Stroke Post Processing Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

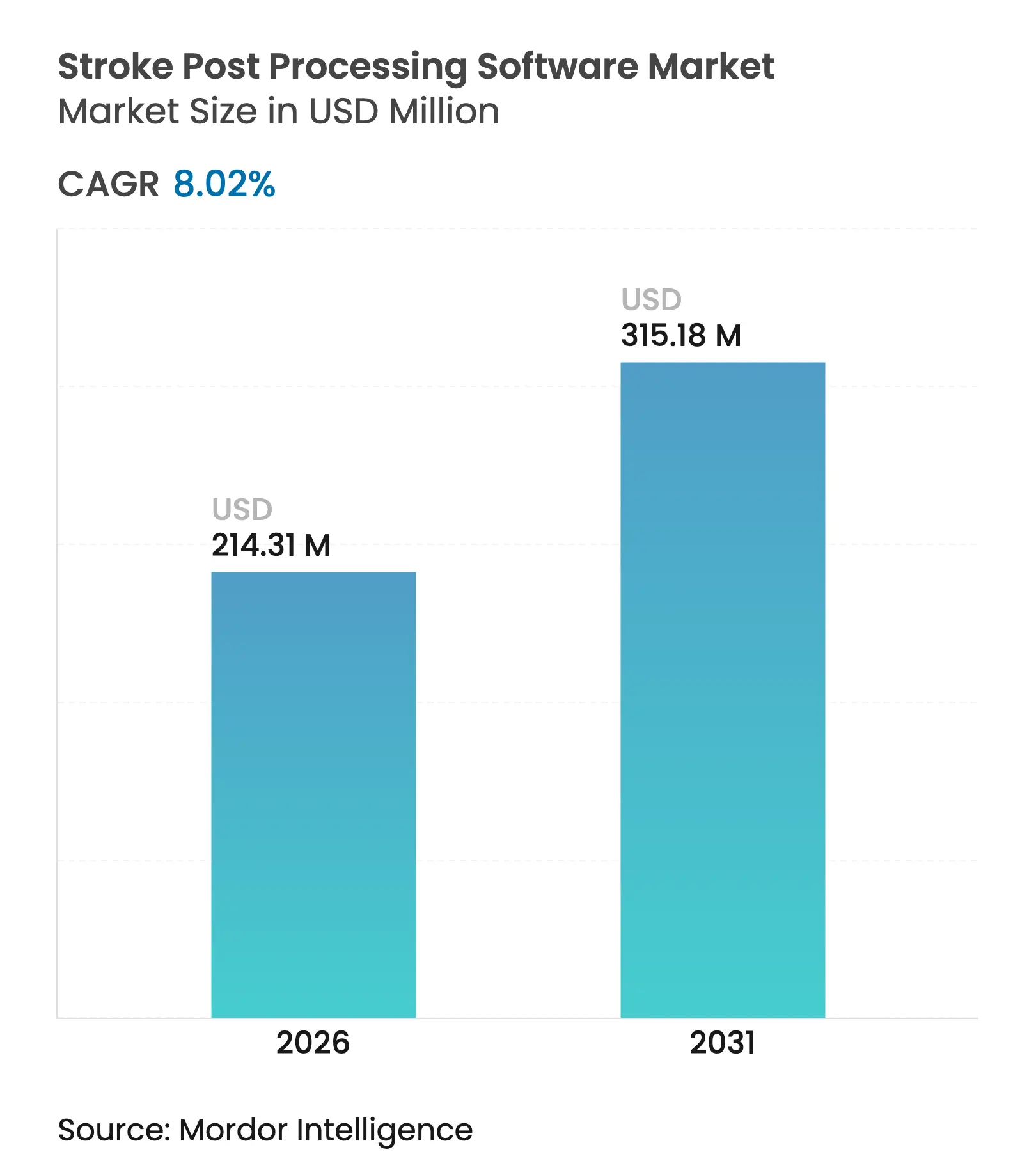

| Market Size (2026) | USD 214.31 Million |

| Market Size (2031) | USD 315.18 Million |

| Growth Rate (2026 - 2031) | 8.02 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Stroke Post Processing Software Market Analysis by Mordor Intelligence

The stroke post processing software market size in 2026 is estimated at USD 214.31 million, growing from 2025 value of USD 198.39 million with 2031 projections showing USD 315.18 million, growing at 8.02% CAGR over 2026-2031. Rising global stroke incidence, rapid integration of artificial intelligence in neuroimaging workflows, and the push to compress door-to-needle times underpin this expansion. Regulatory momentum is equally pivotal; the United States Food and Drug Administration (FDA) has already authorized 22 AI or machine-learning tools dedicated to stroke diagnosis and rehabilitation, signalling unprecedented clinical validation of these solutions[1]Semantic Scholar, “FDA-cleared AI/ML devices for stroke care,” semanticscholar.org. Cloud deployment models widen access by lowering on-premise infrastructure barriers, while hybrid edge-cloud architectures tackle latency and data-sovereignty concerns. Meanwhile, venture capital inflows toward specialist vendors, as evidenced by RapidAI’s USD 75 million Series C funding round, accelerate commercialisation and global roll-outs.

Key Report Takeaways

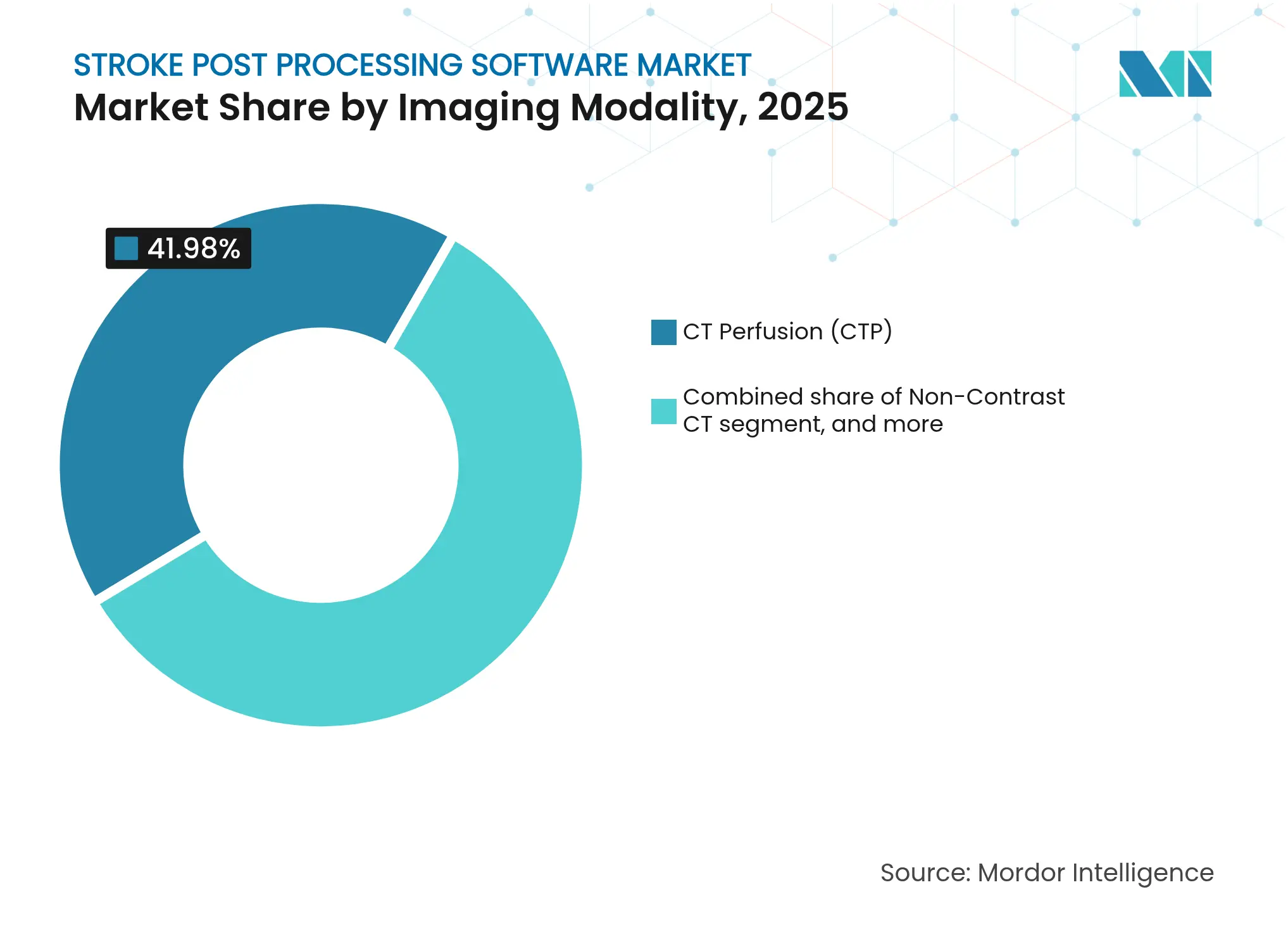

- By imaging modality, CT perfusion held 41.98% of stroke post processing software market share in 2025; hybrid/multi-modal platforms are forecast to grow at a 10.12% CAGR through 2031.

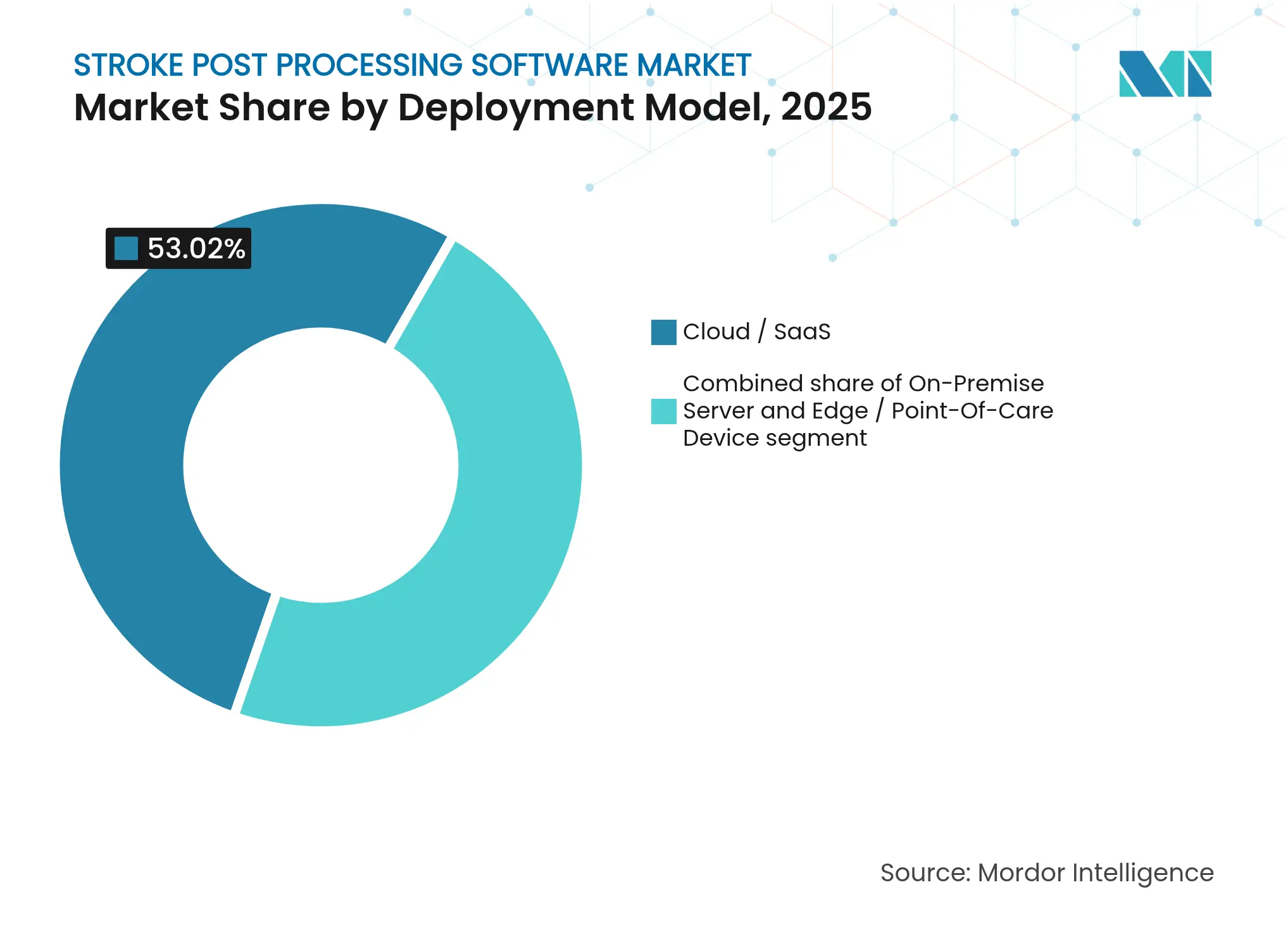

- By deployment model, cloud/SaaS commanded 53.02% of the stroke post processing software market size in 2025 and is expanding at a 10.28% CAGR to 2031.

- By end-user, comprehensive stroke centers captured 47.76% of stroke post processing software market share in 2025, while teleradiology service providers record the highest projected CAGR at 11.09% until 2031.

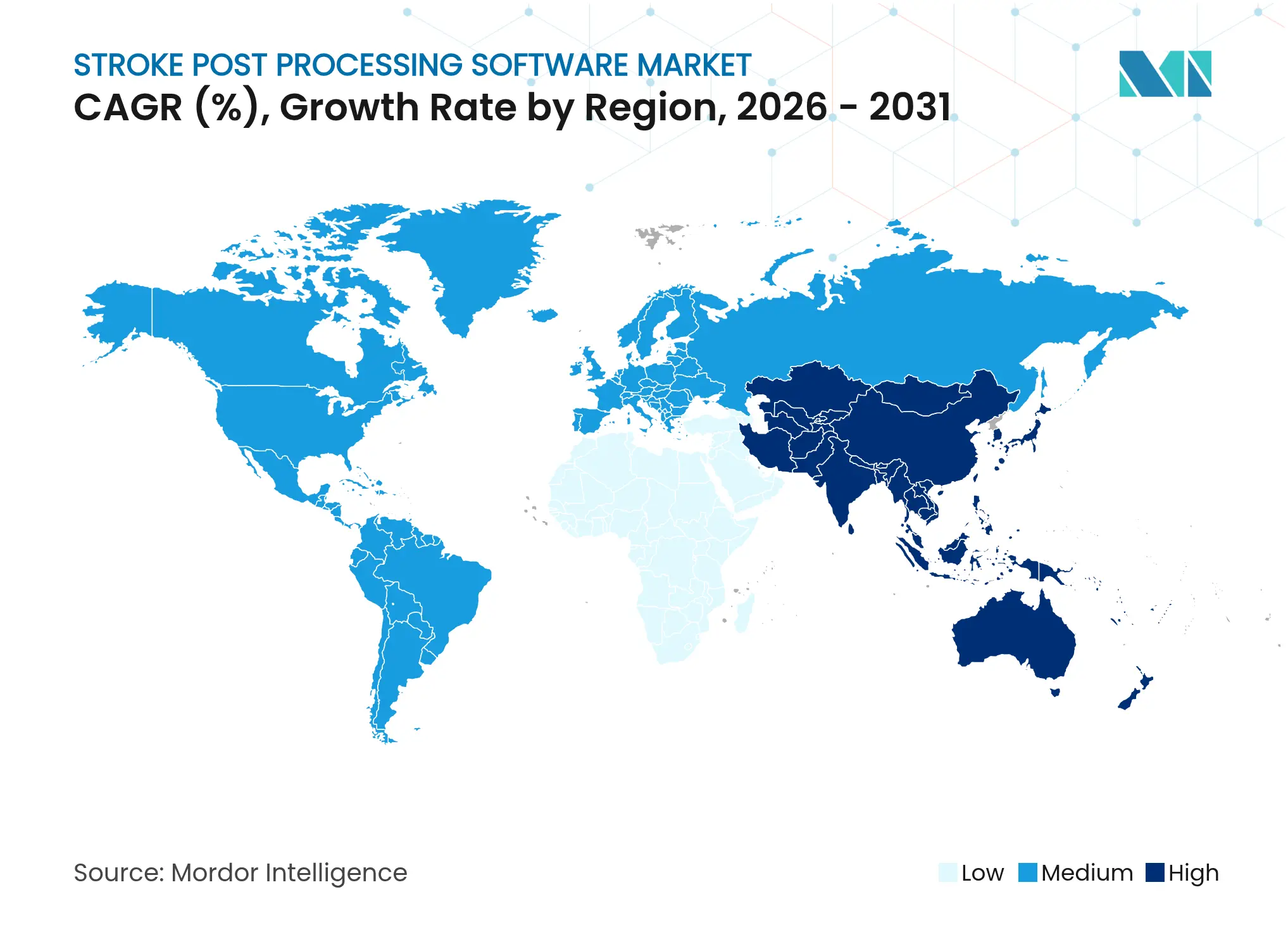

- By geography, North America led with 42.71% revenue share in 2025; Asia-Pacific is the fastest-growing region at 9.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stroke Post Processing Software Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising stroke incidence and aging population Rising stroke incidence and aging population | +2.1% | Global, strongest in Asia-Pacific and North America | Long term (≥ 4 years) | % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Global, strongest in Asia-Pacific and North America | Impact Timeline:Long term (≥ 4 years) |

Increasing demand for rapid neuroimaging workflow efficiency Increasing demand for rapid neuroimaging workflow efficiency | +1.8% | Global, acute in comprehensive stroke centers | Medium term (2-4 years) | |||

Favorable reimbursement policies for AI-enabled imaging solutions Favorable reimbursement policies for AI-enabled imaging solutions | +1.5% | North America & EU, expanding in Asia-Pacific | Medium term (2-4 years) | |||

Expansion of telestroke and hub-and-spoke care models Expansion of telestroke and hub-and-spoke care models | +1.2% | Global, emphasis on rural and underserved regions | Long term (≥ 4 years) | |||

Integration of AI with multi-modality imaging platforms Integration of AI with multi-modality imaging platforms | +0.9% | Global, led by advanced markets | Short term (≤ 2 years) | |||

Growing investments from venture capital and strategic vendors Growing investments from venture capital and strategic vendors | +0.6% | North America & EU, increasing in Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Stroke Incidence and Aging Population

China recorded 2.77 million new ischemic stroke cases in 2025, illustrating the demographic pressure fueling demand for advanced imaging solutions. In the United States, stroke already imposes a USD 43 billion annual economic burden, intensifying the need for workflow optimisation across health systems[2]American Heart Association, “Heart Disease & Stroke Statistics 2025 Update,” heart.org. AI algorithms capable of processing head scans within 20 seconds, such as Avicenna.ai’s CINA Head, demonstrate how technology directly alleviates workforce bottlenecks. The convergence of higher life expectancy, urban lifestyles, and rising cardiovascular risk factors ensures sustained adoption of the stroke post processing software market across mature and emerging economies alike.

Increasing Demand For Rapid Neuroimaging Workflow Efficiency

Time-dependent stroke therapy has shifted strategic priorities from hardware procurement to comprehensive workflow integration. Clinical data show that AI-guided care cuts the risk of new vascular events within three months by 25.6% compared with standard pathways. Brainomix’s 360 Stroke platform boosted mechanical thrombectomy utilisation by 50% and reduced inter-facility transfer delays by nearly 50 minutes. Mobile stroke units equipped with AI detection of large-vessel occlusion reach 0.80 area under the curve accuracy, extending advanced diagnostics into pre-hospital environments. Collectively these findings reinforce the stroke post processing software market as an indispensable enabler of evidence-based, speed-centred clinical pathways.

Favorable Reimbursement Policies For AI-Enabled Imaging Solutions

Local Coverage Determinations by US Medicare Administrative Contractors now reimburse AI-augmented CT perfusion analyses performed in certified stroke centers, formalising the technology’s medical necessity[3]Centers for Medicare & Medicaid Services, “Local Coverage Determination for Perfusion Imaging,” cms.gov. The FDA has created new product codes for AI-based stroke detection, smoothing market access for innovators. Europe’s evolving reimbursement environment ties payment to compliance with the forthcoming EU AI Act, linking revenue opportunities to rigorous quality-management standards. This regulatory-reimbursement alignment strengthens demand certainty for vendors operating in the stroke post processing software industry.

Expansion Of Telestroke And Hub-And-Spoke Care Models

Hub-and-spoke networks using Viz.ai shortened neurointerventionalist notification times from 89 minutes to 54 minutes, demonstrating measurable clinical impact. Hospitals participating in telestroke consortia save on average USD 358,435 per year while improving home-discharge rates. AI-enabled triage automates imaging prioritisation, allowing specialists to remotely manage more patients without compromising accuracy. Emerging health-systems across Asia-Pacific see telestroke as a scalable strategy to overcome specialist shortages, driving outsized regional growth within the stroke post processing software market.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent regulatory validation requirements for AI algorithms Stringent regulatory validation requirements for AI algorithms | -1.4% | North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:North America & EU | Impact Timeline:Medium term (2-4 years) |

High initial implementation and staff training costs High initial implementation and staff training costs | -0.8% | Global, sharper in emerging markets | Short term (≤ 2 years) | |||

Data privacy and cybersecurity concerns in cloud deployments Data privacy and cybersecurity concerns in cloud deployments | -0.7% | Global, especially EU & North America | Short term (≤ 2 years) | |||

Limited interoperability across legacy PACS and IT systems Limited interoperability across legacy PACS and IT systems | -0.6% | Global, most acute in older hospital networks | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Regulatory Validation Requirements For AI Algorithms

FDA clearance for adaptive AI systems often demands multi-site trials spanning 2-3 additional years beyond traditional software evaluations, stretching cash-burn cycles for start-ups. The EU AI Act intensifies scrutiny with mandatory quality-management systems and independent conformity assessments. Data-diversity mandates further elevate costs since algorithms must prove robustness across ethnicities and scanner types. These layers of oversight may inadvertently consolidate the stroke post processing software market around capital-rich incumbents equipped to navigate extended regulatory roadmaps.

High Initial Implementation And Staff Training Costs

Comprehensive stroke centers can invest more than USD 500,000 to licence software, refresh hardware, and train multidisciplinary teams for AI-driven workflows. Interoperability fixes with ageing PACS environments frequently require middleware, adding expense and deployment time. Smaller hospitals and rural facilities shoulder disproportionate cost burdens because they lack high case volumes. Ongoing algorithm maintenance, cybersecurity updates, and compliance audits impose recurring outlays that challenge stretched healthcare budgets, moderating adoption velocity despite clear clinical benefits.

Segment Analysis

By Imaging Modality: Multi-Modal Integration Drives Innovation

CT perfusion controlled 41.98% of stroke post processing software market share in 2025, underlining its pivotal role in selecting candidates for thrombectomy. Hybrid multi-modal platforms are expected to expand at 10.12% CAGR, the fastest of all modalities, as clinicians increasingly demand comprehensive perfusion, angiography, and non-contrast analysis within a single interface. The stroke post processing software market size for multi-modal solutions is projected to accelerate in tandem with the shift toward evidence-based, late-window intervention protocols. RapidAI’s NCCT Stroke became the first FDA-cleared AI tool to detect intracranial hemorrhage and large-vessel occlusion from non-contrast CT, highlighting continued innovation in established modalities.

MRI diffusion-weighted imaging and perfusion-weighted imaging retain key roles for treatment decisions beyond the 6-hour window, while CT angiography enriches vessel-level detail crucial to interventionalists. Unified platforms cut duplicate steps, automatically fuse perfusion and angiography data, and deliver standardised, colour-coded mismatch maps that reduce variability between radiologists. This convergence cements multi-modality integration as a principal growth engine of the stroke post processing software market.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Model: Cloud Dominance Amid Security Evolution

Cloud and software-as-a-service frameworks accounted for 53.02% of the stroke post processing software market size in 2025, growing at 10.28% CAGR as hospitals pursue predictable, subscription-based spending models. Cloud vendors deliver 24/7 processing power, pushing advanced analytics to small facilities without on-premise GPU clusters. The emerging edge-cloud hybrid model lowers real-time latency for mobile stroke units while keeping longitudinal datasets in secure, HITRUST-certified clouds.

Healthcare executives remain wary of cyber threats and data-residency regulations, especially under Europe’s General Data Protection Regulation and the forthcoming EU AI Act. Vendors such as RapidAI address these concerns through zero-trust architectures and single-tenant deployments that segment protected health information at rest and in transit. On-premise servers persist among academic health systems with bespoke IT teams, whereas point-of-care devices gain traction for rural outreach programmes. The diverse deployment landscape ultimately enhances choice, letting organisations align risk appetites with budget constraints across the stroke post processing software market.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Teleradiology Transformation Accelerates

Comprehensive stroke centers held 47.76% of revenue in 2025, benefitting from statutory certification requirements that incentivise acquisition of advanced imaging analytics. Teleradiology service providers, however, exhibit the highest 11.09% CAGR as health systems contract out night-time and overflow interpretations. AI triage tools embedded in teleradiology workflows automatically escalate suspected large-vessel occlusions, enabling subspecialists to prioritise critical cases regardless of location, which directly expands the stroke post processing software market.

Primary stroke centers leverage AI for rapid diagnosis prior to transferring patients to comprehensive hubs, tightening network efficiency. Academic institutions play a dual role—running validation studies that support CE marking and 510(k) submissions while also deploying commercial software for teaching purposes. Mobile stroke units integrate edge processing solutions that feed CT angiography data to remote neurologists within minutes, closing pre-hospital gaps in rural settings. As AI maturity increases, these end-user groups collectively converge on platform solutions rather than standalone modules, reinforcing vendor emphasis on broad clinical-decision ecosystems.

Geography Analysis

North America retained 42.71% of global revenue in 2025, propelled by early regulatory approvals, favourable Medicare reimbursement for CT perfusion analysis, and extensive hospital networks adopting AI triage tools. The region’s research infrastructure is evident in the FDA’s cumulative 692 cleared AI-driven medical devices, many of which target neurovascular applications. Strategic alliances between US cloud leaders and university health-systems accelerate enterprise-scale deployments within the stroke post processing software market.

Asia-Pacific will post the fastest 9.21% CAGR through 2031 thanks to China’s 2.77 million annual stroke caseload, robust telestroke investment, and nearly 600 AI health-tech start-ups developing imaging applications. Japan’s Class III Shonin approval for RapidAI demonstrates regulatory alignment, while Australia and Singapore run national AI funding schemes that subsidise hospital adoption. This ecosystem nurtures local competitors and joint ventures, ensuring sustained momentum for regional vendors.

Europe’s regulatory environment is in flux as the EU AI Act establishes uniform risk-classification and post-market surveillance criteria. Vendors respond with dedicated conformity-assessment pathways to secure CE marking, even as hospital groups pilot AI through horizon-scanning programmes. Telestroke expansion across Germany, Spain, and the Nordics demands interoperable cloud platforms aligned with strict data-protection rules. Meanwhile, the Middle East & Africa and South America experience early-stage but promising growth, driven by public-private partnerships aiming to bridge diagnostic gaps.

Competitive Landscape

Market Concentration

The stroke post processing software market is moderately fragmented, with roughly 20 vendors commanding notable footprints. RapidAI, Viz.ai, and Brainomix collectively hold an estimated 31% share, powered by robust venture funding, multi-modal image-processing pipelines, and extensive hospital contracts. RapidAI’s portfolio spans CT perfusion, NCCT, angiography, and edge-cloud deployment, processing more than 10 million scans globally and offering 98% sensitivity for large-vessel occlusion detection. Viz.ai mirrors this breadth across 1,700 hospitals, capitalising on workflow-integrated messaging that connects radiologists, neurologists, and endovascular teams.

Strategic partnerships heighten competitive intensity. Medtronic aligned with Brainomix to embed AI triage within its neurovascular devices across Western Europe, enabling closed-loop care pathways from detection to treatment. The same device giant also collaborated with Methinks AI for emerging markets, underscoring convergence between device makers and software specialists. In parallel, Siemens Healthineers and GE HealthCare integrate third-party algorithms through open-app stores, positioning themselves as platform orchestrators rather than pure-play competitors.

Price competition remains muted because buyers prioritise accuracy, regulatory pedigree, and service integration over licence discounts. Vendors differentiate via cybersecurity certifications, real-world performance analytics, and turnkey deployment services that include image-routing, RIS integration, and clinician education. White-space opportunities include AI-driven outcome prediction, secondary haemorrhage detection, and personalised rehabilitation planning, each of which could spawn new entrants or acquisition targets inside the stroke post processing software market.

Stroke Post Processing Software Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: RapidAI obtained FDA 510(k) clearance for Lumina 3D, an AI-powered 3D head–neck CTA reconstruction tool delivering images in minutes.

- April 2025: Medtronic partnered with Methinks AI to combine detection software with treatment devices across Central and Eastern Europe, Africa, Turkey, and the Middle East.

- March 2025: Brainomix raised USD 18 million to fund US expansion of its 360 Stroke platform.

- February 2025: Medtronic and Brainomix formalised collaboration to enhance stroke care workflows in Western Europe.

- February 2025: RapidAI published clinical results showing 33% higher large-vessel occlusion detection accuracy than leading peers, with 98% sensitivity.

Table of Contents for Stroke Post Processing Software Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Stroke Incidence and Aging Population

- 4.2.2Increasing Demand for Rapid Neuroimaging Workflow Efficiency

- 4.2.3Favorable Reimbursement Policies for AI-Enabled Imaging Solutions

- 4.2.4Expansion of Telestroke and Hub-And-Spoke Care Models

- 4.2.5Integration of AI With Multi-Modality Imaging Platforms

- 4.2.6Growing Investments from Venture Capital and Strategic Vendors

- 4.3Market Restraints

- 4.3.1Stringent Regulatory Validation Requirements for AI Algorithms

- 4.3.2High Initial Implementation and Staff Training Costs

- 4.3.3Data Privacy and Cybersecurity Concerns in Cloud Deployments

- 4.3.4Limited Interoperability Across Legacy PACS and IT Systems

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat Of New Entrants

- 4.5.2Bargaining Power Of Buyers

- 4.5.3Bargaining Power Of Suppliers

- 4.5.4Threat Of Substitutes

- 4.5.5Intensity Of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Imaging Modality

- 5.1.1Non-Contrast CT

- 5.1.2CT Angiography (CTA)

- 5.1.3CT Perfusion (CTP)

- 5.1.4MRI Diffusion-Weighted Imaging (DWI)

- 5.1.5MRI Perfusion-Weighted Imaging (PWI)

- 5.1.6Hybrid / Multi-Modal

- 5.2By Deployment Model

- 5.2.1On-Premise Server

- 5.2.2Cloud / SaaS

- 5.2.3Edge / Point-Of-Care Device

- 5.3By End-User

- 5.3.1Comprehensive Stroke Centers

- 5.3.2Primary Stroke Centers

- 5.3.3Teleradiology Service Providers

- 5.3.4Academic & Research Institutions

- 5.3.5Mobile Stroke Units

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1RapidAI (ISchemaView)

- 6.3.2Viz.AI

- 6.3.3Siemens Healthineers

- 6.3.4GE HealthCare

- 6.3.5Philips Healthcare

- 6.3.6Canon Medical Systems

- 6.3.7Nico.Lab

- 6.3.8Brainomix

- 6.3.9Aidoc

- 6.3.10Blackford Analysis

- 6.3.11Qure.AI

- 6.3.12MaxQ AI

- 6.3.13Avicenna AI

- 6.3.14Imbio

- 6.3.15Cercare Medical

- 6.3.16Olea Medical

- 6.3.17ImageBiopsy Lab

- 6.3.18Imagia Cybernetics

- 6.3.19Cleerly Health

- 6.3.20ERad (Merge – IBM)

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Stroke Post Processing Software Market Report Scope

As per the scope of this report, Stroke post-processing software allows doctors to make more informed decisions about stroke patients. AI-powered software solutions allow for faster patient transfers. When a blood artery in the brain ruptures and bleeds, or when the blood supply to the brain is cut off, a stroke ensues. Blood and oxygen are unable to reach the brain's tissues due to the rupture or obstruction. Transient ischemic attack, ischemic stroke, and hemorrhagic stroke are the most common three forms of strokes that occur around the world. The Stroke Post Processing Software Market is segmented by Installation (Desktop and Mobile Phones & Tablets), By Modality (CT scan and MRI), By Type (Ischemic Stroke, Hemorrhagic Stroke, and Others), By End user (Hospitals & Clinics, Specialty Centers, and Others) and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.