Blast Chillers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

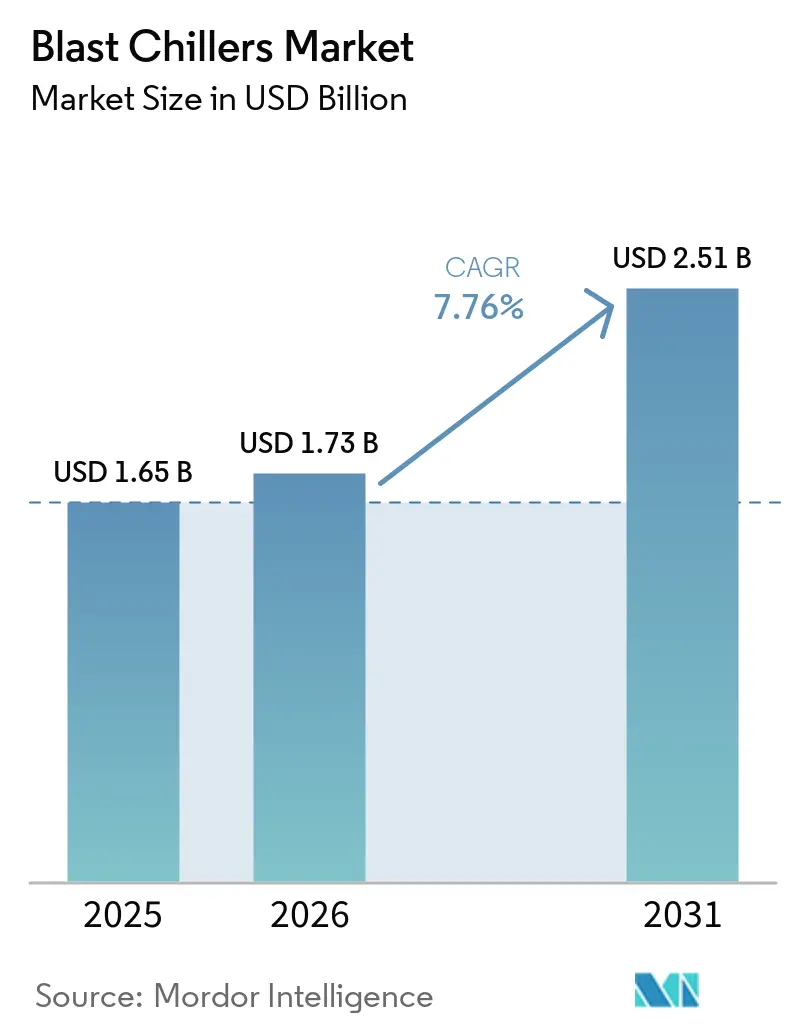

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

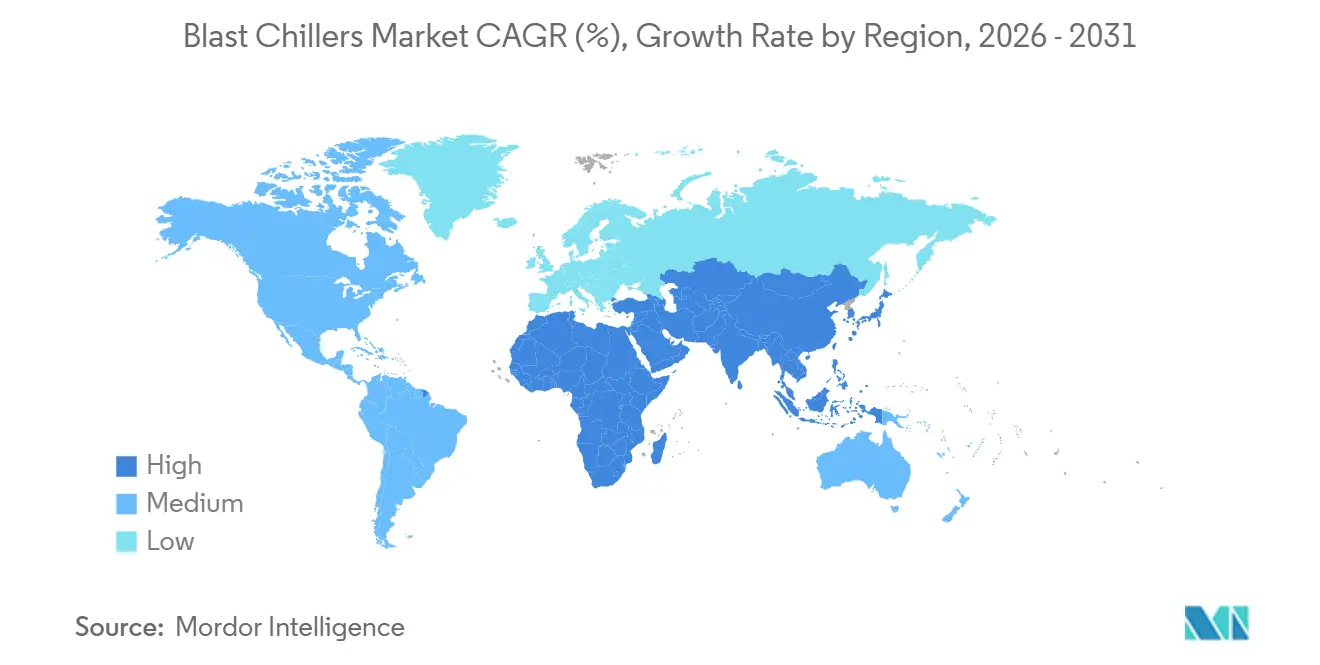

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blast Chillers Market Analysis by Mordor Intelligence

The blast chillers market size is expected to grow from USD 1.65 billion in 2025 to USD 1.73 billion in 2026 and is forecast to reach USD 2.51 billion by 2031 at 7.76% CAGR over 2026-2031. The blast chillers market is being driven by tighter refrigerant and energy regulations, especially in North America and Europe, where compliance now shapes replacement timing as much as kitchen expansion plans [1]U.S. Environmental Protection Agency, “AIM Act Restrictions on Commercial Refrigeration Refrigerants,” EPA, epa.gov. The blast chillers market is also benefiting from the wider adoption of cook-chill batch preparation, which is making blast chilling standard equipment in hotels, institutional kitchens, and larger food processing sites rather than a discretionary purchase. Regional demand remains uneven, with Asia-Pacific building new volume through QSR expansion and cold chain investment, while Europe is moving through a steadier replacement cycle shaped by mature adoption and strict standards. Competition in the blast chillers market is moving away from headline purchase price and toward lifecycle cost, service coverage, refrigerant readiness, and digital monitoring features that matter to multi-site operators. The top 5 companies accounted for 62% of global revenue in 2025, leaving room for regional manufacturers, especially in price-sensitive countries and in the mid-capacity range, where distribution reach still matters.

Key Report Takeaways

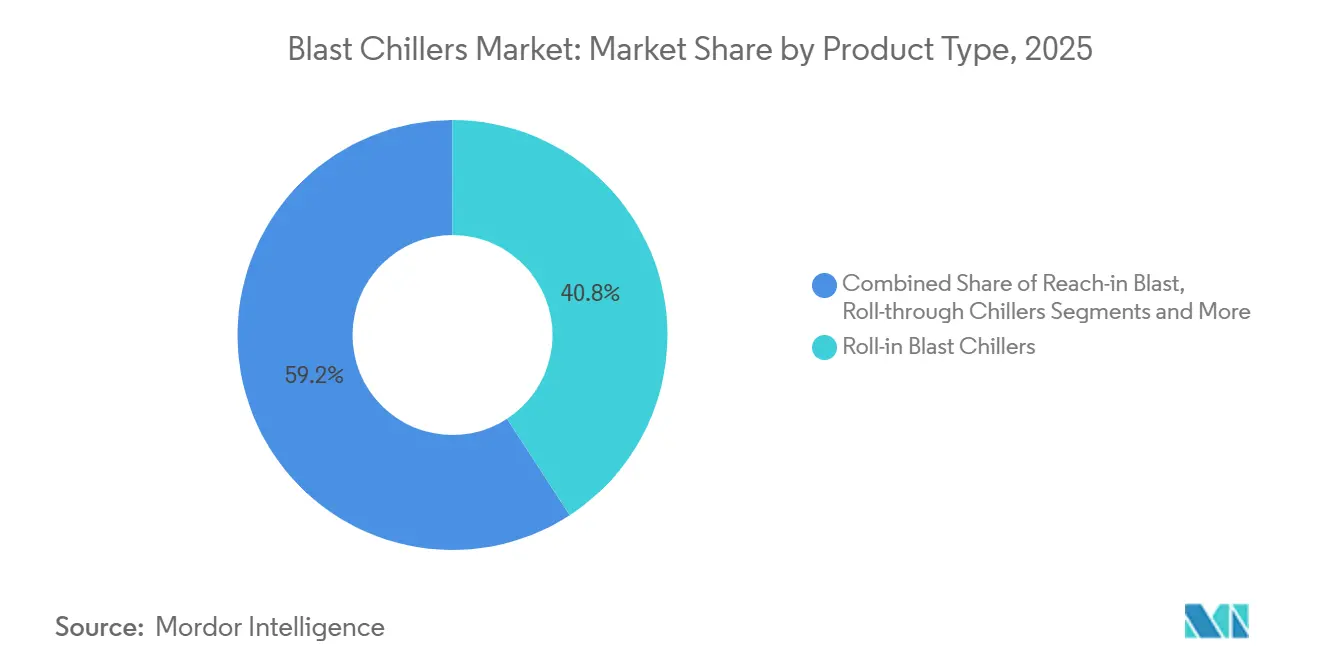

- By product type, roll-in blast chillers led with 40.8% revenue share in 2025, while roll-through blast chillers are projected to expand at a 7.97% CAGR through 2031 in the blast chillers market.

- By capacity, the 50-100 kg band accounted for 34.1% of the blast chillers market in 2025, while the above-200 kg band is forecast to grow at an 8.16% CAGR through 2031.

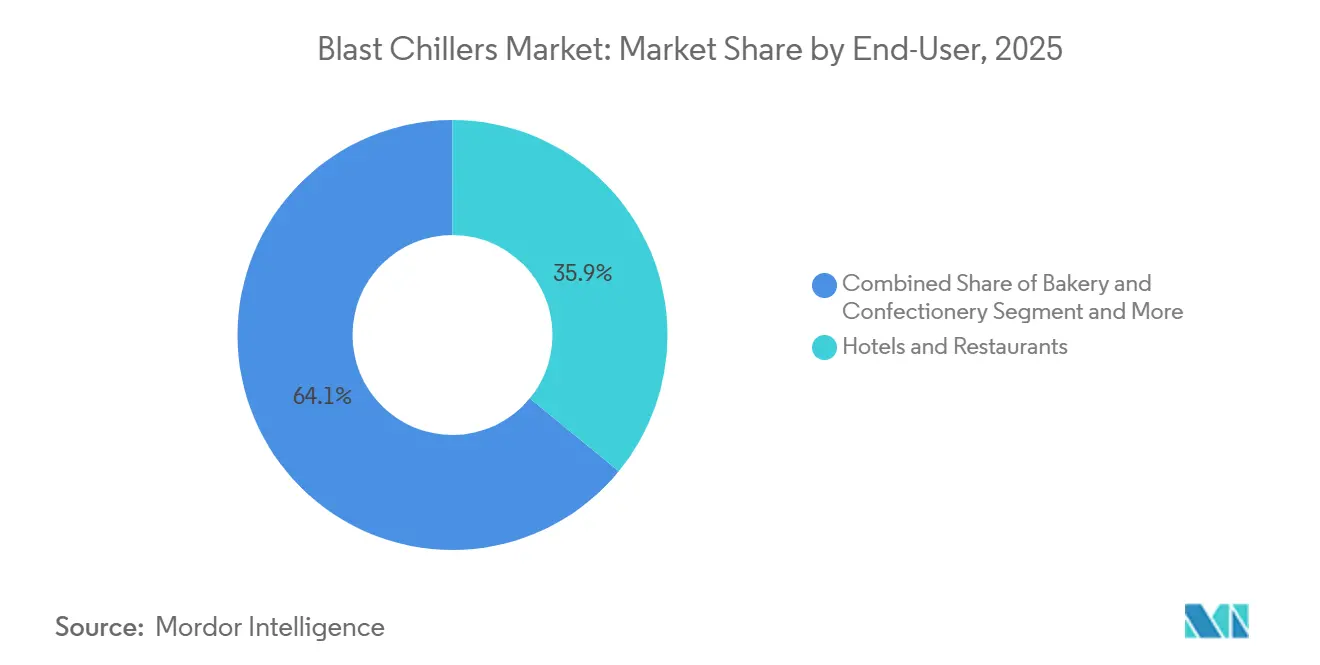

- By end user, hotels and restaurants held 35.9% of the blast chillers market share in 2025, while food processing and manufacturing plants recorded the highest projected CAGR at 8.43% through 2031.

- By distribution channel, distributors and dealers accounted for 53.8% of global demand in 2025, while direct sales are projected to grow at an 8.26% CAGR through 2031.

- By geography, Europe accounted for 33.3% of global revenue in 2025, while Asia-Pacific is set to post the fastest regional CAGR of 9.12% through 2031 in the blast chillers market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blast Chillers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy Efficiency Regulations In Foodservice | +1.5% | North America and the European Union | Short term (≤ 2 years) |

| Rapid Growth Of Frozen Ready Meal Demand In Asia-Pacific | +1.3% | Asia-Pacific core, spill-over to Middle East & Africa | Medium term (2-4 years) |

| Decarbonization Targets Driving Low-GWP Refrigerants | +1.1% | Global | Medium term (2-4 years) |

| Kitchen Automation Integration In QSR Formats | +1.0% | North America, Asia-Pacific, European Union | Medium term (2-4 years) |

| Cold Chain Expansion For E Grocery Last Mile | +0.9% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| EU Ecodesign Enforcement For Professional Refrigeration | +0.7% | European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations In Foodservice Drive A Product Redesign Cycle

The blast chillers market is being reshaped by rules that now tie purchasing decisions directly to refrigerant and equipment compliance. From January 2025, the United States EPA barred new self-contained commercial refrigeration equipment using refrigerants with a GWP above 150, which changed specification choices in the largest national market for blast chillers. A further EPA requirement, effective from January 2026, for remote systems with a GWP cap of 1,400, extended this pressure to medium-capacity refrigeration applications used in food retail and processing environments. Suppliers that had already moved into natural refrigerant platforms were better placed when buyers accelerated replacement decisions, which gave product readiness a clear commercial advantage. The result in the blast chillers market is a wider gap between larger manufacturers that can fund redesign work and smaller fabricators that face tighter margins in regulated regions.

Rapid Growth Of Frozen Ready-Meal Demand In Asia-Pacific Sustains A New Procurement Class

The blast chillers market in Asia-Pacific is no longer tied solely to hotels and premium kitchens, as QSR commissaries and frozen meal facilities are adding blast chilling as standard line equipment. Demand formation is being supported by urban food delivery systems, wider central kitchen models, and expanding cold chain networks across China, India, and Southeast Asia. Hoshizaki’s decision to establish its first Southeast Asia production base within ARICO’s Ho Chi Minh City facility, with shipments beginning in April 2026, showed that suppliers are aligning manufacturing footprints with this regional demand shift [2]Hoshizaki Corporation, “ARICO Share Acquisition and Vietnam Production Expansion,” Hoshizaki, hoshizaki.com. That move matters for the blast chillers market because regional production improves lead times, supports channel development, and lowers the friction around service and spare parts coverage. The broader effect is that procurement in Asia-Pacific is becoming a recurring capital cycle rather than a one-off event, which supports sustained volume growth in the blast chillers market through the forecast period.

Decarbonization Targets Driving Low-GWP Refrigerants: Transform The Competitive Architecture

The blast chillers market is moving toward a split product landscape, with legacy HFC units and newer R-290 or CO2 platforms. European Union Implementing Regulation 2025/33 granted a temporary exemption for certain blast cabinets containing F-gases with a GWP of 150 or above until June 30, 2026, creating a defined transition runway for manufacturers and buyers. The European Commission then published Implementing Decision 2026/151 on January 23, 2026, which set the harmonized standard for blast cabinets under the existing ecodesign framework. In the blast chillers market, that sequence compressed demand into the current period because operators faced a hard deadline to replace or qualify equipment under the new standard. It also underscored the importance of trained service capacity, because the move to natural refrigerants requires new installation and maintenance capabilities that are still uneven across countries.

Cold-Chain Expansion For E-Grocery Last-Mile Creates A New Demand Tier For Blast Chillers

The blast chillers market is gaining a new layer of demand from dark stores, micro-fulfillment centers, and prepared meal nodes that did not previously require professional blast chilling at scale. In these formats, operators use blast chilling to hold prepared meals and fresh-cut products within narrow shelf-life windows before final delivery. This pattern matters because it shifts demand toward mid-range configurations rather than just large central kitchen systems, broadening the addressable equipment base in the blast chillers market. It also supports a stronger demand for compact reach-in and roll-in layouts that fit urban sites with space constraints and rapid order turnover. As e-grocery networks expand beyond major metropolitan areas, the blast chillers market stands to gain from a larger site count, even as unit capacity per location remains moderate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Cost For SMB Operators | -0.8% | Global, concentrated in South and Southeast Asia | Medium term (2-4 years) |

| Skilled Technician Shortage For Natural Refrigerant Systems | -0.7% | Global | Short term (≤ 2 years) |

| Refrigerant Phase Down Uncertainty In Emerging Markets | -0.5% | Middle East & Africa, South America, developing Asia-Pacific | Medium term (2-4 years) |

| Volatile Stainless Steel Prices Post 2025 | -0.5% | Global, the European Union concentrated | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost For SMB Operators Limits Volume At The Base Of The Market

The blast chillers market still faces a basic affordability barrier for small foodservice operators, who cannot easily justify the upfront cost of specialized rapid-chill equipment. Entry-level units can absorb a large share of a small café or local kitchen’s equipment budget, which slows adoption even when labor or waste savings are clear in theory. This problem is stronger in South and Southeast Asia, where equipment finance for professional refrigeration is less developed and payback models are harder for smaller buyers to validate before purchase. Leasing models and subscription-style equipment programs are beginning to appear, but the pace of uptake remains limited outside markets where those financing structures are already familiar. The result is that the blast chillers market continues to move at 2 speeds, with well-funded chains upgrading faster while independent operators continue to use conventional refrigeration for longer.

Skilled-Technician Shortage For Natural-Refrigerant Systems Slows Adoption Velocity

The blast chillers market is also constrained by the specialized skills required to install and maintain R-290 and CO2 systems at scale. Natural refrigerant systems demand different handling standards than legacy HFC equipment, which means a standard refrigeration service base cannot always support the newly installed fleet without additional training. This gap is especially visible in Southeast Asia and parts of the Middle East and Africa, where hydrocarbon service capability is not yet as deep as the equipment transition now requires. The International Institute of Refrigeration and national certification bodies are expanding training coverage, but instructor capacity and exam infrastructure still limit how quickly that workforce can scale [3]International Institute of Refrigeration, “Training and Certification Context for Refrigeration Technicians,” IIR, iifiir.org. Manufacturers with proprietary service networks can reduce some of this risk, yet the blast chillers market still depends on a broader technical ecosystem that will take time to develop.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Roll-In Platforms Set the Baseline for Commercial Demand

Roll-in blast chillers accounted for 40.8% of product revenue in 2025, making them the largest product category in the blast chillers market. Their lead comes from a strong fit with institutional kitchens and high-volume foodservice sites, where trolley-based batch handling reduces labor touchpoints and improves kitchen flow. The segment also benefits from tighter integration with adjacent cooking systems, especially in kitchens seeking a more predictable cook-chill sequence [4]Electrolux Professional, “SkyLine ChillS and SkyDuo Integrated Workflow Platform,” Electrolux Professional, electroluxprofessional.com. Electrolux Professional’s SkyDuo communication protocol, which links the SkyLine oven and SkyLine ChillS blast chiller, shows how integrated workflow design is helping hold roll-in demand in the blast chillers market. That operating logic matters most in hotels, hospitals, contract catering, and central kitchen sites where repeatability and food safety records carry more weight than the lowest purchase price.

Roll-through systems are forecast to grow at 7.97% through 2031, making them the fastest-growing product niche in the blast chillers market. Food manufacturing settings favor them because straight-line loading and unloading lower turnaround time and support a more continuous production flow. Reach-in units remain important in bakeries, smaller catering operations, and urban kitchens because their footprint and ticket size are easier to manage. Williams Refrigeration’s 2025 reach-in launch with a hydrocarbon refrigerant charge below 150 g shows that compliance-led design upgrades are now extending to smaller form factors as well as larger systems.

By Capacity: Larger Bands Gain From Centralized Production Models

The 50-100 kg band accounted for 34.1% of the blast chillers market in 2025, making it the largest capacity range by revenue. Its position reflects broad use across hotels, contract caterers, bakeries, and other mid-scale sites that need batch chilling without full industrial throughput. The range fits the current shape of the blast chillers market because it balances capacity, floor space, and purchase cost better than either the smallest or the heaviest units. At the same time, the 100-200 kg band is seeing steady upgrades from hospitals, schools, and contract catering operators that must document faster chilling cycles under tighter food safety audits. The sub-50 kg range is expanding more slowly because many operators now see it as too small for the batch volumes generated by commissary and dark-store formats.

The above 200 kg segment is projected to grow at 8.16% through 2031, which makes it the fastest-growing capacity band in the blast chillers market. This demand is tied to central production units, frozen meal plants, and food processors that are scaling output across multi-site distribution networks. Buyers in this range also place greater weight on predictive maintenance, HACCP integration, and remote monitoring because downtime incurs higher costs at higher throughput levels. Hoshizaki’s broader transition to natural refrigerants across 66 models in 2025 supports buyer confidence that servicing and platform continuity will improve across multiple equipment classes, not just in one premium line.

By End-User: Processing Plants Build Momentum While Hospitality Stays Largest

Hotels and restaurants accounted for 35.9% of the blast chillers market share in 2025, keeping hospitality as the largest end-user group. Their lead came from HACCP compliance requirements, the need to replace their installed base, and the steady adoption of cook-chill workflows in high-turnover commercial kitchens. Hospitality buyers also tend to assess energy use, refrigerant readiness, and service support more closely now than in past replacement cycles. Bakery and confectionery operators remain a distinct demand pool because they need tightly controlled cycles for items such as laminated dough, sugar work, and ganache stabilization. Catering and banqueting operations continue to favor roll-in equipment, where large-batch handling and clear documentation are critical for event production and compliance.

Food processing and manufacturing plants are forecast to grow at 8.43% through 2031, which makes them the fastest-growing end-user segment in the blast chillers market. The shift reflects more centralized preparation across retail, foodservice, and e-grocery supply chains, where blast chilling supports both safety and distribution consistency. Institutional kitchens in hospitals and schools are also moving upward, though more gradually, as audit frameworks push for documented rapid-chill records. Irinox has also framed blast chilling as a food waste reduction tool rather than solely a compliance tool, broadening the economic case for buyers who had previously viewed the equipment as optional.

By Distribution Channel: Dealer Reach Remains Critical Even As Direct Sales Accelerate

Distributors and dealers accounted for 53.8% of global revenue in 2025, making them the largest route to market for blast chillers. Their position remains strong because many independent restaurants, caterers, and institutional kitchens still rely on local channel partners for product access, installation coordination, and after-sales support. In many Tier-II cities across South and Southeast Asia, distributor networks still provide practical coverage that direct OEM teams cannot consistently match. That makes the channel a structural part of the blast chillers market even as global brands expand their own service and sales footprints. It also helps smaller and regional manufacturers stay visible in local tenders where service responsiveness often matters as much as brand scale.

Direct sales are projected to grow at 8.26% through 2031, which makes them the fastest-growing channel in the blast chillers market. Multi-site hotel groups, QSR chains, and commissary operators increasingly prefer direct contracts when they want one equipment platform across multiple sites. That trend favors companies with broader geographic service coverage and stronger support for refrigerant transitions, including Hoshizaki, Ali Group, and Electrolux Professional. As a result, the blast chillers industry is seeing a narrower gap between local reseller-led procurement and direct enterprise contracting, especially where digital monitoring and firmware support matter after installation.

Geography Analysis

Europe accounted for 33.3% of global revenue in 2025, making it the largest regional market for blast chillers. Italy remains central to European manufacturing because it hosts several specialist producers, including Irinox, Coldline, Risco, and Friulinox. Germany, France, and the United Kingdom continue to anchor hospitality and institutional demand, with buyers placing greater emphasis on lifecycle costs and compliance-readiness during equipment selection. The June 30, 2026, deadline tied to the European Union F-gas exemption also compressed a final replacement wave into the current period, supporting near-term sales of blast chillers across the region.

North America is forecast to grow at 6.1% through 2031 in the blast chillers market, with regulation-led replacement now driving much of the current demand cycle. The United States and Canada remain the largest regional demand centers, while Mexico is benefiting from food processing investment linked to nearshoring. The EPA AIM Act accelerated replacement across restaurants, healthcare kitchens, and higher education foodservice by forcing buyers to move away from non-compliant standalone equipment.

Asia-Pacific is set to record the fastest regional CAGR of 9.12% through 2031, keeping it the main growth engine for the blast chillers market. China and India are driving installations through QSR expansion, dark-store growth, and larger central kitchen networks. At the same time, Japan remains a more mature institutional market with stronger adoption of connected systems. South Korea is upgrading older HFC-based equipment under tighter environmental requirements, and Southeast Asia is gaining importance as both a demand center and a production base.

Competitive Landscape

The blast chillers market remains moderately concentrated, with the top 5 companies accounting for 62% of global revenue in 2025. That leaves a meaningful long tail of regional and national fabricators active in local markets, especially where price and lead time outweigh advanced digital features. The main competitive divide is now less about basic equipment supply and more about who can pair compliance-ready product lines with service depth, refrigerant transition support, and connected monitoring. This is why the blast chillers market is seeing stronger positions for large groups that can spread redesign and certification costs across broad portfolios. It also explains why smaller firms stay more exposed in markets where the transition to natural refrigerants is moving quickly.

Ali Group remains one of the broadest players in the blast chillers market because it can combine blast chilling with a much wider commercial kitchen portfolio across brands and channels. Its March 2026 acquisition of BUNN broadened that cross-selling reach, especially in QSR and institutional accounts, where beverage and back-of-house equipment are often specified together. Hoshizaki is pursuing a different route, using acquisitions and capacity additions to strengthen its regional manufacturing and service presence, including the deeper consolidation of ARICO in Vietnam. Electrolux Professional and Irinox continue to compete through workflow integration, premium performance, and digital tools such as cloud-linked HACCP logging and remote diagnostics.

Smaller competitors such as Sagi, Risco, Coldline, and Everlasting remain important in the blast chillers market. Still, they compete more on price, delivery speed, and local familiarity than on full digital capability. Refrigerant-transition investment is raising pressure on mid-sized Italian and European manufacturers that must fund platform upgrades without the scale advantages of diversified groups. Irinox’s MultiFresh Next range and its recognition for energy-efficient design underline how intellectual property and product architecture are becoming stronger differentiators at the premium end of the blast chillers market. Over time, the market structure is likely to maintain a barbell shape, with global OEMs holding stronger positions in highly regulated markets and fragmented regional players retaining share in lower-spec, more price-sensitive countries.

Blast Chillers Industry Leaders

Ali Group Srl (Friginox, Lainox, Victory)

Electrolux Professional AB

Irinox S.p.A.

Foster Refrigerator (ITW)

Hoshizaki Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Ali Group completed the acquisition of Bunn Commercial LP, BUNN. The transaction broadens Ali Group's cross-selling capabilities, particularly in institutional and QSR channels where blast chillers and beverage equipment are co-specified, and reinforces its position as one of the most diversified global foodservice equipment groups.

- March 2026: Hoshizaki signed an agreement with SEAREFICO to acquire additional shares in ARICO, Asia Refrigeration Industry JSC, Vietnam, raising its stake from 51% to 99.616%. The consolidation enables Hoshizaki to accelerate production decision-making at its first Southeast Asia manufacturing base in Ho Chi Minh City, where commercial refrigerator shipments commenced in April 2026.

- November 2025: Hoshizaki announced the expansion of 66 models across 4 product lines, including cubelet ice makers and commercial refrigerators, to isobutane, R-600a, with shipments commencing from mid-December 2025 as part of its program to transition the full product range to HFC-free refrigerants.

- January 2025: Williams Refrigeration launched a new range of reach-in blast chillers using natural hydrocarbon refrigerant with a propane charge below 150 g, providing faster chilling times from 90°C to 3°C in 90 minutes and broader installation flexibility across commercial kitchens.

Global Blast Chillers Market Report Scope

This delves into the global blast chillers market, examining factors such as product type, capacity, end user, distribution channel, and geography. The analysis anchors its study period with 2025 as the base year, 2026 as the current year, and forecasts from 2026 to 2031, aligning with the provided market sizing and growth outlook. The research scrutinizes both demand and supply dynamics shaping equipment adoption. Key factors include regulatory compliance, refrigerant transitions, the expansion of cook-chill workflows, the growth of central kitchens, investments in food processing, and the competitive landscape among major OEMs and regional suppliers. Furthermore, the analysis offers a qualitative assessment of market drivers, restraints, product innovations, shifts in distribution channels, regional demand trends, and notable industry developments pertinent to the procurement and deployment of blast chillers.

The Global Blast Chillers Market is Segmented by Product Type (Reach-in, Roll-in/Trolley, Roll-through, Under-counter, and Walk-in), Capacity (Below 50 kg, 50–100 kg, 100–200 kg, and Above 200 kg), End-User (Hotels & Restaurants, Bakery, Catering, Institutional, and Food Processing), Distribution Channel (Direct, and Distributors/Dealers), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East & Africa). Market Forecasts are in Value (USD).

| Reach-in Blast Chillers |

| Roll-in / Trolley Blast Chillers |

| Roll-through Blast Chillers |

| Under-counter Blast Chillers |

| Modular / Walk-in Blast Chillers |

| Less than 50 kg |

| 50–100 kg |

| 100–200 kg |

| More than 200 kg |

| Hotels & Restaurants |

| Bakery & Confectionery |

| Catering & Banqueting |

| Institutional Kitchens (Hospitals, Schools) |

| Food Processing/Manufacturing Plants |

| Direct Sales |

| Distributors / Dealers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Reach-in Blast Chillers | |

| Roll-in / Trolley Blast Chillers | ||

| Roll-through Blast Chillers | ||

| Under-counter Blast Chillers | ||

| Modular / Walk-in Blast Chillers | ||

| By Capacity | Less than 50 kg | |

| 50–100 kg | ||

| 100–200 kg | ||

| More than 200 kg | ||

| By End User | Hotels & Restaurants | |

| Bakery & Confectionery | ||

| Catering & Banqueting | ||

| Institutional Kitchens (Hospitals, Schools) | ||

| Food Processing/Manufacturing Plants | ||

| By Distribution Channel | Direct Sales | |

| Distributors / Dealers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for blast chillers through 2031?

The blast chillers market size is expected to rise from USD 1.73 billion in 2026 to USD 2.51 billion by 2031 at a 7.76% CAGR, supported by regulation-led replacement and wider cook-chill adoption.

Which region is growing fastest for blast chilling equipment?

Asia-Pacific is projected to grow at 9.12% through 2031, making it the fastest-growing regional market as QSR chains, central kitchens, and cold chain networks expand.

Which product category leads demand for blast chillers?

Roll-in units led with 40.8% share in 2025 because they fit institutional kitchens and high-volume foodservice sites that rely on trolley-based batch handling.

Which buyer group is expanding fastest?

Food processing and manufacturing plants are forecast to grow at 8.43% through 2031 as centralized production models gain share across retail, foodservice, and e-grocery supply chains.

Why are natural refrigerants important in this space?

Refrigerant rules in the United States and Europe are pushing buyers toward R-290 and CO2 systems, which makes compliance, service capability, and trained technicians more important in vendor selection.

How concentrated is competition among blast chiller suppliers?

The top 5 companies accounted for 62% of revenue in 2025, indicating a moderately concentrated field with strong global players and a meaningful tail of regional manufacturers.

Page last updated on: