Chiller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.21 Billion |

| Market Size (2031) | USD 16.97 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chiller Market Analysis by Mordor Intelligence

The chiller market size is projected to be USD 12.56 billion in 2025, USD 13.21 billion in 2026, and reach USD 16.97 billion by 2031, growing at a CAGR of 5.14% from 2026 to 2031. Rising rack-level heat loads in artificial-intelligence data centers, stricter global warming potential (GWP) rules, and a growing preference for modular cooling solutions are converging to shorten replacement cycles and lift average selling prices. Facility owners are shifting evaluation criteria from first cost to total cost of ownership, rewarding suppliers that blend high seasonal efficiency with predictive-maintenance software. Simultaneously, electrification mandates in major economies are spurring the adoption of reversible heat-pump chillers that offset on-site fossil-fuel boilers. Manufacturers are responding with magnetic-bearing centrifugal machines, low-GWP refrigerant portfolios, and service contracts that guarantee uptime through cloud analytics.

Key Report Takeaways

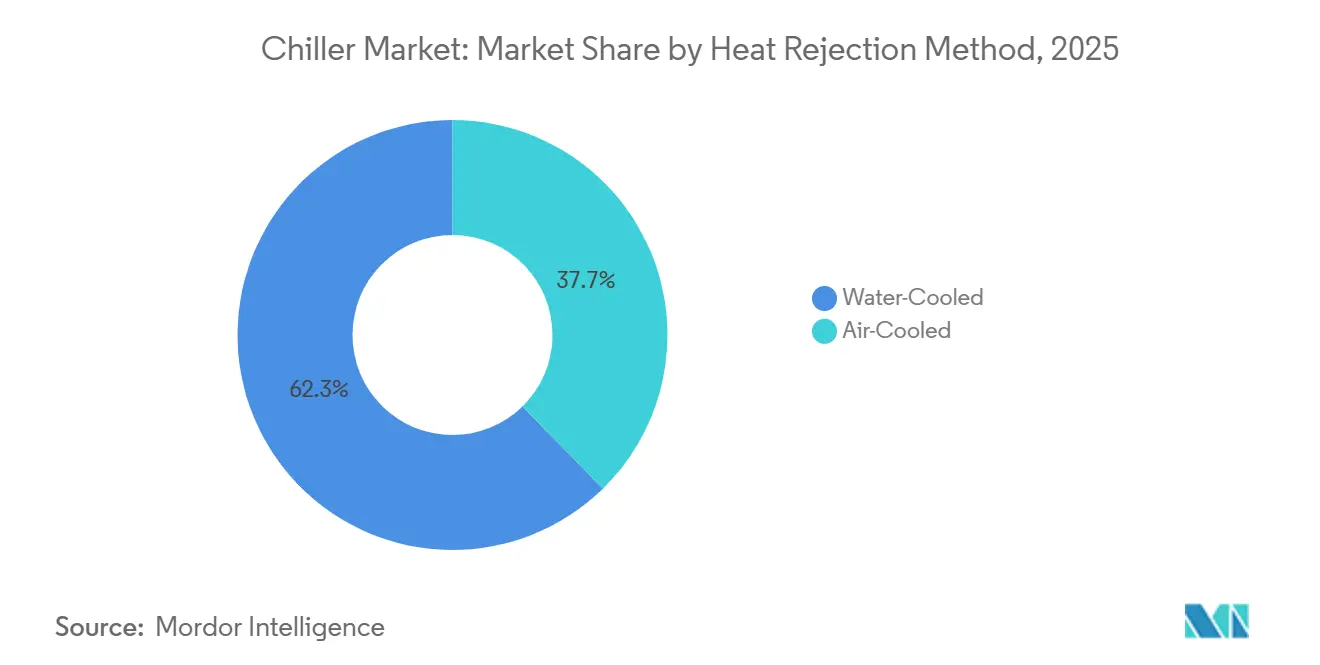

- By heat rejection method, water-cooled chillers led with a 62.33% revenue share in 2025, while air-cooled units are projected to record the fastest 5.57% CAGR through 2031.

- By compressor type, screw chillers commanded 43.89% chiller market share in 2025, and scroll technology is forecast to grow at a 6.16% CAGR between 2026 and 2031.

- By capacity range, the 350-kilowatt to 700-kilowatt bracket held a 36.91% share of the chiller market in 2025, whereas sub-50-kilowatt models are expected to expand at a 6.19% CAGR to 2031.

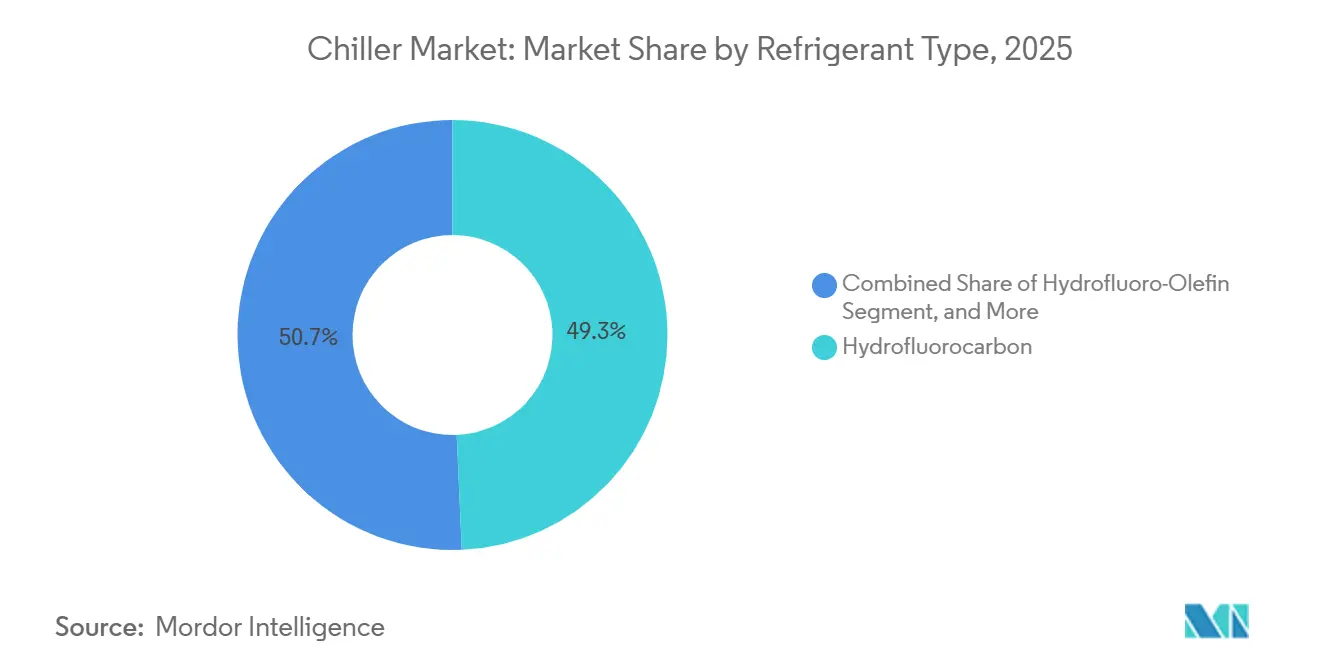

- By refrigerant type, hydrofluorocarbons retained 49.32% revenue share in 2025, while hydrofluoro olefins are set to rise at a 5.93% CAGR through 2031.

- By end user, commercial buildings accounted for 28.67% of 2025 sales, and data centers and information technology facilities are projected to advance at a 6.59% CAGR during 2026 2031.

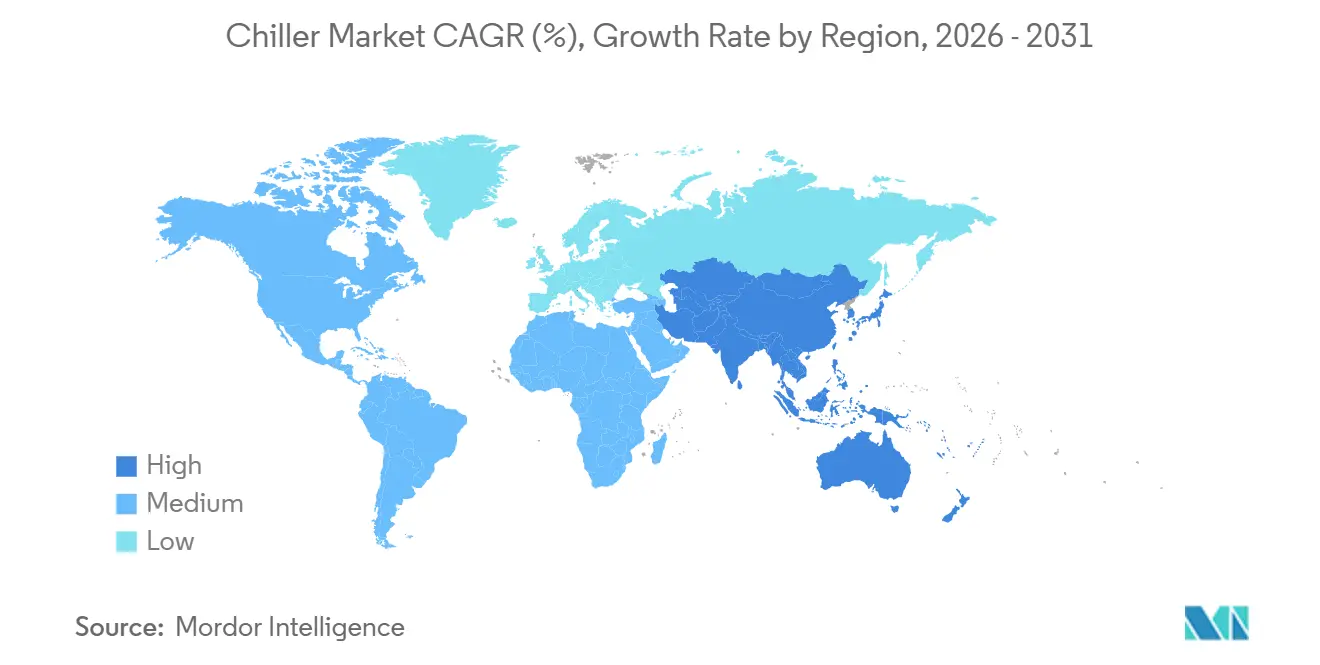

- By geography, Asia Pacific accounted for 39.16% of 2025 turnover and is also the fastest-growing region, with a 6.11% CAGR expected over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chiller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision Cooling Demand in Data Centers | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| HVAC Chiller Uptake in Commercial Buildings | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Processed Food and Beverage Expansion | +0.7% | Asia-Pacific, South America, Middle East | Medium term (2-4 years) |

| Industrialization in Emerging Economies | +0.8% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Low-GWP Refrigerant Uptake (CBAM) | +0.6% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| AI-Enabled Predictive Maintenance | +0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Precision Cooling in Data Centers

Hyperscale operators are installing rear-door heat exchangers and liquid distribution units to hold rack inlet temperatures below 18 °C, a shift that elevates chilled-water quality and redundancy standards.[1]Midea Building Technologies, “MagBoost Apex Pro Data Sheet,” midea.com Magnetic-bearing centrifugal and variable-speed screw chillers meet these tighter tolerances by minimizing oil carry-over and enabling flat efficiency curves at part load. New campuses in Northern Virginia, Frankfurt, and Singapore are designing N+1 chiller redundancy and modular growth paths that favor scalable, factory-tested packages. Regulatory scrutiny of power-usage effectiveness is intensifying, shifting procurement focus to integrated part-load performance rather than peak nameplate ratings. Suppliers able to couple equipment with digital-twin analytics are gaining preferred-vendor status for multiyear framework agreements.

Growing Adoption of HVAC Chillers in Commercial Buildings

Energy codes linked to LEED and BREEAM require minimum seasonal energy-efficiency ratios, prompting retrofits of constant-speed machines with variable-speed drive alternatives.[2]Mitsubishi Electric Corporation, “Variable Refrigerant Flow Systems 2025 Program,” mitsubishi-electric.com Building automation systems based on BACnet and Modbus consolidate chiller data for fault detection, reducing unplanned downtime and extending service intervals. Electrification ordinances in California and New York are accelerating the replacement of gas boilers with reversible heat-pump chillers, creating dual-season demand for the same plant-room footprint. Tenant expectations for high indoor-air quality after the pandemic continue to elevate chilled-water demand, especially where air-side economizers cannot reach target humidity. Performance contracting and energy-as-a-service schemes are unlocking capital for premium-efficiency equipment in cash-constrained real estate portfolios.

Increasing Consumption of Processed Food and Beverages

Cold-chain upgrades in Southeast Asia and Latin America underpin procurement of scroll and screw chillers sized 50–350 kilowatts for dairy pasteurization, brewery fermentation, and ready-meal packaging.[3]Danfoss, “PSG Scroll Compressors for Industrial Heat Pumps,” danfoss.com Food-safety frameworks such as HACCP and ISO 22000 require continuous temperature logging, driving the adoption of dual-circuit designs that maintain output even during service on a single refrigeration loop. Product innovation in plant-based proteins heightens the need for rapid chill to protect texture and shelf life, favoring modular air-cooled units that can be installed close to process lines. Suppliers offering sanitary heat-exchanger finishes and cleanable tube sheets gain an edge with beverage bottlers. Rising electricity tariffs motivate processors to specify integrated heat-recovery features that preheat wash-down water, improving overall site energy balance.

Rapid Industrialization in Emerging Economies

Chemical, pharmaceutical, and plastics plants in India, Vietnam, and Saudi Arabia are specifying air-cooled screw and centrifugal chillers capable of withstanding 45 °C ambient peaks without derating. Greenfield industrial parks are bundling thermal-energy storage with central chiller houses to flatten grid demand curves and qualify for reduced connection fees. Larger export-focused manufacturers now ask bidders to quote five-year maintenance packages and remote diagnostics portals, signaling a shift toward lifecycle partnering. Government incentives for domestic capital-equipment production, such as India’s production-linked incentive scheme, are attracting global OEMs to build regional assembly lines, thereby cutting lead times and import duties. Suppliers with bilingual service teams and localized spare-parts hubs are moving ahead of pure-export competitors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure | -0.8% | South America, Africa, Global price-sensitive tiers | Short term (≤ 2 years) |

| Stricter Environmental Regulation on HFCs | -0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Volatile Copper Prices | -0.4% | Global | Short term (≤ 2 years) |

| Skilled-Technician Shortage | -0.3% | Emerging markets, Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure

Magnetic-bearing centrifugal chillers and integrated distribution units command 30–50% price premiums over constant-speed alternatives, pushing payback beyond 5 years when electricity tariffs are low. Financing barriers are acute in South America and parts of Africa, where currency depreciation and elevated interest rates deter large capital inflows. Modular air-cooled scroll units below 50 kilowatts are gaining favor for trimming installation costs and sidestepping cooling-tower water fees. Energy-as-a-service contracts, in which a third party funds the plant and shares verified savings, are emerging but remain confined to mature legal regimes. Consequently, many small facility owners defer replacement even as maintenance costs on legacy equipment climb.

Stricter Environmental Regulation on HFCs

The American Innovation and Manufacturing Act triggered a 40% reduction in HFCs on 1 January 2025, while the European Union accelerated its F-Gas phase-down schedule, pushing owners to retire equipment well before the end of its life. Transitioning to mildly flammable A2L refrigerants such as R-32 and R-454B requires additional leak detection, smaller charge volumes, and updated technician certifications, thereby increasing installation complexity. Parallel product lines for legacy HFC and low-GWP variants inflate inventory costs for manufacturers and distributors. Small builders, wary of evolving norms, sometimes postpone capital spending until refrigerant pathways appear stable. Long procurement cycles for replacement machines risk cooling shortages in mission-critical sites if planning lags.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Heat Rejection Method: Water-Cooled Efficiency Versus Air-Cooled Simplicity

Water-cooled systems accounted for 62.33% of 2025 revenue, reflecting entrenched use in large commercial towers and process industries, where lifetime energy savings offset auxiliary water-pump consumption. Their coefficient of performance is typically 20–30% higher than air-cooled equivalents, a margin that compounds over two decades of operation. The chiller market size for air-cooled offerings is set to expand fastest as code authorities in water-scarce regions penalize evaporative cooling. Modular rooftop arrays let owners add capacity in 75-kilowatt blocks, aligning investment with incremental tenant loads.

Rapid adoption of hybrid designs that blend dry-cooler coils with conventional condensers is narrowing the cost-of-ownership gap. Geoclima’s free-cooling Circlemiser series illustrates how ambient air can offset compressor runtime during cooler seasons. For data centers in desert climates, zero-water-use mandates now tip specifications in favor of air-cooled packages despite higher electrical draw, confirming that environmental compliance can trump raw efficiency.

By Compressor Type: Scroll Momentum, Screw Resilience

Screw machines retained 43.89% of 2025 turnover on the strength of continuous-duty industrial use, yet scroll volumes are climbing at a 6.16% clip as distributed cooling proliferates. Multiple scroll cores in a shared header deliver n+1 redundancy and low acoustic profiles valued by hotels and outpatient clinics. The chiller market share for magnetic-bearing centrifugal models is small today but rising, as oil-free operation slashes maintenance labor and elevates part-load tallies.

New scroll platforms from Danfoss push discharge temperatures high enough for 100 °C process hot water, blurring lines between chiller and heat pump. Meanwhile, screw technologies defend their turf in the 350–1,200 kilowatt band through field-serviceable rotors and robust slide-valve capacity control. Centrifugal models are migrating down to 700 kilowatts thanks to compact two-stage impellers, nibbling at screw incumbency.

By Capacity Range: Mid-Tier Core, Micro Units Surge

Units rated 350–700 kilowatts delivered 36.91% of 2025 sales, a sweet spot for medium-rise offices and multi-process manufacturing halls. Owners appreciate a single-machine solution that fits standard freight elevators and simplifies redundancy planning. Sub-50 kilowatt systems, however, represent the fastest lane, with a 6.19% CAGR, underpinned by 5G edge nodes, small data centers, and modular retail outlets. Here, plug-and-play packages shave weeks off construction schedules.

On the other hand, districts and hyperscale campuses are increasingly deploying centrifugal chillers with capacities exceeding 1,200 kilowatts. These chillers are integrated with thermal energy storage tanks, which enable the decoupling of production from peak demand periods, thereby improving energy efficiency and operational flexibility. Within the capacity range of 700 to 1,200 kilowatts, there is a significant transition underway. Variable-speed compressors are progressively replacing constant-speed units, a trend driven by tariff structures that incentivize flexible load-shifting and promote the optimization of energy consumption strategies.

By Refrigerant Type: Legacy HFCs Confront HFO Ramp-Up

HFC machines still account for 49.32% of installed value, yet hydrofluoro-olefins are pacing at a 5.93% CAGR as global phase-downs bite. R-1234ze(E) dominates large centrifugal launches because its GWP of 7 aligns with forthcoming carbon tariffs under the European Union carbon-border-adjustment mechanism. The chiller market size for A2L blends is rising fastest in air-cooled segments, where factory charge reductions cap site-level flammability risk.

Water-based magnetic-bearing systems, which eliminate the need for synthetic refrigerants, are increasingly preferred by corporations that prioritize sustainability objectives, even if this choice entails incurring higher capital expenditures. At the same time, ammonia continues to maintain its relevance within a limited industrial niche, primarily in regions where skilled technicians are readily available, and regulatory frameworks are more accommodating. In the current market landscape, original equipment manufacturers (OEMs) aiming to secure global frame contracts must make strategic investments in supply-chain capabilities that support readiness for multiple refrigerants.

By End-User Industry: Commercial Volume, Data-Center Velocity

Commercial real estate accounted for 28.67% of 2025 billings, as offices, malls, and hotels refreshed aging plants to meet tighter environmental benchmarks. Variable-speed retrofits deliver 20–30% energy savings at part load, securing quick wins for landlords amid rising utility rates. In contrast, data-center owners are the growth pacesetters at 6.59% CAGR, specifying redundant N+1 chillers with liquid-cooling interfaces that deliver water at 15–18 °C.

Process industries, including chemicals, plastics, food, and pharmaceuticals, place a high priority on maximizing uptime. As a result, they tend to prefer screw and centrifugal platforms equipped with serviceable bearings and sufficient headroom to meet their operational needs. Similarly, users in the healthcare and laboratory sectors prioritize maintaining precise temperature control and ensuring backup capacity to protect the integrity of their products. To achieve this, they often install dual chillers connected to separate electrical feeders.

Geography Analysis

Asia-Pacific accounted for the largest share, 39.16%, in 2025 and is expected to compound at 6.11% through 2031. Policy incentives for domestic semiconductor fabs in China and India are translating into multi-megawatt chiller procurements. Government-backed industrial corridors in Indonesia and Vietnam create additional pull, while growing adoption of district-cooling concessions in the Gulf sustains order books for water-cooled centrifugal machines.

North America benefits from record hyperscale campus rollouts in Virginia, Texas, and Arizona, as well as electrification mandates that favor reversible chillers in commercial retrofits. The chiller market size for low-GWP models is escalating as the Environmental Protection Agency’s 40% HFC cut takes hold, spurring wholesale refrigerant transitions in replacement projects. Canada’s carbon-pricing framework likewise steers owners toward R-32 and R-454B scroll units.

Europe’s trajectory is shaped by accelerated F-Gas quotas and carbon border levies that reward R-1234ze(E) and magnetic-bearing designs. District-cooling networks in Stockholm, Copenhagen, and Paris pair absorption chillers with waste-to-energy plants, easing grid pressure during summer peaks. South America’s outlook is mixed: Brazilian food-export processors invest in high-efficiency scroll systems, yet tight credit conditions constrain large real-estate refurbishments. Africa remains nascent apart from mining and cold-storage nodes in South Africa and Nigeria, where basic air-cooled screws dominate purchases.

Mordor Intelligence provides coverage of the chiller market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

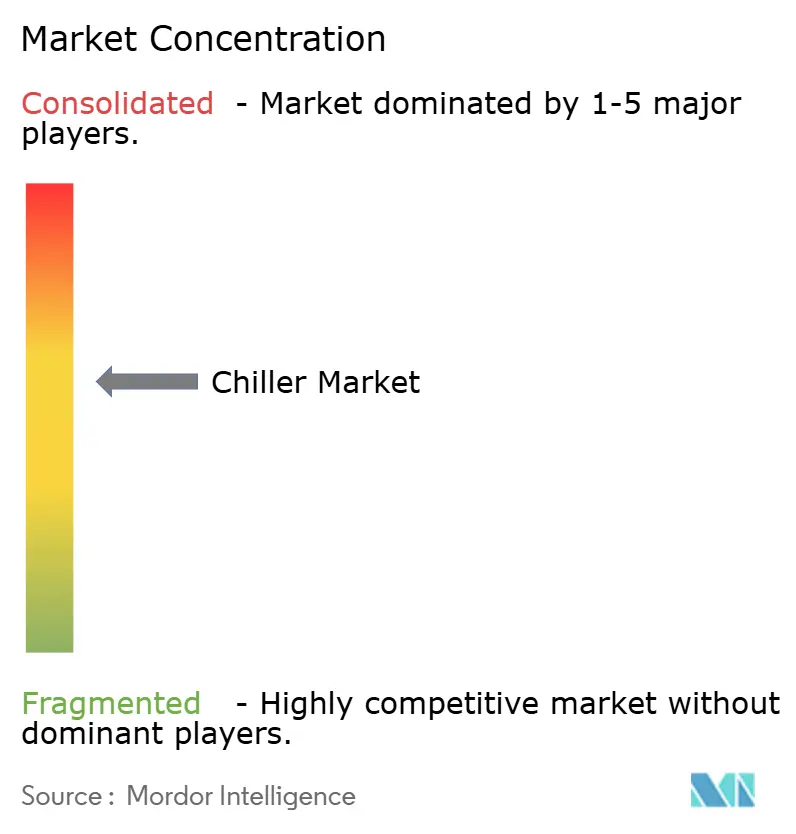

The five largest suppliers, Carrier, Trane, Johnson Controls, Daikin, and Mitsubishi Electric, collectively account for roughly 45–50% of global revenue, indicating moderate concentration. They compete on digital twins, multi-refrigerant readiness, and extended service agreements that monetize machine learning insights. Johnson Controls reports a 66% reduction in unplanned repairs across its connected portfolio, a statistic driving multi-year service conversions over traditional break-fix contracts.

Chinese challengers Midea, Haier, and Shuangliang leverage scale economics to underprice incumbents in Asia-Pacific and Africa while rapidly localizing low-GWP centrifugal production. Smardt, an oil-free specialist, secures high-margin projects where maintenance avoidance trumps capex. Patent activity is brisk in microchannel heat exchangers, partial-load algorithms, and refrigerant-charge minimization, reflecting a race to meet tightening environmental metrics without eroding profitability.

Regulatory hurdles for mildly flammable refrigerants create entry barriers for small brands lacking certification labs and global field-support teams. Meanwhile, long-tail regional firms defend niche shares through customized packages and quick-turn engineering for retrofit footprints that global OEMs sometimes overlook. Overall, price competition at the low end coexists with premium pricing power for highly efficient, digitally enabled flagship models.

Chiller Industry Leaders

Carrier Global Corporation

Mitsubishi Electric Corporation

Daikin Industries, Ltd.

Johnson Controls International plc

Polyscience Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Midea Building Technologies unveiled the MagBoost Apex Pro magnetic-bearing centrifugal chiller at AHR Expo 2026, citing an integrated part-load value of 9.71 on R-1234ze(E) and modular scalability to 16 linked units.

- November 2025: Midea displayed R-32 variable-refrigerant-flow systems, R-290 heat pumps, and the MagBoost Apex Pro at C&R 2025 in Madrid, highlighting low-GWP alignment.

- August 2025: Danfoss introduced the NeoCharge refrigerant-charge-reduction solution and qualified larger PSG scroll compressors for R-1234ze, R-515B, and R-600a service.

- July 2025: Danfoss certified MTZ four-cylinder compressors for A2L blends R-454A, R-454C, and R-455A, issuing updated installation guidance.

Global Chiller Market Report Scope

The Chiller Market Report is Segmented by Heat Rejection Method (Water-Cooled, and Air-Cooled), Compressor Type (Screw Chillers, Scroll Chillers, Reciprocating Chillers, Centrifugal Chillers, Absorption Chillers), Capacity Range (Below 50 kW, 50kW-350 kW, 350kW-700 kW, 700kW-1,200 kW, Above 1,200 kW), Refrigerant Type (Hydrofluorocarbon, Hydrofluoro-Olefin, Hydrochlorofluorocarbon, Water-Based/Magnetic-Bearing), End-User Industry (Chemicals and Petrochemicals, Food and Beverage, Medical and Pharmaceutical, Plastics and Rubber, Data Centres and IT, Commercial Buildings, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Water-Cooled |

| Air-Cooled |

| Screw Chillers |

| Scroll Chillers |

| Reciprocating Chillers |

| Centrifugal Chillers |

| Absorption Chillers |

| Below 50 kW |

| 50kW - 350 kW |

| 350kW - 700 kW |

| 700kW - 1,200 kW |

| Above 1,200 kW |

| Hydrofluorocarbon |

| Hydrofluoro-Olefin |

| Hydrochlorofluorocarbon |

| Water-Based / Magnetic-Bearing |

| Chemicals and Petrochemicals |

| Food and Beverage |

| Medical and Pharmaceutical |

| Plastics and Rubber |

| Data Centres and IT |

| Commercial Buildings |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Heat Rejection Method | Water-Cooled | ||

| Air-Cooled | |||

| By Compressor Type | Screw Chillers | ||

| Scroll Chillers | |||

| Reciprocating Chillers | |||

| Centrifugal Chillers | |||

| Absorption Chillers | |||

| By Capacity Range | Below 50 kW | ||

| 50kW - 350 kW | |||

| 350kW - 700 kW | |||

| 700kW - 1,200 kW | |||

| Above 1,200 kW | |||

| By Refrigerant Type | Hydrofluorocarbon | ||

| Hydrofluoro-Olefin | |||

| Hydrochlorofluorocarbon | |||

| Water-Based / Magnetic-Bearing | |||

| By End-User Industry | Chemicals and Petrochemicals | ||

| Food and Beverage | |||

| Medical and Pharmaceutical | |||

| Plastics and Rubber | |||

| Data Centres and IT | |||

| Commercial Buildings | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the chiller market expected to grow through 2031?

It is projected to expand from USD 13.21 billion in 2026 to USD 16.97 billion by 2031 at a 5.14% CAGR.

Which region generates the largest demand for chillers?

Asia-Pacific held 39.16% of 2025 revenue and remains the fastest-growing region at a 6.11% CAGR.

What compressor technology is gaining share the quickest?

Scroll compressors show the highest growth, advancing at a 6.16% CAGR as modular, low-noise units proliferate.

How are regulations affecting refrigerant choices?

The AIM Act in the United States and EU F-Gas rules are pushing a fast transition from legacy HFCs to low-GWP HFO and A2L blends.

Why are data centers significant for future chiller demand?

High-density AI workloads require precision liquid cooling, driving a 6.59% CAGR in the data-center segment and favoring magnetic-bearing centrifugal designs.

What is the main barrier to wider adoption of high-efficiency chillers?

Upfront capital cost premiums of 30–50% remain a key constraint, especially in regions with limited financing options.

Page last updated on: