Steering Column Control Modules Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

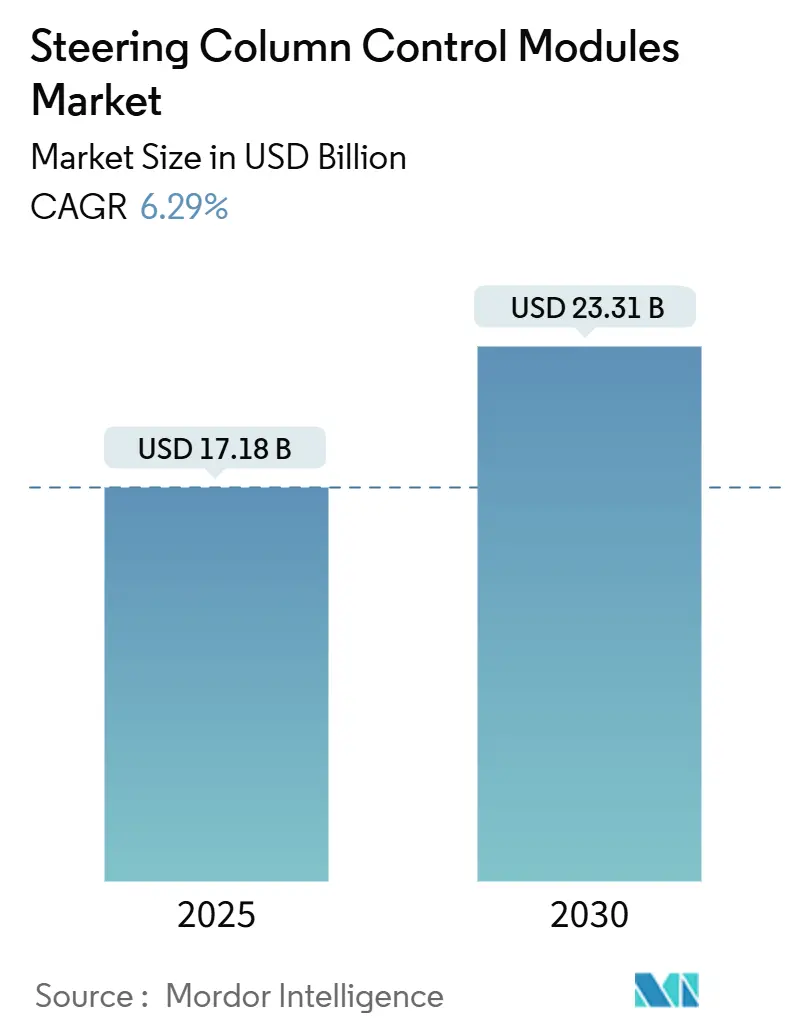

| Market Size (2025) | USD 17.18 Billion |

| Market Size (2030) | USD 23.31 Billion |

| Growth Rate (2025 - 2030) | 6.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Steering Column Control Modules Market Analysis by Mordor Intelligence

The steering column control modules market size stands at USD 17.18 billion in 2025 and is forecast to expand to USD 23.31 billion by 2030 at a 6.29% CAGR. Momentum stems from the automotive sector’s pivot toward electronic power steering, Level 2+ autonomy, and regulations mandating physical control redundancies. Passenger-car electrification, 48 V adoption, and haptic-feedback innovation further raise unit value, while semiconductor bottlenecks and cybersecurity compliance temper growth. Asia-Pacific dominates both demand and supply owing to China’s electric-vehicle surge and India’s cost-competitive manufacturing ecosystem. Competitive intensity is moderate as top players race to embed software-defined capabilities and redundant electronic architectures within steering assemblies, creating fresh opportunities for vertically integrated suppliers that can bundle actuators, sensors, and cybersecurity features into a unified module solution.

Key Report Takeaways

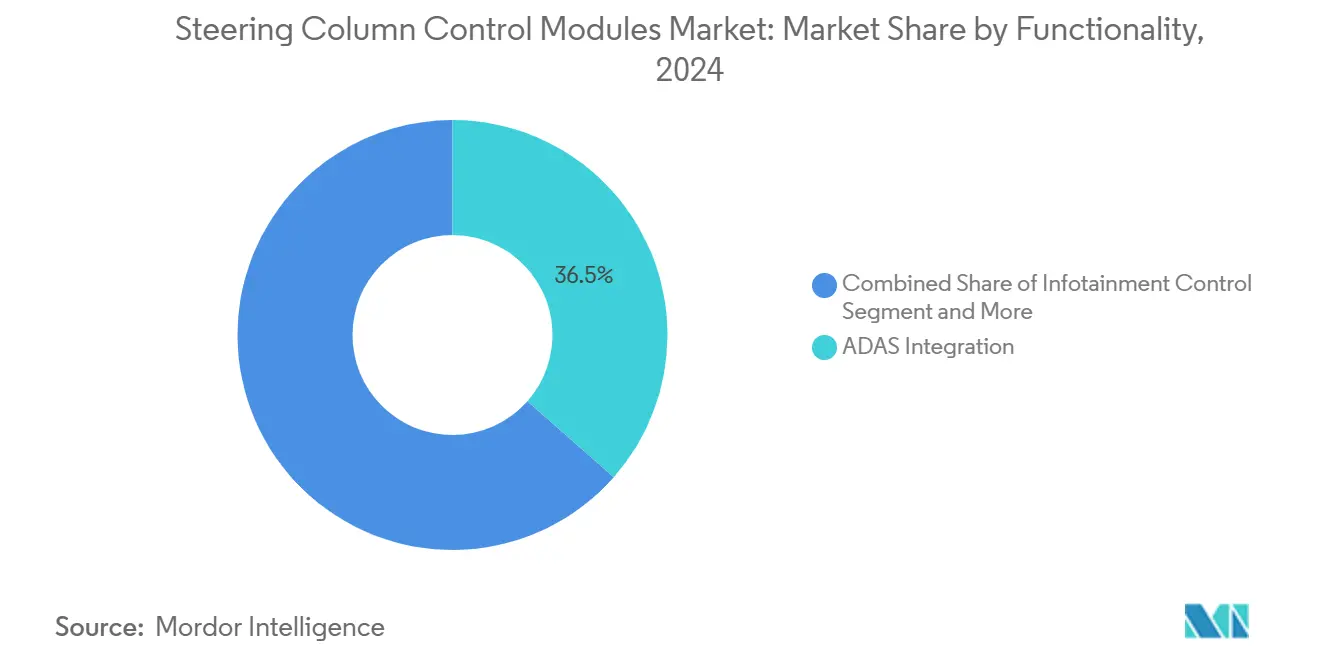

- By functionality, ADAS integration captured 36.51% revenue in 2024; cruise-control haptics is projected to expand at a 12.46% CAGR through 2030.

- By component position, on-steering-wheel solutions led with 57.38% share in 2024, while around/below-wheel assemblies are the fastest-growing at 12.05% CAGR.

- By steering type, electric power steering held 54.25% of the steering column control modules market share in 2024; steer-by-wire is forecast to accelerate at a 15.83% CAGR to 2030.

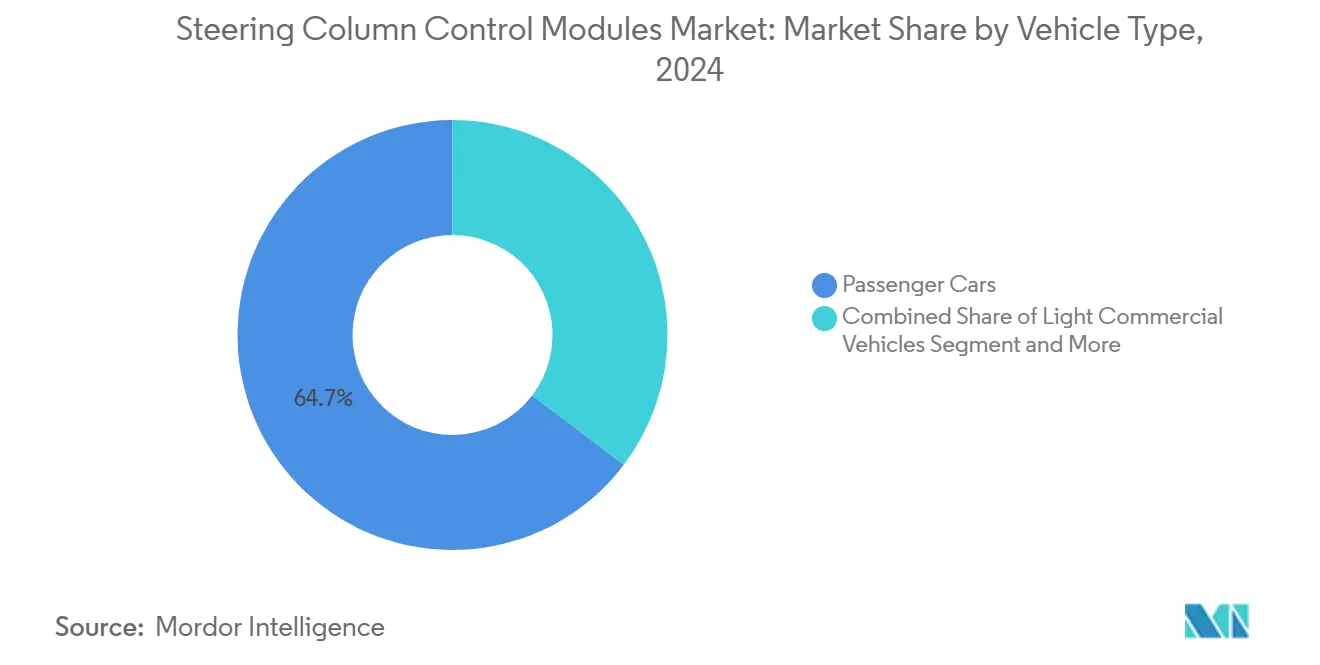

- By vehicle type, passenger cars accounted for 64.68% of the steering column control modules market size in 2024 and are advancing at a 13.99% CAGR through 2030.

- By distribution channel, OEM deliveries represented 78.24% of 2024 revenues, whereas aftermarket retrofits are expanding at a 9.51% CAGR to 2030.

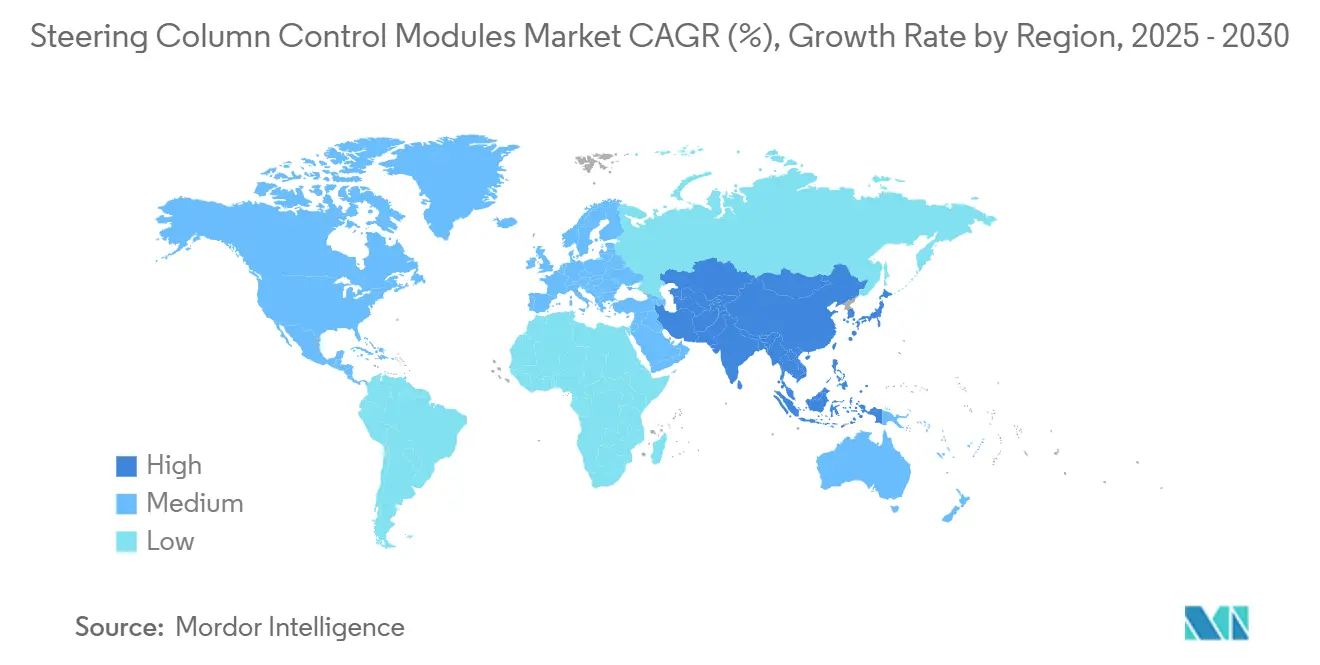

- By geography, the Asia-Pacific captured 50.08% of 2024 revenues and is projected to advance at a 9.09% CAGR through 2030.

Global Steering Column Control Modules Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of Electric Power Steering (EPS) | +2.1% | Global, with APAC leading adoption | Medium term (2-4 years) |

| ADAS Integration | +1.8% | North America and Europe early, APAC scaling | Long term (≥ 4 years) |

| Safety Regulations | +1.2% | Europe and North America regulatory, Global implementation | Short term (≤ 2 years) |

| Passenger-Car Production Growth | +0.9% | APAC core, spill-over to emerging markets | Medium term (2-4 years) |

| Feedback Modules for L2+ Autonomy | +0.7% | Premium segments in developed markets | Long term (≥ 4 years) |

| 48-V Modular ECUs | +0.5% | China and North America EV hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adoption of Electric Power Steering (EPS)

EPS eliminates hydraulic pumps, cuts parasitic losses, and makes steering software-definable. The technology draws current only on demand, aiding OEM emissions targets and enabling variable assist tailored to speed and load. Electronic torque overlay provides a platform for lane-keeping and automated parking, driving demand for multi-function switches and mode selectors embedded in the wheel. Suppliers now integrate motor-control units within column modules, shortening wire runs and simplifying diagnostics. As global EV output rises, EPS serves as the default baseline for new platforms, cementing its pull on the steering column control modules market[1]“Electric Power Steering System,” Renesas Electronics Corporation, renesas.com.

ADAS Integration

Level 2+ systems require precise driver-vehicle handovers, spurring uptake of hands-on detection, rim-embedded haptics, and redundant CAN gateways. Regulation No. 171 obliges continuous driver monitoring, prompting OEMs to fit capacitive sensors and vibrotactile alerts inside steering wheels. Premium brands trial steer-by-wire yokes for 2026 launches, demanding dual-channel ECUs and fail-operational designs. Suppliers capable of bundling actuators, software, and cybersecurity keys under one part number enjoy margin upside. The convergence of ADAS and human-machine interfaces positions steering modules as a nerve center rather than a passive switch cluster.

Safety Regulations Mandating Steering-Wheel Controls

Euro NCAP’s 2026 protocol requires mechanical buttons for five critical functions, challenging touchscreen-only interiors, and guaranteeing baseline demand for tactile inputs. The rule aligns with UNECE driver-distraction standards and ISO 26262 redundancy clauses, compelling any minimalist cockpit to retain physical controls. OEM design teams, therefore, balance aesthetic minimalism with compliance, leaning on multi-zone haptics and illuminated icons to reconcile both. Module suppliers that pre-validate switch layouts against crash-pulse and air-bag kinematics gain RFQ preference. Early adoption in Europe sets a template likely to propagate into U.S. NHTSA and Chinese NCAP frameworks[2]“Cars Will Need Buttons Not Just Touchscreens to Get a 5-Star Euro NCAP Safety Rating,” European Transport Safety Council, etsc.eu.

Growth in Passenger-Car Production

Asia-Pacific light-vehicle lines ramp capacity to serve domestic demand and export pipelines into the Middle East, Africa, and Latin America. Subsidies for EVs in China and India lift content per vehicle because electric cabins are quieter, heightening the need for tactile cues. Multifunction wheels that once appeared only in premium sedans now permeate B-segment hatchbacks, swelling volume. Localized module production inside India’s supplier parks helps OEMs meet cost targets and avoid tariff exposure. Scale advantages fuel the steering column control modules market trajectory by absorbing R&D overhead across high-run platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Modules Cost | -1.4% | Global, acute in price-sensitive segments | Short term (≤ 2 years) |

| CAN-Bus Cyber-security Risks | -0.8% | Connected vehicle markets globally | Medium term (2-4 years) |

| Reliability Concerns | -0.6% | Mature markets with high durability expectations | Long term (≥ 4 years) |

| MCU Supply-Chain Shortages | -0.5% | Global, concentrated in automotive semiconductors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Modules

Haptic-feedback, hands-on detection, and 48 V compatibility add 40-60% cost over mechanical switches, squeezing entry-level trims. Automotive-grade micro-controllers with secure boot and ASIL-D certification raise the bill-of-materials even before tooling amortization. Volume allocation helps, yet smaller suppliers lack the capital for automated optical inspection lines needed to hit defect ppm targets. OEM cost-down cycles force tier-ones to dual-source plastics and leverage global molding footprints. Until economies of scale deepen, premium feature sets will remain optional bundles outside top-selling variants.

Cyber-Security Risks in CAN-Bus

Column modules sit on the steering CAN, making them potential attack vectors. Remote update pathways and Bluetooth hand-off functions widen the surface area. UNECE R155 enforces cybersecurity management systems, obliging suppliers to audit software suppliers and implement key-rotation protocols. Encryption chips and intrusion-detection firmware add cost and weight, yet failure to comply threatens vehicle-type approval. Continuous monitoring and patching blur the line between hardware sales and lifetime service contracts, altering cash-flow models and vendor responsibilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functionality: ADAS Integration Drives Premium Features

ADAS integration held the highest revenue at 36.51% in 2024 and is expected to post a 12.46% CAGR through 2030, underscoring the steering column control modules market shift toward autonomous-ready cockpits. Integration aligns with Regulation No. 171, provoking widespread adoption of capacitive rim sensors and vibrotactile alerts. Infotainment control remains universal, but its growth settles as saturation approaches in developed economies. Cruise-control haptics and communication shortcuts migrate to lower trims, widening addressable volume.

Suppliers differentiate by embedding multi-function touch keys and force-feedback actuators into single silicon footprints, controlling latency and energy draw. Renesas’ low-cost haptic module allows tactile confirmation inside 12 mm switch depths, satisfying both packaging and distraction limits. Continental’s gesture-recognition demos preview a post-button era, yet Euro NCAP rules ensure physical redundancies will stay. The segment thereby balances futuristic interactions with regulatory pragmatism, anchoring its dominant share through 2030.

By Component Position: Stalkless Designs Challenge Traditional Layouts

On-wheel assemblies delivered 57.38% revenue in 2024, reflecting OEM preference for thumb-accessible controls that keep hands at the rim. Around/below-wheel modules, however, are rising at a 12.05% CAGR as minimalist dashboards experiment with steering-column pods that consolidate lighting, wiper, and ADAS toggles. Tesla-style stalk deletion sparks interest in capacitive pads hidden behind spoke trim, yet meeting tactile click demands remains a design hurdle.

TG0’s pressure-mapped polymer surfaces demonstrate how zero-gap designs can match mechanical switch ergonomics without protrusions. Euro NCAP compliance could slow pure touch solutions, but hybrid touch-plus-button clusters offer a compromise path. As OEMs rationalize part numbers across global models, modular pods that bolt to common steering frames unlock volume leverage, amplifying momentum in the steering column control modules market.

By Steering Type: Steer-by-Wire Emerges as Disruptive Technology

Electric power steering held a 54.25% share in 2024, reflecting its status as the baseline architecture for fuel-efficient and software-defined vehicles. Hydraulic racks continue to retreat to legacy commercial platforms because they weigh more and limit ADAS scalability. Manual systems remain in ultra-budget segments, yet their influence on the steering column control modules market is shrinking as safety and comfort expectations rise. Steer-by-wire, although small today, is valued for packaging freedom and customizable ratios that mechanical linkages cannot deliver.

The steer-by-wire segment is projected to advance at a 15.83% CAGR as premium programs launching from 2026 validate fail-operational designs. Mercedes-Benz pairs the technology with retractable yokes, demonstrating how electronic actuation enables dashboard stowage and novel seating ergonomics. ZF’s dual-motor actuators showcase redundancy strategies that satisfy ISO 26262 and UNECE rules without adding steering columns. As OEMs shift to 48 V zonal power nets, steer-by-wire modules benefit from higher headroom for motors and processors, reinforcing their disruptive momentum in the steering column control modules market.

By Vehicle Type: Passenger Cars Lead Electrification Trends

Passenger cars preserved a 64.68% share in 2024 and are forecasted to grow at a 13.99% CAGR because EV adoption lifts content per unit. Light commercial vans post steady demand tied to e-commerce, but cost ceilings delay widespread use of premium haptics and steer-by-wire. Heavy trucks and buses adopt electronic columns more slowly, limited by long fleet life cycles and stringent durability tests. Nonetheless, safety mandates such as lane-departure systems are nudging those segments toward smarter steering interfaces.

SUV proliferation amplifies interest in rear-axle steering to offset size-related agility issues, letting suppliers cross-sell column modules and rear-steer actuators in one package. Nexteer’s 2025 rollout of cost-effective rear-steer illustrates how passenger-vehicle innovations migrate into pickups and crossovers. In EV cabins, reduced drivetrain noise raises the need for tactile confirmation, driving uptake of multi-zone haptics among mainstream sedans. These trends collectively sustain the steering column control modules market size expansion across vehicle classes.

By Distribution Channel: OEM Dominance Faces Aftermarket Growth

OEM fitment commanded 78.24% revenue in 2024 because steering modules must align with air-bag deployment logic and encrypted CAN messaging from day one. Factory integration reduces homologation risk and simplifies ISO 26262 audits, keeping automakers loyal to tier-one suppliers. Cyber-secure key exchanges and driver-monitoring hooks are baked into production ECUs, strengthening OEM channel stickiness. Even so, the growing population of older vehicles creates latent demand for replacement switch packs and convenience upgrades.

Aftermarket kits are set to rise at a 9.51% CAGR as vehicle life spans exceed 12 years, though retrofit complexity restricts scope to plug-and-play offerings. Tier-ones now co-brand service parts with automakers to preserve warranty while monetizing long-tail replacements. Hands-on detection rims and illuminated thumb wheels appear in dealer-installed bundles aimed at tech-savvy consumers. Despite this upside, the steering column control modules market will stay OEM-centric because safety certifications and cybersecurity pairing place natural barriers around high-function retrofits.

Geography Analysis

Asia-Pacific held 50.08% of 2024 revenue and is projected to grow at a 9.09% CAGR to 2030. China’s dominance in battery-electric production fuels high-content steering wheels featuring hands-on detection and 48 V-ready ECUs. India’s production-linked incentives lure tier-ones to localize columns and switch packs, trimming logistics costs. ASEAN facilities assemble global models for export, anchoring supplier scale, while Japanese and Korean firms contribute IC design and haptic algorithms. The region’s blend of volume and value cements its leadership in the steering column control modules market.

North America ranks second, expanding at 5.22% CAGR. Early ADAS uptake and pickup-truck popularity raise demand for column-mounted trailer-assist switches and rear-steer selectors. Tesla’s 48 V platform highlights U.S. appetite for electrical innovation, though supply-chain fragility around semiconductors compels multi-sourcing strategies. Canada’s magnesium casting capacity supports lightweight steering frames, and Mexico’s low-cost wiring-harness plants offer FOB savings for mid-tier suppliers. Regulatory certainty around FMVSS keeps design validation predictable, aiding time-to-market.

Europe records 4.65% CAGR, constrained by macro uncertainties yet propelled by stringent safety mandates. Euro NCAP physical-button rules guarantee baseline demand for mechanical interfaces even as luxury brands trial touch-sensitive spokes. Germany’s engineering depth drives steer-by-wire R&D, France focuses on ergonomic compliance, and Italy refines leather-trim craftsmanship. Rising energy costs challenge manufacturing economics, encouraging relocation of labor-intensive assembly to Eastern Europe, but premium OEMs retain local high-precision machining of magnesium steering frames.

Competitive Landscape

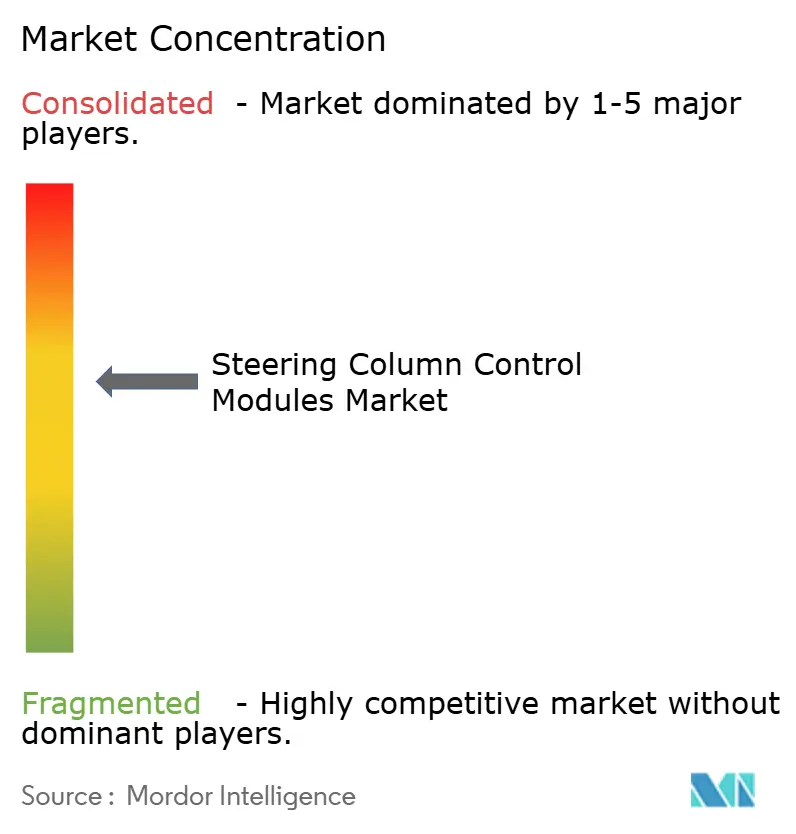

The steering column control modules market shows moderate concentration. Bosch leverages broad electronics expertise to deliver turnkey steer-by-wire stacks complete with driver-monitoring and cyber-security layers, ensuring single-vendor accountability for OEMs. JTEKT couples column modules with rack-drive motors, using system-level sales pitches to defend share against pure electronics newcomers. Together, these players set benchmark specifications that shape RFQ criteria across global vehicle programs.

Technology differentiation now hinges on haptic feedback depth, hands-on detection sensitivity, and secure over-the-air update frameworks. Nexteer invests in subscription-based steering modes, planning future revenue from downloadable handling profiles after initial vehicle sale. ZF Lifetec focuses on rim-retract concepts that enable Level 3 cabin reconfiguration, courting luxury OEMs seeking design freedom. Each leader channels R&D into redundancy architectures that can pass ASIL-D targets without excessive weight or cost.

Consolidation is active downstream as smaller plastics and switch specialists struggle with the capital burden of cyber-secure microcontrollers. ZF Rane’s acquisition of a domestic wheel plant in 2024 typifies vertical-integration moves that shore up supply certainty while lowering landed cost for growth regions. Suppliers emphasizing modular, cross-platform designs gain negotiation leverage because one assembly can serve multiple vehicle lines. Overall, competitive dynamics reward firms that marry mechanical craftsmanship with electronics, software, and compliance know-how, positioning them to capture rising steer-by-wire demand and aftermarket replacement cycles.

Steering Column Control Modules Industry Leaders

Robert Bosch GmbH

JTEKT Corporation

Nexteer Automotive

NSK Ltd.

ThyssenKrupp AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ZF Lifetec unveiled a folding-rim steering wheel that retracts into the dashboard within two seconds, enabling smoother Level 3 handover.

- August 2025: Marquardt introduced multi-zone hands-on detection employing capacitive grids for higher precision in driver monitoring.

- February 2025: ZF began series production of steer-by-wire actuators for NIO, supplying both wheel and gear modules plus safety software.

Global Steering Column Control Modules Market Report Scope

| Infotainment Control |

| Cruise Control |

| Communication Control |

| ADAS Integration |

| On the Steering Wheel | Sound Control |

| Airbags | |

| Around/Below Steering Wheel | Stalk Levers: Wiper Control |

| Stalk Levers: Headlight Control |

| Manual Steering |

| Hydraulic Power Steering (HPS) |

| Electric Power Steering (EPS) |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses and Coaches |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Functionality | Infotainment Control | |

| Cruise Control | ||

| Communication Control | ||

| ADAS Integration | ||

| By Component Position | On the Steering Wheel | Sound Control |

| Airbags | ||

| Around/Below Steering Wheel | Stalk Levers: Wiper Control | |

| Stalk Levers: Headlight Control | ||

| By Steering Type | Manual Steering | |

| Hydraulic Power Steering (HPS) | ||

| Electric Power Steering (EPS) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| Buses and Coaches | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the steering column control modules market?

The steering column control modules market size is USD 17.18 billion in 2025.

Which segment holds the largest functionality share?

ADAS integration leads with 36.51% revenue thanks to Level 2+ autonomy adoption.

Which region is growing fastest?

Asia-Pacific is forecast at a 9.09% CAGR through 2030 due to China’s EV boom.

How will steer-by-wire influence future demand?

Steer-by-wire is projected to grow at 15.83% CAGR as premium launches prove reliability and unlock new cabin layouts.

What is driving aftermarket growth?

Longer vehicle lifespans and demand for retrofit convenience features push the aftermarket channel at a 9.51% CAGR.

Page last updated on: