Demulsifier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 3.57 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

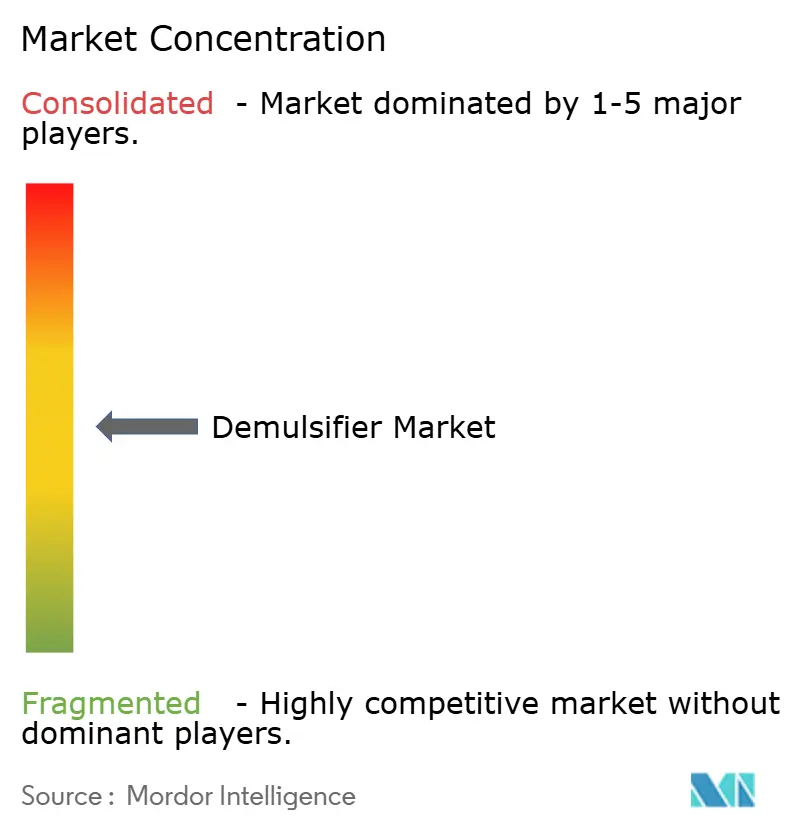

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Demulsifier Market Analysis by Mordor Intelligence

Demulsifier market size in 2026 is estimated at USD 2.93 billion, growing from 2025 value of USD 2.82 billion with 2031 projections showing USD 3.57 billion, growing at 4.01% CAGR over 2026-2031. Expansion stems from the rapid build-out of deepwater production systems and tighter environmental rules that push operators toward higher-efficiency separation chemicals. Growing water-cut levels in mature wells amplify demand for advanced formulations that maintain crude quality while managing produced-water volumes, further propelling the demulsifier market. Competitive activity is intensifying as suppliers race to commercialize biodegradable chemistries and ionic-liquid platforms that align with global sustainability goals. Operators increasingly treat chemicals as strategic levers for field optimization, channeling spending toward products that lower total lifting costs, support emissions compliance, and extend asset life.

Key Report Takeaways

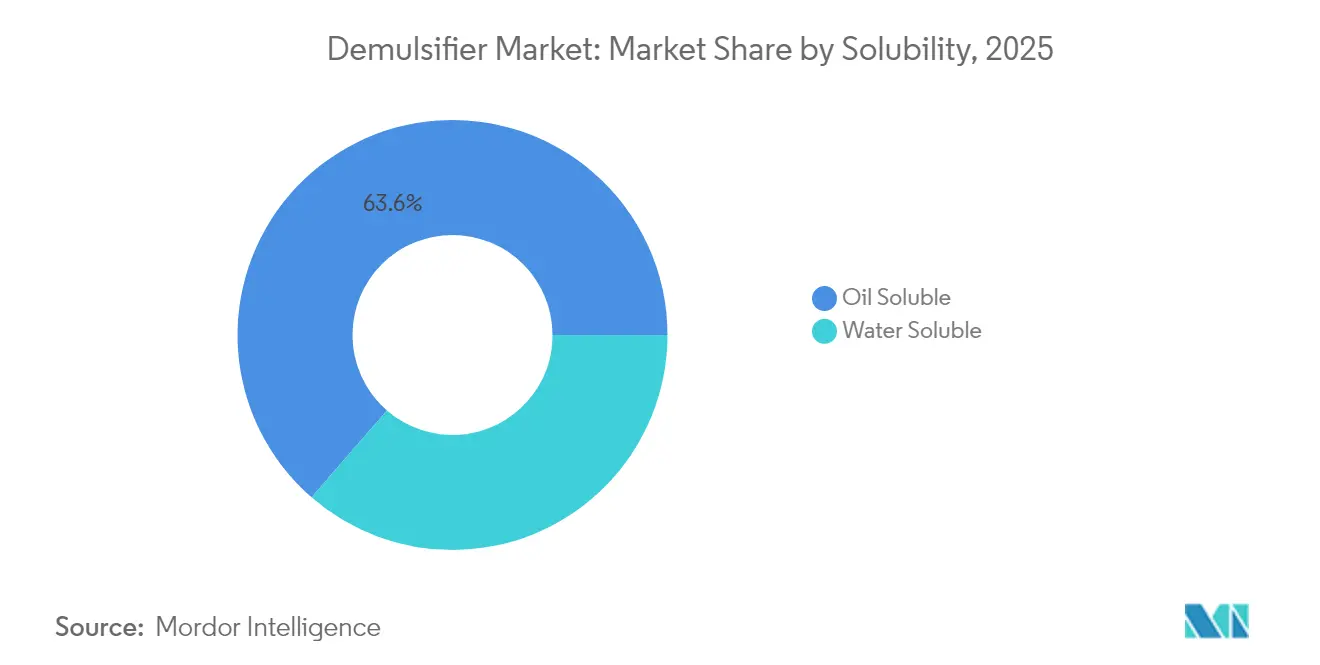

- By solubility, oil-soluble products led with 63.62% of the demulsifier market share in 2025, while water-soluble variants are projected to achieve a 5.78% CAGR through 2031.

- By chemistry, non-ionic reagents held 34.74% revenue in 2025; ionic liquids register the fastest growth at a 6.47% CAGR to 2031.

- By oilfield location, onshore operations commanded 59.51% of the demulsifier market size in 2025, whereas offshore deployments are expanding at 4.97% CAGR over the forecast period.

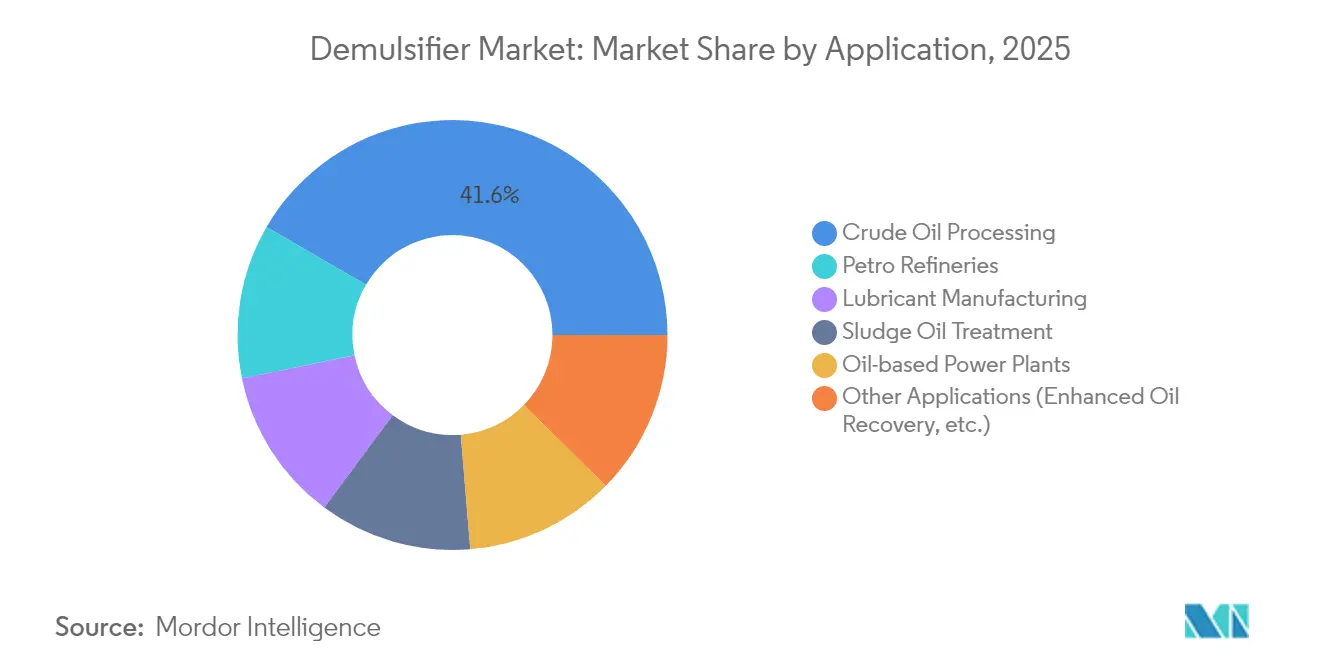

- By application, crude-oil processing captured 41.63% of the demulsifier market size in 2025, while enhanced oil recovery is slated for a 6.62% CAGR up to 2031.

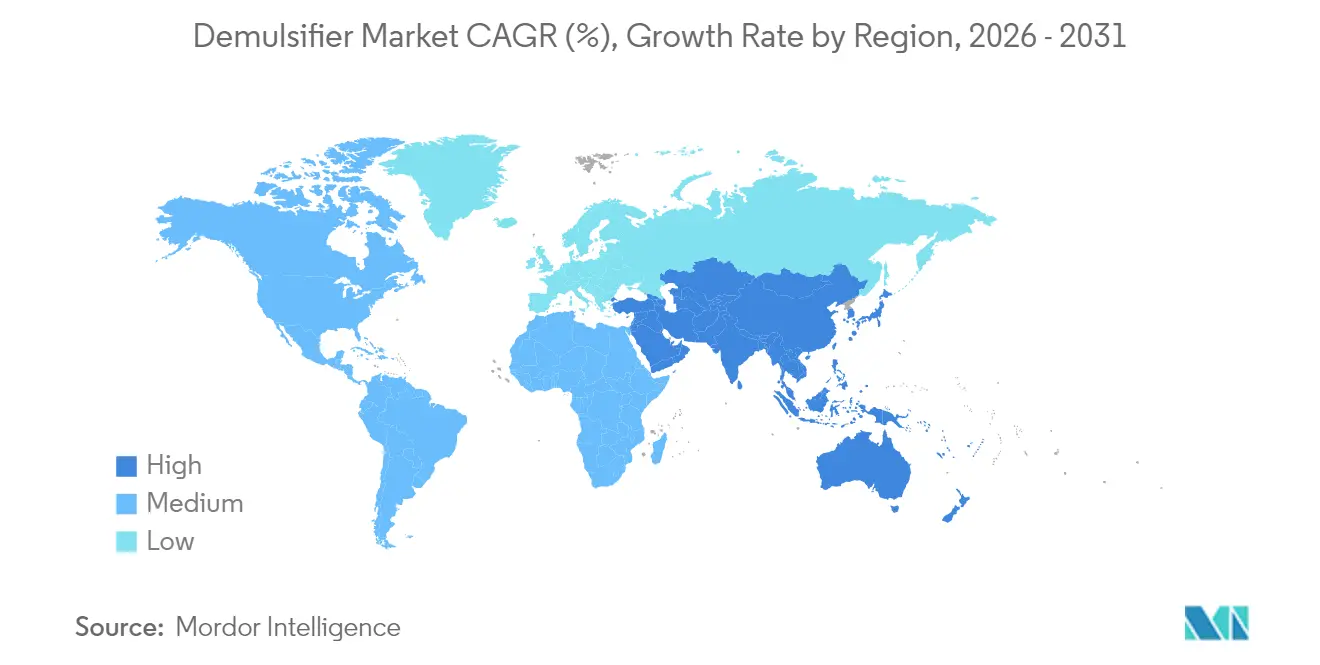

- By geography, North America dominated with 30.24% revenue in 2025; Asia-Pacific exhibits the highest regional growth at 6.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Demulsifier Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain security needs in mature oilfields | +0.8% | Global, concentrated in North America & Middle East | Medium term (2-4 years) |

| Shift toward deeper offshore production & higher water-cut wells | +1.2% | Global offshore regions, led by Gulf of Mexico & North Sea | Long term (≥ 4 years) |

| Stringent water-discharge norms raising separation performance specs | +0.9% | Global, with stricter enforcement in North America & Europe | Short term (≤ 2 years) |

| Growing demand from increasing production of crude oil | +0.7% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| Commercialization of biodegradable polyester-based demulsifiers | +0.4% | Global, early adoption in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-chain Security Needs in Mature Oilfields

Rising water-cut levels in declining reservoirs are forcing producers to adopt tailored separation programs that keep established assets viable. Baker Hughes reports that 70% of global crude flows now originate from mature fields, a share that heightens dependence on high-efficiency demulsifiers[1]Baker Hughes, “Mature Assets Solutions,” bakerhughes.com. Field trials demonstrate that squeeze-treatment packages can lift production between 50% and 200% while bringing per-well chemical costs down to USD 2,500, reinforcing the cost-effectiveness of chemical intervention. Operators view these gains as vital for offsetting lower reservoir pressures and shrinking margins. As a result, demulsifier market demand is tightly linked to life-extension programs for legacy assets. The trend is expected to remain a medium-term growth pillar as global producers optimize brownfield portfolios to hedge against crude-price volatility.

Shift Toward Deeper Offshore Production & Higher Water-Cut Wells

Deepwater investments in the Gulf of Mexico, the North Sea, and pre-salt Brazil place exacting performance requirements on demulsifier technology. Separators on floating production systems must process emulsions that may exceed 80% water content while meeting discharge limits below 40 mg oil per liter[2]Offshore Magazine, “Deepwater Separation Challenges,” offshore-mag.com. The demulsifier market is therefore innovating around formulations that tolerate high pressure and temperature without sacrificing dehydration efficiency. Offshore applications are delivering a 5.08% CAGR as operators pair chemicals with compact coalescers and membrane skids to save topside weight. These projects are inherently long-cycle, locking in durable chemical demand across the life of field. Suppliers that provide proven performance under extreme subsea conditions secure multi-year contracts, anchoring revenue visibility.

Stringent Water-Discharge Norms Raising Separation Performance Specs

Environmental regulators are ratcheting down permissible oil-in-water limits, compelling producers to revisit separation schemes. The U.S. Environmental Protection Agency enforces broad spill-prevention rules under 40 CFR Part 112, pushing discharge targets below 30 mg oil per liter. Canada’s addition of coal tars and PAHs to its toxic-substances list underscores a similar drive toward lower aromatic releases[3]Government of Canada, “Toxic Substances List,” canada.ca. Water-soluble demulsifiers, which enhance downstream clarification, benefit most and are advancing at a 5.90% CAGR. Operators are also scrutinizing chemical biodegradability, prompting a pivot toward polyester-based blends that degrade rapidly yet maintain interfacial activity. Short-term compliance pressures are stimulating a wave of product reformulations that strengthen the demulsifier market entry barriers.

Growing Demand from Increasing Production of Crude Oil

Asia-Pacific refiners chalked up record throughputs of 14.8 million bpd in 2023, a volume that widens the region’s appetite for separation chemicals. The build-out of integrated petrochemical hubs in China and India introduces heavier crude slates that challenge conventional dehydration practices. Specialty-chemical vendors note parallel opportunities in the Middle East, where new refining expansions are tied to hydrocarbon diversification strategies. These capacity hikes underpin the 6.67% regional CAGR and reinforce the demulsifier market’s cyclical linkage to crude-production growth. Medium-term prospects remain upbeat as Southeast Asian projects move from FEED to execution, driving chemical demand throughout the late 2020s.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil prices curbing CapEx on production chemicals | -1.1% | Global, most pronounced in North America & Middle East | Short term (≤ 2 years) |

| Increasing bans on alkyl-phenol ethoxylates | -0.6% | Europe & North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Scale-up challenges for ionic-liquid formulations | -0.3% | Global, concentrated in advanced technology markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil Prices Curbing CapEx on Production Chemicals

The International Energy Forum predicts a 1.4 million bpd surplus in 2025, a scenario that pressures operators to defer discretionary chemical spend. When spot prices slide below breakeven thresholds, procurement teams prioritize base-load volumes and renegotiate price-indexed contracts that compress supplier margins. Specialty blends carrying higher unit costs, including ionic liquids, become prime targets for short-term cutbacks. This cyclical pullback is the strongest near-term headwind and subtracts 1.1 percentage points from the projected CAGR. Although chemical adoption rebounds with pricing recovery, the restraint underscores the demulsifier market’s sensitivity to macro-oil cycles.

Increasing Bans on Alkyl-Phenol Ethoxylates

Endocrine-disruption data have prompted regulatory agencies to phase out alkyl-phenol ethoxylates. The European Chemicals Agency classifies several phenolic surfactants as substances of very high concern, spurring multi-year reformulation programs across the supplier base. Similar draft rules in the United States are under review, portending wider restrictions. Manufacturers must run parallel production during the transition, inflating operating costs and temporarily limiting product availability. Medium-term headwinds will ease once new chemistries achieve full commercial scale, yet the reformulation burden weighs on the demulsifier industry’s near-term growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solubility: Water Treatment Drives Soluble Growth

Oil-soluble products controlled 63.62% of 2025 revenues, underscoring their entrenched role in primary dehydration units and separator train injections. Their dominance is rooted in quick interfacial action that expedites free-water drop-out at the wellhead, a critical step in minimizing corrosion and desalter upsets. Water-soluble alternatives, though smaller today, are scaling quickly at a 5.78% CAGR as operators expand produced-water treatment infrastructure to meet stricter disposal limits. This surge aligns with the demulsifier market’s pivot toward holistic water management rather than singular focus on crude quality.

Second-generation membrane-bioreactor systems increasingly specify soluble demulsifiers to pre-condition feed streams, boosting oil-in-water polishing stages. Hybrid treatment trains employing coalescing media and polymeric adsorbents gain efficiency when soluble chemistries improve emulsion destabilization upstream. Consequently, suppliers broaden portfolios beyond conventional resin bases to polyethylene glycol, polyetheramine, and biodegradable ester backbones that perform across varying pH windows. The trend signals a gradual but unmistakable shift in specification patterns that will reshape future demulsifier market demand profiles.

By Chemistry: Ionic Liquids Challenge Traditional Formulations

Non-ionic blends held 34.74% revenue in 2025, prized for versatility across crude grades from light tight oil to extra-heavy. They integrate seamlessly with corrosion inhibitors, scale squeezes, and paraffin solvents, simplifying chemical management for multi-well pads. Ionic liquids, in contrast, are the breakout story with a 6.47% CAGR, buoyed by laboratory data showing superior stability under reservoir conditions up to 200 °C and salinities above 200,000 ppm.

Commercial momentum is tempered by cost barriers and supply-chain immaturity, yet pilot successes in the South China Sea and Gulf of Mexico underscore their potential. Amphoteric and cationic products retain niche appeal where charge-based separation mechanisms yield higher efficiency in acidic crudes. Meanwhile, anionic surfactants see steady demand in refinery desalter circuits, where their compatibility with brine desalting aids in chloride removal. Over the coming decade, competitive edge will hinge on suppliers’ ability to hybridize ionic-liquid functionalities with non-ionic cost profiles, a prospect that could further disrupt the demulsifier market.

By Oilfield Location: Offshore Technology Demands Drive Innovation

Onshore fields retained 59.51% revenue in 2025 thanks to massive shale plays across North America and conventional output in the Middle East. Their chemical-consumption patterns are mature, emphasizing cost-per-barrel efficiencies and ease of logistics for pad-based delivery systems. Offshore projects, however, represent the innovation frontier as deepwater producers face severe space and weight constraints on floating platforms. Offshore volumes are expanding at 4.97% CAGR, introducing complex emulsions that test conventional chemistries.

High-pressure, high-temperature conditions in pre-salt reservoirs demand demulsifiers that withstand 15,000 psi while preserving droplet coalescence rates. Operators also seek formulations compatible with monoethylene glycol, hydrate inhibitors, and topside foam-control chemicals to avoid cross-treatment interference. Successful deployments in the Campos Basin demonstrate how bespoke blends can maintain production uptime, illustrating why offshore applications will shape the future requirements of the demulsifier market.

By Application: Enhanced Recovery Accelerates Chemical Demand

Crude-oil processing remains the cornerstone application at 41.63% of 2025 sales, encompassing wellhead separation, transportation tank treatments, and refinery desalting. Operators value reliable break times and low basic sediment and water readings to avoid downstream fouling. Enhanced oil recovery constitutes the fastest-growing use case at 6.62% CAGR as alkali-surfactant-polymer floods gain traction in aging reservoirs. Laboratory studies show displacement efficiencies improving by 19% when demulsifiers are optimized alongside surfactant packages.

Chemical EOR campaigns prioritize demulsifiers that mitigate injectant back-production issues while safeguarding treater performance. Petrochemical refineries, sludge-oil remediation, and lubricant blending supply steady if modest demand streams that diversify supplier revenue. Over the forecast horizon, integrated EOR programs will account for a growing share of the demulsifier market as producers chase incremental recovery factors to balance investment discipline and reserve replacement pressures.

Geography Analysis

North America led the global demulsifier market with 30.24% revenue in 2025, anchored by prolific shale liquids output and complex Gulf of Mexico deepwater assets. Operators in the United States are set to boost 2025 production, reinforcing a steady draw on separation chemicals even as ESG mandates tighten discharge permits. Canada’s heightened scrutiny of PAHs further nudges suppliers toward eco-friendly chemistries that avoid phenolic precursors. Regional service companies partner with chemical majors to deliver bundled optimization offerings, embedding demulsifier selection into holistic water-management strategies as pad counts rise across the Permian and Montney formations.

Asia-Pacific stands out with a 6.52% CAGR, underpinned by China’s record 14.8 million bpd refining throughput and sustained petrochemical investment across Zhejiang and Guangdong clusters. Integrated complexes amplify demulsifier usage by processing heavier crudes and resid-based feeds that generate stable emulsions. Southeast Asia’s chemical market is poised to nearly double to USD 448 billion by 2030, drawing specialty-chemical players into Vietnam, Indonesia, and Malaysia. India’s expanded refinery slate and coal-bed methane developments present additional volume upside as local operators adopt advanced separation packages to meet Bharat Stage-VI fuel standards.

Europe and the Middle East & Africa display mature yet resilient demand, guided by stringent REACH compliance and large-scale brownfield upgrades in the North Sea and Arabian Peninsula. European operators prioritize biodegradable demulsifiers to satisfy Water Framework Directive thresholds, whereas Middle Eastern producers focus on reducing water-handling costs in high-salinity reservoirs. South America offers moderate growth led by Brazil’s expanding pre-salt portfolio and Argentina’s unconventional drives. Collectively, geographic variations reveal how local production profiles, regulatory regimes, and investment cycles shape the trajectory of the demulsifier market.

Competitive Landscape

The demulsifier market features moderate fragmentation, with diversified chemical conglomerates sharing space with niche oilfield service specialists. Baker Hughes, BASF, Clariant, and Halliburton leverage global logistics and wellsite technical staff to secure master-service agreements across supermajor portfolios. Their integrated offerings bundle demulsification with flow-assurance, corrosion inhibition, and production-optimization analytics, raising switching costs for operators. Competitive edge now hinges on data-backed evidence of value creation, driving suppliers to invest in real-time emulsion-quality monitoring and AI-driven dosage optimization.

Pricing pressure remains acute in commoditized onshore basins, forcing suppliers to pursue efficiency gains in supply logistics and raw-material sourcing. Offshore and EOR markets, by contrast, reward high-specification performance and technical support, allowing premium pricing. Intellectual-property portfolios centered on novel chemistries and application-specific formulations serve as key barriers to entry. Vendors that demonstrate robust ESG credentials and transparent stewardship metrics further differentiate themselves, shaping procurement decisions as operators align supply chains with corporate sustainability targets.

Demulsifier Industry Leaders

Baker Hughes Company

Halliburton Company

BASF

Clariant

SLB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: In Brazil's Campos Basin, at a depth of 1,400 meters, an operator needed a subsea demulsifier that met stringent safety standards and was fully compatible with MEG. SLB responded by developing DS-83066, a solution that enhanced production stability, strengthened well integrity, and optimized topside operations under deep-water conditions.

- December 2023: New wells altered crude composition on the Norwegian continental shelf, reducing demulsifier efficiency and overloading separators. SLB developed a custom-engineered EB-82116 emulsifier that addressed diverse crude challenges, reduced water in oil (WIO) and oil in produced water, and lowered operating costs by minimizing demulsifier usage.

Global Demulsifier Market Report Scope

The report on the demulsifier market includes:

| Water Soluble |

| Oil Soluble |

| Anionic |

| Cationic |

| Non-ionic |

| Amphoteric |

| Ionic Liquids |

| Onshore |

| Offshore |

| Crude Oil Processing |

| Petro Refineries |

| Sludge Oil Treatment |

| Oil-based Power Plants |

| Lubricant Manufacturing |

| Other Applications (Enhanced Oil Recovery, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa |

| By Solubility | Water Soluble | |

| Oil Soluble | ||

| By Chemistry | Anionic | |

| Cationic | ||

| Non-ionic | ||

| Amphoteric | ||

| Ionic Liquids | ||

| By Oilfield Location | Onshore | |

| Offshore | ||

| By Application | Crude Oil Processing | |

| Petro Refineries | ||

| Sludge Oil Treatment | ||

| Oil-based Power Plants | ||

| Lubricant Manufacturing | ||

| Other Applications (Enhanced Oil Recovery, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

Key Questions Answered in the Report

What is the current Demulsifier Market size?

The demulsifier market size stands at USD 2.93 billion in 2026 and is projected to climb to USD 3.57 billion by 2031 at a 4.01% CAGR.

Which region leads global demand for demulsifiers?

North America holds the largest regional share at 30.24% due to intensive shale production and Gulf of Mexico deepwater projects.

Why are water-soluble demulsifiers growing faster than oil-soluble types?

Stricter produced-water discharge limits favor water-soluble chemistries that excel in polishing steps, pushing their CAGR to 5.78% through 2031.

How will deepwater expansion affect demulsifier consumption?

Deepwater fields require high-performance formulations that withstand extreme conditions, supporting a 4.97% CAGR for offshore applications and driving product innovation.

Page last updated on: