Ice-Cream Freezers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

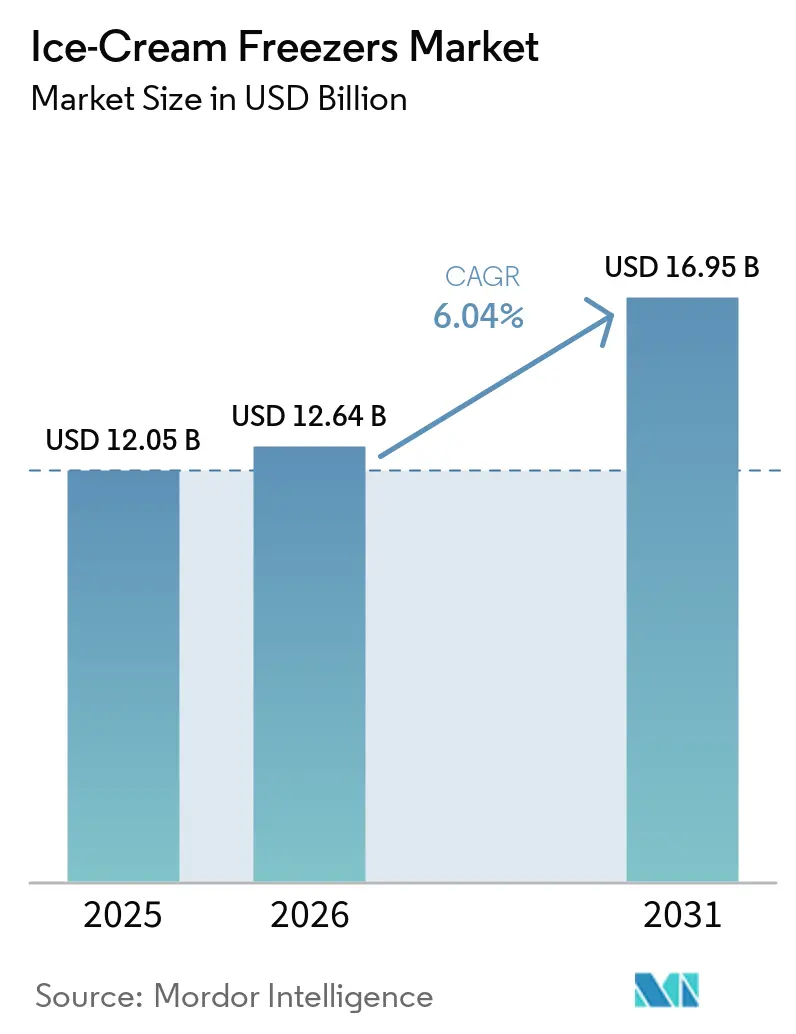

| Market Size (2026) | USD 12.64 Billion |

| Market Size (2031) | USD 16.95 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ice-Cream Freezers Market Analysis by Mordor Intelligence

The ice-cream freezers market size is expected to increase from USD 12.05 billion in 2025 to USD 12.64 billion in 2026 and reach USD 16.95 billion by 2031, growing at a CAGR of 6.04% over 2026-2031. The ice-cream freezers market is being lifted by a replacement cycle that has moved from deferred spending to active purchasing as HFC rules tighten in Europe and the United States. The Kigali Amendment is exerting the same pressure on developing economies as cold-chain distribution for frozen desserts is expanding, widening the replacement window across Southeast Asia, South America, and the Middle East. The ice-cream freezer market is also benefiting from a broader shift toward natural refrigerants and higher-efficiency cabinets, as operators now weigh power use and refrigerant servicing risk together rather than treating them as separate decisions. Compliance requirements tied to technician certification and product registration are lengthening the time required for some purchase decisions. Yet, those same rules are making equipment upgrades more visible and more difficult to postpone in the ice-cream freezer market [1]European Commission, “F-Gas Regulation and Refrigeration Policy Materials,” European Commission, commission.europa.eu.

Key Report Takeaways

- By geography, Asia-Pacific accounted for 37.13% of revenue in 2025 in the ice-cream freezers market and recorded the fastest projected CAGR of 7.23% through 2031.

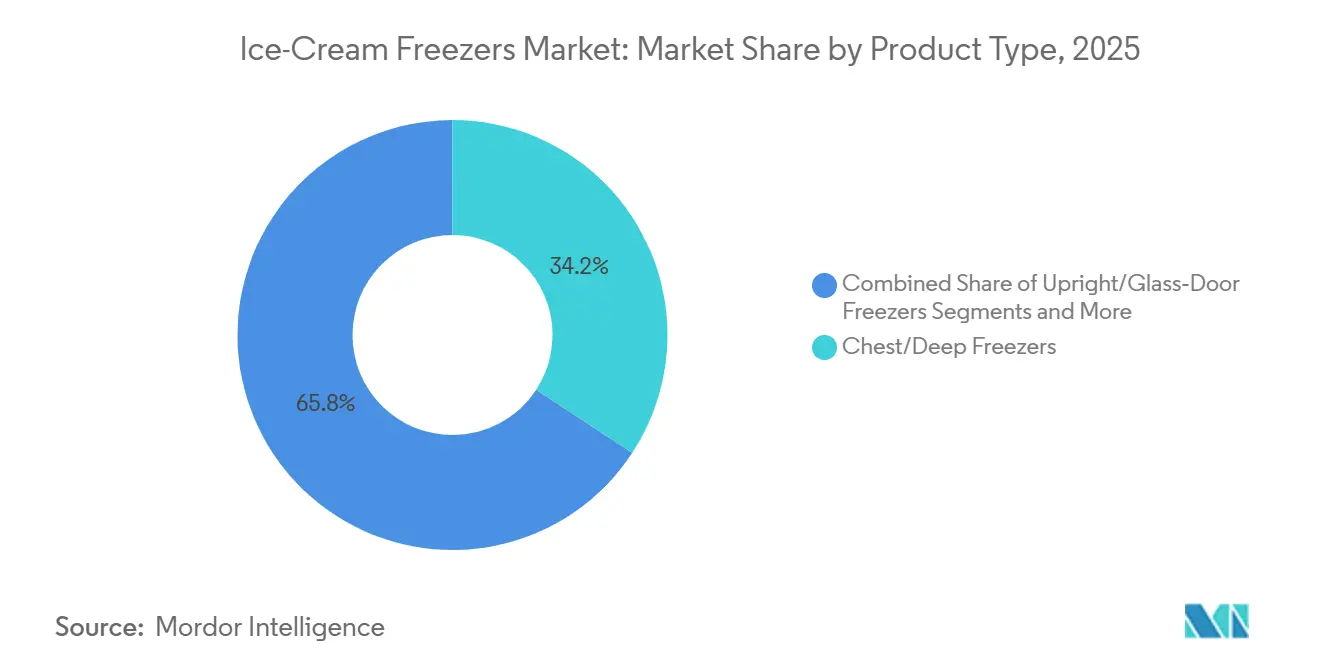

- By product type, Chest/Deep Freezers held 34.23% of the ice-cream freezers market share in 2025, while Upright/Glass-Door Freezers recorded the fastest projected CAGR at 6.18% through 2031.

- By cooling technology, Static systems accounted for 44.92% of revenue in 2025, while Remote Glycol/Waterloop (SPI) systems advanced at the highest projected CAGR of 6.88% through 2031.

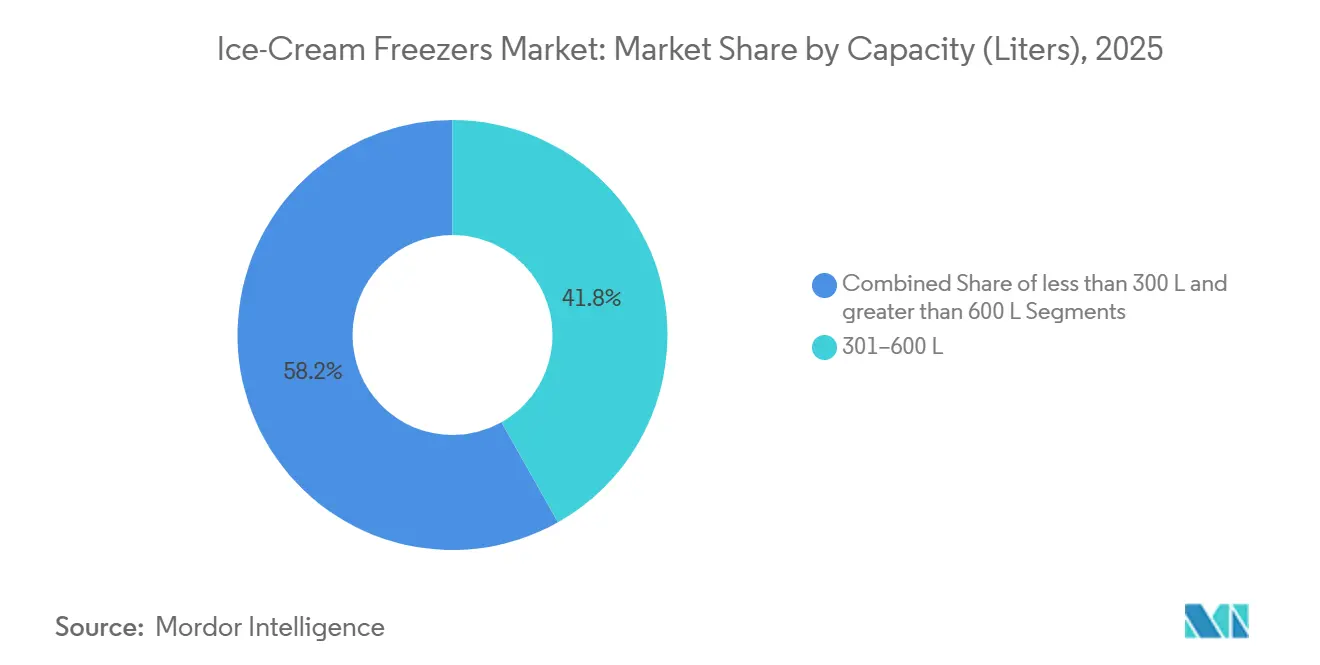

- By capacity, the 301-600L segment accounted for 41.84% of the ice-cream freezer market in 2025, while the >600L segment is forecast to expand at a 6.35% CAGR through 2031.

- By end user, Supermarkets/Hypermarkets accounted for 38.72% of revenue in 2025, while Ice-Cream Parlors & Gelaterias posted the highest projected CAGR of 7.12% through 2031.

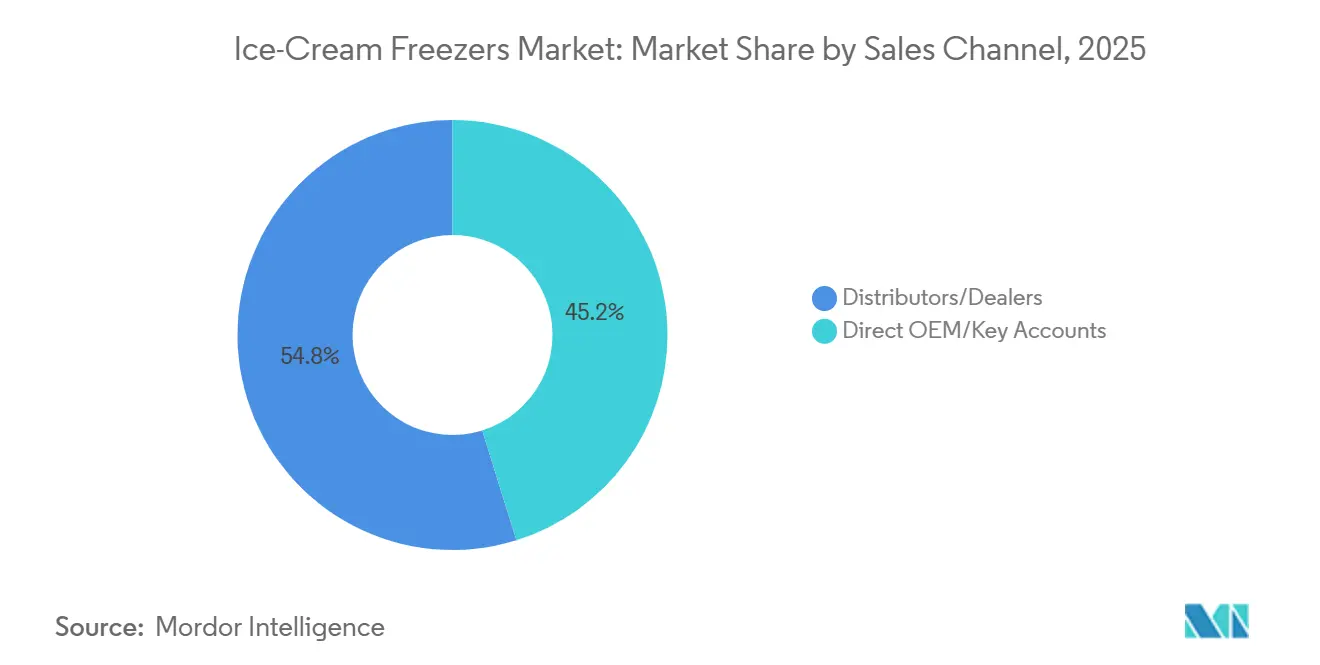

- By sales channel, Distributors/Dealers accounted for 54.82% of revenue in 2025, while Direct OEM/Key Accounts is projected to grow at a 6.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ice-Cream Freezers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HFC Phase-Down and Efficiency Mandates Driving Replacement Cycles | +1.3% | Global, led by the European Union and North America, will spill over to the Asia-Pacific and South America via Kigali. | Medium term (2-4 years) |

| Retail Footprint Expansion and Modernization in the Asia-Pacific | +1.2% | Asia-Pacific core, India, China, Southeast Asia, spill-over to the Middle East and Africa | Long term (≥ 4 years) |

| Natural Refrigerants Adoption Enabling Higher-Efficiency Plug-Ins | +0.9% | European Union, North America, Australia, and early-stage in Southeast Asia and South America | Medium term (2-4 years) |

| Growth Of Supermarkets, Convenience Formats, and Premium Gelato Outlets | +0.8% | Global, with concentration in Europe, North America, and India | Long term (≥ 4 years) |

| Energy Labeling and Procurement Transparency: Accelerating Upgrades | +0.6% | European Union, with secondary effects in the United Kingdom, Switzerland, and export-compliant markets | Short term (≤ 2 years) |

| Waterloop and Semi Plug-In Architectures Enabling Heat Recovery and Flexible Layouts | +0.4% | European Union core, early adoption in Southeast Asia, Thailand, Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

HFC Phase-Down and Efficiency Mandates Creating Structural Replacement Demand

The ice-cream freezer market is entering a structural replacement phase because the European Union F-Gas Regulation (EU) 2024/573 banned fluorinated gases with a GWP of 150 or more in new self-contained commercial refrigeration equipment from January 1, 2025, directly affecting legacy R134a and R404A freezer fleets. In the United States, the AIM Act requires new stand-alone commercial refrigeration units to shift to refrigerants with a GWP below 150 on the same date, while the HFC allowance cap for 2024-2028 fell to 60% of baseline [2]United States Environmental Protection Agency, “Technology Transitions Under The AIM Act,” U.S. EPA, epa.gov. European Union HFC consumption in 2024 was already 60% below Montreal Protocol targets, which shows how quickly the available refrigerant pool has tightened for owners of legacy systems. That change matters for the ice-cream freezers market because operators who keep older equipment in service face higher servicing exposure due to virgin HFC supply contracts. The result is that replacement decisions are increasingly being justified by total ownership cost and compliance risk rather than by simple end-of-life timing.

Retail Footprint Expansion and Modernization in Asia-Pacific

Asia-Pacific combines the largest current base with the fastest growth path, giving the ice-cream freezers market a stronger structural demand base than in regions where growth depends on replacement. India’s ice-cream business was valued at INR 30,000 crore (USD 3.5 billion) in 2023, and the category is expected to grow at 13%-15% as organized retail expands and per-capita consumption rises. That retail build-out is not limited to large-format hypermarkets, because neighborhood grocery and convenience formats are also widening frozen-food capacity across China, India, and Southeast Asia. Those smaller stores usually need plug-in cabinets rather than centralized systems, so demand tilts toward the ≤300L and 301-600L bands in the ice-cream freezers market. The practical effect is that store-count growth in warm-climate urban corridors converts directly into new cabinet demand, especially where impulse purchases still dominate frozen dessert sales.

Natural Refrigerant Adoption Enabling Higher-Efficiency Plug-in Units

Natural refrigerants are becoming the default design pathway in the ice-cream freezers market across regulated geographies. The ATMOsphere 2024 Market Report stated that European food retail had an installed base of 17 million hydrocarbon self-contained refrigerated cabinets as of December 2024, indicating broad adoption beyond pilot deployments. In North America, transcritical CO2 adoption in commercial refrigeration rose sharply in 2024 and 2025, reaching 6,360 supermarket and industrial sites, which shows that low-GWP platforms are scaling in mainstream food retail rather than in isolated projects. The LIFE ICEGREEN project also showed that R290-based ice-cream machines reduced energy use by an average of 27% compared with legacy HFC systems, strengthening the operating-cost case for conversion. This combination of policy pressure and energy savings is shifting the ice-cream freezer market toward units that meet both refrigerant and electricity targets without relying on future servicing exceptions.

Growth of Supermarkets, Convenience Formats, and Premium Gelato Outlets

The ice-cream freezers market is also supported by broader changes in where frozen desserts are sold. Supermarkets and convenience stores continue to anchor volume. Yet, the popularity of specialist gelato and premium dessert formats is driving demand for dipping cabinets, scooping units, and countertop displays that differ technically from standard chest units. Italy’s artisan gelato sector generated close to EUR 3 billion in 2024, and SIGEP expected another strong year in 2025 after European gelato consumption increased 2.1% in 2024. That matters because premium parlors buy for presentation, temperature stability, and brand experience, not only for low upfront cost. The outcome for the ice-cream freezers market is a mix shift toward more specialized cabinets with higher selling prices and stronger specification control from franchise and branded concepts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technician Skill Gaps and Safety Code Compliance For HC and CO2 | -0.7% | European Union core, North America, and acute in emerging Asia-Pacific and South America | Short term (≤ 2 years) to Medium term (2-4 years) |

| High Upfront Costs Amid Energy Price Volatility | -0.5% | Global, acute in cost-sensitive SME segments and emerging markets | Medium term (2-4 years) |

| Hydrocarbon Charge and Room-Size Limits Restricting Some Sites | -0.3% | Global, most acute in small-format emerging-market stores | Long term (≥ 4 years) |

| European Union Market Surveillance and Conformity Burdens Elongating Purchase Cycles | -0.2% | European Union, United Kingdom, secondary effects in export-compliant markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technician Skill Gaps and Safety Code Compliance for HC/CO2

The ice-cream freezers market faces a conversion bottleneck because the move to R290 and CO2 systems depends on a technician base that is still catching up with new safety and handling requirements. European Union F-Gas Regulation (EU) 2024/573 requires member states to establish certification programs for natural-refrigerant technicians, and implementing rules began to appear through 2025. The gap between certification timelines and workforce capacity can cause installation and fleet conversion to lag even when buyers are ready to spend. Smaller operators are particularly cautious because improper handling of hydrocarbon systems can raise insurance concerns and trigger building code violations. As a result, the ice-cream freezers market may see demand remain healthy while actual installation velocity is constrained by labor availability and compliance risk.

High Upfront Costs Amid Energy Price Volatility

The ice-cream freezers market also faces resistance due to the higher upfront costs of natural-refrigerant and semi-plug-in systems, especially among small retailers and foodservice operators. EuroShop noted that hybrid SPI waterloop systems can offer stronger long-term economics, but they still require more initial capital than conventional air-cooled plug-ins [3]EuroShop, “Store Refrigeration and Waterloop System Economics,” EuroShop, euroshop-tradefair.com . Those economics become harder to approve when electricity prices are volatile, because projected payback periods can shift materially between procurement review and operating reality. Larger chains can absorb that uncertainty more easily, but the independent store base that drives unit volumes in Asia and Africa remains more price-sensitive. This makes financing and capital budgeting, rather than only product availability, a meaningful restraint on the ice-cream freezers market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Impulse Formats Hold Ground as Upright Displays Gain Share

Chest/Deep Freezers held 34.23% of the ice-cream freezer market share in 2025, reflecting their deep entrenchment in branded freezer programs across Asia-Pacific, Africa, and South America. Their position remains strong because multinational ice-cream brands continue to place chest units with independent retailers under exclusive or semi-exclusive distribution arrangements. That installed base is replaced on a cycle shaped more by refrigerant compliance than by merchandising obsolescence. The ice-cream freezers market still relies on chest formats in impulse-heavy locations where low cost, durability, and simple maintenance matter more than visual presentation. This keeps chest units highly relevant in roadside retail, kiosks, and neighborhood outlets where frozen dessert turnover is steady, but floor area is limited.

Upright/Glass-Door Freezers are projected to grow at a 6.18% CAGR through 2031, the fastest rate among product types, as organized retail shifts toward vertical visibility and clearer product comparisons. European Union energy rules have reinforced that shift, as ice-cream freezers had to meet an EEI threshold of 50% or less from September 1, 2023, favoring newer vertical designs in regulated markets [4]Topten, “Commercial Refrigeration Energy Requirements,” Topten, topten.eu. Dipping Cabinets and Scooping Freezers are gaining more addressable demand as gelato and premium dessert formats expand into markets where they previously had little formal presence. Island/Multideck Freezers remain tied to larger supermarket floor displays and are being refreshed on lower-GWP platforms as store fleets modernize. Countertop Ice-Cream Freezers remain the smallest sub-segment, yet they benefit from café, QSR, and dessert menu expansion, which gives the ice-cream freezers industry a specialist product layer beyond mainstream retail.

By Cooling Technology: Static Holds the Base While Waterloop Defines the Direction

Static cooling systems accounted for 44.92% of 2025 revenues, underscoring how much the ice-cream freezers market still relies on low-cost plug-in cabinets used in branded fleets and small-format retail. Their staying power is linked to simplicity, lower acquisition costs, and a long history of installation in impulse channels. Static systems have also remained viable because compliance pressure has pushed manufacturers to optimize familiar platforms rather than abandon them. In practice, many operators prefer an improved static unit that is easy to service and install. That dynamic helps explain why the base of the ice-cream freezers market remains broad even as advanced technologies gain attention.

Remote Glycol/Waterloop (SPI) systems are growing at 6.88% through 2031, the fastest pace among cooling technologies, because they address both refrigerant compliance and store-layout flexibility. AHT Cooling Systems deployed its VENTO SPI waterloop system in Thailand in 2025. They reported a 12% reduction in annual energy use against an R404A rack system, along with a 97% reduction in refrigerant charge. A hybrid R290 plug-in water-loop installation in Germany also cut total supermarket energy use by 8.8% and reduced air-conditioning load by up to 40% in warmer months. Charge-limit rules under EN IEC 60335-2-89:2022 have further strengthened the case for distributed architectures by spreading refrigerant across smaller sealed circuits rather than a single large, centralized charge. In the ice-cream freezers market, which means waterloop systems are shaping the future of technology, even as static units continue to dominate the installed base.

By Capacity (Liters): Mid-Range Dominates, Large Format Gains Ground

The 301-600L segment accounted for 41.84% of the ice-cream freezer market in 2025, as it meets the needs of supermarket aisles and mid-size convenience stores that require a visible display without excessive power draw. This capacity band offers a practical balance between merchandising area, replenishment frequency, and store-space efficiency. It also works well for retailers that refresh frozen inventory daily but do not have the volume density of a large hypermarket. As a result, the mid-range band remains the default choice in much of the ice-cream freezer market where operators want broad SKU visibility with manageable operating costs. That balance makes it harder for either the smallest or the largest capacity class to displace the middle outright.

The >600L segment is projected to grow at a 6.35% CAGR through 2031, which reflects the build-out of hypermarkets, warehouse-style formats, and larger frozen-food displays in growth markets. Larger cabinets suit stores that allocate more floor area to frozen desserts and need a stronger visual impact for family and bulk purchases. At the same time, the ≤300L range remains structurally secure because independent retailers and branded impulse programs continue to place compact units in local shops and transit-adjacent outlets. Convenience-store densification across Asia keeps both the ≤300L and 301-600L bands active, as those formats require smaller footprints, fast turnover, and simple replenishment. This split between compact impulse units and larger showcase formats gives the ice-cream freezers industry a broad capacity profile rather than a single dominant migration path.

By End User: Supermarkets Lead but Gelaterias Set the Pace

Supermarkets/Hypermarkets accounted for 38.72% of 2025 end-user revenues, reflecting their position as the main off-premise channel for packaged ice-cream in developed and organized retail markets. Their purchases are increasingly tied to compliance programs, energy reviews, and network-wide refresh cycles rather than ad hoc freezer replacements. That pattern favors suppliers that can handle fleet planning, product registration, and after-sales support across many stores. It also means procurement can arrive in concentrated waves when a retailer moves from legacy HFC stock to lower-GWP equipment. In the ice-cream freezers market, large-format food retail remains the volume anchor, even as smaller channels grow faster in some countries.

Ice-Cream Parlors & Gelaterias are projected to expand at a 7.12% CAGR through 2031, making them the fastest-growing end-user segment in the ice-cream freezers market. Demand here is tied to franchise growth, premiumization, and the rise of specialist display formats that depend on precise serving conditions and stronger visual merchandising. These buyers need dipping cabinets, scooping units, and countertop displays that differ materially from standard packaged-ice-cream freezers. Convenience Stores/Gas Stations also remain an important growth segment in Asia-Pacific and North America. At the same time, HoReCa demand is being bolstered by the expansion of dessert menus across quick-service and café formats. Bars & Clubs remain a niche user group, yet their demand is premium-priced and product-specific, which adds a small but specialized layer to the ice-cream freezers market size.

By Sales Channel: Distributor Networks Underpin Breadth, Direct OEM Scales Premium

Distributors/Dealers accounted for 54.82% of 2025 revenues, reflecting the wide geographic spread and service intensity of the installed base in the ice-cream freezer market. Local partners remain important because they provide language support, spare parts, maintenance coordination, and fast response across thousands of small end-user sites. Many independent gelaterias, neighborhood groceries, and convenience outlets are not reachable through a direct manufacturer model alone. That keeps distributor networks central in markets where service density matters as much as product specification. In that sense, the channel structure of the ice-cream freezers market still mirrors the fragmentation of its end users and regional operating conditions.

Direct OEM/Key Accounts is forecast to grow at 6.73% through 2031 as large retail chains centralize procurement into multi-year fleet agreements. This channel works best for buyers who want bundled services, remote monitoring, and clear compliance management across large store networks. Kroger has committed to deploying transcritical CO2 refrigeration in all new United States stores from 2025, while ALDI United States has already built a substantial estate of transcritical CO2 stores, which shows how major chains are shifting to direct, specification-led procurement. For manufacturers, a direct key-account contract can create more predictable demand and a stronger role in refrigerant-transition planning. That is why the ice-cream freezer industry is likely to maintain its distributor breadth while expanding direct OEM depth at the premium end of the sales channel mix.

Geography Analysis

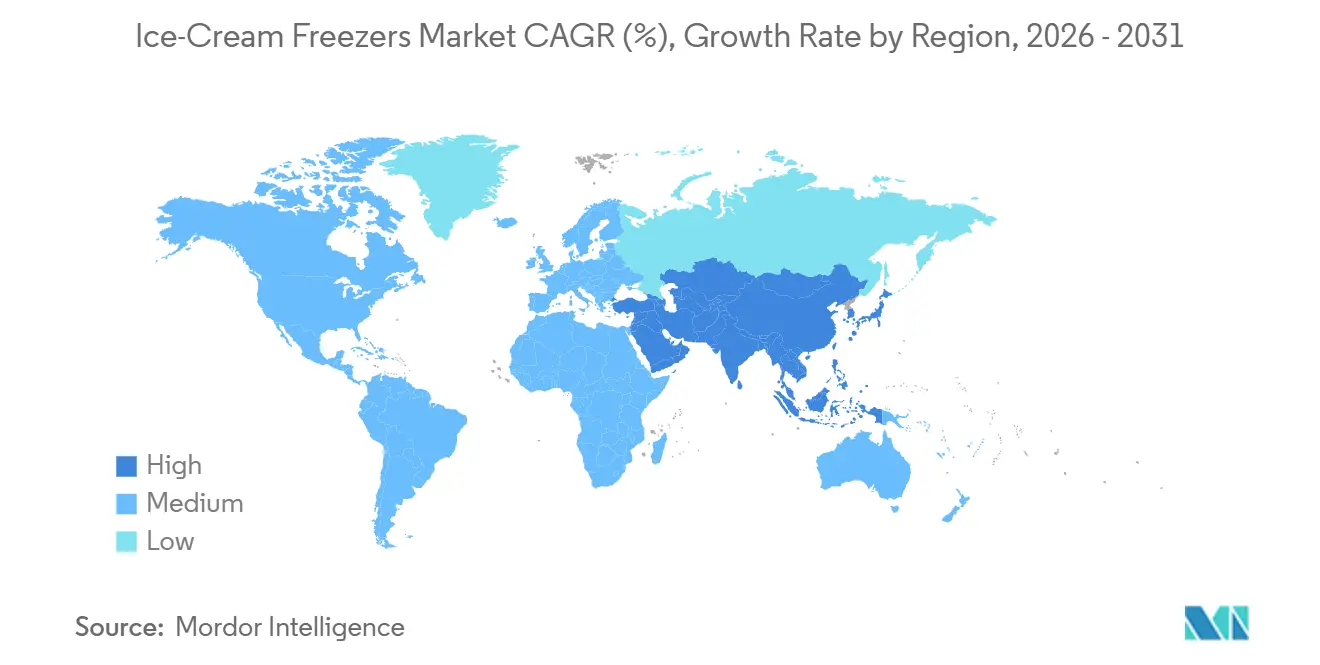

Asia-Pacific held 37.13% of the ice-cream freezer market share in 2025 and is also forecast to post the fastest regional CAGR of 7.23% through 2031. That rare combination points to structural demand rather than a short replacement spike. The region benefits from rising frozen dessert consumption, rapid retail formalization, and climate conditions that sustain year-round demand for visible commercial freezer placement. India adds a strong long-term layer because organized retail expansion is improving cold-chain reach while per-capita consumption continues to rise from a low base. The region also offers an early commercial case for waterloop and semi plug-in systems because high ambient temperatures make heat rejection a more immediate store-level issue than in many temperate markets.

Europe is projected to grow at 3.50% through 2031, which is slower than Asia-Pacific but still supported by a clear compliance-led replacement cycle. The region’s installed base is large and mature, so equipment refresh depends more on regulations, efficiency, and technology upgrades than on the creation of new outlets. European Union Ecodesign and EPREL rules have made product comparison more transparent, and the European Union F-Gas Regulation (EU) 2024/573 has accelerated pressure on legacy HFC fleets. North America is forecast to grow at 4.50% through 2031, supported by the AIM Act and by demand for premium and artisan frozen dessert formats. In both regions, the ice-cream freezers market is moving toward better-specified, lower-GWP, and more data-visible equipment rather than simply toward higher unit volumes.

South America is projected to grow at 5.00% through 2031, while Western Asia is expected to expand in the 5%-6% range and Africa in the 4% range, from lower bases. These regions are at an earlier stage of development, so retail modernization and cold-chain investment matter more than regulation-driven replacement in the near term. The Kigali framework remains important because it pulls developing economies onto the HFC phase-down path and supports a gradual shift away from legacy refrigerants. As store networks and foodservice formats modernize, the ice-cream freezers market in these geographies should expand through a mix of first-time installations and selective upgrades, rather than solely through broad fleet conversion.

Competitive Landscape

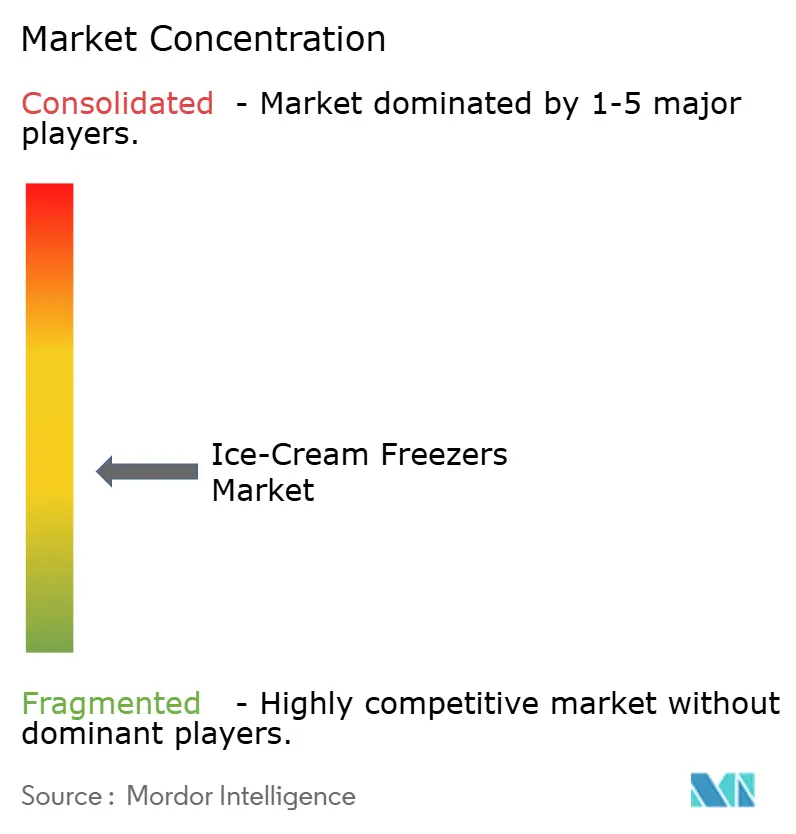

The ice-cream freezers market is moderately fragmented. The key players are AHT Cooling Systems, Epta Group, Liebherr Professional, Hussmann, and Arneg Group. These range from chest freezers and gelato cabinets to multideck systems and waterloop-based solutions. Consequently, no single player can dominate across all segments. Regional demand, service capabilities, and compliance standards further influence competition.

Leading players are setting themselves apart through technological advancements and innovations centered on efficiency. AHT Cooling Systems has broadened its offerings with R290-based systems, like the KIGALI XL, which boasts a larger display area and a reduced environmental footprint. Their BOREA multideck range prioritizes energy efficiency. In parallel, competitors are not only expanding their channels but also embracing digital integration. This includes strategic acquisitions to bolster regional presence and the introduction of platforms for remote monitoring and predictive maintenance.

Even amid ongoing consolidation, regional and niche manufacturers fiercely compete, especially in applications tailored to specific locales and climates. The varied demand across regions and end-user formats curtails the potential for large-scale consolidation. Furthermore, heightened regulatory transparency and energy-efficiency benchmarks, such as EPREL-linked procurement, underscore the importance of compliance and after-sales service in buying decisions. These dynamics foster a balanced competitive landscape, allowing global OEMs and regional specialists to thrive together and resulting in moderate market concentration.

Ice-Cream Freezers Industry Leaders

AHT Cooling Systems (Daikin)

Epta Group (IARP)

Liebherr Professional

Hussmann (Panasonic)

Arneg Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mini Melts USA and The Magnum ice-cream Company announced a strategic partnership to deploy Magnum-branded vending kiosks and grab-and-go freezers across high-traffic US venues starting Summer 2026.

- April 2025: AHT Cooling Systems launched BOREA, a successor to its VENTO multideck series, available as a full plug-in and semi plug-in (SPI) with R290 refrigerant; glass-door models consume 40% less energy than the predecessor VENTO Eco range and offer a 6% increase in total display area.

- March 2025: TEFCOLD acquired Serrco, a Dutch professional beverage cooling specialist, strengthening its Benelux distribution footprint and product portfolio for commercial refrigeration, including ice-cream freezer categories.

- February 2025: TEFCOLD launched three new scoop ice-cream freezer ranges (DELTA RV, SUPER CAPRI, and ISOA), targeting the premium gelato display segment with dual-zone refrigeration, ventilated cooling, and large glass display panels.

Global Ice-Cream Freezers Market Report Scope

Ice-cream freezers, specialized commercial cabinets or machines, store, display, or produce ice-cream at temperatures usually at or below -5°F (-21°C). These units ensure frozen desserts maintain their texture and don't melt. You'll often find them in retail shops, cafes, and ice-cream parlors.

The Ice-Cream Freezers Market is Segmented by Product Type (Chest, Upright, Dipping, Countertop, and Island/Multideck), Cooling Technology (Static, Ventilated, Hybrid, and Glycol/Waterloop), Capacity (≤300L, 301–600L, and >600L), End User (Supermarkets, C-Stores, Ice-Cream Parlors, HoReCa, and Bars), Sales Channel (Distributors and Direct OEM), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts in Value (USD).

| Chest/Deep Freezers |

| Upright/Glass‑Door Freezers |

| Dipping Cabinets/Scooping Freezers |

| Countertop Ice‑Cream Freezers |

| Island/Multideck Freezers for Ice-Cream |

| Static |

| Ventilated/Forced‑Air |

| Hybrid |

| Remote Glycol/Waterloop (SPI) |

| ≤300 L |

| 301–600 L |

| >600 L |

| Supermarkets/Hypermarkets |

| Convenience Stores/Gas Stations |

| Ice‑Cream Parlors & Gelaterias |

| HoReCa (Restaurants, Cafés, QSRs) |

| Bars & Clubs |

| Distributors/Dealers |

| Direct OEM/Key Accounts |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia‑Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia‑Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Chest/Deep Freezers | |

| Upright/Glass‑Door Freezers | ||

| Dipping Cabinets/Scooping Freezers | ||

| Countertop Ice‑Cream Freezers | ||

| Island/Multideck Freezers for Ice-Cream | ||

| By Cooling Technology | Static | |

| Ventilated/Forced‑Air | ||

| Hybrid | ||

| Remote Glycol/Waterloop (SPI) | ||

| By Capacity (Liters) | ≤300 L | |

| 301–600 L | ||

| >600 L | ||

| By End User | Supermarkets/Hypermarkets | |

| Convenience Stores/Gas Stations | ||

| Ice‑Cream Parlors & Gelaterias | ||

| HoReCa (Restaurants, Cafés, QSRs) | ||

| Bars & Clubs | ||

| By Sales Channel | Distributors/Dealers | |

| Direct OEM/Key Accounts | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia‑Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia‑Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the projected value of the ice-cream freezers market by 2031?

The ice-cream freezers market is forecast to reach USD 16.95 billion by 2031 from USD 12.64 billion in 2026, expanding at a 6.04% CAGR over 2026-2031.

Which region leads the ice-cream freezer market?

Asia-Pacific leads with 37.13% of 2025 revenue and the fastest forecast regional CAGR of 7.23% through 2031.

Which product type grows the fastest in commercial ice-cream freezer demand?

Upright/Glass-Door Freezers are projected to grow the fastest within the product type, with a 6.18% CAGR through 2031, while Chest/Deep Freezers remained the largest category in 2025.

Why are natural refrigerants important for ice-cream freezer purchases?

Regulations in Europe and the United States are pushing buyers toward low-GWP systems, while projects such as LIFE ICEGREEN showed that R290 platforms can also reduce energy use.

Which end users account for the most spending on ice-cream freezers?

Supermarkets/Hypermarkets led end-user demand with 38.72% of 2025 revenues, while Ice-Cream Parlors & Gelaterias are expected to post the fastest CAGR at 7.12% through 2031.

Page last updated on: