Door Control Modules Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

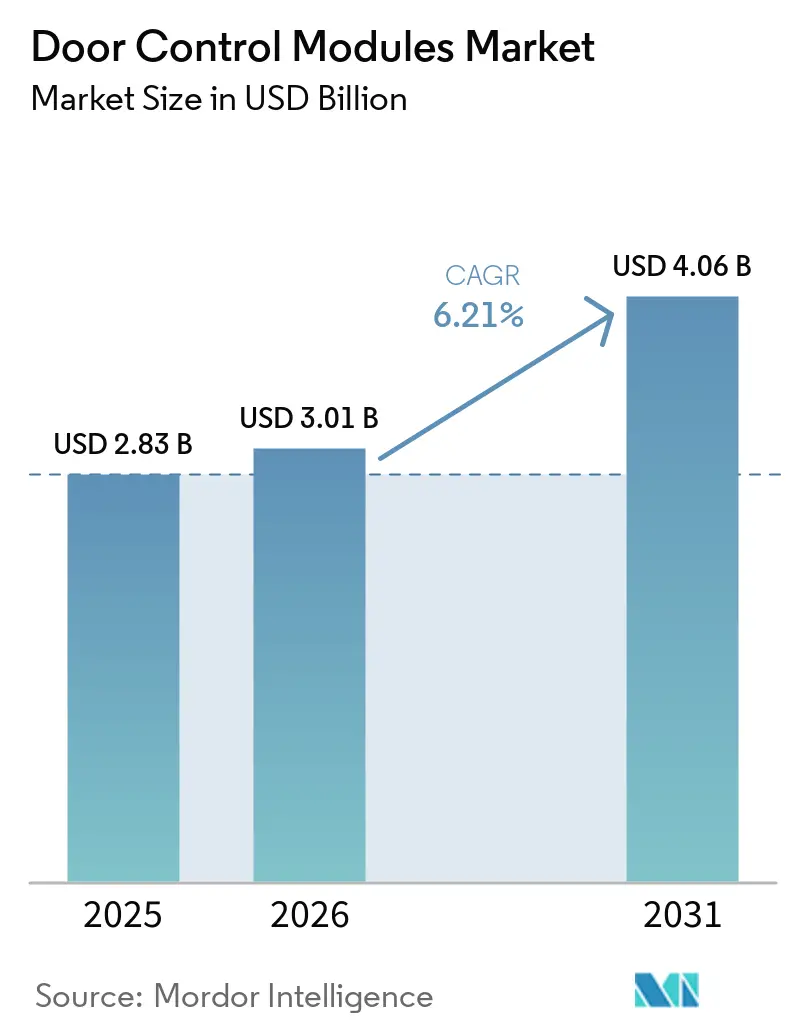

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 4.06 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Door Control Modules Market Analysis by Mordor Intelligence

The door control modules market size is expected to grow from USD 2.83 billion in 2025 to USD 3.01 billion in 2026, and is forecast to reach USD 4.06 billion by 2031, growing at a CAGR of 6.21% from 2026 to 2031. Multiple automakers are moving lock, window, mirror, illumination, and child-safety functions into software-defined controllers, and that architectural shift is the primary driver of new revenue. Suppliers that embed secure over-the-air capabilities are best positioned, as UNECE cybersecurity rules and Euro NCAP occupant-monitoring protocols now treat door zones as critical safety surfaces. At the same time, adoption of ultra-wideband digital keys and radar-based obstacle detection is pushing more computing to the edge of the vehicle, creating a technology gap between legacy electromechanical vendors and full-stack electronics specialists. Finally, a growing pool of aftermarket retrofits is beginning to influence bill-of-materials decisions for original-equipment programs, as right-to-repair laws give independent garages access to calibration data and firmware.

Key Report Takeaways

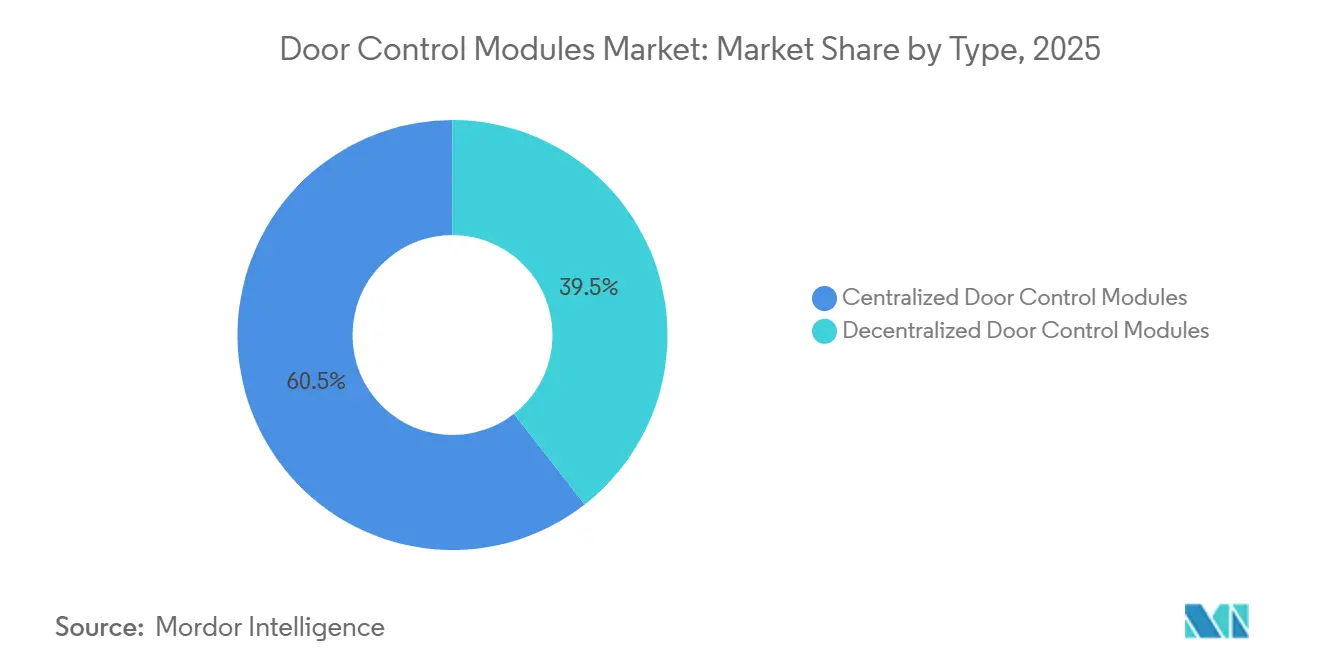

- By type, centralized modules held 60.55% of the Door Control Modules market share in 2025, while decentralized architectures are advancing at an 8.51% CAGR through 2031.

- By application, door-lock units accounted for 42.42% of the Door Control Modules market in 2025; electrochromic-mirror controllers are set to expand at a 11.07% CAGR over 2026-2031.

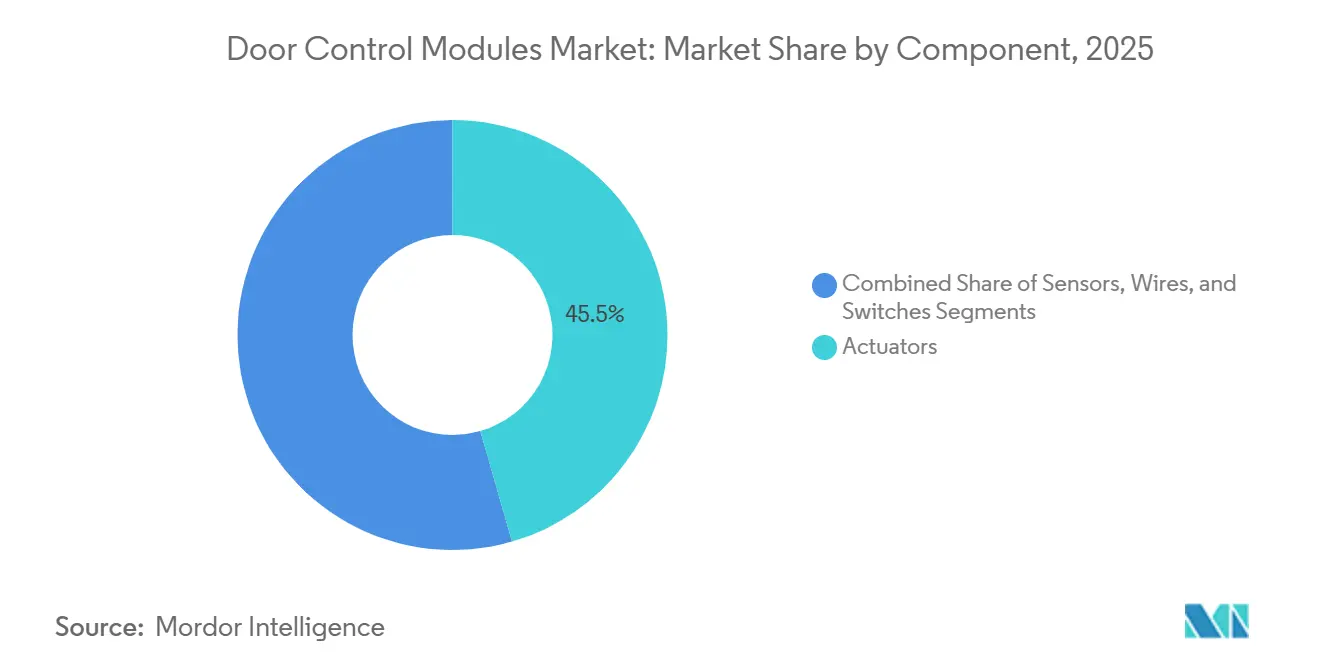

- By component, actuators accounted for 45.54% of 2025 revenue in the Door Control Modules Market, but sensors are the fastest-growing segment with an 8.35% CAGR through 2031.

- By sales channel, OEM programs captured 82.78% of the Door Control Modules market share in 2025, yet the aftermarket is pacing at a 7.09% CAGR on the back of an aging global vehicle parc.

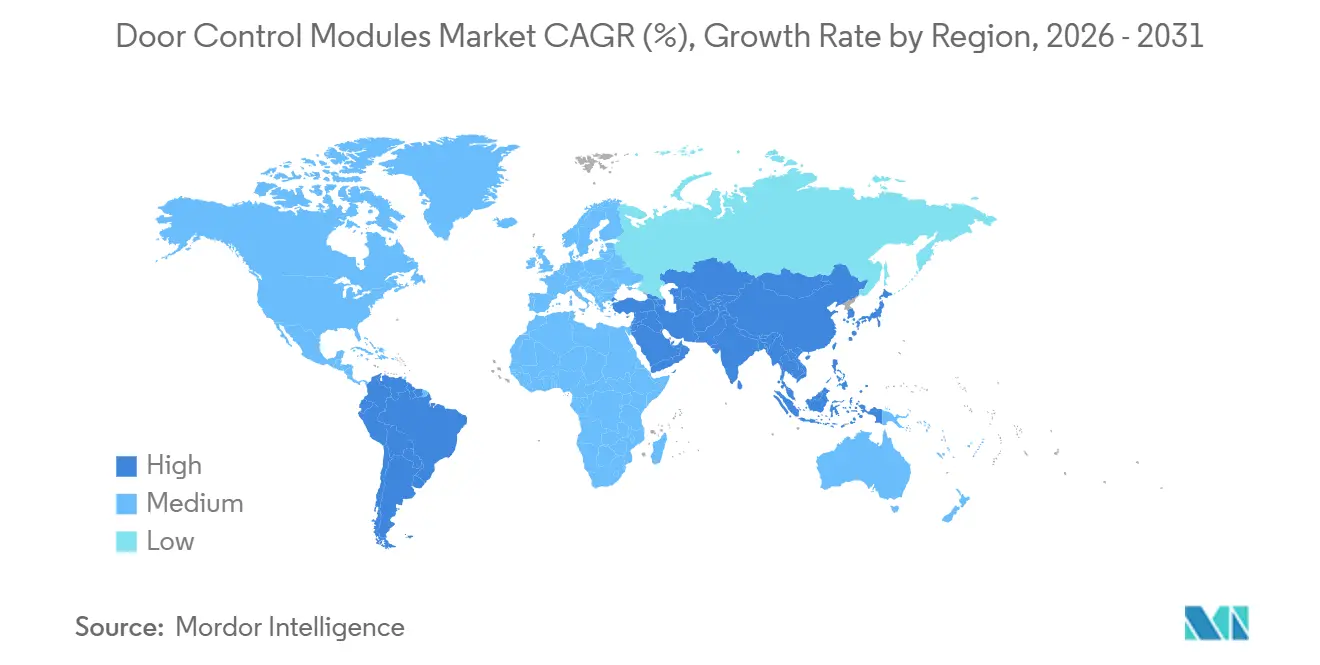

- By geography, Asia-Pacific led with 39.12% of the Door Control Modules market share in 2025, whereas South America is projected to grow at 8.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Door Control Modules Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification | +2.8% | Global, with APAC and Europe leading | Medium term (2-4 years) |

| ADAS-Ready Smart Door Modules | +2.1% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Passive Keyless Entry Systems | +1.4% | Global, premium to mainstream migration | Short term (≤ 2 years) |

| Ageing Vehicle Parc | +0.9% | North America and Europe primarily | Long term (≥ 4 years) |

| Cyber-Secure Module | +0.7% | Global, early adoption in premium segments | Long term (≥ 4 years) |

| Child-Presence Detection Mandates | +0.5% | Europe and North America initially | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification Boosting Electronic Content Per Door

Electric-vehicle platforms provide ample low-voltage power, enabling body engineers to integrate gesture control, radar-based obstacle sensing, and battery-disconnect logic in a single door controller. More functions per controller translate into larger software footprints, so tier-one suppliers now bundle AUTOSAR stacks and cybersecurity libraries as default features. Tight coordination between the battery-management system and the door control modules market enables safe post-crash unlocking even when high-voltage contactors are open. Chinese manufacturers pioneered the approach and now export similar architectures to Europe. Component vendors that ship highly integrated driver ICs are gaining design wins because they simplify layout, shrink harness weight, and cut validation cycles.

Rising Adoption of ADAS-Ready Smart Door Modules

Advanced driver-assistance features have grown beyond forward-looking cameras to include side-looking radar inside door skins. These sensors prevent “dooring” incidents by locking a door if a cyclist approaches, then releasing it once the path is clear. Euro NCAP awards safety credit for such functions, so mainstream brands are following earlier luxury-segment deployments[1]“Euro NCAP announces 2026 protocol changes to tackle modern driving risks,” Euro NCAP, www.euroncap.com. Because radar and camera data must remain tamper-proof, door ECUs now incorporate secure boot and authenticated firmware update processes, requirements that favor silicon suppliers with built-in hardware root of trust. The upshot is a richer technology stack that pushes the door control modules Market toward the same cybersecurity rigor as powertrain and ADAS domains.

Surge in Passive Keyless Entry Systems

Smartphone-based digital keys use ultra-wideband ranging to decide when a driver is close enough to unlock the vehicle. Those same radios also serve as secure channels for feature updates, helping OEMs reduce warranty claims due to lost key fobs. Low quiescent-current regulators keep sleep power in check, removing a longstanding hurdle for entry-level trims. Component makers offer reference designs that integrate UWB, Bluetooth LE, and CAN on a single board, accelerating time-to-market for smaller brands. With radio resources centralized, mechanical barrel locks are disappearing from many premium platforms, sharpening focus on door-controller resilience during battery failure[2]“Euro NCAP’s 2026 protocol: Advances for firefighters,” CTIF, ctif.org.

Ageing Vehicle Parc Driving Aftermarket Replacements

Average vehicle age is rising in North America and Europe, and owners of older cars are increasingly demanding modern safety and convenience features. Right-to-repair legislation unlocks technical documentation once reserved for franchised dealers, allowing independent garages to flash new firmware into replacement door modules. This change is expanding the addressable aftermarket for secure over-the-air-ready controllers. Suppliers that pre-program modules with calibration files for multiple vehicle variants hold a cost advantage because a single SKU can serve multiple part numbers. As a result, the door control modules market now supports a secondary layer of software specialists who resell calibration subscriptions to workshop networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply Volatility | -1.8% | Global, acute in APAC manufacturing hubs | Short term (≤ 2 years) |

| Price Pressure | -1.2% | Global, most severe in cost-sensitive segments | Medium term (2-4 years) |

| Reliability Challenges | -0.7% | Global, critical in extreme climate regions | Long term (≥ 4 years) |

| Solid-State E-Latches | -0.4% | Premium segments initially, mass market following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply Volatility

Memory vendors have shifted capacity to high-bandwidth products for AI data centers, leaving automotive customers short on legacy DRAM. Lead times tightened to just a few weeks in late 2025, forcing module integrators to place non-cancellable orders long before program freeze. Some automakers now redesign controllers to support newer memory standards, adding cost and engineering overhead that stalls launches. The result is a drag on the door control modules market as platform owners delay optional comfort features until component availability stabilizes.

Price Pressure on Tier-1 Suppliers

OEMs insist that tier-ones absorb most raw-material inflation, pushing margins toward mid-single digits. Body-electronics providers with mature factories face especially stiff price ceilings because locks and window lifts deliver little perceived consumer value compared with infotainment screens. Suppliers counter by relocating production to lower-cost regions and by merging mechanical, power, and sensor boards into a single PCB. While that strategy cuts the bill of materials, it also concentrates risk, because any defect now affects multiple functions. Cost discipline, therefore, shapes competitive dynamics more than pure technology in several portions of the door control modules market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Centralized Control Remains Prevalent, Zonal Adoption Rises

Centralized controllers held 60.55% of the Door Control Modules market share in 2025. Integrating all four doors into a single ECU reduces the CAN node count and software variants, appealing to high-volume platforms with long production lifecycles. Engineers appreciate the predictable power budget and simplified diagnostic schemes that accompany this layout. However, the weight of wiring harnesses and the increasing diversity of features are making the architecture less attractive for electric vehicles, where every gram matters.

Decentralized or zonal units, advancing at an 8.51% CAGR, split compute power between individual doors, trimming harness length, and letting designers add features by flashing only local code. This modularity aligns with emerging software subscription models because upgrades can activate dormant hardware on a per-door basis. Over-the-air updates also complete faster when the binary size shrinks, improving customer experience. Suppliers that pre-validate smaller controllers for multiple locations in the vehicle stand to win more global platforms, signaling a gradual pivot in the door control modules market.

By Application: Door Locks Dominate, Electrochromic Mirrors Accelerate

Door-lock modules controlled 42.42% of the Door Control Modules market share in 2025 within the Door Control Modules Market. Passive entry, crash unlock coordination, and child-safety integration keep this sub-segment essential even when other door functions migrate to central body controllers. The lock motor’s physical nature also means replacement cycles are tied to wear, ensuring volume for aftermarket channels.

Electrochromic-mirror controllers, the fastest sub-segment at 11.07% CAGR, ride on premium demand for glare reduction and camera-based rear visibility. Because these mirrors require dynamic voltage control and light sensing, the associated ECU often carries richer analog front ends than a basic window lift. Integration trends now merge mirror, indicator, and ambient lighting under a single LIN node, paving the way for wider adoption beyond luxury tiers.

By Component: Actuators Anchor Spend, Sensors Capture Momentum

Actuators accounted for 45.54% of 2025 component revenue in the Door Control Modules Market. Motorized latches, window drives, and mirror folds remain non-negotiable hardware, so supply chains for these parts emphasize mechanical robustness and validated endurance. Consolidation among motor suppliers aims to leverage scale in raw materials such as copper windings and magnets.

Sensors are growing fastest at 8.35% CAGR because radar, Hall-effect, and capacitive devices turn mechanical doors into data-rich safety zones. Direct child-presence detection, anti-pinch monitoring, and gesture recognition all depend on accurate sensing. Package miniaturization enables more sensors to fit into existing assemblies without redesigning door skins, lowers incremental costs, and encourages broader feature rollout across the door control modules market.

By Sales Channel: OEM Programs Lead, Aftermarket Finds Opportunity

OEM contracts accounted for 82.78% of the Door Control Modules market in 2025. Vehicle manufacturers, often locking in hardware specifications years before production begins, inadvertently grant significant negotiating power to established tier-one suppliers. Moreover, rigorous compliance testing for both cybersecurity and functional safety poses a formidable barrier to new entrants, as validation costs become disproportionately high at lower volumes.

The aftermarket, growing at a 7.09% CAGR, serves an aging fleet whose original modules lack over-the-air updates or suffer mechanical wear. Independent repair shops equipped with secure flashing tools can now install upgraded controllers that add passive entry or soft-close functions. Suppliers offering universal door modules pre-loaded with multiple calibration profiles stand to capture a larger share of do-it-yourself enthusiasts and specialist installers within the broader door control modules market.

Geography Analysis

Asia-Pacific leads the Door Control Modules Market, holding 39.12% share in 2025. Rapid electric-vehicle rollout in China and sustained investment in South Korean mechatronics underwrite continued dominance. Local tier-ones expand capacity in India to supply both regional OEMs and export customers, further reinforcing the area’s supply-chain gravity. The region’s software-defined-vehicle momentum also accelerates demand for highly integrated controllers.

South America, while smaller in absolute terms, is the fastest-growing territory at 8.83% CAGR. Near-shoring by Asian suppliers reduces tariff exposure and shortens delivery times for Brazilian and Argentine assembly plants. Emerging trade corridors in Mexico encourage hybrid production models that pair imported electronics with locally stamped housings, seeding a base for future regional R&D.

North America and Europe grow more modestly as vehicle penetration is mature. New safety rules on seat-belt reminders in the United States and Euro NCAP child-presence scoring drive selective feature upgrades, but macroeconomic caution tempers unit volumes. Strong aftermarket networks, however, cushion the impact, allowing retrofit door-modules to proliferate in older fleets. Overall, geographic demand patterns force suppliers to balance high-tech requirements of advanced markets with cost-sensitive needs of growth regions, shaping investment across the door control modules market.

Competitive Landscape

The Door Control Modules Market shows moderate concentration, with the five largest suppliers collectively holding a mojority share, but with no clear leader. Global tier-ones broaden their portfolios by pairing actuation, sensing, and secure software into turnkey door-zone systems, simplifying logistics for vehicle manufacturers. Recent contract wins for radar-equipped electromechanical doors signal growing interest in touchless opening solutions.

Technology roadmaps emphasize cybersecurity compliance and seamless over-the-air updates. Some semiconductor providers now deliver complete reference boards, lifting them from component suppliers to system partners. This blurs traditional tier boundaries and prompts mechanical specialists to acquire software expertise or form joint ventures to stay relevant.

Regional challengers focus on price-optimized modules for high-volume domestic cars and on aftermarket replacements, where certification hurdles are lower. Venture investment flows into niche firms that supply solid-state latches or low-power radar sensors. As automakers consolidate their supplier bases to cut validation workload, acquisition activity is likely to increase, potentially raising the concentration index for the door control modules market.

Door Control Modules Industry Leaders

Continental AG

Robert Bosch GmbH

Denso Corporation

Valeo SA

Aisin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Marelli plans to debut a microcontroller-free door module at Auto China 2026. The innovation shifts key functions to a zone controller, streamlining wiring and facilitating quicker updates.

- August 2025: LG Innotek unveiled its next-generation digital key solution that links smartphones to vehicle doors via 5G modules, enabling lock, unlock, and engine start functions.

- May 2025: HIRAIN’s body-control unit helped a light-truck model meet European cybersecurity rules, marking its first commercial-vehicle domain-control win on the continent.

- April 2025: Brose introduced its Smart Cockpit System in China, which features synchronized lighting and sound and a digital key for proximity-based keyless entry.

Global Door Control Modules Market Report Scope

The Door Control Modules Market is analyzed based on type, application, component, sales channel, and geography.

By Type, the market is segmented into Centralized Door Control and Decentralized Door Control. By Application, the market is segmented into Door Lock, Mirror Adjustment, Window Lift, Illumination, Mirror Defroster, Central Locks and Child Safety, and Electrochromic Mirror. By Component, the market is segmented into Actuators, Sensors, Wires, and Switches. By Sales Channel, the market is segmented into OEM and Aftermarket. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (United Kingdom, Germany, Spain, Italy, France, Russia, and Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, Egypt, South Africa, and Rest of Middle East and Africa).

Market forecasts are provided in terms of Value (USD) and Volume (Units).

| Centralized Door Control Modules |

| Decentralized Door Control Modules |

| Door Lock |

| Mirror Adjustment |

| Window Lift |

| Illumination |

| Mirror Defroster |

| Central Locks and Child Lock |

| Electrochromic Mirror |

| Actuators |

| Sensors |

| Wires |

| Switches |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Centralized Door Control Modules | |

| Decentralized Door Control Modules | ||

| By Application | Door Lock | |

| Mirror Adjustment | ||

| Window Lift | ||

| Illumination | ||

| Mirror Defroster | ||

| Central Locks and Child Lock | ||

| Electrochromic Mirror | ||

| By Component | Actuators | |

| Sensors | ||

| Wires | ||

| Switches | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Door Control Modules market size be by 2031?

The market is forecasted to reach USD 4.06 billion, reflecting a 6.21% CAGR over 2026-2031.

Which regional market leads current demand for door control modules?

Asia-Pacific held the largest share at 39.12% in 2025.

What sub-segment is growing fastest within door applications?

Electrochromic-mirror controllers are projected to advance at an 11.07% CAGR.

Why are decentralized door modules gaining traction?

They cut wiring weight and support zonal architectures that ease over-the-air feature updates.

Page last updated on: