Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

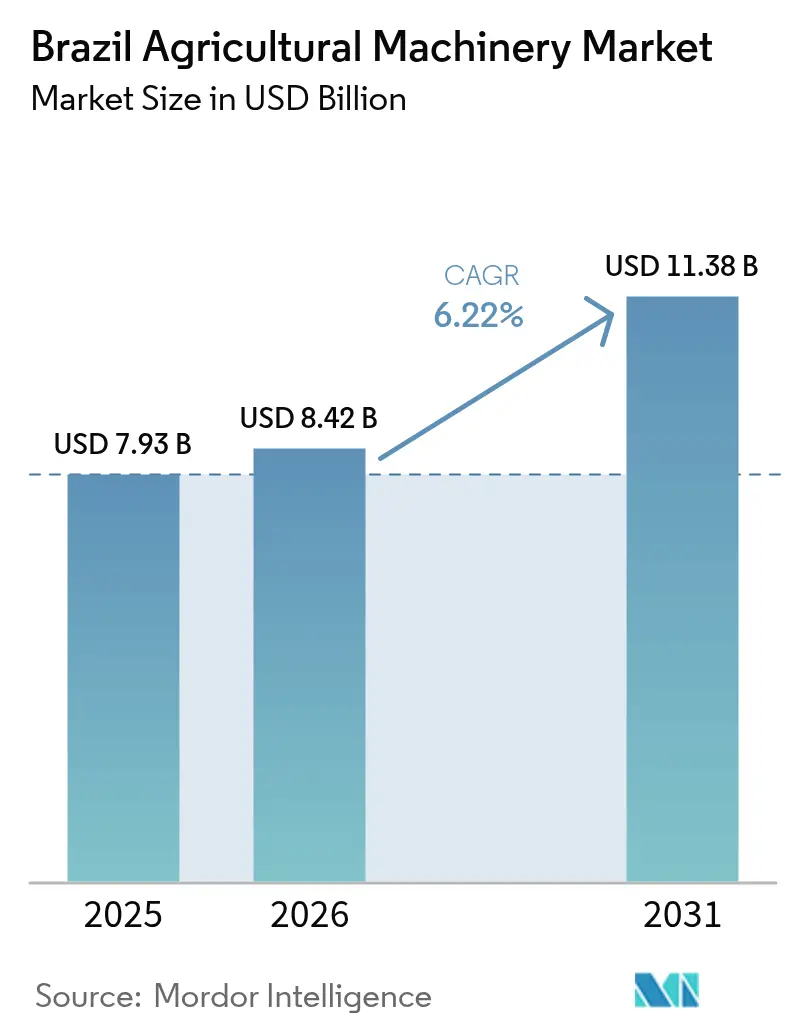

| Base Year Market Size (2025) | USD 7.93 Billion |

| Market Size (2026) | USD 8.42 Billion |

| Market Size (2031) | USD 11.38 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

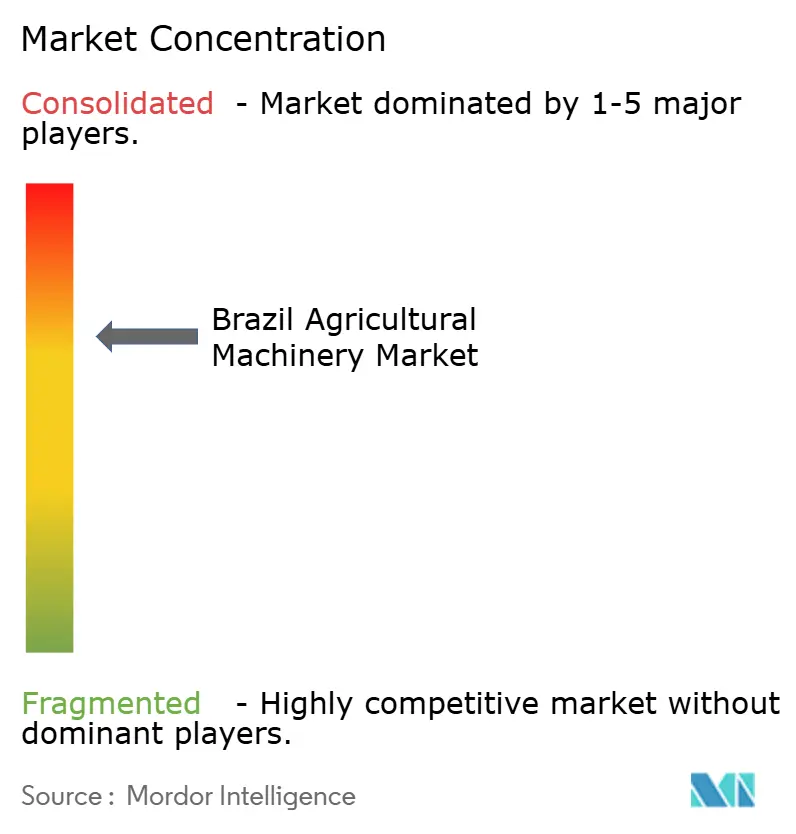

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Agricultural Machinery Market Analysis by Mordor Intelligence

The Brazil agricultural machinery market size is expected to grow from USD 7.93 billion in 2025 to USD 8.42 billion in 2026 and is forecast to reach USD 11.38 billion by 2031 at 6.22% CAGR over 2026-2031. Continued expansion of large-scale soybean, corn, and sugarcane farms, wider access to subsidized credit, and rapid diffusion of precision farming tools are the core engines propelling the Brazil agricultural machinery market. Demand remains resilient even in a high-interest-rate environment because government programs channel low-cost funds toward machinery upgrades, and OEM (Original Equipment Manufacturer) service bundles cut operating costs through predictive maintenance. Farm consolidation in the Center-West supports steady replacement cycles for tractors and harvesters, while frontier regions such as Matopiba (a region formed by parts of Tocantins, Maranhao, Piaui, and Bahia states) fuel first-time purchases of irrigation and spraying systems. At the same time, carbon-credit incentives and sustainability mandates expand the addressable base for fuel-efficient models that lower emissions and capture additional income streams for growers.

Key Report Takeaways

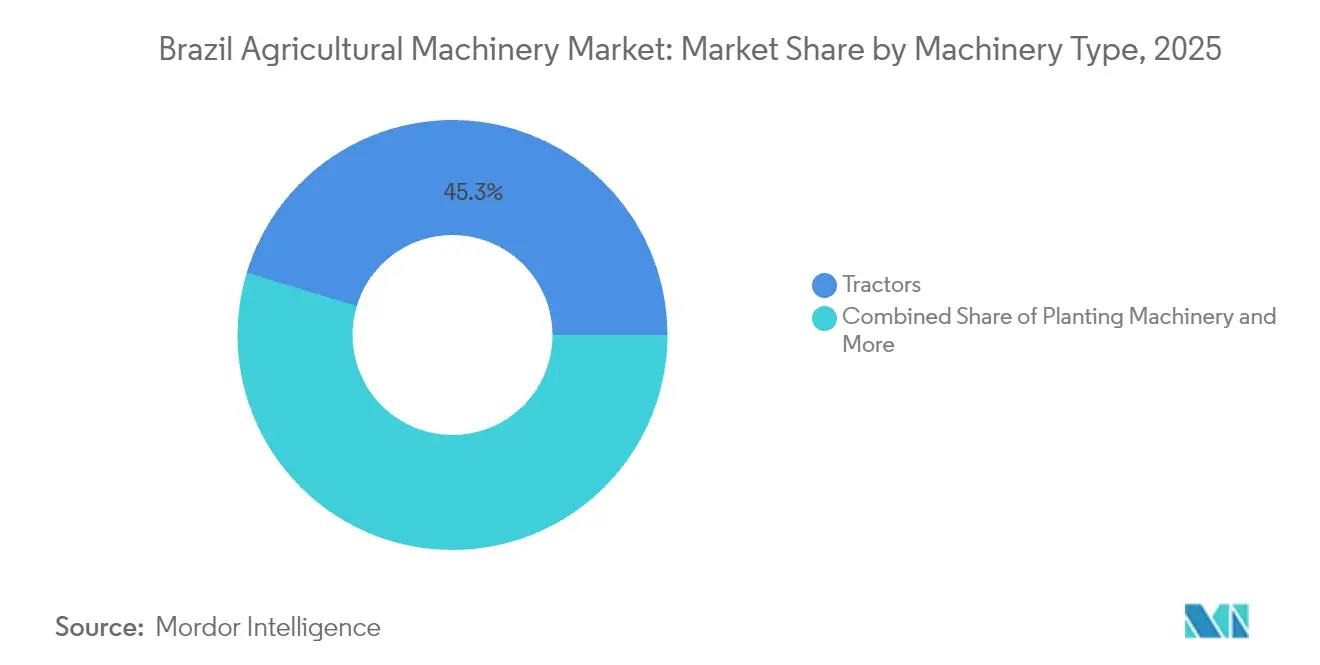

- By machinery type, tractors commanded 45.32% of Brazil agricultural machinery market share in 2025, while hay and forage machinery is projected to expand at a 5.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Mechanized-Harvest Mandates | +1.2% | São Paulo, Minas Gerais, Goiás | Medium term (2-4 years) |

| Digital-ag Credit from Government Policies | +0.9% | National, Center-West focus | Short term (≤2 years) |

| Expansion of Center-Pivot Financing via Banks | +0.8% | Mato Grosso, Goiás, Bahia | Medium term (2-4 years) |

| OEM Telematics-as-a-Service Bundles | +0.7% | National, large farms early | Long term (≥4 years) |

| Carbon-Credit Premiums for Tractors | +0.5% | Amazon basin, Cerrado fringe | Long term (≥4 years) |

| Satellite-Enabled Ag-IoT Expansion in Frontier Ecosystems | +0.6% | MATOPIBA, North | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-ag Credit from Government Policies

Plano Safra 2025/26 released BRL 516.2 billion (USD 93.9 billion) in rural credit, with lines priced at 2.5% for machinery up to BRL 100,000 (USD 18,200) and 5% up to BRL 250,000 (USD 45,500). Embedded fintech processes accelerate loan approval, enabling mid-sized growers to transition from cash purchases to structured financing. BNDES (The Brazilian Economic and Social Development Bank) added BRL 70 billion (USD 12.8 billion) solely for tech-enabled equipment bundles, linking funding to precision-ag Key Performance Indicators.[1]Banco Nacional de Desenvolvimento Econômico e Social, “Plano Safra 2025/26 Credit Lines,” bndes.gov.br Newly issued digital grain receipts (CPRs) are now accepted as collateral, broadening credit access for tenant farmers.

Expansion of Center-Pivot Financing via Banks

Center-pivot counts in Mato Grosso leapt 226% in one year as lenders lengthened amortization to eight harvest cycles. Lindsay Corporation’s Smart Pivot trials confirmed 15% yield lifts and 27% water savings, validating the returns that underpin those loan products.[2]Lindsay Corporation, “Smart Pivot Performance in Brazil,” lindsay.com Insurers now bundle rainfall-index coverage with irrigation loans, trimming default risk tied to drought. Equipment dealers respond by stocking modular spans that can be expanded when growers refinance.

OEM Telematics-as-a-Service Bundles

Deere & Company’s SpaceX satellite link lets machines stream diagnostics from frontier fields, and AGCO’s PTx Trimble stack pushes remote software updates. Subscription pricing converts capital outlays into predictable opex, cushioning growers against commodity swings. Predictive maintenance has cut unplanned downtime by 18% on early adopter fleets, validating the pay-as-you-go model. Deere & Company recently added agronomic prescription services to the same package, turning telematics into a full decision-support platform.

Carbon-Credit Premiums for Tractors

Law 15.042 lets farms monetize fuel-efficient tractor upgrades, and Petrobras pledged BRL 450 million (USD 81.8 million) for forest-linked offsets. Tier 4-final engines documented through onboard telematics qualify for saleable credits that average USD 7 per metric ton. The National Green Mobility Program stacks purchase rebates on top, shrinking payback to under four seasons. Large cereal growers now factor projected carbon revenue into machine TCO (Total Cost of Ownership) calculations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Financing Costs amid Selic Volatility | -1.8% | National, sharpest in Northeast and South | Short term (≤2 years) |

| Grain-Price Downturn Dampening CAPEX | -1.1% | Center-West, Rio Grande do Sul | Medium term (2-4 years) |

| Data-Sovereignty Litigation on Farm Analytics | -0.4% | National, large enterprises | Long term (≥4 years) |

| Sub-Scale Farms’ Limited ROI on Automation | -0.7% | Northeast, family farms | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Financing Costs Amid Selic Volatility

The Selic climbed from 10.5% to 13.25% in early 2025, driving commercial equipment loans above 20%. Bank data show a 30% drop in non-subsidized applications, with mid-size growers delaying combine replacements. Currency swings inflate imported parts costs, further eroding purchasing power. Some OEMs now offer factory-backed rate buy-downs to keep volumes moving.

Data-Sovereignty Litigation on Farm Analytics

Court challenges over cross-border data flows raise compliance costs for cloud telematics. OEMs must invest in local servers and legal audits, adding up to 8% to subscription fees. Large growers hesitate to share operational data with foreign platforms until rules stabilize.[3] Brazilian Government, “Data Sovereignty and LGPD Compliance in Agriculture,” gov.br Industry groups now lobby for a sector-specific data framework to unlock adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Dominance of Tractors and Upswing in Forage Equipment

Tractors accounted for 45.32% of Brazil agricultural machinery market share in 2025, underscoring their position as the primary power source across grain, sugarcane, and mixed-farming operations. Their broad utility makes them the anchor of fleet-renewal cycles, and steady replacement demand in the Center-West keeps this segment the largest contributor to Brazil agricultural machinery market size. Harvesting and spraying equipment follow in value as growers pair combines and self-propelled sprayers with precision guidance to protect yield and curb input waste. Irrigation systems post double-digit value gains in frontier regions, yet their absolute share remains smaller because high upfront costs limit initial adoption outside Mato Grosso and Goiás.

Hay and forage machinery is the fastest-growing category, advancing at a 5.82% CAGR through 2031 as integrated crop-livestock systems widen across the Cerrado and South. Growth in planting and cultivation equipment stays linked to conservation tillage practices that require lighter, residue-friendly implements rather than deep inversion tools. Demand for planting, harvesting, and spraying machinery also benefits from bundled telematics that convert capital purchases into data-driven productivity gains. Together, these trends reinforce a balanced expansion pattern in which tractors retain scale leadership while hay and forage equipment captures the momentum edge within the Brazil agricultural machinery market.

Geography Analysis

Equipment demand clusters in the Center-West, where Mato Grosso alone accounts for more than one-third of Brazil agricultural machinery market value. Mega-farms averaging 3,400 hectares generate ample cash flow for successive upgrades to high-horsepower tractors, GPS combines, and variable-rate pivots. Logistics corridors to export ports have improved, helping dealers manage parts inventories and field service over vast distances. Financing penetration is deepest here because balance sheets accommodate structured debt, reinforcing a virtuous cycle of technology adoption.

The South ranks second in value, yet differs in structure. Average holdings of around 62 hectares rely on cooperatives to negotiate discounts and share high-ticket equipment. Tractor demand tilts toward sub-130 HP models that suit mixed cropping and livestock. Rice farms in Rio Grande do Sul use crawler tractors and specialized threshers, reflecting agro-climatic needs distinct from Cerrado grain belts. Cooperative financing and group maintenance arrangements stabilize sales volumes, maintaining the South’s reliable share within Brazil agricultural machinery market.

The Southeast specializes in sugarcane and specialty crops, making it the epicenter for cane harvesters and self-propelled sprayers with narrow wheel tracks. São Paulo’s mechanization mandate keeps harvester replacement rates brisk, while Minas Gerais coffee estates invest in drip irrigation and small-frame sprayers. Further Matopiba (a region formed by parts of Tocantins, Maranhão, Piauí, and Bahia states) and parts of Pará emerge as frontier zones where irrigation and land clearing equipment comprise the bulk of first-cycle orders. Growth rates here exceed national averages, but infrastructure gaps and credit access still cap absolute volumes.

Competitive Landscape

The Brazil agricultural machinery market remains moderately concentrated. Deere & Company leads, leveraging the country’s most extensive dealer network, a captive finance arm, and satellite-enabled Operations Center software that unifies fleet data. CNH Industrial N.V. follows, combining Case IH and New Holland Agriculture product ranges and a Sorocaba combine plant that supplies the entire Southern Cone. AGCO Corporation gains a technology edge through its PTx Trimble joint venture. Kubota Corporation and Mahindra & Mahindra Ltd round out the top group, focusing on mid-horsepower tractors and expanding parts logistics in the South.

Localization strategies dominate. Deere & Company, AGCO Corporation, and CNH Industrial N.V. all operate foundries and transmission lines inside Brazil, insulating cost structures from exchange-rate swings and qualifying for domestic-content credit incentives. Technology partnerships intensify AGCO Corporation and Trimble Inc.’s precision stack, complement Deere & Company’s in-house systems, while CNH Industrial N.V. integrates Raven Applied Technology guidance across Case IH and New Holland Agriculture brands.

Financing solutions differentiate competitors as much as horsepower or boom width. Deere Financial, CNH Industrial Capital, and AGCO Finance tailor seasonal lines tied to crop calendars, absorbing some rate risk away from growers during volatile Selic cycles. This captive approach stabilizes unit sales even in bearish commodity years. Consequently, the competitive arena hinges on who couples machinery, data services, and funding into the most farmer-friendly bundle, a dynamic that will define Brazil agricultural machinery market evolution over the next decade.

Brazil Agricultural Machinery Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Mahindra & Mahindra Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Deere & Company and Banco Bradesco established a 50:50 joint venture to improve financing services in Brazil. The partnership aims to enhance access to equipment, parts, and subscription-based solutions. The collaboration expands John Deere's financial presence in Brazil's agricultural and construction sectors by providing competitive and technology-enabled financing options for customers and dealers.

- May 2024: CNH Industrial N.V.'s Case IH introduced the Axial-Flow Series 160 Automation harvesters, manufactured at its Sorocaba facility in São Paulo, Brazil.

Brazil Agricultural Machinery Market Report Scope

Machines used for agricultural activities, such as planting, seeding, fertilizing, pest control, irrigation, harvesting, and haymaking, and post-harvest activities, including loading, unloading, and storage, are considered agricultural machinery.

The Brazilian agricultural machinery market is segmented by tractor (below 80 HP, 81 to 130 HP, and above 130 HP), ploughing and cultivating machinery (ploughs, harrows, cultivators and tillers, and other ploughing and cultivating machinery), planting machinery (seed drills, planters, spreaders, and other planting machinery), harvesting machinery (combine harvesters, forage harvesters, and other harvesting machinery), haying and forage machinery (mowers, balers, and other haying and forage machinery), and irrigation machinery (sprinkler irrigation, drip irrigation, and other irrigation machinery). The report offers market sizes in terms of value (USD) for all the abovementioned segments.

By Machinery Type

| Tractors | Below 80 HP |

| 81 to 130 HP | |

| Above 130 HP | |

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Cultivators and Tillers | |

| Other Plowing and Cultivating Machinery (Subsoilers, Ridgers, etc.) | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery (Transplanters, Precision Seeders, etc.) | |

| Harvesting Machinery | Combine Harvesters |

| Sugarcane Harvesters | |

| Forage Harvesters | |

| Other Harvesting Machinery (Beet Harvesters, Potato Harvesters, etc.) | |

| Hay and Forage Machinery | Mowers |

| Balers | |

| Other Haying and Forage Machinery (Rakes, Tedders, etc.) | |

| Irrigation Machinery | Center-Pivot Irrigation |

| Sprinkler Irrigation | |

| Drip Irrigation | |

| Other Irrigation Machinery (Micro-Sprinklers, Flood/Furrow Systems, etc.) | |

| Spraying Machinery | Self-Propelled Sprayers |

| Tractor-Mounted Sprayers | |

| Aerial Drone Sprayers |

| By Machinery Type | Tractors | Below 80 HP |

| 81 to 130 HP | ||

| Above 130 HP | ||

| Plowing and Cultivating Machinery | Plows | |

| Harrows | ||

| Cultivators and Tillers | ||

| Other Plowing and Cultivating Machinery (Subsoilers, Ridgers, etc.) | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery (Transplanters, Precision Seeders, etc.) | ||

| Harvesting Machinery | Combine Harvesters | |

| Sugarcane Harvesters | ||

| Forage Harvesters | ||

| Other Harvesting Machinery (Beet Harvesters, Potato Harvesters, etc.) | ||

| Hay and Forage Machinery | Mowers | |

| Balers | ||

| Other Haying and Forage Machinery (Rakes, Tedders, etc.) | ||

| Irrigation Machinery | Center-Pivot Irrigation | |

| Sprinkler Irrigation | ||

| Drip Irrigation | ||

| Other Irrigation Machinery (Micro-Sprinklers, Flood/Furrow Systems, etc.) | ||

| Spraying Machinery | Self-Propelled Sprayers | |

| Tractor-Mounted Sprayers | ||

| Aerial Drone Sprayers | ||

Key Questions Answered in the Report

How large is the Brazil agricultural machinery market in 2026?

The Brazil agricultural machinery market size is USD 8.42 billion in 2026 and is projected to reach USD 11.38 billion by 2031.

What is the projected growth rate for Brazilian farm equipment through 2031?

The market is forecast to expand at a 6.22% CAGR between 2026 and 2031.

Which machinery type leads sales today?

Tractors hold 45.32% of Brazil agricultural machinery market share, making them the dominant category.

Which segment is growing the fastest?

Hay and forage equipment posts the highest 5.82% CAGR through 2031 due to livestock intensification.

Page last updated on: