Coupling Agent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

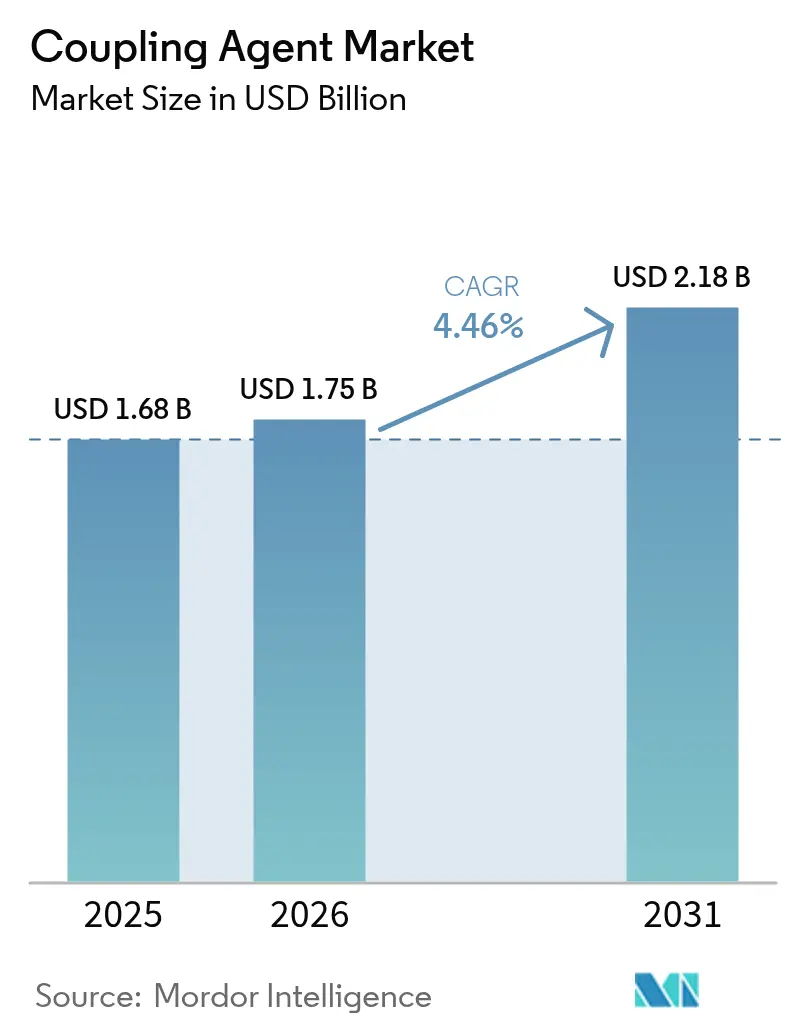

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coupling Agent Market Analysis by Mordor Intelligence

The Coupling Agent Market size was valued at USD 1.68 billion in 2025 and estimated to grow from USD 1.75 billion in 2026 to reach USD 2.18 billion by 2031, at a CAGR of 4.46% during the forecast period (2026-2031). Rising demand for multi-material designs in automotive, construction, and electronics manufacturing continues to cement coupling agents as performance-critical additives rather than commodity chemicals. Lightweight vehicle architectures, green tires, solvent-free construction sealants, and advanced semiconductor packages all rely on specialized interfacial chemistry, keeping the coupling agents market resilient despite raw-material cost swings. Competitive intensity stays moderate because no single supplier controls a dominant share, yet scale economies and niche formulation expertise both create viable strategic paths. Regional growth remains skewed toward Asia-Pacific, where expanding tire and automotive output intersects with a vast local consumer base to reinforce capacity-driven cost advantages.

Key Report Takeaways

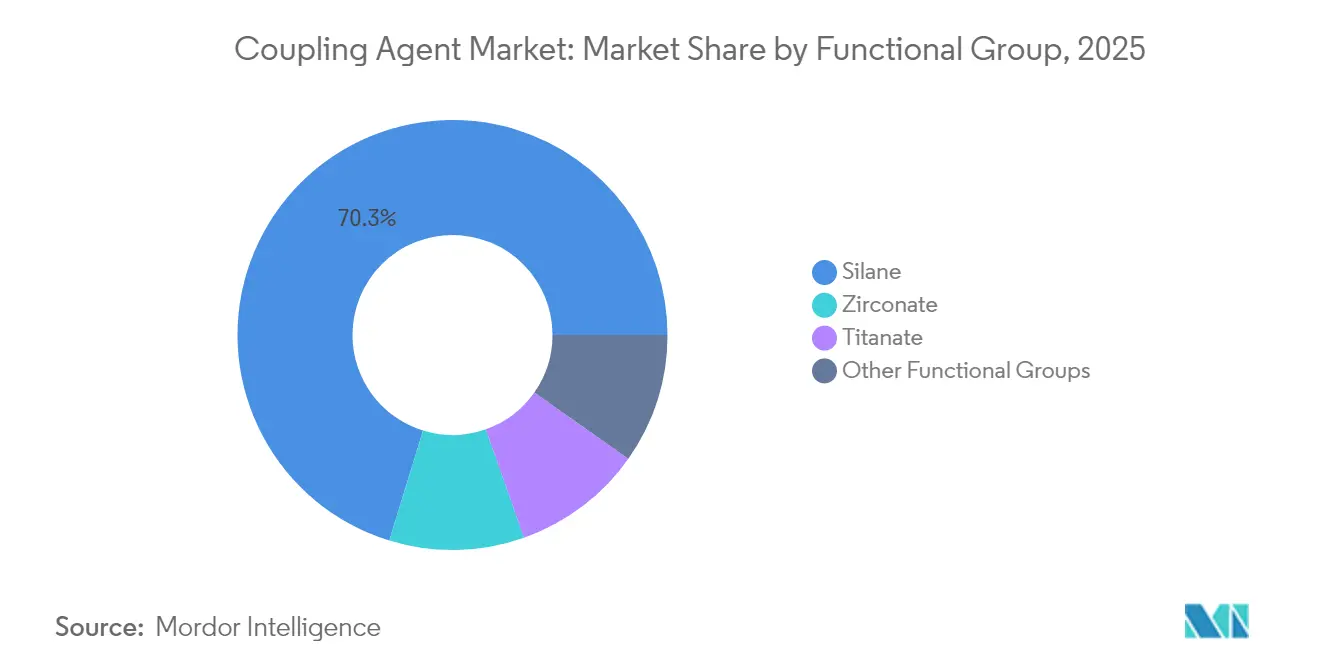

- By functional group, silane chemistry led with 70.25% revenue share in 2025, while zirconate variants posted the fastest 4.73% CAGR through 2031.

- By application, rubber and plastics captured 46.10% of the coupling agents market share in 2025 and are projected to expand at a 4.62% CAGR to 2031.

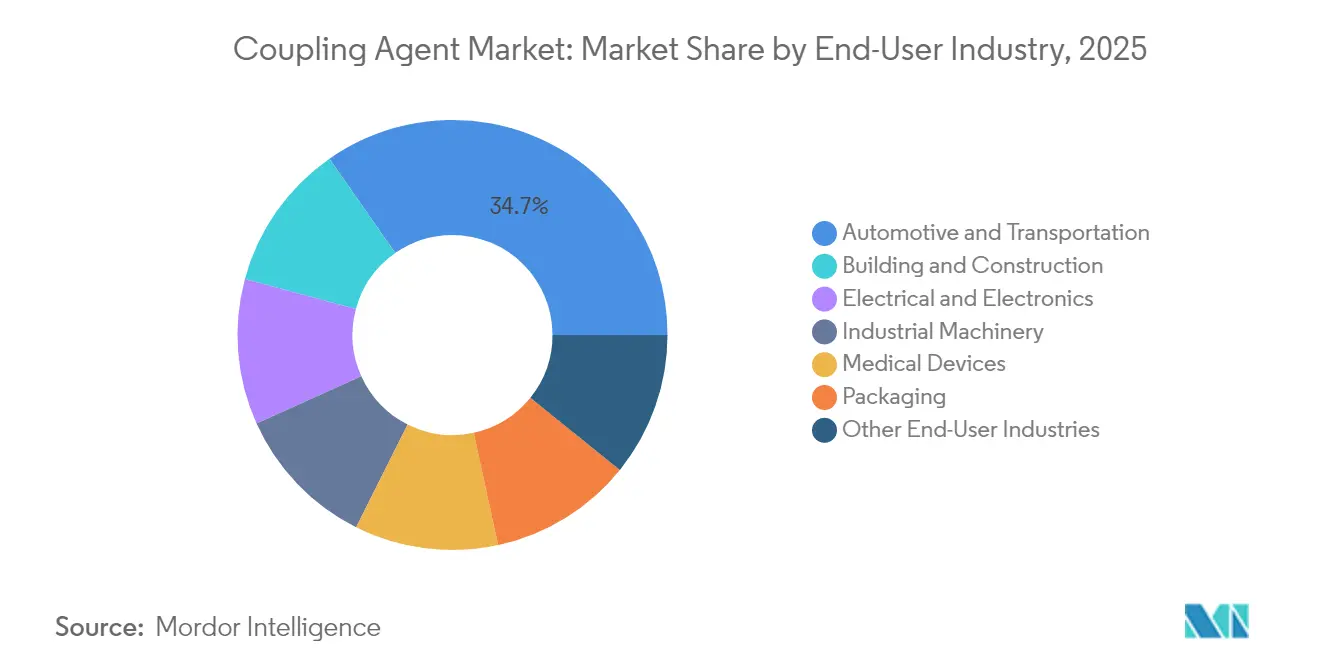

- By end-user, automotive and transportation held 34.70% of the coupling agents market size in 2025 and will advance at the highest 4.78% CAGR over the forecast horizon.

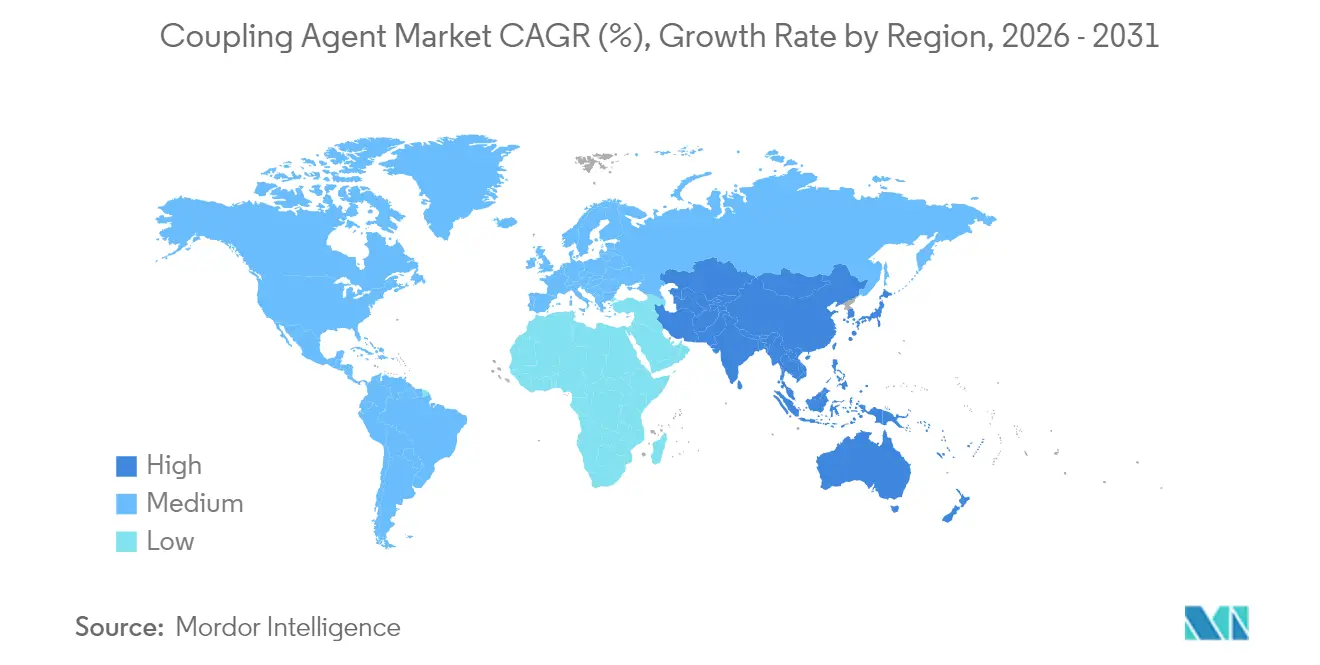

- By geography, Asia-Pacific dominated with 38.30% share in 2025 and is set to grow at a 4.67% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coupling Agent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-tire demand for silica–silane technology | +1.2% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| Lightweight plastics & composites adoption | +0.9% | North America & Europe automotive, APAC aerospace | Long term (≥ 4 years) |

| Construction sealants & adhesives boom | +0.7% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Electronics miniaturization & moisture protection | +0.6% | APAC electronics hubs, expanding to global | Medium term (2-4 years) |

| Shift to solvent-free SMP adhesives | +0.4% | Europe and North America regulatory-driven | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweight plastics & composites adoption

Automotive OEMs targeting stringent fleet-average CO₂ caps increasingly rely on carbon-fiber-reinforced plastics, aluminum–polymer hybrids, and multi-material joints that must survive vibration, salt-spray, and temperature cycles. The U.S. Department of Energy’s 2025 harsh-environment materials roadmap identifies functional surface treatments—including silane-anchored primers—as a cross-cutting enabler for next-generation chassis and battery enclosures[1]U.S. Department of Energy, “National Landscape of High-Impact Crosscutting Opportunities for Next-Generation Harsh-Environment Materials,” energy.gov. Additive-manufactured aerospace brackets fabricated via direct ink writing posted 39% tensile-stiffness gains once silane-modified pre-impregnation was introduced, illustrating how 3D-printing unlocks new demand nodes for coupling agents.

Construction sealants & adhesives boom

Rapid urbanization across India, Indonesia, and Vietnam boosts volumes of glazing sealants, structural silicone adhesives, and façade coatings. Moisture-cure polyurethane and silyl-modified polymer (SMP) technologies dominate specifications in tropical climates because silane-terminated networks resist humidity-induced debonding. Huntsman’s 2025 portfolio repositioning toward battery-material and construction-adhesive chemistries exemplifies how integrated producers chase high-growth civil-infrastructure opportunities. Growing adoption of building-information-modeling workflows is spawning smart-adhesive systems that pair mechanical bonding with embedded sensors—a functionality best delivered through tailored coupling-agent interfaces.

Electronics miniaturization & moisture protection

Advanced wafer-level packages in 5G handsets and AI accelerators demand ultrathin, low-dielectric barrier films that combat moisture-induced delamination. Shin-Etsu’s 2024 hydrocarbon resins for 5G substrates highlight the shift toward formulations stable at elevated reflow temperatures yet compatible with intricate copper redistribution layers. Research on chemical-catalytic silicon-dioxide wafer bonding achieved higher adhesion energy at reduced anneal temperatures, confirming the performance leverage of optimized silane chemistries in chiplet architectures. As component footprints shrink, precise control of silane-concentration and condensate cross-link density becomes critical for maintaining dielectric integrity.

Shift to solvent-free SMP adhesives

European VOC ceilings and stricter EPA oversight in North America accelerate the migration from solvent-borne contact cements to moisture-cure SMP systems. Coupling-agent innovation now centers on room-temperature-curing alkoxysilane oligomers that match historical bond strength while eliminating isocyanates and methylene chloride. The South Coast Air Quality Management District’s updated Rule 1151 underscores the compliance pressure pushing formulators toward silane-rich, solvent-free technologies[2]U.S. Environmental Protection Agency, “Methylene Chloride Regulations Update,” epa.gov . Winning suppliers invest in tailor-made silane blends that deliver rapid green strength without sacrificing storage stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silane raw-material price volatility | -0.8% | Global, with Asia-Pacific manufacturing most exposed | Short term (≤ 2 years) |

| Stringent VOC & health regulations | -0.5% | Europe and North America regulatory-driven | Medium term (2-4 years) |

| Titanium-tetrachloride supply risk | -0.3% | Global titanate coupling agent production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Silane raw-material price volatility

Ethyl-silicate and chlorosilane feedstock prices swung up to 18% quarter-on-quarter during 2024 as storms interrupted coastal Chinese production clusters. Limited shelf life forces formulators to run lean inventories, magnifying the cash-flow impact of spot-market spikes. Suppliers with backward integration into silicon-metal smelting or long-term chloride contracts shield margins better, prompting merger interest from commodity siloxane makers aiming to lock in monomer security. Tier-two players lacking hedging tools confront tighter working-capital cycles, which may trigger further consolidation.

Stringent VOC & health regulations

The European Chemicals Agency tightened restrictions on specific organosilicon compounds in 2024, raising compliance-testing costs and lengthening product-registration lead times. In the United States, the EPA broadened methylene-chloride prohibitions, catalyzing a shift to water-based adhesion promoters that often require higher silane-loading levels but deliver lower immediate tack. Smaller formulators must either fund new analytical labs or exit solvent-borne lines, concentrating future growth among well-capitalized multinationals capable of rapid reformulation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functional Group: Silane Chemistry Dominates Multi-Substrate Interfaces

Silane variants commanded 70.25% of 2025 revenue, underlining their unrivaled compatibility with both organic polymers and inorganic fillers. Stable siloxane linkages generated through hydrolysis and condensation let formulators bridge glass, metal, mineral, and polymer surfaces in a single step, driving sustained preference within the coupling agents market. Zirconate molecules, although representing a smaller share, posted the quickest 4.73% CAGR to 2031 because they tolerate service temperatures that cause siloxane scission. Titanate offerings remain niche, often selected for moisture-sensitive filled-polyolefin systems where their chelating action suppresses water-induced viscosity rise.

Recent academic work shows that integrating a 2-pyrone-4,6-dicarboxylic-acid moiety into polydimethylsiloxane chains raises thermal-oxidative resistance by 27 °C while doubling lap-shear strength on aluminum substrates. Such results validate ongoing efforts to extend conventional silane performance envelopes rather than replace the chemistry outright. Consequently, the coupling agents market continues to revolve around incremental silane innovation alongside targeted zirconate deployment in high-heat aerospace and electronics assemblies.

By Application: Rubber & Plastics Lead the Green-Mobility Transition

Rubber and plastics captured 46.10% of 2025 demand and are forecast to grow at a 4.62% CAGR through 2031, confirming their status as the prime engine of coupling agents market expansion. Silica-silane tire treads lower rolling resistance, while silanized glass or basalt fibers reinforce polyamide and polypropylene body-in-white parts without penalizing recyclability. Adhesives and sealants remain the next-largest outlet, propelled by megacity housing starts and retrofits that favor SMP bonding over mechanical fasteners. Paints and coatings rely on organofunctional silanes to enhance adhesion to galvanized steel façades and composite panels.

Additive-manufactured components now form a fast-emerging sub-application: studies revealed that pre-impregnated continuous-fiber filaments coated with 3-aminopropyl-triethoxysilane attained 58% higher tensile strength than unmodified controls, offering designers confidence to substitute 3D-printed parts for milled aluminum in drones and sporting goods. These performance gains ensure an expanding future addressable base for the coupling agents market within high-value engineered plastics.

By End-User Industry: Automotive Continues to Champion Lightweighting

Automotive and transportation accounted for 34.70% of 2025 usage and will record a 4.78% CAGR through 2031, aligning with aggressive fleet electrification and weight-reduction targets worldwide. Battery-electric vehicles incorporate multi-material packs where thermally conductive gap fillers must adhere to both aluminum cases and polymeric dielectric films, an interface managed through epoxy-functional silanes. Electric drivetrains also raise under-hood operating temperatures, accelerating interest in zirconate and phosphate coupling chemistries.

Building and construction forms the second-largest outlet, capitalizing on high-rise glass façades, modular prefabrication, and net-zero retrofits that depend on long-term sealant durability. Electronics demand, while smaller in tonnage, commands premium unit values because each advanced package layer integrates microliter quantities of silane but yields outsized device-level reliability improvements. The push for solid-state batteries, hydrogen fuel cells, and smart-grid hardware further diversifies coupling-agent targets, reinforcing growth prospects for suppliers able to cross-pollinate learning from automotive to energy-storage ecosystems.

Geography Analysis

Asia-Pacific retained a 38.30% share in 2025 and will expand at a 4.67% CAGR to 2031, cementing its position as the epicenter of coupling agents market demand. China produces over half of the world’s radial tires, and every incremental switch from carbon-black to silica–silane tread blends directly amplifies local silane offtake. India’s passenger-car assembly capacity is set to surpass 7 million units by 2027, escalating consumption of adhesion promoters for glass bonding, under-body coatings, and lightweight composites. Japan and South Korea concentrate on high-margin electronics and semiconductor applications where ultra-pure silanes deliver critical moisture barriers. ASEAN economies, especially Vietnam and Thailand, attract foreign direct investment into tire, electronics, and consumer-appliance plants, providing new customer bases for regional silane producers.

North America represents a mature yet technologically dynamic arena. The Inflation Reduction Act’s domestic-content rules incentivize U.S. and Mexican battery and EV OEMs to source local coupling-agent volumes, potentially disrupting Asia-centric supply chains. OEM migration toward resin-transfer-molded pickup frames and carbon-fiber driveshafts pushes demand for aminosilane surface treatments. Canada’s oil-sands equipment and Arctic infrastructure create niche requirements for coupling systems resilient to thermal shock and chemical exposure.

Europe’s stringent Green Deal legislation forces rapid reformulation toward low-VOC, bio-based chemistries. German carmakers lead global deployment of mixed-material battery trays secured with silane-cured adhesives, while Nordic prefabricated timber high-rises rely on silane-enhanced hybrid sealants for fire integrity and moisture control. Eastern European markets enlarge the addressable base as Momentive extended its Safic-Alcan partnership in 2024 to strengthen regional distribution. Collectively, these dynamics ensure that Europe remains both a compliance catalyst and a premium segment within the global coupling agents market.

Competitive Landscape

The coupling agents industry features a moderately fragmented competitive structure. Dow, Evonik, Shin-Etsu, Momentive, and Wacker command multiregional production footprints and integrated siloxane chains, affording them procurement advantages and global technical-service networks. Yet specialty houses such as Gelest or Nusil carve profitable niches through custom organofunctional silanes, ultra-high-purity grades, and collaborative formulation services. Market entry barriers stay moderate: capital outlay for basic silane hydrolyzers is manageable, but replicating multipurpose pilot labs and application-testing centers demands larger investment.

Strategic trends emphasize vertical integration and solution bundling. Evonik’s 2024 merger of its Silica and Silanes activities into Smart Effects targets combined offerings of coupling agents with reinforcing fillers to capture greater share of tire customers’ compound budgets. Wacker collaborates with adhesive formulators to preload silane crosslinkers into SMP polymer drums, simplifying downstream blending and locking in long-term volume contracts. Conversely, innovators explore bio-silane precursors derived from rice-husk ash and sugarcane bagasse to decouple pricing from chlorosilane feedstock volatility.

Coupling Agent Industry Leaders

Momentive

Dow

Evonik Industries AG

Wacker Chemie AG

Shin-Etsu Chemical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Momentive Performance Materials group (Momentive) signed an agreement with Jiangxi Hungpai Material Co., Ltd. (Hungpai) to form a joint venture in Asia. The partnership combines Momentive’s expertise with Hungpai’s silane manufacturing capabilities, including Organofunctional silanes, to address the growing Asia Pacific market and support the coupling agents sector.

- March 2024: Evonik has introduced Silanes to improve adhesives and sealants. Dynasylan Organofunctional silanes act as adhesion promoters or coupling agents, linking inorganic materials (glass, minerals, metals) with organic polymers (thermosets, thermoplastics, elastomers).

Global Coupling Agent Market Report Scope

The Coupling Agent Market report includes:

| Silane |

| Titanate |

| Zirconate |

| Other Functional Groups |

| Rubber and Plastics |

| Adhesives and Sealants |

| Paints and Coatings |

| Fiber Treatment |

| Other Applications |

| Automotive and Transportation |

| Building and Construction |

| Electrical and Electronics |

| Industrial Machinery |

| Medical Devices |

| Packaging |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Functional Group | Silane | |

| Titanate | ||

| Zirconate | ||

| Other Functional Groups | ||

| By Application | Rubber and Plastics | |

| Adhesives and Sealants | ||

| Paints and Coatings | ||

| Fiber Treatment | ||

| Other Applications | ||

| By End-User Industry | Automotive and Transportation | |

| Building and Construction | ||

| Electrical and Electronics | ||

| Industrial Machinery | ||

| Medical Devices | ||

| Packaging | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Coupling Agent Market size?

The coupling agents market size reached USD 1.75 billion in 2026.

What is the expected CAGR for coupling agents through 2031?

Forecasts indicate a 4.46% CAGR over the 2026-2031 period.

Which functional group dominates demand?

Silane chemistry led with 70.25% market share in 2025 due to its broad compatibility.

Why are green tires important for coupling agents suppliers?

Silica–silane tread compounds lower rolling resistance by 15-20%, driving sustained silane consumption.

Page last updated on: