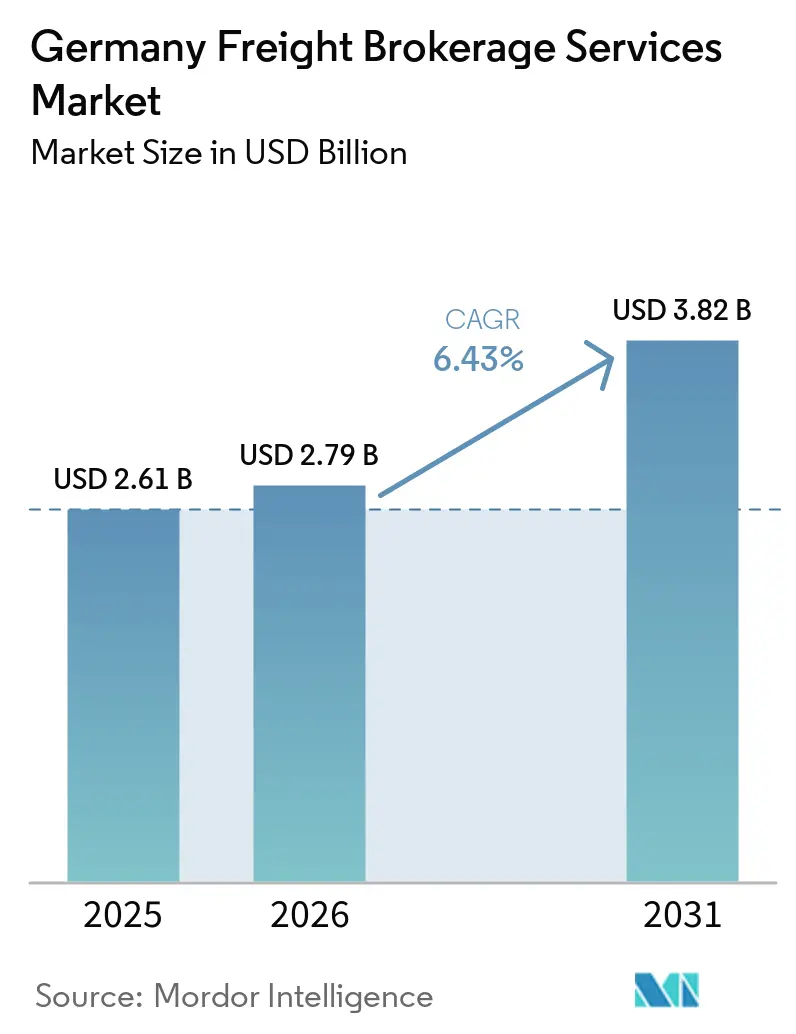

| Base Year Market Size (2025) | USD 2.61 Billion |

| Market Size (2026) | USD 2.79 Billion |

| Market Size (2031) | USD 3.82 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Freight Brokerage Services Market Analysis by Mordor Intelligence

The Germany freight brokerage services market size is projected to be USD 2.61 billion in 2025, USD 2.79 billion in 2026, and reach USD 3.82 billion by 2031, growing at a CAGR of 6.43% from 2026 to 2031.

Demand expands because manufacturers diversify Eurasian trade routes, shippers chase real-time load visibility, and federal policy keeps toll exemptions for zero-emission trucks. Digital platforms now compress quoting cycles to seconds, while wage-parity audits and cyber-risk compliance lift operating costs. Venture funding remains strong, illustrated by cargo.one’s USD 18.5 million raise in February 2026, which fuels algorithmic carrier matching across 121 countries. Carrier power is also shifting as DSV finishes its USD 15.2 billion purchase of DB Schenker, pledging USD 1 billion in local investments that will deepen integrated service offerings.[1]Federal Ministry for Digital and Transport, “Overall Approach to Climate-Friendly Commercial Vehicles: 2026 Progress Report on Market Ramp-up and Infrastructure Integration,” bmdv.bund.de

Key Report Takeaways

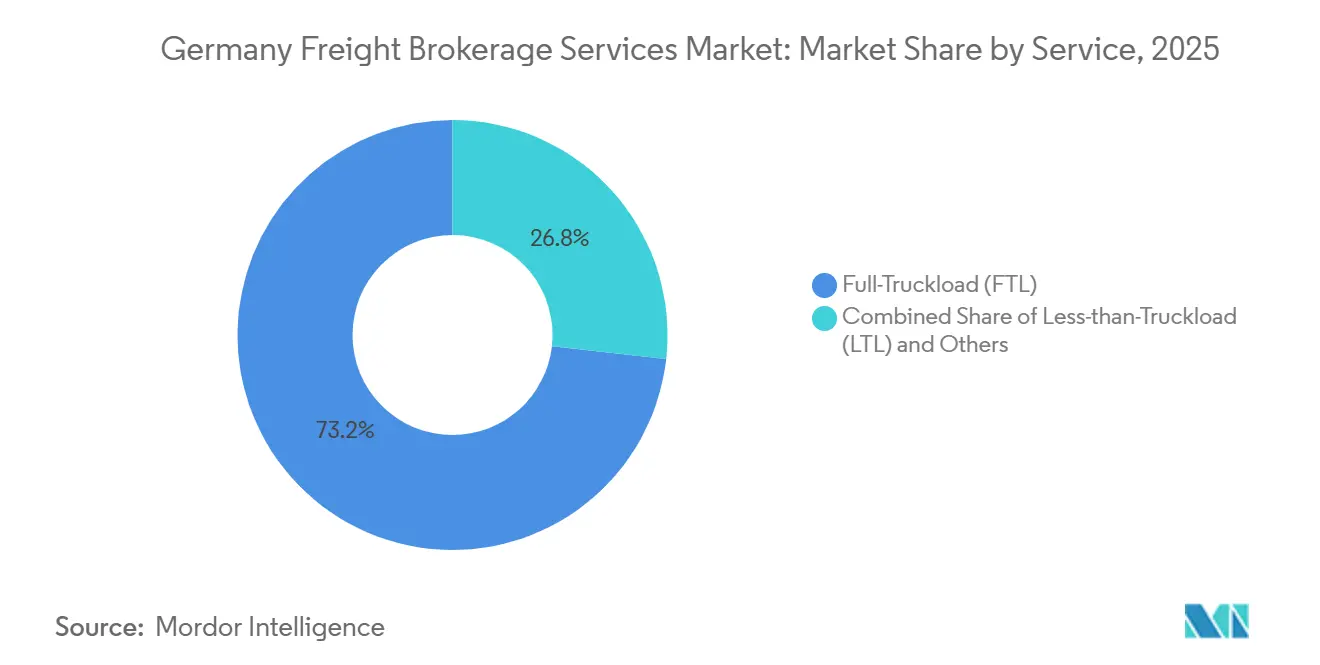

- By service type, full-truckload held 73.22% of Germany freight brokerage services market share in 2025, while less-than-truckload is forecast to expand at an 8.09% CAGR to 2031.

- By equipment, dry-van trailers captured 38.41% of the Germany freight brokerage services market size in 2025, whereas refrigerated vans are projected to grow at an 8.67% CAGR through 2031.

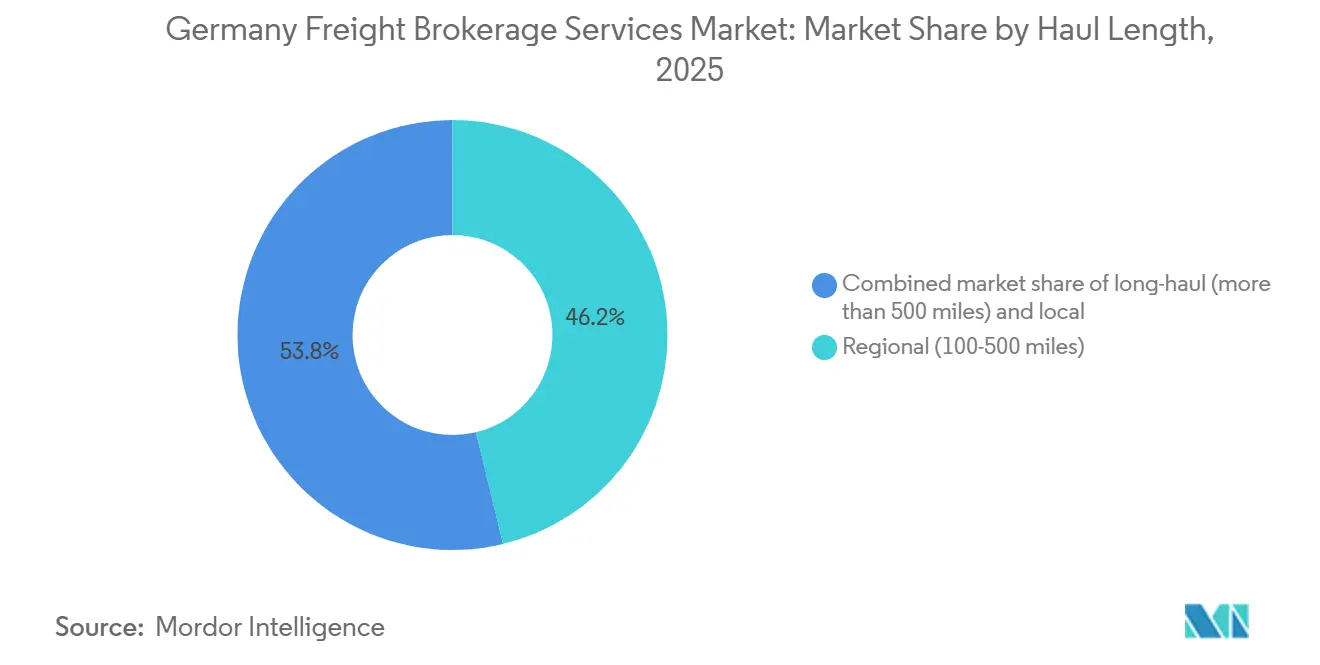

- By haul length, regional lanes controlled 46.23% share in 2025, yet local hauls under 100 miles are advancing at an 8.91% CAGR over the forecast window.

- By business model, traditional brokers commanded 68.32% revenue in 2025, but digital freight brokerage is set to rise at a 27.98% CAGR to 2031.

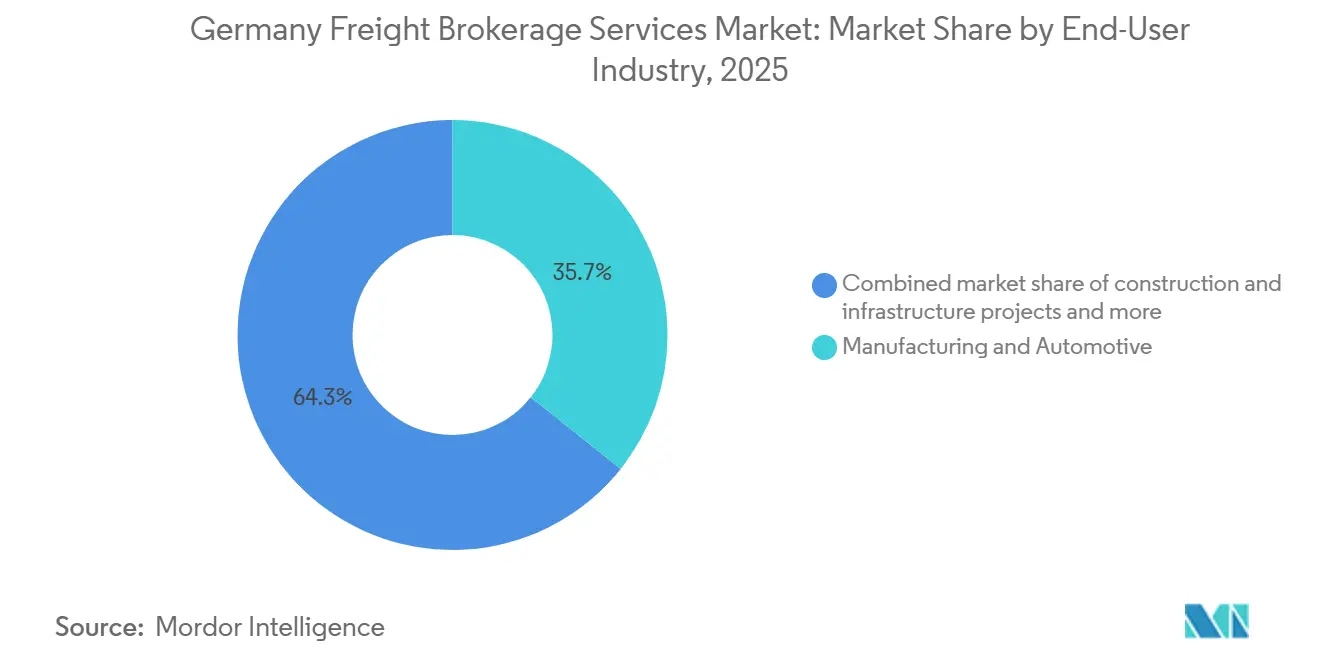

- By end-user industry, manufacturing and automotive accounted for 35.70% of brokerage outlay in 2025, while e-commerce and 3PL fulfillment is climbing at an 18.62% CAGR.

- By customer size, large enterprises produced 70.85% of spend in 2025, whereas small businesses are growing at a 14.00% CAGR backed by self-service digital portals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Germany. The freight brokerage services market share in our global report expresses these relative weights.

Germany Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Red Sea diversion boosting Eurasian rail-to-road trans-loading through Germany | +1.5% | Duisburg, Hamburg hubs with spill-over to Benelux and Poland | Medium term (2-4 years) |

| Electrified-truck subsidy wave unlocking new capacity corridors | +1.2% | National, early build-out in Baden-Württemberg, Nordrhein-Westfalen, Bayern | Medium term (2-4 years) |

| AI-based dynamic lane-pricing demanded by the top 500 German shippers | +0.9% | National, centered on DAX manufacturers and retailers | Short term (≤ 2 years) |

| Corporate Scope-3 emissions audits creating a premium for tracked loads | +0.7% | Automotive, pharma, FMCG clusters nationwide | Long term (≥ 4 years) |

| Shift from FOB to DDP terms in Mittelstand exports raising brokerage need for door-to-door control | +0.6% | Export-heavy regions in Baden-Württemberg, Bayern, Hessen | Medium term (2-4 years) |

| Federal “ETA transparency mandate” accelerating API adoption | +0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post–Red-Sea Diversion boosting Eurasian Rail-to-Road Trans-loading through Germany

Persistent piracy risk has pushed Asia-Europe ocean cargo toward Eurasian rail, lifting China-EU rail volume to 380,434 TEU in 2024, an 80.2% jump year on year. Duisburg and Hamburg act as gateways where inland terminals shift containers to trucks for final delivery, creating high-margin, time-sensitive loads for brokers. Empty-box repositioning also grows as westbound rail leaves fewer empties in Germany, compelling brokers to organize backhauls to North Sea ports. Unless Red Sea routes normalize, brokers can rely on this rail-driven uplift through at least 2027, embedding new revenue channels in Germany freight brokerage services market operations.

Electrified-Truck Subsidy Wave Unlocking New Capacity Corridors

Germany has allocated USD 1.74 billion for 1,410 high-power chargers along major autobahns, a move that lowers per-kilometer energy cost by 40% for battery trucks and widens lane options for brokers. Toll exemptions for zero-emission heavy vehicles now run to mid-2031, shrinking the total cost of ownership and encouraging mid-sized carriers to replace diesel tractors sooner. Brokers that ingest telematics data from electric fleets can reroute around scarce chargers, cut dwell time, and advertise low-carbon capacity to shippers seeking greener loads. Charging clusters on A3, A5, and A7 already shift volume from diesel lanes. The program therefore delivers both cost savings and new selling points that propel Germany freight brokerage services market growth.[2]European Commission, “State Aid SA.115462: German scheme for the deployment of fast-charging infrastructure for electric heavy-duty vehicles,” ec.europa.eu/competition-policy

AI-Based Dynamic Lane-Pricing Demanded by Top 500 German Shippers

Large manufacturers now insist on algorithmic spot pricing that digests real-time capacity, weather, and historic volatility to refresh quotes within minutes. Cargo.one’s February 2026 purchase of Cargofive embeds this AI engine, letting brokers return binding offers at platform speed and compress procurement cycles. TIMOCOM and Saloodo follow suit with price-prediction modules that also screen carriers for fraud. While the tech squeezes margins on commodity lanes, it opens premium revenue streams around cross-dock services and customs brokerage. Rapid, transparent pricing therefore strengthens customer loyalty and keeps Germany freight brokerage services market competitive.

Corporate Scope-3 Emissions Audits Creating Premium for Tracked Loads

The EU Corporate Sustainability Reporting Directive forces large firms to count freight emissions, prompting procurement teams to pay 5-10% premiums for loads with verifiable CO₂ data. Digital brokers plug telematics feeds into tools such as EmissionTrack to supply activity-based emissions numbers, easing audit pain for automotive and pharmaceutical shippers. Carriers lacking ISO 14001 certification now face reduced tender invitations, tightening compliance capacity, and nudging rates upward. Over time, ETS expansion will likely embed carbon cost into spot quotes, making tracked low-carbon loads a baseline expectation rather than a differentiating perk.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Mobility Package IV wage-parity audits inflating compliance overhead | -0.8% | National with cross-border checks in Benelux, France, and Austria | Short term (≤ 2 years) |

| Cyber-attacks on freight-exchange APIs increasing insurance premiums | -0.5% | Digital platforms and TMS providers nationwide | Medium term (2-4 years) |

| Logistic-hub zoning freeze limiting cross-dock expansion | -0.3% | Nordrhein-Westfalen, Rhine-Ruhr corridor | Long term (≥ 4 years) |

| Volatile OEM production cycles driving demand swings | -0.6% | Automotive clusters in Baden-Württemberg, Bayern | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Mobility Package IV Wage-Parity Audits Inflating Compliance Overhead

From January 2026, Germany will enforce a USD 15.1 hourly wage floor for posted drivers, erasing the historical 25% rate edge held by Eastern European carriers. Brokers now spend extra hours auditing payroll files and tachograph logs, or risk stiff penalties. Smart Tachograph 2 rules, hitting light vans in July 2026, widen the audit scope. Some small brokers are exiting cross-border lanes rather than funding compliance tools, which tightens capacity and raises spot prices but also crimps broker margins.[3]Federal Ministry of Labour and Social Affairs (BMAS), “Report on the Development of the Statutory Minimum Wage and the Posting of Workers in the Transport Sector: 2026 Compliance Audit Findings,” bmas.de

Cyber-Attacks on Freight-Exchange APIs Increasing Insurance Premiums

Half of German logistics firms reported hacks in 2025, and insurers have since lifted cyber-liability premiums 15-25% for high-volume brokers. The NIS2 directive now classifies large freight exchanges as essential entities, forcing 24-hour incident reporting and annual penetration tests. Platforms without ISO 27001 certification face coverage exclusions, steering shippers toward larger, better-protected brokers. Compliance costs eat into profit, yet failure risks even greater losses from ransomware downtime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Full-Truckload Retains Scale While LTL Gains Speed

Full-truckload commanded 73.22% of Germany freight brokerage services market share in 2025, as automotive just-in-sequence shipments and bulk chemicals relied on dedicated trailers. Contract lanes give shippers predictable rates, and brokers earn steady margins from repeat volume. Network depth along A4, A6, and A9 supports same-day north–south runs, a critical feature for tier-one suppliers.

Less-than-truckload solutions are projected to grow at an 8.09% CAGR to 2031, supported by e-commerce parcel consolidation and small-batch industrial orders. IDS Logistik’s tie-up with Spedition Kleine brings 800 daily deliveries into its Grevenbroich hub, a case that proves how dock-scheduling APIs can cut yard dwell by 70%. Brokers aggregating 2-10-pallet loads now leverage AI to optimize cube and reduce empty miles, lifting yield and enhancing the Germany freight brokerage services market size for LTL operators.

By Equipment Type: Dry Vans Dominate, Reefers Outpace

Dry-van trailers held 38.41% of equipment revenue in 2025 because they move consumer goods, packaged foods, and industrial parts with minimal special handling. Their ubiquity ensures the widest carrier pool, which keeps spot quotes competitive.

Refrigerated vans are forecast to expand at an 8.67% CAGR, fueled by cold-chain audits for vaccines and the spread of online grocery. Seasonal fruit runs from Spain and Italy boost Germany-bound reefer spot rates to double dry-van levels during winter peaks. Brokers that pre-book electric reefer units at grid-connected parking bays enjoy lower diesel surcharges and gain loyalty from carbon-conscious food retailers, increasing the size of the German freight brokerage services market captured in the temperature-controlled niche.

By Haul Length: Regional Corridors Anchor Volume, Local Miles Accelerate

Regional trips of 100-500 miles contributed 46.23% of Germany freight brokerage services market size in 2025, by stitching together Germany’s dense industrial clusters and cross-border flows into Benelux and Poland. Contract rates protect margins, and carriers optimize driver schedules within daily hours limits.

Local hauls below 100 miles will climb at an 8.91% CAGR through 2031 as urban micro-fulfillment centers demand frequent restocks. Hermes deployed zero-emission vans in 80 cities in February 2026, setting a blueprint for same-day grocery and health-care deliveries. Brokers integrating AI route planners cut empty mileage in tight urban zones, preserving profitability despite short trip lengths.

By Business Model: Relationship Brokers Hold Value, Digital Platforms Scale Fast

Traditional brokers still controlled 68.32% of Germany freight brokerage services market share in 2025, using long-standing carrier ties and extended credit terms to lock in blue-chip shippers. Their field teams solve exceptions rapidly, a service that digital portals cannot always match.

Digital platforms are on track for a 27.98% CAGR thanks to real-time capacity feeds and instant documentation. Cargo.one’s new AI engine now returns quotes in seconds, trimming average procurement cycles by days. Platforms acting as the contractual counterparty, such as Saloodo, further ease shipper risk by guaranteeing quick carrier payments, expanding the size of the German freight brokerage services market that flows through marketplaces.

By End-User Industry: Manufacturing Leads Spend, E-Commerce Surges

Manufacturing, including automotive, held 35.70% of spend in 2025 because just-in-sequence flows penalize delays and pay premium rates for reliability. OEMs in München and Stuttgart rely on brokers with ISO-certified carriers and real-time visibility dashboards.

E-commerce and 3PL fulfillment segments are projected to post an 18.62% CAGR. Rhenus now manages Zwilling’s European warehouse in Wesel, combining engraving and kitting services with returns handling, which generates steady inbound and reverse-logistics loads. Brokers able to flex fleet mix between parcel vans and 7.5-ton trucks will capture this rising Germany freight brokerage services market size slice.

By Customer Size: Large Enterprises Drive Revenue, SMEs Widen the Base

Large shippers above USD 100 million in revenue supplied 70.85% of the value in 2025, leveraging annual tenders and demanding API connections to ERP systems. Multi-year contracts increase predictability but leave little margin for brokers that fail key performance metrics.

Small businesses will expand at a 14.00% CAGR through self-service portals. Quicargo’s backhaul marketplace promises up to 30% savings for one-off pallets, a boon for makers of craft beverages and niche components. This democratization broadens Germany freight brokerage services market participation beyond traditional high-volume shippers.

Geography Analysis

Nordrhein-Westfalen, Bayern, and Baden-Württemberg together generated almost 60% of 2025 brokerage activity because they house dense manufacturing clusters, the Rhine-Ruhr rail hub, and key autobahn intersections. Duisburg’s terminals now process record Eurasian rail freight, yet zoning caps on new warehouses force brokers to route overflow to Hessen, lengthening average delivery distance and nudging rates upward.

Northern gateways Hamburg and Bremen specialize in container drayage toward Scandinavia. Toll exemptions for zero-emission heavy trucks on long Hamburg-to-Munich corridors can save carriers up to USD 152 per trip, accelerating electric-truck uptake and giving brokers greener capacity to market.

Eastern states, Sachsen and Brandenburg, grow as low-cost alternatives close to Polish and Czech factories. IDS Logistik’s new Grevenbroich node illustrates how well-placed cross-docks pull cargo toward the Rhine-Ruhr corridor for final distribution. As cross-border tendering simplifies, brokers with multilingual dispatch teams and local carrier ties will secure a larger slice of Germany freight brokerage services market share.[4]Federal Office for Logistics and Mobility (BALM), “Structure of the German Logistics Market: Regional Activity Analysis and Infrastructure Impact Report 2025/2026,” balm.bund.de

Mordor Intelligence examines the freight brokerage services market across diverse other regional markets as well, including Europe and North America, while also offering granular country-level perspectives for Spain, Netherlands, Canada, Saudi Arabia, Brazil, South Africa, and South Korea and more.

Competitive Landscape

The field stays fragmented; no broker tops 10% of national revenue, yet consolidation gains pace. Sennder closed its purchase of C.H. Robinson’s European surface arm in February 2025, blending an API-first platform with a USD 1.52 billion lane book and 1,700 staff to anchor a top-five regional position.

DSV’s USD 15.2 billion takeover of DB Schenker in April 2025 includes a promised USD 1 billion investment that widens branch networks and folds road, sea, and air into one interface. Smaller specialists respond by teaming up; CTL joined pfenning-Gruppe in June 2025 to unify LTL, warehousing, and contract logistics under one contract, simplifying shipper workflows.

Tech dictates future winners. Platforms with ISO 27001 security, live telematics dashboards, and AI carrier scoring win compliant shippers while analog brokers face fines under the NIS2 cyber law. White-space niches such as GDP-certified pharma loads or electrified reefer tracking still allow focused entrants to earn double-digit margins despite mounting scale economies in the wider Germany freight brokerage services industry.

Germany Freight Brokerage Services Industry Leaders

DHL Group

Kuehne + Nagel

Rhenus Logistics

Hellmann Worldwide Logistics

DSV A/S (including DB Schenker)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: cargo.one closed its acquisition of the ocean rate platform Cargofive, simultaneously launching the industry's first AI-native operating system for multimodal freight. Backed by a new USD 20 million investment, the platform now provides instant quoting and "AI agents" that work alongside human dispatchers across 172 countries.

- February 2026: Kuehne+Nagel acquired the road logistics division of LSL-Lohmoller, a Northwest German specialist with an annual turnover of EUR 23.5 million (USD 27.7 million). The deal integrates 142 specialists and 50 trucks into the K+N network, significantly strengthening its position within the IDS groupage cooperation during a period of high market consolidation.

- January 2026: Germany officially enforced the extension of 100% toll exemptions for zero-emission heavy-duty vehicles until June 30, 2031. This policy has triggered a "subsidy wave," as brokers now prioritize electric-truck capacity to save up to EUR 140 (USD 163) per long-haul trip, fundamentally reshaping the competitive landscape for 2026 tenders.

- April 2025: Transporeon launched the "All-in-One" Digital Freight Platform. The platform was built to bridge the gap between freight forwarders looking for reliable spot capacity and asset-operating carriers seeking loads.

Germany Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid & Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing & Automotive |

| Construction & Infrastructure Projects |

| Oil, Gas, Mining & Chemicals |

| Agriculture & Food / Beverage |

| Retail, FMCG & Wholesale Distribution |

| Healthcare & Pharmaceuticals |

| E-commerce & 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid & Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing & Automotive |

| Construction & Infrastructure Projects | |

| Oil, Gas, Mining & Chemicals | |

| Agriculture & Food / Beverage | |

| Retail, FMCG & Wholesale Distribution | |

| Healthcare & Pharmaceuticals | |

| E-commerce & 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10–100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How large will Germany freight brokerage services market be by 2031?

It is projected to reach USD 3.82 billion by 2031, advancing at a 6.43% CAGR from 2026.

Which service type currently dominates brokerage revenue?

Full-truckload held 73.22% of revenue in 2025 because automotive and bulk shippers value dedicated trailers.

What segment is growing fastest?

Digital freight brokerage is rising at a 27.98% CAGR to 2031 as instant quoting and API visibility spread.

Why are refrigerated trailers in higher demand?

Cold-chain audits for vaccines and growth in online grocery push reefer demand, giving the segment an 8.67% CAGR.

How do EU wage-parity rules impact brokers?

Minimum wage audits add hours of compliance per load and narrow the cost gap between domestic and Eastern European carriers, lifting operating costs.

Which regions inside Germany generate the most brokerage activity?

Nordrhein-Westfalen, Bayern, and Baden-Württemberg contribute nearly 60% of national brokerage volume due to rail hubs and automotive clusters.

Page last updated on: