Brazil Agricultural Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

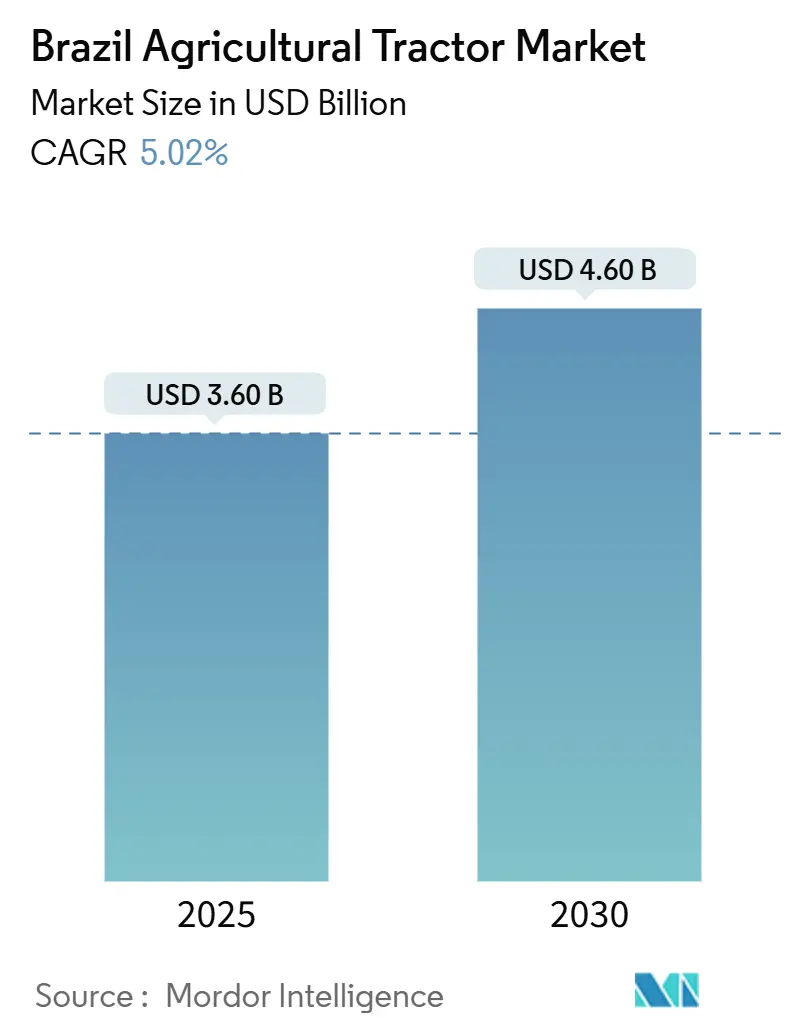

| Market Size (2025) | USD 3.60 Billion |

| Market Size (2030) | USD 4.60 Billion |

| Growth Rate (2025 - 2030) | 5.02% CAGR |

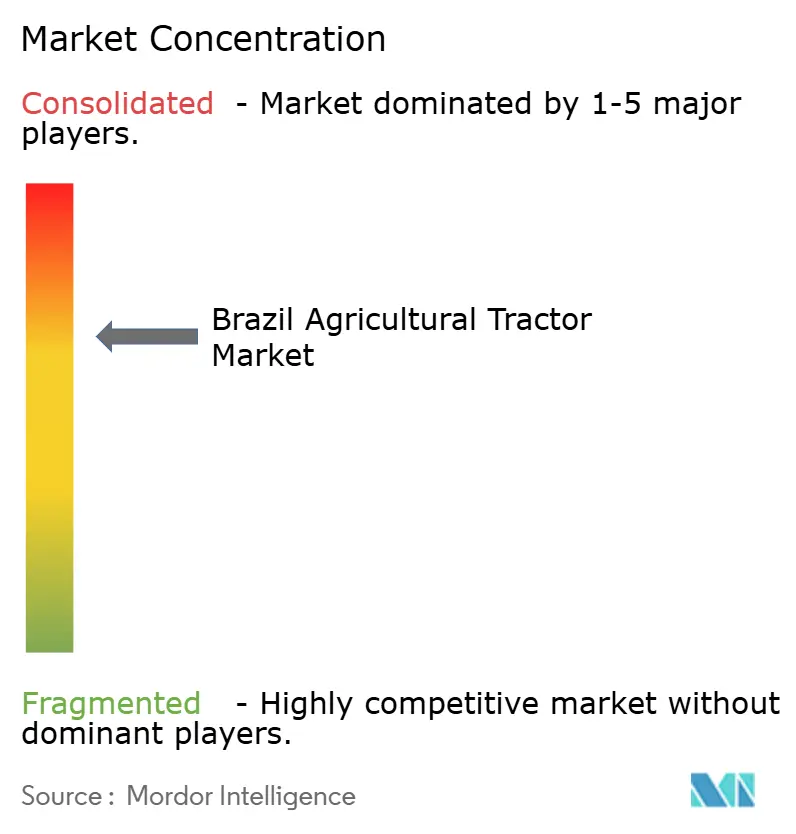

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Agricultural Tractor Market Analysis by Mordor Intelligence

The Brazil agricultural tractors market size is projected to grow from USD 3.6 billion in 2025 to USD 4.6 billion by 2030, registering a CAGR of 5.02%. The market growth is supported by advanced drivetrain adoption, improved credit accessibility through government policies, and increased digitization in grain and sugarcane production.[1]Confederação da Agricultura e Pecuária do Brasil, “Panorama do Agro,” CNABRASIL.ORG.BR While high interest rates currently affect purchasing capacity, ongoing government initiatives like Plano Safra and higher ethanol blending requirements continue to drive mechanization. The agricultural labor shortage is increasing the demand for tractors. The market is also benefiting from partnerships between equipment manufacturers and financial technology companies that enhance financing options, while local manufacturing capabilities reduce delivery times and reliance on imports.

Key Report Takeaways

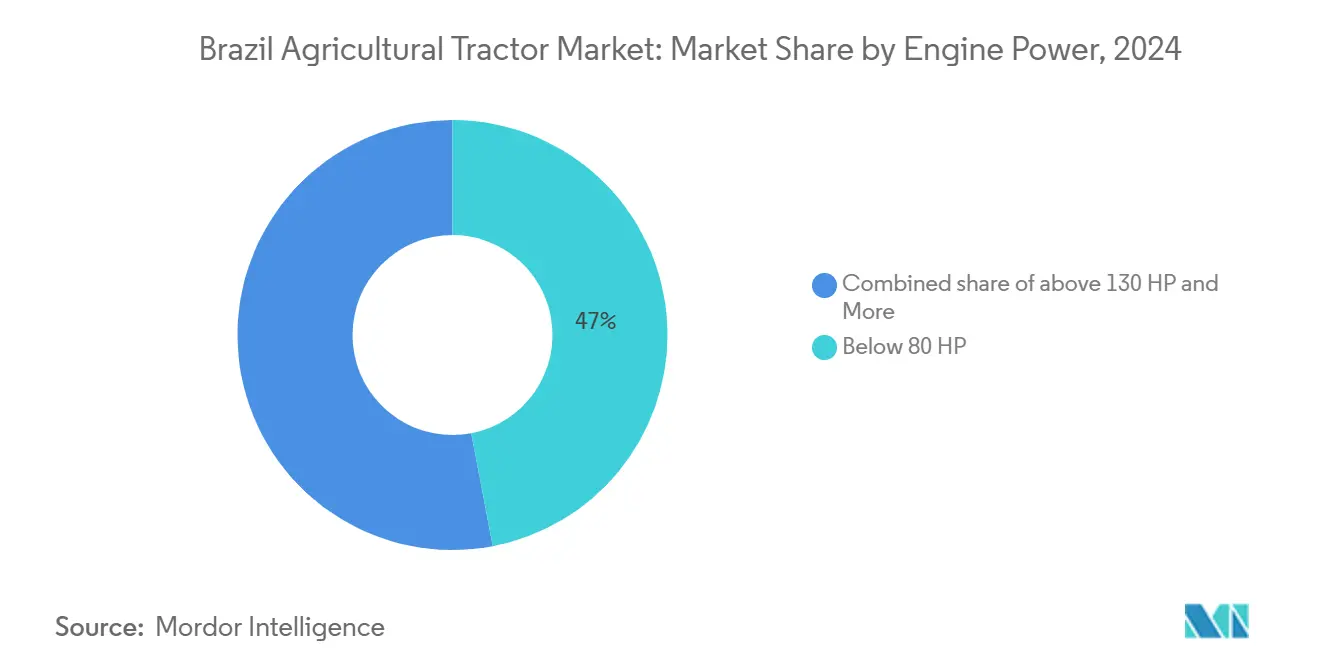

- By engine power, tractors under 80 HP held 47% of the Brazil agricultural tractors market size in 2024, while the above 130 HP category is tracking the fastest 7.5% CAGR through 2030.

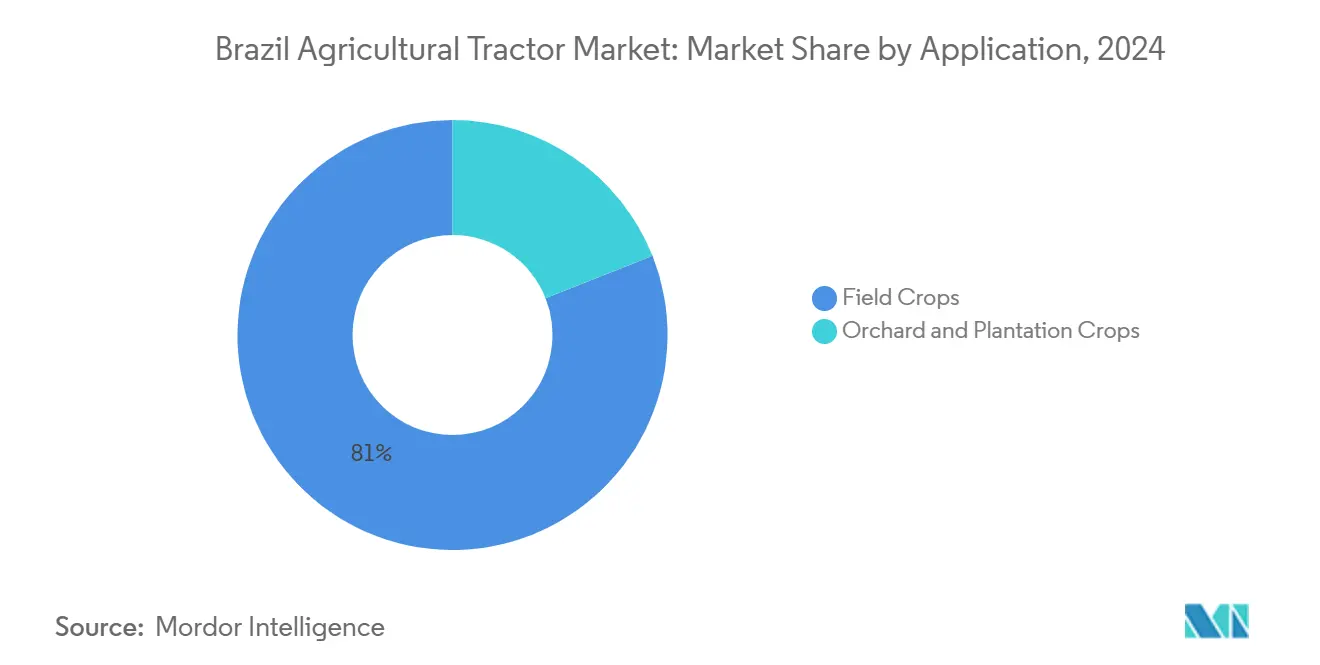

- By application, field-crops accounted for 81% of the Brazil agricultural tractors market size in 2024, while orchard and plantation crops are expanding at a 6.8% CAGR through 2030.

Brazil Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Advancements in Powertrain and Precision Steering | +1.20% | Center-West and Southeast | Medium term (2-4 years) |

| Rising Shortage of Agricultural Labor | +0.80% | National, acute in São Paulo and Goiás | Short term (≤ 2 years) |

| Expansion of Government Subsidized Credit Lines | +0.70% | National, higher in family-farming belts | Short term (≤ 2 years) |

| Digitization of Agribusiness Value-chains | +0.60% | Center-West and Southeast, moving Northeast | Medium term (2-4 years) |

| Biofuel-driven Demand for Sugarcane Mechanization | +0.50% | São Paulo, Goiás, Minas Gerais | Long term (≥ 4 years) |

| OEM–fintech Collaborations Easing Retail Financing | +0.40% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Powertrain and Precision Steering

Innovations in powertrain and precision steering systems are improving fuel economy and field precision. Companies are developing AI-enabled tractors for diverse crop environments. The adoption of continuously variable transmissions is increasing, particularly in higher-powered models. Agricultural groups are implementing private connectivity networks to optimize fleet operations and reduce per-ton costs. Farmers are increasingly using georeferenced soil sampling and mobile applications for operations management, indicating a transition to data-driven agriculture.

Rising Shortage of Agricultural Labor

Mechanized harvesting is becoming prevalent as younger generations shift toward technology-oriented farming roles. The agricultural workforce is aging, and manual labor availability is decreasing. Large-scale farms now use GPS-guided tractor that enables single operators to manage multiple units simultaneously, which reduces labor requirements during harvest periods and increases operational efficiency. The labor shortage is accelerating automation adoption and digital tool implementation, transforming workforce patterns.

Expansion of Government Subsidized Credit Lines

Government-backed credit programs are expanding to facilitate tractor purchases, particularly for small and medium-sized farms.[2]Ministério da Agricultura e Pecuária, “Governo Federal lança Plano Safra 2025/2026 com R$ 516,2 bilhões para impulsionar o agro brasileiro,” GOV.BR Higher limits on subsidized loans are improving access to financing for compact and mid-range equipment. Financial programs are essential for mechanization in rural areas with limited capital access. Affordable credit availability is driving agricultural modernization and equipment upgrades.

Digitization of Agribusiness Value-chains

Digital technologies are becoming essential in farm management, with most producers utilizing digital tools. Mobile networks are expanding across agricultural regions, enabling real-time data access and remote monitoring. Agritech startups are developing AI-powered scheduling and analytics platforms to optimize planting and harvesting cycles. IoT device integration has demonstrated yield improvements in pilot programs. Digital transformation is increasing productivity, reducing waste, and creating service-based revenue opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retail Price and Associated Cost | -1.10% | National | Short term (≤ 2 years) |

| Fragmented Land Holdings Limiting Horsepower Migration | -0.80% | Northeast, North | Long term (≥ 4 years) |

| Data-privacy and Cyber-security Apprehensions | -0.40% | Large commercial farms | Medium term (2-4 years) |

| Slow Rural 5G Rollout Constraining Telematics ROI | -0.60% | Remote belts nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retail Price and Associated Cost

Equipment and land costs have increased substantially, impeding new tractor investments. Farmers are delaying purchases or seeking used equipment, resulting in decreased market transactions. These constraints are reducing demand and slowing mechanization adoption. The market remains vulnerable to macroeconomic changes, with cost being a primary adoption barrier.

Fragmented Land Holdings Limiting Horsepower Migration

Small family farms constitute the majority but control minimal farmland, restricting high-horsepower tractor deployment. Small plot sizes and reduced annual usage hours complicate larger equipment investment justification. Many regional farm sizes cannot accommodate advanced heavy-weight tractor. This fragmentation reduces efficiency and impedes mechanized operations. The uptake of powerful tractors remains inconsistent across rural areas without land consolidation or equipment sharing systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Power: Compact Traction Dominates yet High-power Demand Accelerates

The below 80 HP agricultural tractors represented 47% of the Brazil agricultural tractors market share in 2024, supported by credit programs for small-scale farms. Mid-range tractors (81-130 HP) serve mixed grain operations, providing optimal torque and fuel efficiency for double-cropping systems. Tractors above 130 HP show the highest growth at 7.5% CAGR, driven by large farms expanding tillage operations and sugarcane operations requiring high-drawbar models. Advanced transmissions and modular platforms support this market evolution across different farm sizes.

Regional patterns reflect this segmentation. The Center-West's year-round cropping cycles require powerful machines. The South and Northeast regions prefer compact units due to smaller landholdings and diverse fruit crops. Manufacturers maintain competitiveness through local component and engine production to minimize currency risk. While high-horsepower demand increases, compact models remain significant as credit accessibility and land consolidation progress gradually.

By Application: Field Crops Lead while Orchard Units Gain Pace

Field-crop tractors represent 81% of the 2024 market share, primarily serving soybean and corn cultivation.[3]National Supply Company, “Grain Production 2024-2025,” NATIONALSUPPLYCOMPANY.GOV.BR These units emphasize precision guidance systems and compatibility with large planting equipment. Sugarcane operations contribute to demand through modified field-crop chassis. The orchard and plantation segment, though smaller, grows at 6.8% annually as citrus and coffee producers upgrade their equipment.

Each application requires specific design features. Orchard tractors need narrow frames and low profiles for row navigation, while field-crop models require wider bases for soil stability. Manufacturers use modular designs to accommodate various terrain requirements. Double-cropping practices increase field-crop tractor turnover rates, maintaining consistent replacement cycles and equipment demand.

Geography Analysis

The Center-West region, comprising Mato Grosso, Goiás, Mato Grosso do Sul, and the Federal District, dominates Brazil's agricultural tractor market through extensive grain cultivation and intensive machine utilization. Farmers in this region opt for high-horsepower tractors equipped with precision technologies for managing soybean, corn, and cotton rotations. Strategic dealer locations in Cuiabá and Goiânia provide efficient access to parts and services, reducing operational downtime during critical seasons. The region's level terrain and extensive farm areas support advanced tractor deployment and continuous mechanized operations.

In the Southeast, São Paulo and Minas Gerais demonstrate consistent demand for CVT tractors with smart features, primarily from sugarcane mills and fruit estates. The region includes significant manufacturing facilities, such as Massey Ferguson's plant in Canoas, Rio Grande do Sul. In the Southern states of Paraná and Santa Catarina, mid-range tractors serve mixed farming operations, including dairy, tobacco, and cereal production across diverse topography. High market penetration persists despite smaller land holdings and varied crop patterns, supported by cooperative purchasing programs and dealer financing options.

The Northeast and North regions, including Bahia, Pernambuco, Maranhão, Pará, Amazonas, and Tocantins, encounter obstacles in land distribution and rural infrastructure development. Bahia and Pernambuco's agricultural sectors utilize compact tractors for fruit and vegetable production, while Pará and Amazonas contend with transportation and logistical limitations. The expansion of mobile service centers and 4G networks increases market potential, particularly in Tocantins and Maranhão. The prevalence of small agricultural plots and limited mechanization indicates that tractors below 80 HP will continue to dominate these regions.

Competitive Landscape

The Brazil agricultural tractor market share is moderately concentrated, with Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra Limited holding significant market share. These manufacturers differentiate themselves by integrating advanced technologies, including smart connectivity, predictive maintenance, and autonomous features, to improve operational efficiency. These technological advancements address farmers' requirements for efficient and reliable tractors.

Manufacturers are establishing remanufacturing facilities across Brazil to reduce ownership costs and extend equipment lifecycles. They are also forming partnerships with financial institutions and fintech platforms to transform traditional sales models. These partnerships provide faster credit access and embedded financing options, making advanced tractors more accessible to small and medium-scale farmers. Due to anticipated stricter local content regulations, manufacturers are increasing domestic sourcing of components, including engines and electronics, to ensure compliance and reduce import dependency.

Companies are expanding their offerings beyond equipment to include data-driven agronomic support and retrofit solutions for existing fleets. Their growth strategies focus on new product launches, strategic alliances, and acquisitions. Research and development investments and innovative product development will shape market dynamics in the coming years. Global manufacturers are partnering with domestic firms to expand distribution networks and develop tractors that meet the specific needs of Brazilian farmers.

Brazil Agricultural Tractor Industry Leaders

AGCO Corporation

Deere & Company

CNH Industrial N.V.

Mahindra & Mahindra Limited

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Deere & Company launched an ethanol-powered 8R tractor prototype at Agrishow 2025, designed to reduce emissions while maintaining performance for Brazilian agricultural operations. The tractor features a software-calibrated engine and is currently undergoing field testing in sugarcane and grain farms, utilizing Brazil's established ethanol infrastructure.

- April 2025: At Agrishow 2025 in Brazil, CNH Industrial's New Holland unveiled more than 15 new products, showcasing its latest agricultural tractor innovations. The exhibition featured updated T8, T7, and T5 tractor models designed to meet diverse farming requirements.

Brazil Agricultural Tractor Market Report Scope

| Less than 80 HP |

| 81-130 HP |

| Above 130 HP |

| Field Crops |

| Orchard and Plantation Crops |

| By Engine Power | Less than 80 HP |

| 81-130 HP | |

| Above 130 HP | |

| By Application | Field Crops |

| Orchard and Plantation Crops |

Key Questions Answered in the Report

How large is the Brazil agricultural tractors market in 2025?

The market is valued at USD 3.6 billion in 2025 and is projected to reach USD 4.6 billion by 2030.

What is the forecast CAGR for tractor sales in Brazil?

Sales are projected to expand at a 5.02% CAGR between 2025 and 2030.

Which engine-power segment is growing fastest?

Tractors above 130 HP are growing quickest at 7.5% CAGR due to large-scale grain and sugarcane expansion.

How big is the field-crop application share?

Field-crop tractors account for 81% of 2024 revenue, mirroring Brazil's dominance in soybean and corn.

Page last updated on: