Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.40 Billion |

| Market Size (2026) | USD 29.74 Billion |

| Market Size (2031) | USD 37.45 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil 3PL Market Analysis by Mordor Intelligence

The Brazil 3PL market size is expected to grow from USD 28.40 billion in 2025 to USD 29.74 billion in 2026 and is forecast to reach USD 37.45 billion by 2031 at 4.72% CAGR over 2026-2031. Expansion is unfolding even as logistics expenses absorb 12.3% of national GDP—far above developed-market norms—because shippers are turning to multimodal corridors, asset-light orchestration, and warehouse automation to trim waste and improve visibility. Private-equity inflows into Grade-A logistics parks, completion of the North–South Railroad, and fast-growing cold-chain demand are reshaping competitive dynamics. E-commerce volumes from tier-2 cities, ESG-driven procurement mandates, and hybrid logistics models that combine owned and partner fleets are widening the service scope of leading providers. Taken together, these forces are repositioning the Brazil 3PL market as a platform for nationwide fulfillment rather than a patchwork of regional distribution hubs.

Key Report Takeaways

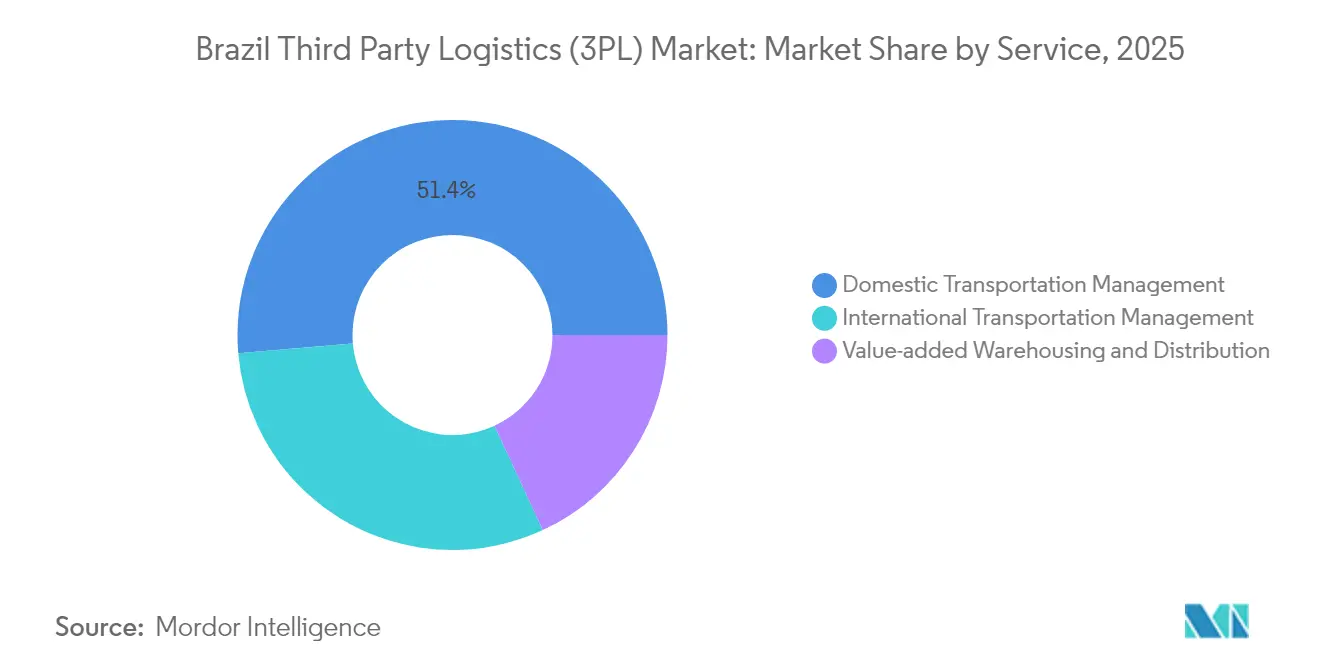

- By service, Domestic Transportation Management led with 51.35% share of the Brazil 3PL market size in 2025, while Value-added Warehousing & Distribution is forecast to expand at a 7.18% CAGR to 2031.

- By geography, the Southeast captured 46.55% of the Brazil 3PL market share in 2025; the North region is projected to grow at a 5.74% CAGR through 2031.

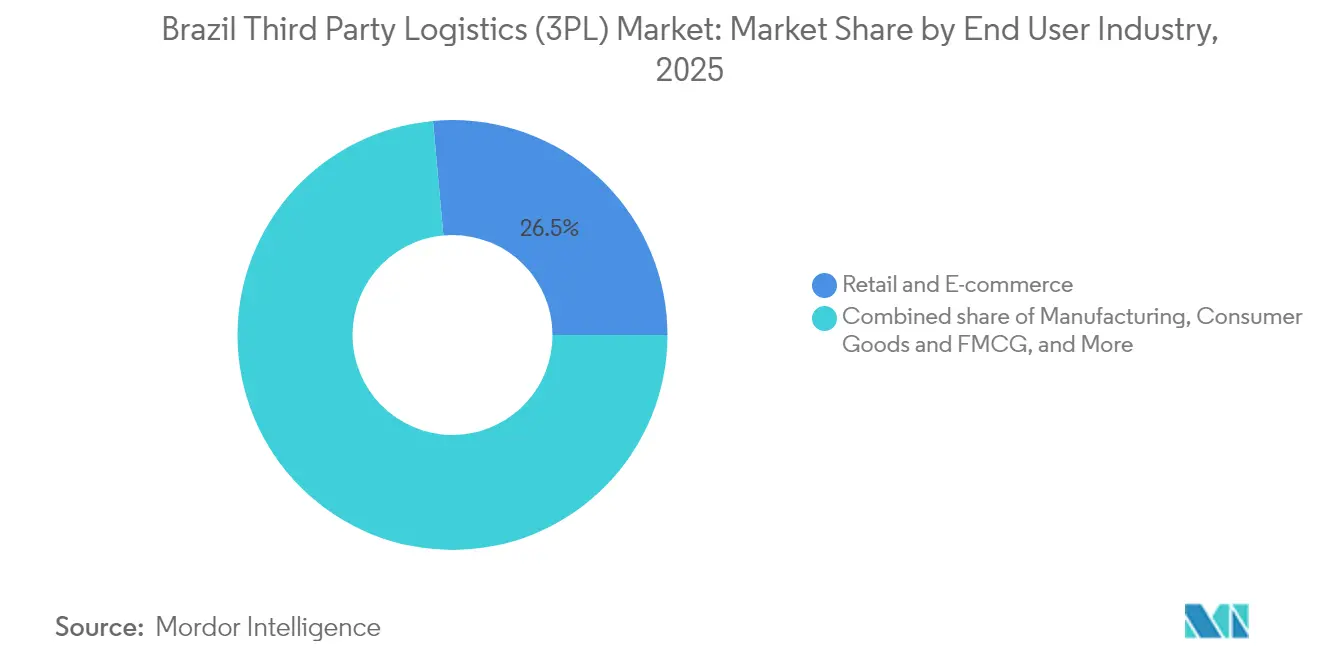

- By end-user industry, Retail & E-commerce commanded 26.45% share of the Brazil 3PL market size in 2025; Life Sciences & Healthcare is advancing at a 8.75% CAGR between 2026-2031.

- By logistics model, Asset-Light operations held 47.30% of the Brazil 3PL market share in 2025, while Hybrid models are on course for the fastest 6.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce demand in tier-2 cities | +1.8% | National; concentration in Southeast & South | Short term (≤ 2 years) |

| Biologics & vaccine cold-chain uptick | +1.2% | Southeast, South, Northeast | Medium term (3-4 years) |

| Agribusiness grain-export boom | +1.5% | Center-West, North, Northeast | Medium term (3-4 years) |

| Mandatory ESG reporting | +0.9% | Southeast, South | Long term (≥ 5 years) |

| Private-equity-led Grade-A warehouse build-out | +1.6% | Southeast, South | Short term (≤ 2 years) |

| Digital Tax Voucher (DT-e) mandate accelerating 3PL tech adoption | +0.8% | National | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Explosive E-commerce Demand in Tier-2 Cities

Tier-2 urban areas posted the fastest online sales growth worldwide in 2024, pushing fulfillment volumes into regions where modern logistics stock is scarce. Mercado Libre is doubling its Brazilian distribution-center count to 21 by 2025, investing BRL 23 billion to place facilities in Rio Grande do Sul, Brasília, and Pernambuco. These nodes are cutting last-mile costs by up to 50% and lifting same-day delivery reach by 40%, forcing competitors to reassess network footprints[1]Mercado Libre, “Sustainability Report 2024,” mercadolibre.com. New multimodal routes that pair truckload line-haul with regional air uplift are gaining favor because they sidestep congested highways around São Paulo. For the Brazil 3PL market, the surge means tighter warehouse vacancy—forecast to hit 6.8% in 2025, the lowest on record—and rising demand for order-management technology that orchestrates omnichannel flows across scattered inventory pools. Providers able to balance throughput speed with cost discipline are capturing long-term contracts from both domestic and cross-border merchants.

Biologics & Vaccine Cold-Chain Uptick

Life-sciences volumes are growing at 9.2% CAGR as injectable GLP-1 therapies and combination vaccines move deeper into Brazil’s public-health programs. Novo Nordisk is investing BRL 6.4 billion to upgrade its Montes Claros plant, adding capacity that will require validated 2-8 °C transport lanes for nationwide distribution[2]Novo Nordisk, “Novo Nordisk Invests BRL 6.4 Billion in Montes Claros Expansion,” Novo Nordisk, novonordisk.com. Specialty 3PLs are installing IoT-based lane monitoring that meets Anvisa’s Good Distribution Practices, lowering reported product-loss rates tied to temperature excursions that cost the sector BRL 15 billion each year. Start-ups such as Pharmalog integrate real-time thermal dashboards with blockchain audit trails, giving shippers line-item traceability. For the Brazil 3PL market, the cold-chain build-out is expanding the profit pool beyond foodstuffs and inviting consolidation, as regional warehouses retrofit for dual-zone storage to meet higher-margin pharmaceutical requirements.

Agribusiness Grain-Export Boom

Soybean exports climbed to 25.4 million t in Q3 2024 at an average FOB price of USD 434.91 t, anchoring a freight surge from farm belts in Mato Grosso and MATOPIBA. The completed North–South Railroad now links inland grain silos to Northern Arc ports, lowering end-to-end cost by 30% and reducing transit by four days[3]ANEC, “Northern Arc Logistics Corridor Report 2024,” ANEC, anec.com.br. Multimodal 3PLs are leasing block trains and coordinating barges on the Tapajós River to secure capacity during peak harvest, replacing fragmented spot trucking. Clients are locking in multi-year rail allocation, signaling durable volume shifts that elevate the share of non-road ton-miles in the Brazil 3PL market.

Mandatory ESG Reporting

Federal procurement policy (Plano Diretor de Logística Sustentável) now embeds emissions criteria in public-sector tenders, and lenders such as Bradesco have tied BRL 250 billion in credit lines to verified low-carbon supply chains. Corporates respond by outsourcing to 3PLs that operate electric fleets or rail-first routings. Eletrobras already audits 100% of critical carriers on ESG metrics. Mercado Libre increased its Brazilian electric-vehicle fleet by 30% in 2024, trimming urban CO₂ output and enhancing brand equity among eco-conscious shoppers. Integrating Scope 3 analytics platforms has therefore become a qualification hurdle, accelerating digital adoption across the Brazil 3PL market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic truck-driver shortage | −1.2% | National | Medium term (3-4 years) |

| High logistics-cost share for SMEs | −0.8% | North, Northeast, Center-West | Medium term (3-4 years) |

| Cargo-theft hotspots elevating insurance costs | −0.5% | Southeast (São Paulo & Rio de Janeiro) | Short term (≤ 2 years) |

| Port of Santos congestion and 8-day average dwell time | −0.9% | Southeast; nationwide supply-chain implications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Truck-Driver Shortage

Road haulage moves significant share of Brazilian freight but the licensed driver pool is aging, and women hold just 3.4% of heavy-vehicle licenses. Wage inflation has climbed faster than diesel costs, pressing margins for both carrier-owned fleets and 3PL subcontractors. Programs such as IVECO’s “Caminhos para Elas” placed 60% of female trainees into trucking roles in its first year, yet structural gaps persist. Autonomous-vehicle trials in São Paulo hint at long-run relief, but regulatory and infrastructure adoption will take the decade. In the interim, the shortage nudges shippers toward rail and short-sea alternatives, limiting road-based capacity available to the Brazil 3PL market during seasonal peaks.

High Logistics-Cost Share for SMEs

For small manufacturers, logistics expenses can exceed 25% of product value because fragmented carrier networks, multilayer taxes, and limited bargaining power inflate door-to-door rates. Research shows that repositioning inventories to tax-advantaged states trims landed cost, yet SMEs often lack data to optimize hubs. 3PLs offering shared warehousing and multi-shipper milk-runs are capturing this underserved tier. Without scale-efficient solutions, SME competitiveness erodes, tempering e-commerce expansion and capping growth potential for the broader Brazil 3PL market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Warehousing Rewrites Fulfillment Economics

Domestic Transportation Management captured 51.35% of 2025 revenue, anchored in a road network that still carries 58% of national tonnage. That dominance ensures stable baseline volumes for the Brazil 3PL market, but mounting driver shortages and corridor congestion are encouraging modal diversification. Value-added Warehousing & Distribution (VAWD) is advancing at a 7.18% CAGR, propelled by omnichannel retailers requesting inventory postponement, pick-and-pack, and reverse-logistics services within the same node. Mercado Libre targets 2 million m² of warehousing by 2025, illustrating the upmarket shift toward automated fulfillment centers with mezzanine robotics and micro-sortation. Providers that marry real-time stock visibility with distributed inventory placement are securing premium margins. The Brazil 3PL market size for VAWD sub-services is projected to increase in double digits as e-commerce and healthcare shippers outsource non-core activities.

In parallel, International Transportation Management gains leverage from new corridors like the North-South Railroad, enabling bundled rail-truck-port solutions that slash grain export costs. Airfreight retains a niche for high-value pharmaceuticals and electronics, with 3PLs integrating temperature-controlled ULDs and API-driven booking engines. As service complexity rises, shippers gravitate toward partners that provide unified dashboards across transport and warehousing, further consolidating the Brazil 3PL market.

By End-User Industry: Healthcare Challenges Retail Primacy

Retail & E-commerce accounted for 26.45% of Brazil's 3PL market revenue in 2025 on the back of 16% online sales expansion. Last-mile innovation, including drone-ready micro hubs and community-based drop-off points in favelas, enables parcel density that sustains the same-day service levels outside tier-1 metros. Yet Life Sciences & Healthcare, growing at 8.75% CAGR, is narrowing the gap thanks to vaccine and biologics volumes that command premium rates. Cold-chain upgrades, lane qualification, and GDP compliance generate new revenue lines, lifting the Brazil 3PL market size for temperature-controlled services. Automotive, Energy, and FMCG remain sizable contributors, but healthcare’s capital intensity and regulatory oversight raise switching barriers, locking in multi-year contracts. Providers that layer serialization, returns compliance, and customs brokerage under one SLA are best positioned to outpace baseline sector growth.

By Logistics Model: Hybrid Platforms Gain Momentum

Asset-Light operations delivered 47.30% of Brazil's 3PL market revenue in 2025, valued for scalability and minimal capex. However, the fastest 6.42% CAGR belongs to Hybrid models that selectively own cross-docks, trucks, or railcars while contracting less strategic legs. This structure provides resilience against subcontractor bottlenecks and supports ESG reporting with verified emissions data. The Brazil 3PL market share for Hybrid operations is climbing as large shippers seek guaranteed capacity during peak harvest or shopping seasons. Asset-heavy models persist in hazardous-materials transport and bulk liquids, where dedicated fleets mitigate compliance risk. Across models, the common thread is orchestration technology: control-tower platforms that integrate TMS, WMS, and IoT telemetry into a single decision stack, giving shippers end-to-end visibility.

Geography Analysis

The Southeast remains the fulcrum of the Brazil 3PL market, holding 46.55% of 2025 revenue on the strength of São Paulo’s industrial clusters and Santos’ deep-sea connectivity. Yet, chronic port congestion and under-funded highways cost exporters revenue, illustrated by 637,767 bags of coffee that missed March 2025 shipment windows, forfeiting USD 1.568 million of potential earnings. Infrastructure shortfalls make modal agility, rail, cabotage, cross-docking, an imperative for 3PLs operating in the region.

The North region represents the smallest base but posts the swiftest 5.74% CAGR to 2031 as grain corridors pivot to Northern Arc ports. These terminals handled 52.3 million tons of soy and corn in 2024, 47.4% of national corn exports. Still, only 41% of paved roads are in good condition, and river draft restrictions tied to climate change threaten dry-season capacity. 3PLs hedge by combining rail legs on Estrada de Ferro Carajás with barge fleets outfitted with shallow-draft pontoons, preserving schedule reliability during low-water months.

Center-West territories, led by Mato Grosso, are the locus of Brazil’s soybean expansion, adding 5.4 million hectares of planted area since 2017. The National Logistics Plan (PNL2035) aims to grow rail coverage by 91%, promising 10-23% freight savings once dedicated grain aisles reach interiors. 3PLs pre-leasing track slots and building integrated transload yards are staking early claims on volumes expected to surge as 70 million acres of degraded pasture convert to cropland.

The Northeast secures multilateral funding to counterbalance under-developed infrastructure. A USD 150 million World Bank loan to Bahia rides alongside a USD 200 million sustainable-infrastructure program targeting road and energy upgrades. MATOPIBA’s soybean area grew from 4.1 million to 5.8 million ha in seven years, intensifying demand for rail-road-port chains that bypass clogged coastal highways. 3PLs with local warehousing footprints and customs-brokerage capabilities can accelerate cycle times to export markets.

Competitive Landscape

Competition in the Brazil 3PL market is intensifying as global forwarders buy local specialists while domestic players modernize warehouse portfolios. The September 2024 agreement by CMA CGM to acquire 48% of Santos Brasil for USD 1.13 billion marks a pivot toward vertical integration of terminal assets with inland logistics. Scan Global Logistics followed by taking over Blu Logistics Brasil, adding BRL 570 million in 2023 revenue and a robust ocean freight book. Consolidators pursue scale to negotiate ocean contracts, secure port berths, and feed rail networks, squeezing smaller operators that lack capital for tech upgrades or green fleets.

Niche entrants are carving out defensible positions. Favela Brasil Xpress delivers 4,000 parcels daily to informal neighborhoods, pairing crowdsourced delivery personnel with AI routing to cut failed-delivery rates. Estoca operates omnichannel nodes powered by proprietary WMS, promising 20% logistics cost cuts for mid-market merchants. Cold-chain heavyweights such as Emergent Cold Latin America command a combined 157 million ft³ of capacity, enabling national coverage for pharmaceutical and frozen-food clients. Technology adoption is the great equalizer: digitized supply chains raise profit margins by 40% and slash logistics expenses by 50% for early movers.

Strategic investments focus on clean-energy fleets and network density. Vibra Energia operates 10,000 drivers and 8,000 contracted trucks, rolling out electric tankers to lower Scope 1 emissions. Ultracargo’s 50% stake in ethanol-terminal operator Opla extends bulk-liquid storage into multimodal distribution. Within this mosaic, leading 3PLs converge on platform models that blend asset ownership with brokerage scale, reinforcing the hybrid trend mapped earlier.

Brazil 3PL Industry Leaders

DHL Supply Chain (Deutsche Post AG)

A.P. Moller - Maersk Logistics & Services

BBM Logística SA

JSL SA

CEVA Logistics AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novo Nordisk committed BRL 6.4 billion to expand its Montes Claros site, creating 600 logistics-reliant jobs.

- February 2025: The Ministry of Transport unveiled a logistics-cost-reduction plan targeting a 40% drop in food-haulage expenses via improved roads and waterway concessions.

- February 2025: Eletrobras launched a Supplier ESG Program that monitors 100% of critical carriers for sustainability compliance.

- January 2025: Brazil enacted Complementary Law 214/2025, implementing a dual IBS-CBS consumption tax regime effective Jan 2026, compelling 3PLs to overhaul tax-planning engines.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Brazil third-party logistics market as every paid, multi-client service that handles domestic or cross-border transportation, value-added warehousing, or end-to-end orchestration on behalf of shippers across industries. According to Mordor Intelligence, revenues earned by asset-light managers and asset-based contractors are both captured, provided the 3PL controls the freight or inventory flow.

Scope exclusion: In-house captive fleets and pure parcel couriers that operate only last-mile routes without warehousing assets sit outside this scope.

Segmentation Overview

- By Service

- Domestic Transportation Management

- Road

- Air

- Rail

- Inland Waterways

- International Transportation Management

- Road

- Air

- Sea

- Multimodal / Intermodal

- Value-Added Warehousing and Distribution (VAWD)

- Domestic Transportation Management

- By End-User Industry

- Automotive

- Energy and Utilities

- Manufacturing

- Life Sciences and Healthcare

- Technology and Electronics

- Retail and E-commerce

- Consumer Goods and FMCG

- Food and Beverages

- Others

- By Logistics Model

- Asset-Light (Management-Based)

- Asset-Heavy (Own Fleet and Warehouses)

- Hybrid

- By Region (Domestic)

- Southeast

- South

- Northeast

- Center-West

- North

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview 3PL executives, e-commerce merchants, agribulk exporters, and regional warehouse developers across Sao Paulo, Parana, Bahia, and Amazonas. These dialogs validate tariff trends, contract churn rates, and technology adoption timelines, filling data gaps flagged during desk analysis and shaping consensus assumptions.

Desk Research

We begin with government and trade datasets such as ANTT road freight surveys, Receita Federal import-export declarations, IBGE manufacturing shipment indices, and port throughput logs from ANTAQ, which clarify cargo volumes and modal shares. Supplementary insight comes from Associacao Brasileira de Logistica white papers, World Bank logistics cost tables, listed 3PL filings, and press archives screened through Dow Jones Factiva and D&B Hoovers. Paid shipment trackers like Volza help benchmark international lanes. The sources noted are illustrative; many additional publications and databases guide our desk work.

Market-Sizing & Forecasting

A top-down build starts from Brazil's logistics spend, broken out by mode and end-user, and then allocates the spend pool to outsourced share using penetration ratios gleaned from interviews. Select bottom-up checks, sampled 3PL revenue disclosures, warehouse square-meter stock, and average billing rates calibrate totals. Key variables in our model include real GDP, e-commerce parcel volumes, interstate grain tonnage, diesel price index, and Grade-A warehouse absorption; each is forecast through multivariate regression with scenario bands reviewed by practitioners. Where provider data are missing, reasonable proxies (for example, BR-116 freight rate series) bridge the gap before final triangulation.

Data Validation & Update Cycle

Outputs pass variance checks against independent metrics; then a senior analyst reviews anomalies prior to sign-off. Reports refresh each year, with interim updates if policy shifts, major M&A, or fuel price shocks materially alter our baseline. A last-minute pulse check ensures clients receive the latest view.

Why Mordor's Brazil Third Party Logistics Baseline Commands Confidence

Published estimates often differ because firms choose unique service mixes, pricing levers, or refresh cadences.

Key gap drivers visible in Brazil include whether captive fleets are counted, the share of informal trucking assumed, ASP progression for value-added warehousing, and the year in which currency conversions are frozen. Our team reports a balanced base case, refreshed in 2025, while some publishers rely on older trade matrices or aggressive e-commerce growth curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.40 B (2025) | Mordor Intelligence | - |

| USD 29.25 B (2024) | Regional Consultancy A | Excludes asset-heavy contracts; projects higher outsourcing share from retail |

| USD 30.75 B (2023) | Global Consultancy B | Uses pre-COVID modal split and rolls forward with fixed 6% CAGR |

Taken together, the comparison shows how our disciplined scope definition, annual refresh, and dual-path validation deliver a dependable reference point that decision-makers can trace back to transparent variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Brazil 3PL market?

The Brazil 3PL market size stands at USD 29.74 billion in 2026 and is projected to reach USD 37.45 billion by 2031.

Which service segment is growing fastest?

Value-added Warehousing & Distribution leads with a 7.18% CAGR forecast for 2026-2031 as omnichannel retailers outsource complex fulfillment tasks.

Why is the North region expanding faster than other areas?

Completion of the North-South Railroad and rising grain exports through Northern Arc ports are driving a 5.74% CAGR in the North’s 3PL revenue.

How are ESG regulations influencing logistics outsourcing?

Mandatory ESG disclosures push companies to hire 3PLs with electric fleets, rail-first solutions, and emissions-tracking platforms, opening new contract opportunities.

Page last updated on: