Bolivia Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

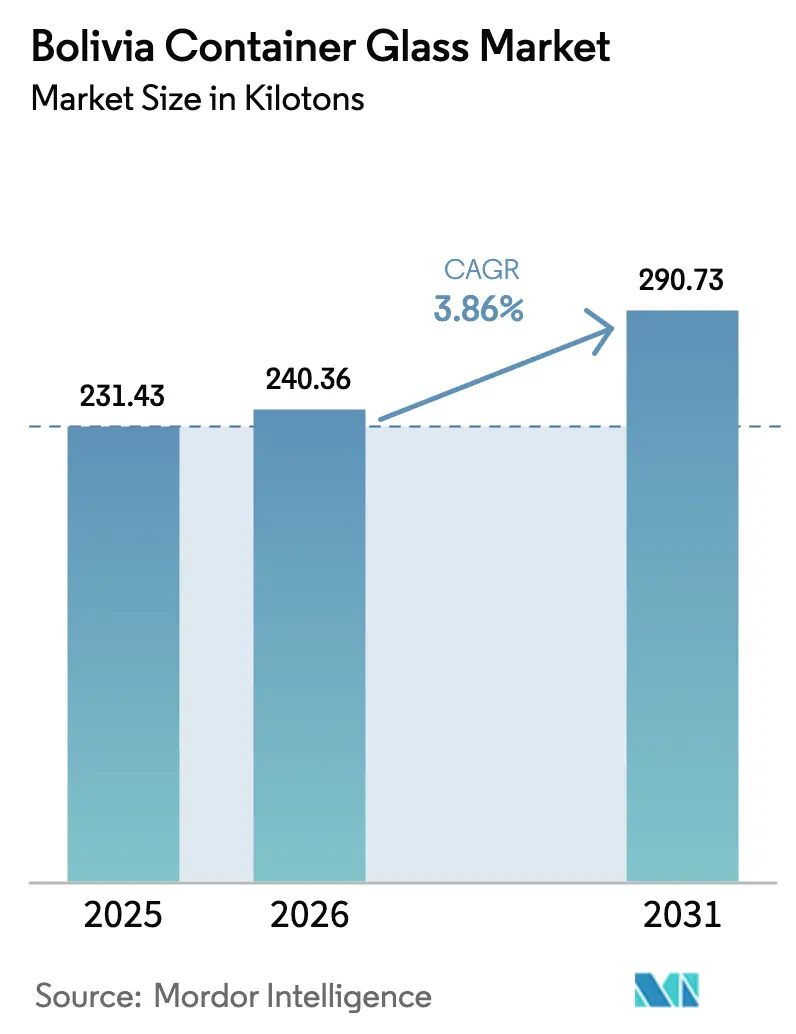

| Base Year Market Size (2025) | 231.43 kilotons |

| Market Volume (2026) | 240.36 kilotons |

| Market Volume (2031) | 290.73 kilotons |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

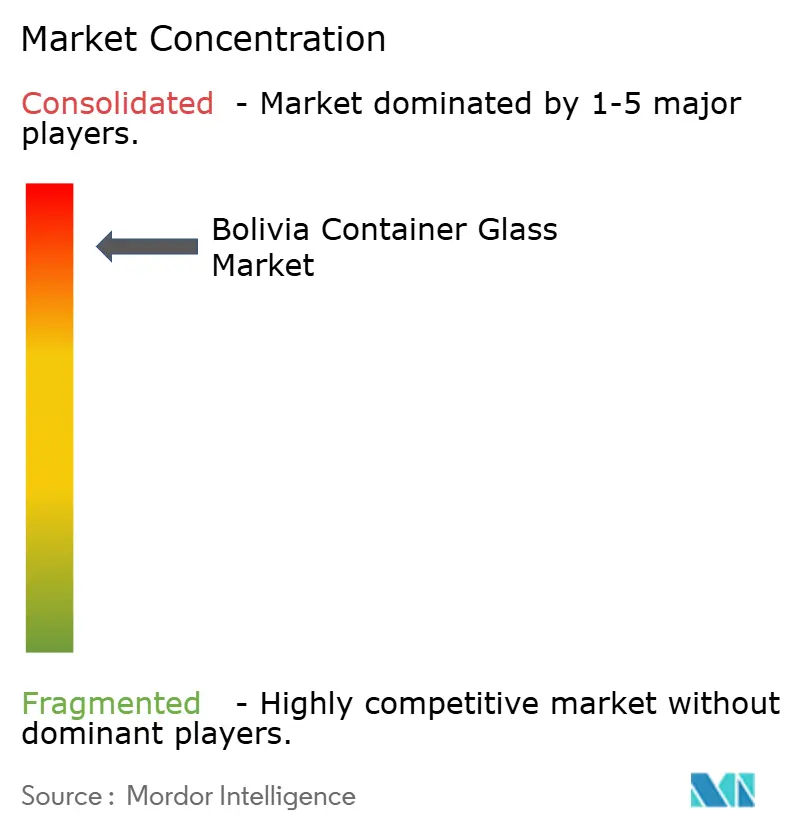

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bolivia Container Glass Market Analysis by Mordor Intelligence

The Bolivian container glass market size in 2026 is estimated at 240.36 kilotons, growing from 2025 value of 231.43 kilotons with 2031 projections showing 290.73 kilotons, growing at 3.86% CAGR over 2026-2031. Government-led import-substitution policies, the reopening of the state-owned Envases de Vidrio de Bolivia (ENVIBOL) plant, and rising demand from beverage, pharmaceutical, and cosmetics brands together uphold the positive volume outlook. Near-term growth also benefits from preferential procurement margins of 10-25% that favor locally manufactured goods, reduced customs paperwork for domestic producers, and steady recovery in household purchasing power. Longer-term prospects hinge on the successful implementation of circular-economy legislation that promotes recycling infrastructure and the utilization of glass cullet. Meanwhile, the planned bioceanic railway promises to reduce export transit time by roughly one-third, thereby easing logistics costs for value-added beverage shipments. Competitive dynamics remain moderate: Bolivia’s land-locked location raises freight differentials that generally protect domestic producers, yet PET and metal packages still threaten share in cost-sensitive soft-drink lines.[1]Inter-American Development Bank, “Logística en América Latina y el Caribe: Oportunidades, desafíos y líneas de acción,” iadb.org

Key Report Takeaways

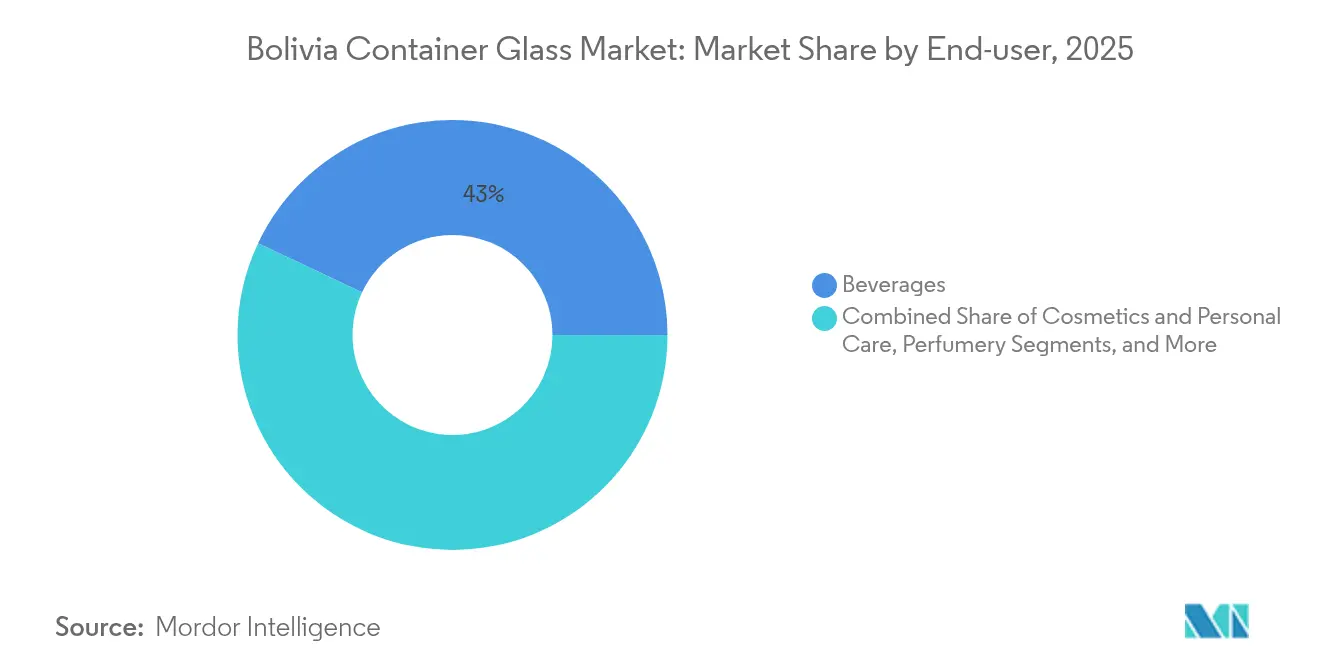

- By end-user, beverages captured 42.98% of the Bolivia container glass market share in 2025.

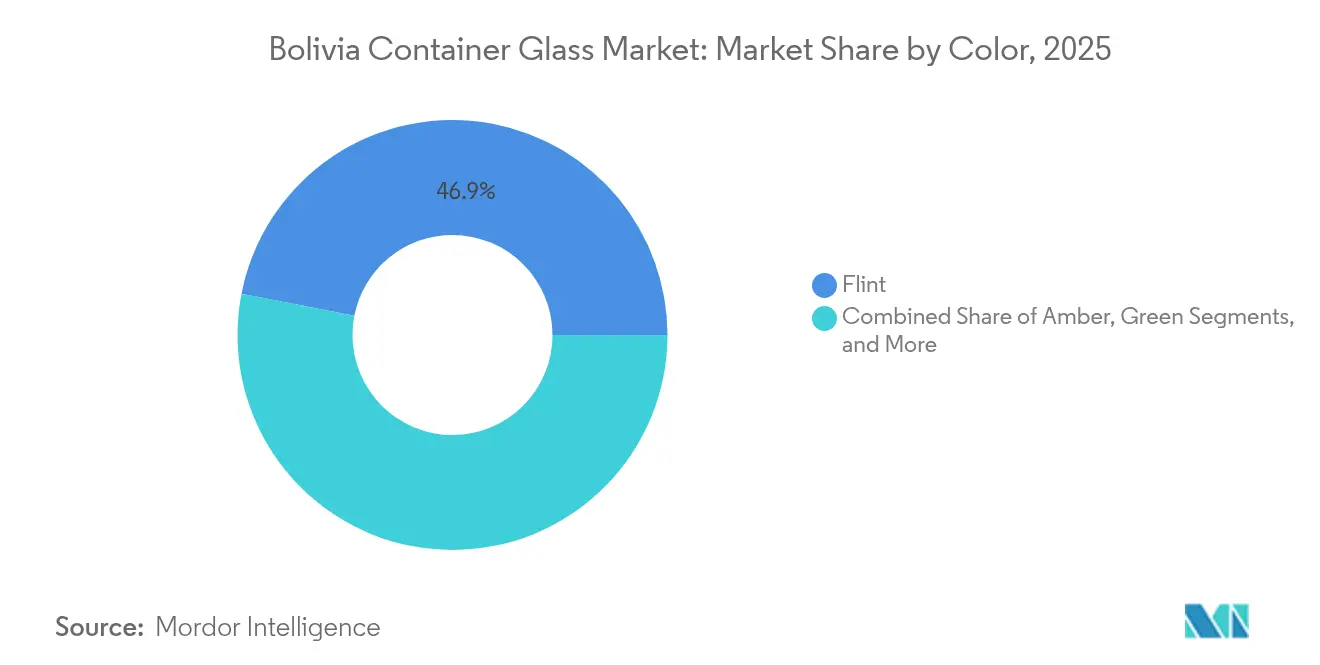

- By color, the Bolivia container glass market for amber glass is projected to grow at a 5.06% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bolivia Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising beverage-industry demand | +0.8% | Santa Cruz and La Paz metropolitan corridors | Medium term (2-4 years) |

| Sustainability and circular-economy push | +0.6% | Nationwide; pilot clusters in La Paz | Long term (≥ 4 years) |

| Government import-substitution policy | +0.9% | National; manufacturing hub in Chuquisaca | Short term (≤ 2 years) |

| Craft beer and artisanal-spirits boom | +0.4% | Urban centers, chiefly La Paz and Santa Cruz | Medium term (2-4 years) |

| Export-oriented Andean super-fruit juices | +0.3% | Export corridors to the United States and European Union | Long term (≥ 4 years) |

| Municipal glass-recycling tax incentives | +0.2% | City programs, led by La Paz | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Beverage-Industry Demand

Domestic breweries and bottlers are increasingly sourcing locally to reduce freight charges and capitalize on state price preferences. ENVIBOL supplied 1.8 million glass bottles to Cervecería Nacional Potosí in April 2025, generating BOB 3.6 million (USD 0.52 million) and validating plant capacity ramp-up.[2]Ce ere and ese, “Envibol pondrá 1.8 millones de botellas…,” noticiasvioleta.com Similar purchase commitments from craft beer and specialty-juice brands reinforce baseline demand, while compliance with Bolivian Institute of Standardization and Quality (IBNORCA) norms secures uniform quality for export-grade lots. Premium glass positioning aligns further with consumer shifts toward authenticity and environmentally friendly materials.

Sustainability and Circular-Economy Push

Bolivia enacted Extended Producer Responsibility rules in 2024, obliging brand owners to finance the collection of post-consumer containers. A USD 100 million Inter-American Development Bank loan equips cities with glass-sorting lines, which increase cullet availability while simultaneously reducing furnace energy loads and carbon emissions. Programs such as La Paz Recicla now upcycle glass shards into a secondary raw material worth roughly four times that of untreated waste. These moves bolster the attractiveness of glass vis-à-vis single-use plastics, whose compliance costs are rising.

Government Import-Substitution Policy

Decreto Supremo Nº 3010 anchors the “Hecho en Bolivia” label, mandates up to 25% bid preferences for goods with at least 50% domestic content, and accelerates payments to state suppliers. ENVIBOL, described by the Ministry of Productive Development as the most modern glass plant in Latin America, adds 40,000 tons of annual capacity and serves as a reference client for European technology vendors, including Bottero and Tiama, who installed new forming and inspection lines in 2025. Policy shelter allows local players to scale while integrating imported know-how.

Craft Beer and Artisanal-Spirits Boom

Bolivia hosts more than 45 registered craft breweries, up from fewer than 15 in 2019, many of which market Andean-ingredient lagers in distinctive embossed bottles that support premium price tags. Urban middle-class consumers favor glass for its aesthetic appeal and reusability, propelling niche orders that carry margins 18-22 percentage points above mainstream SKU averages. Government micro-enterprise incentives, 20% procurement preferences, and relaxed guarantee terms, lower entry barriers for start-ups seeking domestic packaging support

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET and metal-can competition | −0.7% | National, strongest in carbonated beverages | Short term (≤ 2 years) |

| Volatile LPG / energy costs | −0.5% | All production clusters | Short term (≤ 2 years) |

| Land-locked logistics bottlenecks | −0.4% | Export corridors to Pacific and Atlantic | Medium term (2-4 years) |

| Limited high-grade silica-sand deposits | −0.3% | South-eastern quarries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PET and Metal-Can Competition

Light-weight PET bottles trim freight bills and minimize breakage across Bolivia’s rougher road network. The average perfect-order index of 62% indicates that fragile containers experience more transit losses than in peer markets. Metal cans also attract carbonated-drink fillers seeking durability during the 42-day journey to Pacific ports. Nonetheless, as EPR fees on non-recyclable formats mount, brand owners face rising compliance costs that gradually swing preference toward infinitely recyclable glass.

Volatile LPG / Energy Costs

ENVIBOL’s reliance on LPG increases the furnace energy share of the cost of goods sold to roughly 7%, two percentage points above its peers running on pipeline natural gas. Price swings squeeze margins and curb reinvestment capacity. Efficiency retrofits, cullet ratios above 40%, and pilot studies on electric boosting are under evaluation but require significant capital outlays and stable policy signals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Retain Primacy

Beverages generated the largest slice of Bolivia container glass market size in 2025 at 42.98%. The segment’s resilience traces to growing lager, malt, and premium water lines that value product clarity, barrier strength, and brand differentiation. Beer producers routinely specify 330 milliliter flint bottles with pressure tolerances exceeding 16 bar, while wineries in Tarija are migrating to Burgundy-style glass to enhance shelf tactility. Moving forward, non-alcoholic wellness drinks anchored in quinoa, camu-camu, and aguaymanto extracts should help lift export-oriented orders, leveraging packaging transparency to showcase their natural hues. Cosmetics and personal care, while currently modest in volume, are forecast to outpace all other segments at a 4.85% CAGR through 2031, benefitting from urban specialty retailers and cross-border e-commerce demand for high-end serums and fragrances.

The Bolivia container glass market benefits from government measures that treat container supply as a strategic input for food security and value-added agriculture. ENVIBOL allies with small condiment and jam processors via discounted batch runs, strengthening rural linkages and ensuring homogenous bottle sourcing. Pharmaceutical and nutraceutical fillers represent a defensive niche, given stringent migration limits and the superior chemical inertness of borosilicate and type III soda-lime formulations. Emerging veterinary biologics producers also tap amber vials to guard against UV degradation, extending shelf life across Bolivia’s varied climate zones.

By Color: Flint Leads, Amber Accelerates

Flint accounted for 46.92% of Bolivia's container glass market share in 2025, dominating the market due to its versatility and superior clarity, which underscores its premium positioning across beverages, condiments, and cosmeceuticals. ENVIBOL’s continuous-color forehearths facilitate rapid switchover among 200-milliliter sauce, 500-milliliter spirit, and 750-milliliter wine formats, helping customers minimize mold inventory. Clearwater profiles also enhance recycling visibility, encouraging consumers to separate glass from organic waste at the household level.

Amber, forecasted to post a 5.06% CAGR, is gaining traction in pharmaceutical and specialty-beer lines, where its light-blocking properties protect sensitive ingredients. Tarija-based wineries exploring barrel-aged orange wines rank UV protection as a key differentiator in export markets. Green retains a cultural affinity with European-style pilsners, but sees modest shifts as plant designers favor two-color production to maintain forehearth efficiency. The Bolivian container glass market size for novel hues, such as cobalt blue, remains embryonic, restricted to limited-edition craft gins seeking shelf standout. Research into tin-mining tailings as flux substitutes may widen color palette options while trimming raw-material import ratios

Geography Analysis

Bolivia's container glass market activity is primarily concentrated in the Chuquisaca manufacturing belt, yet final demand centers in La Paz, Santa Cruz, and Cochabamba account for nearly 70% of the finished bottles. The highland-to-lowland haul imposes freight surcharges of USD 26-USD 29 per ton, but domestic sourcing still undercuts imported Argentine or Brazilian glass by an average 14% on a landed basis. La Paz municipal authorities, bolstered by IDB funding, commissioned twin color-sorting lines in 2024 that can process 18 tons of cullet daily, directly feeding ENVIBOL’s furnaces and reducing natural-gas equivalence by nearly 3 GJ per ton melted. Cross-border trade relies on multimodal routes: Pacific access via Arica, Chile, Atlantic flows through Puerto Suárez and the Paraguay-Paraná corridor, and north-bound lorry traffic to Peru. The USD 14 billion bioceanic railway, 52% complete as of mid-2025, is projected to reduce door-to-port lead time from 67 to 42 days. Such gains could unlock niche export plays for super-fruit nectars packaged in embossed glass, targeting eco-conscious consumers in California, Germany, and Japan. Nonetheless, Bolivia’s 28 km corridor to Ilo, Peru, remains hampered by customs backlogs that occasionally leave full container loads idle for up to nine calendar days.

Intra-Andean integration influences procurement: Owens-Illinois subsidiaries in Peru and Chile share mold libraries with their Bolivian affiliates, thereby shortening tooling cycles for regional beverage launches. MERCOSUR accession talks promise tariff harmonization on soda-ash imports, potentially reducing raw-material costs by 4-5%, although rules of origin stipulations are still under review. Free-trade-zone statutes already exempt duty on imported forming machines, thereby encouraging modernization among second-tier converters.

Competitive Landscape

Bolivia's container glass market is moderately competitive. ENVIBOL leads domestic tonnage and enjoys a price preference of up to 25% on public tenders, yet privately held Fabrica Boliviana de Vidrios and Vidrio Lux provide a counterbalance across the food and cosmetics niches. Owens-Illinois subsidiaries utilize global mold standards and multi-plant sourcing contracts to serve multinational beverage labels that require uniform bottle geometry across the Southern Cone.

Strategic partnerships define recent moves. In January 2025, ENVIBOL contracted European suppliers Bottero for IS lines, Antonini for annealing lehrs, Zecchetti for palletizing, and Tiama for automated inspection, thereby lifting daily melt capacity to 120 tons and expanding the job count to 150 direct roles and 500 indirect roles. Domestic producer VASA positions itself in specialty containers below 350 milliliters, targeting chili sauce exporters and boutique cosmetics.[3]VASA, “Listado de productos,” vasa.com.bo ENVIBOL’s adoption of 38% cullet feed stands out regionally, reducing energy intensity by approximately 90 kWh per ton compared to virgin batch melts.

Environmental credentials offer a differentiation axis: firms attaining ISO 14001 and qualifying for the “Hecho en Bolivia Reciclable” valve stamp gain retail shelf prominence, aiding in premium pricing. Research institutes are exploring the use of tin-mine tailings as a substitute for silica, offering cost mitigation and reputational benefits linked to circular economy narratives. Mergers or joint ventures remain plausible, particularly if fiscal incentives align with MERCOSUR's tariff structures.

Bolivia Container Glass Industry Leaders

Envases de Vidrio de Bolivia (ENVIBOL)

O-I Glass, Inc.

Lss Africa

Saverglass SAS

Yantai Hongning International Trade Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ICEX España issued a study naming SIMPACK, COMARQ and SERVOPACK as Bolivia’s three notable packaging-machinery makers and forecasting 4.82% CAGR for packaging equipment demand to 2027.

- April 2025: ENVIBOL secured a contract to supply 1.8 million bottles to Cervecería Nacional Potosí, generating BOB 3.6 million (USD 0.52 million) in revenue.

- January 2025: European suppliers Bottero, Antonini, Zecchetti and Tiama signed turnkey agreements with ENVIBOL for a 120-ton-per-day expansion in Zudáñez, adding 150 direct roles.

- November 2024: Swisscontact’s Proyecto Basura 0 entered phase 2, scaling circular-economy pilots and drafting national EPR regulations slated for 2026 rollout.

Bolivia Container Glass Market Report Scope

Glass containers, specifically bottles and jars, are crafted from glass, excluding windows and other non-container glass products. Their chemical inertness, sterility, and non-permeability make them a preferred choice in both alcoholic and non-alcoholic beverage industries. Valued for its transparency and inertness, glass packaging plays a crucial role in preserving the quality and integrity of its contents.

Bolivia container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the forecast volume for Bolivia’s container glass sector by 2031?

The market is projected to reach 290.73 kilotons by 2031, growing at a 3.86% CAGR over 2026-2031 from 240.36 kilotons in 2026.

Which segment holds the largest share of Bolivia’s container glass demand?

Beverages lead with 42.98% share in 2025, powered by domestic beer and emerging craft labels.

Why is flint glass preferred in Bolivia?

Flint’s transparency enhances product visibility and supports economies of scale, giving it a 46.92% share in 2025.

How are sustainability policies influencing packaging choices?

Extended Producer Responsibility rules and IDB-funded recycling lines favor recyclable glass over single-use plastic, pushing brands toward glass containers.

What logistics projects could lower export costs for Bolivian glass?

Completion of the USD 14 billion bioceanic railway is expected to cut door-to-port lead-time from 67 to 42 days, improving export competitiveness.

Who are the major domestic glass producers?

State-owned ENVIBOL leads, while Vidrio Lux, Fabrica Boliviana de Vidrios, and VASA occupy key niches in the beverages, food, and cosmetics sectors.

Page last updated on: